India Drywall Market Size, Share, Trends and Forecast by Type, Application, and Region 2026-2034

India Drywall Market Summary:

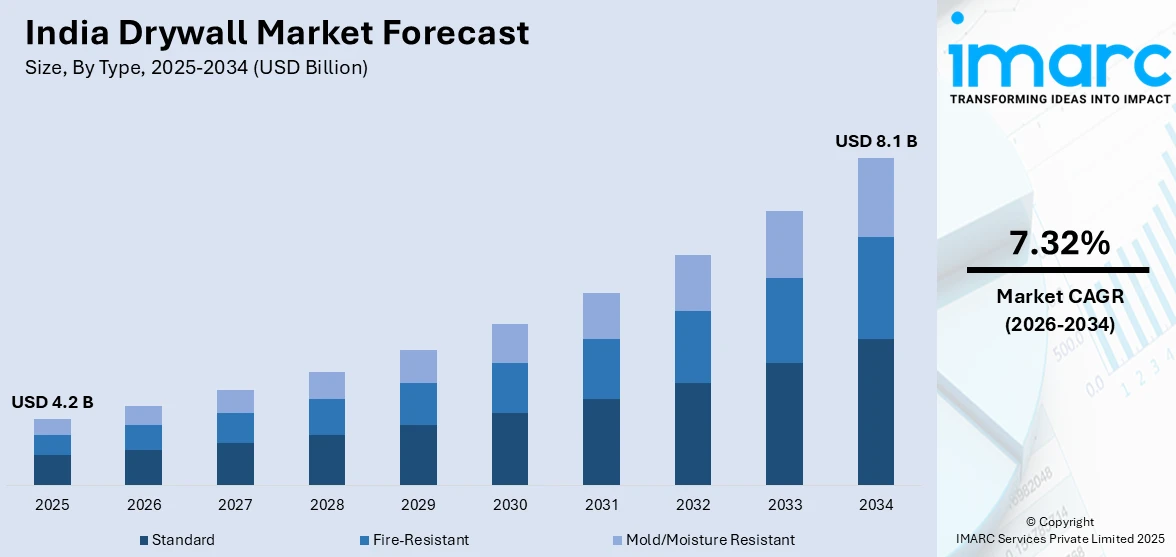

The India drywall market size was valued at USD 4.2 Billion in 2025 and is projected to reach USD 8.1 Billion by 2034, growing at a compound annual growth rate of 7.32% from 2026-2034.

The India drywall market is experiencing robust growth, driven by rapid urbanization, increasing infrastructure development, and rising demand for sustainable, lightweight, and fire-resistant construction materials, with expanding adoption across commercial, residential, and industrial projects, while government initiatives promoting affordable housing and green building standards further support market expansion, positioning drywall as a preferred solution for modern Indian construction and interior applications.

Key Takeaways and Insights:

- By Type: Standard dominates the market with a share of 52.0% in 2025, preferred for general construction projects.

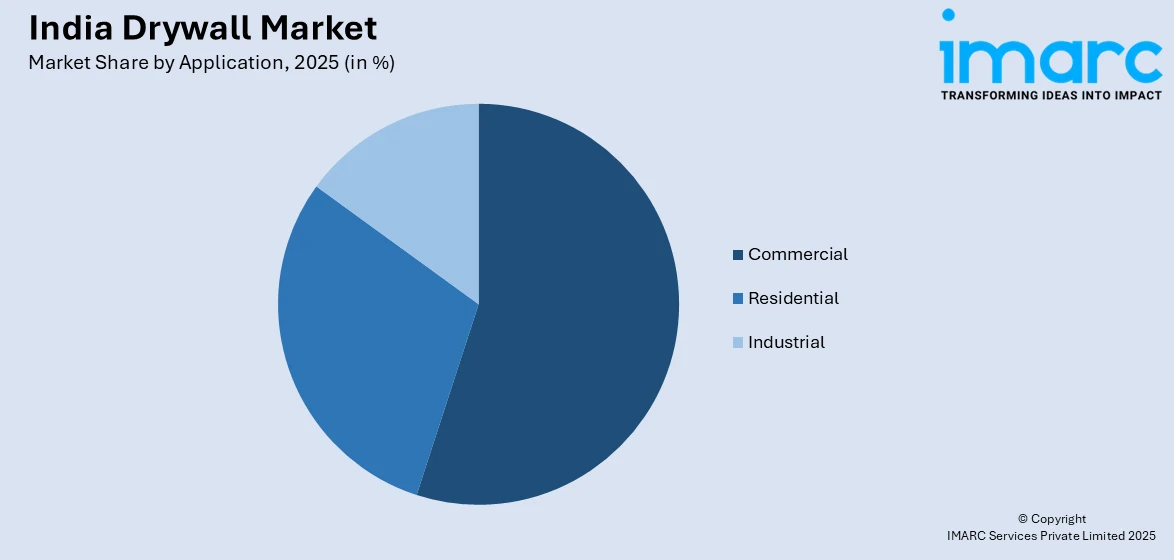

- By Application: Commercial accounted for the highest market share of 46.5% in 2025, driven by offices and retail construction demand.

- By Region: West India held the largest market segment in 2025, capturing 34.8% share, due to concentrated urban development and industrial projects.

- Key Players: The competitive landscape features domestic and international manufacturers focusing on product innovation, capacity expansion, strategic partnerships, and regional distribution networks to capture growing construction and renovation demand across India.

To get more information on this market Request Sample

The India drywall market is expanding steadily, driven by increasing investments in modern infrastructure and urban housing projects. Over the past decade, India’s urban infrastructure sector attracted INR 30 Lakh Crore in investments and is expected to secure another INR 10 Lakh Crore in the next four years, as per an industry report. In line with this, rising adoption of modular construction and interior renovation solutions is promoting the use of drywall for faster, cleaner, and more flexible wall and ceiling systems. Manufacturers are also focusing on lightweight, durable, and moisture-resistant variants to meet diverse climatic and architectural requirements. Growing awareness of sustainable construction practices and energy-efficient materials is further supporting market adoption. Additionally, the rapid emergence of tier-2 and tier-3 cities as construction hotspots is creating new regional opportunities. Besides this, ongoing technological advancements in prefabrication, coupled with collaborations among local and international players, are enhancing product availability and quality.

India Drywall Market Trends:

Rising Adoption of Prefabricated Drywall Systems

The Indian drywall market is witnessing increased adoption of prefabricated systems, as they accelerate construction timelines and reduce on‑site labour requirements. Builders and developers are increasingly specifying prefabricated drywall panels in commercial and residential projects to achieve uniform quality and minimize construction waste. These systems also support efficient integration with electrical, HVAC, and finishing elements, promoting streamlined project execution. As contractors prioritize productivity and cost‑effectiveness, prefabrication is emerging as a key trend shaping drywall utilization. An industry report highlights that pre-engineered buildings (PEBs) provide up to 40% lower costs and faster ROI than traditional construction, making them an ideal choice for Indian companies in 2025.

Integration of Fire‑Resistant and Acoustic Solutions

There is growing demand for enhanced drywall solutions with superior fire resistance and acoustic performance in India. As such, in September 2025, Knauf India launches GIFAfloor, a high-performance, gypsum-based raised flooring system complementing its leading drywall and ceiling solutions. Offering quick, dry, and eco-friendly installation, the system provides fire resistance, sound insulation, and versatile load capacity for offices, hospitals, data centers, and commercial spaces. Furthermore, regulatory emphasis on building safety and occupant comfort is encouraging developers to select advanced drywall compositions engineered for fire deterrence and sound attenuation. Educational institutions, healthcare facilities, and high‑rise residential complexes are also increasingly adopting these specialized products. Manufacturers are responding by optimizing gypsum formulations and panel designs to meet stringent safety, thermal, and acoustic benchmarks, reinforcing drywall’s role in resilient, well‑performing structures.

Growth of Drywall in Institutional and Industrial Retrofits

The application of drywall in institutional and industrial retrofit projects is gaining traction across India as aging facilities undergo modernization. Retrofit initiatives in schools, government buildings, and manufacturing plants are specifying drywall to improve interior environments rapidly without extensive structural alteration. Drywall’s flexibility enables quick installation around existing electrical and mechanical systems, reducing downtime and disruption. This trend highlights drywall’s adaptability and cost‑efficient benefits, positioning it as a preferred solution in renovation projects beyond traditional new construction.

Market Outlook 2026-2034:

The India drywall market is projected to grow as investments in sustainable construction and modern building technologies increase. As such, in 2025, the government allocated INR 1.5 Lakh Crore for sustainable infrastructure, a 25% increase from 2024, funding green mobility, EV infrastructure, renewable energy, and INR 50,000 Crore for climate-resilient projects in coastal and rural areas. In accordance with this, expanded use in institutional, healthcare, and mixed‑use developments is expected to propel the market. The continual advancements in material science and manufacturing scale are projected to enhance product performance and reduce costs. Further integration with smart building systems and digital construction practices will improve project efficiencies. Additionally, broader acceptance of drywall in rural and suburban regions will bolster long‑term demand across diverse segments of the Indian construction industry. The market generated a revenue of USD 4.2 Billion in 2025 and is projected to reach a revenue of USD 8.1 Billion by 2034, growing at a compound annual growth rate of 7.32% from 2026-2034.

India Drywall Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Type |

Standard |

52.0% |

|

Application |

Commercial |

46.5% |

|

Region |

West India |

34.8% |

Type Insights:

- Standard

- Fire-Resistant

- Mold/Moisture Resistant

Standard dominates with a market share of 52.0% of the total India drywall market in 2025.

Its ease of installation and compatibility with various finishing techniques make it a preferred choice for residential, commercial, and institutional projects. Contractors and builders increasingly rely on standard drywall for interior partitioning, ceilings, and renovation works, as it allows faster project execution and consistent quality across diverse construction environments, reinforcing its leading position in the market. For example, USG Boral launched its SHEETROCK Standard Plasterboard in India, offering high-quality, durable drywall and ceiling solutions. Manufactured in Rajasthan and Andhra Pradesh, it combines 100 years of innovation, sag resistance, and sustainable construction benefits.

In addition, standard drywall supports integration with electrical, plumbing, and HVAC systems, enhancing operational efficiency and reducing labor costs. Its adaptability to various surface treatments, including paint and laminate finishes, further enhances its appeal. The combination of cost-effectiveness, performance reliability, and widespread availability solidifies standard drywall’s dominance, making it the default choice for developers seeking a balance between functionality and construction efficiency across India.

Application Insights:

Access the comprehensive market breakdown Request Sample

- Residential

- Commercial

- Industrial

Commercial leads with a share of 46.5% of the total India drywall market in 2025.

Developers prefer drywall in commercial projects due to its ability to provide modular and aesthetically appealing interiors, reduce construction time, and enhance sustainability. Similarly, rising urbanization, modernization of workplaces, and demand for flexible space layouts contribute to the segment’s market leadership, positioning commercial applications as the largest driver of drywall adoption.

Moreover, drywall in commercial settings ensures acoustic comfort, fire resistance, and energy efficiency, aligning with regulatory standards and modern design expectations. Its rapid installation capability allows businesses to minimize operational disruptions while achieving high-quality interiors. The increasing emphasis on environmentally friendly construction materials also supports drywall preference in commercial applications, further reinforcing its status as the dominant segment in India’s expanding construction landscape.

Region Insights:

- North India

- South India

- East India

- West India

West India exhibits a clear dominance with a 34.8% share of the total India drywall market in 2025.

Cities like Mumbai, Pune, and Ahmedabad are witnessing large-scale commercial, residential, and institutional construction, which drives drywall demand. Additionally, increasing investments in infrastructure modernization and high-rise construction projects support the adoption of efficient, lightweight partitioning solutions, establishing West India as the leading regional market for drywall. For example, in November 2025, a real estate developer based in Mumbai invested INR 700 Crore in a 53-storey luxury tower in Borivali, offering over 300 apartments, premium amenities, strong transit access, and sustainable design, highlighting rising demand for vertical, climate-resilient, and inclusive urban housing.

The region’s market leadership is further strengthened by the presence of key manufacturing and distribution hubs, which ensure timely product availability and competitive pricing. Apart from this, rapid expansion in tier-2 cities and suburban areas is further enhancing drywall penetration, as developers seek faster, cost-effective, and aesthetically flexible solutions.

Market Dynamics:

Growth Drivers:

Why is the India Drywall Market Growing?

Increased Integration of Drywall in Green Building Certifications

The India drywall market is witnessing greater emphasis on sustainable construction as more projects pursue green building certifications such as IGBC and GRIHA. Drywall’s recyclability, low embodied energy, and contribution to improved thermal performance make it attractive for eco‑friendly building initiatives. Developers and consultants are also specifying drywall systems to optimize indoor air quality and reduce environmental impact. Furthermore, heightened adoption of certified sustainable materials is enhancing market credibility, supporting regulatory compliance, and aligning with corporate social responsibility objectives in modern construction practices.

Heightened Adoption of Digital Design and BIM

The use of Building Information Modeling (BIM) and digital design tools is transforming drywall planning and installation processes across India. Accordingly, Next Synergy Solutions empowered metal framing and drywall contractors with BIM-driven planning, 3D modeling, clash detection, and field-ready documentation, enhancing speed, accuracy, cost-efficiency, compliance, and aesthetic quality across commercial, residential, industrial, and infrastructure projects. Stakeholders are leveraging BIM to optimize material take‑offs, reduce errors, and coordinate drywall integration with mechanical, electrical, and plumbing systems. This digital shift enhances design precision, minimizes waste, and accelerates project delivery timelines. As construction technology evolves, enhanced digital workflows are improving collaboration among architects, engineers, and contractors, strengthening drywall’s role in efficient, data‑driven construction projects.

Emergence of Retrofit and Renovation Markets

Retrofit and interior renovation projects are driving incremental demand for drywall as commercial and residential spaces undergo modernisation. For example, in March 2025, Trimurti launched innovative construction solutions, including Gypsum Boards, Plasters, GI Channels, POP Wiremesh, and Drywall Fasteners, offering durability, cost-efficiency, ease of use, and superior finishes for residential and commercial wall, ceiling, and plaster applications. Property owners are replacing traditional masonry partitions with drywall to increase usable space, improve acoustics, and facilitate rapid installation with minimal disruption. Renovation initiatives in educational institutions, healthcare facilities, and co‑working environments are particularly driving drywall adoption. This trend highlights drywall’s flexibility and cost‑effective advantages in updating existing structures while maintaining operational continuity.

Market Restraints:

What Challenges the India Drywall Market is Facing?

High Initial Installation Costs

One of the key challenges in the India drywall market is the relatively high upfront cost compared to traditional masonry. Although drywall offers long-term savings through reduced labor and construction time, developers and contractors often hesitate due to initial expenditure on materials, specialized tools, and skilled labor. This cost barrier is particularly significant for small-scale residential projects and budget-conscious developers, limiting market penetration in price-sensitive regions despite drywall’s long-term efficiency and performance advantages.

Limited Skilled Workforce for Installation

The drywall market in India faces constraints due to a shortage of trained and certified installers. Proper installation requires expertise in cutting, joining, and finishing panels, as well as integrating electrical and plumbing systems. Inadequate workforce skills can lead to improper fitting, surface defects, and reduced durability, discouraging adoption among developers unfamiliar with modern construction techniques. Training initiatives and workforce development remain critical to overcoming this barrier and ensuring consistent quality in drywall projects nationwide.

Supply Chain and Material Availability Challenges

Drywall adoption in India is occasionally hindered by supply chain inefficiencies and inconsistent material availability. Manufacturing facilities are concentrated in select regions, causing delays and higher logistics costs for remote areas. Additionally, reliance on imported gypsum and related components can expose the market to price volatility and import restrictions. These supply constraints impact timely project execution, particularly in tier-2 and tier-3 cities, restraining market growth despite increasing demand for lightweight, efficient interior partitioning solutions.

Competitive Landscape:

The competitive landscape of the India drywall market is characterized by the presence of both domestic manufacturers and international suppliers focusing on product innovation, quality enhancement, and regional expansion. Key players are investing in manufacturing capacity, supply chain optimization, and strategic partnerships with construction companies and contractors. Competitive strategies also include offering customized drywall solutions, technical support, and sustainable product lines to meet evolving building standards. Pricing, brand recognition, and timely project delivery remain critical differentiators, while growing demand in commercial, residential, and infrastructure sectors intensifies competition, driving continuous improvements in efficiency, performance, and customer engagement across the market.

Recent Developments:

- In December 2025, Knauf India inaugurated a new Metal Line at its Khushkhera plant, doubling production capacity. This expansion strengthens its drywall and ceiling solutions portfolio, enhancing the supply of high-quality gypsum boards, metal frames, and related systems, supporting faster, efficient construction for residential and commercial projects.

- In May 2025, Knauf India launches DewBloc Gypsum Plasterboard, a moisture-resistant, lightweight, and eco-friendly drywall solution for wet areas. Compliant with IS 2095 and BS EN 520 standards, it enables fast installation, durable performance, versatile designs, and sustainable construction, addressing moisture challenges in residential and commercial interiors.

India Drywall Market Report Coverage:

|

Report Features |

Details |

|

Base Year of the Analysis |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Units |

USD Billion |

|

Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

|

Types Covered |

Standard, Fire-Resistant, Mold/Moisture Resistant |

|

Applications Covered |

Residential, Commercial, Industrial |

|

Regions Covered |

North India, South India, East India, West India |

|

Customization Scope |

10% Free Customization |

|

Post-Sale Analyst Support |

10-12 Weeks |

|

Delivery Format |

PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Drywall Market Report

The India drywall market size was valued at USD 4.2 Billion in 2025.

The India drywall market is expected to grow at a compound annual growth rate of 7.32% from 2026-2034 to reach USD 8.1 Billion by 2034.

Standard dominated the market with 52.0% share in 2025, due to its cost-effectiveness, wide availability, ease of installation, and suitability for residential and commercial construction projects across diverse regions.

Key factors driving the India drywall market include growing urbanization, rising residential and commercial construction, government infrastructure initiatives, increased preference for lightweight and fire-resistant materials, and demand for faster, cleaner, and sustainable building solutions.

Major challenges in the India drywall market include high initial costs, limited awareness in smaller towns, competition from traditional construction materials, skilled labor shortages, and fluctuating raw material prices.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)