India Digital Health Market Size, Share, Trends and Forecast by Type, Component, and Region, 2026-2034

India Digital Health Market Summary:

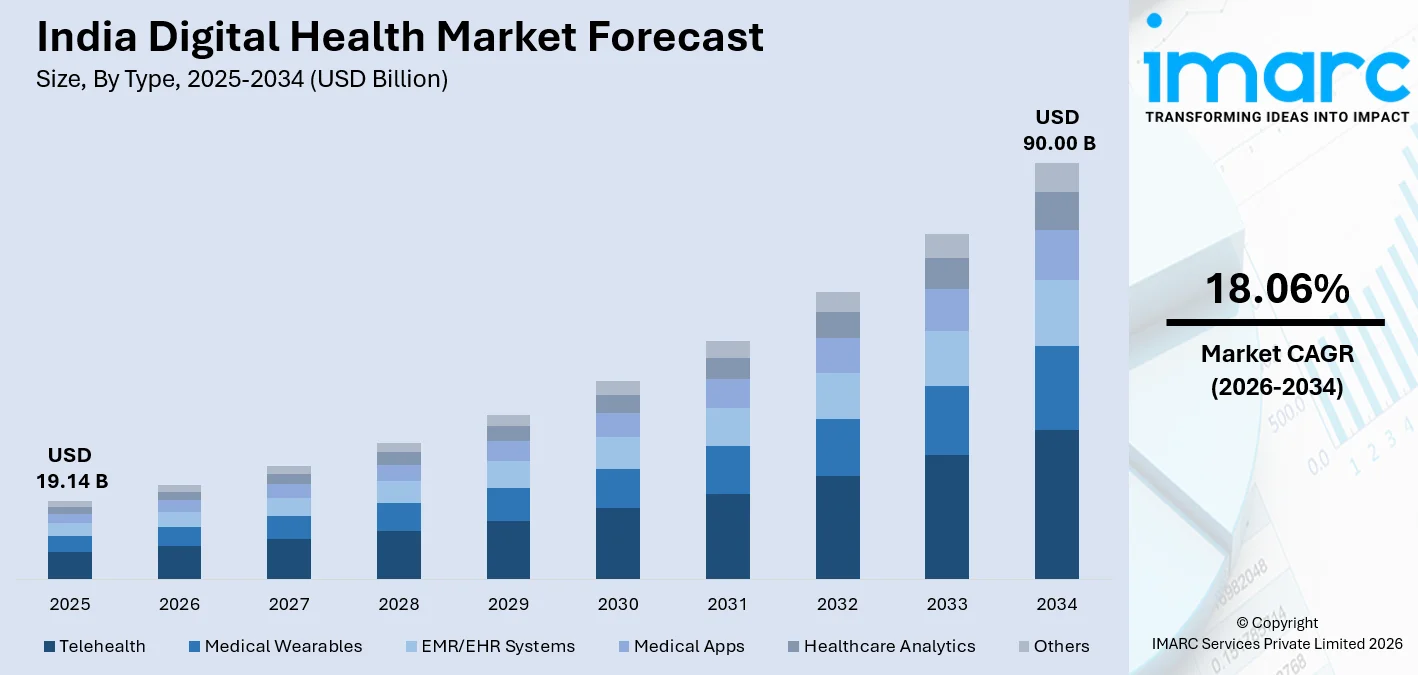

The India digital health market size was valued at USD 19.14 Billion in 2025 and is projected to reach USD 90.00 Billion by 2034, growing at a compound annual growth rate of 18.06% from 2026-2034.

The India digital health market is growing at a fast pace, given the rise in digital connectivity, favorable government initiatives, and the changing needs of patients, all of which are contributing to the growth of the digital health market in the country. The increased need for remote health solutions, integrated health services, and artificial intelligence-based diagnostics tools is strengthening the India digital health market. Increasing access to mobile health services and the need for preventive and chronic care are also contributing to the growth of the India digital health market share.

Key Takeaways and Insights:

- By Type: Telehealth dominates the market with a share of 36.2% in 2025, driven by its ability to bridge geographical gaps and deliver accessible remote consultations to patients across urban and rural settings.

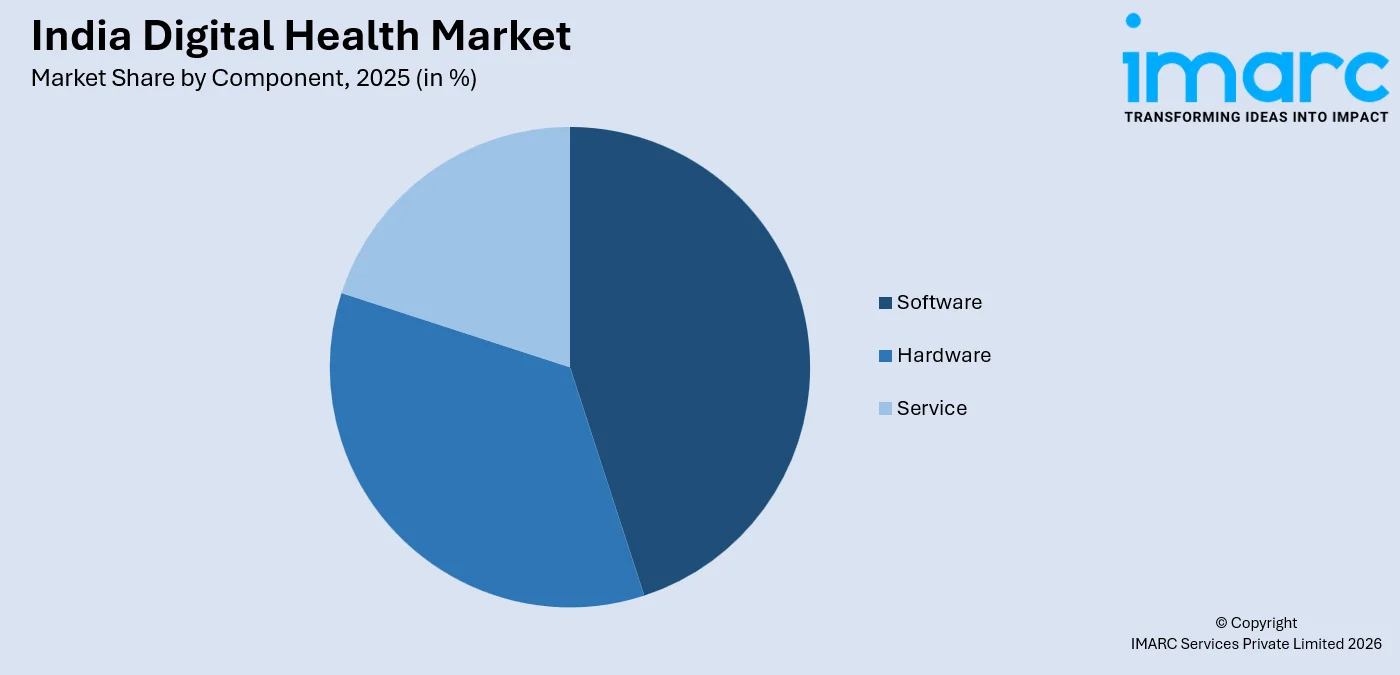

- By Component: Software represents the largest segment with a market share of 42.8% in 2025, underpinned by its scalability, interoperability, and integral role in powering electronic health records, analytics platforms, and telehealth applications.

- By Region: South India leads the market with a share of 33.5% in 2025, reflecting its strong digital infrastructure, proactive healthcare policies, and high concentration of technology-driven health service providers.

- Key Players: The India digital health market features a competitive mix of domestic startups and established healthcare technology providers focusing on expanding telehealth platforms, AI-driven diagnostics, mobile health applications, and integrated health record systems.

To get more information on this market Request Sample

The India digital health market is undergoing a rapid and structural transformation driven by the convergence of advancing technology, progressive government policy, and evolving consumer expectations. The country’s vast and digitally connected population is increasingly turning to technology-enabled healthcare solutions for convenience, affordability, and accessibility. The integration of artificial intelligence, cloud computing, and Internet of Things-enabled devices is redefining how healthcare is accessed, monitored, and delivered. Notably, in 2026, the National Health Authority launched the eSushrut@Clinic platform, a government-backed digital solution designed to help small and mid-sized clinics adopt digital health tools and integrate with the Ayushman Bharat Digital Mission ecosystem, improving clinical decision-making and expanding digital access across India’s fragmented healthcare network. Government-backed digital health missions are creating a robust foundational infrastructure, encouraging interoperability and standardization across the ecosystem. Growing chronic disease burden and rising health awareness are also compelling providers to adopt digital platforms for continuous patient engagement and management. Together, these forces are positioning India as an increasingly significant hub for digital health innovation and India digital health market growth.

India Digital Health Market Trends:

Expansion of AI-Integrated Telehealth Services

Artificial intelligence is increasingly embedded into telehealth platforms, enabling smarter patient triage, predictive diagnostics, and personalized care recommendations. For instance, in 2026, the Government of India reported that its national telemedicine platform eSanjeevani had delivered over 282 million consultations, including around 12 million cases supported by AI-recommended diagnoses, highlighting the growing integration of AI into remote care delivery. This integration enhances the quality of remote consultations while reducing the burden on physical healthcare infrastructure. As AI capabilities mature, telehealth platforms are evolving from basic consultation tools into comprehensive, intelligent care delivery systems.

Rising Adoption of Wearable Health Monitoring Devices

The growing penetration of wearable health devices is enabling continuous monitoring of vital signs, physical activity, and chronic conditions. Patients and providers are leveraging real-time data for proactive health management and early intervention. For instance, in 2026, Microsoft launched its AI-powered “Copilot Health” platform, which integrates data from over 50 wearable devices and thousands of healthcare providers to generate personalized health insights and support clinical decision-making. This trend is catalyzing demand for integrated digital health platforms capable of analyzing and acting on personal health data to deliver timely, preventive care.

Widespread Deployment of Cloud-Based EMR and Health Information Systems

Cloud-based electronic medical records and health information systems are increasingly replacing legacy, paper-based documentation across hospitals and clinics. These systems streamline data management, improve interoperability, and support regulatory compliance. For instance, in 2025, Oracle introduced a next-generation, cloud-native electronic health record (EHR) system built on Oracle Cloud Infrastructure with integrated AI and voice capabilities to enhance clinical workflows and real-time data access across healthcare networks. Their capacity for real-time sharing and multi-site accessibility is enabling healthcare providers to deliver more coordinated, evidence-based, and patient-centered care at scale.

Market Outlook 2026-2034:

The digital health market in India is expected to grow at a robust rate during the forecast period, with the market growth driven by the rise of digital technologies, the development of the Indian government framework, and the increasing dependence of patients on digital health services. The increasing demand for remote consultations, AI-based diagnostics, personalized wellness, and interoperability is driving innovation across the ecosystem, with strategic investments in digital health infrastructure, the rise of mobile connectivity, and the development of public-private partnerships expected to expand the market across rural India as well. The market generated a revenue of USD 19.14 Billion in 2025 and is projected to reach a revenue of USD 90.00 Billion by 2034, growing at a compound annual growth rate of 18.06% from 2026-2034.

India Digital Health Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

|

Type |

Telehealth |

36.2% |

|

Component |

Software |

42.8% |

|

Region |

South India |

33.5% |

Type Insights:

- Telehealth

- Medical Wearables

- EMR/EHR Systems

- Medical Apps

- Healthcare Analytics

- Others

The telehealth dominates with a market share of 36.2% of the total India digital health market in 2025.

Telehealth has established itself as the dominant segment of the India digital health market, driven by its unmatched ability to deliver healthcare services remotely and conveniently. The segment benefits from widespread smartphone adoption, expanding broadband connectivity, and a growing patient preference for accessible and cost-effective consultations. Its capacity to bridge geographical and infrastructural gaps in healthcare access has made telehealth a cornerstone of India's broader digital health transformation strategy across urban and rural settings.

The continued evolution of telehealth platforms is allowing for the delivery of comprehensive care, not just basic consultations, with the advent of remote diagnostics, chronic care management, and even AI-based clinical decision support tools. Healthcare providers are increasingly integrating telehealth services with their current services, while the government is launching digital health missions that are creating the necessary interoperability that is expected to sustain the growth of telehealth services. The increased awareness of the need for preventive care, along with the acceptance of virtual care, is adding strength to the position of telehealth at the center of the healthcare ecosystem.

Component Insights:

Access the comprehensive market breakdown Request Sample

- Software

- Hardware

- Service

The software leads with a share of 42.8% of the total India digital health market in 2025.

Software has emerged as the leading component segment of the India digital health market, underpinned by its foundational role across the entire digital health ecosystem. From powering electronic health records and telehealth platforms to enabling health analytics and clinical decision-support systems, it forms the technological backbone of modern healthcare delivery in India. Its scalability, ease of deployment, and capacity for continuous enhancement make it the preferred investment priority for healthcare providers and digital health developers alike.

The increasing trend towards cloud-native solutions and AI-powered solutions is further driving the growth of this segment, as solution providers are looking at more intelligent and interoperable solutions in data management and care coordination. Hospitals, clinics, and insurance companies are increasingly looking at optimizing their digital workflows and outcome-based analytics solutions. Innovation in health information systems and the increasing trend in care platforms are expected to drive the growth of this market in the coming years.

Regional Insights:

- North India

- West and Central India

- South India

- East and Northeast India

South India exhibits a clear dominance with a 33.5% share of the total India digital health market in 2025.

The South Indian market holds the largest regional share in terms of size in the India digital health market, owing to its advanced digital infrastructure, progressive health policies at the state level, and a pre-existing ecosystem of tech-enabled healthcare service providers. The South Indian market has been able to create a highly conducive ecosystem with its connectivity, skilled workforce, and leading hospital networks/health tech companies, thereby facilitating sustained adoption and innovation in various service verticals.

The region is expected to continue its leadership position in the delivery of telehealth services, AI-based diagnostics, as well as integrated health information systems, with the active participation of the government in investing in the field, as well as the private sector. The high digital literacy of the population, along with the well-developed healthcare delivery system, is expected to help the region maintain its leadership position during the forecast period as well.

Market Dynamics:

Growth Drivers:

Why is the India Digital Health Market Growing?

Government Digital Health Initiatives and Policy Frameworks

India’s national and state-level governments have developed a comprehensive policy ecosystem that actively supports the adoption and scaling of digital health solutions. For example, under the Ayushman Bharat Digital Mission (ABDM), the state of Uttar Pradesh has become a national model for digital healthcare by digitally linking over 130 million health records to the Ayushman Bharat Health Account (ABHA) system and rolling out digital prescriptions and OPD services, positively impacting more than 240 million people. Initiatives focused on creating unified digital health identities, interoperable health record systems, and publicly accessible telemedicine platforms have established a robust and enabling infrastructure. These programs provide a common digital foundation that encourages both public institutions and private healthcare providers to transition to technology-driven care delivery models. The resulting alignment between public investment, regulatory encouragement, and private sector participation is accelerating the pace of digital transformation across primary, secondary, and tertiary care settings. This strong governmental support continues to build market confidence and sustain momentum across the India digital health landscape.

Rising Burden of Chronic Diseases and Demand for Remote Monitoring

India’s growing prevalence of non-communicable diseases such as diabetes, cardiovascular disorders, and respiratory conditions is creating an acute and sustained demand for digital health technologies capable of supporting continuous management and remote monitoring. According to a 2025 programme in Chhattisgarh, integration of Ayushman Bharat Health Account (ABHA) IDs with the national NCD portal for hypertension and diabetes patients improved follow‑up rates from ~37 % in non‑linked patients to ~68 % among ABHA‑linked patients, while control rates for these conditions increased markedly, illustrating the impact of digital tools in chronic care management. Patients managing chronic conditions require regular engagement with healthcare services, and digital platforms offer scalable, cost-effective solutions that reduce the need for frequent in-person visits. Telehealth consultations, wearable monitoring devices, and AI-powered diagnostic tools are increasingly deployed to enable proactive intervention and reduce complications. As the burden of chronic illness rises across demographic groups and geographic regions, digital health technologies are becoming integral to managing disease prevalence and delivering personalized, longitudinal care to patients throughout India.

Growing Smartphone and Internet Penetration

India’s rapidly expanding digital connectivity is a foundational enabler of the digital health market. The widespread availability of affordable smartphones and data services is bringing internet access to a growing segment of the population, including those in semi-urban and rural areas that have historically been underserved by traditional healthcare infrastructure. For instance, the Prayagraj district administration launched a pilot to develop 23 “model digital villages” with high‑speed internet connectivity to improve access to education, healthcare, and government services, enabling e‑health, video consultations, and online health information delivery in rural settings by May 2026. This expanding digital access enables patients to utilize telehealth applications, access electronic health records, and engage with mobile health platforms for the first time. Healthcare providers are also leveraging the connected digital environment to extend the reach of their services, improve patient communication, and deliver health interventions at scale. The deepening penetration of digital devices and data services is directly and sustainably broadening the addressable market for digital health solutions across India.

Market Restraints:

What Challenges the India Digital Health Market is Facing?

Limited Digital Health Literacy and Infrastructure in Rural Areas

A large section of the population in India, especially in rural and rural-off-taking areas, is not digitally literate enough or does not have access to reliable internet connectivity. This is affecting the ability of individuals to independently use and benefit from various digital health platforms, applications, and telehealth services. There is a need to create digital literacy alongside health literacy at the grassroots level so that individuals can benefit from various digital health services.

Data Privacy and Security Concerns

The increasing digitization of health records and the expansion of cloud-based health platforms raise significant concerns around patient data privacy, cybersecurity, and regulatory compliance. Healthcare providers and technology developers must invest substantially in securing sensitive health information, maintaining consent-based data governance, and adhering to evolving national data protection frameworks. These compliance requirements can increase operational costs and create uncertainty among providers and patients who lack confidence in data security measures.

Fragmented Ecosystem and Interoperability Challenges

India’s healthcare system encompasses a diverse range of institutional types, ownership models, and technology environments, making system-wide interoperability a persistent challenge. Existing disparities in technology adoption between large hospitals and smaller, rural facilities create barriers to seamless health data exchange and coordinated care delivery. Without standardized data protocols and shared infrastructure, the potential of integrated digital health platforms to improve population health outcomes remains only partially realized across the ecosystem.

Competitive Landscape:

The India digital health market is characterized by a dynamic and increasingly competitive landscape featuring a diverse mix of established healthcare information technology providers, dedicated digital health platforms, telehealth specialists, and innovative startups. Competition is primarily concentrated across telehealth services, health analytics, electronic health records, mobile health applications, and connected device solutions. Market participants are differentiating through investment in artificial intelligence capabilities, cloud-based platform development, and the creation of comprehensive integrated care ecosystems. Strategic collaboration between technology developers and healthcare institutions is accelerating the deployment of scalable solutions tailored to India’s complex and multi-tiered healthcare environment. Partnerships between digital health platforms and insurance providers are also emerging as a key competitive lever, enabling expanded coverage and patient access. The competitive environment continues to evolve as platform consolidation, venture capital investment, and public-private partnership models reshape participation and drive ongoing innovation across the market.

Recent Developments:

- In March 2026, Smart health wearable company Oura has officially entered India with the launch of its Oura Ring 4, a device that tracks 50+ health metrics and provides personalized insights using advanced sensing technology.

India Digital Health Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Telehealth, Medical Wearables, EMR/EHR Systems, Medical Apps, Healthcare Analytics, Others |

| Components Covered | Software, Hardware, Service |

| Regions Covered | North India, West and Central India, South India, East and Northeast India |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Digital Health Market Report

The India digital health market size was valued at USD 19.14 Billion in 2025.

The India digital health market is expected to grow at a compound annual growth rate of 18.06% from 2026-2034 to reach USD 90.00 Billion by 2034.

Telehealth, holding a 36.2% share, leads the market as the dominant segment, driven by growing adoption of virtual consultations, remote patient monitoring, and expanding access to digital care platforms across urban and rural populations.

Key factors driving the India digital health market include rising smartphone and internet penetration, government digital health initiatives, growing chronic disease burden, increasing demand for telemedicine services, and widespread adoption of AI-enabled healthcare platforms.

Major challenges include limited digital literacy in rural areas, data privacy and cybersecurity concerns, fragmented healthcare infrastructure, interoperability barriers, and high implementation costs for smaller healthcare providers.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade