India Disinfectant Market Size, Share, Trends and Forecast by Type, Formulation, End-User, Distribution Channel, and Region 2026-2034

India Disinfectant Market Summary:

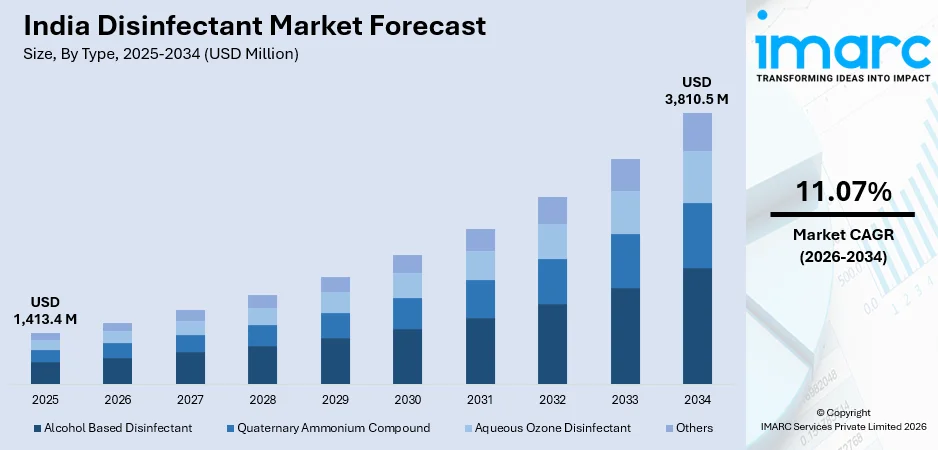

The India disinfectant market size was valued at USD 1,413.4 Million in 2025 and is projected to reach USD 3,810.5 Million by 2034, growing at a compound annual growth rate of 11.07% from 2026-2034.

The India disinfectant market is experiencing robust growth, driven by heightened hygiene awareness, rising healthcare infrastructure, and increased demand from commercial, residential, and industrial sectors, with consumers and institutions prioritizing advanced, effective formulations to prevent infections, enhance safety, and comply with regulatory standards, while innovations in eco-friendly and multipurpose disinfectants further expand adoption across urban and rural regions.

Key Takeaways and Insights:

- By Type: Alcohol-based disinfectants held the largest share in the market at 48.7% in 2025, owing to their rapid action, proven effectiveness, and widespread use in healthcare and institutional settings.

- By Formulation: Liquid dominates the market with a share of 63.2% in 2025, owing to ease of application, superior surface coverage, and versatility across multiple sectors.

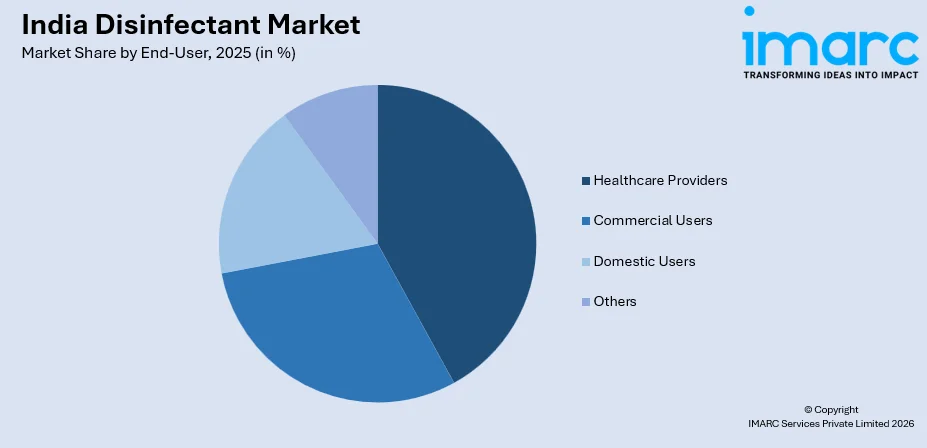

- By End-User: Healthcare Providers accounted for the highest market share of 41.5% in 2025 due to stringent infection control protocols and high hygiene compliance standards.

- By Distribution Channel: B2B dominates the market with a share of 52.6% in 2025, owing to established supplier networks and bulk purchasing agreements supporting institutional demand.

- By Region: West India held the largest market segment capturing 30.9% share in 2025, supported by industrial hubs, urban population, and high healthcare infrastructure density.

- Key Players: The competitive landscape comprises multinational and domestic manufacturers emphasizing innovation, expanded production capacity, regulatory compliance, strategic partnerships, and marketing to strengthen brand presence and meet growing institutional and consumer demand.

To get more information on this market Request Sample

The India disinfectant market is witnessing significant expansion, driven by rising incidences of infectious diseases and the emphasis on infection prevention in hospitals and clinics. Similarly, continual technological advancements, including the development of long-lasting, multi-surface, and eco-friendly disinfectants, are shaping market dynamics. Growth in industrial sectors, such as food processing and hospitality, is also stimulating market demand. Likewise, rapid urbanization, expanding healthcare infrastructure, and rising disposable incomes contribute to wider product adoption. As per the World Bank, India is witnessing growing urbanization. By 2036, cities and towns are expected to house 600 million people, 40% of the population, up from 31% in 2011, while urban areas will generate nearly 70% of GDP. Apart from this, manufacturers are increasingly focusing on innovative formulations, efficient delivery systems, and strategic distribution networks to strengthen market penetration.

India Disinfectant Market Trends:

Innovation in Eco‑Friendly and Biodegradable Disinfectants

The India disinfectant market is increasingly focused on eco‑friendly and biodegradable formulations as consumers and institutions seek products with reduced environmental impact. Manufacturers are developing plant‑based and low‑toxicity disinfectants that maintain efficacy while minimizing chemical residues. This shift is supported by rising environmental awareness, regulatory support for sustainable products, and growing institutional buyer preference for safer alternatives. A 2024 industry survey found that nearly 80% of Indian consumers are very concerned about climate change and environmental sustainability, and 60% are willing to pay a premium for eco-friendly products. As demand for green solutions expands across residential and commercial segments, eco‑innovative disinfectants are becoming key differentiation factors in product portfolios.

Growth of Contactless and Automated Disinfection Technologies

Contactless and automated disinfection solutions are gaining traction in India, particularly in high‑traffic public spaces and healthcare settings. Technologies such as UV‑C light sterilization, automated spray systems, and sensor‑based dispensers are being adopted to enhance hygiene with minimal human intervention. For instance, in November 2025, India’s agricultural sprayer technology has evolved from manual knapsacks to GPS-enabled precision systems. Modern sprayers with electrostatic and air-induction nozzles boost efficiency, reduce chemical drift, lower input costs, and support sustainable, high-yield farming practices. These innovations improve operational efficiency, reduce cross‑contamination risks, and support compliance with stringent sanitation protocols. As organizations prioritize advanced hygiene infrastructure, automated disinfection technologies complement traditional chemical disinfectants, driving integrated market growth.

Increased Adoption in Non‑Healthcare Institutional Sectors

Recent trends indicate rising disinfectant usage in non‑healthcare institutional sectors such as education, transportation, and corporate offices. Awareness of pathogen transmission risks has prompted schools, transit authorities, and workplaces to implement regular disinfection routines. Bulk procurement of disinfectants and professional sanitation services is becoming standard practice in facility management contracts. Additionally, regulatory expectations around public safety and hygiene certification standards are encouraging broader institutional integration of disinfectant protocols, expanding overall market demand beyond conventional healthcare users.

Market Outlook 2026-2034:

The India disinfectant market is expected to sustain strong growth as hygiene standards become integral to public health and safety practices across sectors. Similarly, expansion in organized retail, digital healthcare platforms, and facility management services will broaden product accessibility. For instance, in December 2025, Trivitron Digital.AI, a joint venture with ResoHealth, launches cloud-based, AI-enabled digital healthcare solutions in India, integrating LIS, Web-PACS, and mobile PHRs to enhance hospital efficiency, interoperability, patient care, and accessibility, especially in Tier-2/3 regions. The continued investment in research and development is likely to yield advanced, multipurpose disinfectants with enhanced efficacy and user convenience. Furthermore, rapid integration with smart sanitation systems and institutional procurement frameworks is anticipated to support consistent demand, reinforcing long‑term market resilience and diversification. The market generated a revenue of USD 1,413.4 Million in 2025 and is projected to reach a revenue of USD 3,810.5 Million by 2034, growing at a compound annual growth rate of 11.07% from 2026-2034.

India Disinfectant Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Type |

Alcohol Based Disinfectant |

48.7% |

|

Formulation |

Liquid |

63.2% |

|

End-User |

Healthcare Providers |

41.5% |

|

Distribution Channel |

B2B |

52.6% |

|

Region |

West India |

30.9% |

Type Insights:

- Quaternary Ammonium Compound

- Aqueous Ozone Disinfectant

- Alcohol Based Disinfectant

- Others

Alcohol based disinfectants captured the largest segment of the India disinfectant market, representing 48.7% of the total market share in 2025.

The portability, ease of application, and minimal residue have increased adoption across healthcare facilities, corporate offices, and public spaces. Furthermore, regulatory approvals and endorsements for infection control have further strengthened their market leadership, making them the preferred choice among hospitals and hygiene-conscious consumers.

Rising awareness of hygiene and the frequency of sanitisation practices are significantly driving demand for alcohol-based disinfectants. A study in Himachal Pradesh found high hand hygiene awareness: 87.6% of participants understood its disease-prevention benefits, 84.3% recognized critical handwashing occasions, and 77.6% knew the recommended 20-second handwashing duration. These products are increasingly being incorporated into hand sanitizers, surface cleaners, and wipes. Additionally, government campaigns promoting hand hygiene and infection prevention in healthcare and community settings have amplified usage. The versatility, proven efficacy, and convenience of alcohol-based disinfectants ensure sustained market dominance over alternative types.

Formulation Insights:

- Liquid

- Wipes

- Spray

- Others

Liquid dominates with a market share of 63.2% of the total India disinfectant market in 2025.

They are widely utilized in healthcare institutions, hospitality, educational facilities, and industrial environments. The compatibility of liquid disinfectants with various dispensing systems and cleaning routines enhances operational efficiency, supporting institutional end-users' bulk purchasing strategies. Their high effectiveness in reducing microbial load further reinforces preference over gels, sprays, and wipes.

The liquid form also facilitates precise concentration control and is adaptable for multiple purposes, including floor, surface, and instrument disinfection. Manufacturers are increasingly innovating liquid formulations with enhanced stability, longer shelf life, and eco-friendly components. This adaptability, combined with established distribution channels and institutional adoption, ensures continued dominance and strong market growth for liquid disinfectants in India.

End-User Insights:

Access the comprehensive market breakdown Request Sample

- Healthcare Providers

- Commercial Users

- Domestic Users

- Others

Healthcare Providers leads with a share of 41.5% of the total India disinfectant market in 2025.

High patient volumes, surgical procedures, and regular sterilization requirements amplify disinfectant demand. The necessity to maintain patient safety, comply with regulatory norms, and prevent hospital-acquired infections positions healthcare providers as the primary market segment for disinfectant products.

Hospitals and clinics prioritize effective, rapid-acting disinfectants to minimize cross-contamination risks. Partnerships with established disinfectant manufacturers and bulk procurement strategies enhance operational efficiency. For example, in June 2025, Solenis planned to acquire NCH Corporation, combining water treatment and hygiene solutions, including disinfectants and cleaners, to create a diversified, global leader offering sustainable, digital, and customer-centric solutions across industrial, commercial, and middle-market sectors. Furthermore, government initiatives promoting hospital hygiene and accreditation requirements reinforce healthcare facilities’ reliance on disinfectants, sustaining their position as the leading end-user segment in India.

Distribution Channel Insights:

- B2B

- Retail Outlets

- Online Sales Channel

- Others

B2B dominates with a market share of 52.6% of the total India disinfectant market in 2025.

Strong relationships between suppliers and corporate or institutional buyers streamline supply chains, ensuring consistent availability. Bulk purchasing agreements and contract-based sales models enhance market penetration, providing cost advantages and reinforcing B2B as the primary channel.

Businesses increasingly prefer B2B channels due to reliability, standardized product quality, and comprehensive service support. Suppliers offer tailored solutions including scheduled deliveries, bulk discounts, and after-sales technical assistance. This structured approach strengthens long-term partnerships, ensuring sustained market share for the B2B distribution channel over retail or online alternatives.

Region Insights:

- North India

- South India

- East India

- West India

West India exhibits a clear dominance with a 30.9% share of the total India disinfectant market in 2025.

West India holds the largest regional share due to the concentration of industrial hubs, commercial centers, and urban populations. Accordingly, Maharashtra, India’s second-most populous state, shows varied urbanization: Mumbai and Mumbai Suburban are fully urban, Gadchiroli and Sindhudurg under 15% urban, and Greater Mumbai UA, the largest in India, has 18.41 million, with six UAs above one million. High awareness regarding hygiene, coupled with significant institutional demand from hospitals, offices, and manufacturing plants, further drives market growth.

Infrastructure development and urbanization have amplified the adoption of disinfectants in both public and private sectors, consolidating West India’s dominance. Additionally, the presence of key distributors, logistical infrastructure, and regional manufacturing facilities enhances product availability and supply chain efficiency. Moreover, favorable government health initiatives and corporate sanitation mandates promote widespread usage of disinfectants.

Market Dynamics:

Growth Drivers:

Why is the India Disinfectant Market Growing?

Expansion of the Hospitality and Tourism Sector

The rapid growth of hotels, resorts, and other tourism facilities in India is driving demand for disinfectants. As such, India’s Union Budget FY26 allocated INR 2,541.06 Crore (USD 291.07 Million) to boost tourism, enhancing infrastructure, skills, connectivity, e-visa access, developing 50 top destinations, and providing MUDRA loans for homestay expansion. In tandem, establishments are implementing stringent hygiene protocols to ensure guest safety, especially post-pandemic. This is leading to increased adoption of high-quality disinfectants across lobbies, restaurants, and guest rooms. Moreover, rising consumer expectations for sanitized environments are encouraging hotels to maintain continuous disinfection.

Increasing Adoption in Public Transportation and Mass Transit Systems

The Indian government and private operators are prioritizing cleanliness in trains, buses, and metro networks to curb disease transmission. Regular disinfection of high-touch surfaces such as handrails, seats, and ticket counters is becoming standard practice. This trend boosts demand for both liquid and spray disinfectants suitable for large-scale applications. Public awareness campaigns emphasizing safe commuting and hygiene have further accelerated disinfectant adoption, making mass transit systems an important growth driver for the national market. For example, the Swachhata Hi Seva 2025 campaign, led by MoSPI, transformed 52 CTUs, cleaned 104 public spaces, held health camps, and engaged 2,500+ volunteers in Shramdaan, promoting cleanliness, hygiene, preventive healthcare, and environmental stewardship nationwide.

Surge in Institutional Bulk Procurement Contracts

Large-scale institutional procurement has become a key trend in the Indian disinfectant market, driven by hospitals, manufacturing units, and educational institutions. Bulk purchase agreements provide cost efficiencies, uninterrupted supply, and long-term partnerships with manufacturers. Institutions are increasingly standardizing disinfectant brands and formulations to ensure uniform hygiene protocols. This trend is further reinforced by government-led initiatives promoting sanitized environments and regulatory frameworks mandating stringent infection prevention measures, strengthening institutional reliance on organized, high-volume disinfectant supply chains.

Market Restraints:

What Challenges the India Disinfectant Market is Facing?

High Raw Material Costs and Supply Chain Volatility

Fluctuating prices of key ingredients such as ethanol, isopropyl alcohol, and chemical additives increase production costs for disinfectant manufacturers. Supply chain disruptions due to import dependencies, transportation delays, and regulatory restrictions further complicate consistent supply. Smaller manufacturers often struggle to absorb these cost variations, impacting profit margins. As a result, pricing pressures and occasional product shortages limit widespread market expansion, particularly in price-sensitive segments such as small healthcare facilities and retail outlets.

Strict Regulatory Compliance and Certification Requirements

Disinfectant products in India must comply with stringent regulatory standards set by agencies such as the CDSCO and FSSAI for formulation, labeling, and efficacy testing. Obtaining necessary approvals and certifications is time-consuming and costly, particularly for new entrants. Non-compliance can result in product recalls, fines, or bans, discouraging smaller manufacturers. This regulatory complexity slows market entry and innovation, creating barriers for new product development despite growing demand across healthcare, hospitality, and industrial sectors.

Consumer Awareness and Misuse Concerns

Despite growing demand, a significant portion of consumers lack proper knowledge of disinfectant usage, dilution, and storage guidelines. Overuse or incorrect application may lead to reduced efficacy, surface damage, or health hazards, affecting consumer trust. Misconceptions regarding effectiveness against specific pathogens or bacteria also hinder adoption in some residential and small commercial settings. Manufacturers must invest in education campaigns and clear labeling, but persistent misuse concerns continue to challenge consistent market growth and long-term customer retention.

Competitive Landscape:

The competitive landscape of the India disinfectant market is characterized by the presence of both domestic manufacturers and multinational corporations striving for market leadership through product innovation, cost optimization, and brand recognition. Companies focus on expanding production capacities, developing specialized formulations for healthcare, commercial, and industrial applications, and strengthening distribution networks across B2B and B2C channels. Likewise, strategic partnerships, mergers, and acquisitions are increasingly common to enhance geographic reach and technological capabilities. Moreover, pricing strategies, regulatory compliance, and sustainability initiatives further differentiate players, fostering intense competition while encouraging continuous improvement in quality, efficiency, and market responsiveness.

Recent Developments:

- In September 2025, IIT Madras-incubated startup JSP Enviro deployed its BEADS wastewater treatment system in Tamil Nadu industries. The oxygen-free, electrode-assisted technology reduces electricity, chemical use, and sludge, recovers energy, lowers CO₂ emissions, and offers cost savings, proving sustainable, profitable wastewater management with potential for nationwide and global expansion.

- In June 2025, HUL’s Vim UltraPro Floor Cleaner revolutionized home cleaning in India by using probiotics and Surface Modification technology. The natural bacteria activate on dirt, provide long-lasting cleanliness, remove tough stains, reduce odors, and release soothing fragrances, offering an effective, sustainable, and consumer-friendly solution for modern households.

India Disinfectant Market Report Coverage:

|

Report Features |

Details |

|

Base Year of the Analysis |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Units |

Million USD |

|

Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

|

Types Covered |

Quaternary Ammonium Compound, Aqueous Ozone Disinfectant, Alcohol Based Disinfectant, Others |

|

Formulation Covered |

Liquid, Wipes, Spray, Others |

|

End-Users Covered |

Healthcare Providers, Commercial Users, Domestic Users, Others |

|

Distribution Channels Covered |

B2B, Retail Outlets, Online Sales Channel, Others |

|

Regions Covered |

North India, South India, East India, West India |

|

Customization Scope |

10% Free Customization |

|

Post-Sale Analyst Support |

10-12 Weeks |

|

Delivery Format |

PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Disinfectant Market Report

The India disinfectant market size was valued at USD 1,413.4 Million in 2025.

The India disinfectant market is expected to grow at a compound annual growth rate of 11.07% from 2026-2034 to reach USD 3,810.5 Million by 2034.

Alcohol Based Disinfectant dominated the market with 48.7% share in 2025, driven by their wide usage across healthcare, commercial, and household sectors due to effectiveness, fast action, and easy availability.

Key factors driving the India disinfectant market include rising hygiene awareness, increased healthcare infrastructure, pandemic-driven demand, government initiatives promoting sanitation, expanding commercial and residential cleaning needs, and growing adoption in industrial, hospitality, and public sectors.

Major challenges in the India disinfectant market include high chemical costs, inconsistent quality of unbranded products, supply chain disruptions, limited awareness in rural areas, regulatory compliance hurdles, and competition from traditional cleaning methods.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)