India E-Bike Battery Market Size, Share, Trends and Forecast by Battery Type, Battery Pack Position Type, and Region, 2026-2034

India E-Bike Battery Market Size, Share, Trends & Forecast (2026-2034)

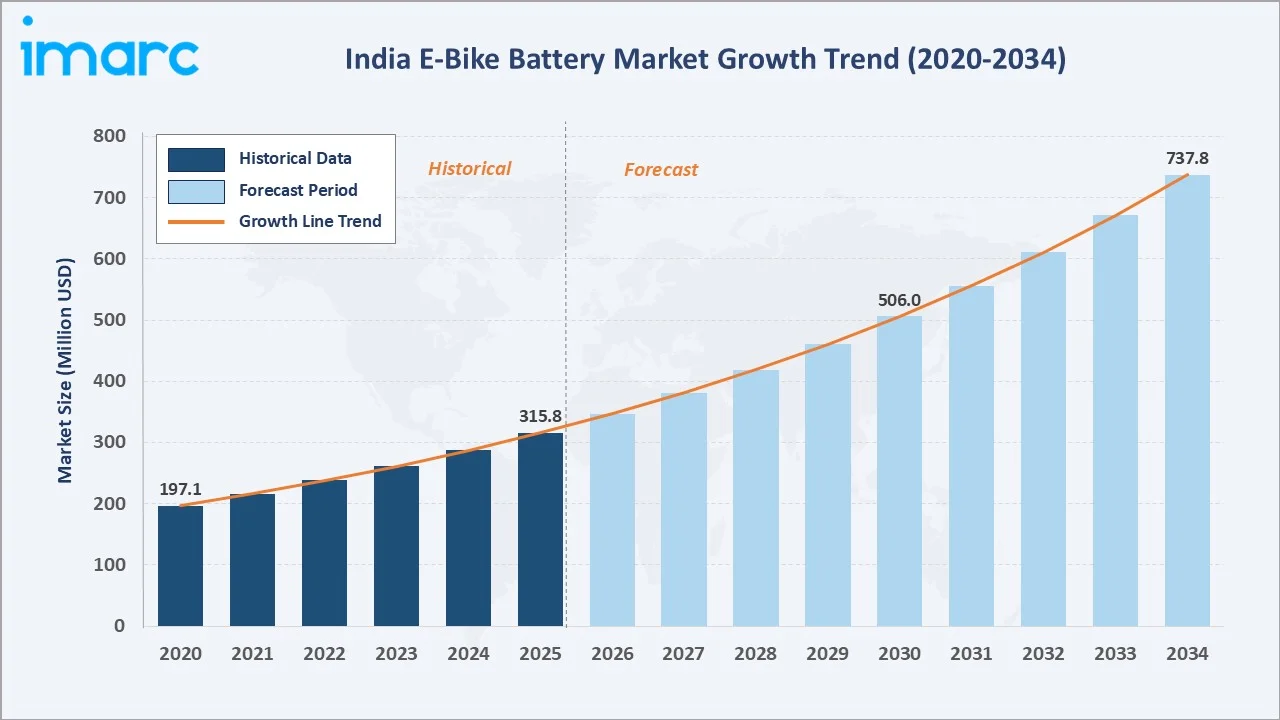

The India e-bike battery market reached USD 315.8 Million in 2025 and is projected to reach USD 737.8 Million by 2034, growing at a CAGR of 9.89% during 2026-2034. The market is driven by accelerating electric two-wheeler adoption, government subsidies under FAME II, rising fuel prices, and rapid domestic lithium-ion manufacturing expansion.

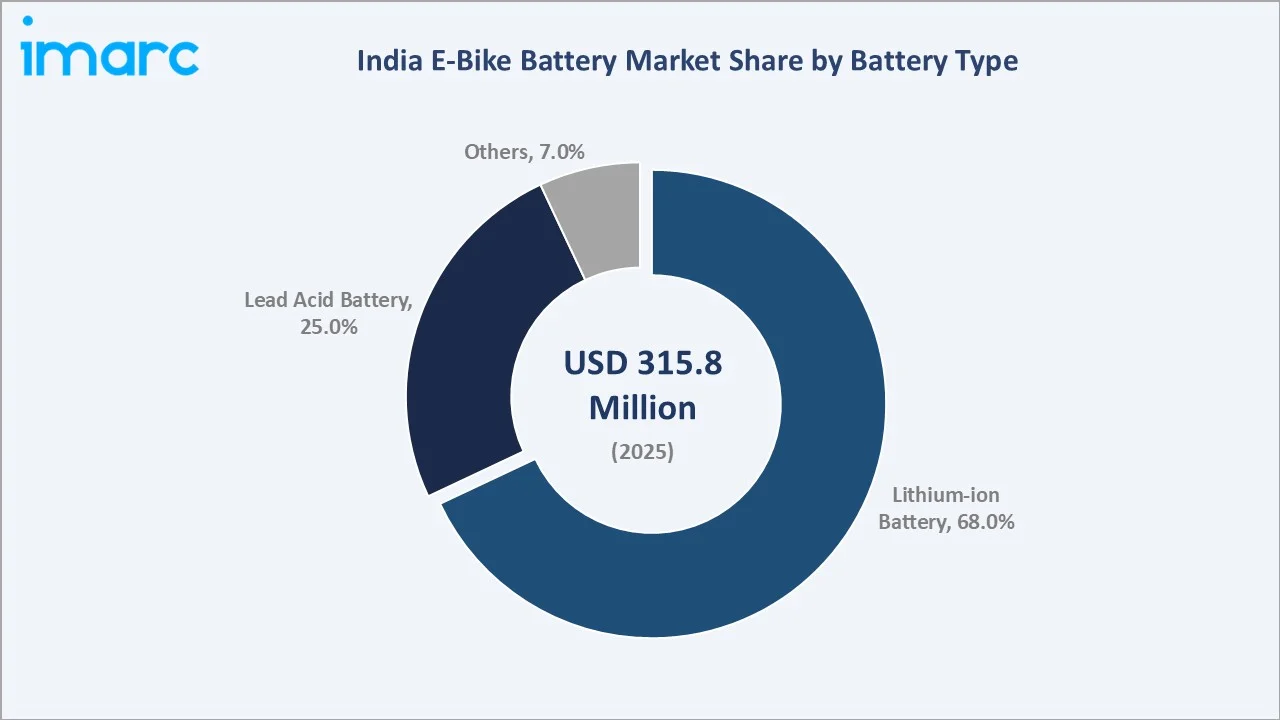

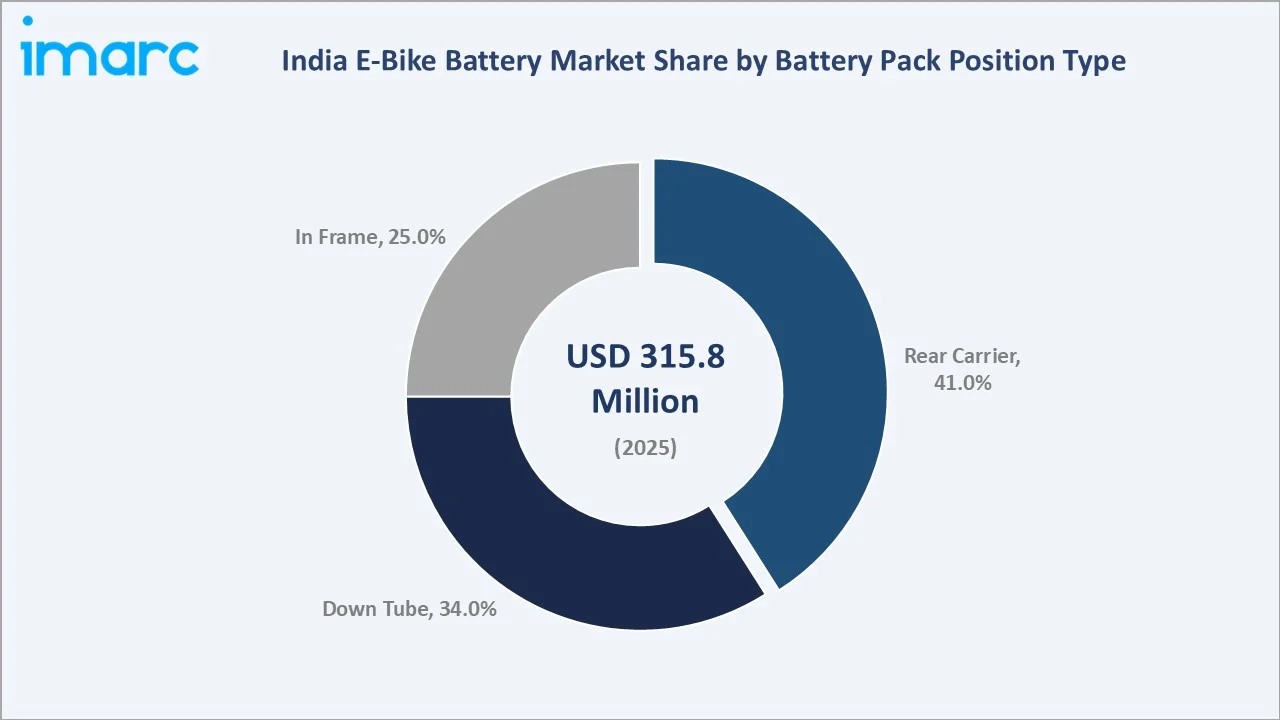

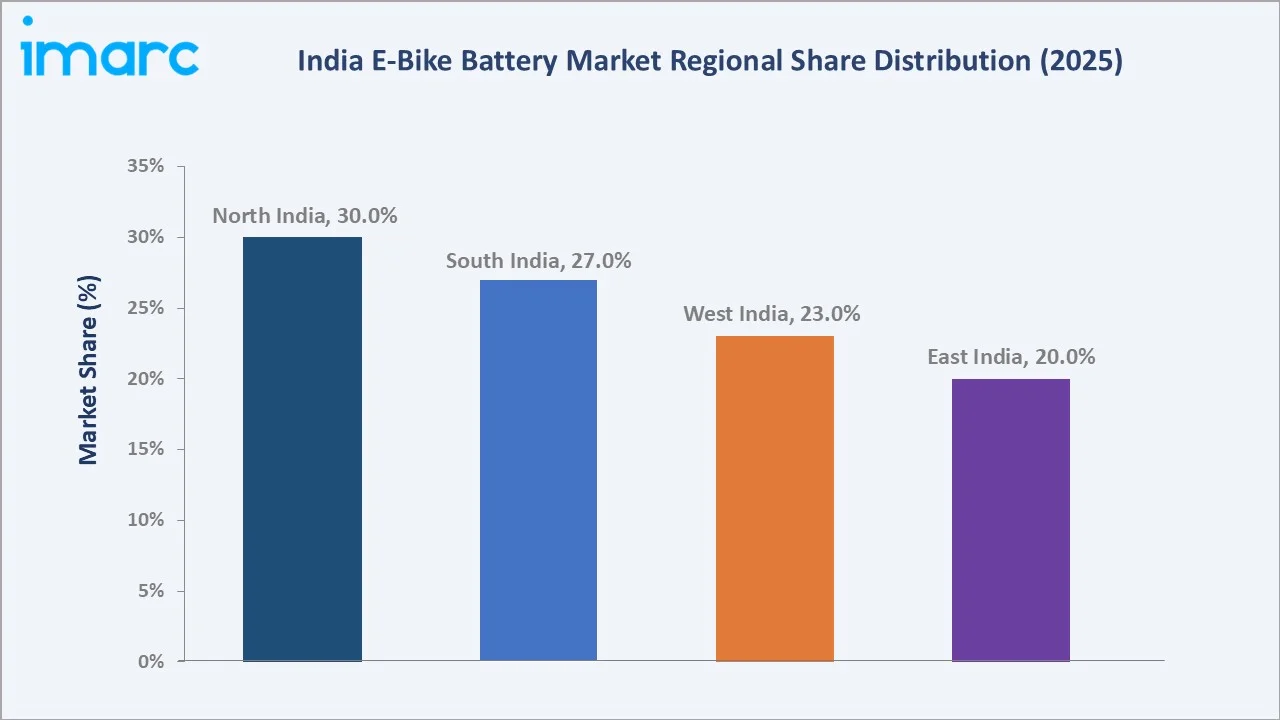

Lithium-ion battery leads with 68.0% share in 2025. Rear Carrier dominates battery pack position at 41.0%. North India commands 30.0% of the regional market.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 315.8 Million |

|

Forecast Market Size (2034) |

USD 737.8 Million |

|

CAGR (2026-2034) |

9.89% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Battery Type |

Lithium-ion Battery (68.0%, 2025) |

|

Dominant Pack Position |

Rear Carrier (41.0%, 2025) |

|

Leading Region |

North India (30.0%, 2025) |

The market expanded from USD 197.1 Million in 2020 to USD 315.8 Million in 2025, anchored at USD 506.0 Million in 2030 and projected to reach USD 737.8 Million by 2034. The FAME II policy drove adoption with EV penetration climbing from 0.71% in FY20 to 7.50% in FY25. Lithium-ion displacement of lead-acid chemistry accelerated per-unit revenue, while PLI-backed domestic cell manufacturing lowered costs and strengthened supply chain resilience.

To get more information on this market, Request Sample

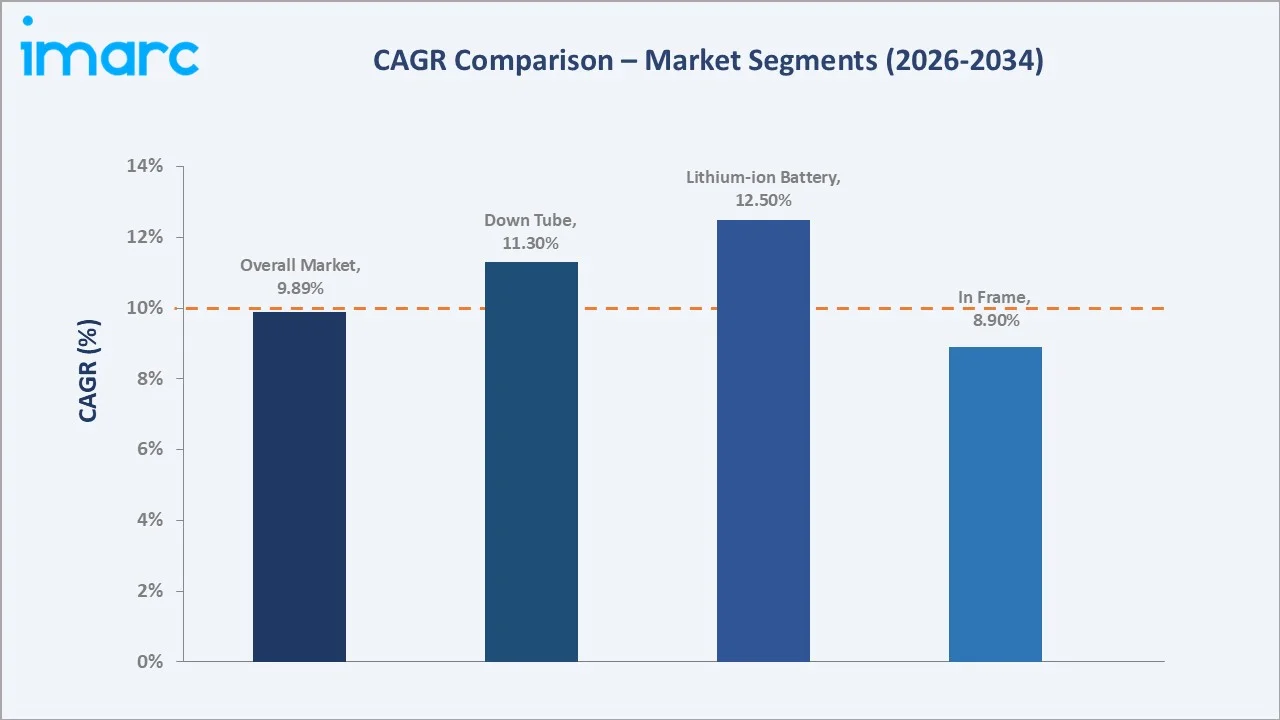

Lithium-ion battery segment grows fastest at ~12.5% CAGR as domestic cell manufacturing scales under the PLI ACC scheme. Rear carrier position type maintains dominance through lower installation cost and battery swap compatibility. North India sustains regional leadership through urbanisation, EV subsidies, and last-mile delivery fleet electrification.

Executive Summary

The India e-bike battery market reached USD 315.8 Million in 2025, representing one of India's highest-growth electric mobility component segments driven by the structural electrification of urban transport. The battery pack is the defining component of the e-bike powertrain, accounting for 30-40% of vehicle cost and the primary determinant of range, performance, and total ownership cost. The market is projected to reach USD 737.8 Million by 2034.

Lithium-ion battery at 68.0% dominates through superior energy density and declining costs from domestic manufacturing scale. Rear carrier at 41.0% leads through ease of installation and battery-swap compatibility. North India at 30.0% leads through metropolitan density, distribution infrastructure, and aligned state-level EV incentives.

Key Market Insights

|

Insight |

Data |

|

Dominant Battery Type |

Lithium-ion Battery – 68.0% share (2025) |

|

Dominant Pack Position |

Rear Carrier – 41.0% market share (2025) |

|

Leading Region |

North India – 30.0% market share (2025) |

|

Market Opportunity |

Battery swapping networks; solid-state chemistry; indigenous cell manufacturing; IoT-enabled BMS services |

Key Analytical Observations Supporting the Above Data:

- Lithium-ion Battery at 68.0%: Lithium-ion dominates as it delivers energy density of 150-250 Wh/kg versus 30-50 Wh/kg for lead-acid, enabling longer e-bike range at lower weight. Falling cell costs and PLI-backed domestic cell production further accelerate displacement of lead-acid in mid-to-premium segments.

- Rear Carrier at 41.0%: Rear carrier leads as it offers the lowest installation complexity and greatest compatibility with traditional bicycle frame structures used by Indian OEMs targeting affordable price points. Battery swap access supports swapping business models gaining traction in urban delivery fleets.

- North India at 30.0%: North India leads through Delhi-NCR's concentrated demand, Uttar Pradesh's high per-vehicle EV subsidy, and commercial fleet electrification by quick-commerce players generating consistent battery replacement demand.

India E-Bike Battery Market Overview

The India e-bike battery market encompasses the design, manufacture, and supply of all battery systems used to power electric bicycles across urban, semi-urban, and rural segments. It integrates lithium-ion cell producers, lead-acid battery manufacturers, battery pack assemblers, BMS developers, e-bike OEMs, charging infrastructure operators, and battery swapping network providers.

The ecosystem integrates raw material suppliers, cell manufacturers, pack assemblers, BMS technology developers, e-bike OEMs, distribution channels, and aftersales service providers. Macroeconomic factors include rising petrol prices, government EV incentive programs, growing urbanisation, environmental sustainability imperatives, and India's PLI scheme for ACC manufacturing targeting 50 GWh of domestic capacity.

Market Dynamics

To evaluate market opportunities, Request Sample

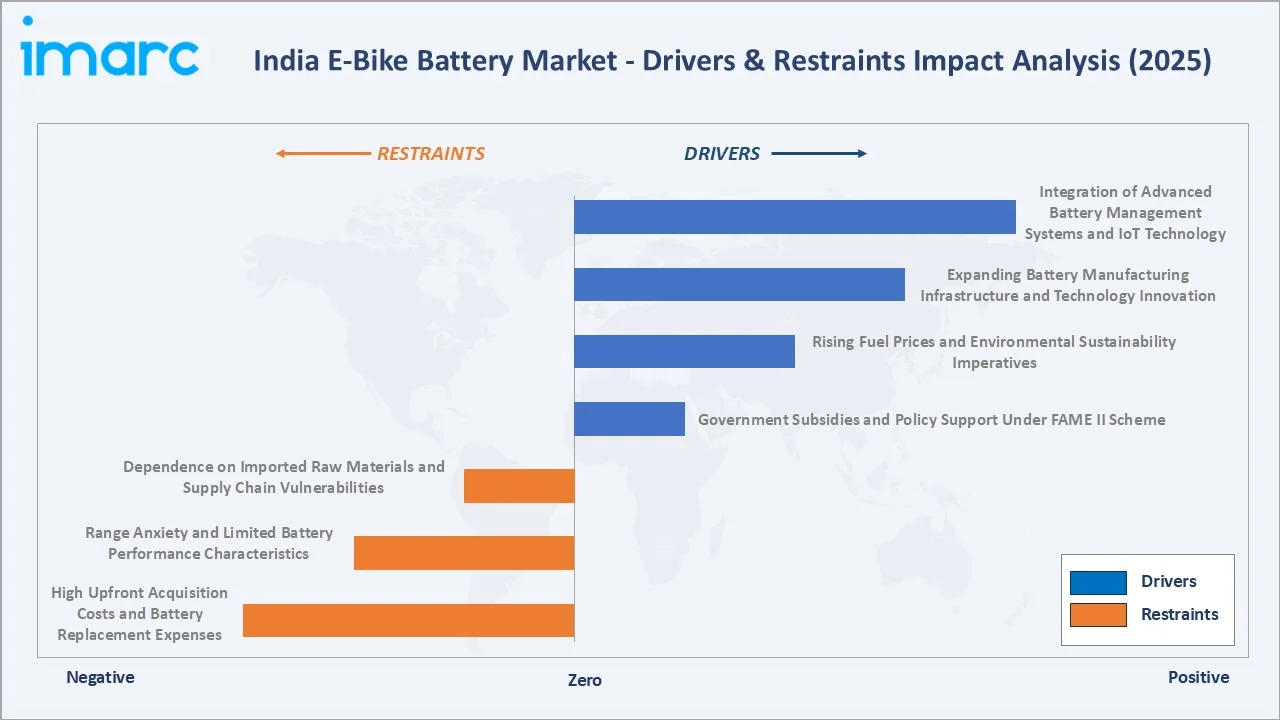

Market Drivers

- Government Subsidies and Policy Support Under FAME II Scheme: FAME II increased the average per-kWh subsidy to INR 12,000 from INR 5,000 under FAME I, directly reducing consumer acquisition cost. By March 2025, FAME II facilitated the sale of 16,71,606 EVs. The Electric Mobility Promotion Scheme 2024 allocated INR 500 crore, sustaining affordability-driven demand expansion and strengthening India e-bike battery market share across urban and peri-urban segments.

- Rising Fuel Prices and Environmental Sustainability Imperatives: Domestic petrol prices rose sharply through 2022, and October 2025 petrol consumption grew 7.03% YoY to 3.65 million tonnes. Rising fuel expenditure compels urban commuters and commercial delivery operators to adopt e-bikes as cost-efficient alternatives, directly expanding battery demand and contributing to a positive India e-bike battery market outlook.

- Expanding Battery Manufacturing Infrastructure and Technology Innovation: Growing investments in domestic battery manufacturing facilities and continuous advancements in lithium-ion battery technology are strengthening the electric vehicle ecosystem. Expansion of local production capacity, improvements in battery chemistry and energy density, and increasing collaboration between battery manufacturers and automotive companies are reducing reliance on imports, improving supply chain resilience, lowering production costs, and supporting wider adoption of electric vehicles across the country.

- Integration of Advanced Battery Management Systems and IoT Technology: Modern e-bike batteries feature AI-powered BMS with IoT connectivity enabling real-time health monitoring, predictive maintenance, and thermal performance optimisation. These systems extend battery lifespan and improve charging efficiency, with industry projections targeting 80% charge completion within one hour as standard for high-capacity battery systems, directly addressing consumer range anxiety.

Market Restraints

- High Upfront Acquisition Costs and Battery Replacement Expenses: Battery packs account for 30-40% of total e-bike vehicle cost, creating affordability barriers for price-sensitive consumers. Premium lithium-ion battery replacement costs deter adoption among budget-conscious buyers, while limited rural credit infrastructure restricts financing access and constrains market penetration beyond urban affluent demographics.

- Range Anxiety and Limited Battery Performance Characteristics: Most e-bikes offer 70-250 km battery ranges, creating consumer apprehensions for longer journeys. Charging times of one to several hours contrast with instant conventional refuelling. Battery capacity degradation in India's high-temperature climate reduces actual range below manufacturer specifications, undermining confidence and slowing replacement cycle acceleration in Tier 2 and Tier 3 markets.

- Dependence on Imported Raw Materials and Supply Chain Vulnerabilities: India's limited domestic lithium, cobalt, and nickel reserves necessitate import dependency, exposing manufacturers to global commodity price volatility and geopolitical supply risks. Supply chain concentration in China creates strategic vulnerabilities, with potential trade restrictions threatening component availability and requiring costly inventory buffers that compress margins and elevate consumer prices.

Market Opportunities

- Battery Swapping Network Infrastructure Development: Battery swapping is emerging as a critical enabler for commercial e-bike fleet electrification. Automated swap stations completing exchanges within 90 seconds enable continuous delivery fleet operations. Government guidelines under the PM E-DRIVE scheme allocated INR 2,000 crore to develop public charging and battery swapping infrastructure, accelerating standardised interoperable network deployment across Tier 1 and Tier 2 cities.

- Domestic Lithium-ion Cell Manufacturing Scale-Up Under PLI Scheme: India's 50 GWh ACC PLI scheme creates a capital deployment framework for domestic cell manufacturing, enabling beneficiaries to achieve below-import-cost cell pricing. Suppliers achieving domestic cell cost parity with Chinese imports gain a structural cost advantage in India's price-sensitive e-bike battery market that cannot be replicated by import-dependent competitors.

Market Challenges

- Consumer Awareness and Technology Confidence Barriers: Limited consumer awareness of e-bike battery capabilities, charging requirements, and lifecycle economics constrains market expansion beyond early adopters in metros. Misconceptions about battery reliability, range limitations, and long-term performance create hesitation, particularly in Tier 2 and Tier 3 cities where product demonstrations and word-of-mouth exposure remain limited.

- Battery Safety and Thermal Management in Tropical Climates: India's tropical climate creates thermal management challenges for lithium-ion battery systems, with elevated ambient temperatures accelerating cell degradation and increasing thermal runaway risk. Meeting BIS safety standards while maintaining cost competitiveness requires advanced thermal management solutions that increase manufacturing complexity and add to system cost for Indian market conditions.

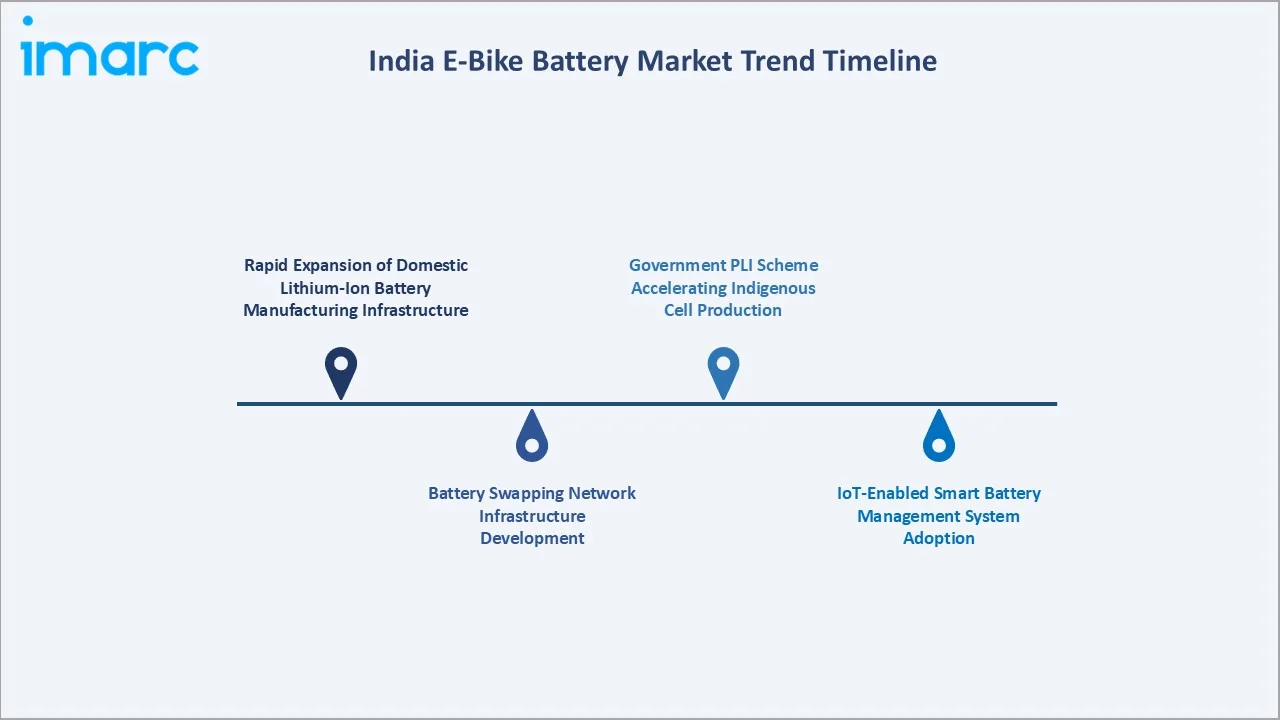

Emerging Market Trends

1. Rapid Expansion of Domestic Lithium-Ion Battery Manufacturing Infrastructure

India's battery production sector is transforming with gigafactory commissioning under the 35 GWh PLI ACC scheme. Exide, Amara Raja, and others are scaling capacity, collectively targeting 40+ GWh domestic output, reducing import dependency and lowering per-kWh battery costs for Indian e-bike OEMs and consumers.

2. Battery Swapping Network Infrastructure Development

Battery swapping infrastructure is emerging as a critical enabler for commercial e-bike fleet electrification. Automated swap stations completing battery exchanges within 90 seconds enable continuous fleet operations for delivery and ride-hailing operators. Standardisation of swappable battery formats across OEMs is progressing, with government guidelines supporting interoperable swapping network development across Tier 1 and Tier 2 cities nationwide.

3. IoT-Enabled Smart Battery Management System Adoption

Advanced BMS incorporating AI and cloud connectivity transforms e-bike batteries from passive storage into intelligent operational assets. Remote health monitoring, predictive cell degradation alerts, and anti-theft features are becoming standard in mid-to-premium battery packs. AI-powered systems optimise charge cycles, monitor thermal performance, and predict failures before occurrence, significantly extending battery lifespan and operational efficiency.

4. Government PLI Scheme Accelerating Indigenous Cell Production

The Ministry of Heavy Industries increased ACC PLI fund allocation from INR 12.01 crore to INR 250 crore for FY 2023-24. Government initiatives promoting domestic battery manufacturing and advanced cell production are encouraging investments across the battery value chain. Policy support, production-linked incentives, and measures aimed at strengthening local manufacturing capabilities are fostering technology development, reducing import dependence, enhancing supply chain resilience, and accelerating the growth of India's electric vehicle ecosystem.

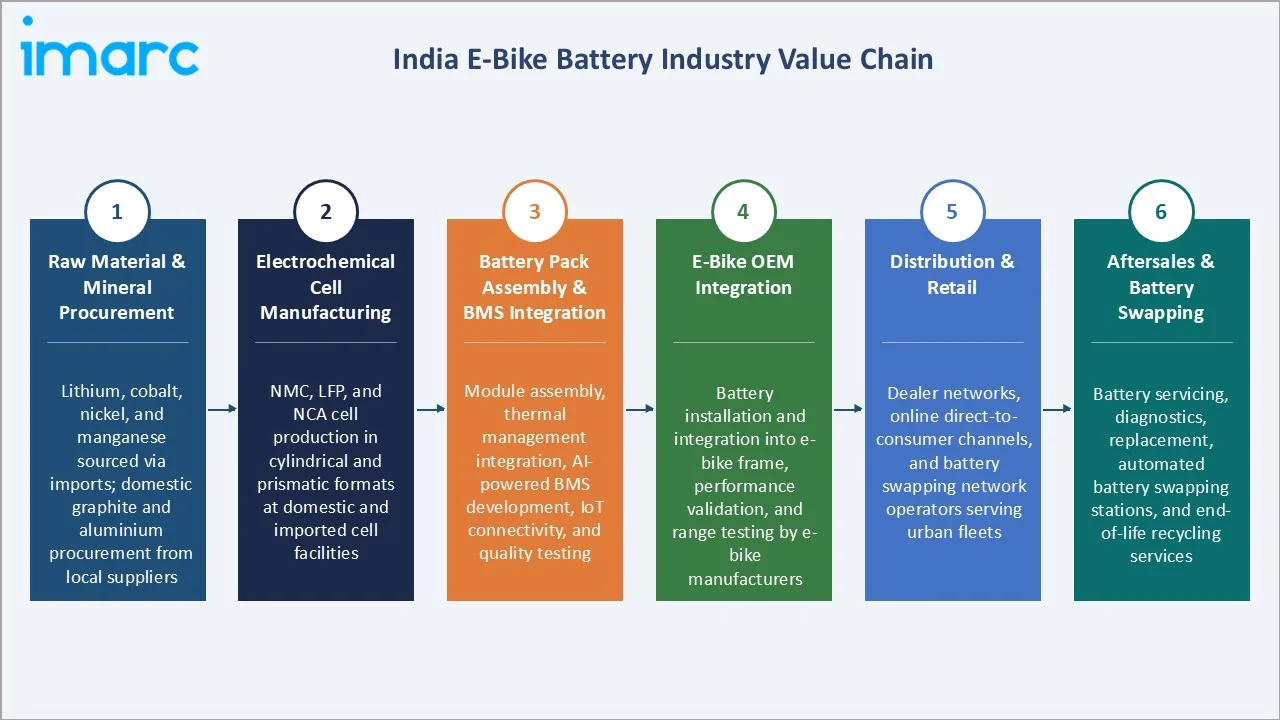

Industry Value Chain Analysis

The India e-bike battery value chain integrates raw material procurement, electrochemical cell manufacturing, battery pack assembly, BMS integration, e-bike OEM integration, retail distribution, and aftersales servicing. The value chain's commercial architecture is progressively consolidating around integrated pack and BMS assembly as the dominant format, with OEMs increasingly seeking turnkey battery solutions from suppliers reducing vehicle assembly complexity.

|

Stage |

Key Participants |

|

Raw Material & Mineral Procurement |

Lithium, cobalt, nickel, and manganese sourced via imports; domestic graphite and aluminium procurement from local suppliers |

|

Electrochemical Cell Manufacturing |

NMC, LFP, and NCA cell production in cylindrical and prismatic formats at domestic and imported cell facilities |

|

Battery Pack Assembly & BMS Integration |

Module assembly, thermal management integration, AI-powered BMS development, IoT connectivity, and quality testing |

|

E-Bike OEM Integration |

Battery installation and integration into e-bike frame, performance validation, and range testing by e-bike manufacturers |

|

Distribution & Retail |

Dealer networks, online direct-to-consumer channels, and battery swapping network operators serving urban fleets |

|

Aftersales & Battery Swapping |

Battery servicing, diagnostics, replacement, automated battery swapping stations, and end-of-life recycling services |

The raw material procurement tier is the most geopolitically sensitive stage due to lithium and cobalt import dependency from a concentrated supplier base. The BMS and pack assembly tier is experiencing the fastest technology transition as AI-powered and IoT-connected systems displace passive management architectures across premium and mid-range e-bike battery segments.

Technology Landscape in the India E-Bike Battery Industry

Lithium-Ion Battery Technology

Lithium-ion battery technology has become the preferred power source for electric bicycles due to its high energy density, lightweight design, long cycle life, and fast-charging capability. Continuous advancements in battery chemistry and cell design are improving energy efficiency, extending riding range, and enhancing overall battery performance, supporting the growing adoption of e-bikes across urban and recreational applications.

Battery Management System (BMS) Technology

Battery Management Systems play a critical role in ensuring the safe and efficient operation of e-bike batteries by monitoring parameters such as voltage, current, temperature, and state of charge. Advanced BMS solutions help optimize battery performance, improve charging efficiency, prevent overcharging and overheating, and extend battery lifespan while enhancing user safety and reliability.

Smart Battery Connectivity and Fast Charging Technologies

The integration of smart connectivity features and advanced charging technologies is enhancing the overall e-bike ownership experience. IoT-enabled battery monitoring, mobile application integration, and real-time diagnostics allow users to track battery health and performance remotely. At the same time, ongoing developments in fast-charging solutions and energy-efficient charging systems are reducing charging times, improving convenience, and supporting wider adoption of electric bicycles across India.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Battery Type |

Lithium-ion Battery |

68.0% |

2025 |

|

Battery Pack Position Type |

Rear Carrier |

41.0% |

2025 |

|

Region |

North India |

30.0% |

2025 |

By Battery Type

Lithium-ion battery leads at 68.0% in 2025, capturing the mainstream e-bike market through superior energy density, faster charging, and rapid cost decline from domestic manufacturing scale. Lithium-ion's energy density of 150-250 Wh/kg versus 30-50 Wh/kg for lead-acid enables 2-4x longer range per charge cycle, making it the preferred choice for urban commuters and commercial fleet operators seeking operational efficiency.

To access detailed market analysis, Request Sample

Lead acid battery at 25.0% retains significant share in entry-level e-bike segments where upfront affordability outweighs lifecycle cost considerations. Its established supply chain, lower replacement cost, and wide service availability sustain demand in semi-urban and rural markets. Others at 7.0% include nickel-metal hydride and emerging solid-state battery prototypes targeting premium performance segments.

By Battery Pack Position Type

Rear carrier leads at 41.0% due to its practicality and widespread adoption in commuter-focused e-bike models dominant across India's volume sales segments. This battery placement offers the lowest installation complexity and greatest compatibility with traditional bicycle frame structures used by Indian OEMs targeting affordable price points. Battery swap compatibility further reinforces rear carrier's commercial position across urban commercial delivery fleet deployments.

Down tube at 34.0% is gaining share driven by premium and performance e-bike models prioritising lower centre of gravity and improved handling characteristics. In frame at 25.0% represents the highest-integration approach used in advanced e-bike designs with streamlined aesthetics, growing in mid-to-premium urban commuter and recreational segments as OEM design sophistication increases.

Regional Market Insights

|

Region |

Share (2025) |

Key E-Bike Battery Market Drivers & Characteristics |

|

North India |

30.0% |

Driven by metropolitan concentration in Delhi-NCR, Uttar Pradesh EV subsidies, last-mile delivery electrification, manufacturing hub proximity, and high consumer EV awareness across urban centres |

|

South India |

27.0% |

Supported by Bengaluru technology-driven EV adoption, Tamil Nadu manufacturing base, Ather Energy home market advantage, and strong state-level EV policy frameworks |

|

West India |

23.0% |

Driven by Maharashtra EV incentive programs, Mumbai commercial fleet electrification, Gujarat manufacturing ecosystem, and growing demand from Pune urban commuter base |

|

East India |

20.0% |

Emerging segment with West Bengal leading, driven by affordable e-bike adoption, growing urban commuter base, and expanding distribution networks across Tier 2 cities |

North India, at 30.0%, leads through the concentration of India's largest urban agglomeration in Delhi-NCR, the highest per-state EV subsidy from Uttar Pradesh, and commercial fleet electrification by quick-commerce and last-mile logistics operators generating consistent battery replacement demand. South India, at 27.0%, reflects Bengaluru's technology-driven EV adoption and Ather Energy's manufacturing concentration.

West India, at 23.0%, and East India, at 20.0%, represent rapidly growing markets driven by Maharashtra's EV promotion policy and Bengal's expanding affordable e-bike consumer base. With continued infrastructure expansion and consumer shift toward sustainable mobility, all four regions are expected to sustain above-market growth rates through the forecast period.

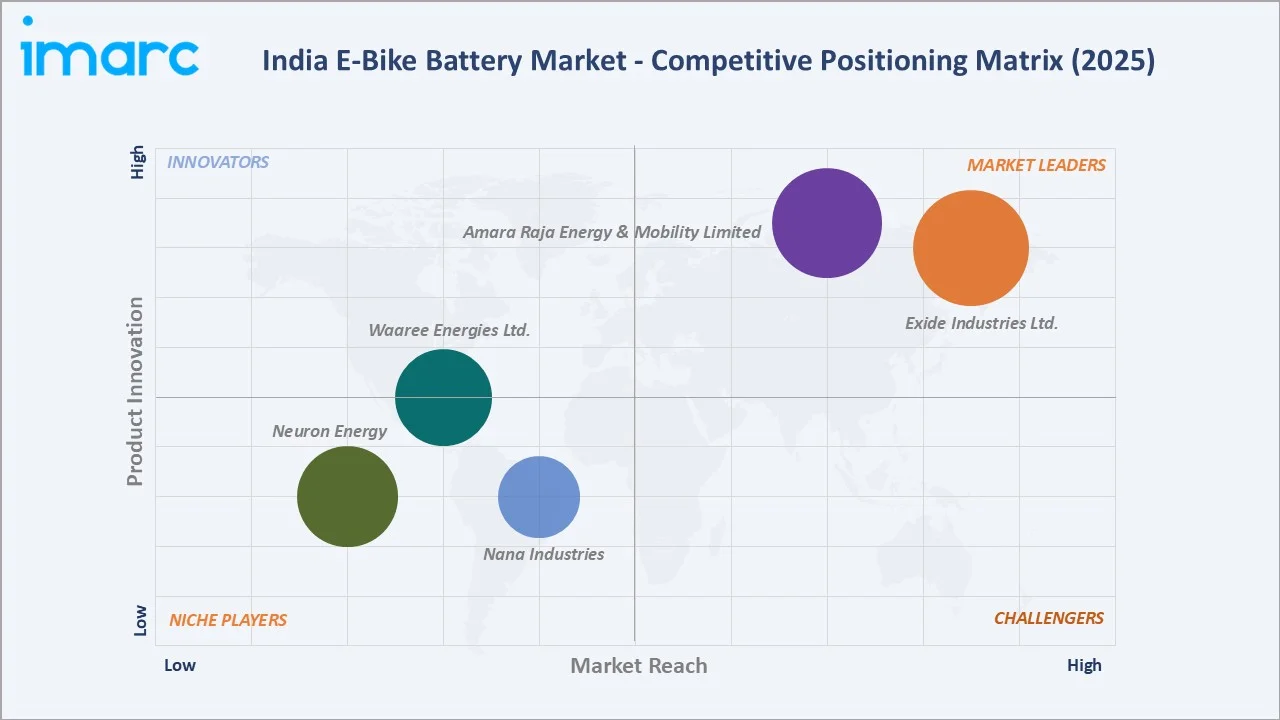

Competitive Landscape

The India e-bike battery market competitive landscape features domestic lead-acid battery incumbents, emerging lithium-ion cell and pack manufacturers, captive OEM battery divisions, and battery swapping service providers. The landscape is moderately fragmented with three competitive tiers: national-scale established battery manufacturers, technology-focused lithium-ion pack assemblers, and early-stage battery swapping and leasing operators.

|

Company Name |

Key Products |

Market Position |

Core Strength |

|

Exide Industries Ltd. |

Exide Electrica, Li-ion battery modules and packs |

Market Leader |

Scale manufacturing, established distribution network, and 12 GWh Li-ion cell plant investment via EESL subsidiary |

|

Amara Raja Energy & Mobility Limited |

E-bike Li-ion packs, lead-acid batteries |

Market Leader |

Strong automotive OEM supply relationships and expanding lithium-ion pack assembly capabilities |

|

Neuron Energy |

Gen 2 Li-ion battery packs |

Niche Player |

Second-generation Li-ion series for two-wheelers and three-wheelers targeting OEM and fleet buyers |

|

Waaree Energies Ltd. |

LIT series, LYNX series, Liger series, Lion series |

Established Player |

Diversified LiFePO4 and Li-ion battery portfolio spanning e-bike, EV traction, BESS, and telecom applications, backed by 20 GWh manufacturing scale-up under Waaree Energy Storage Solutions |

|

Nana Industries |

Electric bike batteries |

Niche Player |

Pioneer battery manufacturer in Pune with pan-India presence, serving e-bike OEMs and aftermarket segments through competitively priced battery and charging solutions |

Key players include Exide Industries Ltd., Amara Raja Energy & Mobility Limited, Neuron Energy, Waaree Energies Ltd., Nana Industries, and others.

Key Company Profiles

Exide Industries Ltd

Exide Industries is an India-based manufacturer of lead-acid and lithium-ion storage batteries with a strong presence in the e-bike battery market through its subsidiary Exide Energy Solutions Limited building a 12 GWh lithium-ion cell manufacturing facility in Bengaluru, Karnataka.

- Key Products: Lead-acid e-bike batteries; lithium-ion battery packs via Exide Energy Solutions Limited; energy storage systems for electric mobility applications.

- Recent Developments: In March 2026, Exide Industries announced a fresh capital infusion to support the expansion of its lithium-ion battery manufacturing operations in Bengaluru. The investment will accelerate the development of the company's advanced battery production facility, strengthening domestic manufacturing capabilities for electric vehicles and stationary energy storage solutions.

- Strategic Focus: Transitioning from lead-acid incumbency to lithium-ion leadership through domestic cell manufacturing scale-up; targeting e-bike, commercial EV, and stationary energy storage market segments with locally produced battery systems.

Neuron Energy

Neuron Energy is a Mumbai-based manufacturer of lithium-ion batteries established in 2018, with a strong presence in the India e-bike battery market through its advanced battery packs for electric two-wheelers, three-wheelers, and light commercial vehicles.

- Key Products: Gen 2 Li-ion battery packs

- Recent Developments: In June 2025, Neuron Energy introduced its second-generation (Gen 2) lithium-ion battery packs for electric two-wheelers, three-wheelers, and light commercial vehicles (LCVs). The new battery series incorporates enhanced structural durability, improved thermal management, vibration resistance, and an upgraded Battery Management System (BMS) to improve reliability, safety, and overall performance under Indian operating conditions.

- Strategic Focus: Scaling battery manufacturing capabilities across EV mobility and energy storage segments, strengthening research and development, reliability engineering, and expanding domestic and international market presence.

Market Concentration Analysis

The India e-bike battery market is moderately fragmented, with the top 4-5 key players collectively accounting for approximately 45-55% of lithium-ion battery pack revenue. Market concentration is declining as PLI-backed entrants commission capacity and new lithium-ion pack assemblers gain OEM supply contracts through 2028, broadening the competitive base.

Investment & Growth Opportunities

Highest Growth Segments

Lithium-ion battery packs (~12.5% CAGR), down tube position type (~11.3% CAGR), South India market (~11.5% CAGR from strong urbanisation), battery swapping network infrastructure (~25%+ CAGR from low base), solid-state battery technology (~30% CAGR from near-zero commercial base), and AI-enabled BMS as a standalone monetisable service represent the highest-growth investment vectors in the India e-bike battery market through 2034.

Emerging Investment Opportunities

Battery swapping infrastructure for commercial e-bike fleet electrification represents the market's highest per-capital emerging investment opportunity. Automated swapping stations enabling 90-second battery exchanges address the operational constraints of traditional charging for last-mile delivery fleets, with quick-commerce expansion across Tier 1 and Tier 2 cities creating a structurally growing demand pool that compounds through 2034.

Investment Themes

- PLI-Backed Domestic Lithium-Ion Cell Manufacturing: India's 50 GWh ACC PLI scheme creates a capital deployment framework for domestic cell manufacturing investment, enabling beneficiaries to achieve below-import-cost cell pricing by 2027-2028. Suppliers achieving domestic cell cost parity with Chinese imports gain a durable structural cost advantage in India's price-sensitive e-bike battery market that competitors dependent on imports cannot replicate.

- Battery Swapping Network Development for Commercial Fleet Electrification: India's commercial e-bike fleet electrification for last-mile delivery creates a battery-as-a-service model where swapping operators generate recurring revenue from fleet operators, decoupling battery upfront cost from vehicle purchase and addressing the primary affordability barrier for fleet electrification at scale across urban India.

Future Market Outlook (2026-2034)

The India e-bike battery market is projected to grow from USD 315.8 Million in 2025 to USD 737.8 Million by 2034, delivering a 9.89% CAGR over the forecast period. The market is expected to anchor at approximately USD 506.0 Million by 2030 as PLI-backed domestic cell manufacturing achieves commercial scale, lithium-ion battery costs fall below INR 8,000 per kWh, and battery swapping infrastructure reaches urban fleet maturity across Tier 1 cities.

Three structural forces define e-bike battery market growth through 2034. The e-bike fleet compounding demand from FAME II and successor policy continuity creates durable volume growth above the broader two-wheeler market. Lithium-ion displacement of lead-acid creates per-unit revenue mix improvement above volume growth rates. Battery swapping and AI-enabled BMS monetisation create new revenue streams beyond traditional battery pack supply, expanding total addressable market size above headline volume growth.

Research Methodology

Primary Research

Primary research comprised structured interviews with 50+ industry stakeholders in 2025, including e-bike OEM procurement leads, battery pack technology engineers, battery swapping network operators, government EV policy officials, and retail channel managers across North India, South India, and West India.

Secondary Research

Secondary research encompassed company annual reports, Ministry of Heavy Industries EV policy documents, FAME II scheme disbursement data, India EV data from SIAM and SMEV, lithium-ion cost trend data from Bloomberg NEF, PLI ACC scheme progress reports, and industry publications covering Indian electric mobility sector. Over 60 secondary sources were reviewed.

Forecasting Models

Market revenue forecasts were developed using a bottom-up demand model: e-bike unit sales forecast by segment type, average battery pack value per unit by chemistry and position type, technology mix shift assumptions for lithium-ion displacement of lead-acid, and policy continuity adjustment for FAME successor scheme incentive structures through the 2026-2034 forecast horizon.

India E-Bike Battery Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Battery Types Covered | Lithium-ion Battery, Lead Acid Battery, Others |

| Battery Pack Position Types Covered | Rear Carrier, Down Tube, In Frame |

| Regions Covered | North India, South India, East India, West India |

| Companies Covered | Exide Industries Ltd., Amara Raja Energy & Mobility Limited, Neuron Energy, Waaree Energies Ltd., Nana Industries, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India E-Bike Battery Market Report

The India e-bike battery market reached USD 315.8 Million in 2025, driven by lithium-ion battery dominance at 68.0%, rear carrier position type leading at 41.0%, North India commanding 30.0% share, and accelerating government subsidies under FAME II and the Electric Mobility Promotion Scheme 2024 reducing consumer acquisition barriers.

The India e-bike battery market grows at 9.89% CAGR during 2026-2034, reaching USD 737.8 Million by 2034. This growth reflects PLI-driven domestic cell manufacturing cost reduction, increasing lithium-ion penetration, battery swapping infrastructure expansion, and sustained FAME successor policy support for electric mobility across India.

Lithium-ion battery leads at 68.0%, capturing the mainstream e-bike market through superior energy density of 150-250 Wh/kg, faster charging capability, and rapidly declining costs from PLI-backed domestic cell manufacturing scale-up. Lithium-ion is projected to exceed 80% share by 2030 as lead-acid displacement accelerates.

Rear carrier leads at 41.0% through the lowest installation complexity and greatest compatibility with traditional bicycle frame structures used by Indian OEMs targeting affordable price points. Battery swap compatibility further reinforces rear carrier's commercial position across urban commercial delivery fleet deployments and swapping network models.

North India leads at 30.0% through Delhi-NCR urbanisation, Uttar Pradesh's high per-vehicle EV subsidy, last-mile delivery fleet electrification by quick-commerce players, and manufacturing hub proximity reducing distribution costs for battery suppliers serving the metropolitan market.

Leading companies include Exide Industries Ltd., Amara Raja Energy & Mobility Limited, Neuron Energy, Waaree Energies Ltd., Nana Industries, and others.

The India e-bike battery market is projected to reach approximately USD 506.0 Million by 2030, with domestic lithium-ion cell manufacturing reaching commercial scale, battery swapping networks achieving urban maturity across Tier 1 cities, and solid-state battery prototypes beginning early commercial evaluation by premium e-bike OEMs.

Three priority investment opportunities: PLI-backed domestic lithium-ion cell manufacturing for structural cost advantage, battery swapping network development creating recurring fleet service revenue, and AI-enabled BMS as a standalone monetisable technology layer generating software-as-a-service revenue above hardware battery pack sales to e-bike OEMs and fleet operators.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)