India Drug Delivery Devices Market Size, Share, Trends and Forecast by Route of Administration, Application, End User, and Region, 2026-2034

India Drug Delivery Devices Market Size, Share, Trends & Forecast (2026-2034)

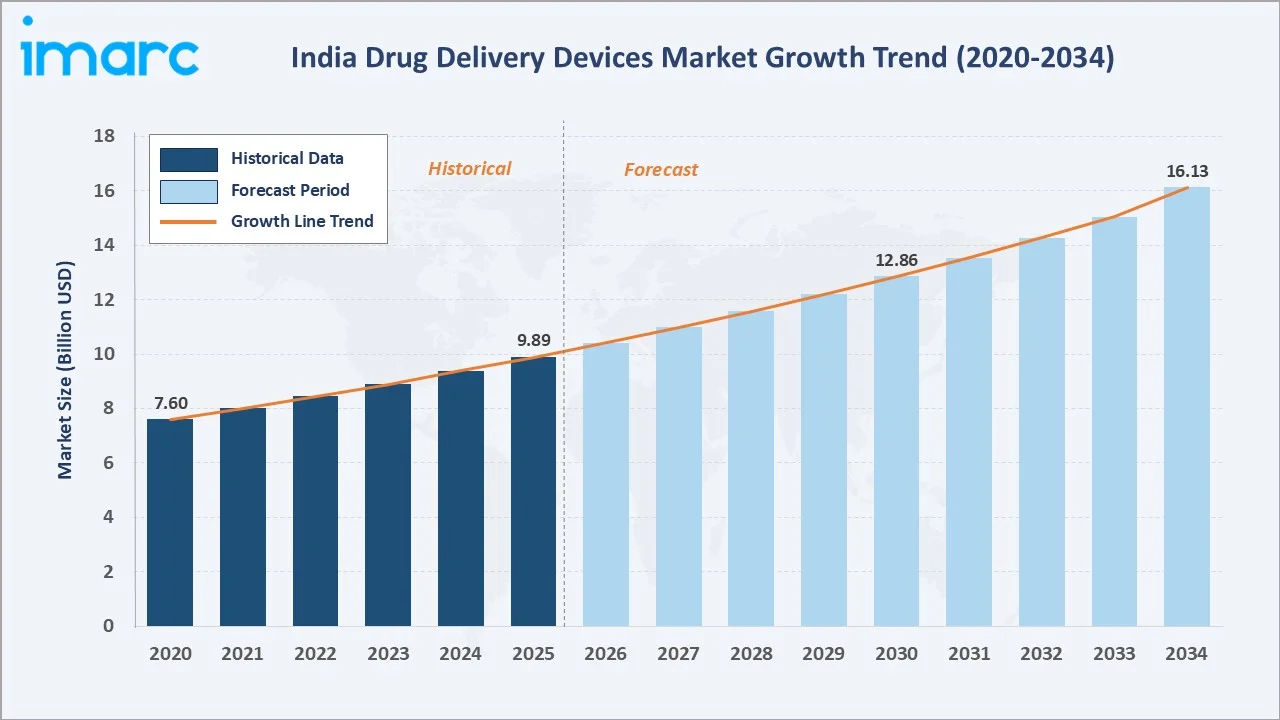

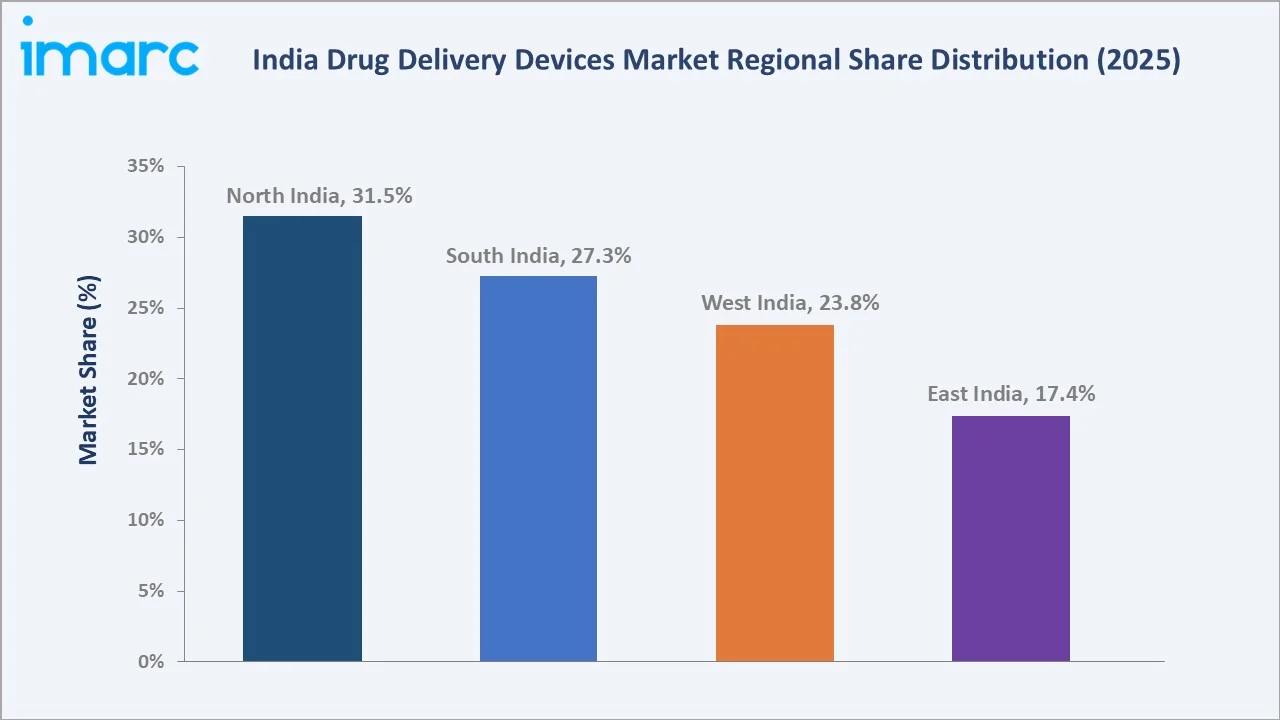

The India drug delivery devices market reached USD 9.89 Billion in 2025 and is projected to reach USD 16.13 Billion by 2034, growing at a CAGR of 5.39% during 2026-2034. Rising chronic disease burden, pharmaceutical sector expansion, government healthcare schemes, and growing adoption of smart and non-invasive delivery technologies are driving the market. North India leads regionally with a 31.5% share in 2025.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 9.89 Billion |

|

Forecast Market Size (2034) |

USD 16.13 Billion |

|

CAGR (2026-2034) |

5.39% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

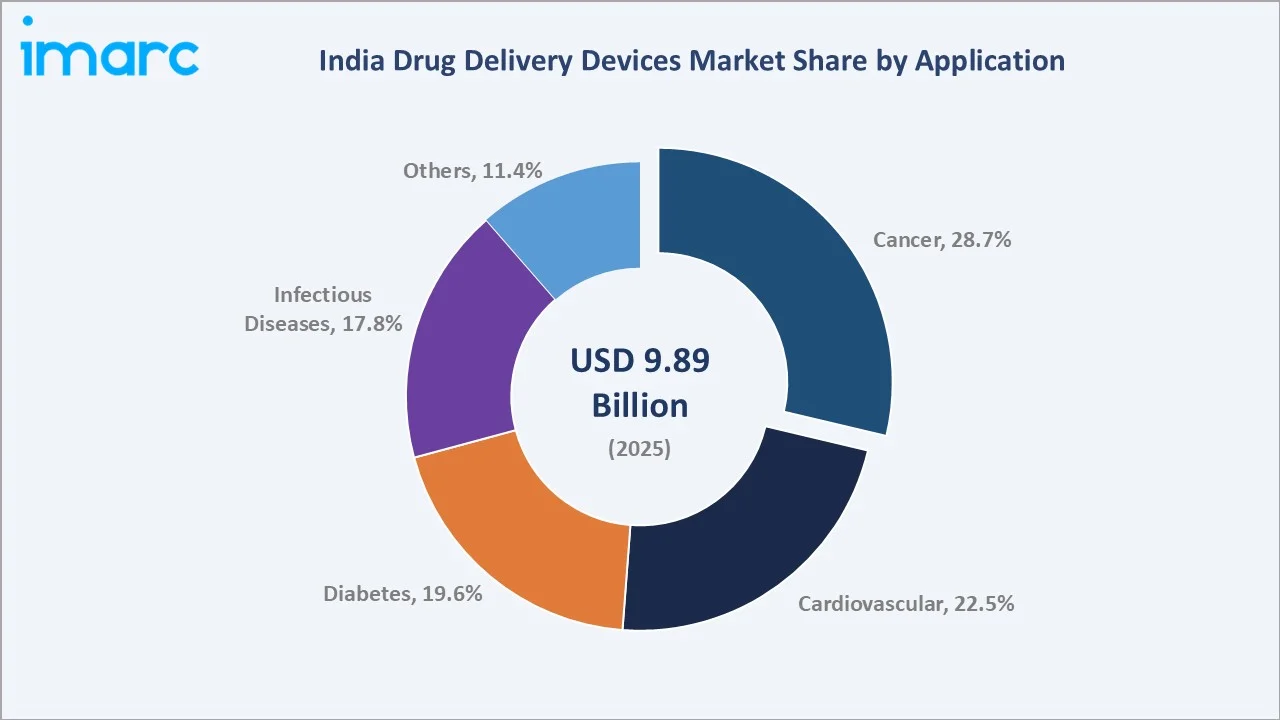

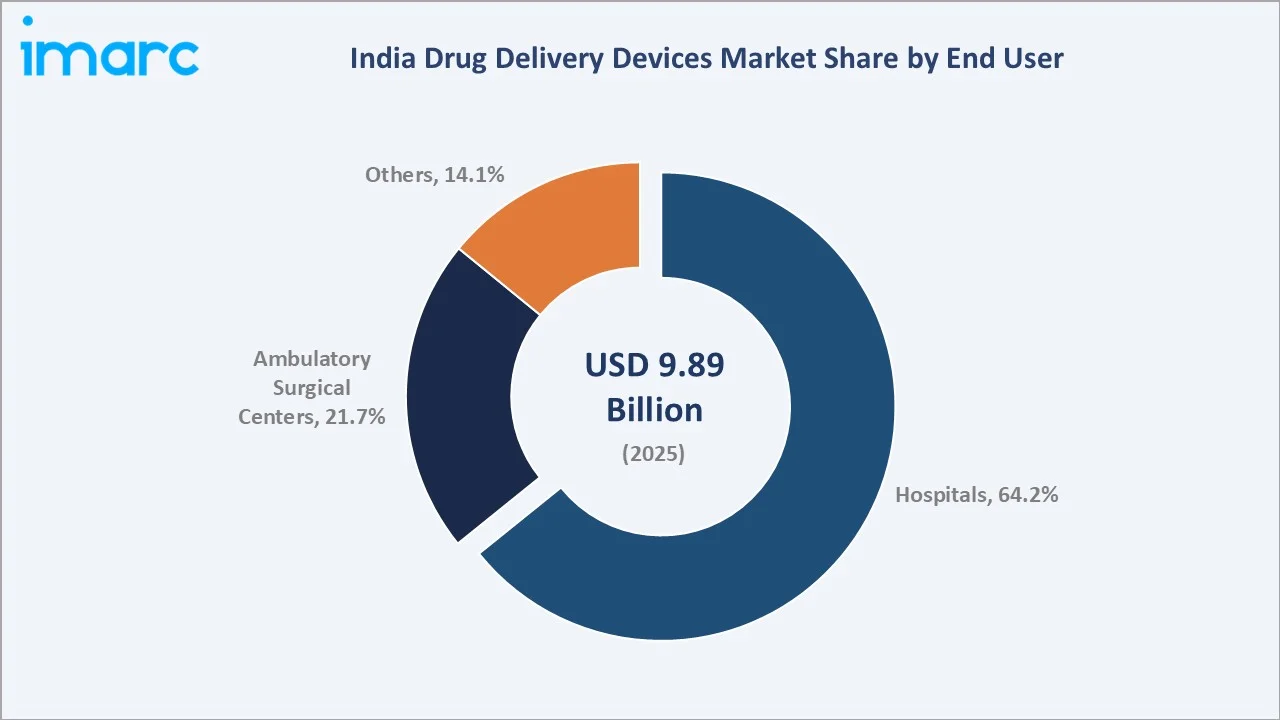

Cancer leads the application segment with a 28.7% share in 2025, driven by India’s rising oncology burden and complex drug regimen requirements. Hospitals dominate end-user demand at 64.2%, reflecting high patient volumes and advanced infusion infrastructure across tertiary care facilities.

To get more information on this market, Request Sample

The market grew steadily from USD 7.60 Billion in 2020 to USD 9.89 Billion in 2025, driven by chronic disease burden, PLI incentives, and smart device adoption. The forecast to USD 16.13 Billion by 2034 is reinforced by digital health integration and sustained pharma sector investment.

Executive Summary

India’s drug delivery devices market is expanding at a steady 5.39% CAGR, supported by a rising non-communicable disease burden, a maturing pharma manufacturing ecosystem, and progressive government policy. The market grew from USD 7.60 Billion in 2020 to USD 9.89 Billion in 2025 and is forecast to reach USD 16.13 Billion by 2034, generating USD 6.24 Billion in incremental value.

Cancer retains the top application share at 28.7% in 2025, as cancer incidence in India is expected to reach approximately 2.46 million cases by 2045. Cardiovascular (22.5%) and diabetes (19.6%) reflect India’s double burden of non-communicable diseases. Hospitals command 64.2% of end-user demand. Ambulatory surgical centers at 21.7% are the fastest-growing segment as outpatient care decentralization accelerates.

North India leads regionally at 31.5%, anchored by Delhi-NCR’s super-specialty hospital density. South India (27.3%) benefits from its biotech-pharma manufacturing corridor in Hyderabad and Bengaluru. Key players, including Becton, Dickinson and Company and Medtronic, are intensifying investments in smart, connected, and needle-free delivery systems.

Key Market Insights

|

Insight |

Data |

|

Largest Application |

Cancer – 28.7% share (2025) |

|

Second Application |

Cardiovascular – 22.5% share (2025) |

|

Largest End User |

Hospitals – 64.2% share (2025) |

|

Fastest Growing End User |

Ambulatory Surgical Centers – ~6.8% CAGR (2026-2034) |

|

Leading Region |

North India – 31.5% share (2025) |

|

Top Companies |

Becton, Dickinson and Company, Medtronic, Baxter International, Inc., B. Braun SE |

Key Analytical Observations:

- Cancer at 28.7% (2025) leads applications as, according to GCO estimates, cancer incidence in India is expected to reach approximately 2.46 million cases by 2045, driving demand for targeted infusion pumps, drug-eluting stents, and precision injectable delivery systems in oncology departments.

- Hospitals at 64.2% (2025) dominate end-user demand due to high patient volumes, complex parenteral protocols, and mandated certified delivery devices. Tertiary care expansion under Ayushman Bharat directly adds hospital-based device consumption.

- North India’s 31.5% regional share reflects Delhi-NCR super-specialty hospital density, UP pharma manufacturing clusters, and the highest organized-sector outpatient traffic of any Indian region in 2025.

- Ambulatory surgical centers at ~6.8% CAGR through 2034 are the fastest-growing end-user segment, as same-day surgery trends shift chemotherapy infusions, insulin pump management, and post-operative drug delivery away from inpatient settings.

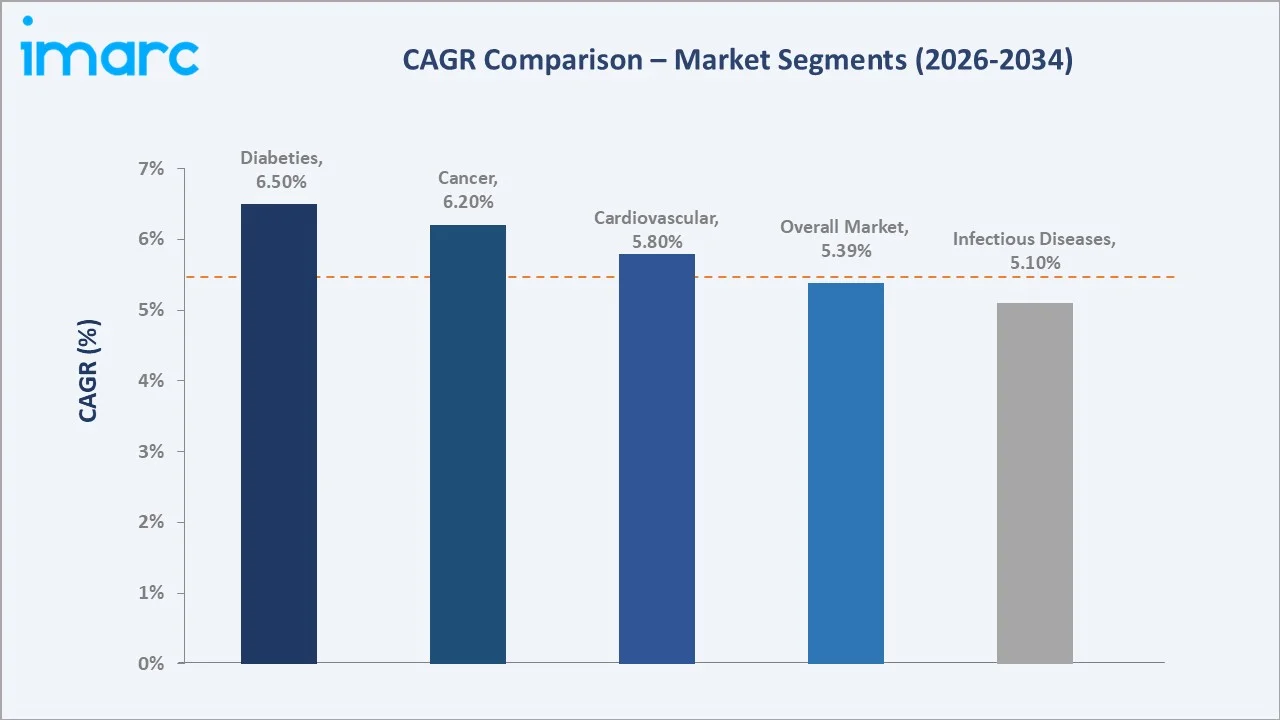

- Diabetes at 19.6% is driven by IDF’s projection of 92 million Indian diabetic patients by 2030, sustaining insulin pen, pre-filled syringe, and continuous delivery device demand throughout the forecast period.

- The overall market’s 5.39% CAGR through 2034 is underpinned by PLI scheme incentives for domestic device manufacturing, reducing import dependence and building a cost-competitive local supply chain for both basic and advanced delivery formats.

India Drug Delivery Devices Market Overview

Drug delivery devices are medical instruments that administer pharmaceutical compounds in precise, controlled doses via injectable, oral, topical, pulmonary, ocular, and transdermal routes. India’s market spans syringes, infusion pumps, auto-injectors, inhalers, transdermal patches, and implantable devices.

India’s PLI scheme for medical devices (INR 3,420 crore) is catalyzing domestic advanced delivery manufacturing, reducing import dependence. Ayushman Bharat PM-JAY is the world’s largest health assurance scheme, providing annual health coverage of INR 5 lakh per family for secondary and tertiary care hospitalization. The scheme covers over 12 crore poor and vulnerable families, representing nearly 55 crore beneficiaries from the bottom 40% of India’s population.

Market Dynamics

To evaluate market opportunities, Request Sample

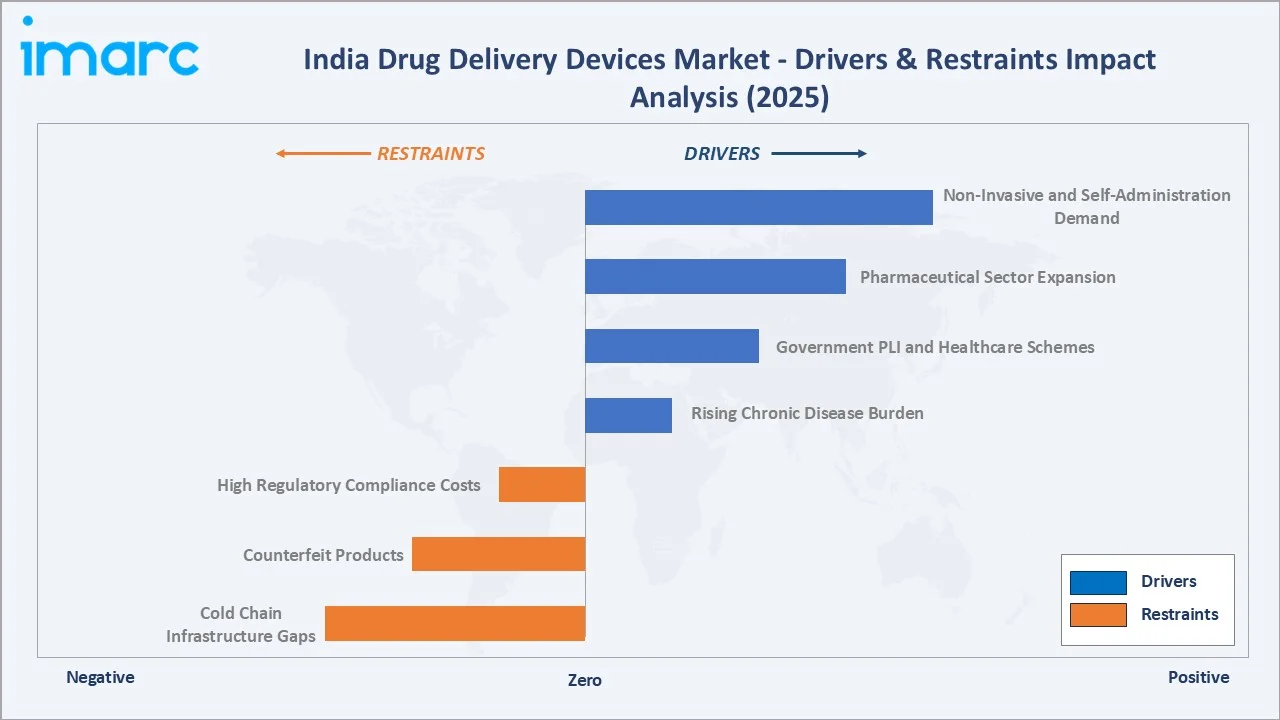

Market Drivers

- Rising Chronic Disease Burden: India’s non-communicable diseases account for over 60% of total mortality. IDF projects 92 million diabetic patients by 2030. Cancer incidence exceeded 1.46 million new cases in 2022, sustaining demand for oncology, cardiac, and diabetes drug delivery systems.

- Government PLI and Healthcare Schemes: The INR 3,420 crore PLI scheme incentivizes production of 4 priority device categories. Ayushman Bharat PM-JAY provides coverage to more than 12 crore poor and vulnerable families, benefiting nearly 55 crore people who represent the bottom 40% of India’s population.

- Pharmaceutical Sector Expansion: According to the Economic Survey 2025–26, the sector’s annual turnover reached INR 4.72 lakh crore in FY25, while exports expanded at a CAGR of 7% over the last decade, from FY15 to FY25. Each biologic launch requires validated delivery systems. Wearable injectors, needle-free systems, and smart pumps are gaining clinical traction as biologic pipelines expand.

- Non-Invasive and Self-Administration Demand: Patient preference for home care drives auto-injector and transdermal patch adoption. Needle-free systems eliminate needle-stick injuries and improve compliance in pediatric and elderly populations.

Market Restraints

- High Regulatory Compliance Costs: Central Drugs Standard Control Organization (CDSCO) Class C and D device approvals, alongside Medical Device Rules, 2017 certification, require significant investment. Small domestic manufacturers face disproportionate compliance burdens that restrict portfolio breadth and slow time-to-market.

- Counterfeit Products: CDSCO estimates up to 12% of devices in circulation may be non-compliant. Counterfeit syringes and IV sets in rural distribution channels erode pricing power and create patient safety risks.

- Cold Chain Infrastructure Gaps: Biologic delivery systems require cold-chain storage 2–8°C. Rural and semi-urban infrastructure gaps limit the distribution of temperature-sensitive device-drug combinations.

Market Opportunities

- Smart Connected Delivery Systems: IoT and mobile health integration enables real-time adherence monitoring and telemedicine. The Indian digital health market reached USD 19.14 Billion by 2025, driving connected inhalers, smart insulin pens, and app-enabled infusion pump adoption.

- Nanotechnology and Targeted Delivery: Nanoparticle systems enable site-specific oncology drug release. Sun Pharma and Cipla are investing in nanoformulation, creating demand for precision delivery devices validated for nano-drug administration.

Market Challenges

- Price Sensitivity: India’s device market is highly price-competitive, with L1 pricing in public tenders creating margin pressure on smart devices. Government facilities, accounting for 35%+ of institutional volumes, slow premium product adoption.

- Evolving Regulatory Environment: MDR 2017 and subsequent 2020 and 2023 amendments require ongoing compliance recalibration. Foreign companies must re-register India-specific SKUs under evolving CDSCO norms.

Emerging Market Trends

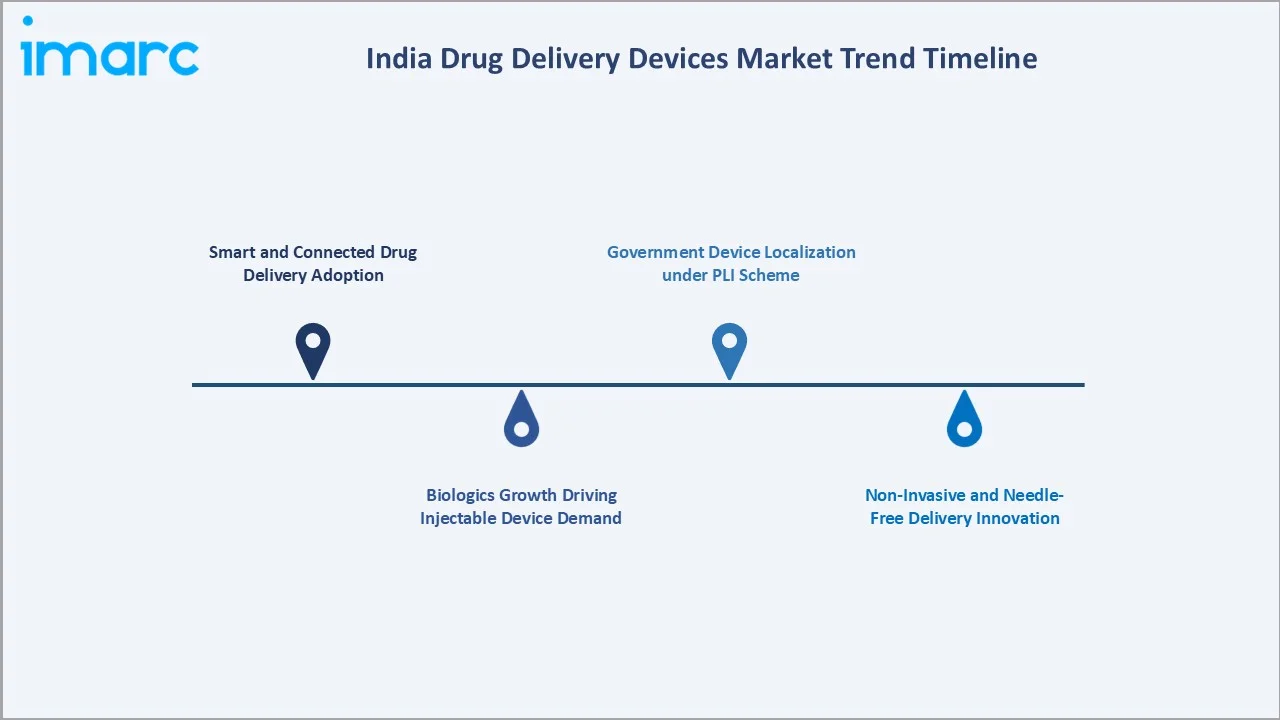

1. Smart and Connected Drug Delivery Adoption

IoT-enabled drug delivery devices are gaining traction in India’s diabetic and respiratory care segments. Indian scientists developed a self-actuating drug delivery system for rheumatoid arthritis that offers targeted, longer-lasting relief with fewer side effects. The system improves drug bioavailability and retention in affected joints, potentially reducing the need for frequent injections and lowering systemic toxicity.

2. Biologics Growth Driving Injectable Device Demand

Biosimilar and biologic drug launches surged 34% between 2022 and 2025. Each biologic requires validated injectable delivery systems. In September 2024, BD announced the commercial launch of the BD Neopak XtraFlow Glass Prefillable Syringe and expanded capacity for its Neopak Glass Prefillable Syringe platform to meet rising demand for biologic therapies. The new syringe is designed to improve subcutaneous delivery of higher-viscosity drugs by reducing injection force and time, supporting better usability for next-generation biologics.

3. Non-Invasive and Needle-Free Delivery Innovation

Transdermal patches for pain, hormones, and cardiac therapy are expanding through India’s pharmacy retail channel. Needle-free injection systems address needle phobia affecting ~25% of Indian patients. The transdermal delivery sub-segment is estimated to grow at ~7.1% CAGR through 2034.

4. Government Device Localization under PLI Scheme

The PLI Scheme for Promoting Domestic Manufacturing of Medical Devices, with a total budgetary outlay of INR 3,420 crore and a five-year incentive period from FY2022–23 to FY2026–27, recorded cumulative eligible sales of INR 10,413.40 crore as of March 2025, including export sales worth INR 5,002 crore.

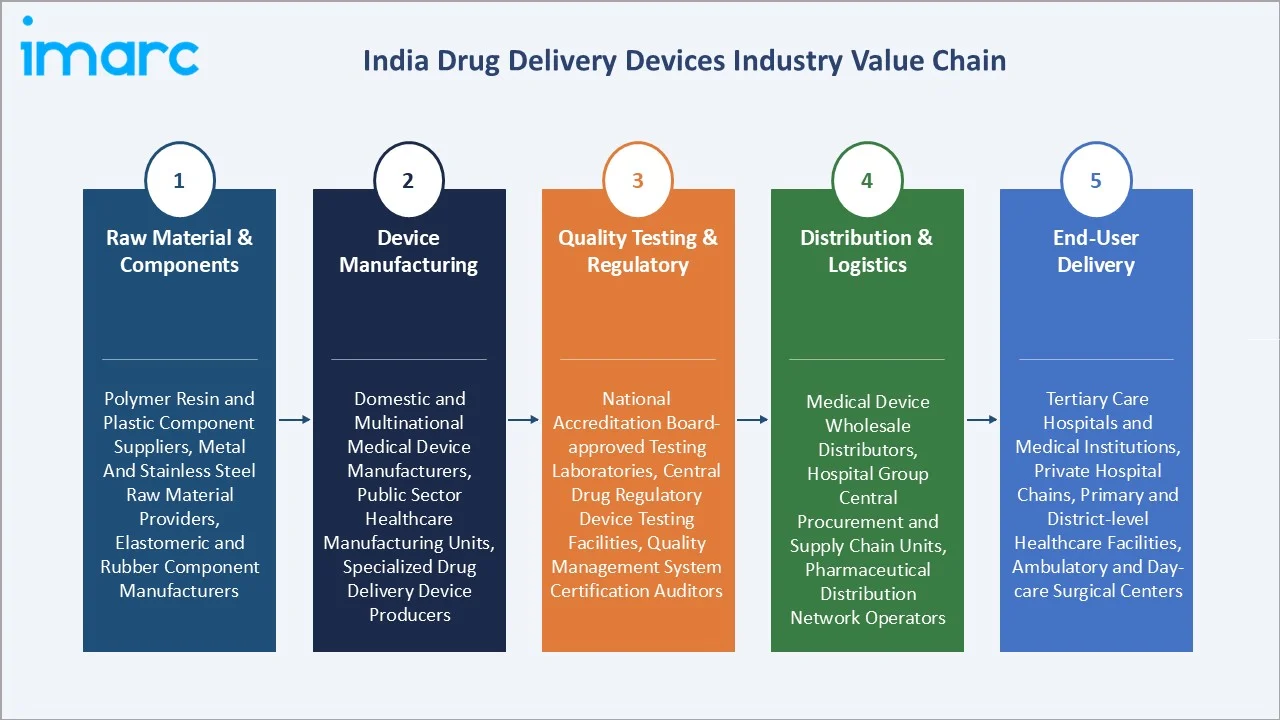

Industry Value Chain Analysis

|

Stage |

Key Players / Examples |

|

Raw Material & Components |

Polymer resin and plastic component suppliers, metal and stainless steel raw material providers, elastomeric and rubber component manufacturers |

|

Device Manufacturing |

Domestic and multinational medical device manufacturers, public sector healthcare manufacturing units, specialized drug delivery device producers |

|

Quality Testing & Regulatory |

National accreditation board-approved testing laboratories, central drug regulatory device testing facilities, quality management system certification auditors |

|

Distribution & Logistics |

Medical device wholesale distributors, hospital group central procurement and supply chain units, pharmaceutical distribution network operators |

|

End-User Delivery |

Tertiary care hospitals and medical institutions, private hospital chains, primary and district-level healthcare facilities, ambulatory and day-care surgical centers |

Technology Landscape in the India Drug Delivery Devices Industry

Advanced Injectable and Smart Delivery Systems

Auto-injectors, pre-filled syringes, and closed-loop insulin pumps are replacing conventional vials across biologics and diabetes management. BD’s Uniject device and Medtronic’s MiniMed 780G are widely deployed in Indian hospitals. A pre-post study conducted in a pediatric hospital found that reported infusion errors declined by 73% following the introduction of smart pumps, along with standardized drug concentrations and updated medication labels.

Pulmonary, Transdermal, and Implantable Devices

Dry powder inhalers and smart nebulizers serve India’s 34-35 million asthma patients. Transdermal patches for pain and cardiac therapy are expanding through urban pharmacy retail. Drug-eluting stents from Medtronic and Abbott lead India’s coronary intervention segment, with sub-dermal oncology implant procedures increasing 18% between 2022 and 2025.

Digital Health and Connected Device Integration

Connected drug delivery devices integrating with India’s digital health infrastructure, including Co-WIN, ABDM health IDs, and hospital EMR systems, are gaining traction. Bluetooth-enabled insulin pens and app-connected nebulizers enable remote adherence monitoring, reducing hospitalization rates by an estimated 15–20% in managed chronic disease programs.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Application |

Cancer |

28.7% |

2025 |

|

End User |

Hospitals |

64.2% |

2025 |

|

Route of Administration |

🔒 |

🔒 |

2025 |

|

Regional |

North India |

31.5% |

2025 |

By Application

Cancer leads at 28.7% in 2025. India’s growing cancer incidence is expected to reach approximately 2.46 million cases by 2045, leading to rising demand for infusion pumps, chemotherapy ports, and drug-eluting stents. Cardiovascular disease at 22.5% reflects India’s ischemic heart disease burden (GBD 2019 ranked as the leading cause of death). Diabetes at 19.6% is driven by IDF’s 92 million patient projection for 2030.

To access detailed market analysis, Request Sample

Infectious diseases at 17.8% are served by IV antibiotic and antiviral infusion devices for hospital-acquired infection management. Others at 11.4% encompass neurological, respiratory, and ophthalmological drug delivery applications.

By End User

Hospitals dominate at 64.2% in 2025. India’s 70,000+ registered hospitals generate the highest device consumption through IV infusion, surgical delivery, and oncology administration. Super-specialty facilities drive premium procurement, including smart pumps and implantable delivery systems. Demand benefits directly from Ayushman Bharat’s expansion of covered procedures.

Ambulatory surgical centers (ASCs) hold 21.7% at ~6.8% CAGR, driven by 30–40% lower costs than inpatient care and same-day procedure growth. ASCs require portable infusion pumps and single-use auto-injectors. Others (14.1%) include home care nursing and specialty clinics adopting self-administration devices.

Regional Market Insights

North India leads at 31.5% in 2025. Delhi-NCR hosts India’s highest concentration of super-specialty hospitals, including AIIMS, Fortis, and Max Healthcare, driving premium device procurement. UP pharma manufacturing hubs in Noida support domestic supply chains for basic delivery devices.

South India, at 27.3% (2025), is the most innovation-forward region, with BD, Abbott, and Medtronic R&D centers in Hyderabad and Bengaluru. Chennai handles about 25% of India’s medical tourists, generating premium device demand. East India, at 17.4%, is the fastest-growing region as hospital investment accelerates under central government programs.

|

Region |

Share (2025) |

Key Growth Drivers |

|

North India |

31.5% |

Super-specialty hospital density in Delhi-NCR, PLI-incentivized device manufacturing, high chronic disease burden in large urban populations |

|

South India |

27.3% |

Biotech-pharma corridor in Hyderabad and Bengaluru, strong private hospital networks, high surgical device adoption |

|

West India |

23.8% |

Mumbai BFSI and pharma trade hub, Maharashtra hospital infrastructure, Gujarat device manufacturing and exports |

|

East India |

17.4% |

Expanding hospital infrastructure in Kolkata and Odisha, PMJAY expansion, rising chronic disease incidence in eastern states |

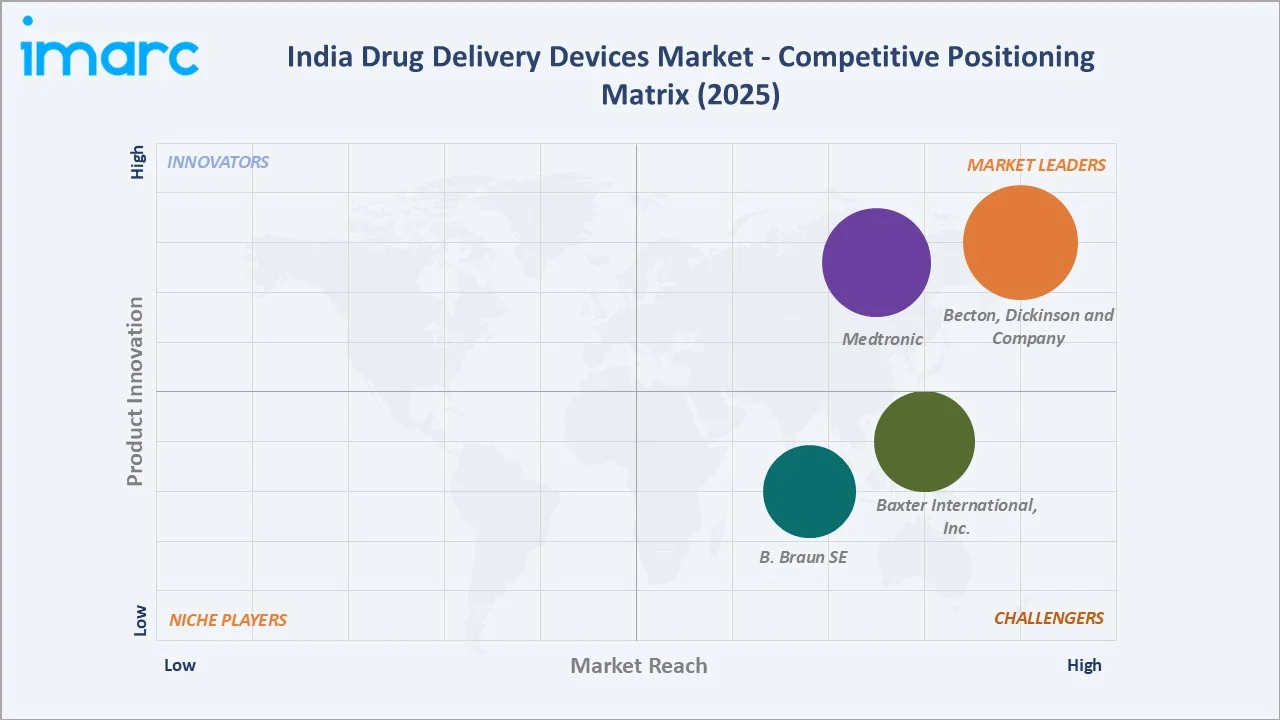

Competitive Landscape

India’s drug delivery devices market is moderately concentrated. Becton, Dickinson and Company, Medtronic, Baxter International, Inc., and B. Braun SE dominate advanced device categories, including infusion pumps and implantable systems. Domestic manufacturers HMD and HLL Lifecare lead volume-sensitive basic segments through government tenders.

|

Company |

Brand Name |

Market Position |

Core Strength |

|

Becton, Dickinson and Company |

BD Medical |

Market Leader |

Global leader in syringes, pre-filled delivery, infusion systems; strong India manufacturing |

|

Medtronic |

SynchroMed III intrathecal pump, MiniMed 780G system |

Market Leader |

Infusion pump leadership, insulin delivery, cardiac drug systems; large India service network |

|

Baxter International, Inc. |

Intravenous solutions & medication delivery systems |

Strong Challenger |

IV infusion systems, PCA pumps, parenteral nutrition delivery, strong hospital formulary presence |

|

B. Braun SE |

compactplus pump, Infusomat Space Large Volume Pump, Perfusor Space Syringe Pump

|

Strong Challenger |

Infusion therapy, needle technology, IV access devices, growing India manufacturing base |

PLI incentives are driving global companies to localize manufacturing, intensifying competition at mid-tier price points.

Key Company Profiles

Becton, Dickinson and Company

Becton, Dickinson and Company is the global leader in drug delivery device manufacturing, operating in 190+ countries. BD India produces syringes, pen needles, pre-filled delivery systems, and infusion accessories for public procurement and private hospital networks.

- Product Portfolio: BD Uniject pre-filled device, BD AutoShield Duo pen needle, BD Alaris infusion pumps, BD Neopak glass pre-fillable syringes, BD PhaSeal closed system drug transfer devices for oncology.

- Recent Developments: In May 2026, Becton Dickinson raised its annual profit forecast after reporting stronger-than-expected second-quarter results, supported by robust demand for drug-delivery devices and surgical equipment. Demand for injectable GLP-1 diabetes and obesity drugs continued to benefit BD’s injection pen business, although analysts noted potential future pressure from oral weight-loss drugs.

- Strategic Focus: Biologic delivery co-development with Indian pharma; BD Alaris smart pump expansion in Indian hospitals; AutoShield Duo pen needle growth across diabetes specialty clinics.

Medtronic plc

Medtronic plc’s subsidiary Medtronic India serves hospitals with cardiac, diabetes, and pain management drug delivery systems, and leads India’s insulin pump therapy and cardiac drug delivery segments.

- Product Portfolio: MiniMed 780G system, SynchroMed III intrathecal pump, and SynchroMed implantable pumps.

- Recent Developments: In June 2025, Medtronic inaugurated a Diabetes Global Capability Center in Pune, India, with a planned investment of USD 50 million over five years. The center is expected to support innovation in diabetes drug delivery technologies, including insulin delivery systems, automated insulin delivery, and connected care solutions.

- Strategic Focus: Closed-loop insulin delivery leadership; intrathecal pain device growth in Indian clinics; drug-eluting stent renewal for India’s coronary interventions.

Market Concentration Analysis

India’s drug delivery devices market is moderately concentrated. Becton, Dickinson and Company, Medtronic, Baxter International, Inc., and B. Braun SE collectively hold ~45–55% of the premium segment revenue in 2025.

The basic device segment is more fragmented, with domestic manufacturers HMD, Dispovan, and Iscon commanding volume through government tenders. PLI incentives are driving new domestic capacity creation in mid-tier segments, gradually reducing multinational dominance.

Investment & Growth Opportunities

Fastest Growing Segments

Ambulatory surgical centers (~6.8% CAGR), diabetes delivery devices (~6.5% CAGR), smart connected infusion systems, and nanotechnology-based targeted delivery are the highest-value investment vectors through 2034.

Emerging Market Expansion

Tier-2 and Tier-3 cities are the largest under-penetrated geography. Expanding private hospital chains (Narayana, Care, Aster) and PM-ABHIM infrastructure investment create compounding demand in cities historically reliant on government facility-based delivery.

Venture and Institutional Investment Trends

- India’s MedTech ecosystem attracted USD 850+ Million in venture investment during 2023–2025, with drug delivery and diagnostics leading. Mivi Healthcare received Series B+ rounds for AI-enabled therapeutic delivery platforms.

- PLI allocated INR 3,420 crore to 4 priority device clusters, creating setup opportunities for global and domestic manufacturers in Andhra Pradesh, Tamil Nadu, Himachal Pradesh, and Uttar Pradesh.

Future Market Outlook (2026-2034)

India’s drug delivery devices market will expand from USD 9.89 Billion in 2025 to USD 16.13 Billion by 2034 at a 5.39% CAGR. Cancer, diabetes, and cardiovascular disease will drive premium device adoption. ASCs will drive volume growth in portable, single-use delivery formats.

By 2034, AI-enabled closed-loop systems and personalized nanoparticle-based delivery will transition to mainstream adoption at leading Indian hospitals. India’s biosimilar manufacturing role will create parallel demand for domestic biologic delivery devices, positioning Indian manufacturers as export-oriented suppliers for Asian and African markets.

Research Methodology

Primary Research

Primary research comprised structured interviews with over 90 industry participants in 2024–2025, including hospital procurement managers, oncology pharmacists, diabetes specialists, device manufacturer sales teams, and CDSCO regulatory consultants across Delhi, Mumbai, Bengaluru, and Hyderabad.

Secondary Research

Secondary research covered CDSCO device databases, MoHFW National Health Profile, ICMR cancer registry, IDF Diabetes Atlas, Ministry of Commerce trade statistics, SEBI filings, and publications including Medical Buyer, Express Healthcare, and Device Alliance India.

Forecasting Models

Market estimations used bottom-up and top-down approaches, incorporating hospital procurement data, disease incidence projections, and import-export balances. A 5.39% CAGR reflects consensus validated against CDSCO registration trends and IMARC’s primary expert panel inputs through 2034.

India Drug Delivery Devices Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Routes of Administration Covered | Injectable, Topical, Ocular, Others |

| Applications Covered | Cancer, Cardiovascular, Diabetes, Infectious Diseases, Others |

| End Users Covered | Hospitals, Ambulatory Surgical Centers, Others |

| Regions Covered | North India, South India, East India, West India |

| COmpanies Covered | Becton, Dickinson and Company, Medtronic, Baxter International, Inc., B. Braun SE, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the India drug delivery devices market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the India drug delivery devices market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the India drug delivery devices industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the India Drug Delivery Devices Market Report

The market reached USD 9.89 Billion in 2025 and is forecast to reach USD 16.13 Billion by 2034 at a 5.39% CAGR.

Cancer leads at 28.7% in 2025, driven by India’s projected 2.46 million cancer cases by 2045 and oncology drug complexity requiring precision delivery systems.

Hospitals dominate at 64.2% in 2025, reflecting high patient volumes, complex drug protocols, and large-scale IV infusion and injectable device consumption.

North India leads at 31.5% in 2025, anchored by Delhi-NCR super-specialty hospitals and pharma manufacturing clusters in Uttar Pradesh and Haryana.

Key players include Becton, Dickinson and Company, Medtronic, Baxter International, Inc., and B. Braun SE.

Ambulatory surgical centers are the fastest-growing end user at approximately 6.8% CAGR through 2034, as outpatient care decentralization shifts drug delivery away from inpatient settings.

With IDF projecting 92 million diabetic patients in India by 2030, insulin pens, pumps, and continuous delivery systems are among the fastest-growing sub-categories at ~6.5% CAGR through 2034.

Key challenges include high regulatory compliance costs, counterfeit product infiltration, cold-chain infrastructure gaps in rural areas, and L1 pricing pressure in government procurement tenders.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)