India Diesel Genset Market Size, Share, Trends and Forecast by Power Output, Power Rating, Application, End User, and Region, 2026-2034

India Diesel Genset Market Size, Share, Trends & Forecast (2026-2034)

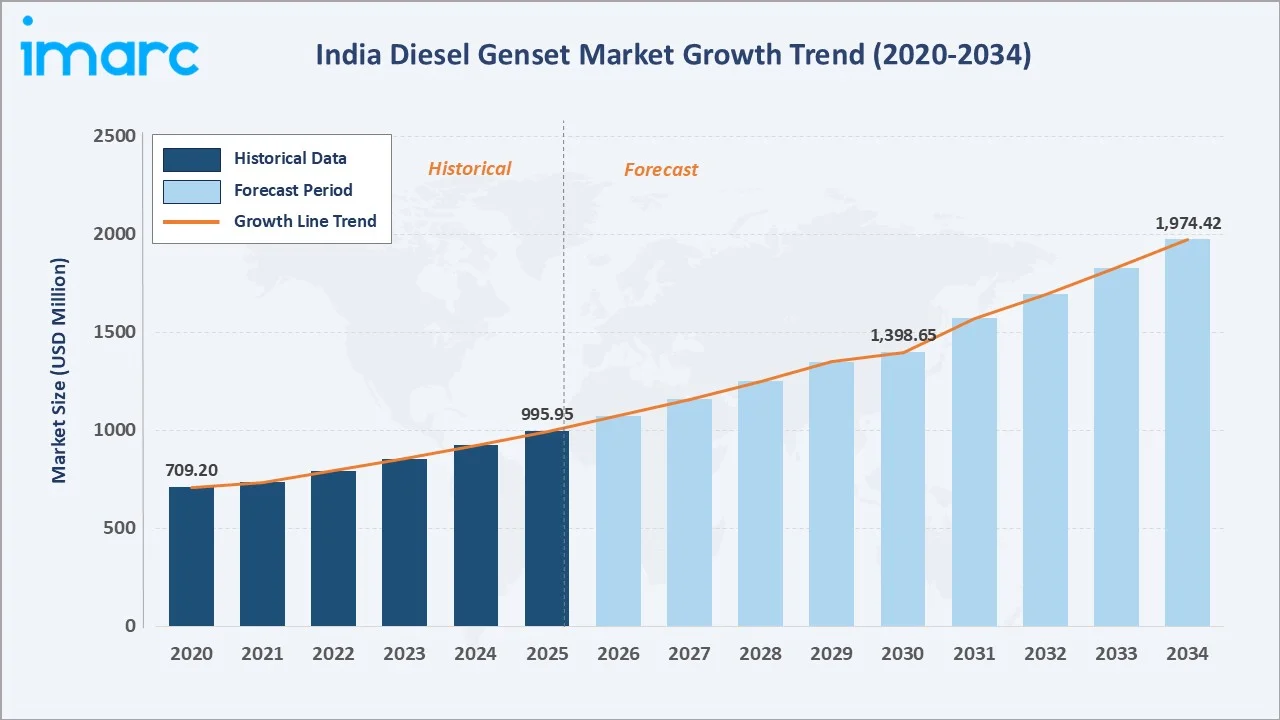

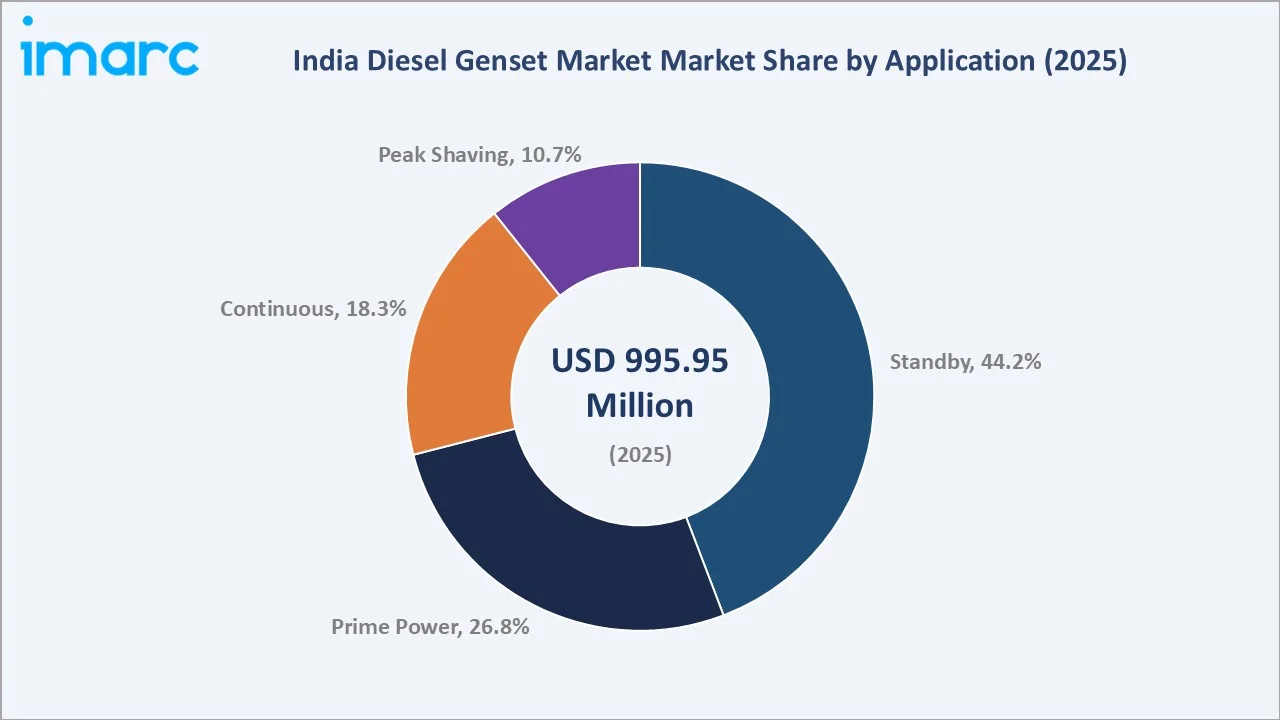

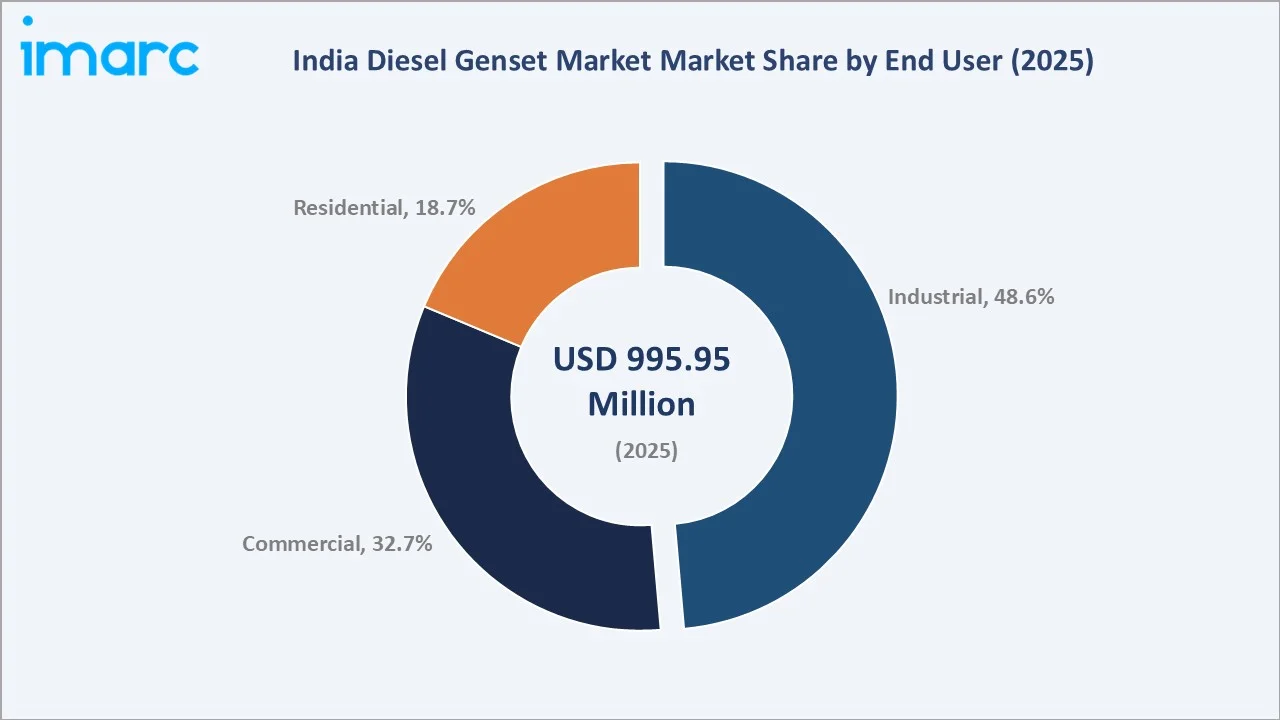

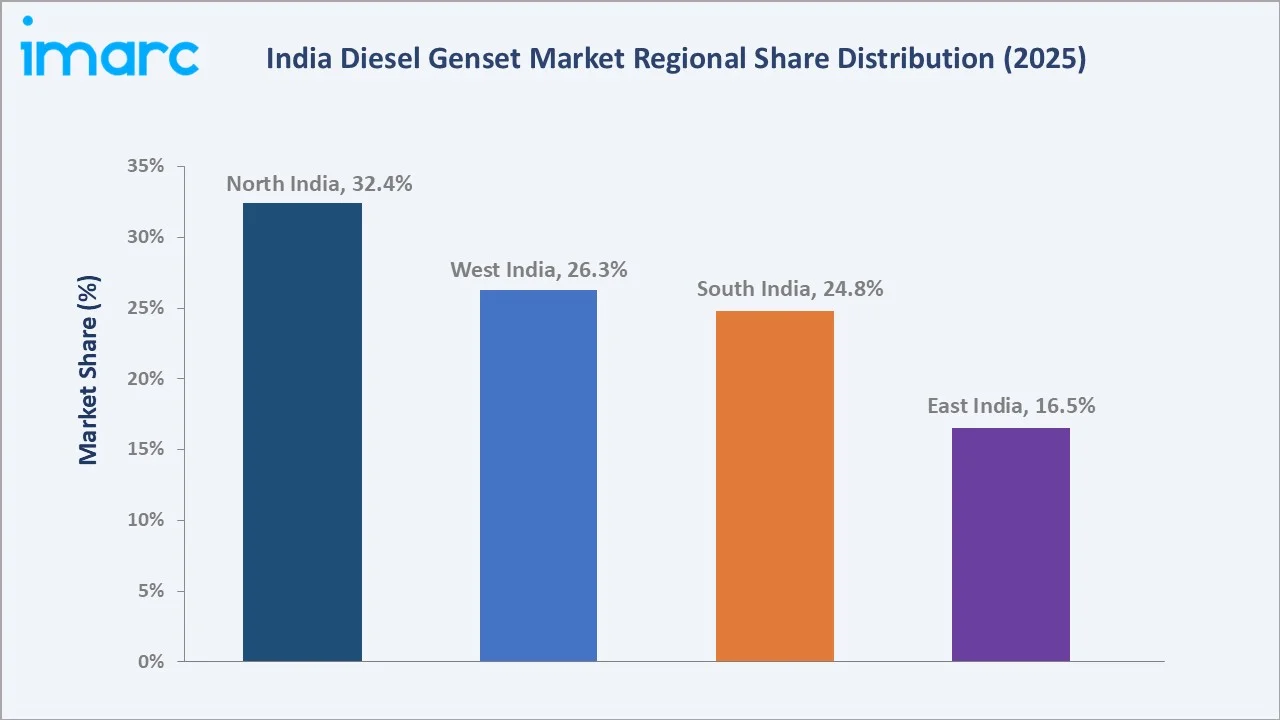

The India diesel genset market size reached USD 995.95 Million in 2025 and is projected to reach USD 1,974.42 Million by 2034, exhibiting a CAGR of 7.03% during 2026-2034. Growing power demand driven by rapid urbanization, industrial expansion, and rural electrification gaps is the primary catalyst. Standby applications dominate at 44.2% share in 2025, while the industrial end-user segment leads at 48.6%. North India accounts for 32.4% of national revenue in 2025, the largest regional contributor. Persistent grid reliability deficits, CPCB IV+ emission compliance mandates, and rising data-centre backup requirements are further shaping the market trajectory.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 995.95 Million |

|

Forecast Market Size (2034) |

USD 1,974.42 Million |

|

CAGR (2026-2034) |

7.03% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

North India (32.4% share, 2025) |

|

Fastest Growing Region |

East India (high rural electrification growth) |

|

Leading Application |

Standby (44.2%, 2025) |

|

Leading End User |

Industrial (48.6%, 2025) |

To get more information on this market, Request Sample

Executive Summary

The India diesel genset market is experiencing sustained growth, propelled by the country's expanding power infrastructure and persistent reliability gaps in grid supply. Valued at USD 995.95 Million in 2025, the market is forecast to reach USD 1,974.42 Million by 2034 at a CAGR of 7.03%. India's installed power capacity stood at 454.45 GW as of October 2024, according to the India Brand Equity Foundation (IBEF). Despite this, an estimated 85% of households in smaller cities experience 2 to 4 hours of daily power outages, sustaining indispensable demand for diesel gensets across all end-user categories.

Standby applications command the largest segment at 44.2% in 2025, serving hospitals, data centres, telecom towers, and commercial establishments requiring uninterrupted power backup. Industrial end users lead at 48.6%, encompassing manufacturing plants, warehouses, and construction sites. Prime Power applications at 26.8% serve off-grid and remote areas.

North India holds the dominant regional share at 32.4% in 2025, driven by high industrial activity in Uttar Pradesh, Punjab, and Haryana. West India follows at 26.3%, led by Maharashtra and Gujarat's large manufacturing and commercial base. Key competitors including Cummins India Ltd., Kirloskar Oil Engines Ltd., and Mahindra Powerol collectively command approximately 55%-60% of the organized market in 2024. The market outlook through 2034 remains robust, supported by India's USD 1.4 trillion National Infrastructure Pipeline (NIP) and continued data centre investment momentum.

Key Market Insights

|

Insight |

Data |

|

Largest Application Segment |

Standby – 44.2% share (2025) |

|

Second Application Segment |

Prime Power – 26.8% share (2025) |

|

Leading End-User Segment |

Industrial – 48.6% revenue share (2025) |

|

Leading Region |

North India – 32.4% revenue share (2025) |

|

Top Companies |

Cummins India, Kirloskar KOEL, Mahindra Powerol, Caterpillar, Ashok Leyland |

|

Market Opportunity |

Data centre backup, rural electrification, EPC project site power |

Key Analytical Observations Supporting the Above Data:

- Standby segment dominance at 44.2% in 2025 reflects India's ongoing grid reliability deficit, with hospitals, telecom towers, and commercial establishments maintaining constant backup investment.

- Industrial end users at 48.6% lead all categories; manufacturing plants and construction sites view diesel gensets as essential operational infrastructure, with Cummins reporting 30.8% revenue growth in Q2 FY25 driven by data-centre orders alone.

- Prime Power applications at 26.8% in 2025 serve off-grid rural businesses and telecom repeater sites, where grid connectivity remains unreliable across Bihar, Jharkhand, and Rajasthan.

- North India's 32.4% revenue share is underpinned by high industrial density in the NCR-Noida-Gurgaon corridor and large-scale construction activity under PMGSY and AMRUT 2.0 urban development programmes.

- East India at 16.5% represents the fastest-growing regional pocket, driven by rising infrastructure investment in Odisha, Jharkhand, and West Bengal under the government's eastern economic corridor strategy.

India Diesel Genset Market Overview

Diesel generator sets (gensets) are self-contained power generation units combining a diesel internal combustion engine with an alternator to produce electrical energy. They serve four core functions: standby backup (emergency power upon grid failure), prime power (sole power source in off-grid locations), continuous operation (base-load generation at near full capacity), and peak shaving (supplementing grid supply during peak-demand periods). Units range from sub-5 kVA portable sets to 2,500 kVA+ industrial-scale clusters. Applications span residential housing societies, commercial complexes, industrial manufacturing, telecom tower networks, healthcare facilities, data centres, construction sites, and government infrastructure projects. Macro-economic drivers include India's USD 1.4 trillion National Infrastructure Pipeline (NIP), rapid urbanization with India projected to house 600 million urban residents by 2030, and significant power consumption growth across the manufacturing and digital services sectors.

Market Dynamics

To evaluate market opportunities, Request Sample

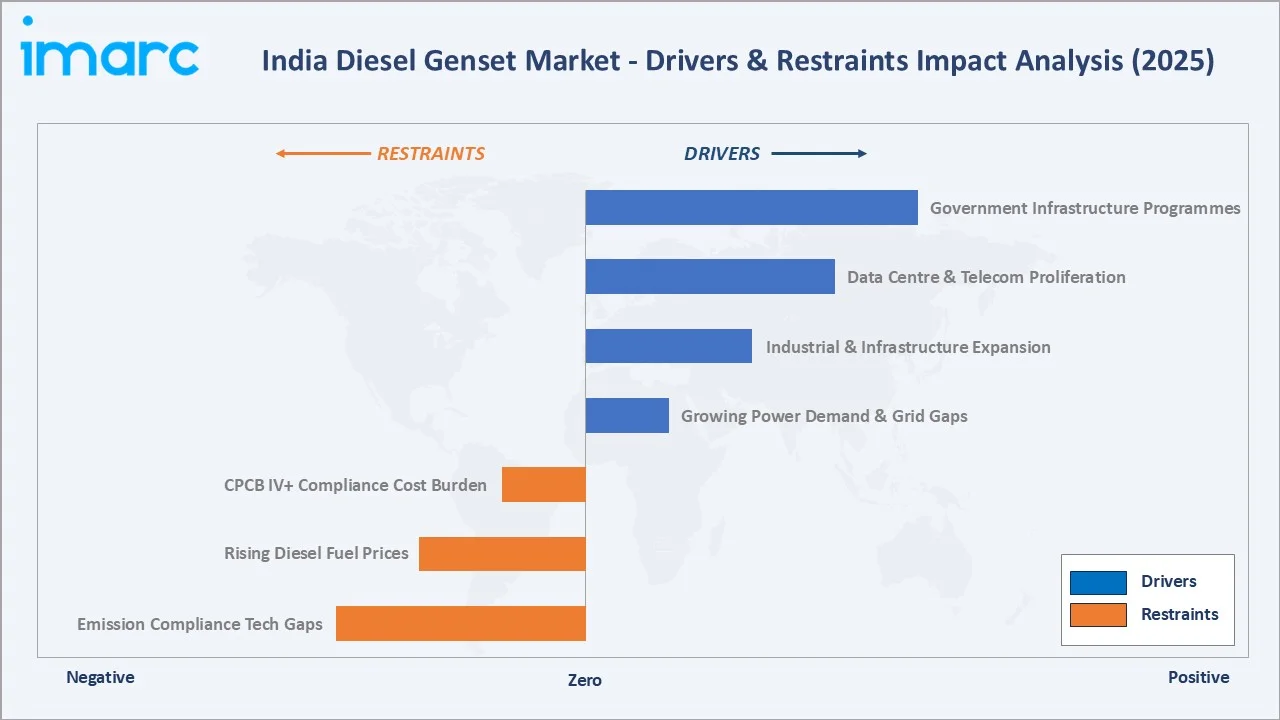

Market Drivers

- Growing Power Demand and Grid Reliability Gaps: India's power grid, despite an installed capacity of 454.45 GW as of October 2024, continues to face localized outages. Studies indicate that 85% of households in smaller cities still suffer 2 to 4 hours of daily outages, making diesel gensets indispensable backup infrastructure. India's electricity consumption is expected to grow at 6%-7% annually through 2030, directly proportional to genset demand growth.

- Industrial and Infrastructure Expansion: Manufacturing sector growth under the Production-Linked Incentive (PLI) scheme, with Rs. 1.97 trillion disbursed through 2024, is generating sustained industrial power backup demand. EPC project site requirements, metro rail construction, and highway expansion are creating large-scale prime-power genset demand clusters across the country.

- Data Centre and Telecom Tower Proliferation: India's data center capacity will grow fivefold by 2030 to over 8GW. Each 1 MW of IT load requires approximately 1.5 MW of standby diesel backup. Telecom tower count reached 800,000+ active towers in 2024, most requiring reliable genset backup, representing a structural long-term demand anchor.

- Government Infrastructure Programmes: The National Infrastructure Pipeline (NIP) covering over 9,000 projects worth USD 1.4 trillion through 2025 and beyond is generating sustained project-site genset demand. Hospital construction under Ayushman Bharat and school development under PM Poshan are increasing institutional standby demand.

Market Restraints

- CPCB IV+ Compliance Cost Burden: The Central Pollution Control Board's CPCB IV+ emission norms mandate SCR and DPF technology integration, significantly raising manufacturing costs. Smaller genset manufacturers face disproportionate R&D and compliance investment burdens, with product prices increasing 12%-18% post-compliance relative to CPCB II-era products.

- Rising Diesel Fuel Prices: Diesel retail prices in India reached Rs. 89-92 per litre across major cities in 2024-2025, increasing the total cost of ownership (TCO) for genset operators. Higher fuel costs are accelerating the evaluation of hybrid and gas-based alternatives, particularly among commercial and large industrial users with ESG commitments.

Market Opportunities

- Data Centre Backup Power Demand: The India's data centre industry is poised for explosive growth, with capacity projected to surge 77% by 2027, reaching a staggering 1.8 GW, creates a multi-year, high value genset procurement pipeline. Hyperscale data centres require multi-megawatt N+1 redundant genset clusters, representing the highest average order value in the market.

- Hybrid Genset and IoT Integration: The launch of hybrid gensets combining diesel engines with battery energy storage systems (BESS) addresses both fuel economy and emission concerns. Manufacturers integrating IoT-enabled remote monitoring, predictive maintenance, and cloud-connected dashboards can command 15%-22% premium pricing over conventional units.

- Rural Electrification Gaps and Off-Grid Markets: India's rural electrification under Saubhagya may have achieved household connection but grid quality remains poor. Off-grid small businesses, cold-chain operators, and agri-processing units in Uttar Pradesh, Bihar, and Odisha represent an under-penetrated prime-power genset market.

Market Challenges

- Emission Compliance Technology Gaps for SMEs: Small and medium genset manufacturers lack the R&D capability to independently develop CPCB IV+ compliant engine solutions. Dependence on engine supplier partnerships (Cummins, Perkins, KOEL) creates supply concentration risk and margin pressure for assemblers.

- Skilled Installation and Service Network Gaps: The rapid shift to electronically controlled, emission-compliant engines requires upskilled service technicians. Organized service network coverage remains concentrated in Tier-1 and Tier-2 cities, leaving rural customers with inadequate after-sales support, increasing total lifecycle costs.

Emerging Market Trends

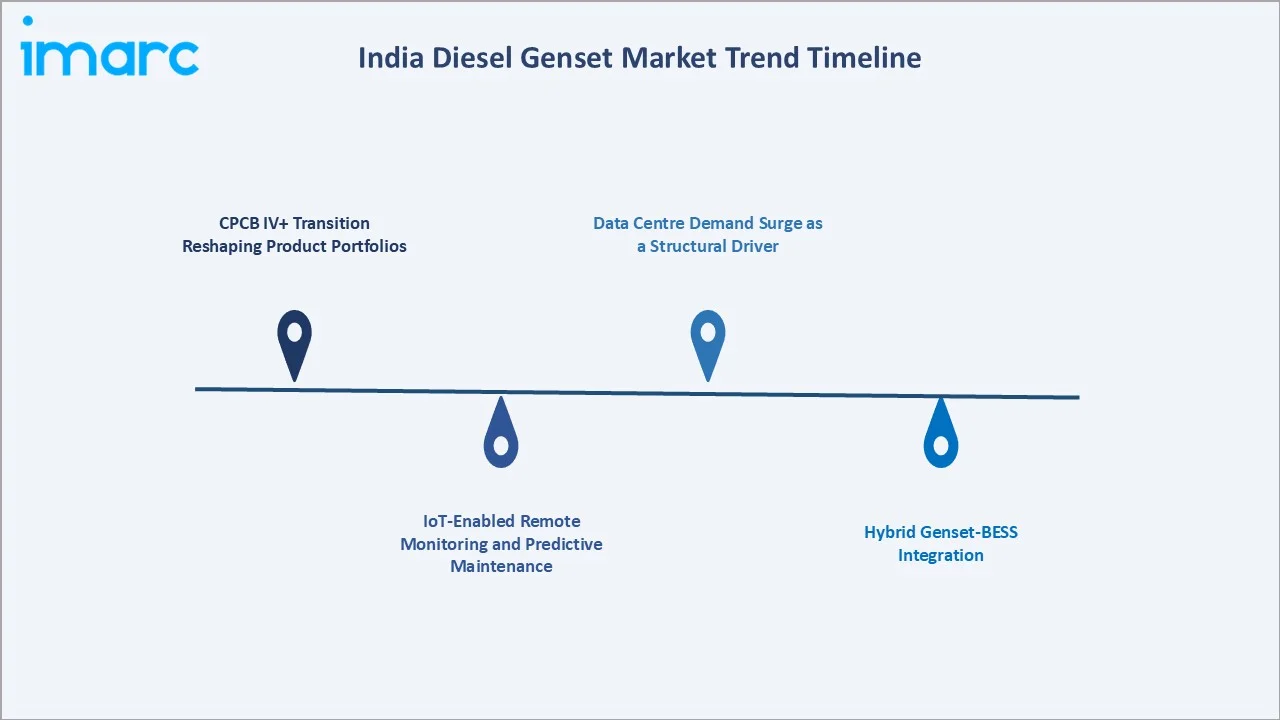

1. CPCB IV+ Transition Reshaping Product Portfolios

The shift to CPCB IV+ emission norms is the most structurally significant regulatory transition in the India diesel genset market's recent history. Manufacturers including Greaves Cotton, Cummins India, and Ashok Leyland launched fully compliant product ranges in 2024, with five-year warranties and 450-point service networks.

2. IoT-Enabled Remote Monitoring and Predictive Maintenance

Kirloskar Oil Engines has integrated cloud dashboards and IoT monitoring into premium genset lines, enabling real-time fuel consumption tracking, load analytics, and predictive maintenance alerts. Cummins India's PowerCommand platform provides remote diagnostics for data-centre clients, reducing unplanned downtime by up to 35% in controlled deployments.

3. Hybrid Genset-BESS Integration

Leading OEMs are developing hybrid configurations combining diesel gensets with lithium-ion battery energy storage systems (BESS). These hybrid systems reduce diesel runtime by 30%-50% in partial-load applications, cutting fuel costs and emissions. Mahindra Powerol and Cummins have announced roadmaps for hybrid commercial availability by 2026-2027.

4. Data Centre Demand Surge as a Structural Driver

India's hyperscale data centre expansion is creating multi-year high-value genset procurement pipelines. Cummins India reported more than 35% revenue growth in Q2 FY25, primarily driven by data centre standby orders of 500-800 kVA units with black-start capability. Each 1 MW of IT load requires approximately 1.5 MW of synchronised standby diesel capacity.

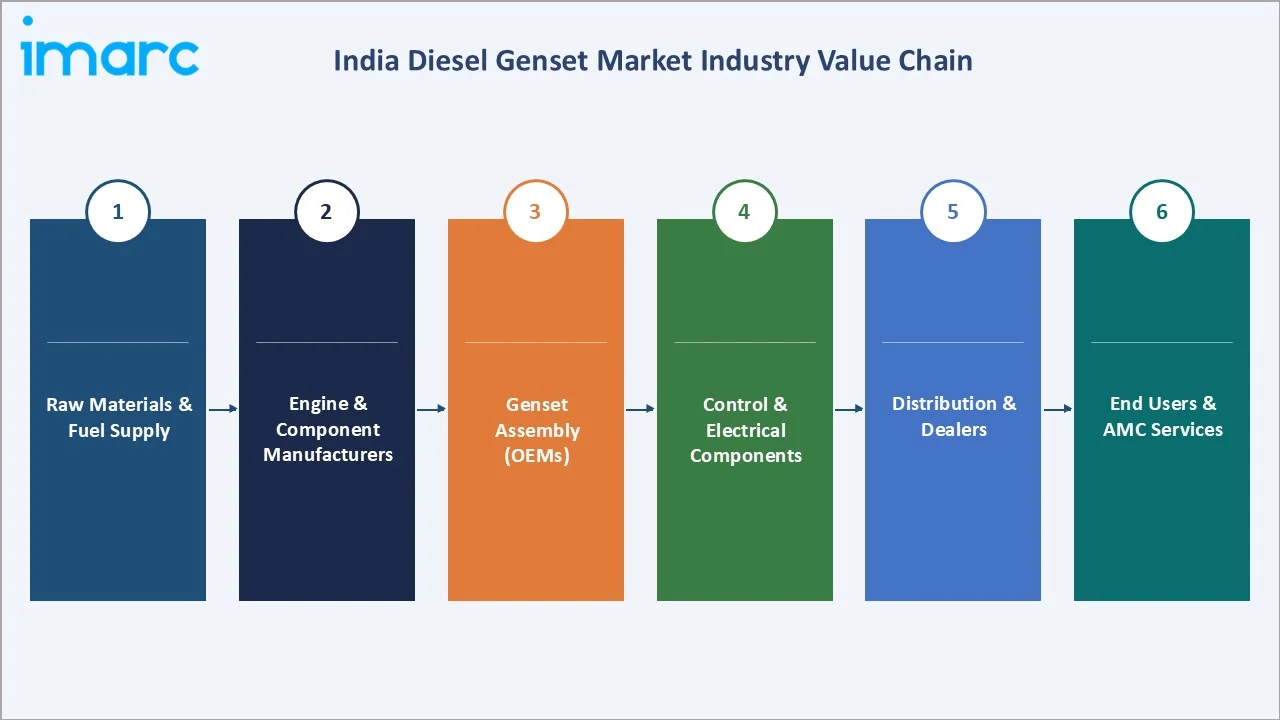

Industry Value Chain Analysis

The India diesel genset value chain spans six integrated stages from raw material procurement through end-user service delivery. Each stage presents distinct competitive dynamics and margin profiles.

|

Stage |

Key Players / Examples |

|

Raw Materials & Fuel Supply |

Steel producers (SAIL, Tata Steel), copper suppliers, HPCL/BPCL diesel distribution networks |

|

Engine & Component Manufacturers |

Cummins India, Kirloskar Oil Engines (KOEL), Greaves Cotton, Perkins (Caterpillar), AVTEC |

|

Genset Assembly (OEMs) |

Mahindra Powerol, Ashok Leyland (LEYPOWER), Jakson Group, Sudhir Power, Powerica Ltd. |

|

Control & Electrical Components |

Deif, DSE (Deep Sea Electronics), ComAp, ABB India, Schneider Electric India |

|

Distribution & Dealers |

Authorized dealer networks, Rental fleet operators (Aggreko, GMMCO), B2B direct sales |

|

End Users & AMC Services |

Industrial plants, commercial complexes, telecom operators, hospitals, data centres, construction |

Engine and component manufacturers occupy the highest strategic value position in the value chain, as OEMs and assemblers depend on engine suppliers for CPCB IV+ compliant powertrains. KOEL, Cummins India, and Greaves Cotton supply engines across the full kVA range, creating upstream concentration risk for assemblers that lack in-house engine development capabilities.

Technology Landscape in the India Diesel Genset Industry

Engine Technology – CPCB IV+ Compliance Architecture

Modern CPCB IV+ compliant engines integrate selective catalytic reduction (SCR), diesel oxidation catalysts (DOC), and diesel particulate filters (DPF) to meet stringent NOx and PM emission limits. Cummins India's QSB6.7 and QSK23 engines, Kirloskar's R550 series, and Greaves Cotton's 3-5 litre engines represent the current CPCB IV+ generation, offering 15%-25% better fuel efficiency than previous-generation CPCB II counterparts.

Digital Control and Remote Monitoring Technology

Electronic engine management systems (EMS) and advanced generator control units (GCU) from DSE, Deif, and ComAp enable sophisticated automatic start-stop, load sharing, and paralleling functions. Kirloskar's cloud-based monitoring platform and Cummins' PowerCommand digital suite allow real-time remote diagnostics, fuel consumption optimization, and predictive fault detection across distributed genset fleets.

Hybrid Genset-BESS Architecture

Hybrid configurations pair diesel gensets with lithium-ion BESS to optimize duty cycles. In light-load scenarios (below 40% rated load), diesel engines operate inefficiently. Hybrid systems dispatch battery power during light-load periods and engage the diesel engine for heavier loads, reducing fuel consumption by 30%-50% and extending engine life. Cummins and Mahindra Powerol have commercialized sub-250 kVA hybrid configurations, with larger models planned for 2026-2028.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Power Output |

🔒 |

🔒 |

2025 |

|

Power Rating |

🔒 |

🔒 |

2025 |

|

Application |

Standby |

44.2% |

2025 |

|

End User |

Industrial |

48.6% |

2025 |

|

Region |

North India |

32.4% |

2025 |

By Application

To access detailed market analysis, Request Sample

Standby application commands a 44.2% majority share in 2025, reflecting India's persistent grid unreliability affecting commercial, institutional, and industrial users. The standby segment benefits from near-universal adoption among hospitals, data centres, retail chains, hotels, and urban residential complexes, all of which maintain dedicated backup gensets as non-negotiable operational infrastructure.

Prime Power applications account for 26.8% in 2025, driven by off-grid industrial sites, mining operations, and rural agri-processing facilities where diesel gensets serve as the primary source of electrical power. Continuous power applications at 18.3% represent base-load generation in remote industrial and telecom network contexts. Peak Shaving at 10.7% is a growing niche, particularly among large electricity consumers utilizing gensets to reduce grid demand charges during tariff peak periods.

By End User

Industrial end users lead with a 48.6% revenue share in 2025, encompassing manufacturing plants, warehouses, fabrication lines, construction sites, and mining operations that cannot sustain unscheduled power interruptions. Process-critical industries including pharmaceuticals, food processing, and automotive manufacturing typically maintain N+1 redundancy, increasing average installed capacity per site.

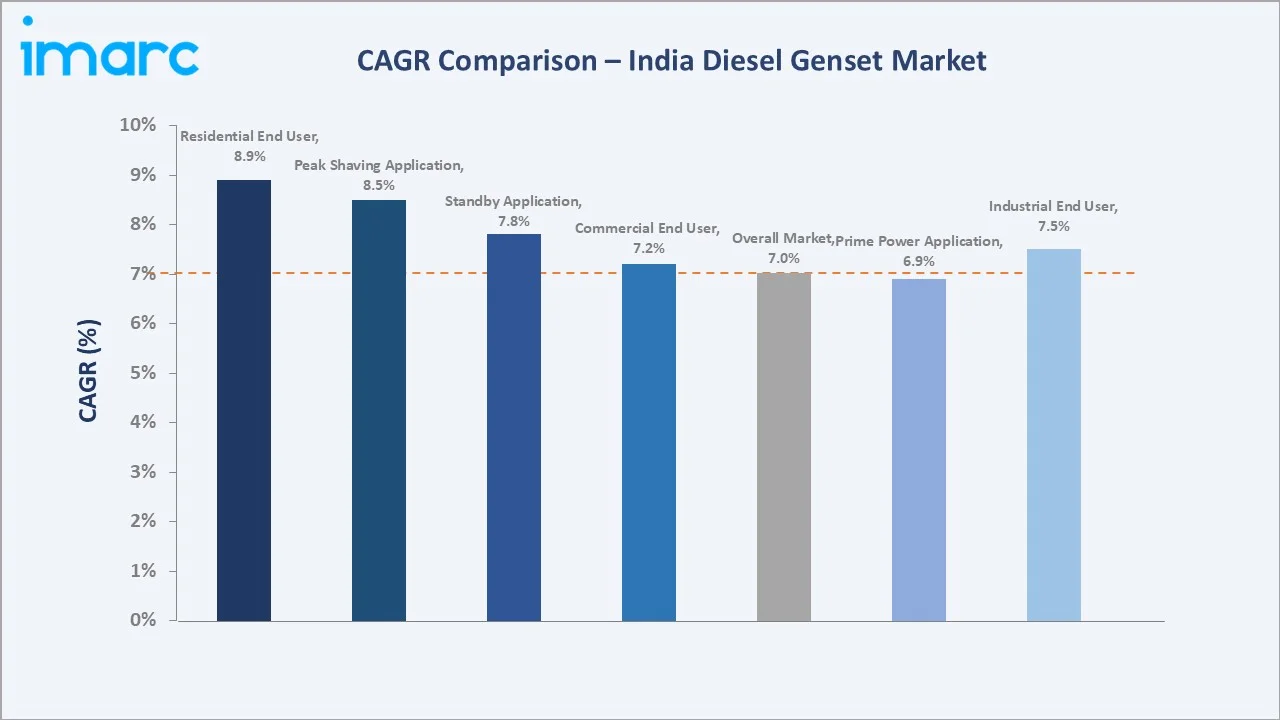

Commercial end users hold a 32.7% share in 2025, anchored by the hospitality sector, retail chains, diagnostic labs, cold-chain logistics, and educational institutions that have upgraded to CPCB IV+ models with comprehensive AMC contracts. Residential end users, at 18.7% in 2025, are rising fastest with an estimated 8.98% CAGR through 2031, driven by gated community backup requirements for elevators, water pumps, and common-area power in Tier-2 cities.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

Major Demand Centres |

|

North India |

32.4% |

NCR industrial corridor, UP/Punjab agri-industries, infrastructure projects, data centres |

Delhi-NCR, Noida, Gurugram, Ludhiana, Kanpur |

|

West India |

26.3% |

Maharashtra manufacturing, Gujarat chemical & pharma, Mumbai commercial & hospitality |

Mumbai, Pune, Ahmedabad, Surat, Vadodara |

|

South India |

24.8% |

TN automotive, Bengaluru IT data centres, Hyderabad pharma, Kerala tourism |

Bengaluru, Chennai, Hyderabad, Kochi |

|

East India |

16.5% |

Mining & steel sector, rural electrification, Kolkata commercial, infrastructure investment |

Kolkata, Bhubaneswar, Raipur, Ranchi |

North India commands a 32.4% share in 2025, the largest regional contribution to India's diesel genset market. The NCR-Noida-Gurugram industrial and commercial corridor, home to over thousands of registered industrial units and India's largest data centre cluster, anchors genset demand at both the standby and prime-power tiers.

West India at 26.3% is driven by Maharashtra's manufacturing and commercial base, Gujarat's export-oriented chemical and pharmaceutical clusters, and Mumbai's high-density commercial and hospitality demand. South India at 24.8% is shaped by Bengaluru's IT data centre expansion, Chennai's automotive corridor, and Hyderabad's rapidly growing pharma and IT infrastructure. East India at 16.5% is the fastest-emerging region, supported by Odisha and Jharkhand's mining and steel industry growth and increasing government infrastructure investment.

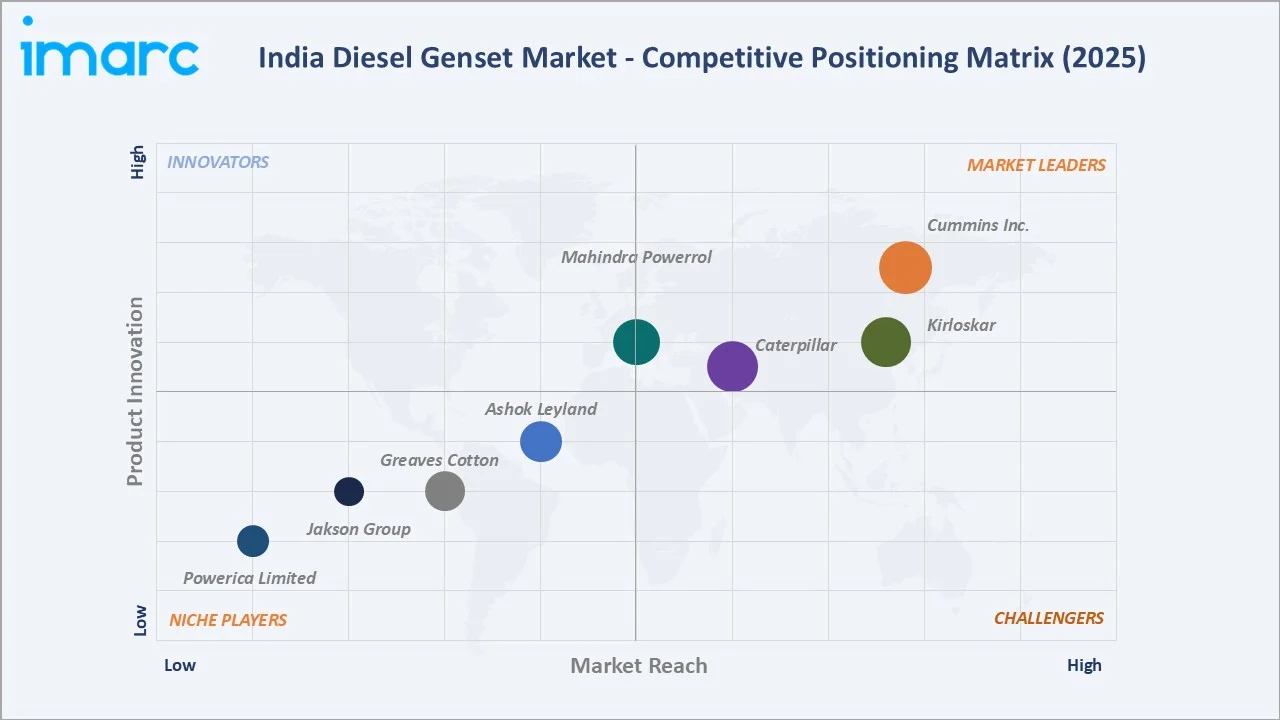

Competitive Landscape

|

Company Name |

Key Brand |

Market Position |

Core Strength |

|

Cummins Inc. |

Cummins / PowerCommand |

Leader |

Full kVA range, CPCB IV+ leader, data-centre specialisation, service network |

|

Kirloskar Proprietary Limited |

Kirloskar Green / Kirloskar Portable & Stationary |

Leader |

Widest domestic product range, 4 mfg. plants, strong rural penetration |

|

Mahindra Powerol |

Mahindra Powerol |

Leader |

Telecom tower specialisation, IoT monitoring, hybrid genset roadmap |

|

Caterpillar |

CAT / Perkins |

Leader |

Large kVA industrial range, global service, premium segment positioning |

|

Ashok Leyland |

LEYPOWER |

Challenger |

Automotive brand leverage, 30 models, SAATHI predictive maintenance platform |

|

Greaves Cotton Limited |

Greaves Power |

Challenger |

SCR/DPF certified CPCB IV+ range, 450-point service network, 5-year warranty |

|

Jakson |

Jakson Power |

Emerging |

EPC project focus, turnkey power solutions, solar-hybrid integration |

|

Powerica Limited |

Powerica Gensets |

Emerging |

Rental fleet operator, diverse kVA range, strong South India presence |

The India diesel genset competitive landscape is moderately concentrated at the organized-sector tier, with Cummins India, Kirloskar KOEL, Caterpillar, Mahindra Powerol, and Greaves Cotton collectively commanding approximately 55%-60% of organized market revenue in 2024. The market also features a significant unorganized sector of small regional assemblers, particularly for sub-75 kVA units serving residential and small commercial applications.

Key Company Profiles

Cummins Inc.

Cummins India is the market-leading diesel genset engine supplier and OEM in India, a subsidiary of Cummins Inc. (USA) with manufacturing operations in Pune, Maharashtra. The company offers gensets across 5 kVA to 3,750 kVA, serving residential, commercial, industrial, and data-centre segments. Cummins holds the strongest position in the premium and large kVA segments.

- Product Portfolio: QSB, QSL, QSM, QST, QSK engine series; PowerCommand control systems; OptiNAS+ filtration; GenVT variable-speed generator technology.

- Recent Developments: In July 2024, Cummins India introduced CPCB IV+ compliant gensets up to 800 kVA with OptiNAS+ filtration, reporting more than 30% revenue growth in Q2 FY25 driven by data-centre demand.

- Strategic Focus: Premium large kVA data-centre and industrial market leadership; digital monitoring platform expansion (PowerCommand); CPCB IV+ compliance across the full product range; fuel-agnostic engine roadmap for HVO and dual-fuel adaptations.

Kirloskar

Kirloskar Oil Engines is the flagship company of the 130-year-old Kirloskar Group and one of India's largest genset manufacturers, operating four state-of-the-art manufacturing facilities in India with a 13-node national office network and a comprehensive authorized dealer ecosystem.

- Product Portfolio: Kirloskar Green gensets, iGreen Version 2.0 (R550 series), portable and stationary sets across 5 kVA to 3,000 kVA; cloud monitoring dashboards; KOEL CARE AMC services.

- Recent Developments: KOEL launched the iGreen Version 2.0 powered by the R550 engine series in 2022 delivering improved fuel economy and power output. The cloud dashboard integration enables real-time fleet monitoring for commercial and industrial customers, reducing unplanned downtime for high-value accounts.

- Strategic Focus: Broadest domestic kVA coverage; fuel-agnostic engine development; IoT-integrated product lines; strengthening rural dealer network penetration; AMC and after-sales revenue expansion.

Mahindra Powerol

Mahindra Powerol is a business unit of Mahindra & Mahindra Ltd., specializing in gensets and power products. The company holds a strong position in the telecom tower backup segment and is expanding into the commercial and industrial sectors with IoT-enabled and hybrid genset offerings.

- Product Portfolio: Powerol diesel gensets (5 kVA to 2,000 kVA), Powerol telecom tower sets, hybrid genset-BESS configurations, tri-energy (diesel/gas/solar) hybrid solutions.

- Recent Developments: Mahindra Powerol has announced a commercial roadmap for hybrid genset-battery configurations through 2026-2027, targeting commercial and telecom applications. The company has also expanded its digital monitoring service offering for fleet operators.

- Strategic Focus: Telecom tower segment leadership; hybrid genset-BESS commercialization; Mahindra Group synergies in EV and energy storage; rural and semi-urban market penetration through Mahindra's agricultural dealer network.

Market Concentration Analysis

The India diesel genset market exhibits moderate concentration at the organized sector level, with the top five players (Cummins India, Kirloskar KOEL, Caterpillar, Mahindra Powerol, and Greaves Cotton) collectively commanding approximately 55%-60% of organized market revenue in 2024. This represents a highly consolidated organized tier operating alongside a fragmented unorganized sector.

The market features a clear bifurcation. In the premium and large kVA segment (above 250 kVA), the market is highly concentrated, with Cummins, Caterpillar, and KOEL commanding over 75% of revenue. Entry barriers include CPCB IV+ engine development capability, ISO certification, specialized service infrastructure, and OEM relationships with control system suppliers. In the sub-75 kVA segment, over 200 small regional assemblers compete on price, leveraging imported or locally sourced engines, creating a highly fragmented competitive environment with limited brand differentiation.

Consolidation is occurring at the mid-market tier (75 kVA to 500 kVA), where CPCB IV+ compliance costs are exceeding the R&D capabilities of smaller assemblers. Greaves Cotton's five-year warranty and 450-point service network, and Cummins' PowerCommand digital platform, are raising the effective entry barriers and accelerating market share concentration among the top organized players.

Investment & Growth Opportunities

Fastest-Growing Segments

Residential end users represent the fastest-growing segment at an estimated 8.98% CAGR through 2031, driven by middle-class housing society backup requirements and the expansion of gated communities in Tier-2 and Tier-3 cities. Standby backup demand from data centres is the highest average-order-value growth opportunity.

Emerging Market Expansion

East India represents the highest-potential regional growth market, with government infrastructure investment in Odisha, Jharkhand, and West Bengal accelerating at a 10%+ annual rate. Rural off-grid prime-power applications across Uttar Pradesh, Bihar, and Rajasthan remain structurally under-penetrated.

Venture and Strategic Investment Trends

Hybrid genset-BESS integration technology is attracting investment from both genset manufacturers (Cummins, Mahindra) and energy storage specialists. IoT platform development for genset fleet monitoring is attracting venture capital, with start-ups offering SaaS-based monitoring and predictive maintenance analytics targeting the large unorganized fleet market.

Future Market Outlook (2026-2034)

The India diesel genset market forecast projects sustained value expansion from USD 995.95 Million in 2025 to USD 1,974.42 Million by 2034 at a CAGR of 7.03%, representing a near-doubling of market value over the forecast period.

By 2034, rapid data centre expansion from ~950 MW in 2024 to over 1,800 MW by 2028 will drive sustained demand for high-value standby gensets, with ~1.5 MW of diesel backup needed per MW of IT load. Simultaneously, the shift toward hybrid genset-BESS systems will reduce diesel consumption per kWh, reshaping market economics toward efficiency, optimization, and digital service-led value creation.

The India diesel genset market is expected to have undergone significant premium segmentation evolution. Large kVA markets (above 250 kVA) will be dominated by full-package digital cockpit systems offering IoT monitoring, remote diagnostics, and predictive maintenance as standard features.

Research Methodology

Primary Research

Structured interviews (2024–2025) with Tier-1 OEM product managers, procurement heads, dealers, rental operators, and regulatory officials informed the study. These insights validated market sizing, segmentation, CPCB IV+ timelines, and competitive positioning across regions.

Secondary Research

Data was sourced from IBEF, CEA, CPCB, Ministry of Power, IEEMA, company reports, and key industry publications. These sources supported analysis of capacity trends, regulations, manufacturing activity, and trade dynamics.

Forecasting Models

Market estimates used top-down and bottom-up models aligned with GDP growth, capex trends, IIP, and urbanization. Segment splits were refined using dealer data, shipment volumes, and import statistics for key components.

India Diesel Genset Market Report Coverage:

|

Attribute |

Details |

|

Market Size (Base Year 2025) |

USD 995.95 Million |

|

Forecast Market Size (2034) |

USD 1,974.42 Million |

|

CAGR |

7.03% (2026-2034) |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Segmentation (Application) |

Standby, Prime Power, Continuous, Peak Shaving |

|

Segmentation (End User) |

Industrial, Commercial, Residential |

|

Segmentation (Power Rating) |

5 kVA-75 kVA, 76 kVA-375 kVA, 376 kVA-750 kVA, Above 750 kVA |

|

Segmentation (Power Output) |

Portable Generators, Inverter Generators, Industrial Generators, Induction Generators |

|

Regional Coverage |

North India, West India, South India, East India |

|

Company Profiles |

Cummins Inc., Kirloskar Proprietary Limited, Mahindra Powerol, Caterpillar, Ashok Leyland, Greaves Cotton Limited, Jakson, Powerica Limited, etc. |

|

Deliverable Format |

PDF + Excel |

|

Customization Available |

Yes – up to 10% customization; 10-12 weeks post-purchase support |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the India diesel genset market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the India diesel genset market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the India diesel genset industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the India Diesel Genset Market Report

The India diesel genset market size reached USD 995.95 Million in 2025, driven by persistent grid reliability gaps, industrial expansion, and data-centre backup demand.

The market is projected to reach USD 1,974.42 Million by 2034, growing at a CAGR of 7.03% during 2026-2034, supported by infrastructure investment and digital economy expansion.

Standby applications lead with a 44.2% share in 2025, driven by hospitals, data centres, commercial complexes, and telecom towers requiring reliable emergency backup power.

Industrial end users dominate at 48.6% in 2025, encompassing manufacturing plants, warehouses, construction sites, and mining operations requiring continuous backup power reliability.

North India commands a 32.4% revenue share in 2025, driven by the NCR industrial corridor, Uttar Pradesh infrastructure projects, and significant data-centre investments in Noida and Gurugram.

Key drivers include grid reliability deficits affecting 85% of smaller city households, India's USD 1.4 trillion National Infrastructure Pipeline, data-centre expansion, and industrial PLI scheme-driven manufacturing growth.

Leading companies include Cummins Inc., Kirloskar Proprietary Limited, Mahindra Powerol, Caterpillar, Ashok Leyland, Greaves Cotton Limited, Jakson, and Powerica Limited collectively holding 55%-60% of organized revenue.

Residential end users represent the fastest-growing segment, estimated at ~8.98% CAGR through 2031, driven by middle-class housing society backup requirements across Tier-2 and Tier-3 Indian cities.

Data centres are a key structural demand anchor, with India's capacity projected to grow from 950 MW (2024) to 1,800+ MW by 2028. Each 1 MW of IT load requires approximately 1.5 MW of standby diesel backup capacity.

Key trends include hybrid genset-BESS integration, IoT-enabled fleet monitoring, biodiesel and HVO fuel compatibility, and the rapid adoption of CPCB IV+ compliant engines with SCR/DPF after-treatment systems.

High-opportunity areas include large-kVA data-centre backup systems, hybrid genset technology, IoT monitoring SaaS platforms, rental fleet expansion, and prime-power solutions for under-electrified rural markets in East India.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)