India Diagnostic Labs Market Size, Share, Trends and Forecast by Provider Type, Test Type, Sector, End User, and Region, 2026-2034

India Diagnostic Labs Market Summary:

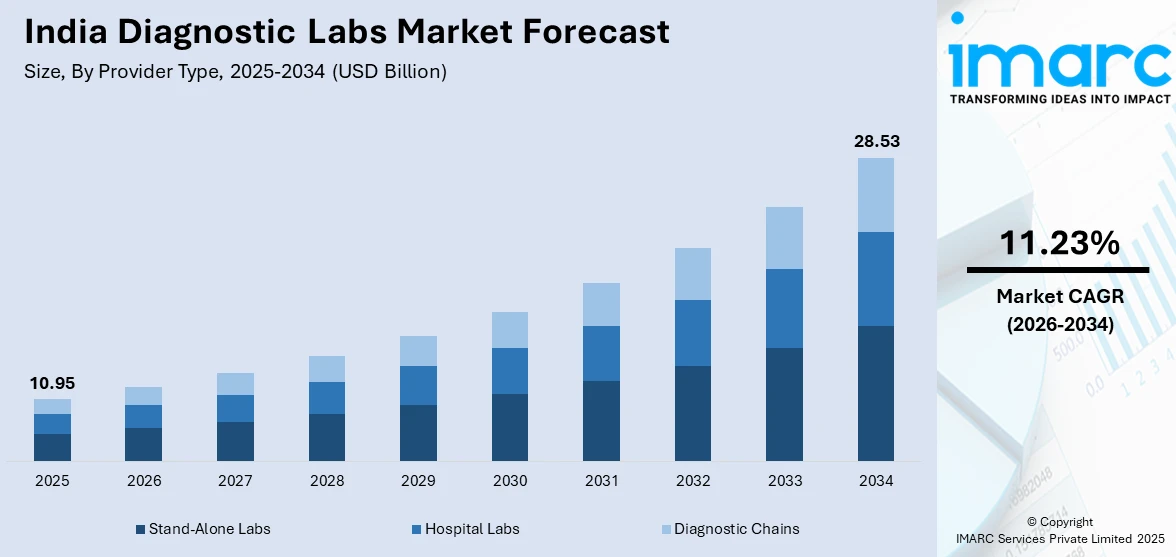

The India diagnostic labs market size was valued at USD 10.95 Billion in 2025 and is projected to reach USD 28.53 Billion by 2034, growing at a compound annual growth rate of 11.23% from 2026-2034.

The India diagnostic labs market is experiencing robust expansion driven by rising healthcare awareness, escalating burden of chronic diseases, and accelerating technological advancements across the healthcare ecosystem. Growing urbanization combined with increasing disposable incomes has elevated consumer expectations for quality diagnostic services, while the expanding middle-class population demonstrates heightened willingness to invest in preventive healthcare screenings and wellness packages. Strategic partnerships between diagnostic laboratories, healthcare providers, and technology companies are creating interconnected ecosystems that improve data sharing, enhance interoperability, and streamline diagnostic processes, ultimately strengthening India diagnostic labs market share.

Key Takeaways and Insights:

- By Provider Type: Stand-alone labs dominate the market with a share of 42% in 2025, owing to their widespread accessibility, cost-effectiveness, and ability to serve patients without prior appointments. Their extensive geographical presence in both urban and rural areas enables convenient diagnostic access for diverse population segments.

- By Test Type: Pathology leads the market with a share of 65% in 2025. This dominance is driven by the fundamental role of pathology tests including blood analysis, urine examination, and tissue diagnostics in routine health checkups, chronic disease monitoring, and preventive healthcare screening programs.

- By Sector: Urban exhibits a clear dominance in the market with 70% share in 2025, reflecting the concentration of advanced diagnostic infrastructure, higher healthcare awareness, greater insurance penetration, and elevated disposable income levels in metropolitan and tier-1 cities across India.

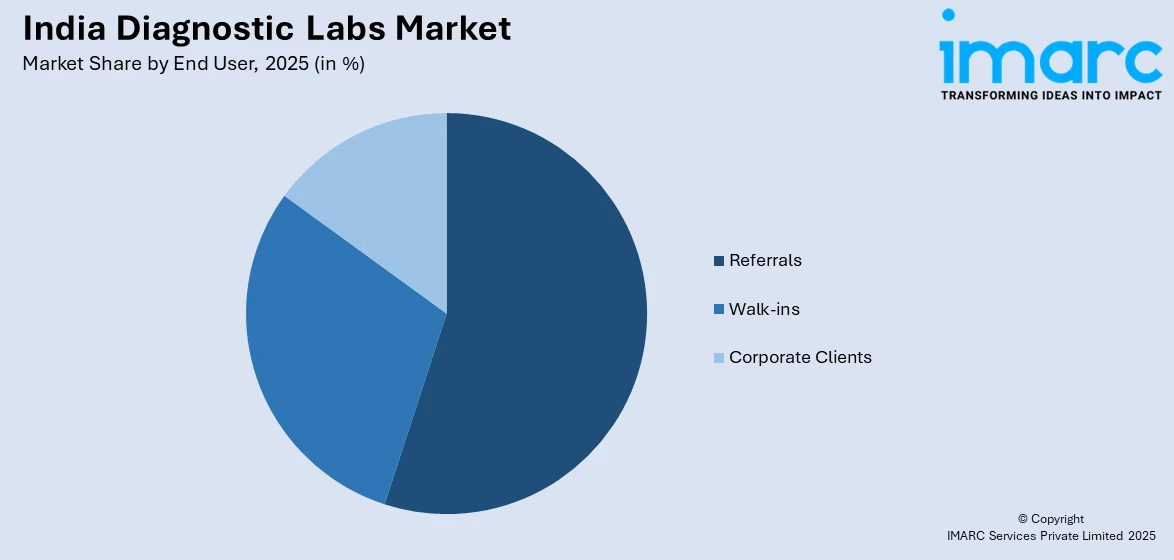

- By End User: Referrals hold the largest segment with a market share of 49% in 2025, driven by the established practice of physician-directed diagnostic testing where healthcare providers recommend specific tests based on clinical assessments, ensuring appropriate diagnostic protocols and treatment pathways.

- By Region: North India represents the leading region with 32% share in 2025, driven by the concentration of organized diagnostic chains, established healthcare infrastructure in Delhi-NCR, and the presence of major diagnostic players serving extensive population bases across Uttar Pradesh, Punjab, Haryana, and Rajasthan.

- Key Players: Key players drive the India diagnostic labs market by expanding network coverage, investing in advanced testing technologies, strengthening quality accreditation standards, and pursuing strategic acquisitions. Their focus on digital transformation, home sample collection services, and specialized diagnostic offerings accelerates market consolidation and improves healthcare accessibility.

To get more information on this market Request Sample

The India diagnostic labs market is experiencing robust expansion driven by rising healthcare awareness, increasing burden of chronic and lifestyle-related diseases, and accelerating technological advancements across the healthcare ecosystem. The sector serves as a critical foundation for evidence-based medicine, enabling accurate disease detection, treatment monitoring, and preventive health management. Growing urbanization combined with increasing disposable incomes has elevated consumer expectations for quality diagnostic services, while the expanding middle-class population demonstrates heightened willingness to invest in preventive healthcare screenings and wellness packages. Government initiatives including Ayushman Bharat and the Production Linked Incentive scheme are fostering domestic manufacturing of diagnostic equipment while enhancing healthcare accessibility across underserved regions. Strategic partnerships between diagnostic laboratories, healthcare providers, and technology companies are creating interconnected ecosystems that improve data sharing, enhance interoperability, and streamline diagnostic processes. Digital transformation through AI-powered diagnostics, cloud-based platforms, and home sample collection services is reshaping service delivery models across the market.

India Diagnostic Labs Market Trends:

Digital Transformation and AI-Powered Diagnostics

The India diagnostic labs market is witnessing accelerating adoption of artificial intelligence and digital technologies that enhance test accuracy, reduce turnaround times, and improve patient accessibility. Cloud-based laboratory information management systems enable seamless data exchange across healthcare facilities while AI-powered diagnostic tools automate slide scanning, image analysis, and reporting processes. Leading diagnostic providers are integrating digital pathology solutions that allow remote specialist consultations, particularly benefiting underserved regions. In January 2026, Dr Lal PathLabs announced plans to launch 'Sovaaka' preventive wellness centres integrating comprehensive diagnostics with personalized digital health guidance, demonstrating the sector's evolution toward technology-enabled patient-centric care models.

Home Sample Collection and Point-of-Care Testing Expansion

Home-based diagnostic services have emerged as mainstream offerings across the India diagnostic labs market, supported by mobile sample collection networks and digital report delivery systems. Point-of-care testing devices are expanding accessibility in remote areas, providing quick and cost-effective diagnostics without requiring patients to travel to centralized facilities. The convenience factor combined with post-pandemic health consciousness has permanently elevated consumer expectations for doorstep services. In December 2024, Orange Health Labs secured funding of USD 12 Million from Amazon Smbhav Venture Fund to fuel product innovation and expand home collection capabilities, highlighting the sector's trajectory toward decentralized diagnostic delivery models.

Preventive Healthcare and Specialized Testing Growth

Consumer preferences are shifting from reactive to proactive healthcare approaches, driving significant demand for preventive wellness packages, genetic testing, and early cancer screening programs across the India diagnostic labs market growth trajectory. Organized diagnostic chains are expanding specialized test portfolios covering oncology, reproductive health, autoimmune disorders, and transplant immunology to capture higher-value testing segments. Advanced molecular diagnostics utilizing next-generation sequencing technologies are enabling personalized medicine approaches that tailor diagnostic protocols to individual patient profiles, improving disease detection accuracy and treatment outcomes.

Market Outlook 2026-2034:

The India diagnostic labs market outlook remains highly promising as the sector continues transforming healthcare delivery through technological innovation, network expansion, and evolving consumer healthcare behaviors. Rising prevalence of lifestyle-related chronic conditions including diabetes, cardiovascular diseases, and cancer necessitates frequent diagnostic monitoring, creating sustained demand growth. Government healthcare initiatives focused on universal health coverage and digital health infrastructure development are enhancing accessibility while driving formal sector expansion. Organized diagnostic chains are pursuing aggressive expansion strategies combining organic growth with strategic acquisitions to consolidate market share from fragmented unorganized players. Increasing health insurance penetration and corporate wellness programs are broadening the consumer base while technology investments enable operational efficiencies that support sustainable growth trajectories. The market generated a revenue of USD 10.95 Billion in 2025 and is projected to reach a revenue of USD 28.53 Billion by 2034, growing at a compound annual growth rate of 11.23% from 2026-2034.

India Diagnostic Labs Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Provider Type |

Stand-Alone Labs |

42% |

|

Test Type |

Pathology |

65% |

|

Sector |

Urban |

70% |

|

End User |

Referrals |

49% |

|

Region |

North India |

32% |

Provider Type Insights:

- Stand-Alone Labs

- Hospital Labs

- Diagnostic Chains

Stand-alone labs dominate with a market share of 42% of the total India diagnostic labs market in 2025.

Stand-alone diagnostic laboratories maintain market leadership through their extensive geographical footprint and accessible service models that cater to diverse population segments across urban and semi-urban areas. These facilities run independently and are not affiliated with any hospitals. They provide competitively priced comprehensive test menus that include routine blood tests, urine analysis, and specialist diagnostics. Their proximity to residential neighborhoods enables convenient patient access without requiring complex appointment scheduling or hospital visits. The segment benefits from lower operational costs compared to hospital-based facilities, allowing competitive pricing strategies that attract price-sensitive consumers.

Stand-alone laboratories are increasingly adopting technology-enabled service delivery including online booking platforms, digital report access, and home sample collection capabilities to enhance patient convenience and capture market share from unorganized players. Quality-conscious consumers demonstrate growing preference for accredited facilities offering standardized testing protocols and reliable results. In April 2025, Lupin Diagnostics announced that all its 27 greenfield laboratories across India achieved NABL accreditation, reflecting the segment's commitment to internationally recognized testing standards that differentiate organized players from fragmented local operators while building consumer trust and physician referral networks.

Test Type Insights:

- Pathology

- Radiology

Pathology leads with a share of 65% of the total India diagnostic labs market in 2025.

Pathology services encompassing biochemistry, hematology, microbiology, and molecular diagnostics form the foundational pillar of diagnostic laboratory operations due to their essential role in disease detection, treatment monitoring, and preventive healthcare screening. These laboratory-based tests analyze blood, urine, tissue, and other biological samples to identify disease markers, evaluate organ function, and monitor therapeutic responses. The widespread applicability of pathology tests across virtually all medical conditions ensures sustained demand from both acute care and chronic disease management protocols. Increasing health awareness combined with preventive healthcare adoption drives regular diagnostic testing among asymptomatic populations.

Advanced molecular diagnostic capabilities including RT-PCR, ELISA, and next-generation sequencing technologies are expanding pathology service portfolios toward precision medicine applications covering oncology, infectious diseases, and genetic disorders. In vitro diagnostics innovations enable earlier and more accurate disease detection while reducing turnaround times for critical results. Chronic conditions including diabetes and hypertension disproportionately affect elderly populations across both rural and urban areas, necessitating ongoing diagnostic monitoring that sustains pathology segment growth. The segment continues evolving through automation investments that enhance testing efficiency while maintaining quality standards across high-volume operations.

Sector Insights:

- Urban

- Rural

Urban exhibits a clear dominance with a 70% share of the total India diagnostic labs market in 2025.

Urban areas command decisive market leadership driven by concentrated healthcare infrastructure, elevated health awareness levels, higher disposable income availability, and greater health insurance penetration among metropolitan populations. Major cities including Delhi, Mumbai, Bengaluru, and Chennai host advanced diagnostic facilities offering comprehensive test portfolios spanning routine screening to specialized molecular diagnostics. The urban population's accessibility to organized diagnostic chains, corporate wellness programs, and digital health platforms accelerates formal sector utilization while creating expectations for quality-assured services with convenient delivery models.

Urban diagnostic markets benefit from physician density enabling referral-based testing protocols while corporate health programs drive systematic employee screening initiatives. According to the industry report, only 25% of populations in semi-rural and rural areas have access to modern healthcare facilities nearby, contrasting sharply with urban accessibility levels. This infrastructure disparity concentrates diagnostic revenues in urban centers while creating expansion opportunities for organized players seeking rural penetration. Leading diagnostic chains are deploying hub-and-spoke models connecting urban reference laboratories with collection centers in surrounding areas to extend geographical reach without duplicating expensive equipment investments.

End User Insights:

Access the comprehensive market breakdown Request Sample

- Referrals

- Walk-ins

- Corporate Clients

Referrals hold the leading segment with a 49% share of the total India diagnostic labs market in 2025.

Physician referrals constitute the primary patient acquisition channel for diagnostic laboratories as healthcare providers direct patients toward specific tests based on clinical assessments, symptom presentations, and treatment monitoring requirements. This referral-driven model ensures appropriate test selection aligned with diagnostic protocols while building sustained relationships between laboratories and prescribing physicians. Hospitals, clinics, and private practitioners generate consistent testing volumes through outpatient consultations where diagnostic workups inform treatment decisions. The referral segment benefits from recurring testing patterns among patients with chronic conditions requiring periodic monitoring.

Organized diagnostic chains actively cultivate physician relationships through service quality assurance, rapid turnaround times, and comprehensive test menus that position them as preferred laboratory partners. Specialized diagnostic capabilities in oncology, reproductive health, and autoimmune disorders attract referrals from specialists seeking advanced testing protocols. In December 2024, Metropolis Healthcare acquired Core Diagnostics for approximately INR 246.8 Crores, strengthen Metropolis' position in Northern and Eastern India and improve its capacity for sophisticated cancer diagnostics. This strategic move demonstrates how diagnostic chains build referral networks through specialized capabilities that differentiate them from general testing facilities while expanding addressable markets.

Regional Insights:

- North India

- West and Central India

- South India

- East and Northeast India

North India represents the largest region with a 32% share of the total India diagnostic labs market in 2025.

North India commands regional market leadership driven by the concentration of major diagnostic chains with established brand equity in Delhi-NCR, extensive healthcare infrastructure across metropolitan centers, and large population bases spanning Uttar Pradesh, Rajasthan, Punjab, Haryana, and Uttarakhand. The region benefits from headquarters operations of leading players that have built dominant market positions through decades of network expansion combined with strong physician referral relationships and comprehensive service portfolios.

Growing consumer healthcare awareness, rising chronic disease prevalence, and expanding insurance coverage are accelerating organized sector penetration in tier-2 and tier-3 cities where unorganized players currently dominate. Diagnostic chains are pursuing strategic acquisitions to strengthen regional presence, with Metropolis Healthcare completing multiple acquisitions in North India during FY2025 including Core Diagnostics in Delhi-NCR, Scientific Pathology in Agra, and DAPIC in Dehradun, significantly expanding its regional footprint and revenue contribution.

Market Dynamics:

Growth Drivers:

Why is the India Diagnostic Labs Market Growing?

Rising Burden of Chronic and Lifestyle-Related Diseases

The escalating prevalence of non-communicable diseases including diabetes, cardiovascular conditions, cancer, and respiratory ailments across India's population creates sustained demand for diagnostic testing services essential for disease detection, progression monitoring, and treatment efficacy evaluation. Lifestyle modifications driven by urbanization, dietary changes, sedentary behaviors, and occupational stress patterns contribute to chronic disease acceleration across younger demographic segments traditionally considered low-risk populations. Diagnostic laboratories serve critical roles throughout patient care journeys from initial screening and disease confirmation through ongoing therapeutic monitoring and periodic health assessments. The aging population demographic transition presents compounding demand pressures as individuals aged 60 and above demonstrate significantly higher chronic disease prevalence requiring frequent diagnostic surveillance. These epidemiological trends ensure diagnostic testing remains fundamental to healthcare delivery while creating growth opportunities for laboratories expanding disease-specific testing capabilities and chronic care management programs.

Government Healthcare Initiatives and Digital Health Infrastructure

Comprehensive government healthcare initiatives including Ayushman Bharat Pradhan Mantri Jan Arogya Yojana and the Ayushman Bharat Digital Mission are transforming healthcare accessibility while integrating diagnostic services into national health coverage frameworks that reach underserved population segments. The PM-JAY scheme provides health insurance coverage to over 50 Crore vulnerable citizens, enabling access to hospitalization services where diagnostic testing forms integral components of care pathways. Ayushman Arogya Mandirs established across primary healthcare facilities are expanding diagnostic availability at community levels while focusing on preventive care and non-communicable disease screening. The digital health ecosystem now encompasses over 67 crore citizens holding Ayushman Bharat Health Account (ABHA) identifications, enabling seamless health record portability across diagnostic facilities. Production Linked Incentive schemes foster domestic manufacturing of diagnostic equipment reducing import dependence while enhancing affordability.

Technology Adoption and Operational Efficiency Improvements

Rapid technological advancement across diagnostic modalities enables laboratories to deliver more accurate results with faster turnaround times while expanding service accessibility through digital platforms, home collection networks, and telemedicine integration. Artificial intelligence applications automate imaging analysis, pathology slide review, and diagnostic interpretation tasks, addressing qualified professional shortages while enhancing consistency and throughput across high-volume operations. Laboratory information management systems streamline sample tracking, result reporting, and quality control processes while enabling seamless data exchange across healthcare ecosystems. Cloud-based platforms facilitate remote specialist consultations through telepathology and teleradiology services that extend diagnostic expertise to underserved regions lacking resident specialists. Point-of-care testing devices enable rapid diagnostics at distributed locations while reducing dependence on centralized laboratory infrastructure. India's AI in medical diagnostics market size reached USD 55.04 Million in 2024. Looking forward, IMARC Group expects the market to reach USD 546.95 Million by 2033, exhibiting a growth rate (CAGR) of 26.90% during 2025-2033, reflecting substantial technology investments transforming diagnostic service delivery. These technological enablers allow organized diagnostic chains to differentiate service offerings while achieving operational efficiencies that support competitive pricing and network expansion strategies.

Market Restraints:

What Challenges the India Diagnostic Labs Market is Facing?

Limited Rural Healthcare Infrastructure and Accessibility Gaps

Rural areas face significant diagnostic access challenges due to inadequate healthcare infrastructure, limited laboratory facilities, and geographical barriers that impede timely service delivery. Many primary health centers lack essential diagnostic equipment while existing facilities contend with resource constraints including outdated technologies and restricted operating hours. Population density challenges make establishing comprehensive diagnostic networks economically unviable across dispersed rural settlements.

Shortage of Skilled Laboratory Professionals

India faces critical shortages of qualified pathologists, microbiologists, laboratory technicians, and other diagnostic professionals that constrain service quality and capacity expansion across the healthcare sector. Limited specialized training programs combined with retention challenges due to competitive opportunities create persistent workforce deficits affecting testing accuracy, turnaround times, and service standardization, particularly in semi-urban and rural regions where qualified professionals remain scarce.

Regulatory Compliance and Quality Standardization Challenges

The fragmented regulatory landscape across state jurisdictions creates compliance complexities for diagnostic laboratories operating multi-state networks while inconsistent quality enforcement allows substandard operators to persist in underserved markets. The predominantly unorganized sector structure with low entry barriers enables proliferation of laboratories lacking proper quality management systems, calibrated equipment, and trained personnel, potentially affecting diagnostic accuracy and patient outcomes.

Competitive Landscape:

The India diagnostic labs market is characterized by intense competition among organized national chains, regional players, and hospital-based laboratories pursuing network expansion, service differentiation, and market share consolidation strategies. Leading players collectively command substantial organized market share while aggressively expanding into tier-2 and tier-3 cities through organic growth and strategic acquisitions. Companies are investing in advanced testing capabilities, digital transformation initiatives, and home collection infrastructure to differentiate service offerings and capture higher-value specialized testing segments. Quality accreditation, physician relationship management, and operational efficiency improvements drive competitive positioning as organized players seek market share gains from fragmented unorganized operators.

India Diagnostic Labs Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Provider Types Covered | Stand-Alone Labs, Hospital Labs, Diagnostic Chains |

| Test Types Covered | Pathology, Radiology |

| Sectors Covered | Urban, Rural |

| End Users Covered | Referrals, Walk-ins, Corporate Clients |

| Regions Covered | North India, West and Central India, South India, East and Northeast India |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Diagnostic Labs Market Report

The India diagnostic labs market size was valued at USD 10.95 Billion in 2025.

The India diagnostic labs market is expected to grow at a compound annual growth rate of 11.23% from 2026-2034 to reach USD 28.53 Billion by 2034.

Stand-alone labs dominated the market with a share of 42%, driven by their widespread geographical presence, convenient accessibility without appointments, competitive pricing, and ability to serve diverse population segments across urban and semi-urban areas.

Key factors driving the India diagnostic labs market include rising chronic disease prevalence, government healthcare initiatives like Ayushman Bharat, increasing health awareness, technology adoption, expanding insurance coverage, and growing demand for preventive healthcare services.

Major challenges include limited rural healthcare infrastructure, shortage of skilled laboratory professionals, regulatory compliance complexities, quality standardization issues across fragmented markets, high operational costs, and data privacy concerns with digital transformation.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade