India Docetaxel Market Size, Share, Trends and Forecast by Indication, Distribution Channel, and Region, 2026-2034

India Docetaxel Market Summary:

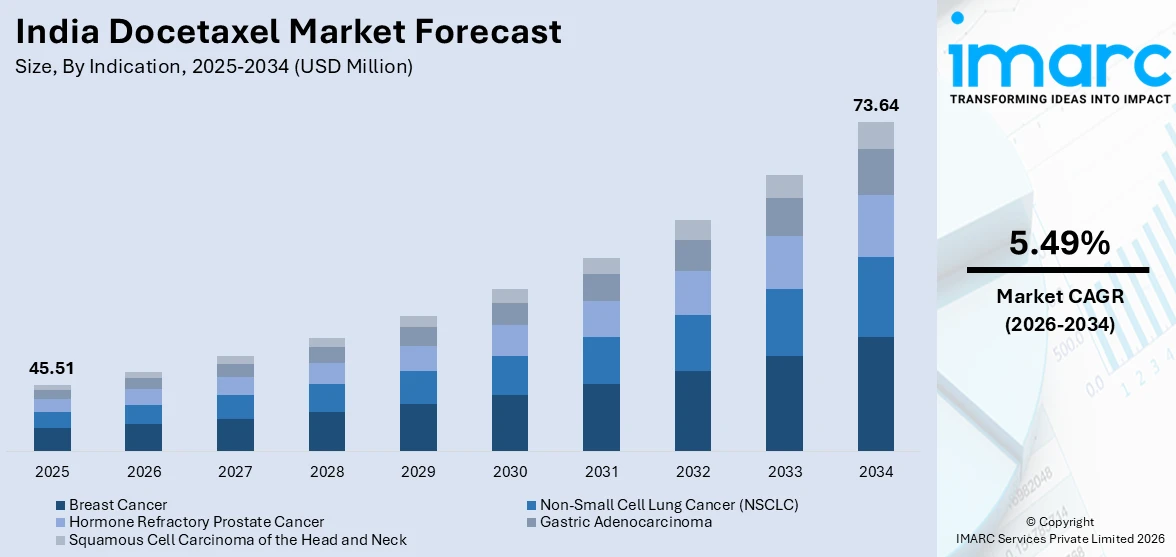

The India docetaxel market size reached USD 45.51 Million in 2025. The market is projected to reach USD 73.64 Million by 2034, growing at a CAGR of 5.49% during 2026-2034. The market is driven by the escalating cancer burden across India, particularly breast cancer and non-small cell lung cancer cases, the expansion of government-funded healthcare infrastructure providing accessible treatment through initiatives like Ayushman Bharat and Day Care Cancer Centres, and the proliferation of affordable generic docetaxel formulations from domestic pharmaceutical manufacturers. These factors are collectively expanding the India docetaxel market share.

|

Report Attribute

|

Key Statistics

|

|---|---|

| Market Size in 2025 | USD 45.51 Million |

| Market Forecast in 2034 | USD 73.64 Million |

| Market Growth Rate (2026-2034) | 5.49% |

| Key Segments | Indication (Breast Cancer, Non-Small Cell Lung Cancer (NSCLC), Hormone Refractory Prostate Cancer, Gastric Adenocarcinoma, Squamous Cell Carcinoma of the Head and Neck), and Distribution Channel (Hospital Pharmacy, Retail Pharmacy, Others) |

|

Base Year

|

2025

|

|

Forecast Years

|

2026-2034

|

India Docetaxel Market Outlook (2026-2034):

The India docetaxel market growth driven by rising cancer incidence rates particularly among urban and aging populations, ongoing government healthcare reforms emphasizing cancer care accessibility, and increasing adoption of combination chemotherapy protocols in oncology treatment centers. The establishment of Day Care Cancer Centres across district hospitals and expansion of Ayushman Bharat coverage will enhance treatment access for economically disadvantaged patients. Additionally, continuous investments by domestic pharmaceutical companies in quality manufacturing and competitive pricing strategies will support market penetration in tier-two and tier-three cities, ensuring sustained demand throughout the forecast period.

To get more information on this market Request Sample

Impact of AI:

Artificial intelligence is revolutionizing cancer treatment protocols in India through improved diagnostic accuracy, personalized medicine approaches, and accelerated drug development pipelines. The IndiaAI-National Cancer Grid partnership's Cancer AI & Technology Challenge Grant Program, launched in August 2025, is fostering innovation in cancer screening and management systems. Leading pharmaceutical companies are integrating AI-driven technologies for biomarker discovery, treatment response prediction, and drug formulation optimization, enhancing the efficacy and safety profiles of chemotherapy agents like docetaxel while reducing development timelines and improving patient outcomes across India's diverse healthcare landscape.

Market Dynamics:

Key Market Trends & Growth Drivers:

Escalating National Cancer Burden Intensifying Chemotherapy Demand

India is witnessing a sharp increase in cancer prevalence, creating strong demand for chemotherapy agents such as docetaxel. The country’s growing cancer burden is driven by rapid urbanization, environmental pollution, unhealthy dietary patterns, and an aging population. Rising incidences of breast, lung, and prostate cancers are significantly contributing to the growing number of patients requiring active treatment. Late diagnosis remains a major challenge, with a large proportion of patients presenting at advanced stages, necessitating prolonged and intensive chemotherapy regimens. As a first-line treatment for several cancer types, docetaxel plays a critical role in improving survival outcomes and managing disease progression. The expansion of diagnostic programs and increased awareness are leading to higher detection rates, thereby expanding the patient base for chemotherapy. Government health initiatives focusing on cancer prevention, early screening, and improved treatment access are further contributing to rising chemotherapy utilization. The increasing establishment of oncology centers across urban and semi-urban regions is improving treatment accessibility and consistency in care delivery. Collectively, these factors are driving sustained growth in docetaxel demand, making it a key component of India’s evolving oncology treatment landscape amid escalating cancer incidences nationwide.

Comprehensive Government Healthcare Infrastructure Expansion and Financial Support Mechanisms

The Indian government is implementing large-scale healthcare reforms aimed at strengthening cancer treatment accessibility, affordability, and infrastructure across the country. Substantial budget allocations to the health sector are facilitating the establishment of specialized facilities and improved cancer care delivery systems. The creation of district-level cancer care units and expanded chemotherapy facilities is enabling broader treatment reach beyond urban centers. Financial support mechanisms, including government-funded insurance schemes and direct medical aid programs, are reducing the economic burden associated with cancer treatment. These initiatives ensure that patients from lower-income groups can access essential chemotherapy medicines such as docetaxel without significant financial strain. Tax exemptions and duty reductions on life-saving drugs have made treatment more affordable and accessible across healthcare institutions. The establishment of regional and state cancer institutes enhances treatment capacity while standardizing quality and protocols across the nation. By integrating cancer care within national health frameworks, the government is fostering a comprehensive ecosystem that supports prevention, diagnosis, and therapy. These efforts are collectively strengthening the docetaxel market by improving accessibility, affordability, and the overall availability of chemotherapy services in India’s public and private healthcare systems.

Proliferation of Cost-Effective Generic Docetaxel Manufacturing and Distribution Network

India’s advanced pharmaceutical manufacturing sector has become a cornerstone for the production and supply of cost-effective generic docetaxel formulations. The country’s strong industrial infrastructure and adherence to global quality standards have positioned it as a leading hub for affordable chemotherapy drugs. The competitive generic landscape following patent expirations has driven substantial price reductions, improving affordability for both domestic and international markets. This cost efficiency ensures that patients across different economic segments have access to essential cancer medications. A well-established network of pharmaceutical facilities spread across major industrial regions supports consistent production, timely distribution, and reliable supply to hospitals and retail pharmacies. Government initiatives promoting generic medicine availability through public healthcare outlets are further enhancing access to affordable chemotherapy options. Domestic production capabilities have also strengthened India’s export potential, contributing to global healthcare affordability while ensuring sufficient supply for the local market. The focus on maintaining high manufacturing standards, coupled with effective distribution channels, supports continuous market stability. This widespread accessibility of quality-assured, low-cost docetaxel formulations underpins the steady expansion of India’s chemotherapy drug industry, aligning with the country’s broader objective of delivering affordable cancer care to all population segments.

Key Market Challenges:

Pharmaceutical Supply Chain Vulnerabilities and Manufacturing Quality Control Deficiencies

The India docetaxel market confronts significant challenges stemming from supply chain fragilities and manufacturing quality assurance gaps that periodically disrupt treatment availability and compromise patient care continuity. India's pharmaceutical industry, while being the largest global supplier of generic finished-drug products, sources over 70 percent of its Active Pharmaceutical Ingredients from China, creating substantial dependency risks. Geopolitical tensions, natural disasters, pandemic-related disruptions, and trade policy changes in China directly impact API availability for Indian docetaxel manufacturers, leading to production interruptions and supply shortages. The 2023 global chemotherapy shortage was precipitated when the U.S. Food and Drug Administration shuttered an Indian generics manufacturer following quality standard violations, demonstrating how manufacturing compliance failures can cascade into widespread treatment disruptions. Quality control issues including contamination concerns, sterility failures, and deviation from Good Manufacturing Practice standards have resulted in periodic FDA import alerts and regulatory actions against Indian pharmaceutical facilities, temporarily removing production capacity from the market. The complex multi-step synthesis required for docetaxel production, involving chiral synthesis, hydrogenation, purification, and chromatographic separation, demands sophisticated manufacturing infrastructure and highly trained personnel, which smaller manufacturers may struggle to maintain consistently.

Economic Pressures and Insufficient Commercial Incentives for Sustained Generic Chemotherapy Production

The India docetaxel market operates within a challenging economic framework where extremely low profit margins on generic chemotherapy drugs create persistent commercial disincentives for manufacturers, threatening long-term market sustainability and supply reliability. Generic docetaxel formulations, despite being essential life-saving medications, command minimal pricing power in India's highly price-sensitive healthcare environment, with hospital procurement systems and government tenders driving aggressive price competition among manufacturers. The cost of producing pharmaceutical-grade docetaxel involves substantial capital investments in specialized HPAPI containment facilities, high-precision chemical reactors, chiral synthesis equipment, hydrogenation autoclaves, and preparative HPLC chromatography systems, alongside ongoing operational expenditures for raw materials, utilities, specialized labor, quality control testing, and regulatory compliance documentation. Raw material procurement, particularly the natural taxane core derived from specific plant sources and complex synthetic side chain precursors, represents the largest variable cost component with pricing volatility linked to global commodity markets. The requirement for stringent Good Manufacturing Practice compliance, environmental controls, solvent recovery systems, and waste disposal protocols adds substantial fixed and variable costs to docetaxel production. However, market pricing for generic docetaxel in India remains suppressed at levels often below international benchmarks, with intense competition from multiple domestic manufacturers and government price control mechanisms limiting revenue potential.

Late-Stage Cancer Diagnosis Patterns Limiting Optimal Treatment Outcomes

The India docetaxel market's growth potential and therapeutic effectiveness are significantly constrained by persistent patterns of late-stage cancer diagnosis that reduce treatment success rates, increase mortality, and create suboptimal utilization of chemotherapy resources. Approximately 60 percent of breast cancer cases in India present at stages three or four, compared to substantially lower proportions in high-income countries where early detection programs achieve predominantly stage one and two diagnoses. Similar patterns exist across lung, prostate, gastric, and head and neck cancers, with majority of patients seeking medical attention only after symptomatic progression indicating advanced disease. This delayed presentation stems from multifaceted barriers including limited awareness about cancer symptoms and screening importance, particularly among rural and less-educated populations, cultural stigma surrounding cancer diagnosis, geographical barriers to healthcare access in remote regions, economic constraints preventing timely medical consultations, and inadequate primary healthcare infrastructure for early detection and referral. Women in India often lack knowledge about breast self-examination, clinical breast examination, and mammography benefits, resulting in breast cancer detection occurring at median younger ages with more aggressive biological characteristics compared to Western populations. The five-year survival rate for stage one breast cancer in India approaches 93.3 percent, while stage four survival plummets to merely 24.5 percent, dramatically illustrating the prognostic impact of diagnosis timing. For patients presenting with advanced-stage disease, docetaxel and combination chemotherapy regimens face inherent limitations in achieving curative outcomes, often shifting treatment intent from cure to palliation with reduced survival benefits.

India Docetaxel Market Report Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the India docetaxel market, along with forecasts at the country and regional levels for 2026-2034. The market has been categorized based on indication and distribution channel.

Analysis by Indication:

- Breast Cancer

- Non-Small Cell Lung Cancer (NSCLC)

- Hormone Refractory Prostate Cancer

- Gastric Adenocarcinoma

- Squamous Cell Carcinoma of the Head and Neck

The report has provided a detailed breakup and analysis of the market based on the indication. This includes breast cancer, non-small cell lung cancer (NSCLC), hormone refractory prostate cancer, gastric adenocarcinoma, and squamous cell carcinoma of the head and neck.

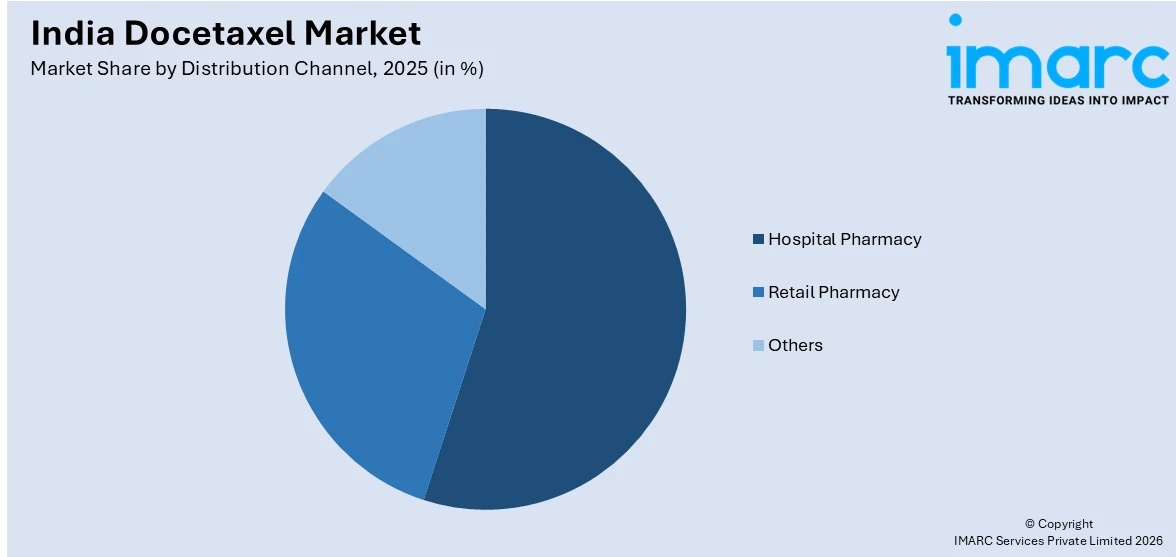

Analysis by Distribution Channel:

Access the comprehensive market breakdown Request Sample

- Hospital Pharmacy

- Retail Pharmacy

- Others

A detailed breakup and analysis of the market based on the distribution channel have also been provided in the report. This includes hospital pharmacy, retail pharmacy, and others.

Analysis by Region:

- North India

- South India

- East India

- West India

The report has also provided a comprehensive analysis of all the major regional markets, which include North India, South India, East India, and West India.

Competitive Landscape:

The India docetaxel market exhibits a moderately fragmented competitive structure characterized by presence of multiple domestic pharmaceutical manufacturers offering generic formulations alongside limited international players. Competition centers on pricing strategies, regulatory compliance credentials, distribution network reach, and quality certifications, with manufacturers striving to secure hospital procurement contracts and government supply agreements. Leading Indian pharmaceutical companies including Dr. Reddy's Laboratories, Sun Pharma, Cipla, Fresenius Kabi India, and Natco Pharma maintain significant market positions through established manufacturing capabilities, WHO-GMP certified facilities, and extensive distribution partnerships. Mid-sized manufacturers such as Florencia Healthcare, Panacea Biotec, and regional players compete aggressively on price points while emphasizing quality standards. The market dynamics favor companies with robust regulatory track records, diversified product portfolios, and strong relationships with major oncology hospitals and cancer treatment centers.

India Docetaxel Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Indications Covered | Breast Cancer, Non-Small Cell Lung Cancer (NSCLC), Hormone Refractory Prostate Cancer, Gastric Adenocarcinoma, Squamous Cell Carcinoma of the Head and Neck |

| Distribution Channels Covered | Hospital Pharmacy, Retail Pharmacy, Others |

| Regions Covered | North India, South India, East India, West India |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC's industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the India docetaxel market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the India docetaxel market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the India docetaxel industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the India Docetaxel Market Report

The India docetaxel market reached a value of USD 45.51 Million in 2025.

The market is projected to grow at a CAGR of 5.49% during 2026-2034, reaching USD 73.64 Million by 2034.

Key growth drivers include rising cancer incidence rates, expanding government healthcare programs, cost-effective domestic generic manufacturing, and increased oncology center accessibility across India.

The report covers segmentation by indication, distribution channel, and region. Each segment includes detailed market size and forecast analysis.

Key trends include usage of artificial intelligence (AI)-driven cancer diagnostics, combination chemotherapy protocol adoption, personalized medicine integration, and expansion of oncology treatment infrastructure across India.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)