India E-KYC Market Size, Share, Trends and Forecast by Product, Deployment Mode, End User, and Region, 2026-2034

India E-KYC Market Summary:

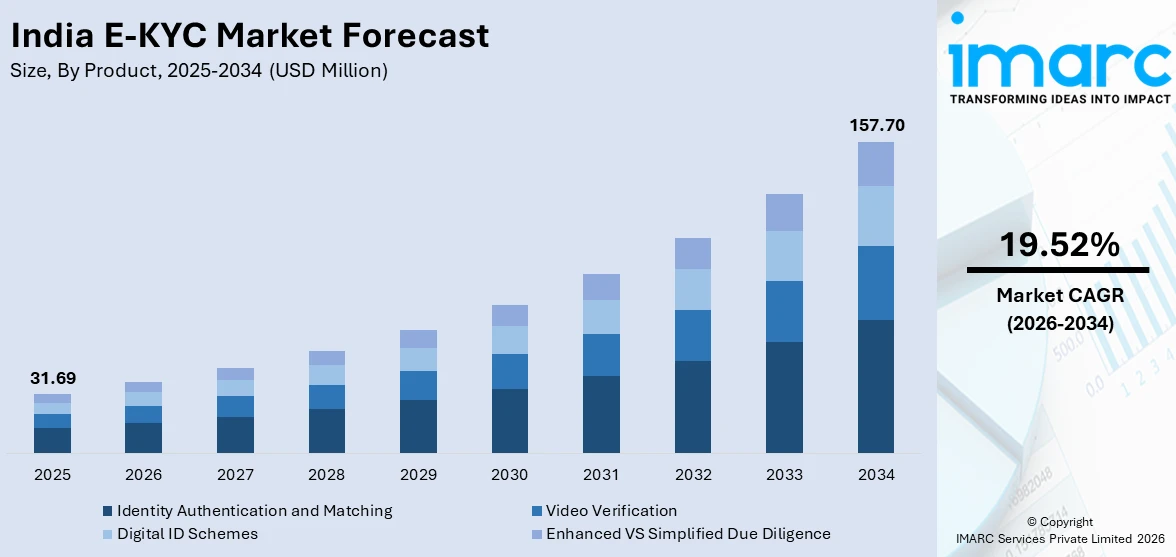

The India e-KYC market size was valued at USD 31.69 Million in 2025 and is projected to reach USD 157.70 Million by 2034, growing at a compound annual growth rate of 19.52% from 2026-2034.

The India e-KYC market is experiencing accelerated growth as the nation deepens its commitment to digital identity verification and financial inclusion. Regulatory mandates from the Reserve Bank of India, expanding Aadhaar authentication infrastructure, and rising adoption of cloud-based verification platforms are collectively driving institutional demand. The convergence of government-led digital initiatives, biometric technology advancements, and the growing fintech ecosystem participation is reshaping client onboarding processes and contributing to the India e-KYC market share.

Key Takeaways and Insights:

- By Product: Identity authentication and matching represent the largest segment with a market share of 32% in 2025, driven by the dominance of Aadhaar-based real-time verification infrastructure enabling secure and instantaneous identity validation across banking, telecom, and government sectors.

- By Deployment Mode: Cloud-based leads the market with a share of 55% in 2025, owing to scalable infrastructure, cost-effectiveness, and the growing preference of financial institutions for flexible and rapidly deployable digital verification platforms.

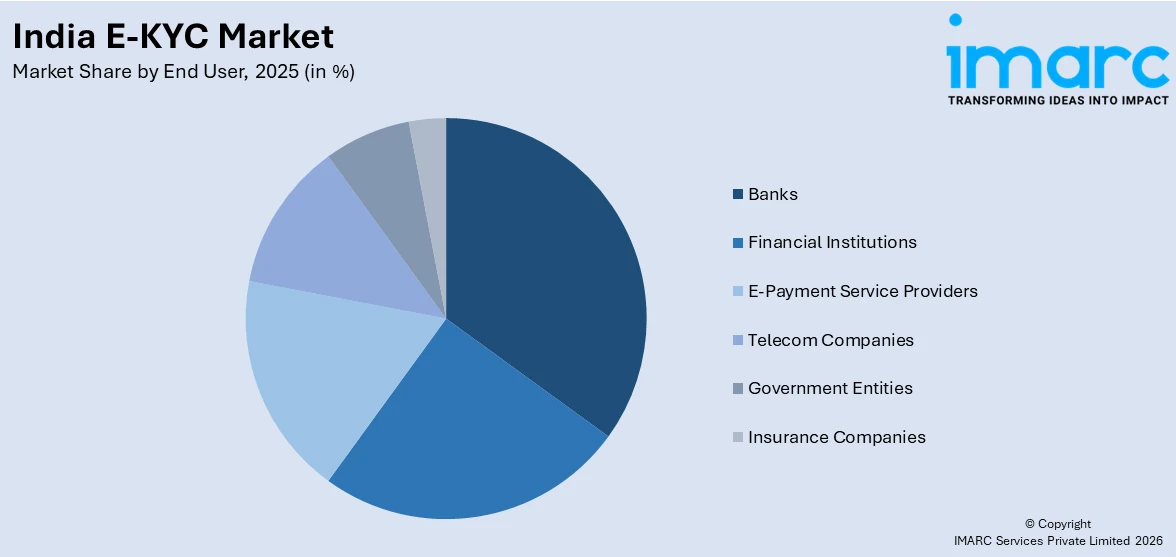

- By End User: Banks dominate the market with a share of 28% in 2025, reflecting stringent regulatory compliance requirements, accelerated digital transformation initiatives, and increasing integration of advanced verification technologies into client onboarding workflows.

- By Region: North India represents the largest segment with a market share of 30% in 2025, supported by the concentration of major banking headquarters, fintech hubs, government administrative centers, and advanced digital infrastructure in the Delhi-NCR region.

- Key Players: The India e-KYC market exhibits a competitive landscape with established technology corporations, specialized identity verification startups, and government-backed platforms competing through advanced biometric innovation, cloud-native architectures, and strategic regulatory partnerships.

To get more information on this market Request Sample

The India E-KYC market is being driven by rapid digital adoption across banking, fintech, telecom, and public services, where instant and paperless identity verification is becoming a critical requirement. Organizations are increasingly shifting from manual documentation to electronic authentication to improve onboarding speed, enhance compliance, and reduce operational costs. Aadhaar-enabled infrastructure continues to support large-scale verification, strengthening trust in digital KYC frameworks. This momentum is reflected in the growing transaction volumes, as the Aadhaar-enabled e-KYC service recorded 37.3 crore transactions in April 2025, representing a 39.7% year-on-year increase, while cumulative e-KYC transactions reached 2,393 Crore by April 30, 2025. Rising smartphone penetration, artificial intelligence (AI)-based biometric authentication, and supportive regulatory initiatives are further expanding adoption across sectors, positioning E-KYC as a key enabler of secure digital service delivery in India.

India E-KYC Market Trends:

Surge in Aadhaar-Based Digital Authentication Volumes

India’s E-KYC market is being strongly driven by the expanding use of Aadhaar-enabled digital identity verification across financial services, telecommunications, and digital platforms. The growing preference for instant, paperless onboarding is positioning Aadhaar authentication as a foundational infrastructure supporting large-scale electronic verification. As per IBEF in 2025, India has exceeded 150 billion (15,011.82 crore) Aadhaar authentication transactions, with close to 210 crore transactions occurring in April alone, indicating an 8% increase compared to the previous year. Such volumes highlight the maturity and scalability of the ecosystem, encouraging wider adoption of E-KYC solutions and strengthening the market growth across sectors requiring secure digital onboarding.

Rapid Adoption of AI-Powered Biometric Verification

The increasing use of AI-driven biometric verification is a key factor accelerating India’s E-KYC market growth by improving identity accuracy and reducing fraud risks. Aadhaar Face Authentication solutions are gaining strong traction, offering secure and convenient verification through simple face scans across both Android and iOS platforms. This modality is being widely adopted in citizen-focused services, with nearly 60% of Digital Life Certificates generated by pensioners in November using Aadhaar face authentication. The scale is expanding rapidly, as 28.29 crore face authentication transactions were executed in November 2025, compared to 12.04 crore during the same month in 2024, reflecting rising institutional confidence.

Regulatory Approvals Expanding Adoption in Capital Markets

Supportive regulatory developments are playing a crucial role in bolstering the growth of India e-KYC market, particularly by enabling wider adoption across new financial segments. Strong compliance requirements in the securities industry have increased demand for faster, paperless investor verification systems. In 2025, SEBI approved NPCI and UIDAI’s e-KYC Setu System for Aadhaar-based digital KYC in the securities market. This interface allowed registered intermediaries, such as stockbrokers and mutual fund distributors, to conduct secure and efficient onboarding. Such initiatives strengthen digital compliance, improve client experience, and broaden e-KYC penetration beyond traditional banking.

Market Outlook 2026-2034:

The India e-KYC market demonstrates strong revenue growth potential throughout the forecast period, driven by digital transformation initiatives and regulatory mandates. The market generated a revenue of USD 31.69 Million in 2025 and is projected to reach a revenue of USD 157.70 Million by 2034, growing at a compound annual growth rate of 19.52% from 2026-2034. Expanding Aadhaar infrastructure, rising adoption of cloud-based verification platforms, and the growing demand from financial institutions and government entities are expected to sustain strong revenue expansion across the India e-KYC ecosystem.

India E-KYC Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Product |

Identity Authentication and Matching |

32% |

|

Deployment Mode |

Cloud-based |

55% |

|

End User |

Banks |

28% |

|

Region |

North India |

30% |

Product Insights:

- Identity Authentication and Matching

- Video Verification

- Digital ID Schemes

- Enhanced VS Simplified Due Diligence

Identity authentication and matching dominate with a market share of 32% of the total India e-KYC market in 2025.

Identity authentication and matching account for the majority of the market share attributed to the central role these solutions play in enabling secure digital onboarding across financial and non-financial sectors. Banks, fintech companies, telecom operators, and government service platforms rely heavily on accurate identity verification to prevent fraud, ensure regulatory compliance, and streamline client acquisition. Authentication tools, such as biometric matching, document validation, and database cross-checking, are essential for building trust in digital transactions, making them the most widely adopted components of e-KYC systems.

The dominance of the segment is further reinforced by India’s rapidly expanding digital economy and the increasing shift toward paperless service delivery. Rising volumes of online financial services, digital payments, and remote account openings require fast and reliable identity matching mechanisms. Organizations prioritize solutions that offer real time verification, strong security features, and seamless integration with national identity frameworks. As regulatory scrutiny increases and fraud risks evolve, demand continues to grow for advanced authentication technologies, supporting their leading position within the e-KYC product landscape.

Deployment Mode Insights:

- Cloud-based

- On-premises

Cloud-based leads with a market share of 55% of the total India e-KYC market in 2025.

Cloud-based holds the biggest market share due to its ability to offer scalable, cost-effective, and rapidly deployable solutions for organizations of all sizes. India's cloud computing sector, valued at approximately USD 37.11 Billion in 2025, as per the IMARC Group, is driving this shift as financial institutions and government agencies migrate verification workloads to cloud environments. The flexibility of cloud deployment enables real-time processing capabilities essential for high-volume Aadhaar authentication operations across diverse geographic locations.

The dominance of cloud-based e-KYC is further strengthened by the shift toward remote service delivery and the need for secure, flexible access across locations. Organizations benefit from reduced upfront infrastructure investment and improved operational agility through cloud deployment. Advanced security frameworks, encryption standards, and continuous monitoring capabilities also enhance trust in cloud systems. As businesses prioritize digital transformation and regulators encourage efficient verification processes, cloud-based platforms continue to gain traction, supporting their leading role in India’s e-KYC deployment landscape.

End User Insights:

Access the comprehensive market breakdown Request Sample

- Banks

- Financial Institutions

- E-Payment Service Providers

- Telecom Companies

- Government Entities

- Insurance Companies

Banks exhibit a clear dominance with a 28% share of the total India e-KYC market in 2025.

Banks represent the largest segment, driven by stringent regulatory requirements and accelerating digital transformation initiatives. A Reserve Bank of India survey conducted in November 2024 assessing 12 state-owned and 19 private sector banks found that AI and ML technologies are predominantly utilized in customer service, sales, marketing, risk management, and KYC processes. This institutional adoption of advanced technologies reinforces banks' position as primary users of e-KYC solutions. Regulatory mandates from financial authorities further strengthen the adoption of e-KYC systems within the banking sector.

The dominance of banks is also supported by India’s accelerating shift toward digital payments and branchless banking models. As banks expand financial inclusion initiatives and reach underserved populations through online channels, e-KYC becomes essential for enabling remote onboarding. Integration with national identity systems and biometric verification improves operational efficiency while reducing paperwork and processing time. Banks also invest heavily in advanced compliance technologies to mitigate fraud and meet evolving regulatory standards, reinforcing their leading position as the primary end users in the India e-KYC market.

Regional Insights:

- North India

- West and Central India

- South India

- East and Northeast India

North India dominates with a market share of 30% of the total India e-KYC market in 2025.

North India leads the market owing to its high concentration of financial institutions, corporate headquarters, and digitally active urban centers. Major cities in the region host large banking networks, fintech hubs, telecom operators, and government offices that require extensive identity verification for service delivery. Strong demand for digital onboarding across sectors, such as banking, insurance, and telecommunications supports widespread adoption of e-KYC solutions. The region’s large population base and rising digital penetration further contribute to higher verification volumes.

The dominance of North India is also reinforced by rapid growth in digital infrastructure, increasing smartphone usage, and expanding access to online financial services. Urbanization and the presence of large commercial markets encourage businesses to adopt efficient client verification systems. Government led digital initiatives and regulatory compliance requirements are also more actively implemented through institutions based in this region. In 2025, the Delhi High Court ordered mandatory e-KYC for all domain name registrations to curb online scams and fake websites. The ruling removed automatic privacy protection, making verified identity checks essential to prevent criminals from hiding behind anonymous domains.

Market Dynamics:

Growth Drivers:

Why is the India E-KYC Market Growing?

Increased Smartphone and Internet Penetration Across Regions

The growth of the India e-KYC market is driven by the widespread adoption of mobile devices, which serve as the primary gateway for remote identity verification. As digital infrastructure matures, the ability of service providers to onboard users in previously inaccessible regions depends heavily on hardware availability. This trend is substantiated by the Results of the Comprehensive Modular Survey: Telecom (2025), which revealed that smartphone ownership among youth aged 15–29 has reached near-universal levels, standing at 95.5% in rural areas and 97.6% in urban centers. Such high levels of device penetration among the most economically active demographic allow financial institutions and telecom operators to bypass physical touchpoints entirely. By leveraging this existing mobile ecosystem, e-KYC solutions can achieve unprecedented scale, fostering greater financial inclusion and strengthening the market demand across diverse geographic and socioeconomic segments of the country.

Regulatory Modernization and Enhanced KYC Mandates

India’s regulatory framework for digital identity verification is undergoing steady modernization, creating sustained demand for e-KYC solutions across regulated sectors. Policymakers are increasingly focusing on improving accessibility, continuity, and compliance within customer verification processes. In this direction, the RBI issued revised KYC norms on 12 June 2025, allowing customers to update KYC through banking correspondents, digital channels such as Aadhaar OTP and Video KYC, and at any branch rather than only the home branch. These measures are designed to reduce dormant accounts and ensure uninterrupted access to welfare-linked funds, particularly for rural and low-risk clients, reinforcing the role of e-KYC in inclusive financial infrastructure.

Advanced Fraud-Resistant Technologies

The growing threat of AI-driven identity fraud is driving adoption of more secure and intelligent solutions. Financial institutions are increasingly prioritizing verification systems that combine speed with strong fraud prevention capabilities. In 2024, Finacus Solutions partnered with AI startup pi-labs.ai to launch a deepfake-proof e-KYC solution in India, integrating advanced deepfake detection into Video KYC workflows. This approach aligns with the RBI’s emphasis on live video-based verification while adding enhanced security layers. Such innovations strengthen institutional confidence, reduce fraud exposure, and contribute to the market growth by ensuring secure digital onboarding.

Market Restraints:

What Challenges the India E-KYC Market is Facing?

Data Privacy and Security Compliance Burden

Stringent data protection regulations, including the Digital Personal Data Protection Act 2023 with penalties reaching up to INR 250 crore per breach and mandatory 72-hour breach notification requirements, create significant compliance challenges for e-KYC providers. Organizations must implement comprehensive consent management frameworks, conduct regular data protection impact assessments, and maintain robust security infrastructure, increasing operational complexity and costs across the value chain.

Integration Complexity with Legacy Systems

Many traditional financial institutions and government organizations operate on legacy technology infrastructure that presents significant challenges when integrating modern e-KYC platforms. The requirement to comply simultaneously with multiple regulatory frameworks, including PCI-DSS, FIPS 140-2, and NIST standards, necessitates complex technical architectures, demanding extensive infrastructure analysis, system upgrades, and specialized technical expertise before successful deployment.

Cost Barriers for Smaller Financial Entities

Smaller banks, non-banking financial companies, and cooperative institutions face substantial financial barriers in adopting advanced e-KYC solutions due to high implementation costs and technology infrastructure requirements. The need to appoint Data Protection Officers, conduct annual data protection impact assessments, and maintain independent audit capabilities under evolving regulatory frameworks places disproportionate financial pressure on resource-constrained organizations.

Competitive Landscape:

The India e-KYC market features a dynamic competitive environment characterized by established technology corporations, specialized identity verification startups, and government-backed platforms operating across multiple deployment models and end-user segments. Market participants are differentiating through advanced AI capabilities, biometric innovation, and regulatory compliance solutions. Competition is intensifying as organizations invest in cloud-native platforms, face authentication technologies, and seamless integration frameworks to capture the growing demand from banking, financial services, telecom, and government sectors. Strategic partnerships with regulatory bodies and financial institutions are emerging as critical competitive advantages in this rapidly evolving market.

Recent Developments:

- August 2025: UIDAI onboarded Starlink Satellite Communication Pvt Ltd to use Aadhaar-based authentication for customer verification in India. This enabled a faster, paperless, and secure onboarding process compliant with KYC norms, supporting seamless access to satellite internet services. The move highlighted the strength of India’s digital public infrastructure, showing how Aadhaar e-KYC can partner with global technology providers to improve service delivery while maintaining transparency and regulatory compliance.

- July 2025: The Department of Posts expanded Aadhaar-based biometric e-KYC services to include Recurring Deposit (RD) and Public Provident Fund (PPF) accounts, effective from 27 June 2025. This allowed depositors to open accounts, make deposits, process loans, and withdraw funds without paper forms at CBS post offices. The initiative strengthens digital banking access, especially in rural areas, while improving security through mandatory Aadhaar masking on all documents.

India e-KYC Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Products Covered | Identity Authentication and Matching, Video Verification, Digital ID Schemes, Enhanced VS Simplified Due Diligence |

| Deployment Modes Covered | Cloud-based, On-premises |

| End Users Covered | Banks, Financial Institutions, E-Payment Service Providers, Telecom Companies, Government Entities, Insurance Companies |

| Regions Covered | North India, West and Central India, South India, East and Northeast India |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India e-KYC Market Report

The India e-KYC market size was valued at USD 31.69 Million in 2025.

The India e-KYC market is expected to grow at a compound annual growth rate of 19.52% from 2026-2034 to reach USD 157.70 Million by 2034.

Identity authentication and matching hold the largest revenue share of 32% in 2025, driven by the dominance of Aadhaar-based real-time verification infrastructure enabling secure identity validation across banking, telecom, and government sectors.

Key factors driving the India e-KYC market include supportive regulatory developments enabling adoption across new financial segments. In 2025, SEBI approved NPCI and UIDAI’s e-KYC Setu System for Aadhaar-based KYC in securities, allowing stockbrokers and mutual fund distributors to onboard investors securely.

Major challenges include stringent data privacy and security compliance requirements under the DPDP Act, integration complexity with legacy banking systems, cost barriers for smaller financial entities, and managing consent frameworks across multiple regulatory jurisdictions.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)