India Electric Car Market Size, Share, Trends and Forecast by Type, Vehicle Class, Vehicle Drive Type, and Region, 2026-2034

India Electric Car Market Size, Share, Trends & Forecast (2026-2034)

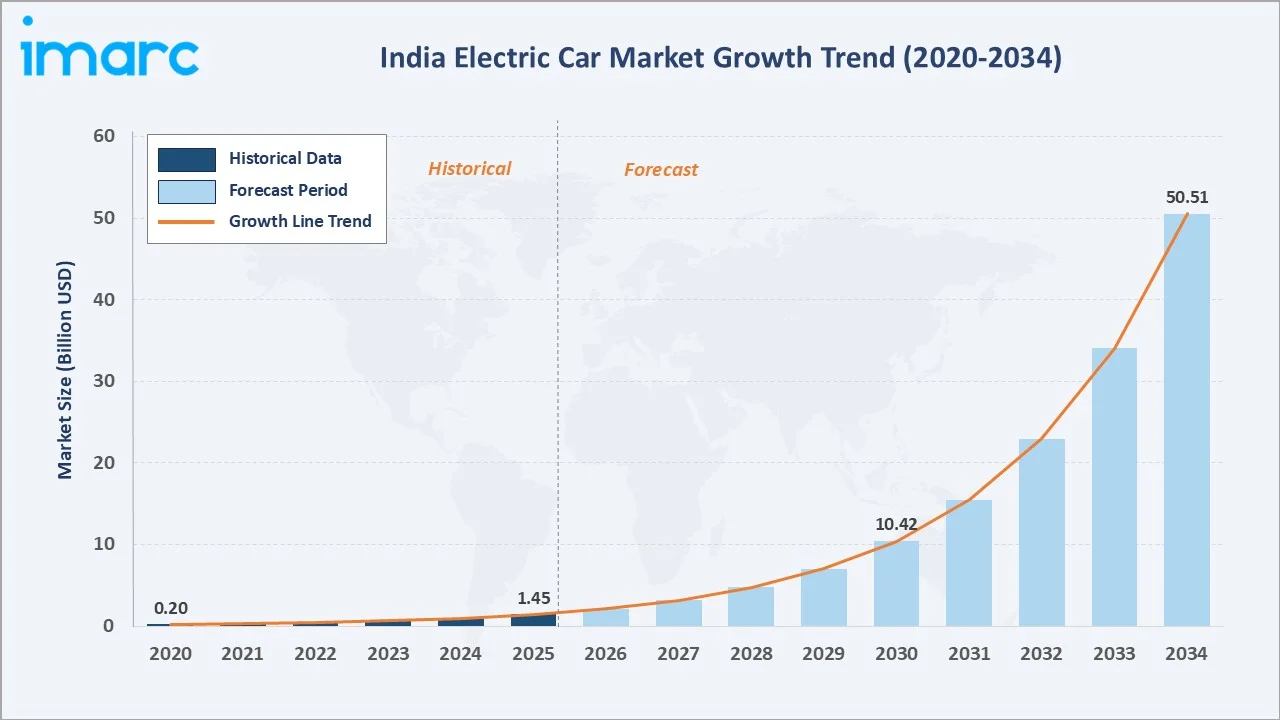

The India electric car market was valued at USD 1.45 Billion in 2025 and is projected to reach USD 50.51 Billion by 2034, exhibiting a CAGR of 48.38% during 2026-2034. Government subsidies, falling battery costs, rising fuel prices, and strong original equipment manufacturer (OEM) investment in localized electric vehicle platforms are the primary drivers shaping the market growth.

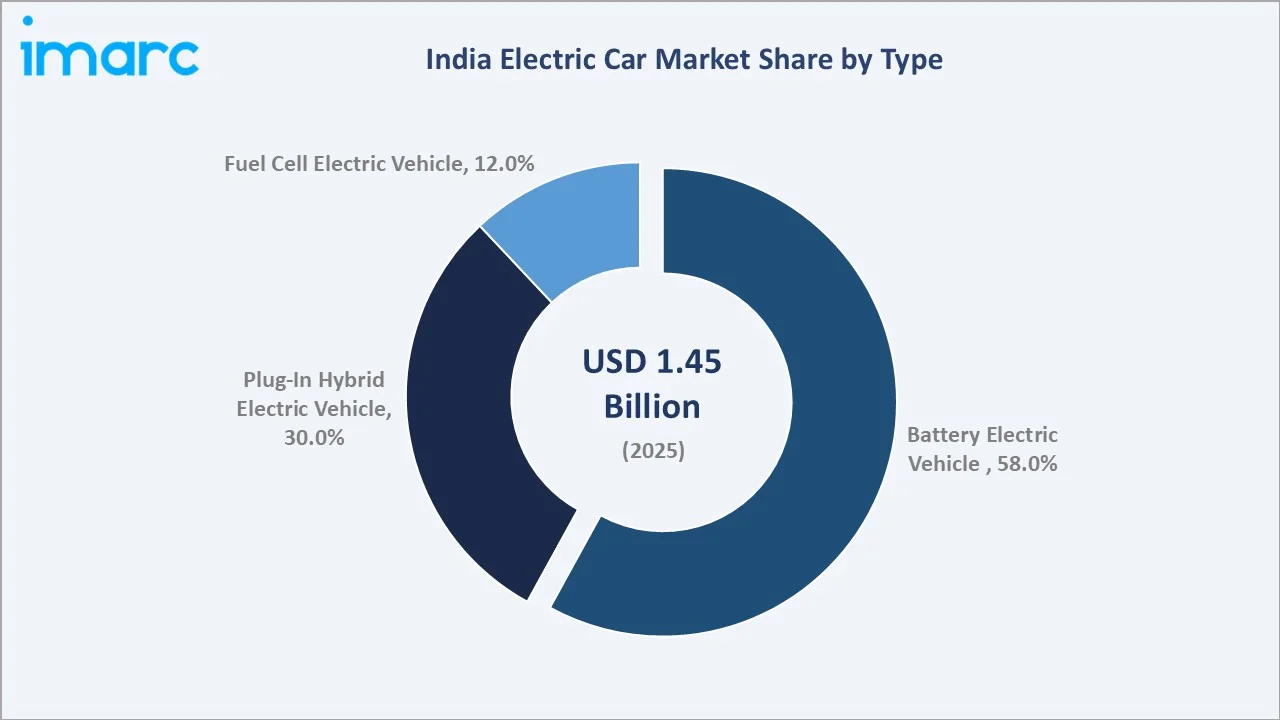

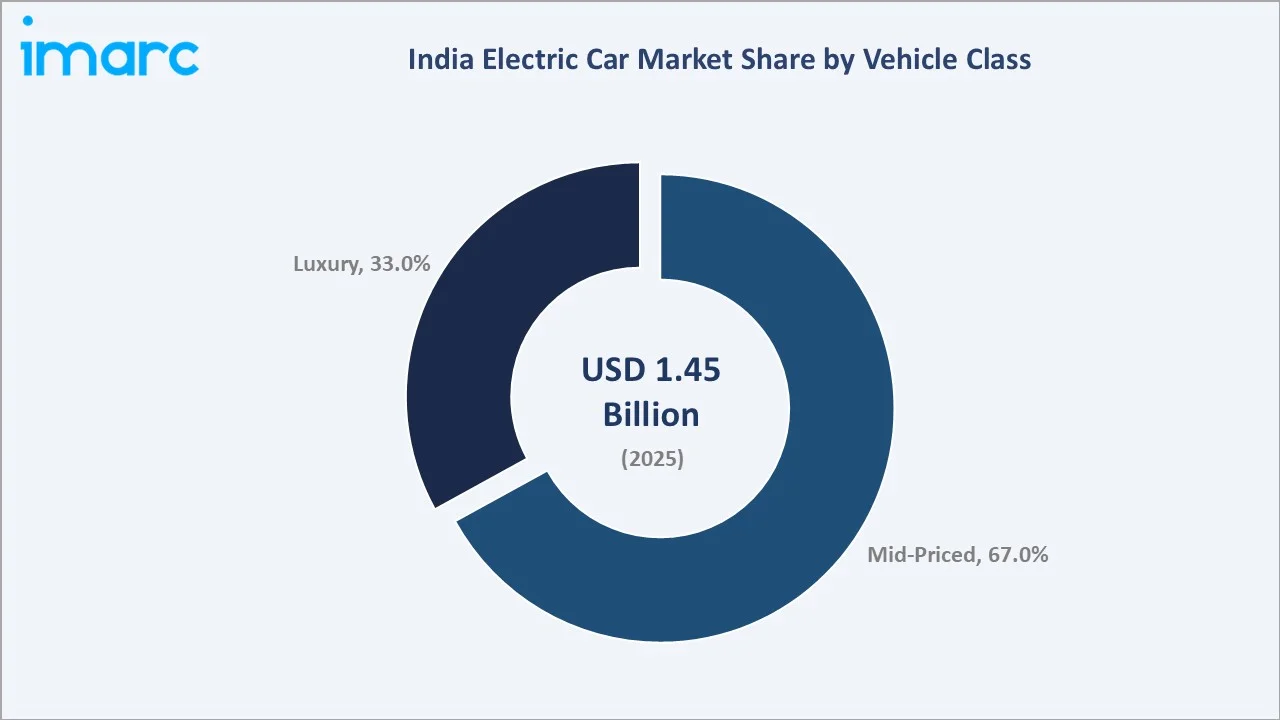

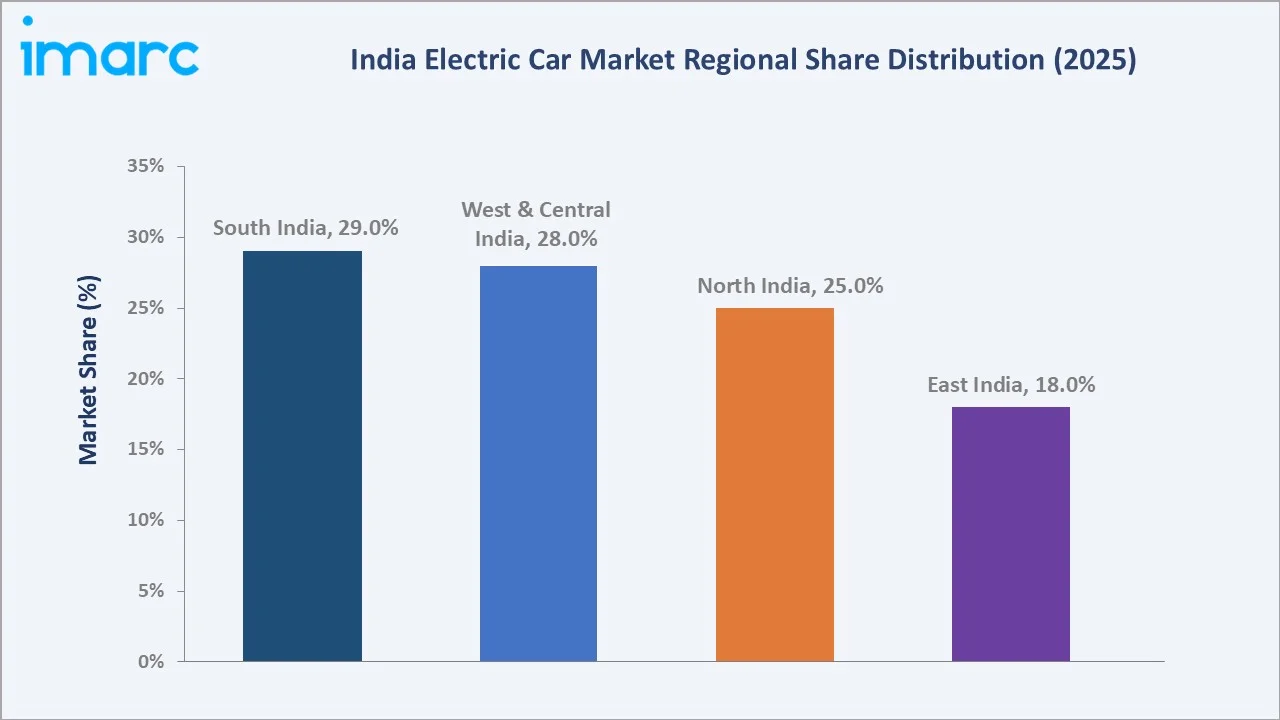

Battery electric vehicle leads the type segment at 58.0%, mid-priced dominates the vehicle class segment at 67.0%, and South India commands 29.0% regional share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 1.45 Billion |

|

Forecast Market Size (2034) |

USD 50.51 Billion |

|

CAGR (2026-2034) |

48.38% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

South India (29.0%, 2025) |

|

Second Largest Region |

West & Central India (28.0%, 2025) |

|

Leading Type |

Battery Electric Vehicle (58.0%, 2025) |

|

Leading Vehicle Class |

Mid-Priced (67.0%, 2025) |

The India electric car market expanded from USD 0.20 Billion in 2020 to USD 1.45 Billion in 2025, driven by declining lithium-ion battery prices and increasing OEM commitment to India-specific electric vehicle platforms. Anchored at USD 10.42 Billion in 2030, the forecast to USD 50.51 Billion by 2034 is supported by PLI scheme benefits, expanding domestic battery cell manufacturing, and investments in public charging networks.

To get more information on this market, Request Sample

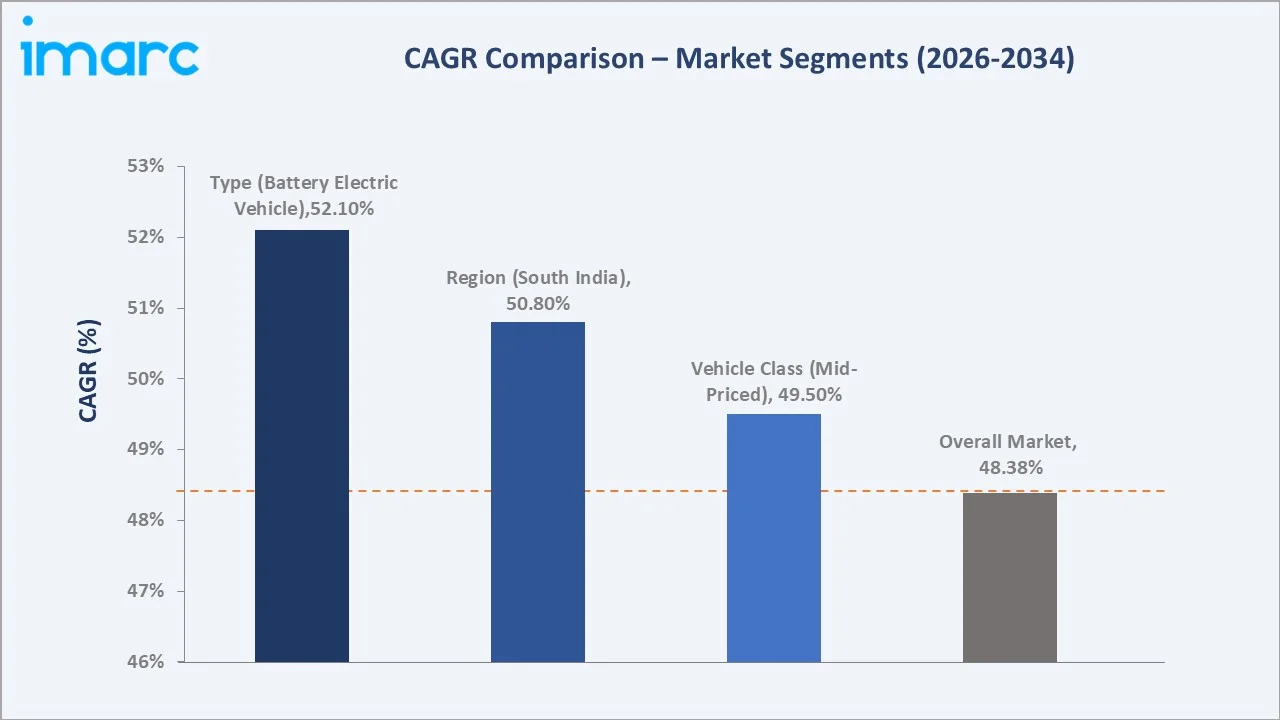

CAGR trajectories across type and vehicle class sub-segments show battery electric vehicle and mid-priced expanding faster than the overall 48.38% market CAGR, driven by scale advantages, government procurement, and improving value-for-money propositions across entry-level and mass-market segments.

Executive Summary

The India electric car market is on a high-growth trajectory, expanding from USD 0.20 Billion in 2020 to USD 50.51 Billion by 2034. The segment has shifted from an early-adoption niche to a mainstream consideration across urban and peri-urban passenger vehicle buyers. Declining battery costs, increasing model availability from both domestic and international OEMs, and supportive government policy are collectively driving this transformation.

Battery electric vehicle leads the type segment at 58.0% in 2025, benefiting from lower total cost of ownership, zero direct tailpipe emissions, and growing confidence in home and workplace charging. Mid-priced dominates the vehicle class segment at 67.0%, anchored by competitively priced models from key players. South India holds the largest regional share at 29.0%, led by strong state-level electric vehicle policies in Tamil Nadu and Karnataka.

Key Market Insights

|

Insight |

Data |

|

Leading Type |

Battery Electric Vehicle – 58.0% share (2025) |

|

Second Largest Type |

Plug-In Hybrid Electric Vehicle – 30.0% share (2025) |

|

Leading Vehicle Class |

Mid-Priced – 67.0% share (2025) |

|

Second Largest Vehicle Class |

Luxury – 33.0% share (2025) |

|

Leading Region |

South India – 29.0% share (2025) |

|

Second Largest Region |

West & Central India – 28.0% share (2025) |

|

Top Companies |

Tata Motors Limited., Mahindra & Mahindra Ltd., Hyundai Motor Company, Stellantis NV |

Key Analytical Observations Expanding On The Data Above:

- Battery electric vehicle dominance at 58.0% is anchored by zero fuel cost operation, growing home-charging adoption, and an expanding portfolio of mass-market models spanning entry-level hatchbacks to mid-size SUVs at competitive price points.

- Plug-in hybrid electric vehicle at 30.0% serves buyers requiring extended range capability who are not yet confident about charging infrastructure availability, particularly across tier-2 cities and inter-city travel routes.

- Mid-priced at 67.0% reflects strong demand from urban salaried households seeking fuel-cost savings and lower lifetime ownership costs without the premium pricing associated with luxury electric vehicles.

- Luxury share at 33.0% is supported by affluent consumers seeking premium technology features, high-performance electric drivetrains, and sustainability-focused brand positioning, particularly in metropolitan cities.

- South India at 29.0% leads regionally, supported by Tamil Nadu's pioneering electric vehicle manufacturing ecosystem and high consumer literacy driving early electric vehicle adoption in Bengaluru and Chennai.

India Electric Car Market Overview

An electric car is a passenger vehicle powered fully or partially by an electric motor, drawing energy from an onboard battery pack or fuel cell. The category spans battery electric cars, plug-in hybrid electric cars, and fuel cell electric cars designed for personal, shared, and commercial mobility across urban, peri-urban, and highway applications.

The Indian electric car ecosystem integrates lithium-ion battery suppliers, cell manufacturers and pack assemblers, OEMs, charging infrastructure providers, power distribution utilities, digital platform operators for fleet and charge management, and government bodies at central and state levels overseeing policy, subsidy disbursement, and emissions regulation.

Market Dynamics

To evaluate market opportunities, Request Sample

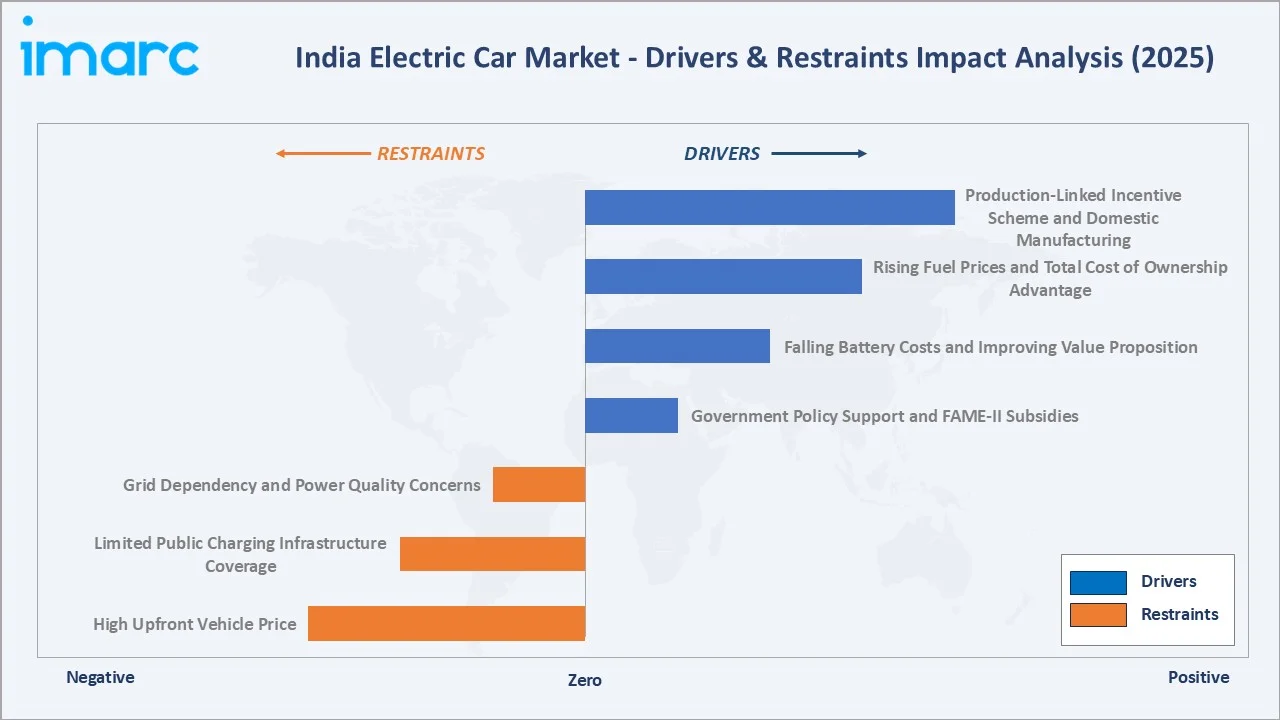

Market Drivers

- Government Policy Support and FAME-II Subsidies: The FAME-II scheme has played a significant role in promoting electric car adoption by helping reduce upfront purchase costs and supporting the expansion of public charging infrastructure across major cities. FAME-II was executed from 01.04.2019 to 31.03.2024 with a budget of INR 11,500 Crore. A total of 16,71,606 electric vehicles were facilitated (sold) during the scheme duration.

- Falling Battery Costs and Improving Value Proposition: Lithium-ion battery pack prices have declined significantly over the past decade, directly improving the economics of electric cars relative to internal combustion alternatives.

- Rising Fuel Prices and Total Cost of Ownership Advantage: Persistent increases in petrol and diesel retail prices have heightened consumer sensitivity to fuel expenditure. Electric cars, with near-zero per-kilometer energy costs when charged at home, offer compelling long-term savings for urban commuters and fleet operators, supporting consistent conversion intent among shortlisted buyers.

- Production-Linked Incentive Scheme and Domestic Manufacturing: India's PLI scheme for Advanced Chemistry Cells and Automobile & Auto Components is incentivizing domestic battery cell manufacturing and electric vehicle platform development. Investment commitments from both established OEMs and new entrants are progressively building a resilient, cost-competitive domestic supply chain.

Market Restraints

- High Upfront Vehicle Price: Despite falling battery costs, entry-level electric cars in India remain priced at a significant premium over equivalent internal combustion engine models. For price-sensitive buyers in tier-2 and tier-3 cities, the upfront cost differential continues to be a primary adoption barrier even after applicable state subsidies and FAME-II benefits.

- Limited Public Charging Infrastructure Coverage: India's public charging station count remains far below the density required to support mass electric vehicle adoption across non-metro geographies. Range anxiety linked to sparse inter-city charging infrastructure constrains consideration among buyers who regularly travel beyond urban boundaries and remains the most cited restraint in the India electric car market.

- Grid Dependency and Power Quality Concerns: Electric vehicle efficiency and battery longevity are sensitive to power quality and supply reliability. Inconsistent grid voltage, frequent outages in rural and semi-urban areas, and limited high-capacity connections in older residential buildings constrain at-home charging adoption outside major metro markets.

Market Opportunities

- Fleet Electrification and Shared Mobility: Ride-hailing platforms, corporate fleet operators, and last-mile delivery networks are large-scale buyers increasingly converting to electric vehicles as total cost of ownership calculations shift in their favor. Fleet aggregators offer OEMs predictable, high-volume demand that can anchor localization investments.

- Green Hydrogen and Fuel Cell Electric Vehicle Development: India's National Green Hydrogen Mission positions the country as a potential global hydrogen hub. Fuel cell electric vehicles represent a long-cycle opportunity for OEMs, infrastructure investors, and industrial gas suppliers willing to invest ahead of the regulatory and cost curve through 2034.

Market Challenges

- Supply Chain Concentration and Critical Mineral Access: Lithium, cobalt, and nickel supply chains are heavily concentrated geographically, exposing Indian OEMs to commodity price volatility and geopolitical supply disruptions. Establishing diversified sourcing and investing in domestic mineral recycling infrastructure are long-term strategic imperatives.

- Consumer Education and Charging Behavior Change: Transitioning buyers from petrol-vehicle habits to electric car ownership requires significant consumer education around charging routines, range management, and service network reliability. Misconceptions about battery degradation, charging times, and resale value continue to be conversion barriers.

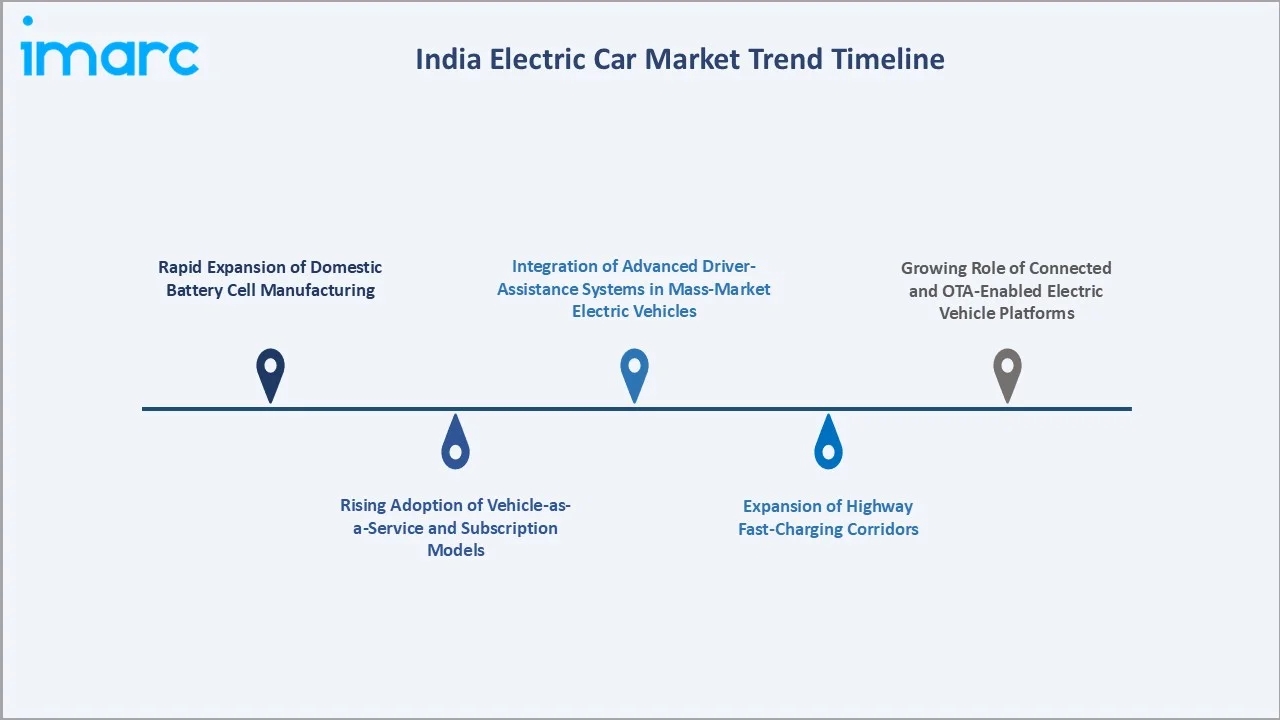

Emerging Market Trends

1. Rapid Expansion of Domestic Battery Cell Manufacturing

India is transitioning from battery pack assembly to full-scale domestic cell manufacturing under the PLI scheme for Advanced Chemistry Cells. This shift is expected to reduce battery costs for Indian OEMs, improve vehicle competitiveness, and lower reliance on imported battery components over the forecast period.

2. Rising Adoption of Vehicle-as-a-Service and Subscription Models

Subscription-based electric car access models are gaining traction among urban consumers who are not ready to commit to full vehicle ownership. Platforms offering monthly all-inclusive electric vehicle subscriptions covering insurance, maintenance, and charging credits are expanding across Bengaluru, Mumbai, and Delhi, lowering the initial commitment threshold and accelerating first-time electric vehicle trial.

3. Integration of Advanced Driver-Assistance Systems in Mass-Market Electric Vehicles

Indian OEMs are progressively embedding ADAS features including lane-keep assist, automatic emergency braking, and adaptive cruise control into mid-priced electric cars. This positioning differentiates electric vehicle offerings from comparably priced ICE alternatives and reinforces the technology-forward value proposition of electrified platforms.

4. Expansion of Highway Fast-Charging Corridors

Government and private sector initiatives are deploying direct current fast chargers along national highways connecting major metro cities, directly targeting inter-city range anxiety. Highway corridor prioritization is expected to unlock purchase decisions among buyers who frequently travel beyond urban boundaries through 2034.

5. Growing Role of Connected and OTA-Enabled Electric Vehicle Platforms

OTA software update capability is becoming standard across new-generation Indian electric cars, enabling post-sale range improvements, feature unlocks, and battery management optimization. As per IMARC Group, the India connected vehicle market is projected to grow at a CAGR of 15.24% through 2034, reflecting deepening integration of telematics, predictive maintenance, and driver analytics into OEM aftersales strategies.

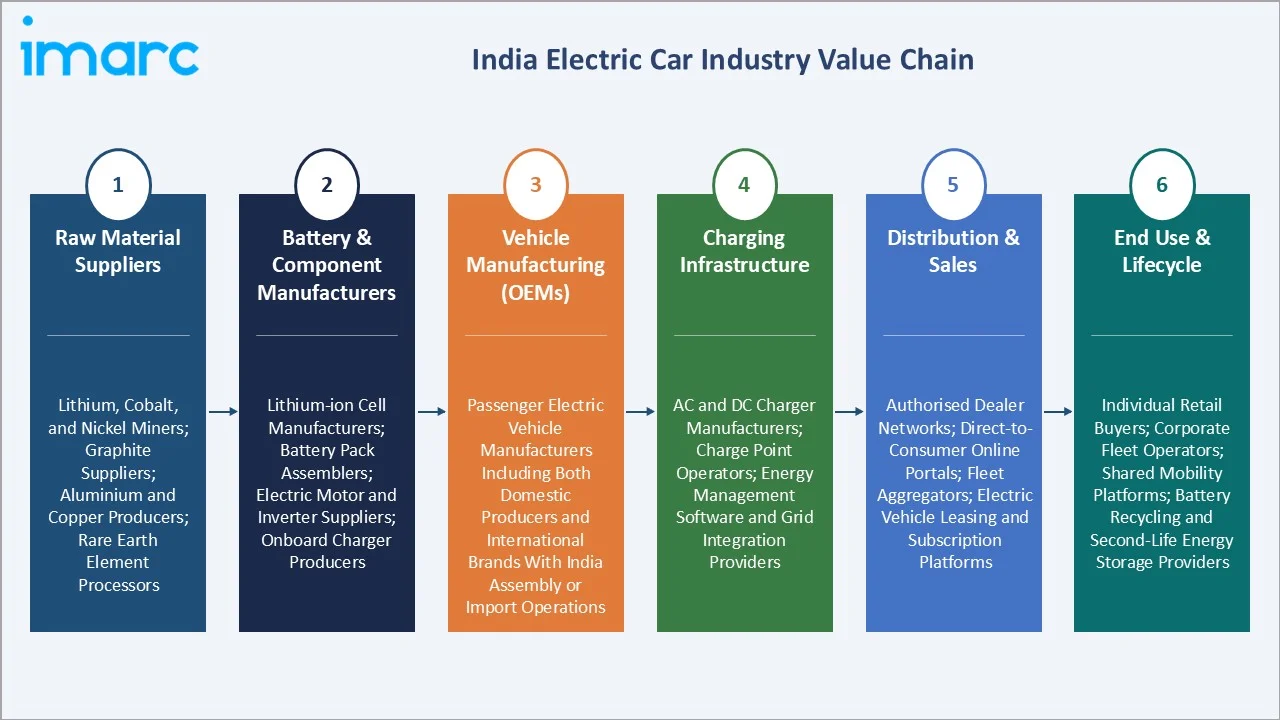

Industry Value Chain Analysis

The India electric car value chain spans six stages from raw material supply through end-use lifecycle management. Battery supply, vehicle manufacturing, and charging infrastructure collectively capture the highest share of value addition, while software, connectivity, and aftersales services are emerging as rapidly growing value pools.

|

Stage |

Key Players / Examples |

|

Raw Material Suppliers |

Lithium, cobalt, and nickel miners; graphite suppliers; aluminum and copper producers; rare earth element processors supplying battery cell manufacturers |

|

Battery & Component Manufacturers |

Lithium-ion cell manufacturers; battery pack assemblers; electric motor and inverter suppliers; onboard charger and thermal management system producers |

|

Vehicle Manufacturing (OEMs) |

Passenger electric vehicle manufacturers including both domestic producers and international brands with India assembly or import operations |

|

Charging Infrastructure |

AC and DC charger hardware manufacturers; charge point operators; energy management software providers; grid integration specialists |

|

Distribution & Sales |

Authorized dealer networks; direct-to-consumer online portals; fleet aggregators; electric vehicle leasing and subscription platforms |

|

End Use & Lifecycle |

Individual retail buyers; corporate fleet operators; shared mobility platforms; battery recycling and second-life energy storage providers |

Vertically integrated players, particularly those with in-house battery technology, localized manufacturing capabilities, and proprietary charging or software ecosystems, are positioned to capture greater value than competitors reliant on imported components and third-party infrastructure.

Technology Landscape in the India Electric Car Industry

Battery Technology and Cell Chemistry Evolution

Lithium iron phosphate chemistry is gaining preference among Indian OEMs for mass-market applications due to superior cycle life, improved thermal stability, and lower cobalt content. Ongoing advancements in battery management systems and cell design are also improving energy efficiency, safety, and long-term performance across electric car platforms.

Electric Powertrain and Motor Innovation

Permanent magnet synchronous motors and induction motors dominate current electric car powertrains in India. OEMs are investing in indigenized motor and inverter development to reduce import bills and optimize powertrain calibration for Indian driving conditions including stop-and-go urban traffic.

Software-Defined Vehicle and Connected Platform Technologies

India's leading electric car OEMs are progressively adopting centralized compute platforms enabling OTA updates and connected services integration. AI-driven battery management systems are improving range estimation accuracy and extending pack longevity across Indian operating conditions.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Type |

Battery Electric Vehicle |

58.0% |

2025 |

|

Vehicle Class |

Mid-Priced |

67.0% |

2025 |

|

Vehicle Drive Type |

Front Wheel Drive |

50.0% |

2025 |

|

Region |

South India |

29.0% |

2025 |

By Type

Battery electric vehicle commands a 58.0% majority share in 2025, driven by zero direct emission operation, lower per-kilometer energy cost, and a rapidly expanding model portfolio spanning compact hatchbacks, sub-compact SUVs, and mid-size sedans. The segment benefits from growing home-charging infrastructure in tier-1 cities and increasing consumer familiarity with electric vehicle ownership.

To access detailed market analysis, Request Sample

Plug-in hybrid electric vehicle at 30.0% in 2025 serves buyers requiring seamless long-distance capability without dependence on charging infrastructure.

By Vehicle Class

Mid-priced dominates at 67.0% in 2025, driven by competitively priced electric SUVs and hatchbacks targeting urban households. This segment benefits from disproportionately higher eligibility for state-level purchase subsidies and road tax exemptions.

Luxury holds 33.0% share in 2025, supported by high-net-worth individual demand for premium imported electric models from European and Korean OEMs. Luxury electric vehicle buyers are motivated by brand prestige, technology content, and sustainability positioning more than subsidy eligibility or fuel-cost mathematics.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

South India |

29.0% |

Progressive electric vehicle policies in Tamil Nadu and Karnataka, high urban consumer purchasing power, strong IT sector employment base, and expanding public charging network across Bengaluru, Chennai, and Hyderabad |

|

West & Central India |

28.0% |

Maharashtra's comprehensive electric vehicle policy with purchase incentives and road tax waiver, strong corporate fleet electrification demand in Mumbai and Pune, and well-developed highway charging infrastructure along key inter-city routes |

|

North India |

25.0% |

Delhi's electric vehicle policy with purchase incentives and congestion charge exemptions, large urban commuter population, expanding metro and feeder electric vehicle fleet, and rising air quality awareness driving preference for zero-emission vehicles |

|

East India |

18.0% |

Emerging state-level electric vehicle policies in West Bengal and Odisha, growing awareness among urban youth segments, rising institutional fleet demand, and government-led public transport electrification creating foundational market awareness |

South India at 29.0% in 2025 leads the regional landscape, anchored by Tamil Nadu's advanced electric vehicle manufacturing ecosystem. In addition, supportive state policies and ongoing investments in charging infrastructure and battery manufacturing continue to strengthen the region's position in the India electric car market.

West & Central India at 28.0% is rapidly closing the gap with South India. Maharashtra's early and sustained electric vehicle policy framework, strong MSME and corporate fleet demand, and Mumbai's advanced public charging rollout position the region as the next dominant growth market through 2034.

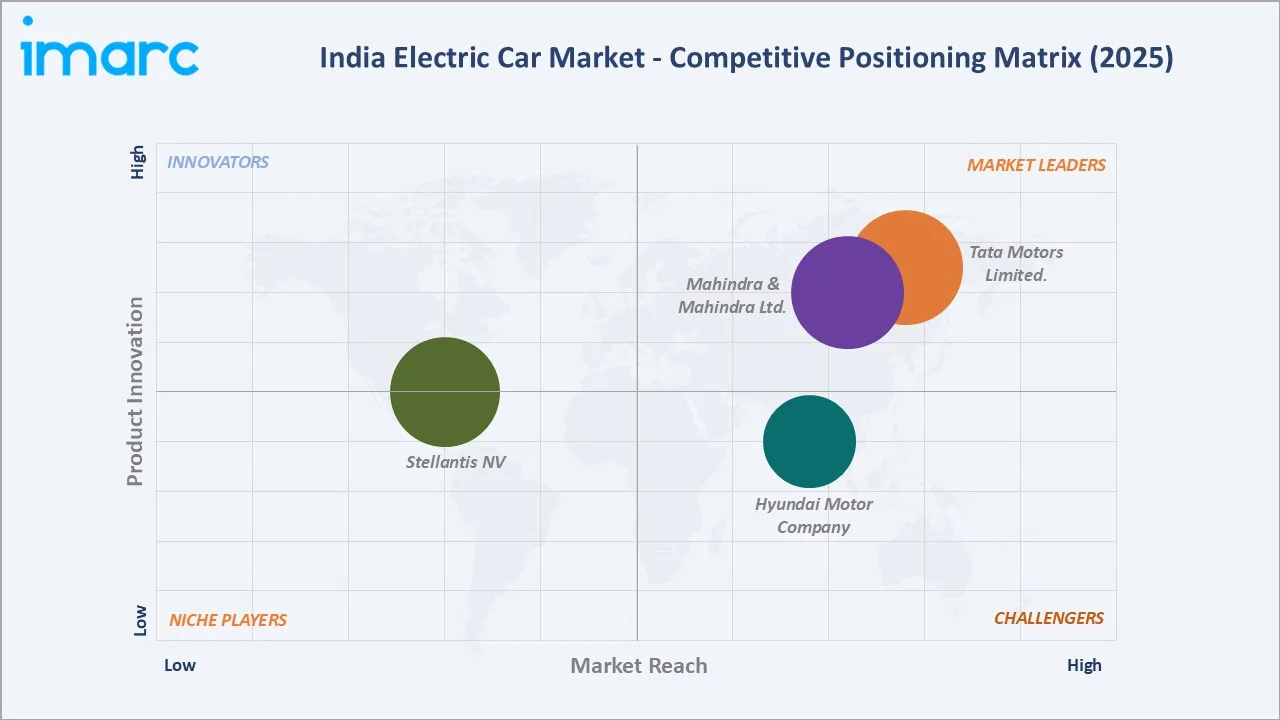

Competitive Landscape

The India electric car market is moderately concentrated, with established automotive manufacturers and emerging electric mobility players competing through expanding product portfolios and localized manufacturing strategies. Leading companies are strengthening their market positions through investments in battery technology, charging ecosystem partnerships, dealership and service network expansion, and the introduction of new electric vehicle models across multiple price segments.

|

Company Name |

Brand / Key Product |

Position |

Strategic Focus |

|

Tata Motors Limited. |

Tata Nexon EV, Tiago EV, Punch EV |

Leader |

Volume leadership in mass-market battery electric vehicle through localized platforms and broad dealer coverage |

|

Mahindra & Mahindra Ltd. |

XEV 9e, BE 6 |

Leader |

Premium battery electric SUV platform built on a dedicated EV architecture, targeting technology-focused and lifestyle-oriented buyers |

|

Hyundai Motor Company |

Creta Electric, IONIQ 5 |

Challenger |

Localized mass-market battery electric vehicle platform complemented by premium electric vehicle models |

|

Stellantis NV |

Citroën ë-C3 |

Emerging |

Affordable locally manufactured battery electric vehicle hatchback targeting entry-level urban electric vehicle buyers |

Key players include Tata Motors Limited., Mahindra & Mahindra Ltd., Hyundai Motor Company, and Stellantis NV, among others.

Key Company Profiles

Tata Motors Limited.

Tata Motors Limited. is one of India's largest and most established automobile manufacturers, with a broad portfolio spanning passenger vehicles, commercial vehicles, and electric vehicles. The company has manufacturing operations across multiple locations in India as well as an international presence through subsidiary brands.

- Product Portfolio: The company offers a range of electric passenger vehicles including the Tata Nexon EV, Tiago EV, and Punch EV, spanning multiple price segments from entry-level hatchbacks to mid-size SUVs and catering to a broad spectrum of urban and semi-urban buyers.

- Recent Developments: In December 2025, Tata Motors Limited. detailed its electric vehicle strategy for 2026. The firm stated that it will join the premium EV sector with the Avinya label by late 2026, after introducing the Sierra.ev and the revamped Punch.ev in the first half.

- Strategic Focus: The company focuses on maintaining volume leadership across mass-market battery electric vehicle segments through a continuously expanding localized electric vehicle platform and a nationwide dealer and service network.

Mahindra & Mahindra Ltd.

Mahindra & Mahindra Ltd. is a leading Indian multinational corporation with diversified operations across automotive, farm equipment, financial services, and information technology sectors. Its automotive division is among the largest utility vehicle manufacturers in India, and the company has made a significant strategic commitment to electric vehicle development through dedicated electric vehicle platforms and architecture.

- Product Portfolio: The company's electric vehicle lineup includes the XEV 9e and BE 6, both built on a purpose-built electric vehicle architecture and targeted at technology-oriented and lifestyle-focused buyers seeking premium battery electric SUVs with advanced features and extended range capability.

- Recent Developments: The company has been scaling up manufacturing capacity for its electric vehicle platforms and expanding its dealer and service network to support the growing base of electric vehicle customers across urban and peri-urban markets in India.

- Strategic Focus: The company is focused on establishing a strong position in the premium battery electric SUV segment through a dedicated electric vehicle architecture, with an emphasis on software-defined features, connected services, and extended range capability to differentiate from conventional utility vehicle offerings.

Hyundai Motor Company

Hyundai Motor Company is a multinational automotive manufacturer with a significant presence in India through locally manufactured passenger vehicles. The company operates a large-scale manufacturing facility in India and has been an active participant in the Indian electric vehicle market, offering both locally produced and imported electric passenger vehicles across different price segments.

- Product Portfolio: The company's electric vehicle offerings in India include the Creta Electric, a locally manufactured mass-market electric SUV, and the IONIQ 5, a premium imported battery electric vehicle, together addressing a wide range of buyer preferences from value-conscious urban commuters to aspirational technology-forward buyers.

- Recent Developments: The company has been expanding its electric vehicle lineup in India and investing in dealer capabilities and charging infrastructure support to enhance the overall electric vehicle ownership experience for Indian customers.

- Strategic Focus: The company's strategy in India centers on offering locally manufactured electric vehicles at competitive price points to drive volume in the mass-market segment, while maintaining a presence in the premium segment through imported electric vehicle models.

Market Concentration Analysis

The India electric car market is moderately concentrated at the leadership tier, with a few established manufacturers accounting for a significant share of overall sales. The competitive landscape reflects the early-mover advantage of companies that have invested in localized electric vehicle platforms, domestic manufacturing capabilities, and dedicated EV product strategies ahead of broader industry adoption.

Barriers to entry include significant capital requirements for dedicated electric vehicle platform development, battery supply chain establishment, dealer and service network build-out, and the need to navigate India's complex certification requirements. These factors favor well-capitalized incumbents, though the PLI scheme is creating additional entry pathways for domestic new entrants with technology partnerships.

Consolidation dynamics are evolving as international OEMs accelerate localization commitments and domestic players expand into adjacent segments. Increasing investments in local manufacturing, battery supply chains, and charging infrastructure partnerships are expected to further intensify competition and reshape market positioning over the forecast period.

Investment & Growth Opportunities

Fastest-Growing Segments

Battery electric vehicle is expanding the fastest within the type segment, driven by falling battery costs, growing home-charging adoption, and progressively improving model availability at mass-market price points. Mid-priced is the primary volume growth engine, with additional models from domestic and international OEMs entering this price band annually.

Emerging Markets

West & Central India is closing the gap with South India as the fastest-growing region, anchored by Maharashtra's comprehensive electric vehicle policy, strong corporate and fleet electrification demand, and expanding highway charging. East India at 18.0% represents significant untapped potential as state-level electric vehicle policies mature.

Venture & Investment Trends

Investment is concentrated in battery cell manufacturing under PLI incentives, charging infrastructure deployment by charge point operators, electric vehicle fleet financing platforms targeting ride-hailing and last-mile delivery operators, and software-defined vehicle technology companies supporting connected services for Indian OEMs.

Future Market Outlook (2026-2034)

The India electric car market is forecast to expand from USD 1.45 Billion in 2025 to USD 50.51 Billion by 2034 at a CAGR of 48.38%, adding approximately USD 49 Billion in incremental market value over the forecast period.

Four forces will shape the market through 2034: a maturing domestic battery manufacturing ecosystem reducing cell import dependency; progressive expansion of public and semi-public charging infrastructure closing the inter-city range gap; deepening OEM commitment to India-specific electric vehicle platforms at competitive price points; and evolving consumer familiarity reducing psychological barriers to first-time electric vehicle purchase.

By 2034, the India electric car market is expected to be defined by a diverse competitive landscape spanning volume-focused domestic manufacturers, localized international OEMs, premium import specialists, and continued emergence of new entrants leveraging India's PLI ecosystem.

Research Methodology

Primary Research

Primary research included structured interviews with electric vehicle product managers, electric vehicle charging infrastructure developers, fleet procurement executives, automotive retail network operators, battery supply chain specialists, and regulatory experts at central and state government bodies.

Secondary Research

Secondary sources included Ministry of Heavy Industries publications on FAME-II disbursements and PLI scheme progress, Vahan dashboard vehicle registration data, SIAM industry statistics, Reserve Bank of India automotive lending data, state electric vehicle policy documents, and annual reports, press releases, and investor presentations from publicly listed electric vehicle manufacturers and battery material suppliers.

Forecasting Models

Market forecasts used top-down and bottom-up models combining domestic vehicle registration data, average transaction price trajectories, segment mix evolution, battery cost curves, infrastructure deployment assumptions, and macroeconomic variables. Sensitivity analysis addressed subsidy policy continuity, battery import duty changes, and pace of charging network deployment.

India Electric Car Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Types Covered | Battery Electric Vehicle, Plug-In Hybrid Electric Vehicle, Fuel Cell Electric Vehicle |

| Vehicle Classes Covered | Mid-Priced, Luxury |

| Vehicle Drive Types Covered | Front Wheel Drive, Rear Wheel Drive, All-Wheel Drive |

| Regions Covered | South India, North India, West and Central India, East India |

| Companies Covered | Tata Motors Limited., Mahindra & Mahindra Ltd., Hyundai Motor Company, Stellantis NV, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Electric Car Market Report

The India electric car market was valued at USD 1.45 Billion in 2025, driven by FAME-II subsidies, falling battery costs, expanding model availability, and growing consumer awareness of total cost of ownership advantages.

The market is projected to grow at a CAGR of 48.38% from 2026 to 2034, reaching USD 50.51 Billion, supported by PLI scheme-led battery manufacturing, expanding charging infrastructure, and deepening OEM commitment to India-specific electric vehicle platforms.

Battery electric vehicle leads at 58.0% in 2025, driven by zero operating fuel costs, growing home-charging adoption, and a diversifying model portfolio from key players spanning hatchbacks to mid-size SUVs.

Mid-priced dominates at 67.0% in 2025, anchored by competitively priced electric SUVs and hatchbacks targeting urban salaried households with strong subsidy eligibility and growing awareness of running cost savings.

South India commands 29.0% in 2025, led by Tamil Nadu's electric vehicle manufacturing ecosystem and supportive state electric vehicle policies offering purchase incentives and road tax exemptions.

Leading players include Tata Motors Limited., Mahindra & Mahindra Ltd., Hyundai Motor Company, and Stellantis NV, among others.

Growth is driven by rising petrol prices widening total cost of ownership advantage, expanding public charging infrastructure, and increasing consumer confidence in electric vehicle ownership.

Key challenges include high upfront vehicle prices relative to ICE alternatives, limited public charging network density outside metro cities, grid reliability constraints for at-home charging, and supply chain concentration risks for critical battery materials.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade