India Digital Payment Market Size, Share, Trends and Forecast by Component, Payment Mode, Deployment Type, End Use Industry, and Region, 2026-2034

India Digital Payment Market Size & Forecast 2026-2034

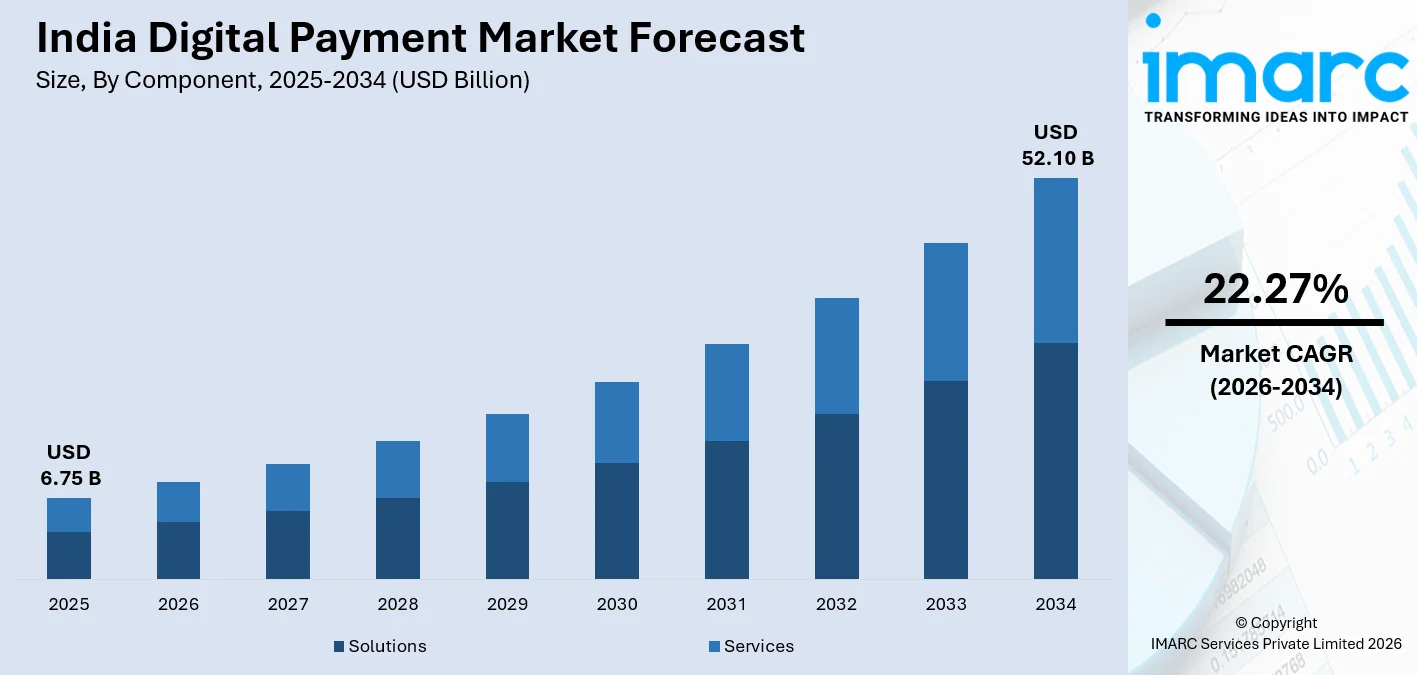

The India digital payment market size, valued at USD 6.75 Billion in 2025, is projected to reach USD 52.10 Billion by 2034, growing at a CAGR of 22.27% from 2026-2034, reflecting the rapid adoption of UPI-based solutions, mobile wallets, and cloud-hosted payment infrastructure across the country. The RBI's Digital Payments Index reached 516.76 in September 2025, up from 493.22 in March 2025, underscoring surging penetration across urban and rural segments. The government's Digital India push, combined with Jan Dhan financial inclusion and Aadhaar-linked identity, continues to expand the addressable user base and drive India digital payment market share.

To get more information on this market Request Sample

India Digital Payment Industry Analysis - Key Insights

- Solutions command 77.2% of the market by component in 2025 - software-led payment infrastructure is structurally dominant. APIs, gateways, and processing engines are the core commercial layer that banks, fintechs, and merchants all depend on.

- Digital wallets own 60.7% of payment mode in 2025 - the highest single-segment dominance across all five categories. PhonePe, with a 46% UPI share, and Google Pay, with 34.6%, together define what digital payments look like at the point of sale for most Indians.

- Cloud-based captures deployment type 74.2% in 2025 - nearly three in four digital payment deployments run on cloud rails. Scalability, cost efficiency, and rapid API integration have made on-premise models effectively obsolete for new entrants.

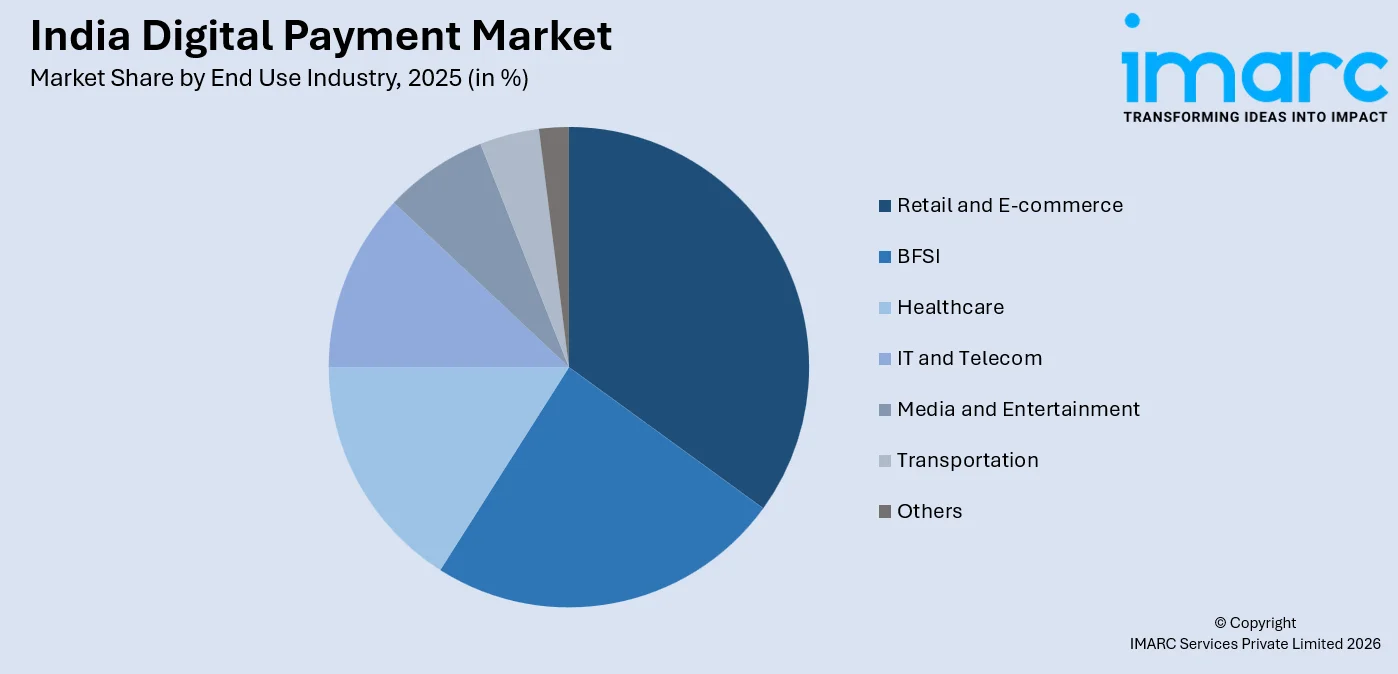

- Retail and e-commerce drive 35.0% of end use industry revenue in 2025 - online retail's explosion powers the single largest end-use segment, with QR merchant payments and in-app checkout both accelerating UPI adoption at an unmatched pace.

- West and Central India leads regionally at 32.6% in 2025 - a dominant regional share anchored by Maharashtra's fintech headquarters and Gujarat's digitized manufacturing corridors.

India Digital Payment Market Trends and Dynamic 2026

Market Trends

Rise of AI-powered and agentic payment experiences

India's digital payment ecosystem is evolving rapidly with artificial intelligence embedding itself into the transaction layer. In October 2025, Razorpay and National Payments Corporation of India (NPCI) partnered with OpenAI to pilot agentic payments on ChatGPT, enabling conversational commerce where users browse, order, and pay within a single chat interaction. The platform uses UPI Reserve Pay and supports merchants, marking a structural shift from reactive to autonomous payment behaviour.

UPI surpasses global benchmarks, reshaping real-time payment standards

The IMF's June 2025 report recognized UPI as the world's largest retail real-time payment system, processing over 640 million daily transactions, surpassing Visa's 639 million for the first time. In August 2025, UPI processed 20 billion transactions worth ₹24.85 lakh crore in a single month. With 85% of all digital payment volumes now flowing through UPI, this structural depth directly defines India digital payment market trends for the next decade.

RBI's GFF 2025 product launches accelerate infrastructure innovation

At the Global Fintech Festival held in Mumbai in October 2025, the RBI Governor unveiled four landmark digital payment innovations: AI-based UPI HELP, IoT Payments with UPI, the interoperable Banking Connect net-banking solution, and UPI Reserve Pay. These launches represent India's pivot to 'intelligence, interoperability, and inclusivity' in its payment infrastructure, elevating the sophistication of the solution ecosystem considerably.

- Biometric UPI Authentication: In October 2025, NPCI debuted facial recognition and fingerprint-based UPI payment confirmation, eliminating the numeric PIN for eligible users.

- IoT-Enabled Micro-Transactions: Connected cars, smartwatches, and smart TVs are now being authorized to initiate UPI payments for fuel, EV charging, and subscriptions, creating frictionless embedded commerce.

- Cross-Border UPI Expansion: UPI is now live in 8 countries, including Qatar, Bhutan, France, Mauritius, Nepal, Singapore, Sri Lanka, and the United Arab Emirates.

- Super-App Wallet Evolution: PhonePe, Paytm, and Google Pay are evolving beyond payments into full financial super-apps integrating insurance, investments, lending, and loyalty retaining users far beyond the transaction.

Growth Drivers

Government-backed digital public infrastructure driving mass-scale adoption

India's Jan Dhan–Aadhaar–Mobile (JAM) trinity continues to pull tens of millions of previously unbanked citizens into the digital economy. As of July 2025, over 55.83 crore Jan Dhan accounts had been opened, each functioning as an on-ramp to UPI. The Union Cabinet approved a ₹1,500 crore incentive scheme for FY 2024-25 in March 2025 to promote low-value BHIM-UPI merchant transactions, directly stimulating India digital payment market growth in Tier-3 to Tier-6 cities.

Rapid smartphone penetration and affordable internet access are fuelling adoption

Approximately India's 25 crore mobile subscribers are using 5G services, and 4.69 lakhs 5G BTSs have been installed across India, which have turned digital payments into a daily utility for even semi-urban populations. UPI's 678 million QR codes and 11.2 million PoS terminals as of H1 2025 reflect deep merchant-side infrastructure build-out, making cashless acceptance the default for kirana stores, street vendors, and hypermarkets alike.

E-commerce expansion creating high-frequency digital payment occasions

India's rapidly expanding e-commerce sector, with online retail players like Meesho, Flipkart, and AJIO driving high-frequency transactions, is a critical engine for digital payment volume. Person-to-Merchant UPI transactions reached 67.01 billion in H1 2025, growing 37% YoY, driven by wider merchant acceptance and Q-commerce delivery platforms embedding UPI at checkout by default. Subscription services for OTT and SaaS add recurring payment volume as well.

- Financial Inclusion Programs: RBI's PIDF deployed 5.45 crore digital touch points in Tier-3 to Tier-6 centres by October 2025, extending merchant acceptance into India's deepest rural markets.

- Rising MSME Digitization: Razorpay's collaboration with NPCI raised UPI limits, creating a critical mass of payment-enabled small businesses.

- Credit-on-UPI Expansion: RuPay credit card linkage to UPI now accounts for 16% of India's credit card spending, opening premium transaction segments within the existing UPI rail.

- AI and Machine Learning Integration: Real-time fraud detection using ML models, conversational finance tools, and personalized payment nudges are raising both security and user engagement across platforms.

Market Restraints

Cybersecurity threats and digital fraud risk: The rapid expansion of digital payment touchpoints has amplified exposure to phishing attacks, account takeovers, and social-engineering fraud. As payment rails become more embedded in everyday commerce, the complexity of protecting consumers and merchants from evolving cybercrime increases substantially, placing pressure on platforms to continuously invest in advanced security infrastructure.

Regulatory complexity and compliance burden: The digital payment landscape in India operates under an intricate and evolving regulatory framework spanning RBI guidelines, NPCI directives, SEBI oversight for investment-linked payments, and DPDP Act 2023 data protection requirements. Navigating this multi-regulator environment demands significant legal, compliance, and technology resources, creating friction for smaller payment aggregators and new market entrants seeking to scale quickly.

Digital literacy gaps and cash dependency in rural segments: Despite impressive infrastructure rollout, a substantial portion of India's rural and semi-urban population remains reliant on cash for everyday transactions due to limited digital literacy, unreliable internet connectivity in remote areas, and a habitual preference for physical currency. Sustained adoption requires not just access but active behavioral change, which takes time, targeted education, and locally-relevant product design to achieve at scale.

India Digital Payment Market Segmentation Analysis

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Component | Solutions | 77.2% | 2025 |

| Payment Mode | Digital Wallets | 60.7% | 2025 |

| Deployment Type | Cloud-based | 74.2% | 2025 |

| End Use Industry | Retail and E-commerce | 35.0% | 2025 |

| Region | West and Central India | 32.6% | 2025 |

Component Insights

Solutions - 77.2% Market Share (2025) | Leading Component

Solutions dominate the India digital payment market, encompassing payment gateways, APIs, processing engines, security and fraud management tools, and transaction risk platforms. Razorpay revenue climbed 65% to ₹3,783 crore in FY25. The solutions segment benefits from enterprise demand for embedded APIs increasingly used by e-commerce, logistics, and healthtech firms for automated checkout, instant settlement, and recurring billing integration.

|

Segment Breakdown Solutions- (Application Program Interface, Payment Gateway, Payment Processing, Payment Security and Fraud Management, Transaction Risk Management, and Others) (77.2%) · Services- (Professional Services and Managed Services) |

Payment Mode Insights

Digital Wallets - 60.7% Market Share (2025) | Leading Payment Mode

Digital wallets command a decisive majority of all payment mode revenue, powered by UPI's seamless bank-to-wallet interoperability and the explosive user growth of PhonePe, Google Pay, and Paytm. PhonePe processed approximately 9.8 billion UPI transactions worth Rs 13.61 lakh crore in December 2025 alone. The wallet segment has also evolved structurally into a financial super-app format.

|

Segment Breakdown Digital Wallets (60.7%) · Bank Cards · Digital Currencies · Net Banking · Others |

Deployment Type Insights

Cloud-based - 74.2% Market Share (2025) | Leading Deployment Type

Cloud-based deployment dominates India's digital payment infrastructure, driven by the need for elastic scalability to handle UPI's 640 million-plus daily transactions and the inherently variable load patterns of retail and festival-season commerce.

|

Segment Breakdown Cloud-based (74.2%) · On-premises |

End Use Industry Insights

Access the comprehensive market breakdown Request Sample

Retail and E-commerce - 35.0% Market Share (2025) | Leading End Use Industry

Retail and e-commerce are the undisputed leaders in end-use revenue, powered by India's fast-growing online shopping ecosystem and widespread QR-based merchant digitization. Platforms such as Flipkart, Meesho, and AJIO have driven deep UPI integration at checkout, while Q-commerce delivery apps on Swiggy and Zepto further amplify high-frequency small-ticket digital transactions throughout the day. BFSI, healthcare, IT and telecom, media and entertainment, and transportation each represent important and growing sub-segments. Healthcare digital payments are rising steadily as patients use PhonePe and Paytm on platforms such as Practo and 1mg for diagnostics, teleconsultation, and pharmacy purchases.

|

Segment Breakdown Retail and E-commerce (35.0%) · BFSI · Healthcare · IT and Telecom · Media and Entertainment · Transportation · Others |

Regional Insights

West and Central India - 32.6% Market Share (2025) | Leading Region

West India commands the largest regional share, anchored by Maharashtra's position as India's premier fintech hub and Gujarat's highly digitized manufacturing corridors. West India's payment gateway market is driven by high smartphone penetration, advanced supply-chain digitization, and MSME adoption of QR payments across Pune, Ahmedabad, and Surat.

|

Metric

|

Details

|

|---|---|

|

Market Share in 2025

|

32.6%

|

|

Key States

|

Maharashtra, Gujarat, Rajasthan, Goa |

|

Major Growth Drivers

|

Fintech HQ concentration, MSME supply-chain digitization, state fintech policy, QR merchant adoption |

|

Outlook

|

Dominant and structurally entrenched regional leader |

|

Regional Breakdown West and Central India (32.6%) · North India · South India · East and Northeast India |

North India:

North India is the second-largest region, powered by Delhi-NCR's concentration of enterprise clients, central government payment mandates, and PFMS-linked bulk payment systems. UPI person-to-person payments dominate in Delhi, Haryana, and Punjab, where smartphone penetration and urban income levels are among the highest in the country. Government procurement portals and salary disbursement systems have standardized QR acceptance across public sector institutions throughout the region.

|

Metric

|

Details

|

|---|---|

|

Key States

|

Delhi, Uttar Pradesh, Haryana, Punjab, Rajasthan, Uttarakhand, Himachal Pradesh, Jammu and Kashmir |

|

Major Growth Drivers

|

Enterprise payment volume, government PFMS integration, high urban smartphone density, P2P dominance |

|

Outlook

|

Robust and enterprise-payment driven |

South India:

South India is one of India's most innovation-dense digital payment regions, anchored by Bengaluru's startup ecosystem and Tamil Nadu's early experiments on ONDC credit rails. According to NPCI, Telangana ranked as the fourth largest contributor in India, clocking ₹1.26 lakh crore worth of transactions in July alone. In June 2025, Cashfree Payments, a Bengaluru-based payment aggregator, launched an RBI-compliant AI-powered Video-KYC solution, claiming to boost onboarding conversions by up to 80%, reflecting the region's continued leadership in payment technology innovation. The Digital Naari empowerment campaign is active across South India, enabling women entrepreneurs in rural clusters to access settlement infrastructure.

|

Metric

|

Details

|

|---|---|

|

Key States

|

Karnataka, Tamil Nadu, Telangana, Andhra Pradesh, Kerala |

|

Major Growth Drivers

|

Bengaluru startup density, ONDC credit experimentation, high digital literacy, fintech talent pool |

|

Outlook

|

Technology hub sustaining national payment innovation |

East and Northeast India:

East and Northeast India represents the fastest-growing regional market. Government financial inclusion drives and rural e-commerce expansion are the key structural catalysts. West Bengal, Odisha, and Assam are emerging as high-growth sub-markets as smartphone penetration accelerates and fintech players target previously unserved MSME clusters.

|

Metric

|

Details

|

|---|---|

|

Key States

|

West Bengal, Odisha, Bihar, Jharkhand, Assam, Meghalaya, Mizoram, Tripura, Manipur, Nagaland, Arunachal Pradesh, Sikkim |

|

Major Growth Drivers

|

PIDF infrastructure rollout, rural UPI adoption, government financial inclusion, Northeast fintech expansion |

|

Outlook

|

Fastest-growing region with highest incremental upside |

Market Outlook 2026-2034

What is the future outlook of the India digital payment market?

The India digital payment market is expected to sustain steady revenue growth through 2034.

With UPI projected to surpass 1 billion daily transactions by FY 2026-2027, the structural foundations for sustained compounding remain firmly in place. Government-led programs, continued 5G expansion, and AI-powered payment personalization will unlock the next wave of rural and semi-urban adoption. Innovation in cross-border UPI linkages, IoT payment rails, and conversational agentic commerce will define the India digital payment market outlook through the forecast decade, positioning India as a global blueprint for real-time inclusive payment infrastructure.

India Digital Payment Market - Leading Key Players

The India digital payment market is shaped by a concentrated group of high-scale fintech and banking technology players who compete fiercely on transaction volume, merchant acquisition, and ecosystem expansion. Key players are increasingly pivoting from pure payment processing toward financial super-apps, offering credit, insurance, investment, and embedded commerce alongside core UPI and gateway services.

| Company | Leading Brands | Highlights |

|---|---|---|

| PhonePe Private Limited | PhonePe App, PhonePe Business | Processed 9.81 billion transactions in December 2025, partnered with SIDBI in September 2025 for merchant credit access via Udyam Assist Registrations |

| Paytm | Paytm App, Paytm Payments Bank | Processes 1.6–1.7 billion monthly UPI transactions contributing 7–8% of overall UPI activity. |

| Razorpay | Razorpay Payment Gateway, RazorpayX | Holds 55% of India's payment gateway market share, In April 2025 became the first gateway on the UPI plugin from NPCI BHIM Services Limited |

Some of the other key market players in India digital payment market are National Payments Corporation of India (NPCI), Google LLC (Google Pay), etc.

Latest Development & News

- In January 2026, Razorpay filed draft prospectus documents targeting an IPO of approximately ₹4,500 crore on Indian exchanges. The company invited merchant bankers to submit bids for the IPO mandate, adding Kotak Mahindra and Axis Capital are frontrunners for the underwriter role.

- In October 2025, Zoho Payment Technologies announced expansion of its financial technology portfolio, launching a full suite of merchant payment solutions including POS devices, QR-code payment devices for digital payment infrastructure.

- In October 2025, Razorpay and YES Bank launched India's first RBI-compliant biometric card-authentication platform. The new access-control server combines AI-driven facial recognition with real-time risk checks, processes 10,000 transactions per second, and delivers highest success rates.

India Digital Payment Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Components Covered |

|

| Payment Modes Covered | Bank Cards, Digital Currencies, Digital Wallets, Net Banking, Others |

| Deployment Types Covered | Cloud-based, On-premises |

| End Use Industries Covered | BFSI, Healthcare, IT and Telecom, Media and Entertainment, Retail and E-commerce, Transportation, Others |

| Regions Covered | North India, West and Central India, South India, East and Northeast India |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the India digital payment market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the India digital payment market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the India digital payment industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the India Digital Payment Market Report

The India digital payment market was valued at USD 6.75 Billion in 2025.

The India digital payment market is anticipated to reach a value of USD 52.10 Billion by 2034.

Solutions dominate the component segment with a share of 77.2%, reflecting strong enterprise and fintech demand for payment gateways, APIs, and processing infrastructure that underpins every digital transaction in the country.

Digital wallets command the payment mode segment with a share of 60.7%, driven by UPI's structural integration with mobile wallets and the rapid expansion of super-app financial ecosystems across the country.

Cloud-based deployment type captures 74.2%, driven by scalability, cost efficiency, and rapid API integration, which have made on-premise models effectively obsolete for new entrants.

Retail and e-commerce drive end use industry segment with 35.0%, driven by QR merchant payments and in-app checkout, both accelerating UPI adoption at an unmatched pace.

West and Central India currently leads the India digital payment market, accounting for a share of 32.6%. The region benefits from Maharashtra's fintech regulatory concentration, Gujarat's manufacturing sector digitization, and the dense clustering of payment infrastructure firms that anchor its structural leadership.

Some of the major players in the market include PhonePe Private Limited, Paytm, Razorpay, National Payments Corporation of India (NPCI), Google LLC (Google Pay), etc.

Key trends include the emergence of biometric UPI authentication replacing numeric PINs, the rapid globalization of UPI now accepted in seven countries, the integration of buy-now-pay-later services within UPI flows, and the growing deployment of voice-based payments through UPI 123PAY for feature phone users. These trends collectively reflect a maturing ecosystem that is expanding beyond smartphone-centric urban users.

Growth is driven by the continued expansion of Aadhaar-linked identity enabling instant digital onboarding, the proliferation of QR-code merchant infrastructure into Tier-4 and Tier-5 geographies, deepening RuPay credit card integration within UPI flows, increasing MSME adoption of cloud-based payment solutions, and India's active cross-border UPI linkages enabling inward remittances and diaspora payments through interoperable real-time rails.

Key challenges include the rising sophistication of cyber fraud targeting UPI accounts and digital wallets, the burden of multi-regulator compliance under RBI, NPCI, SEBI, and DPDP Act 2025 frameworks, the persistently low average ticket size of UPI transactions that constrains per-transaction revenue for platform operators, and the difficulty of achieving genuine last-mile adoption among populations with low digital literacy in India's most remote districts.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade