India Digital Media Market Size, Share, Trends and Forecast by Content Type, Platform, Application, Industry Vertical, and Region, 2026-2034

India Digital Media Market Summary:

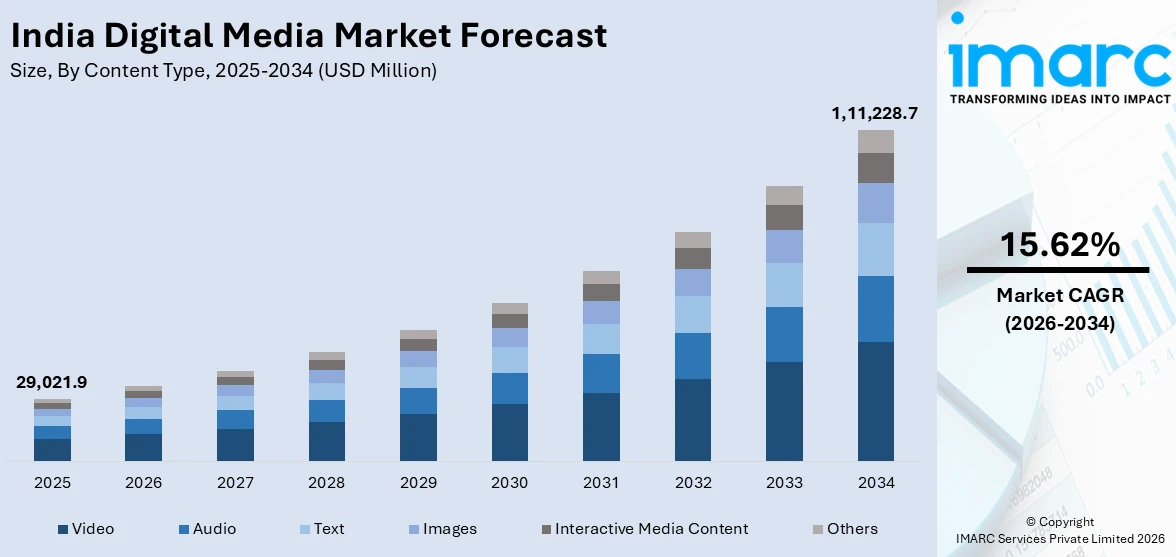

The India digital media market size was valued at USD 29,021.9 Million in 2025 and is projected to reach USD 1,11,228.7 Million by 2034, growing at a compound annual growth rate of 15.62% from 2026-2034.

The market is driven by increasing smartphone penetration, affordable internet connectivity, and growing consumer preference for on-demand digital content across diverse formats. Rapid urbanization, expanding digital infrastructure, and government-led digitalization initiatives are further propelling adoption across urban and semi-urban populations. Rising demand for regional language content and the proliferation of over-the-top streaming platforms continue to reshape consumption patterns, accelerating the overall expansion of India digital media market share.

Key Takeaways and Insights:

-

By Content Type: Video dominates the market with a share of 48.7% in 2025, driven by the proliferation of short-form and long-form streaming content and increasing consumer preference for visual storytelling.

-

By Platform: Smartphone leads the market with a share of 67.3% in 2025, owing to widespread affordable handset availability, ultra-low-cost mobile data plans, and mobile-first internet behavior of the Indian population.

-

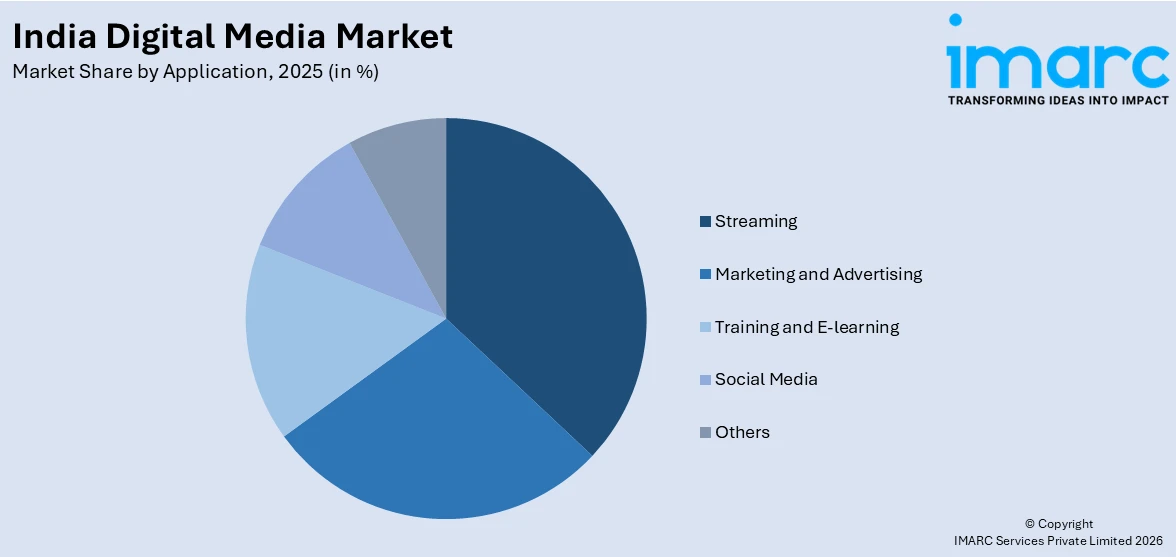

By Application: Streaming represents the largest segment with a market share of 29.5% in 2025, driven by growing consumer appetite for on-demand entertainment and the availability of diverse multilingual content libraries.

-

By Industry Vertical: Entertainment dominates the market with a share of 36.8% in 2025, owing to the massive scale of India's film and music industries and growing digital distribution of creative content.

-

By Region: South India leads the market with a share of 34.6% in 2025, driven by the region's leading technology ecosystem, higher digital literacy rates, robust IT infrastructure, and thriving regional content industry.

-

Key Players: The India digital media market exhibits a highly competitive landscape, with established global technology corporations competing alongside domestic digital-native platforms and emerging regional content providers pursuing aggressive content acquisition strategies.

To get more information on this market Request Sample

The India digital media market is experiencing robust growth fueled by a confluence of structural and technological drivers. The country's massive and increasingly connected population is transitioning rapidly from traditional media to digital channels, supported by affordable smartphone availability, low-cost mobile data plans, and expanding broadband infrastructure reaching semi-urban and rural areas. Government initiatives promoting digital literacy and connectivity are accelerating adoption across previously underserved regions. In 2025, Network18 recorded 2.5 billion CTV views, a 26% year-on-year increase, highlighting audiences shifting to large-screen digital news and long-form content across mobile, CTV, and social platforms. The proliferation of vernacular and regional language content is unlocking new audience segments, while advancements in artificial intelligence (AI) and machine learning (ML) are enabling more personalized, engaging content experiences. Furthermore, the rapid expansion of digital advertising ecosystems, the growing influence of the creator economy, and the increasing integration of e-commerce with digital media platforms are creating diversified revenue streams that collectively sustain the market's upward trajectory.

India Digital Media Market Trends:

Rise of Vernacular and Regional Language Digital Content

The India digital media market is witnessing a transformative shift toward vernacular and regional language content as new internet users originate predominantly from tier-two, tier-three cities, and rural communities. Content creators and platforms are investing heavily in producing material in Hindi, Tamil, Telugu, Bengali, Marathi, Kannada, and other regional languages to serve audiences preferring native-language consumption. As per sources, India’s internet user base exceeded 900 million, with 98% accessing content in Indic languages, reflecting rapid regional language adoption, especially in rural areas driving digital media engagement nationwide. Advances in natural language processing, AI-powered translation tools, and voice-enabled interfaces are making platforms more accessible to non-English speakers.

Integration of Artificial Intelligence in Content Discovery and Personalization

AI is rapidly becoming the backbone of digital media content delivery across India, revolutionizing how consumers discover, engage with, and share media. Machine learning algorithms are powering hyper-personalized recommendation engines that curate individualized content feeds based on user preferences, viewing patterns, and contextual signals. In 2025, Appy Pie launched PixelYatra, India’s first Hindi‑trained generative AI design tool, enabling creators to produce visual content via simple Hindi prompts, democratizing content creation nationwide. AI-driven tools are also transforming content creation itself, enabling automated video editing, dynamic thumbnail generation, and intelligent content tagging in multiple Indian languages.

Convergence of Social Commerce and Digital Media Ecosystems

India's digital media landscape is experiencing an accelerating convergence between social media platforms and commerce, creating integrated ecosystems where content consumption seamlessly transitions into purchase behavior. Live-streaming commerce, shoppable video content, and influence-led product recommendations are blurring traditional boundaries between media entertainment and retail transactions. As per sources, YouTube expanded its Shopping affiliate programme in India by adding merchants like Nykaa and Purplle, enabling creators to tag products in videos and drive direct discovery‑to‑purchase journeys for millions of viewers. This convergence is particularly powerful in India, where a vibrant creator economy comprising millions of digital content creators builds engaged communities that brands leverage for authentic product endorsements.

Market Outlook 2026-2034:

The India digital media market is poised for sustained revenue growth over the forecast period, driven by deepening the internet penetration, rising smartphone adoption, and the continued migration of advertising budgets from traditional media to digital channels. Revenue expansion will be further supported by increasing consumer willingness to pay for premium subscription content, the rapid scaling of programmatic advertising, and the growing contribution of regional language and short-form video content. The market is expected to benefit from ongoing infrastructure investments including nationwide broadband expansion and next-generation mobile connectivity, which will bring millions of new users into the digital fold and generate significant incremental revenue opportunities across content, platform, and application segments. The market generated a revenue of USD 29021.9 Million in 2025 and is projected to reach a revenue of USD 111228.7 Million by 2034, growing at a compound annual growth rate of 15.62% from 2026-2034.

India Digital Media Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Content Type |

Video |

48.7% |

|

Platform |

Smartphone |

67.3% |

|

Application |

Streaming |

29.5% |

|

Industry Vertical |

Entertainment |

36.8% |

|

Region |

South India |

34.6% |

Content Type Insights:

- Video

- Audio

- Text

- Images

- Interactive Media Content

- Others

Video dominates with a market share of 48.7% of the total India digital media market in 2025.

The video commands the largest share of the India digital media market by content type, driven by the explosive growth in both long-form and short-form video consumption across streaming platforms, social media applications, and user-generated content portals. India's vast and youthful population demonstrates a strong preference for visual content formats, with video serving as the primary medium for entertainment, education, news, and social engagement. According to reports, in 2025, an IPSOS study commissioned by Meta found that 97% of Indian consumers watch short‑form video daily, with 92% preferring Instagram Reels as their go‑to format, underscoring video’s dominance in everyday digital habits.

The dominance of video content is further reinforced by the increasing availability of affordable high-speed mobile internet, which has made seamless video streaming accessible to users in semi-urban and rural areas. Content producers are investing heavily in original regional-language video programming to capture linguistically diverse audiences. Technological innovations such as adaptive bitrate streaming and AI-driven content curation continue to enhance the viewing experience, while the integration of interactive and shoppable video formats is creating new engagement and monetization dimensions that solidify video's leading position.

Platform Insights:

- Smartphone

- Television

- Computer

- Tablets

- Others

Smartphone leads with a share of 67.3% of the total India digital media market in 2025.

The smartphone holds the largest share in the India digital media market, reflecting the country's fundamentally mobile-first digital ecosystem. India's massive smartphone user base, fueled by the availability of affordable handsets and competitively priced mobile data plans, has made the smartphone the primary gateway for accessing digital content, social media, streaming services, and online communication. According to reports, 23% of Indians relied solely on mobile phones for entertainment and media consumption, up from 15% in 2023, highlighting the centrality of smartphones in everyday digital behaviour.

The dominance of the smartphone platform is further fueled by the improvements in the capabilities of smartphones, such as improvements in display quality, processing power, and battery life. The mobile-optimized content formats, progressive web applications, and app-based ecosystems are designed to meet the requirements of the Indian on-the-go consumer. As the rural connectivity increases and the next-generation mobile networks become widespread, the smartphone-based digital media consumption is expected to maintain its leading market position, especially among the first-time internet users.

Application Insights:

Access the comprehensive market breakdown Request Sample

- Marketing and Advertising

- Training and E-learning

- Social Media

- Streaming

- Others

Streaming exhibits a clear dominance with a 29.5% share of the total India digital media market in 2025.

The streaming leads the India digital media market by application, driven by the rapid adoption of over-the-top video and audio streaming platforms offering on-demand access to vast content libraries. Indian consumers are increasingly shifting away from traditional linear broadcasting in favor of personalized, time-flexible streaming experiences that offer multilingual content spanning films, series, music, podcasts, and live events. In 2025, India’s OTT audience reached 601 million monthly viewers, demonstrating widespread adoption of on-demand video content across urban and rural markets nationwide.

The leadership in the segment is aided by increasing competition among the streaming services, which are constantly investing in original content, pricing models, and bundled services with telecom operators. The fact that there are both subscription and advertising-funded models of streaming has expanded the addressable market substantially. Moreover, the increasing popularity of live streaming for sports, gaming, and interactive content is opening up new dimensions of engagement. The investments in regional languages by the major streaming services are further cementing the leadership position of the streaming segment in the overall digital media space.

Industry Vertical Insights:

- Entertainment

- Retail and E-commerce

- Healthcare

- Government

- BFSI

- Telecom

- Automotive

- Hospitality

- Non-profit Organizations

- Publishing

- Others

Entertainment leads with a market share of 36.8% of the total India digital media market in 2025.

The entertainment dominates the India digital media market, reflecting the central role of films, music, gaming, and creative content in India's cultural fabric. India's globally renowned entertainment industry, spanning multiple languages and regional markets, has aggressively embraced digital distribution channels enabling unprecedented reach and audience engagement. The migration of theatrical releases to digital-first or simultaneous digital release models has accelerated consumer adoption of entertainment-focused digital media platforms, while music streaming and podcasting have emerged as powerful complementary formats.

The leadership position in the entertainment vertical is further reinforced by the rapid rise of mobile gaming, the increasing popularity of digital music streaming, and the emergence of user-generated content in the entertainment space on social media platforms. The young demographic profile of India is creating a massive demand for various entertainment offerings in different languages and genres. The convergence of interactive and immersive technologies such as augmented reality experiences and interactive storytelling is giving rise to new paradigms in the entertainment space. Furthermore, fan engagement and creator-led entertainment ecosystems are also increasing.

Regional Insights:

- North India

- South India

- East India

- West India

South India dominates with a market share of 34.6% of the total India digital media market in 2025.

South India holds the largest regional share in the India digital media market, driven by the region's robust technology infrastructure, high digital literacy rates, and the presence of major information technology hubs in Bengaluru, Hyderabad, and Chennai. The southern states of Karnataka, Tamil Nadu, Telangana, Kerala, and Andhra Pradesh benefit from relatively higher internet penetration and smartphone adoption compared to other regions, creating a highly conducive environment for digital media consumption and content creation across diverse formats and platforms.

The region's leadership is reinforced by a thriving regional content ecosystem that produces high-quality digital content in Tamil, Telugu, Kannada, and Malayalam languages. South India's entertainment industry has been particularly successful in leveraging digital platforms for content distribution, with regional films and music consistently attracting massive online audiences. Furthermore, the region's strong educational infrastructure, progressive digital governance initiatives, and higher per capita income levels contribute to greater consumer spending on digital media subscriptions and premium services, sustaining its leading position in the market.

Market Dynamics:

Growth Drivers:

Why is the India Digital Media Market Growing?

Expanding Internet Connectivity and Affordable Mobile Data Ecosystems

India's digital media market is experiencing transformative growth driven by the dramatic expansion of internet connectivity and the availability of ultra-affordable mobile data plans. The nationwide rollout of high-speed mobile networks has brought reliable internet access to millions of previously unconnected consumers in semi-urban and rural regions, creating an enormous and rapidly expanding base of digital media consumers. In February 2025, under BharATNet Phase 3, the government announced subsidised broadband expansion to 1.5 crore rural households, significantly enhancing digital inclusion and internet access in remote India. Government-led initiatives promoting broadband infrastructure development and universal connectivity are accelerating this expansion.

Rising Smartphone Penetration and Mobile-First Consumer Behavior

The widespread adoption of affordable smartphones across India is serving as a fundamental growth catalyst for the digital media market. As device manufacturers continue introducing feature-rich handsets at accessible price points, millions of new consumers are gaining their first gateway to digital content consumption. In February 2026, affordable 5G smartphone shipments in India surged over 1,900% year‑on‑year, driven by aggressive pricing and wider network coverage, signalling how rapidly entry‑level devices are proliferating nationwide. India's inherently mobile-first internet culture means that smartphones serve as the primary device for accessing streaming platforms, social media, online gaming, and digital news. The continuous improvement in mobile device capabilities, including enhanced display quality and processing power, enables increasingly sophisticated multimedia experiences that drive deeper consumer engagement with digital media.

Digital Transformation of Advertising and Brand Communication Strategies

The accelerating migration of advertising expenditure from traditional media channels to digital platforms represents a critical growth driver for the India digital media market. Advertisers are increasingly recognizing the superior targeting capabilities, measurable performance metrics, and cost efficiencies offered by digital advertising compared to conventional television, print, and radio channels. The rise of programmatic advertising, data-driven audience segmentation, and AI-powered campaign optimization tools enable brands to deliver highly personalized messages to specific consumer segments at scale. Social commerce integration is further creating closed-loop marketing ecosystems delivering superior return on investment.

Market Restraints:

What Challenges the India Digital Media Market is Facing?

Digital Infrastructure Gaps in Rural and Remote Regions

Despite significant progress in expanding internet connectivity, substantial digital infrastructure gaps persist in India's rural and remote regions. Many areas continue to experience unreliable network coverage, slow connection speeds, and frequent service interruptions that degrade the digital content consumption experience. These infrastructure limitations restrict access to bandwidth-intensive content formats and constrain overall market penetration potential.

Content Monetization and Revenue Sustainability Challenges

The India digital media market faces persistent challenges related to content monetization and long-term revenue sustainability. Indian consumers have historically demonstrated strong price sensitivity and a preference for free, advertising-supported content over paid subscription models. This behavior places significant pressure on platforms to generate adequate returns from advertising revenues alone, constraining profitability across the value chain.

Regulatory Complexity and Content Governance Uncertainties

The evolving and multi-layered regulatory environment governing digital media in India presents significant compliance challenges for market participants. Frequent changes in content regulation, data privacy requirements, and intermediary liability provisions create uncertainty for platforms, content creators, and advertisers. Navigating multiple regulatory frameworks across central and state-level jurisdictions increases operational complexity and compliance costs considerably.

Competitive Landscape:

The India digital media market is characterized by a highly fragmented and intensely competitive landscape, with a diverse mix of global technology conglomerates, domestic digital-native platforms, telecommunications operators, and emerging regional content providers vying for consumer attention and advertising revenues. Market participants are employing multi-pronged competitive strategies encompassing aggressive content investment, technology innovation, strategic pricing, and partnership-driven distribution to capture market share in this rapidly evolving ecosystem. The competitive dynamics are further intensified by low switching costs for consumers, who can easily migrate between platforms based on content availability, pricing, and user experience. Companies are increasingly differentiating through exclusive original content production, advanced personalization algorithms, and regional language content portfolios tailored to India's linguistically diverse audience base.

Recent Developments:

-

In November 2025, JoinTheStory announced a hybrid media-tech platform launching January 1, 2026, focused on credible, data-driven journalism. The initiative will offer multilingual digital portals, OTT storytelling, and an integrated newsroom model to rebuild public trust, engage younger audiences, and strengthen India’s evolving digital media ecosystem and future industry growth nationwide expansion.

India Digital Media Market Report Coverage:

|

Report Features |

Details |

|

Base Year of the Analysis |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Units |

Million USD |

|

Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

|

Content Types Covered |

Video, Audio, Text, Images, Interactive Media Content, Others |

|

Platforms Covered |

Smartphone, Television, Computer, Tablets, Others |

|

Applications Covered |

Marketing and Advertising, Training and E-learning, Social Media, Streaming, Others |

|

Industry Verticals Covered |

Entertainment, Retail and E-commerce, Healthcare, Government, BFSI, Telecom, Automotive, Hospitality, Non-profit Organizations, Publishing, Others |

|

Regions Covered |

North India, South India, East India, West India |

|

Customization Scope |

10% Free Customization |

|

Post-Sale Analyst Support |

10-12 Weeks |

|

Delivery Format |

PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Digital Media Market Report

The India digital media market size was valued at USD 29,021.9 Million in 2025.

The India digital media market is expected to grow at a compound annual growth rate of 15.62% from 2026-2034 to reach USD 1,11,228.7 Million by 2034.

Video held the largest India digital media market share, driven by the explosive growth of streaming platforms, short-form video content, and strong consumer preference for visual media formats across India's digitally connected population.

Key factors driving the India digital media market include expanding internet connectivity and affordable mobile data, rising demand for regional and multilingual digital content, digital transformation of advertising, increasing smartphone penetration, and growing consumer preference for on-demand streaming and personalized content experiences.

Major challenges include persistent digital infrastructure gaps in rural and remote regions, content monetization difficulties amid price-sensitive consumer behavior, evolving and complex regulatory frameworks, intense competition leading to unsustainable content spending, data privacy concerns, and the challenge of combating misinformation and maintaining content quality across platforms.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)