Indian Diabetes Market Size, Share, Trends and Forecast by Segment and Distribution Channel, 2026-2034

Indian Diabetes Market Size, Share, Trends & Forecast (2026-2034)

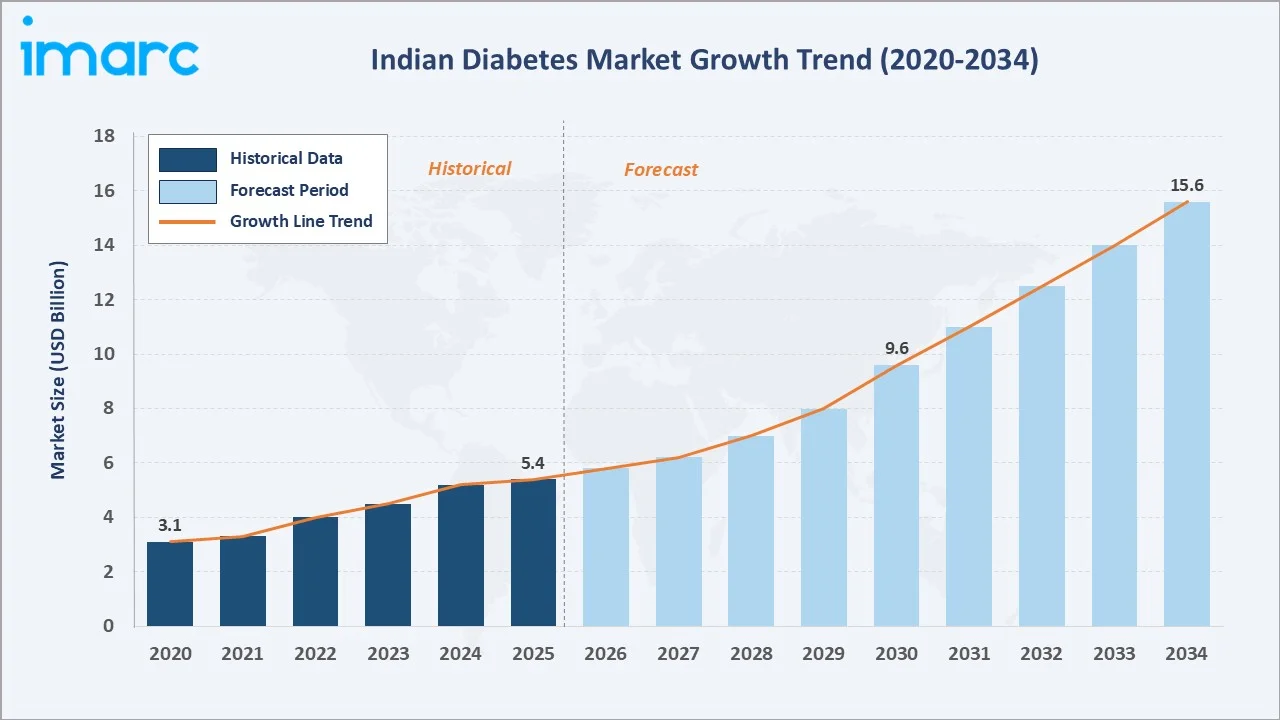

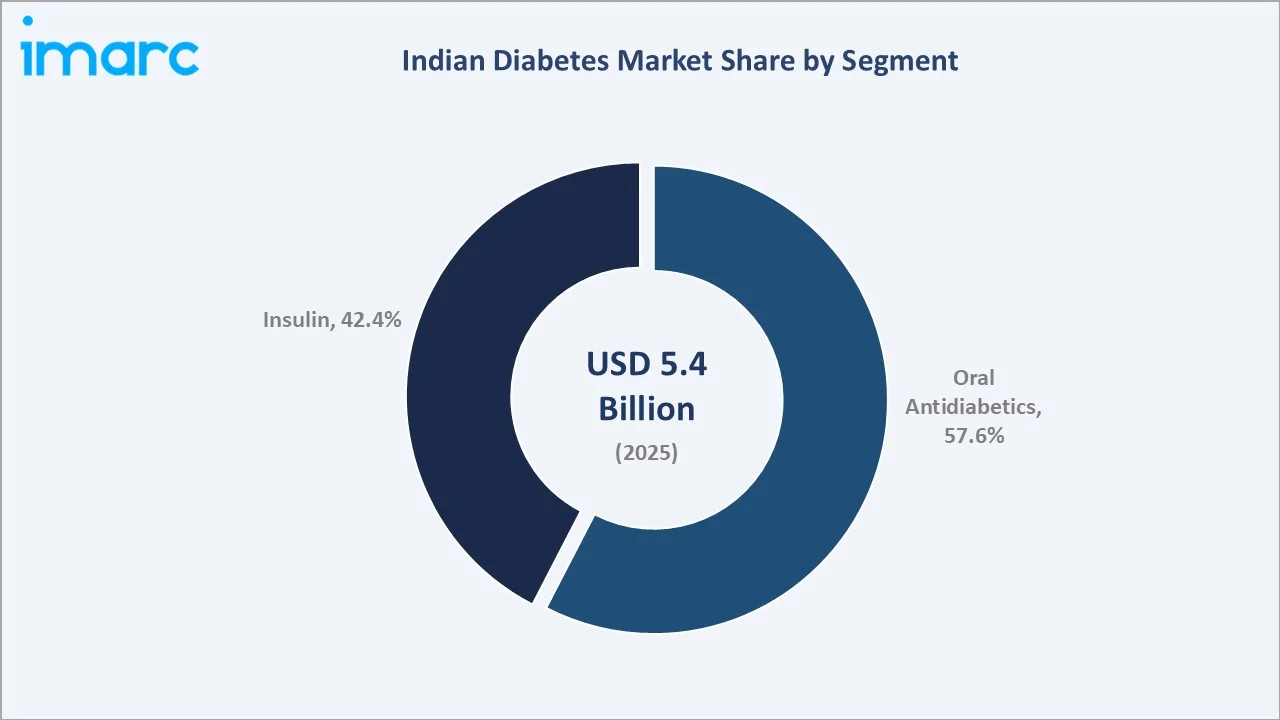

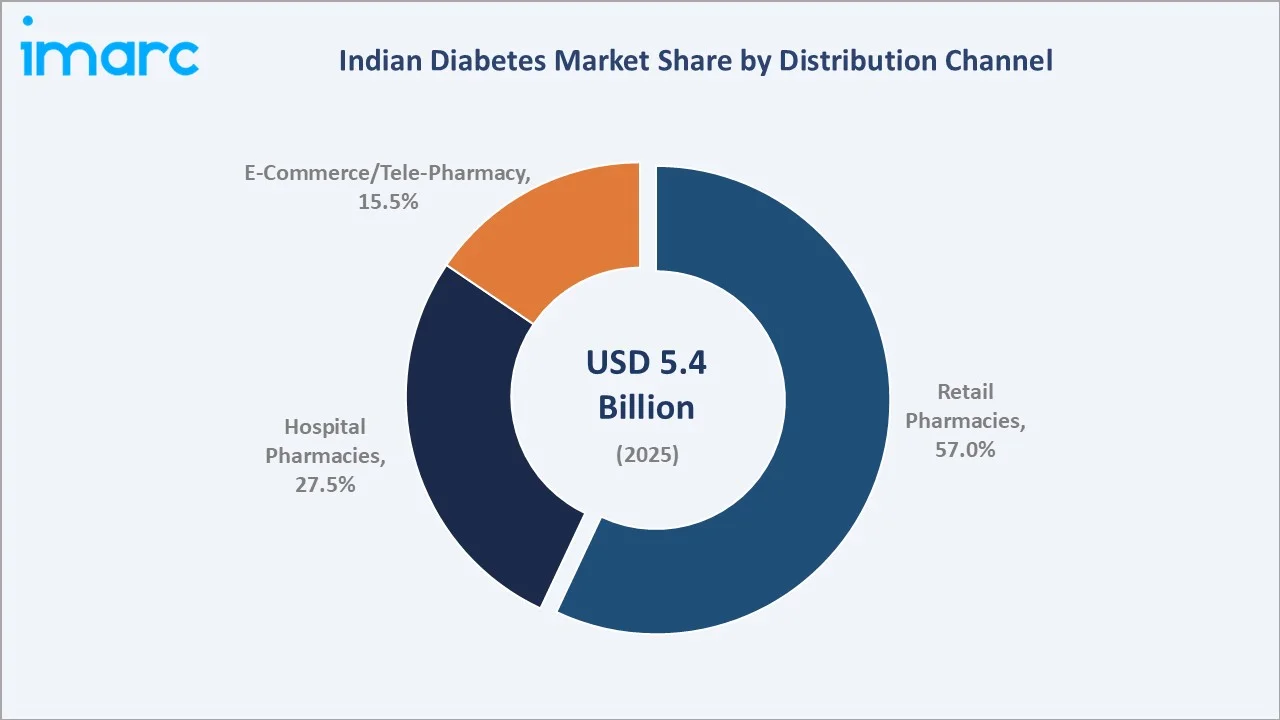

The Indian diabetes market was valued at USD 5.4 Billion in 2025 and is projected to reach USD 15.6 Billion by 2034, growing at a CAGR of 12.08% during 2026-2034. India is home to 89.8 million adults (20–79 years) patients in 2024, and the number is projected to reach 156.7 million by 2050. The market is driven by rising diabetes prevalence, rising aging population and rising obesity cases. Oral antidiabetics lead at 57.6% share; retail pharmacies dominate the distribution channel at 57.0%.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 5.4 Billion |

|

Forecast Market Size (2034) |

USD 15.6 Billion |

|

CAGR (2026-2034) |

12.08% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

The market expanded from USD 3.1 Billion in 2020 to USD 5.4 Billion in 2025, anchored at USD 9.6 Billion in 2030, and forecast to reach USD 15.6 Billion by 2034. This trajectory is driven by India's rising diabetes burden, growing middle-class healthcare spending, Ayushman Bharat scheme enrollment, and accelerating adoption of novel drug classes including SGLT-2 inhibitors and GLP-1 agonists.

To get more information on this market, Request Sample

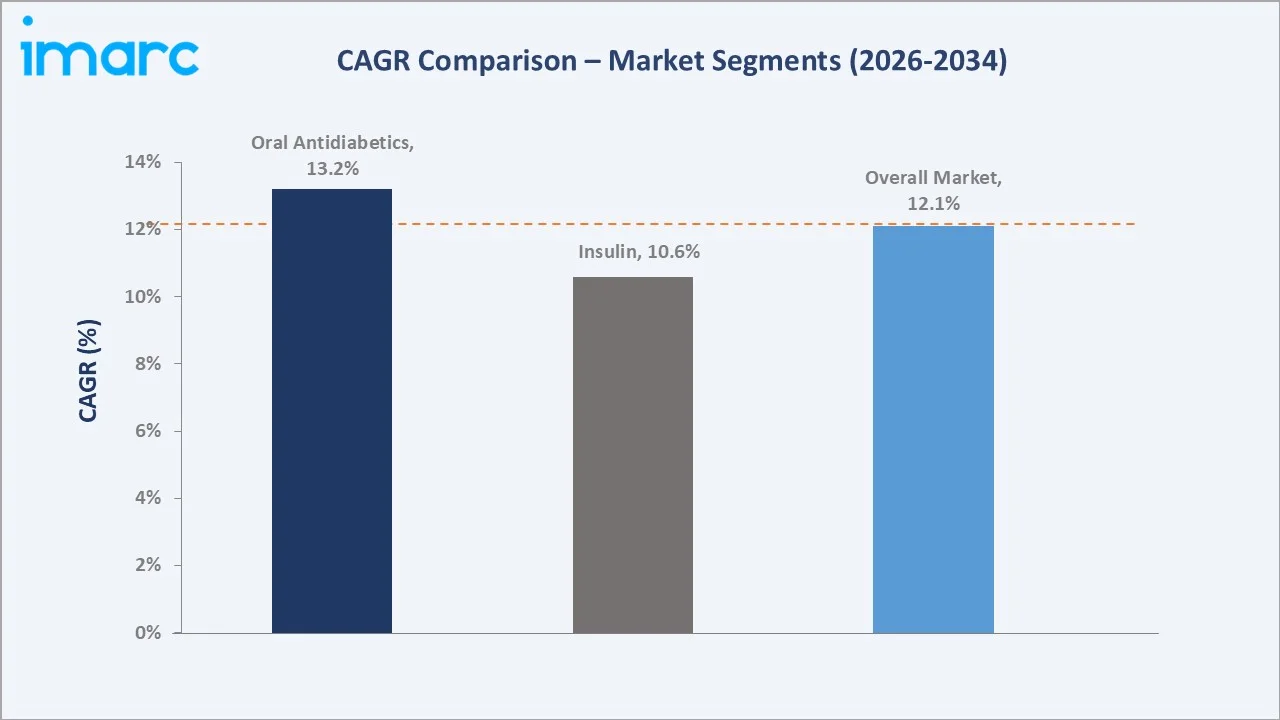

Oral Antidiabetics grow at ~13.2% CAGR versus Insulin at ~10.6%, fueled by metformin generics, SGLT-2, and DPP-4 class premiumization across India's diabetic patient base.

Executive Summary

The Indian diabetes market reached USD 5.4 Billion in 2025, ranking as Asia's second-largest diabetes pharmaceutical market. India's diagnosed patients create a structurally high-volume, rapidly growing market for oral antidiabetics, insulin, and digital diabetes management solutions. India's 12.08% CAGR to USD 15.6 Billion by 2034 reflects rising Type-2 prevalence from sedentary lifestyles, urbanization-driven dietary change, the Ayushman Bharat scheme, and pharmaceutical innovation in affordable biosimilar insulin and novel oral combinations.

Oral Antidiabetics lead with 57.6% share (2025), anchored by high-volume metformin generics and a rapidly expanding premium tier of SGLT-2 inhibitors and GLP-1 agonists. Insulin at 42.4% is growing through biosimilar expansion. Retail Pharmacies at 57.0% remain dominant, while E-Commerce at 15.5% grows fastest at ~17.5% CAGR.

Key Market Insights

|

Insight |

Data |

|

Largest Segment |

Oral Antidiabetics - 57.6% revenue share (2025) |

|

Leading Distribution Channel |

Retail Pharmacies - 57.0% share (2025) |

Key Analytical Observations Supporting the Above Data:

- Oral Antidiabetics at 57.6% share (2025) driven by metformin's universal first-line status: India's Type-2 treatment protocol positions metformin as mandatory first-line therapy across ICMR and ADA guidelines, creating a structurally large generic prescription base.

- Retail Pharmacies at 57.0% anchored by India's licensed pharmacy network: India's Schedule H/H1 prescription mandate ensures retail pharmacies remain the primary diabetes medication dispensing channel. Apollo Pharmacy, MedPlus, and other local pharmacies serve as organized retail pharmacy chains, reinforcing channel dominance.

Indian Diabetes Market Overview

India's diabetes market encompasses all pharmaceutical treatments and monitoring solutions for Type-1, Type-2, and gestational diabetes patients. The ecosystem integrates API suppliers, pharmaceutical manufacturers (multinational and domestic), CDSCO regulatory framework, C&F agents, stockists, and retail/hospital/e-pharmacy dispensing channels serving 101 million+ diagnosed patients (2025).

The market operates under India's Drugs and Cosmetics Act, with CDSCO (Central Drugs Standard Control Organisation) governing approvals and the DPCO (Drug Price Control Order) regulating prices of essential diabetes medicines, including metformin, glibenclamide, and human insulin. Macroeconomic drivers include India's GDP growth, rising household income, urbanization, and Ayushman Bharat coverage.

Market Dynamics

To evaluate market opportunities, Request Sample

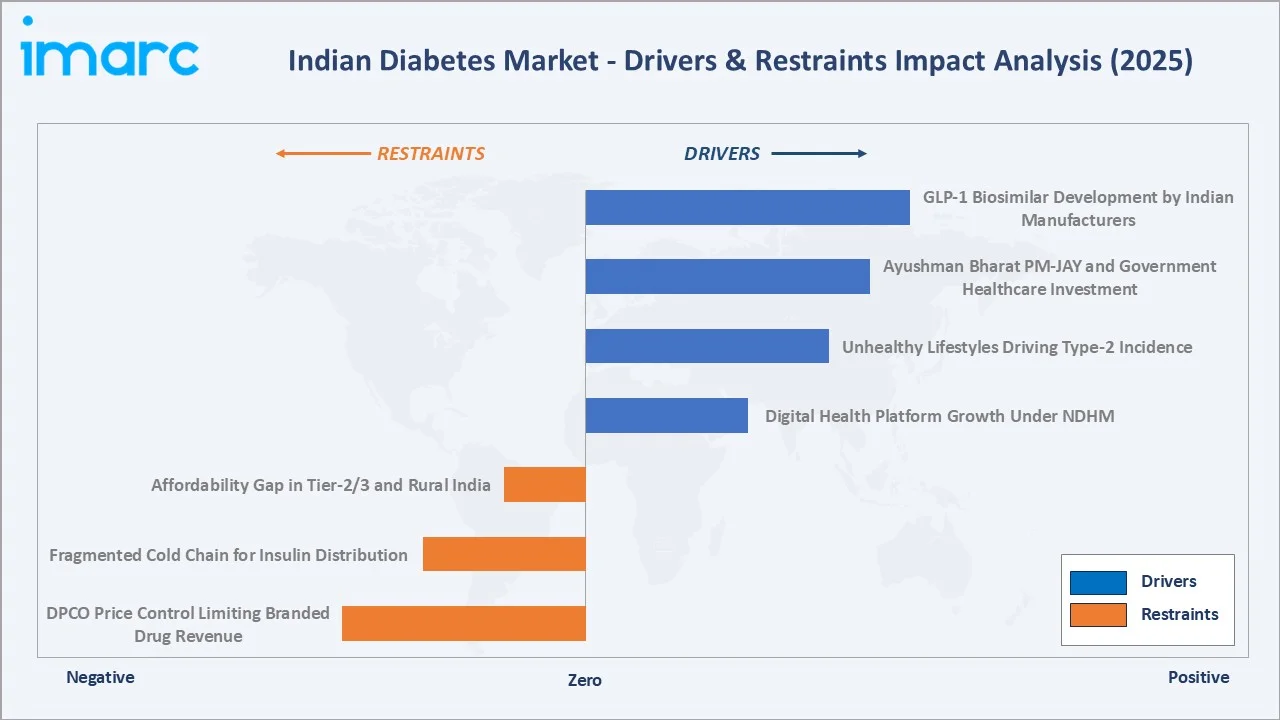

Market Drivers

- Unhealthy Lifestyles Driving Type-2 Incidence: Rising consumption of processed food, sedentary urban jobs, and sleep disruption are creating an epidemic of younger-onset Type-2 diabetes. India's working-age population is creating decades-long therapy demand per patient. India has 89.8 million adults (20–79 years) with diabetes in 2024 and is projected to reach 156.7 million by 2050. This structural patient base creates compounding prescription demand independent of pricing dynamics.

- Ayushman Bharat PM-JAY and Government Healthcare Investment: The "Ayushman Bharat – Pradhan Mantri Jan Arogya Yojana," launched by the National Health Authority (NHA) under the Ministry of Health and Family Welfare, Government of India, seeks to offer cashless hospitalization coverage of ₹5,00,000 annually per family for secondary and tertiary healthcare services, including diabetes medication reimbursement.

Market Restraints

- Affordability Gap in Tier-2/3 and Rural India: Despite DPCO price controls, monthly out-of-pocket costs for insulin analogs, unaffordable for India's diabetes population earning below INR 15,000/month. This affordability barrier limits premium drug penetration and drives generic substitution over branded therapies.

- Fragmented Cold Chain for Insulin Distribution: India's insulin supply chain requires uninterrupted 2-8 degree Celsius storage. Less number of India's rural pharmacies have functional cold storage, creating distribution gaps in Tier-3 towns and villages that limit insulin market penetration below Tier-2 cities.

Market Opportunities

- GLP-1 Biosimilar Development by Indian Manufacturers: Glenmark's Lirafit (liraglutide biosimilar, launched January 2024) marked India's entry into GLP-1 biosimilars, positioning India for indigenous GLP-1 manufacturing that could make this drug class 5-8x more affordable than branded in India.

- Digital Health Platform Growth Under NDHM: India's National Digital Health Mission is creating a unified patient health record for citizens. PharmEasy, 1mg, and Practo are integrating diabetes monitoring, teleconsultation, and prescription fulfilment into single platforms.

Market Challenges

- DPCO Price Control Limiting Branded Drug Revenue: India's Drug Price Control Order caps prices of essential medicines, including metformin, glibenclamide, and human insulin, under the National List of Essential Medicines.

- Counterfeit and Substandard Drug Prevalence: India's pharmaceutical regulator (CDSCO) regularly identifies substandard diabetes drug samples. Counterfeit insulin and oral antidiabetic drugs undermine patient outcomes and create market distortions that disadvantage branded manufacturers.

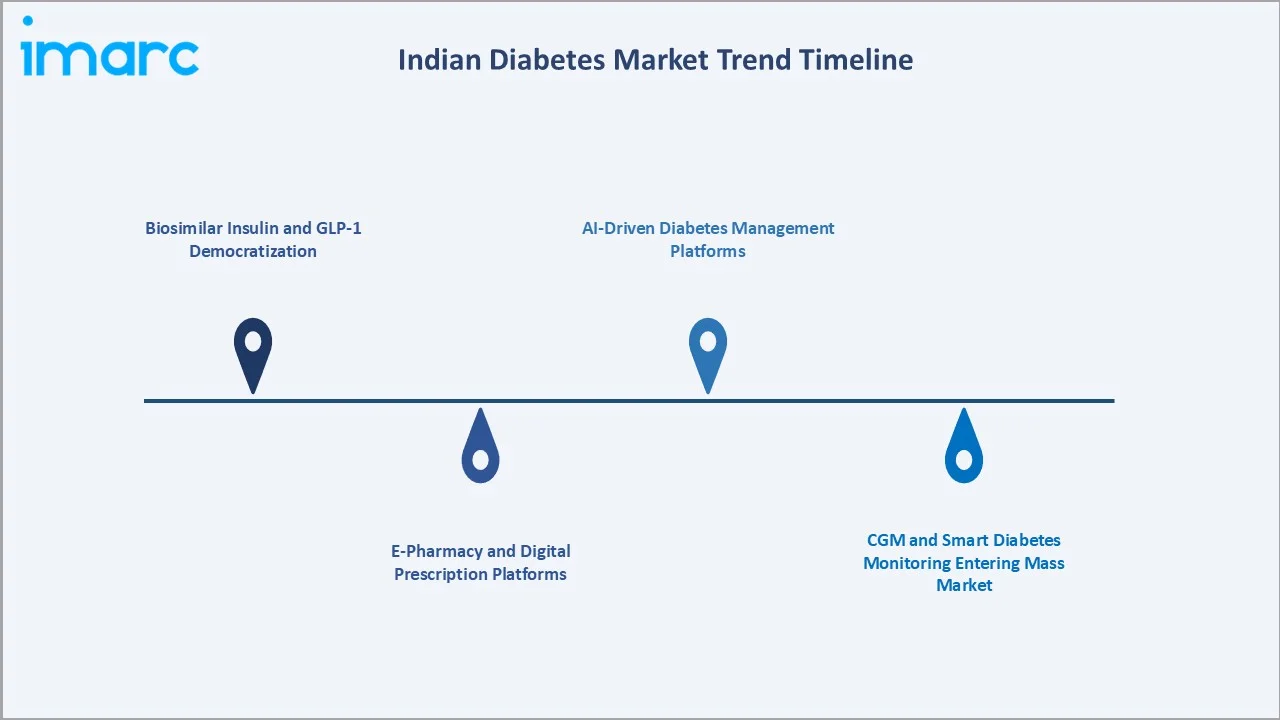

Emerging Market Trends

1. Biosimilar Insulin and GLP-1 Democratization

India's biosimilar manufacturers are making advanced insulin analogs and GLP-1 agonists more affordable than multinational brands.

2. E-Pharmacy and Digital Prescription Platforms

India's online pharmacy market processed diabetes prescriptions. PharmEasy, 1mg, Netmeds, and Apollo 24/7 are integrating AI-powered adherence reminders, HbA1c tracking, and physician teleconsultation directly into medication ordering.

3. CGM and Smart Diabetes Monitoring Entering Mass Market

In 2020, Abbott launched the revolutionary FreeStyle Libre system in India. Abbott's FreeStyle Libre flash CGM system reduced its India price, making real-time glucose monitoring accessible beyond affluent urban patients.

4. AI-Driven Diabetes Management Platforms

In December 2025, India launched the first Artificial Intelligence (AI)-driven community screening programme for Diabetic Retinopathy (DR). AI-powered personalized diabetes coaching platforms integrating CGM data, dietary tracking, and teleconsultation.

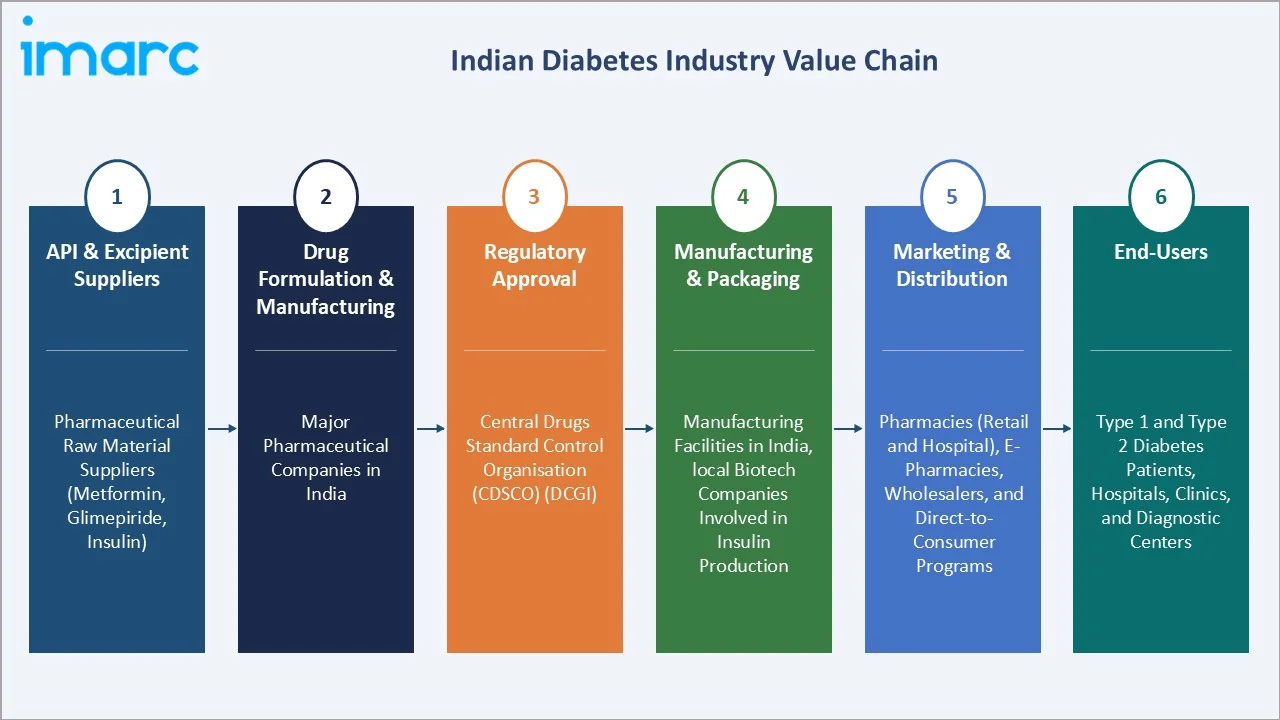

Industry Value Chain Analysis

India's diabetes market value chain integrates API manufacturing, pharmaceutical production, regulatory approval, multi-tier distribution, and end-patient dispensing across 101 million+ patients (2025) under DPCO-regulated pricing and Ayushman Bharat reimbursement frameworks.

|

Stage |

Key Participants |

|

API & Excipient Suppliers |

Pharmaceutical raw material suppliers (active ingredients like metformin, glimepiride, insulin) |

|

Drug Formulation & Manufacturing |

Major pharmaceutical companies in India |

|

Regulatory Approval |

Central Drugs Standard Control Organisation (CDSCO) (DCGI) |

|

Manufacturing & Packaging |

Manufacturing facilities in India, local biotech companies involved in insulin production |

|

Marketing & Distribution |

Distribution channels through pharmacies (both retail and hospital), e-pharmacies, wholesalers, and direct-to-consumer programs |

|

End-Users |

Type 1 and Type 2 diabetes patients, hospitals, clinics, and diagnostic centers |

India's domestic API manufacturers supply active ingredients to formulation manufacturers at competitive costs. Branded manufacturers command 40-60% gross margins on insulin analogs; generic formulators earn 18-25%. Distributors operate on 4-8% trade margins.

Technology Landscape in the Indian Diabetes Industry

Biosimilar Insulin and Novel Formulation Technology

Biocon's recombinant DNA technology platform produces biosimilar insulin analogs at lower cost than innovator brands. In 2025, Biocon received FDA approval for Kirsty (insulin Aspart biosimilar), expanding India's pharmaceutical technology credibility.

Continuous Glucose Monitoring (CGM) Systems

In March 2026, Zydus Lifesciences unveiled its companion diagnostics portfolio, featuring Diasens and GlucoLive, continuous glucose monitoring (CGM) devices specifically developed for managing diabetes, a transformative technology for India's injection-averse patient population.

Fixed-Dose Combinations (FDC) Innovation

India's CDSCO approved new diabetes FDC formulations, including triple combinations of metformin + DPP-4 inhibitor + SGLT-2 inhibitor, demonstrating India's domestic pharmaceutical innovation, accelerating treatment adherence through combination simplification.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Segment | Oral Antidiabetics | 57.6% | 2025 |

| Distribution Channel | Retail Pharmacies | 57.0% | 2025 |

By Segment

By Segment

Oral antidiabetics lead at 57.6% market share (2025). India's Type-2 first-line metformin protocol creates a structurally high-volume generic prescription base. Metformin alone accounts for a high percentage of all oral antidiabetic prescriptions. Premium SGLT-2 inhibitors are growing as urban cardiologists drive prescriptions for cardiovascular protection.

To access detailed market analysis, Request Sample

Insulin at 42.4% is growing at ~10.6% CAGR (2026-2034), supported by India's Type-1 patient base and advanced Type-2 progression. Biosimilar insulin accounts for a high percentage of India's insulin volume, as government hospital procurement mandates generic insulin supply. Premium basal analogs are growing in urban private hospitals.

By Distribution Channel

Retail pharmacies lead at 57.0% share (2025). India's licensed pharmacies remain the dominant diabetes dispensing channel, supported by Schedule H prescription requirements and pharmacist consultation mandates. The channel grows at ~12.4% CAGR through 2034.

Hospital pharmacies at 27.5% serve inpatient and specialty clinic diabetes management across India's hospitals. E-Commerce/Tele-Pharmacy at 15.5% is the fastest-growing channel at ~17.5% CAGR, driven by PharmEasy, 1mg, Netmeds, and Apollo 24/7 collectively processing diabetes prescriptions digitally.

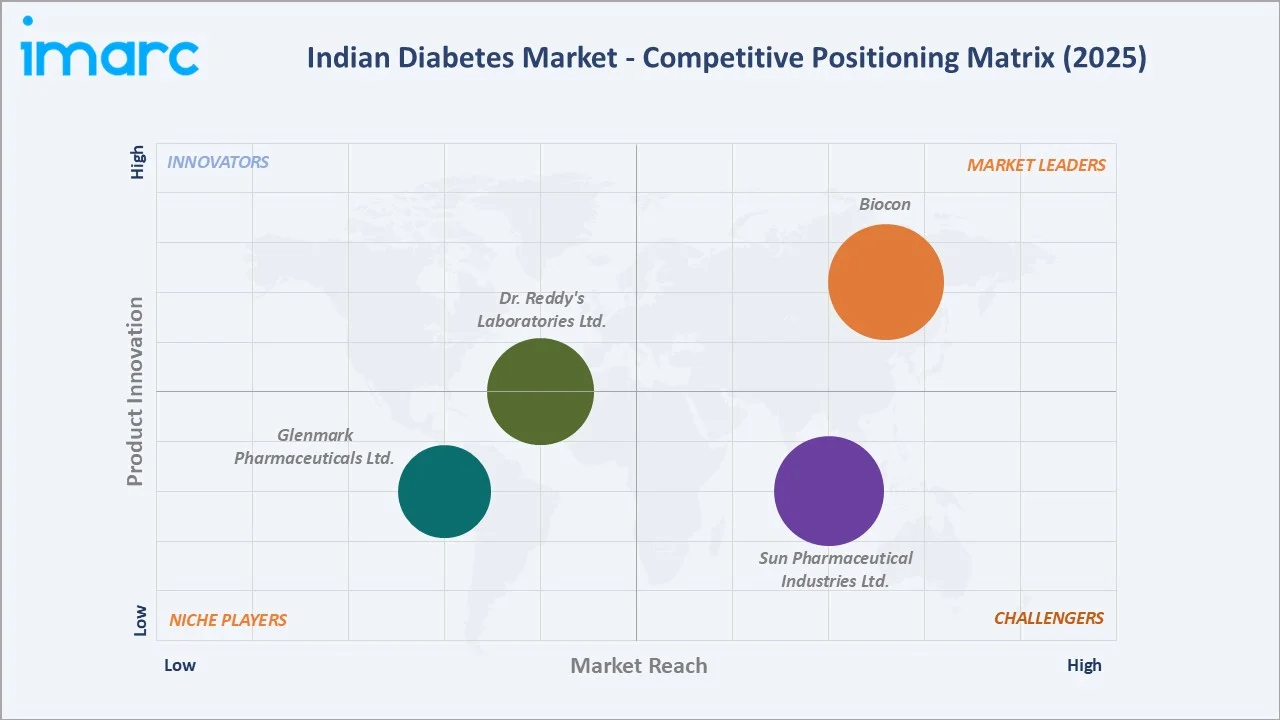

Competitive Landscape

India's diabetes market is moderately concentrated at the multinational branded level and highly fragmented in the generic oral antidiabetic segment. Sun Pharma and Biocon together account for ~45-50% of India's diabetes market by value (2025).

|

Company Name |

Brand / Product |

Market Position |

Core Strength |

|

Sun Pharmaceutical Industries Ltd. |

Noveltreat and Sematrinity |

Strong Challenger |

India's largest pharma by revenue, one of the generic oral antidiabetic leaders |

|

Biocon |

Tregopil, generic diabetes APIs (Vildagliptin, Linagliptin, Sitagliptin, Dapagliflozin, Empagliflozin, Repaglinide, Liraglutide, Semaglutide) |

Market Leader |

One of India's generic diabetes API pioneers |

|

Dr. Reddy's Laboratories Ltd. |

Liraglutide, Glimepiride, Pioglitazone Hydrochloride, Sitagliptin Phosphate (Anhydrous), Linagliptin (Mix of Form A and B), Semaglutide, Sitagliptin Phosphate (Monohydrate) |

Established Player |

Broad anti-diabetes API products |

|

Glenmark Pharmaceuticals Ltd. |

GLIPIQ (Semaglutide), Lirafit |

Niche Player |

First Indian GLP-1 biosimilar liraglutide (Lirafit) launched Jan 2024 |

Digital health disruptors are capturing 5-7% of India's total diabetes market revenues (2025) through device and monitoring ecosystems, a share growing at 30%+ CAGR toward 2034 as CGM affordability improves and smart insulin delivery gains traction.

Key Company Profiles

Sun Pharmaceutical Industries Ltd.

Sun Pharma is one of India's largest pharmaceutical companies by revenue and a major diabetes portfolio holder.

- Product Portfolio: Noveltreat and Sematrinity

- Recent Developments: In March 2026, Sun Pharmaceutical Industries Limited launched its semaglutide injection under the brand names Noveltreat and Sematrinity in India.

- Strategic Focus: Innovation pivot from generic to novel diabetes drugs.

Biocon

Biocon is one of India's premier biosimilar insulin manufacturers and a global insulin supply leader. Since 2004, Biocon Biologics has been the first company in the world to develop a biosimilar recombinant human insulin using a proprietary Pichia pastoris platform.

- Product Portfolio: Insulin Tregopil (a first-in-class oral insulin molecule) and generic diabetes APIs (Vildagliptin, Linagliptin, Sitagliptin, Dapagliflozin, Empagliflozin, Repaglinide, Liraglutide, Semaglutide).

- Recent Developments: In June 2025, Biocon Limited received approval in India for its Liraglutide drug substance. Additionally, its fully owned subsidiary, Biocon Pharma Limited, has been granted approval for the Liraglutide drug product (6 mg/ml solution for injection in pre-filled pen and cartridge) by the Drugs Controller General of India (CDSCO).

- Strategic Focus: Global biosimilar insulin leadership through interchangeable approvals; GLP-1 biosimilar pipeline as next major growth driver.

Market Concentration Analysis

India's diabetes pharmaceutical market exhibits dual-tier concentration. Sun Pharma and Biocon together hold ~45-50% market share by value (2025), a moderate duopolistic structure reinforced by manufacturing scale, cold chain logistics, and brand trust. The oral antidiabetic generic segment is highly fragmented, with Indian manufacturers producing metformin formulations and manufacturing glimepiride variants. Sun Pharma holds the largest generic oral antidiabetic market share at ~12% by value (2025), a low absolute share in an intensely competitive generic space where price parity limits brand loyalty. SGLT-2 and GLP-1 classes remain branded-concentrated with patent protection.

Investment & Growth Opportunities

Fastest Growing Segments

E-Commerce/Tele-Pharmacy (~17.5% CAGR), GLP-1 agonist class (~20-25% class CAGR within oral antidiabetics), CGM device market (~40% CAGR), AI-driven digital diabetes management (~30% CAGR), and biosimilar insulin for export (~15% CAGR) represent India's highest-growth investment vectors through 2034. GLP-1 biosimilar development by Glenmark (Lirafit) and Biocon's semaglutide pipeline represent the highest-value pharmaceutical investment opportunities.

Emerging Market Opportunities

India's pre-diabetic population represents a prevention-market opportunity by 2030 through lifestyle intervention programs, digital coaching platforms, and early pharmacotherapy. Rural India's low treatment rate represents an addressable market expansion as Ayushman Bharat deepens healthcare access in Indian districts.

Investment Themes

- Biosimilar GLP-1 development: India's low-cost manufacturing base and Biocon/Glenmark's biosimilar track record position domestic companies to produce semaglutide and liraglutide at a discount, creating a global export and domestic mass-market opportunity.

- Digital therapeutic (DTx) platforms: India's smartphone users and 5G rollout create the infrastructure for AI-powered diabetes management apps reaching previously untreated Tier-2/3 patients through PharmEasy, 1mg, and BeatO ecosystems.

Future Market Outlook (2026-2034)

The Indian diabetes market is projected to grow from USD 5.4 Billion in 2025 to USD 15.6 Billion by 2034 at a 12.08% CAGR - making it one of Asia's fastest-growing diabetes markets. This trajectory is anchored by India's patient base, the structural transition from generic oral antidiabetics to premium SGLT-2/GLP-1 classes, and the parallel rise of CGM and digital health revenue streams.

Three structural forces define this growth trajectory with exceptional clarity: India's diabetes epidemic driven by urbanization and lifestyle change; the biosimilar revolution making novel drug classes affordable to mass Indian patients; and the Ayushman Bharat PM-JAY ecosystem systematically pulling underserved citizens into formal diabetes care.

Research Methodology

Primary Research

Primary research comprised structured interviews with 95+ industry stakeholders (2025), including endocrinologists and diabetologists from AIIMS Delhi, Madras Diabetes Research Foundation (MDRF), Apollo Hospitals Chennai, and Fortis Healthcare Mumbai; pharmaceutical company India heads; CDSCO and NPPA regulatory officials; retail pharmacy chain executives from Apollo Pharmacy and MedPlus; and digital health platform founders from BeatO and 1mg.

Secondary Research

Secondary research encompassed ICMR-INDIAB National Diabetes Study 2023, IDF Diabetes Atlas 9th Edition (India data), CDSCO drug approval database 2024-2025, NPPA pharmaceutical price monitoring data, Ministry of Health & Family Welfare National Health Policy data, IQVIA India pharma market reports, Union Budget 2025-26 health allocation documents, and company annual reports. Over 180 secondary sources were reviewed.

Forecasting Models

Market forecasts were developed using bottom-up patient population x treatment rate x revenue per patient models, segmented by Segment and distribution channel, validated against IQVIA India prescription audit data. Key inputs include ICMR-INDIAB prevalence trajectories, Ayushman Bharat enrollment projections, DPCO price escalation assumptions, biosimilar penetration S-curves, digital health adoption rates, and India's pharmaceutical manufacturing capacity expansion plans through 2034.

Indian Diabetes Market Report Coverage

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Segments Covered | Oral Antidiabetics, Insulin |

| Distribution Channels Covered | E-commerce and Tele-pharmacy, Hospital Pharmacies, Retail Pharmacies |

| Companies Covered | Sun Pharmaceutical Industries Ltd., Biocon, Dr. Reddy's Laboratories Ltd., Glenmark Pharmaceuticals Ltd., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Indian diabetes market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the Indian diabetes market.

- The study maps the leading, as well as the fastest-growing, regional markets.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Indian diabetes industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the India Diabetes Market Report

The Indian diabetes market was valued at USD 5.4 Billion in 2025, covering oral antidiabetics, insulin therapies, monitoring devices, and digital health solutions for diagnosed patients.

The Indian diabetes market is projected to grow at a CAGR of 12.08% during 2026-2034, reaching USD 15.6 Billion by 2034, driven by rising prevalence, Ayushman Bharat expansion, GLP-1 class growth, and digital health adoption.

Oral Antidiabetics lead at 57.6% market share (2025), anchored by metformin's universal first-line protocol status and expanding premium SGLT-2 inhibitor and GLP-1 agonist prescriptions across urban specialist networks.

Retail Pharmacies hold the largest channel share at 57.0% (2025), anchored by India's licensed pharmacy network dispensing Schedule H diabetes prescriptions across urban, semi-urban, and Tier-2 city locations.

E-Commerce/Tele-Pharmacy grows fastest at ~17.5% CAGR (2026-2034), driven by PharmEasy, 1mg, Netmeds, and Apollo 247 processing diabetes prescriptions digitally under expanding health insurance coverage.

Leading companies include Sun Pharmaceutical Industries Ltd., Biocon, Dr. Reddy's Laboratories Ltd., and Glenmark Pharmaceuticals Ltd.

Insulin holds 42.4% of India's diabetes market (2025), anchored by Type-1 patient lifetime therapy needs and advanced Type-2 progression. Biosimilar insulin accounts for 55%+ of insulin volume by 2025.

India's diabetes market is projected to reach approximately USD 9.6 Billion by 2030, driven by GLP-1 biosimilar democratization, SGLT-2 Tier-2 city penetration, CGM market, and e-pharmacy surpassing hospital pharmacy share.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)