India Diatomite Market Size, Share, Trends and Forecast by Type, Application, and Region 2026-2034

India Diatomite Market Summary:

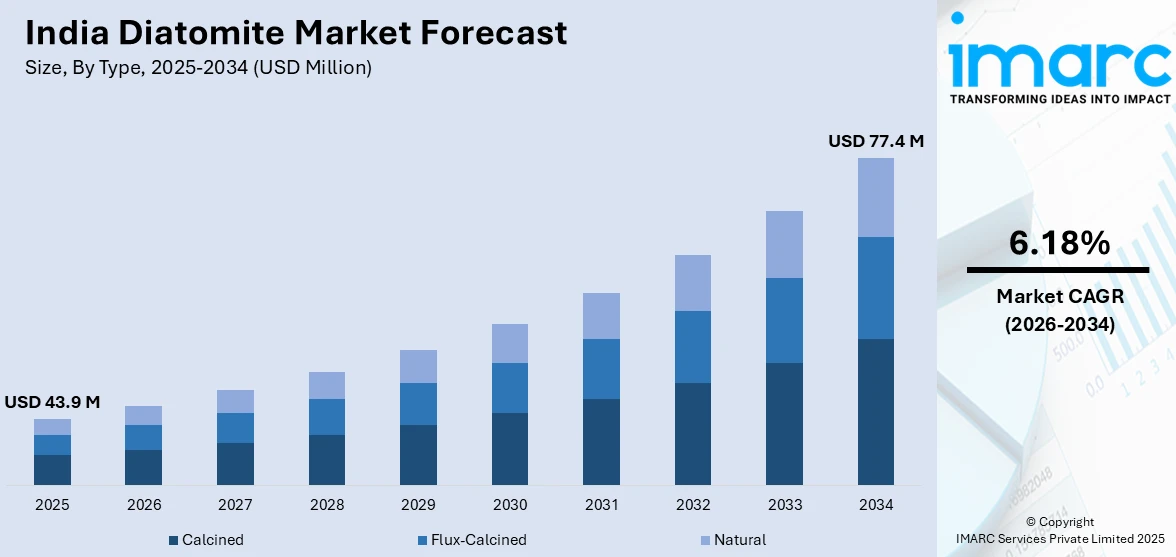

The India diatomite market size was valued at USD 43.9 Million in 2025 and is projected to reach USD 77.4 Million by 2034, growing at a compound annual growth rate of 6.18% from 2026-2034.

The India diatomite market is witnessing steady growth driven by rising demand from filtration, construction, agriculture, and industrial absorbents, supported by infrastructure development, environmental regulations, and expanding manufacturing activities, while challenges include limited domestic reserves, quality variability, and import dependence, prompting investments in processing technologies, capacity expansion, and value added applications to enhance competitiveness and sustainability across regional end-use segments.

Key Takeaways and Insights:

- By Type: Calcined held the largest share in the market at 55.8% in 2025, due to superior filtration efficiency, higher purity, thermal stability, and widespread industrial acceptance.

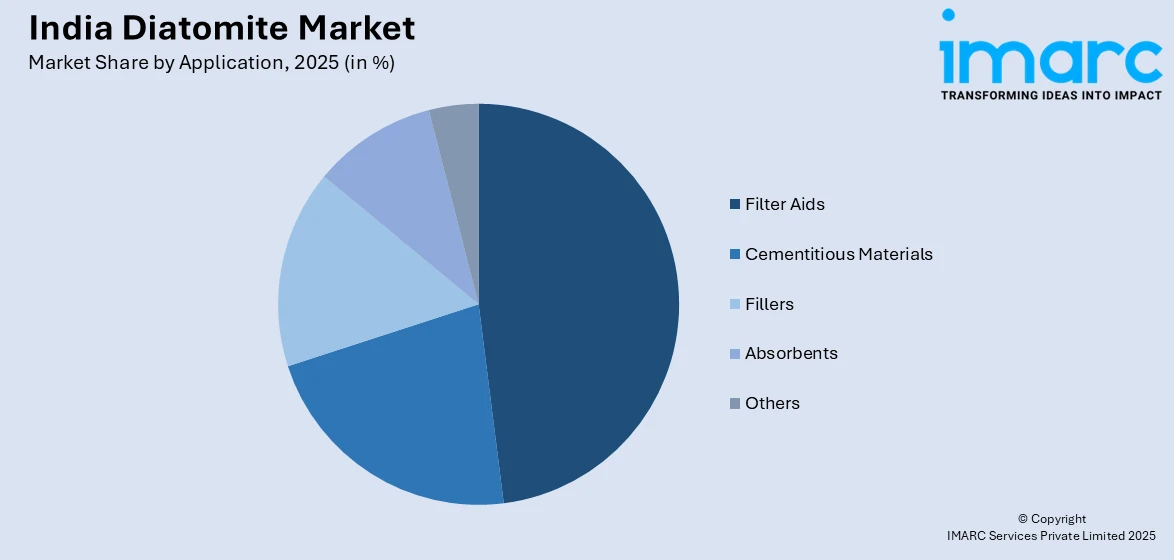

- By Application: Filter aids dominate the market with a share of 48.3% in 2025, owing to extensive use in beverages, chemicals, pharmaceuticals, and water treatment industries.

- By Region: West India held the biggest market segment, capturing 39.5% share, in 2025, driven by industrial concentration, better logistics infrastructure, and proximity to key end-use industries.

- Key Players: The competitive landscape is moderately consolidated, with key players focusing on capacity expansion, product quality improvement, and application diversification. Strategic partnerships, technological advancements, and regional distribution networks are prioritized to strengthen market presence and address rising demand across industrial and filtration applications.

To get more information on this market Request Sample

The India diatomite market is developing gradually as industries seek cost-effective, naturally derived materials for specialized processing requirements. Growth is also supported by increasing emphasis on process optimization, purity standards, and waste reduction across industrial operations. According to the CPCB, India produces nearly 7.9 million tons of hazardous industrial waste each year, along with 10–12 million tons of construction and demolition waste. This growing waste burden supports demand for diatomite in filtration, absorption, and waste-treatment applications. Diatomite’s lightweight structure, chemical inertness, and high porosity make it suitable for niche applications such as insulation, polishing agents, fillers, and soil conditioning. Furthermore, growing regulatory focus on sustainable materials and resource efficiency is encouraging product adoption. Likewise, continual technological upgrades in beneficiation and refinement are improving domestic usability and application range. Demand is largely industrially driven, with purchasing decisions influenced by performance efficiency rather than volume.

India Diatomite Market Trends:

Rising Customization of Diatomite Grades for Industrial Processes

A notable trend in the India diatomite market is the growing demand for customized material grades tailored to specific industrial processes. End-use industries increasingly require controlled particle size, permeability, and purity to enhance operational efficiency and reduce material wastage. This is encouraging suppliers to move beyond standardized products and offer application-specific diatomite solutions. For example, Caltron Clays & Chemicals supplies certified food-grade diatomaceous earth with controlled particle sizes (5–50 microns), ISO 9001:2015 and FSSAI compliance, supporting beverage brands with scalable bulk supply, improved clarity, extended shelf life, and clean-label filtration solutions. Such customization improves performance outcomes in polishing, insulation, and absorbent applications, strengthening supplier–customer collaboration and long-term procurement relationships.

Shift Toward Domestic Value Addition and Processing Capabilities

The market is experiencing a gradual shift toward domestic value addition, with companies investing in localized processing and refinement facilities. Rather than exporting raw diatomite or relying extensively on imported finished grades, manufacturers are focusing on beneficiation, thermal treatment, and grading within India. This trend supports cost optimization, reduces supply chain risks, and improves responsiveness to domestic demand. Moreover, enhanced local processing capabilities also contribute to better quality control and improved consistency across industrial applications.

Increasing Adoption in Niche and Specialty Applications

Recent market developments indicate expanding use of diatomite in niche and specialty applications beyond traditional filtration and construction uses. Industries such as paints, coatings, rubber compounding, and specialty chemicals are incorporating diatomite as a functional filler and performance enhancer. According to the National Pesticide Information Center, over 150 insecticide products contain diatomaceous earth. Studies indicate it can also help control mites, parasites, and internal worms, particularly when used alongside complementary pest management methods.This diversification is driven by the material’s lightweight nature, chemical stability, and absorbent properties. Growing awareness of these functional benefits is gradually broadening the application base and improving overall market resilience.

Market Outlook 2026-2034:

The India diatomite market is projected to maintain steady growth over the coming years, driven by rising industrial modernization and the adoption of advanced manufacturing practices. As per the World Robotics 2024 report, India ranks seventh globally in robot installations, with its industrial robotics market projected to reach USD 264 Million by 2028. Government-led Industry 4.0 and the USD 24 Billion PLI scheme also aim to augment manufacturing GVA from 14% to 21% by 2032. Likewise, increasing awareness of diatomite’s thermal insulation, lightweight filler, and chemical stabilization properties is encouraging uptake in emerging sectors such as automotive components, electronics, and specialty polymers. Furthermore, expansion of regional mining initiatives, coupled with strategic collaborations between suppliers and end-users, is expected to enhance supply reliability, while gradual technological advancements improve product efficiency and broaden potential applications. The market generated a revenue of USD 43.9 Million in 2025 and is projected to reach a revenue of USD 77.4 Million by 2034, growing at a compound annual growth rate of 6.18% from 2026-2034.

India Diatomite Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Type |

Calcined |

55.8% |

|

Application |

Filter Aids |

48.3% |

|

Region |

West India |

39.5% |

Type Insights:

- Calcined

- Flux-Calcined

- Natural

Calcined captured the largest segment, representing 55.8% share of the total India diatomite market, in 2025.

Its enhanced thermal stability, higher porosity, and improved filtration efficiency make it particularly suitable for chemical, pharmaceutical, and food-grade applications. Manufacturers prefer calcined diatomite for its consistent quality and ability to meet stringent industrial standards, contributing significantly to market growth across filtration, insulation, and absorbent applications.

The dominance of calcined diatomite is further supported by increasing demand in downstream processing industries. Its adaptability to both high-temperature and precision applications ensures a competitive advantage over raw or unprocessed variants. With continuous investment in calcination technology and processing infrastructure, the segment is expected to maintain its leadership position, offering reliable performance and scalability to meet evolving industrial needs.

Application Insights:

Access the comprehensive market breakdown Request Sample

- Filter Aids

- Cementitious Materials

- Fillers

- Absorbents

- Others

Filter Aids dominates with a market share of 48.3% of the total India diatomite market in 2025.

The ability of filter aids to remove fine impurities efficiently in beverages, chemicals, pharmaceuticals, and water treatment processes drives widespread adoption. Industries favor diatomite-based filter aids for their high porosity, chemical inertness, and cost-effectiveness, which enhance product quality while ensuring compliance with safety and regulatory standards. As such, in September 2025, 20 Microns Nano Minerals Ltd., India’s leading specialty functional additives manufacturer, produced nano-engineered minerals, including filter aids and diatomite replacements, for paints, plastics, cosmetics, and more, enhancing product performance, sustainability, and efficiency across 12+ industries with customized solutions.

The prominence of filter aids is reinforced by increasing industrial focus on purification and wastewater treatment. As urbanization and industrialization intensify, the demand for high-performance filtration solutions grows. Moreover, continuous product innovation, such as micronized and surface-modified grades, is expanding the scope of filter aid applications, ensuring that this segment remains the primary contributor to overall market value in India.

Region Insights:

- North India

- South India

- East India

- West India

West India exhibits a clear dominance with a 39.5% share of the total India diatomite market in 2025.

The region benefits from developed logistics infrastructure, facilitating efficient distribution to major consumption hubs. Accordingly, in December 2025, Mumbai Port’s Integrated Master Plan 2047 aims to expand capacity to over 100 million tonnes per annum, upgrade liquid bulk and chemical infrastructure, and redevelop port land, with traffic projected to rise from 68.3 to 106.2 million tonnes by 2053. High concentration of manufacturing facilities, particularly in chemicals, water treatment, and construction, supports steady regional demand, reinforcing West India’s dominant position in the national diatomite market.

The region’s leadership is further strengthened by active exploration and mining initiatives, which improve the availability of raw materials and reduce reliance on imports. West India also attracts strategic investments in processing and beneficiation plants, enhancing product quality and market responsiveness. Its industrial diversity and supply chain efficiency make it a focal point for domestic diatomite growth in the foreseeable future.

Market Dynamics:

Growth Drivers:

Why is the India Diatomite Market Growing?

Enhanced Integration with Water Treatment and Environmental Compliance Initiatives

A significant trend in the India diatomite market is its increased integration into water treatment systems aligned with environmental compliance mandates. Municipal and industrial sectors are emphasizing improved wastewater management and effluent standards, driving demand for high‑efficiency diatomite filtration media. According to a report by the Ministry of Housing and Urban Affairs, India could unlock USD 3 Billion annually through circular-economy initiatives, USD 1.7 Billion from municipal solid waste and USD 1.2 Billion from wastewater, supported by a USD 1.2 Billion GOBARdhan investment in 500 bio-CNG plants by 2028–29. This shift underscores the mineral’s role in supporting regulatory frameworks for water quality. As sustainability targets gain prominence, diatomite’s filtration properties and low environmental footprint position it as a preferred solution across purification applications.

Strategic Investments in Regional Logistics Infrastructure

India’s diatomite market is increasingly benefiting from targeted investments in regional logistics infrastructure. Efficient transportation and storage networks are critical because diatomite is bulky, fragile, and often needs careful handling to preserve its filtration and absorption properties. Companies are also developing specialized warehouses, improved road and rail connectivity, and port-based distribution hubs to reduce transit times and lower costs. A 2024 industry survey found over 60% of chemical companies in India plan to digitize supply chains by 2026, using AI, blockchain, and real-time tracking to enhance visibility, compliance, reduce waste, and improve logistics responsiveness. This not only facilitates faster delivery to industrial users across sectors such as pharmaceuticals, food & beverage, and water treatment but also strengthens India’s domestic supply chain, reducing dependency on imported diatomite.

Rising Focus on Quality Standardization and Certification

As industrial applications of diatomite expand in India, there is growing emphasis on quality standardization and certification. High-purity diatomite is crucial for filtration, food, and pharmaceutical uses, where impurities can affect product performance and safety. Manufacturers are increasingly adopting ISO, FSSAI, and other international certifications to ensure consistency, traceability, and regulatory compliance. Standardized grades also allow Indian producers to compete in global markets, gain consumer confidence, and meet strict industrial specifications, fostering growth in both domestic and export segments.

Market Restraints:

What Challenges the India Diatomite Market is Facing?

Limited High‑Grade Resource Availability

One of the principal challenges in the India diatomite market is the limited availability of high‑grade, uniformly consistent deposits. Many indigenous sources contain variable silica content and impurities, necessitating extensive beneficiation to meet industrial specifications, particularly for pharmaceutical, food, and fine filtration applications. This increases processing costs and may deter investment. The scarcity of premium feedstock constrains production scalability, impacts pricing competitiveness, and poses barriers to satisfying both domestic and international quality‑sensitive demand.

Inadequate Processing and Refinement Infrastructure

Despite growing demand, India faces constraints in advanced diatomite processing and refinement infrastructure. Existing facilities often lack modern equipment for controlled micronization, thermal treatment, and particle size standardization. This shortfall leads to inconsistent product quality, higher energy consumption, and dependency on imported value‑added grades. Without significant capital investments in state‑of‑the‑art plants and skilled technical personnel, manufacturers may struggle to meet evolving industry requirements in sectors such as food, pharmaceuticals, and high‑performance industrial filtration.

Environmental and Regulatory Compliance Challenges

Environmental and regulatory compliance presents a persistent challenge for diatomite mining and processing. Stringent environmental norms related to land use, water discharge, and particulate emissions increase operational costs and extend project lead times. Mines in ecologically sensitive zones face protracted clearances, while stringent standards for re‑vegetation and mine closure impose financial burdens. Compliance complexities, coupled with evolving national and state‑level policies, can deter new entrants, slow expansion, and restrict production growth in the diatomite sector.

Competitive Landscape:

The competitive landscape of the India diatomite market is characterised by a mixture of established mineral producers and emerging specialised processors, striving to balance cost‑efficiency with quality enhancements. Domestic players increasingly invest in beneficiation, micronization, and value‑addition to reduce reliance on imports, while targeting high‑growth sectors such as filtration, pharmaceuticals, and food processing. Competitive differentiation also hinges on product purity, certification compliance, and supply reliability. Apart from this, strategic partnerships, regional logistics improvements, and adoption of advanced processing technologies are enabling firms to strengthen market share and compete more effectively both domestically and internationally.

Recent Developments:

- In January 2026, Researchers explored hydrothermal liquefaction (HTL) to convert coastal plastic waste from Chennai into bio-crude without extensive pretreatment. Using diatomaceous earth and aqueous recirculation, they enhanced energy efficiency and yield, demonstrating a scalable, sustainable method for marine waste valorization while advancing clean energy goals.

- In August 2025, Researchers discovered a new diatom species, Climaconeis heteropolaris, on Karnataka’s west coast. Characterized by its unique heteropolar valve, lanceolate-clavate shape, and distinct striae, this finding enhances understanding of marine biodiversity, ecosystem monitoring, and conservation of coastal and estuarine habitats in India.

India Diatomite Market Report Coverage:

|

Report Features |

Details |

|

Base Year of the Analysis |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Units |

Million USD |

|

Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

|

Types Covered |

Calcined, Flux-Calcined, Natural |

|

Application Covered |

Filter Aids, Cementitious Materials, Fillers, Absorbents, Others |

|

Regions Covered |

North India, South India, East India, West India |

|

Customization Scope |

10% Free Customization |

|

Post-Sale Analyst Support |

10-12 Weeks |

|

Delivery Format |

PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Diatomite Market Report

The India diatomite market size was valued at USD 43.9 Million in 2025.

The India diatomite market is expected to grow at a compound annual growth rate of 6.18% from 2026-2034 to reach USD 77.4 Million by 2034.

Calcined dominated the market with 55.8% share in 2025, primarily due to increasing demand for high-purity filtration applications in pharmaceuticals, beverages, and personal care products, driving widespread adoption across industries.

Key factors driving the India diatomite market include rising demand for high-quality filtration, expanding pharmaceutical and beverage industries, increased adoption of clean-label products, growing industrial applications of diatomite, and investments in advanced processing technologies.

Major challenges in the India diatomite market include limited high-grade deposits, inadequate processing infrastructure, high beneficiation costs, strict environmental regulations, and competition from imported value-added diatomite.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: sales@imarcgroup.com

Client Testimonials

.webp)