India E-Waste Management Market Size, Share, Trends and Forecast by Material Type, Source Type, Application, and Region, 2026-2034

India E-Waste Management Market Size, Share, Trends & Forecast (2026-2034)

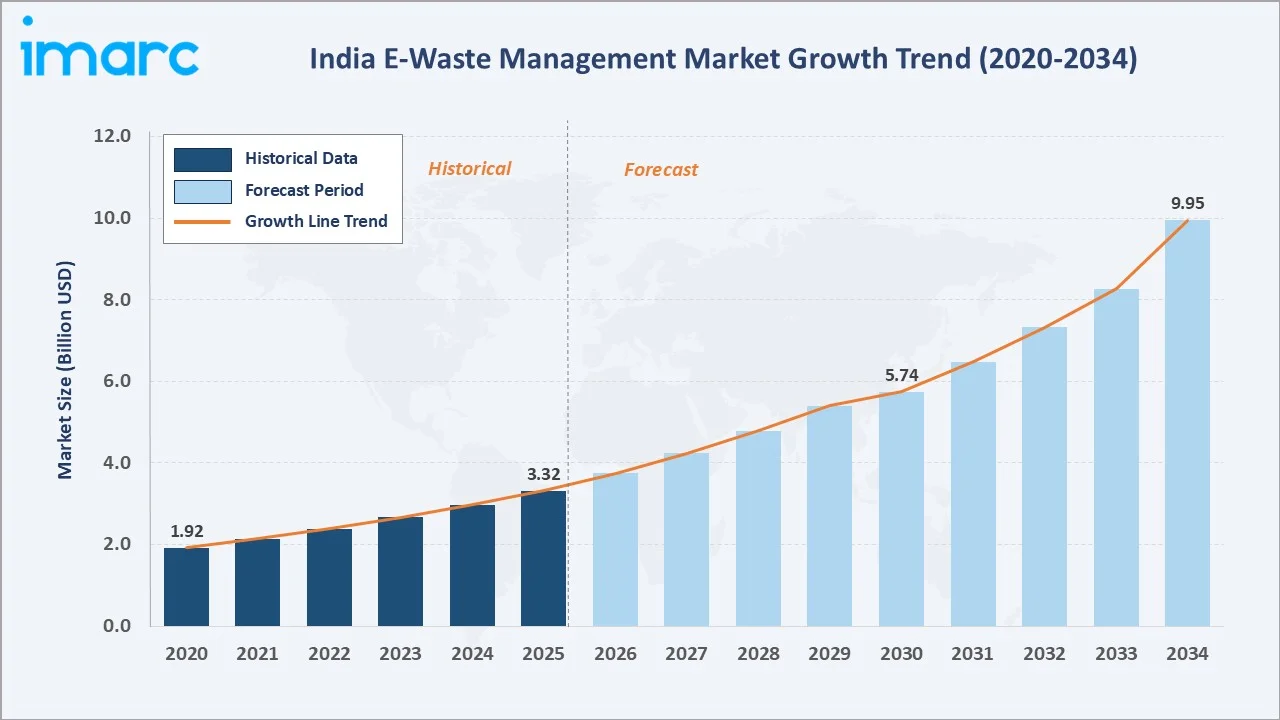

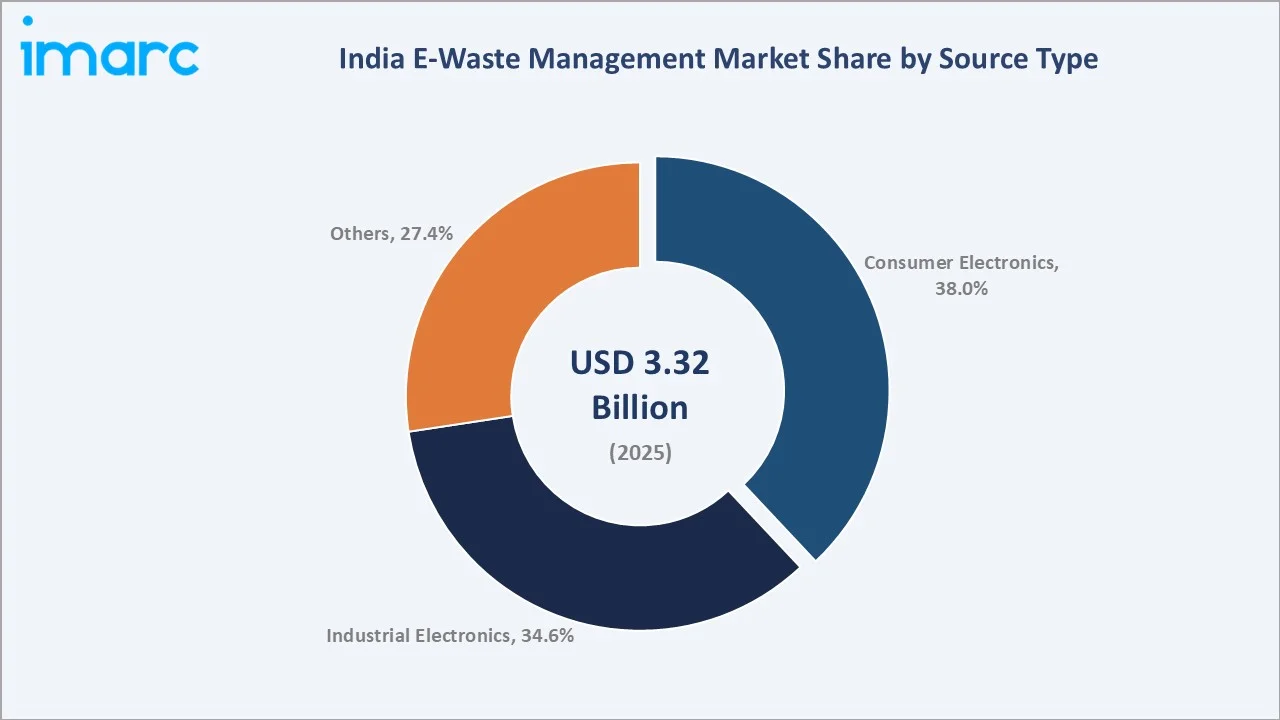

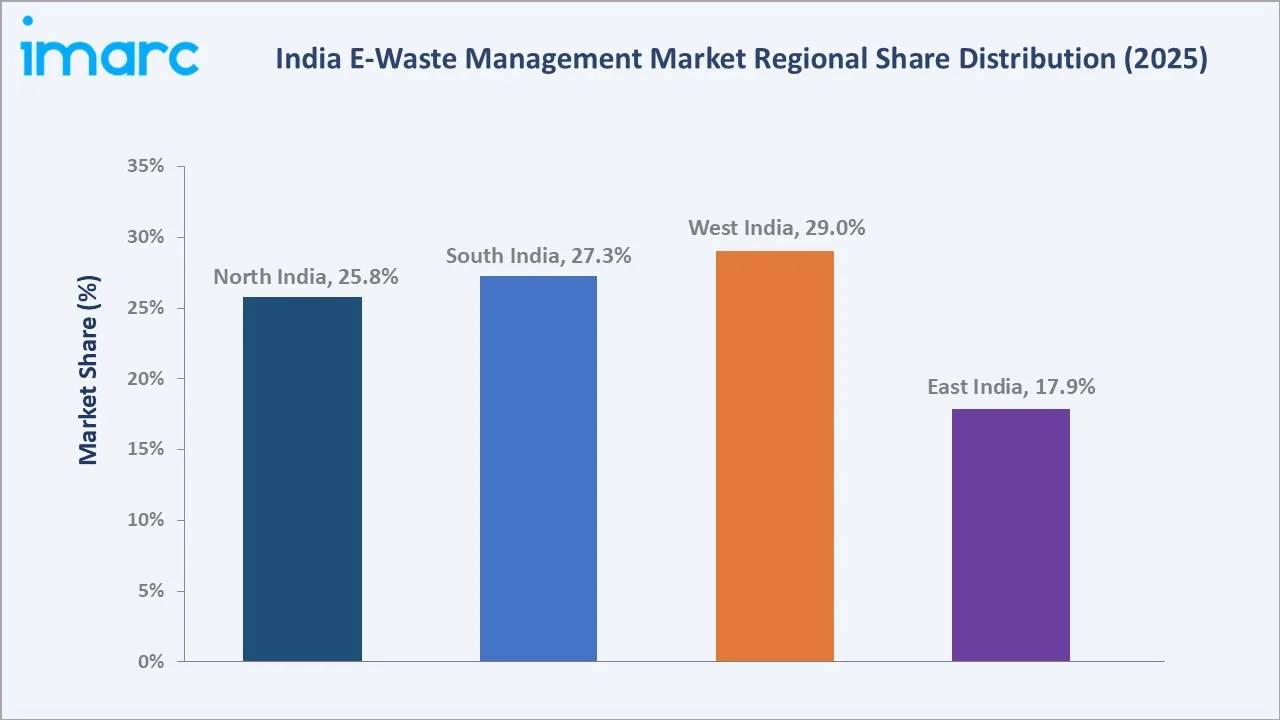

The India e-waste management market reached USD 3.32 Billion in 2025 and is projected to reach USD 9.95 Billion by 2034, growing at a CAGR of 11.59% during 2026-2034. The market is driven by rapid urbanization, rising consumer electronics adoption, and increasingly stringent regulatory frameworks including the E-Waste (Management) Rules, 2022. According to the Central Pollution Control Board (CPCB), India generated 13.97 lakh tonnes of e-waste in FY 2024-25, up from 12.54 lakh tonnes in FY 2023-24. Metal dominates at 46.0% by material type. Consumer Electronics leads at 38.0% by source type. West India commands 29.0% of the national market share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 3.32 Billion |

|

Forecast Market Size (2034) |

USD 9.95 Billion |

|

CAGR (2026-2034) |

11.59% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Material Type |

Metal (46.0%, 2025) |

|

Dominant Source Type |

Consumer Electronics (38.0%, 2025) |

|

Leading Region |

West India (29.0%, 2025) |

India e-waste management market expanded from USD 1.92 Billion in 2020 to USD 3.32 Billion in 2025, anchored at USD 5.74 Billion in 2030, and forecast to reach USD 9.95 Billion by 2034. The formal recycling rate improved from approximately 22% in 2019-20 to over 70% in 2024-25, creating a structural shift from informal to organized processing.

To get more information on this market, Request Sample

The E-Waste (Management) Rules, 2022 mandate manufacturers and producers to achieve specific recycling targets - starting at 60% collection for FY 2023-24 and increasing to 80% by FY 2027-28. Metal segment leads through high economic value of recoverable precious metals including gold, silver, and copper. The industrial electronics segment is growing driven by India's expanding IT and telecom infrastructure replacement cycles.

.webp)

Executive Summary

India e-waste management market at USD 3.32 Billion in 2025 represents one of the fastest-growing segments of the environmental services industry in South Asia. India is the third-largest e-waste producer globally, after China and the United States, generating approximately 2.54 lakh MT in FY 2023-24. The formal recycling ecosystem has undergone transformative expansion, with the formal e-waste recycling rate improving from approximately 22% in 2019-20 to over 70% in 2024-25. The market is projected to reach USD 9.95 Billion by 2034, reflecting the deepening formalization of the recycling value chain, rising precious metal recovery economics, and government-mandated Extended Producer Responsibility (EPR) compliance frameworks.

The regulatory landscape is the primary growth catalyst. The E-Waste (Management) Rules, 2022, effective April 1, 2023, expanded coverage to 106 categories of electrical and electronic equipment (EEE) and introduced mandatory EPR targets with environmental compensation penalties for non-compliance. The Indian government in 2025 cleared an INR 1,500-crore incentive for critical minerals recycling focused on lithium and rare-earth element recovery from electronic waste and batteries, underscoring the strategic importance of the sector.

Metal at 46.0% leads through the high economic value of precious and non-precious metal recovery. Consumer Electronics dominates source type at 38.0% driven by smartphone penetration and shortening product replacement cycles. West India leads regionally at 29.0%, supported by Maharashtra's electronics-manufacturing density and Gujarat's metallurgical clusters.

Key Market Insights

|

Insight |

Data |

|

Dominant Material Type |

Metal - 46.0% share (2025) |

|

Dominant Source Type |

Consumer Electronics - 38.0% share (2025) |

|

Leading Region |

West India - 29.0% share (2025) |

|

Key Players |

Attero Recycling Pvt. Ltd., Eco Recycling Ltd. (Ecoreco), Cerebra Integrated Technologies, Re Sustainability, and Namo eWaste Management Ltd. |

|

Market Opportunity |

EPR compliance expansion, precious metal recovery technology, formal sector growth in Tier-2 cities, urban mining infrastructure |

Key Analytical Observations Supporting The Above Data:

- Metal at 46.0% (2025): Metal dominates due to the high economic value of recoverable precious metals - gold, silver, and copper - from discarded electronics. India's CPCB-authorized facilities process over 1 million MT of e-waste annually, with metal recovery representing the primary revenue driver for formal recyclers.

- Consumer Electronics at 38.0% (2025): Consumer electronics dominate because India sold approximately 150 million smartphones in 2025. Shortening device replacement cycles - now 2.5 to 3 years on average - continuously increase the volume of end-of-life devices entering the recycling stream.

- West India at 29.0% (2025): West India leads through Maharashtra's electronics manufacturing density, Mumbai's BFSI sector server refresh cycles, and Gujarat's established metallurgical processing infrastructure.

- Market CAGR of 11.59% (2026-2034): The above-average growth reflects EPR policy enforcement escalation, rising precious metal commodity prices, and India's National Critical Mineral Mission driving investment in urban mining infrastructure.

India E-Waste Management Market Overview

India e-waste management industry encompasses the collection, transportation, pre-processing, dismantling, material recovery, and secondary market distribution of end-of-life electrical and electronic equipment (EEE). The sector operates under the regulatory authority of the Central Pollution Control Board (CPCB) and State Pollution Control Boards (SPCBs), with approximately 450 authorized recycling facilities registered as of 2024-2025. India's e-waste ecosystem is one of the most complex in the emerging world, integrating a formally expanding organized sector, a deeply entrenched informal sector engaging over 1 million people, and a growing EPR certificate trading marketplace.

The macroeconomic drivers include India's rapidly expanding digital infrastructure - the government's Digital India Mission has accelerated electronics penetration across rural and urban segments - combined with rising disposable incomes creating faster device replacement cycles. The E-Waste (Management) Rules, 2022 expanded regulatory coverage from 21 to 106 equipment categories, dramatically increasing the addressable e-waste volume under formal management. India generated 14.14 lakh metric tonnes of e-waste in FY 2025-26 so far, reflecting a consistent upward trajectory. GST input-credit provisions are widening the cost advantage of compliant recyclers over informal handlers, accelerating formal sector investment.

Market Dynamics

To evaluate market opportunities, Request Sample

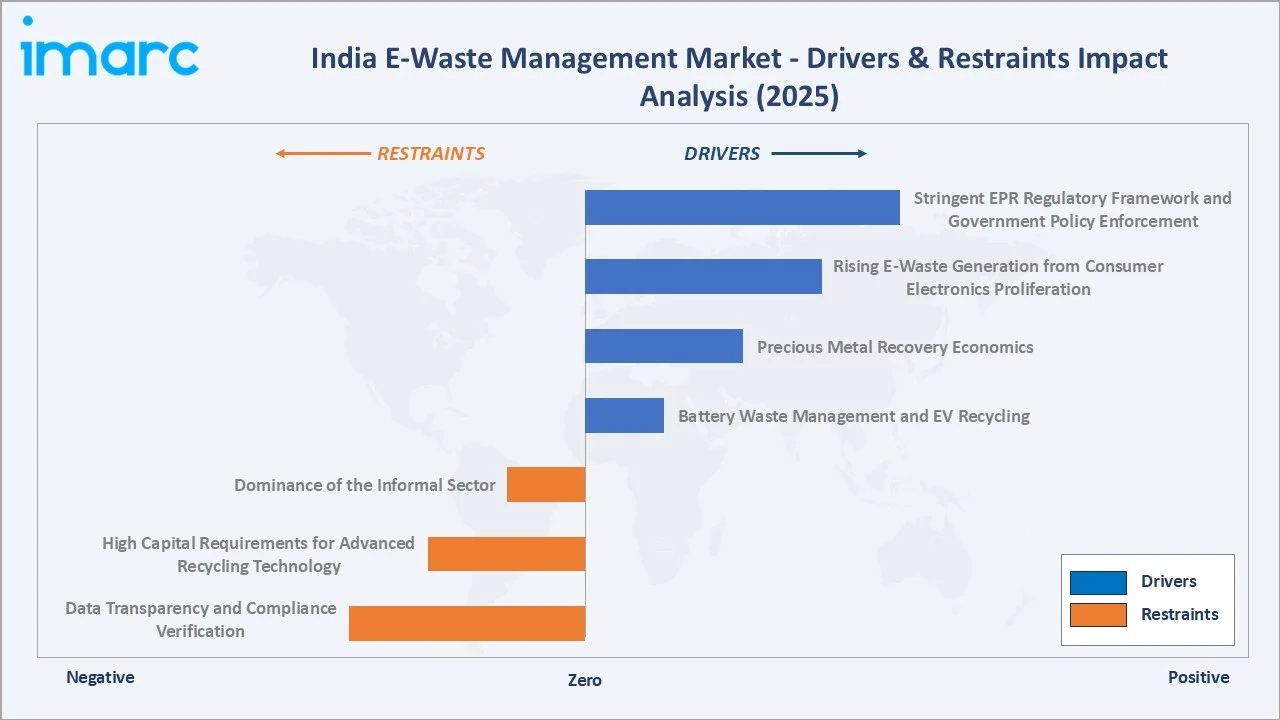

Market Drivers

- Stringent EPR Regulatory Framework and Government Policy Enforcement: The E-Waste (Management) Rules, 2022, effective April 1, 2023, mandate 60% mandatory collection targets for FY 2023-24 scaling to 80% by FY 2027-28, creating structural demand for authorized recyclers. Environmental compensation penalties and CPCB audits, intensified in February 2025, are shifting recycling costs to producers, expanding the volume of waste channeled through formal facilities. The Indian government cleared INR 1,500 crore in June 2025 for critical minerals recycling incentives, focused on lithium and rare-earth recovery from electronic waste and batteries.

- Rising E-Waste Generation from Consumer Electronics Proliferation: India sold approximately 150 million smartphones in 2025 with average replacement cycles of 2.5 to 3 years, continuously expanding the volume of end-of-life devices entering formal recycling streams. Digital India Mission and expanding 5G infrastructure are accelerating enterprise IT equipment refresh cycles, adding industrial e-waste volumes to authorized recycler pipelines.

- Precious Metal Recovery Economics: Hydrometallurgical processing now enables 98% precious metal recovery rates, with gold, silver, copper, cobalt, and lithium recovery from PCBs and batteries creating commercially attractive unit economics independent of regulatory drivers. Attero Recycling's proprietary technology holds over 45 patents and achieves copper purity above 99.95%, enabling direct sales to domestic wire-and-cable mills at premium pricing. The economics of urban mining are becoming independently compelling beyond regulatory compliance. At scale, formal recyclers extract revenue streams from recovered gold, silver, copper, lithium, cobalt, and rare earth elements that significantly exceed the cost of collection and processing.

Market Restraints

- Dominance of the Informal Sector: Approximately 30% of India's e-waste still enters informal channels despite regulatory progress. The informal sector's lower cost structure, relying on manual labor without environmental controls, creates price competition that formal recyclers struggle to match for low-value waste streams. More than 70% of remaining informally handled e-waste is processed unsafely, releasing lead, cadmium, and mercury into soil and water systems, creating both public health risks and regulatory enforcement challenges.

- High Capital Requirements for Advanced Recycling Technology: Hydrometallurgical plants require capital investment of INR 50 crore to INR 200 crore, creating barriers for new entrants and limiting geographic expansion of formal processing capacity beyond major industrial centers. Annual labor cost inflation of 10-12% in urban centers is increasing operational costs for formal recyclers, narrowing margins particularly for collection and logistics operations.

Market Opportunities

- Battery Waste Management and EV Recycling: India's Battery Waste Management Rules 2022 are creating a USD multi-billion recycling opportunity as the first generation of electric vehicles reaches end of life through 2028-2030. Lithium, cobalt, and nickel recovery from EV batteries represents the highest-growth sub-segment. Namo eWaste commissioned a 12,240 MTPA Li-Ion Battery Recycling plant in Nashik in July 2025, funded entirely by IPO proceeds, reflecting investor confidence in battery recycling economics.

- Tier-2 City Formal Sector Expansion: India's Tier-2 and Tier-3 cities generate substantial e-waste volumes but are underserved by authorized recycling infrastructure. Re Sustainability is piloting decentralized micro-plants to reduce reverse-logistics costs and serve emerging industrial clusters, creating a scalable geographic expansion model. The EPR portal's digital traceability requirements are creating opportunities for technology platforms to aggregate informal collectors into formal supply chains, expanding collection network reach without proportional capital investment.

Market Challenges

- Data Transparency and Compliance Verification: CPCB estimates e-waste generation based on average life cycles of 106 EEE categories, creating a gap between estimated generation volumes and actual tracked material flows. Verification and audit mechanisms are still maturing, creating compliance uncertainty for formal operators. EPR certificate trading platform integrity is an emerging regulatory risk, with CPCB intensifying audits in February 2025 to address fraudulent certificate claims.

- Skilled Workforce Shortage for Advanced Processing: Hydrometallurgical and advanced separation processes require specialized technical expertise that India's vocational training infrastructure is still developing. Labor cost inflation of 10-12% annually in urban centers exacerbates the skilled workforce challenge for capital-intensive formal recyclers.

Emerging Market Trends

1. Digitalization of the Scrap Supply Chain

Attero's MetalMandi platform, launched in January 2025, is formalizing India's USD 100 billion unorganized scrap market by enabling transparent AI-driven pricing and secure logistics for scrap dealers nationwide. The platform targets 1,000 tonnes of daily transactions and demonstrates the commercial viability of digital aggregation models. By making 70% of Attero's e-waste sourcing traceable, MetalMandi is creating a replicable model for digital supply chain formalization.

2. AI-Powered Optical Sorting and Robotic Pre-processing

Leading formal recyclers are deploying AI-driven vision systems for automated PCB identification and sorting, improving material purity and reducing manual labor dependency. This technological differentiation is widening the unit economics gap between formal and informal operators.

3. ESG-Linked Finance and Capital Market Participation

Namo eWaste's oversubscribed NSE SME listing in September 2024 demonstrates growing investor appetite for circular-economy plays. Formal recyclers are bundling certified disposal with carbon-credit consulting services to capture multinational decarbonization budgets, creating premium revenue streams beyond basic recycling service fees. India's National Critical Mineral Mission is directing government capital toward e-waste recycling infrastructure as a strategic resource security priority.

4. Urban Mining as a Strategic Resource Security Initiative

India's import dependence on critical minerals - lithium, cobalt, nickel, and rare earth elements - is positioning domestic e-waste recycling as a national resource security strategy. The INR 1,500-crore government incentive cleared in June 2025 for critical minerals recycling reflects this strategic framing. Cerebra Integrated Technologies' 90,000-tonne annual capacity plant in Bengaluru exemplifies the scale of authorized infrastructure being built to capture domestic urban mining opportunity.

Industry Value Chain Analysis

India e-waste value chain integrates formal and informal operators across collection, pre-processing, material recovery, and secondary market distribution stages. The value chain's commercial structure is evolving rapidly as EPR regulations shift financial responsibility upstream to producers and digital platforms create traceability across previously opaque informal collection networks.

|

Stage |

Key Participants |

|

Collection & Reverse Logistics |

Authorized e-waste collectors, PROs (Producer Responsibility Organizations), informal aggregators transitioning to formal networks, doorstep take-back services |

|

Sorting & Disassembly |

CPCB-authorized dismantlers, certified pre-processing facilities, informal sector dismantlers being integrated into formal channels |

|

Pre-processing & Shredding |

Authorized recycling facilities with mechanical shredders, AI-powered optical separators, ferrous and non-ferrous separation units |

|

Recycling & Material Recovery |

Formal recyclers with hydrometallurgical and pyrometallurgical capabilities, precious metal recovery units, plastics granulators |

|

Material Refining |

Smelters, electro-refining facilities, plastics compounders, glass processors converting recovered materials into secondary raw materials |

|

Secondary Market & Compliance |

EPR certificate trading platforms, secondary metal traders, recycled plastics markets, CPCB-registered compliance management firms |

The collection and reverse logistics stage is India e-waste value chain's most commercially competitive and margin-constrained stage. Formal recyclers are investing in partnerships with informal collectors - integrating them into EPR-compliant supply chains through digital platforms while maintaining cost competitiveness. Pre-processing and material recovery represent the highest-value stages, where hydrometallurgical technology investments create proprietary competitive advantages.

Technology Landscape in the India E-Waste Management Industry

Hydrometallurgical Processing Technology

Hydrometallurgy is the standout technology in India's e-waste management market, projected at 8.74% CAGR through 2031. Selective leaching processes minimize dioxin emissions and energy requirements versus pyrometallurgical smelting, while zero-discharge circuits recycle acids and process water, reducing environmental compliance costs. Attero's proprietary hydrometallurgical processes extract 98% of precious metals from PCBs, achieving gold, silver, cobalt, and copper recovery at purity levels competitive with primary mining.

AI-Powered Sorting and Robotic Disassembly

AI-based optical separators and robotic PCB depopulation systems are transforming the pre-processing stage. These systems improve material purity, increase throughput, and reduce dependence on manual labor. Vision systems identify material composition at the component level, directing automated sorting to separate ferrous, non-ferrous, and precious metal-bearing streams with higher accuracy than manual dismantling. RecycleKaro launched India's first Plasma Furnace Technology unit for e-waste in March 2024, targeting 75,000 MT per annum capacity for extraction of precious and rare metals from e-waste and industrial residue.

Battery Recycling and Black Mass Processing

Li-ion battery recycling is the fastest-growing technology application in India's e-waste sector, driven by Battery Waste Management Rules 2022 and India's EV adoption trajectory. Black mass processing, recovering lithium, cobalt, nickel, and manganese from battery cells, requires specialized pyrometallurgical and hydrometallurgical integration. Namo eWaste commissioned a 12,240 MTPA Li-Ion Battery Recycling plant in Nashik in July 2025. Attero is exploring hydrometallurgical units for pure lithium, cobalt, and nickel extraction from black mass, targeting the highest-value recovery tier.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Material Type |

Metal |

46.0% |

2025 |

|

Source Type |

Consumer Electronics |

38.0% |

2025 |

|

Application |

Recycled |

50.4% |

2025 |

|

Region |

West India |

29.0% |

2025 |

By Material Type

Metal leads at 46.0% (2025). The metal segment commands India's e-waste management market through the high economic value of recoverable precious and non-precious metals from discarded electronics. Gold, silver, copper, aluminum, and steel are primary recovery targets. Each tonne of processed PCBs contains gold concentrations 40 to 50 times higher than gold ore, creating compelling urban mining economics.

To access detailed market analysis, Request Sample

Plastic at 28.4% represents the second-largest material type. Recycled plastics from electronic housings, cable insulation, and component packaging feed India's plastics compounding industry. Glass at 15.2% primarily derives from CRT television and monitor panels, with recovery driven by specialized glass processors. Others at 10.4% includes rubber, ceramics, and rare earth-bearing components.

By Source Type

Consumer Electronics leads at 38.0% (2025). Smartphone penetration, laptop adoption, and tablet usage create India's highest-volume and most consistent e-waste stream. The India Cellular and Electronics Association (ICEA) data indicates approximately 150 million smartphones sold in India in 2025, with replacement cycles of 2.5 to 3 years generating a predictable annual volume of end-of-life devices entering collection networks.

Industrial Electronics at 34.6% is the fastest-growing source type, driven by IT infrastructure refresh cycles in India's expanding tech sector, banking sector server upgrades, and government digital infrastructure investments. Telecom equipment, servers, and networking hardware contain higher concentrations of precious metals per unit than consumer devices, improving per-tonne recovery economics. Others at 27.4% include medical equipment, industrial machinery electronics, and automotive electronics.

Regional Market Insights

|

Region |

Share (2025) |

Key Drivers & Characteristics |

|

West India |

29.0% |

Maharashtra's electronics manufacturing density, Gujarat's metallurgical clusters, strategic port access for cross-border material flows |

|

South India |

27.3% |

Bengaluru and Hyderabad IT sector driving high-volume enterprise e-waste; Tamil Nadu manufacturing base supplying industrial electronics scrap |

|

North India |

25.8% |

Delhi-NCR concentration of IT companies, financial institutions, and consumer electronics markets; established authorized recycling infrastructure |

|

East India |

17.9% |

Emerging market with growing formal sector presence; Kolkata industrial corridors and increasing electronics penetration driving future growth |

West India's 29.0% market leadership is built on Maharashtra's electronics manufacturing density, Gujarat's metallurgical processing clusters, and strategic port access facilitating cross-border material flows. Mumbai's BFSI sector refreshes servers every three years, creating a predictable high-value industrial e-waste stream. Pune's auto-tech ecosystem supplies diverse control systems and infotainment units to authorized recyclers.

South India's 27.3% reflects Bengaluru's IT sector generating high-volume enterprise e-waste from technology companies refreshing hardware assets, Hyderabad's pharmaceutical and manufacturing industries contributing industrial electronics scrap, and Tamil Nadu's manufacturing base creating structured electronics waste flows. North India's 25.8% is anchored by Delhi-NCR's concentration of IT companies, financial institutions, and government agencies creating large-scale institutional e-waste volumes. East India's 17.9% is growing above the national CAGR as Kolkata's industrial corridors and increasing electronics penetration in Odisha and northeastern states create first-generation formal recycling demand.

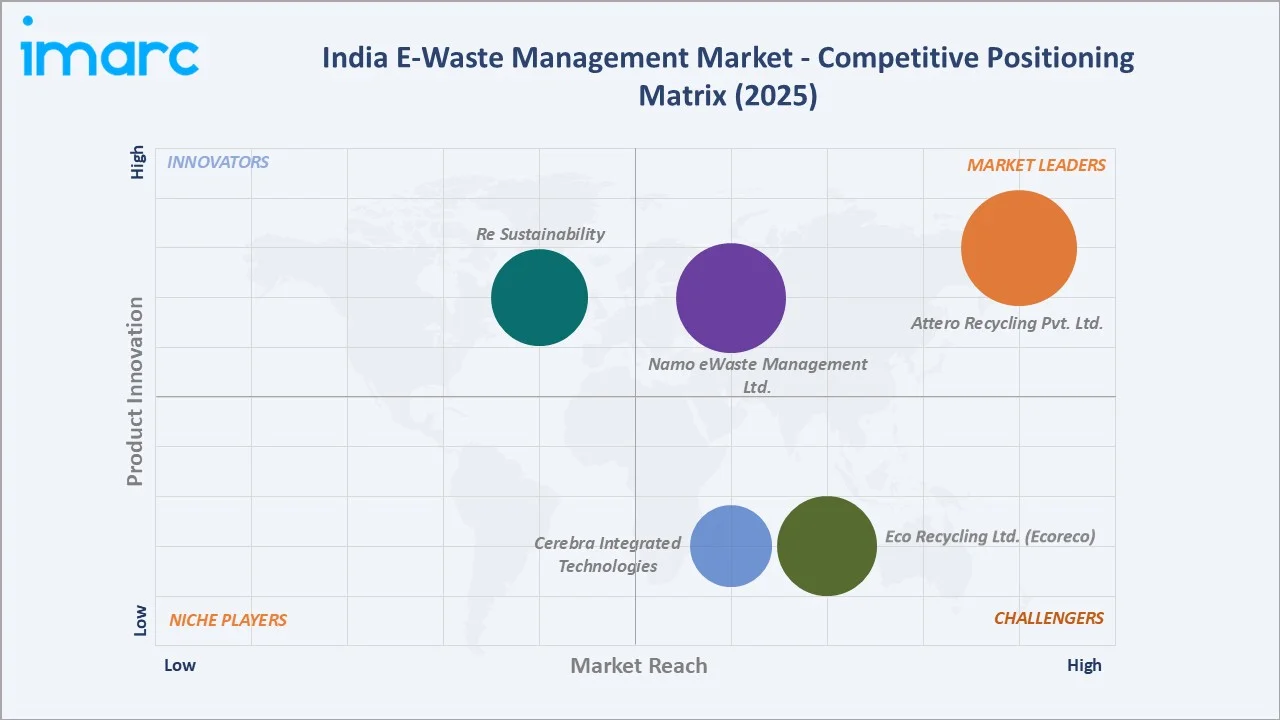

Competitive Landscape

India e-waste management competitive landscape is moderately concentrated in the formal authorized sector, with Attero Recycling commanding approximately 25% of India's organized e-waste sector, creating the market's most commercially dominant single-company position. Competition is intensifying through AI-driven sorting investments, strategic geographic expansion to Tier-2 cities, and bundling of certified disposal with carbon-credit consulting services for multinational ESG compliance programs.

|

Company |

Headquarters |

Market Position |

Core Strength |

|

Attero Recycling Pvt. Ltd. |

Noida, Uttar Pradesh |

Market Leader |

Disruptive technology, industry-leading material recovery rates, and end-to-end regulatory compliance |

|

Eco Recycling Ltd. (Ecoreco) |

Mumbai, Maharashtra |

Strong Challenger |

Secure data destruction, pan-India reverse logistics, a strong commitment to the circular economy, and robust financial discipline |

|

Cerebra Integrated Technologies |

Bengaluru, Karnataka |

Strong Challenger |

Massive e-waste recycling capabilities, enterprise IT solutions, and established electronic manufacturing services (EMS) |

|

Re Sustainability |

Hyderabad, Telangana |

Innovator |

Technology-driven, end-to-end waste management, resource recovery, and sustainability solutions |

|

Namo eWaste Management Ltd. |

Faridabad, Haryana |

Market Leader |

Large-scale processing capabilities, rigorous data security, and sustainable, zero-waste metal recovery technologies |

The competitive landscape's most significant structural dynamic is the EPR certificate trading market, where authorized recyclers earn tradable certificates for each tonne of e-waste formally processed. This creates a financial mechanism beyond service fees, incentivizing capacity expansion and geographic coverage growth. Strategic partnerships between formal recyclers and informal collectors - formalized through digital platforms - are expanding collection network reach while maintaining regulatory traceability.

Key Company Profiles

Attero Recycling Pvt. Ltd.

Attero Recycling is India's leading e-waste and lithium-ion battery recycling company, headquartered in Noida, Uttar Pradesh. Founded in 2008, Attero holds over 45 patents and operates proprietary hydrometallurgical technology capable of extracting 98% of precious metals from electronic waste.

- Key Products/Services: E-waste recycling, Li-ion battery recycling, IT Asset Disposition (ITAD), EPR compliance management, MetalMandi digital scrap marketplace, Selsmart D2C take-back platform.

- Recent Developments: In January 2025, Attero launched MetalMandi, a digital platform targeting 1,000 tonnes of daily scrap transactions with AI-driven pricing.

- Strategic Focus: Scaling Roorkee plant capacity to 150,000 tonnes with AI-driven optical separators for copper purity above 99.95%; expanding the formal scrap supply chain through digital aggregation platforms (Source: Attero website - attero.in).

Eco Recycling Ltd. (Ecoreco)

Eco Recycling Ltd., operating as Ecoreco, is a Mumbai-based pioneer in India's e-waste management industry offering pan-India e-waste solutions and asset recovery services. Ecoreco offers on-site mobile data shredding and degaussing for corporate ITAD clients.

- Key Products/Services: E-waste collection, dismantling, recycling, ITAD, on-site data destruction, EPR compliance services.

- Recent Developments: In July 2025, Eco Recycling Ltd. expanded its overall processing capacity to 31,200 MTPA, including Li-ion battery recycling, with commissioning of a 40,000 sq ft plant at Vasai near Mumbai.

- Strategic Focus: Corporate ITAD market leadership through security-first data destruction capabilities; geographic expansion with new plant near Mumbai to capture Maharashtra's growing industrial e-waste volumes.

Market Concentration Analysis

India e-waste management market is moderately concentrated among authorized formal operators, with Attero Recycling commanding approximately 25% of India's organized e-waste sector and possessing the market's most technologically differentiated processing capabilities. The overall market remains fragmented due to approximately 450 CPCB-authorized facilities, with formal processing capturing approximately 70% of generated volumes in 2024-25 compared to only 22% in 2019-20.

Market concentration is evolving through two competing forces: technology-driven consolidation among leading formal recyclers - where Attero, Ecoreco, and Cerebra collectively command an estimated 45-55% of organized sector revenue - and geographic fragmentation as new authorized facilities emerge in Tier-2 cities under EPR expansion pressure. The EPR certificate market creates a structural consolidation incentive, as larger authorized recyclers with higher certificate generation volumes command greater compliance contract value from producers.

The informal sector's 30% market share persists as a de-concentration factor, competing primarily in collection and low-value material recovery segments. Digital aggregation platforms - particularly MetalMandi and Selsmart - are progressively formalizing informal collector networks, redirecting material flows toward authorized processors and incrementally reducing informal sector market share.

Investment & Growth Opportunities

Highest Growth Segments

Li-ion battery recycling represents India's highest-growth e-waste sub-segment, driven by Battery Waste Management Rules 2022 and India's accelerating EV adoption creating end-of-life battery volumes from 2027 onwards. The National Critical Mineral Mission's INR 1,500-crore incentive for lithium and rare-earth recovery from waste is directly catalyzing investment in hydrometallurgical battery processing infrastructure.

Hydrometallurgy as a processing technology is projected at 8.74% CAGR through 2031, creating the fastest-growing investment category within the formal recycling infrastructure. AI-driven optical sorting investments, with capital payback periods of 3 to 5 years at current throughput rates, represent the highest-return technology investment within the pre-processing stage.

Emerging Investment Opportunities

- Digital aggregation platforms for informal collector formalization: MetalMandi's model - targeting 1,000 tonnes of daily transactions by mid-2025 - demonstrates the commercial viability of digital platforms that bridge informal and formal supply chains with AI-driven pricing and traceability.

- Tier-2 city authorized recycling micro-plants: Re Sustainability's decentralized micro-plant model addresses the reverse logistics cost barrier preventing formal sector penetration of emerging Tier-2 city e-waste volumes. Cities including Jaipur, Lucknow, Coimbatore, and Bhubaneswar represent underserved markets with growing enterprise and consumer electronics scrap generation.

- ESG-linked carbon credit bundling: Formal recyclers are developing carbon-credit consulting services bundled with certified disposal, tapping multinational corporate decarbonization budgets as a premium revenue stream above basic recycling fees.

Investment Themes

- Hydrometallurgical plant investment for battery and PCB precious metal recovery represents India's most commercially compelling formal recycling investment, with improving commodity price environments and EPR revenue creating dual revenue floor certainty.

- EPR portal compliance technology - digital platforms managing certificate tracking, audit documentation, and regulatory reporting for producers - represent a recurring SaaS revenue opportunity within the compliance ecosystem.

- Cross-sector urban mining partnerships with IT companies, government agencies, and financial institutions creating structured take-back programs for high-value IT asset streams.

Future Market Outlook (2026-2034)

India e-waste management market is projected to grow from USD 3.32 Billion in 2025 to USD 9.95 Billion by 2034, delivering an 11.59% CAGR over the forecast period. The anchor value of USD 5.74 Billion in 2030 reflects the market at a structural inflection driven by EPR target escalation to 80% mandatory collection, first-generation EV battery recycling volumes entering processing facilities, and AI-driven technology reducing formal sector cost structures to compete directly with informal operators across all material value tiers.

Three structural forces define India e-waste management market growth through 2034: regulatory formalization escalation under E-Waste Rules 2022 EPR targets, technology cost reduction enabling hydrometallurgy to replace pyrometallurgy across mid-scale operations, and India's National Critical Mineral Mission positioning e-waste recycling as a strategic resource security initiative commanding government investment.

By 2034, India's formal e-waste recycling sector is expected to process over 85% of generated volumes, creating a USD 9.95 Billion market representing one of the world's largest formal e-waste economies. Digital platforms aggregating informal collectors - MetalMandi model - are expected to formalize the remaining informal volumes through traceable, EPR-compliant material flows within the forecast period.

Research Methodology

Primary Research

Primary research comprised structured interviews with India e-waste management industry stakeholders, including Recycling Plant Directors, EPR Compliance Managers, CPCB regulatory officials, Producer Responsibility Organization (PRO) representatives, informal sector aggregators undergoing formalization, corporate IT asset managers, and institutional procurement officers across North, West, South, and East India.

Secondary Research

Secondary research encompassed CPCB e-waste generation and processing data (eprewastecpcb.in dashboard), E-Waste (Management) Rules 2022 regulatory framework documentation, Ministry of Environment, Forest and Climate Change (MoEF&CC) press releases, TRAI telecommunications infrastructure data, India Cellular and Electronics Association (ICEA) device sales data, company annual reports and investor presentations, and industry association publications. Over 60 secondary sources reviewed.

Forecasting Models

Market revenue forecasts were developed using a material flow analysis model: total e-waste generation volume by equipment category multiplied by formal sector capture rate trajectory and average revenue per tonne by material composition. EPR compliance rate escalation model applied to producer-funded recycling volumes. Battery recycling sub-model built using India EV adoption forecasts and battery end-of-life timing distributions.

India E-Waste Management Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Material Types Covered | Metal, Plastic, Glass, Others |

| Source Types Covered | Consumer Electronics, Industrial Electronics, Others |

| Applications Covered | Trashed, Recycled |

| Regions Covered | North India, South India, East India, West India |

| Companies Covered | Attero Recycling Pvt. Ltd., Eco Recycling Ltd. (Ecoreco), Cerebra Integrated Technologies, Re Sustainability, Namo eWaste Management Ltd., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India E-Waste Management Market Report

India e-waste management market reached USD 3.32 Billion in 2025, driven by stringent EPR regulations under E-Waste Rules 2022, rising formal recycling infrastructure, and growing precious metal recovery economics.

India e-waste management market grows at 11.59% CAGR during 2026-2034, reaching USD 9.95 Billion by 2034, driven by EPR compliance escalation, battery waste management expansion, and urban mining investment.

India generated 13.97 lakh metric tonnes of e-waste in FY 2024-25 and 14.14 lakh MT in FY 2025-26 so far, with formal recycling exceeding 70% of generated volumes for the first time in 2024-25 (Source: CPCB).

Metal leads at 46.0% (2025) through the high economic value of gold, silver, copper, and aluminum recovery from discarded electronics, creating the most commercially attractive material stream for authorized recyclers.

Consumer Electronics dominates at 38.0% (2025) driven by smartphone penetration - approximately 150 million units sold in 2025 - and 2.5 to 3 year device replacement cycles continuously feeding e-waste collection networks.

West India leads at 29.0% (2025) through Maharashtra's electronics manufacturing density, Gujarat's metallurgical processing clusters, and strategic port infrastructure. Maharashtra alone holds approximately 25% of India's formal processing capacity.

India e-waste management market is projected to reach approximately USD 5.74 Billion by 2030, with EPR mandatory collection targets at 80% by FY 2027-28 and first-generation EV battery recycling volumes entering processing infrastructure.

Leading companies include Attero Recycling Pvt. Ltd., Eco Recycling Ltd. (Ecoreco), Cerebra Integrated Technologies, Re Sustainability, and Namo eWaste Management Ltd., among others.

Top opportunities include Li-ion battery recycling plants for EV end-of-life volumes, hydrometallurgical precious metal recovery facilities, digital aggregation platforms formalizing informal collectors, and Tier-2 city authorized micro-plant expansion.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)