India Electric Commercial Vehicles Market Size, Share, Trends and Forecast by Vehicle Type, Propulsion Type, Battery Capacity, End User, and Region, 2026-2034

India Electric Commercial Vehicles Market Size, Share, Trends & Forecast (2026-2034)

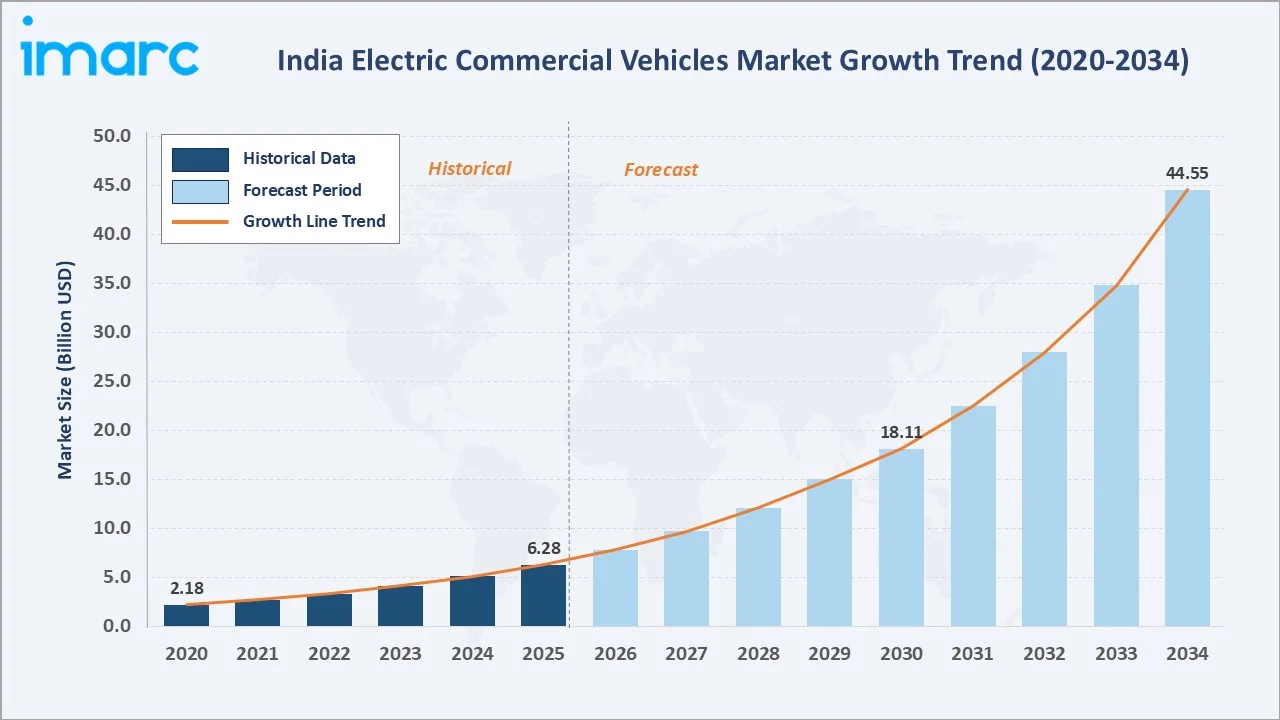

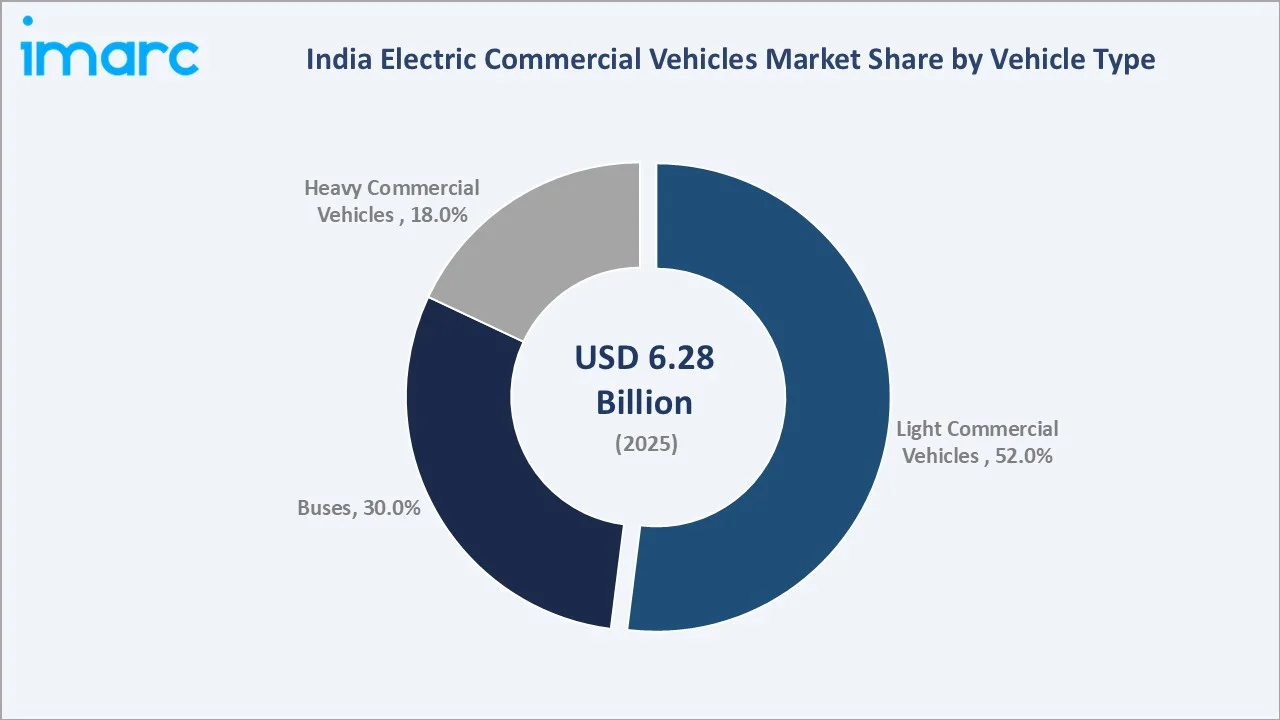

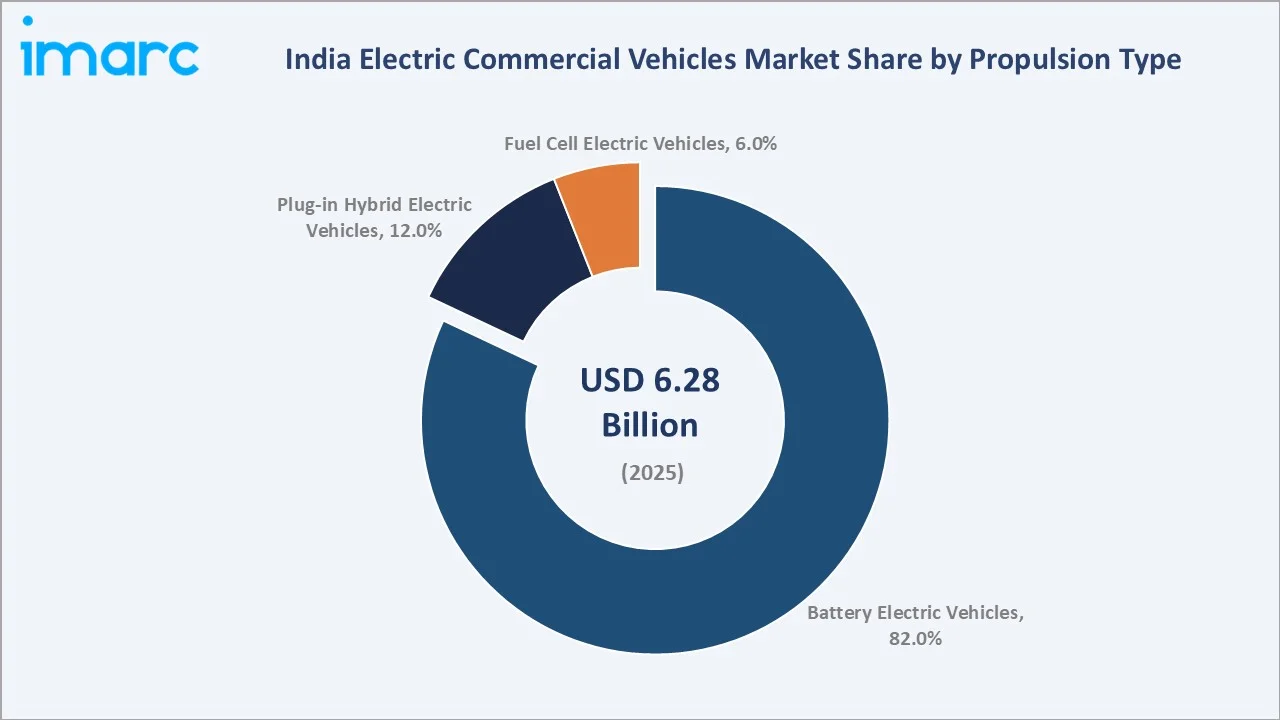

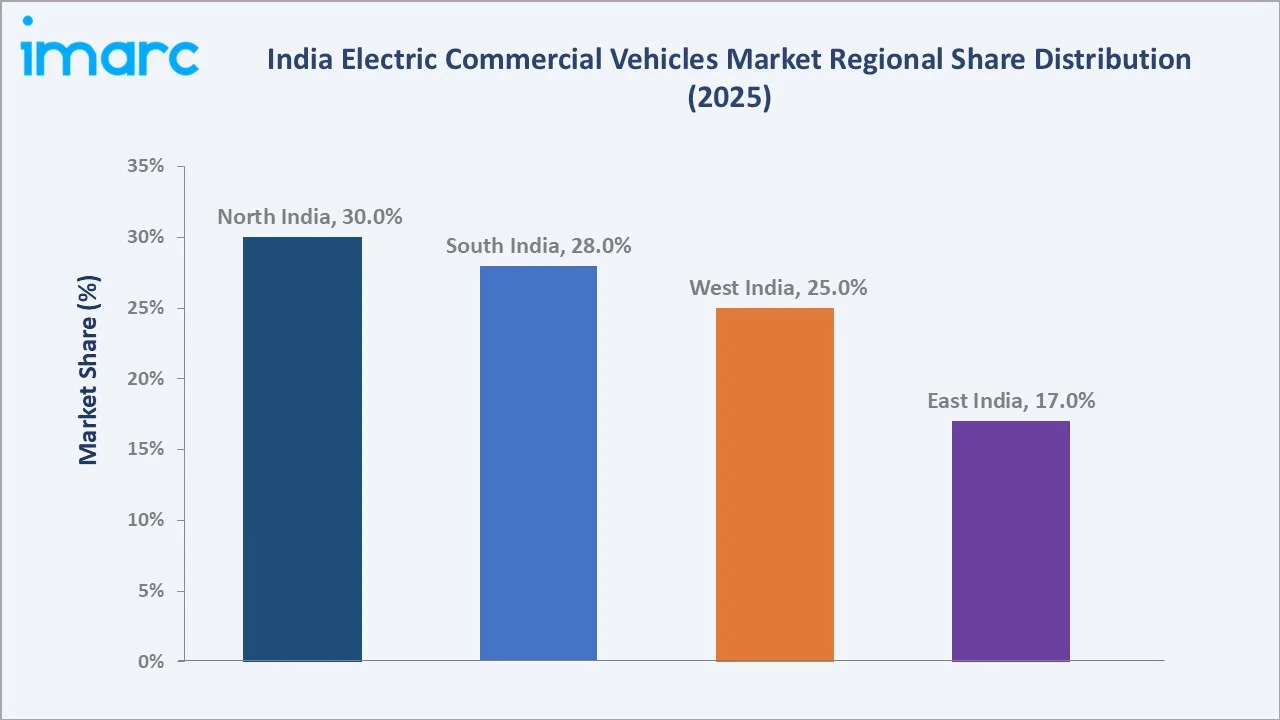

The India electric commercial vehicles (ECV) market reached USD 6.28 Billion in 2025 and is projected to reach USD 44.55 Billion by 2034, growing at a CAGR of 23.59% during 2026-2034. The market is propelled by government mandates under PM E-DRIVE and PM eBus Sewa, declining battery costs, and the compelling total cost of ownership (TCO) advantage for fleet operators. Battery Electric Vehicles (BEV) command 82.0% of propulsion share, while Light Commercial Vehicles (LCVs) lead vehicle type at 52.0%. North India holds the largest regional share at 30.0%.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 6.28 Billion |

|

Forecast Market Size (2034) |

USD 44.55 Billion |

|

CAGR (2026-2034) |

23.59% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region (2025) |

North India (30.0%) |

|

Fastest Growing Segment |

Battery Electric Vehicle (BEV) |

|

Dominant Vehicle Type |

Light Commercial Vehicle (LCV) – 52.0% |

|

Dominant Propulsion Type |

Battery Electric Vehicle (BEV) – 82.0% |

To get more information on this market, Request Sample

The market expanded from USD 2.18 Billion in 2020 to USD 6.28 Billion in 2025, anchored at USD 18.11 Billion by 2030, and forecast to reach USD 44.55 Billion by 2034. This trajectory reflects a structural shift in India's commercial fleet driven by regulatory push, economic viability, and growing charging infrastructure.

Executive Summary

India's electric commercial vehicles market is entering a period of accelerated growth, backed by one of the world's most ambitious EV policy frameworks. The market reached USD 6.28 Billion in 2025, up from USD 2.18 Billion in 2020, and is on course to reach USD 44.55 Billion by 2034. Structural demand drivers include rising fuel costs making EV TCO compelling for fleet operators, state transport undertaking (STU) tenders for electric buses under PM eBus Sewa, and private sector logistics players integrating electric last-mile delivery vehicles.

Battery Electric Vehicles dominate with 82.0% propulsion share (2025), reflecting mature BEV technology, strong charging ecosystem compatibility, and government incentive alignment. The BEV segment is projected to grow at approximately 26.4% CAGR through 2034. Light Commercial Vehicles lead vehicle type at 52.0%, driven by rapid e-commerce and last-mile delivery growth. The Bus segment at 30.0% reflects aggressive STU electrification, anchored by the country's largest-ever e-bus tender for 10,900 buses awarded in December 2025.

North India leads regionally at 30.0% (2025), driven by Delhi-NCR's Switch Delhi EV campaign, freight corridor density, and policy leadership. South India at 28.0% reflects Bengaluru and Chennai logistics expansion. Key players include Tata Motors Limited, Megha Engineering & Infrastructures Limited (MEIL), Ashok Leyland, and Mahindra & Mahindra Ltd., collectively defining India's ECV competitive structure.

Key Market Insights

|

Insight |

Data |

|

Dominant Vehicle Type |

Light Commercial Vehicle (LCV) - 52.0% share (2025) |

|

Dominant Propulsion |

Battery Electric Vehicle (BEV) - 82.0% share (2025) |

|

Leading Region |

North India - 30.0% share (2025) |

|

Market Opportunity |

PM eBus Sewa Phase-2; HCV EV expansion; BaaS models in LCV |

|

Key Companies |

Tata Motors Limited, Megha Engineering & Infrastructures Limited (MEIL), Ashok Leyland, and Mahindra & Mahindra Ltd. |

Key Analytical Observations Supporting the Above Data:

- LCV at 52.0%: Light Commercial Vehicles dominate due to the explosive growth of e-commerce logistics and last-mile delivery. Lower battery size requirements make EVs especially cost-competitive in this segment, with Tata Ace EV and Mahindra Treo Zor setting the benchmark.

- BEV at 82.0%: Battery Electric Vehicles lead propulsion as mature charging infrastructure, falling battery costs (down ~18% in 2024), and government incentive structures strongly favour BEV over PHEV and FCEV.

- North India at 30.0%: The region leads due to Delhi's comprehensive Switch Delhi EV policy, high freight activity on National Highway corridors, and concentrated STU procurement.

- CAGR at 23.59%: Among the highest EV segment growth rates globally, supported by India's PM E-DRIVE subsidy extension, PLI scheme for advanced chemistry cell batteries, and GST reduction on EV components.

India Electric Commercial Vehicles Market Overview

India's electric commercial vehicles market encompasses battery electric, plug-in hybrid, and fuel cell powered trucks, buses, and light commercial vehicles used across logistics, public transport, last-mile delivery, and construction applications. The ecosystem integrates domestic vehicle OEMs, international battery technology partners, government-owned and private fleet operators, state transport undertakings, and a rapidly expanding EV charging infrastructure network. Macroeconomic tailwinds include India's GDP growth at ~6.5% projected for FY2026-27 (RBI), infrastructure development under the National Logistics Policy, and India's commitment to net zero emissions by 2070, driving accelerated fleet electrification.

Market Dynamics

To evaluate market opportunities, Request Sample

Market Drivers

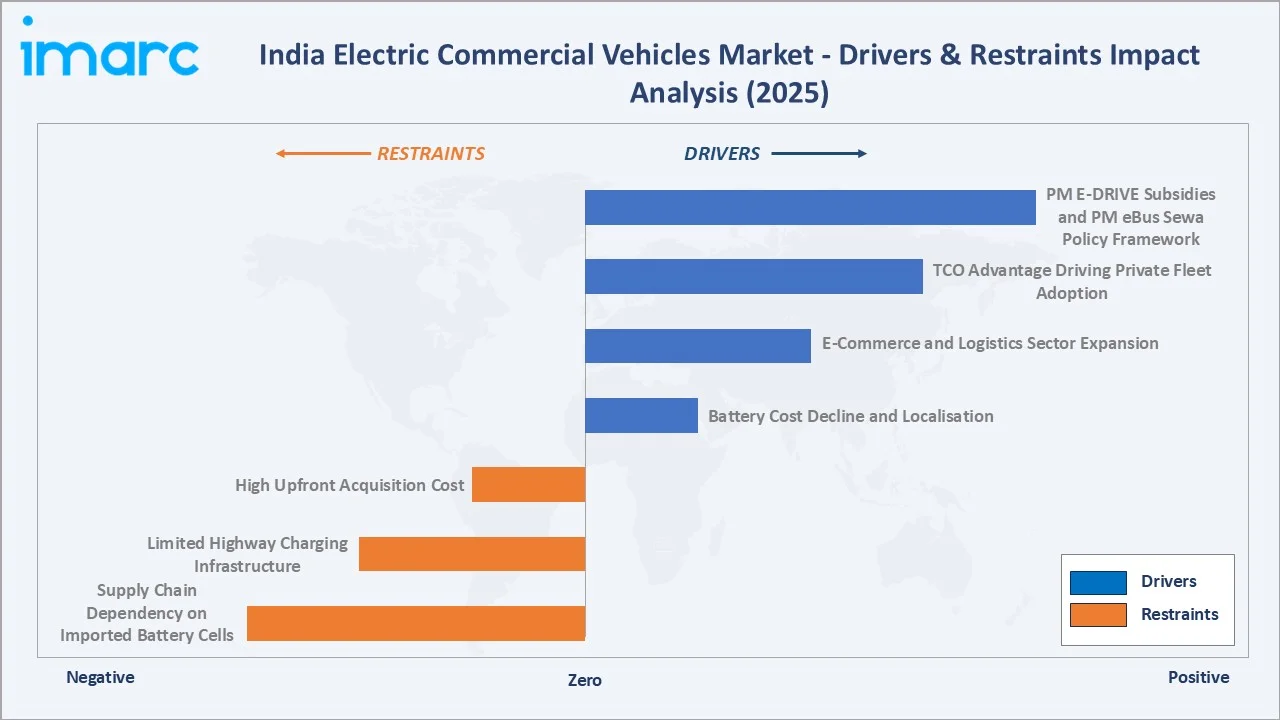

- PM E-DRIVE Subsidies and PM eBus Sewa Policy Framework: Government demand creation is the single largest driver of India's ECV market. The PM E-DRIVE scheme allocated a total outlay of ₹10,900 crore in 2024, with PM eBus Sewa adding INR 57,613 crore to deploy 10,000+ electric buses. The December 2025 tender for 10,900 electric buses, India's largest-ever, is estimated to represent USD 1.2+ Billion in procurement, directly catalysing OEM capacity expansion.

- TCO Advantage Driving Private Fleet Adoption: Electric commercial vehicles offer a compelling total cost of ownership benefit at current utilisation rates. Fleet operators report fuel savings of INR 5-8 per kilometre over diesel equivalents. For last-mile delivery vehicles operating 80-100 km daily, payback period of 3-4 years are achievable. Mahindra Last Mile Mobility's BaaS (Battery-as-a-Service) model with Vidyut, launched in 2025, further reduces upfront acquisition costs to INR 2.50 per km rental.

- E-Commerce and Logistics Sector Expansion: India's e-commerce market is projected to reach USD 350 Billion by 2030 (IBEF), driving structural demand for last-mile delivery EVs. Companies including Flipkart, Amazon India, and Zomato have committed to 100% electric delivery fleets. This creates consistent private-sector demand for LCV EVs, independent of government incentive cycles.

- Battery Cost Decline and Localisation: Battery pack costs in India declined approximately 20% in 2024, reaching USD 115 per kWh for commercial vehicle applications. The PLI Scheme for Advanced Chemistry Cells (ACC) aims to develop 50 GWh of domestic manufacturing capacity, with ACME, Ola Cell Technologies, and Rajesh Exports among winners, targeting further cost reduction to below USD 75 per kWh by 2028-30.

Market Restraints

- High Upfront Acquisition Cost: An electric bus costs INR 1.2-1.5 crore compared to INR 35-50 lakh for a diesel equivalent, limiting private fleet adoption without financing support or government subsidies.

- Limited Highway Charging Infrastructure: India's national highway network has limited fast-charging stations capable of supporting commercial vehicles, creating range anxiety for intercity freight operations.

- Supply Chain Dependency on Imported Battery Cells: Over 70% of lithium-ion cells used in India ECVs are imported from China, creating cost and supply chain vulnerability. The ACC PLI scheme is targeting domestic production, but commercial-scale output is not expected before 2027-28.

Market Opportunities

- HCV Electrification: Heavy commercial vehicles represent an emerging frontier. Tata Motors began deliveries of its 55-ton electric prime mover (Prima E.55S) to BillionE Mobility in April 2026, signalling the start of heavy freight electrification.

- Battery-as-a-Service (BaaS) Models: BaaS structures reduce EV acquisition costs by separating battery ownership from vehicle ownership. Mahindra's partnership with Vidyut and expected similar models from Olectra and JBM can unlock SME fleet adoption.

- Green Freight Corridors: The Ministry of Ports, Shipping, and Waterways is developing EV-priority green freight corridors linking major ports to industrial hubs, creating demand for electric medium-duty trucks in port logistics.

Market Challenges

- Skilled EV Technician Shortage: India lacks sufficient trained technicians for high-voltage EV systems. The government bodies estimate a gap in EV-skilled workers, impacting after-sales service quality.

- Regulatory Complexity Across States: Varying state-level EV policies, permit requirements, and road tax structures create operational complexity for multi-state fleet operators, slowing adoption outside early-mover states like Delhi, Maharashtra, and Karnataka.

Emerging Market Trends

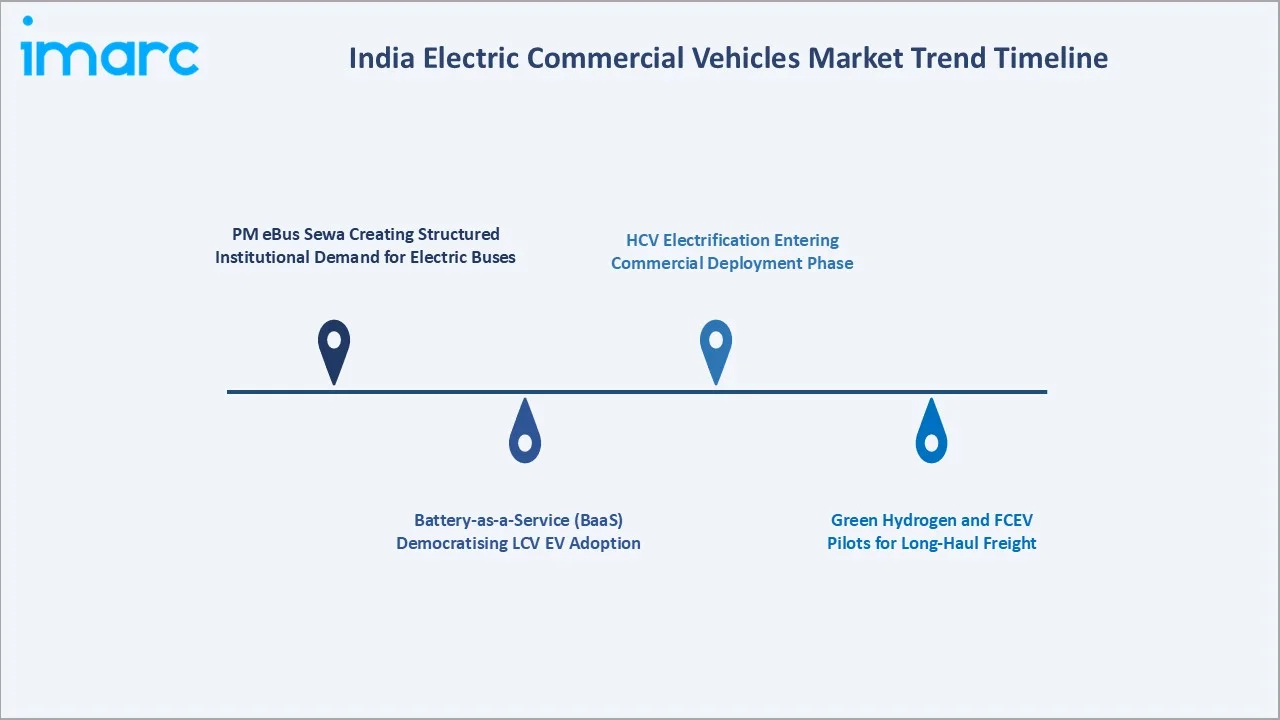

1. PM eBus Sewa Creating Structured Institutional Demand for Electric Buses

PM eBus Sewa is transforming India's electric bus market from project-level pilots to systematic national deployment. The scheme covers 169 cities across 20 states, with operational and maintenance costs borne by the central government for 10 years, eliminating the STU financial risk that previously slowed adoption.

2. Battery-as-a-Service (BaaS) Democratising LCV EV Adoption

BaaS models are removing the primary barrier to LCV EV adoption among SME fleet operators and individual owner-drivers. Mahindra Last Mile Mobility's 2025 BaaS launch at INR 2.50/km effectively converts battery capital expenditure to an operating expense, aligning EV cost structure with driver cash flow patterns. Similar models are expected from Tata Motors and Olectra for bus and truck segments by 2027.

3. HCV Electrification Entering Commercial Deployment Phase

India's heavy commercial vehicle electrification moved from pilot to commercial deployment in 2025-26. Tata Motors' delivery of Prima E.55S 55-ton electric tractor-trailers to BillionE Mobility in April 2026 marks the first commercial heavy freight electrification by an Indian OEM. The company has committed to expanding battery-electric HCV offerings as a key FY27 growth driver.

4. Green Hydrogen and FCEV Pilots for Long-Haul Freight

While BEV dominates the current market at 82.0%, Fuel Cell Electric Vehicles represent 6.0% of propulsion share (2025) and are attracting pilot investments for long-haul applications where battery range is insufficient. NTPC and Indian Oil have commenced hydrogen refuelling station pilots in Delhi-NCR and Pune, creating early infrastructure for FCEV commercial vehicles targeting 2028-30 commercial deployment.

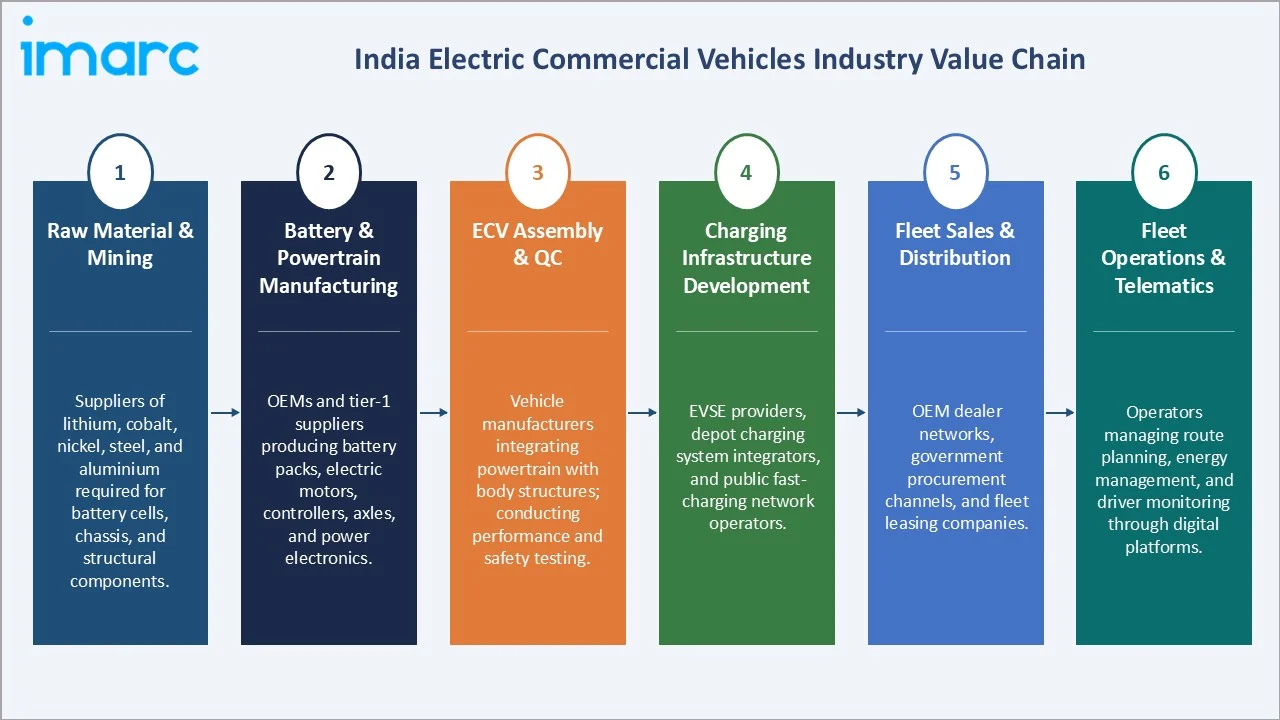

Industry Value Chain Analysis

India's electric commercial vehicles value chain spans eight stages from raw material extraction to end-of-life battery recycling. The chain's strategic bottleneck lies in battery cell manufacturing, where India currently imports over 70% of lithium-ion cells. Government PLI interventions are progressively shifting this balance toward domestic production.

|

Value Chain Stage |

Key Activities & Participants |

|

Raw Material & Mining |

Suppliers of lithium, cobalt, nickel, steel, and aluminium required for battery cells, chassis, and structural components. |

|

Battery & Powertrain Manufacturing |

OEMs and tier-1 suppliers producing battery packs, electric motors, controllers, axles, and power electronics. |

|

ECV Assembly & QC |

Vehicle manufacturers integrating powertrain with body structures; conducting performance and safety testing. |

|

Charging Infrastructure Development |

EVSE providers, depot charging system integrators, and public fast-charging network operators. |

|

Fleet Sales & Distribution |

OEM dealer networks, government procurement channels, and fleet leasing companies. |

|

Fleet Operations & Telematics |

Operators managing route planning, energy management, and driver monitoring through digital platforms. |

The charging infrastructure stage is India's most rapidly evolving value chain component. Tata Power, EESL, NTPC, and private players including Statiq, Volttic, and Zeon Charging are collectively targeting 50,000+ commercial vehicle-compatible charging points by 2028, addressing the infrastructure gap that remains the most cited barrier to fleet electrification.

Technology Landscape in the India Electric Commercial Vehicles Industry

Battery Electric Vehicle (BEV) Technology

BEV technology dominates India's ECV market at 82.0% (2025), driven by NMC (Nickel Manganese Cobalt) and LFP (Lithium Iron Phosphate) chemistries. LFP is gaining preference in buses and LCVs for its superior thermal stability, longer cycle life, and lower cost profile. Battery capacities typically range from 27 kWh (Tata Ace EV) to 270 kWh for heavy-duty electric buses.

Vehicle Telematics and Fleet Management Platforms

Advanced telematics integration is becoming standard across India's electric commercial fleet. OEMs including Tata Motors and Mahindra embed IoT sensors tracking battery state-of-health, route energy consumption, and predictive maintenance triggers. Fleet management platforms from players like FleetX and Locus integrate EV charging scheduling with route optimisation, improving fleet utilisation rates by 15-20% versus manual management.

Charging Technology: Fast and Ultra-Fast DC Charging

Commercial vehicle charging infrastructure is evolving from depot-only AC charging to a hybrid AC+DC fast charging network. CCS2 (Combined Charging System 2) at 50-150 kW is becoming the standard for medium-duty and heavy commercial vehicles.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share (2025) |

|

Vehicle Type |

Light Commercial Vehicle (LCV) |

52.0% |

|

Propulsion Type |

Battery Electric Vehicle (BEV) |

82.0% |

|

Battery Capacity |

🔒 |

🔒 |

|

End User |

🔒 |

🔒 |

|

Region |

North India |

30.0% |

By Vehicle Type

Light Commercial Vehicles (LCVs) lead at 52.0% (2025), driven by last-mile delivery and intra-city logistics. LCVs benefit most from EV economics due to short daily routes, predictable charging patterns, and the elimination of fuel cost as the largest operating expense. E-commerce giants and 3PL logistics companies are the primary demand drivers, with Tata Ace EV and Mahindra Treo Zor dominating the segment.

To access detailed market analysis, Request Sample

Buses hold 30.0% (2025), representing the highest-value segment by per-unit economics. Government STU procurement under PM eBus Sewa is the structural demand driver. Heavy Commercial Vehicles at 18.0% are at an early electrification stage but represent the highest future growth potential as HCV EV technology matures through 2027-30.

By Propulsion Type

Battery Electric Vehicles (BEV) dominate at 82.0% (2025), reflecting the commercial maturity of BEV technology, alignment with India's urban charging infrastructure, and the strongest incentive coverage under PM E-DRIVE and state EV policies. BEV adoption is expanding from buses and LCVs into medium commercial vehicle segments as range and payload capabilities improve.

Plug-in Hybrid Electric Vehicles (PHEV) represent 12.0% (2025), serving as transition technology for operators requiring longer range than current BEV offerings. PHEV adoption is most prominent in medium-duty trucks serving mixed urban-intercity routes. Fuel Cell Electric Vehicles (FCEV) at 6.0% are at pilot stage, with NTPC and Indian Oil hydrogen refuelling pilot programmes in Delhi-NCR and Pune providing early infrastructure, targeting commercial deployment by 2028-30.

Regional Market Insights

|

Region |

Share (2025) |

Key Market Drivers & Characteristics |

|

North India |

30.0% |

Strong government procurement, Delhi EV policy, concentrated freight corridors along NH-44 and NH-48. |

|

South India |

28.0% |

Bengaluru and Chennai IT-driven logistics demand, active state EV policies in Tamil Nadu and Karnataka. |

|

West India |

25.0% |

Mumbai-Pune industrial belt, JNPT container port logistics, Maharashtra EV policy incentives driving adoption. |

|

East India |

17.0% |

Emerging growth in Kolkata and Odisha industrial zones; lowest penetration but fastest incremental growth. |

North India's 30.0% leadership reflects Delhi's Switch Delhi policy, NH-44 and NH-48 freight corridor density, and the highest concentration of STU procurement across Delhi Transport Corporation, Haryana Roadways, and UP SRTC. South India at 28.0% is driven by Karnataka's EV policy, Bengaluru's IT-logistics demand, and Tamil Nadu's manufacturing proximity to EV component suppliers. West India at 25.0% reflects Maharashtra's progressive EV policy, Mumbai's port logistics volume, and the Pune industrial corridor. East India at 17.0% is the least penetrated region but growing above national CAGR from a lower base, driven by Odisha's industrial zone growth and West Bengal's urban bus electrification.

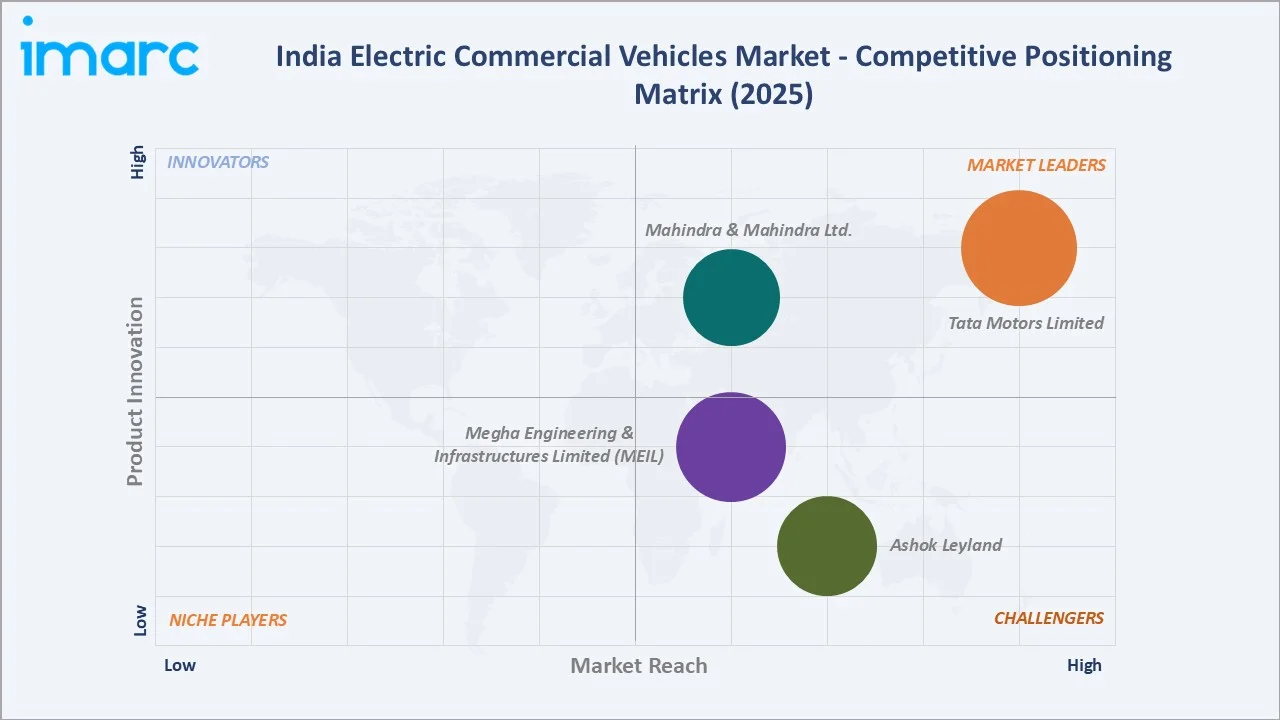

Competitive Landscape

India's electric commercial vehicles competitive landscape is moderately concentrated at the top, with Tata Motors leading across segments and a cluster of strong challengers competing in bus and LCV niches. The competitive dynamic is shaped by government procurement volumes, OEM technology partnerships, and battery supply chain access.

|

Company |

Key Brands / Models |

Market Position |

Core Strength |

|

Tata Motors Limited |

Tata Ace EV, Ultra EV, Prima E.55S |

Market Leader |

Broadest ECV portfolio; largest manufacturing capacity; strong STU contracts. |

|

Megha Engineering & Infrastructures Limited (MEIL) |

C9, K9, K7 e-Bus; Blade Battery Series |

Strong Challenger |

Operates Olectra Greentech Limited; pioneer in electric buses; 10,200+ bus order book; BYD technology partnership. |

|

Ashok Leyland |

Switch EiV12, Switch EiV22, SWITCH IeV3, SWITCH IeV4 |

Strong Challenger |

Operates Switch Mobility; fastest growing share in FY25; state transport undertaking focus. |

|

Mahindra & Mahindra Ltd. |

Mahindra Zeo, Mahindra Zor Grand, Mahindra Treo |

Market Leader |

Operates Mahindra Last Mile Mobility Limited (MLMML); dominates electric last-mile and LCV segments; BaaS partnership with Vidyut. |

Key Company Profiles

Tata Motors Limited

Tata Motors Limited is India's largest commercial vehicle manufacturer with over 35% market share in total CVs and the commanding position in electric commercial vehicles. Its ECV portfolio spans from Tata Ace EV (mini-truck) to Starbus EV (city bus) and Prima E.55S (55-ton electric prime mover).

- Key Products: Tata Ace EV, Ultra EV, Prima E.55S, and others.

- Recent Developments: In April 2026, Tata Motors launched Tata Intra EV Pickup to address the expanding need for delivering a dependable, high earning solution for India’s evolving cargo requirements.

- Strategic Focus: Expanding battery-electric HCV offerings as a key FY27 priority; investing in hydrogen and electric technology portfolio; pursuing international ECV contracts.

Megha Engineering & Infrastructures Limited (MEIL)

Megha Engineering & Infrastructures Limited (MEIL), which operates Olectra Greentech, is India's pioneer electric bus manufacturer. It introduced electric buses to India in 2015 in partnership with BYD and commands approximately 20% of the electric bus market (2025).

- Key Products: C9, K9, K7 Blade Battery electric buses, and others.

- Recent Developments: In February 2025, Olectra Greentech placed an order of over 2,000 electric bus chassis comprising of the K9, C9, and K7 variants, with BYD.

- Strategic Focus: Executing the 10,200+ bus order book; launching next-generation bus platform in Q3 FY27; entering the electric truck segment.

Mahindra & Mahindra Ltd.

Mahindra dominates India's electric LCV and last-mile delivery segment through its Last Mile Mobility division. Its electric three-wheeler cargo vehicle range, Treo Zor and Alfa Cargo EV, has established strong market presence in intra-city logistics.

- Key Products: Mahindra Zeo, Mahindra Zor Grand, Mahindra Treo, and others.

- Recent Developments: In April 2026, Mahindra Last Mile Mobility Limited (MLMML) claimed to reinforce India’s No.1 electric commercial vehicle manufacturer for the fourth consecutive financial year, with a sale of more than 3.4 Lakh EVs till that date.

- Strategic Focus: Deepening BaaS model adoption; expanding 4-wheeler LCV EV portfolio for logistics and delivery segments.

Market Concentration Analysis

India's electric commercial vehicles market is moderately concentrated at the top, with the leading OEMs, Tata Motors Limited, Megha Engineering & Infrastructures Limited (MEIL), Ashok Leyland, and Mahindra & Mahindra Ltd.- controlling approximately 69.27% of the electric CV market in FY25 (FADA data).

Concentration is evolving through two competing forces: Tata Motors' share erosion in electric CVs (from 65.91% to 48.46% in FY25) as Switch Mobility and Mahindra expand, indicating healthy competitive development; while the bus segment shows re-concentration around Olectra and Switch's OEM-STU contract advantages. The HCV EV segment, currently nascent, is expected to consolidate around 2-3 players (Tata, Olectra, and potentially a new entrant) through 2030.

Barriers to entry in the ECV market include high capital requirements for battery technology development or partnership, the need for government certification and approval for STU contracts, and the requirement for nationwide dealer and service networks. These factors sustain the market leadership of established automotive OEMs over pure-play EV startups.

Investment & Growth Opportunities

Highest Growth Segments

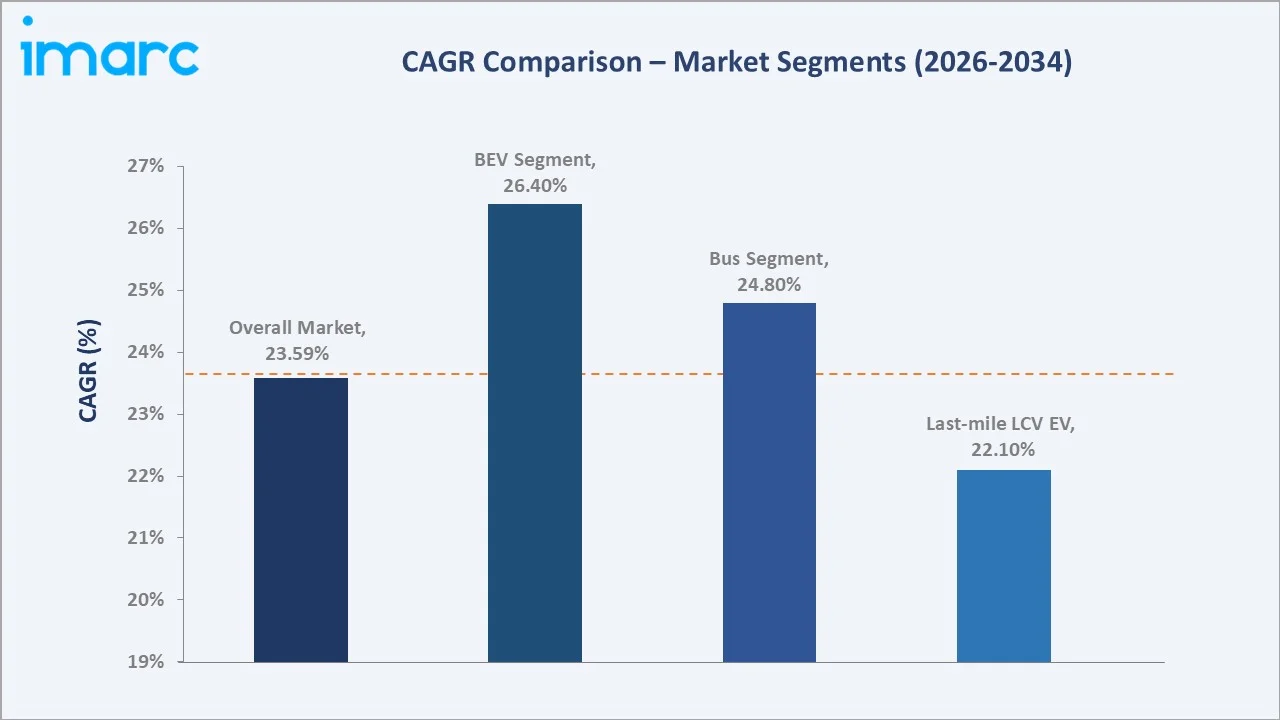

- BEV segment growing at ~26.4% CAGR - the highest within the ECV market - through expanding charging infrastructure and falling battery costs.

- Bus segment at ~24.8% CAGR through institutional PM eBus Sewa demand; 10,900-bus December 2025 tender alone represents USD 1.2+ Billion procurement.

- HCV electrification at early-stage entry with 2028-2032 commercial scale-up as battery energy density and range overcome long-haul freight requirements.

- Last-mile LCV EV platform ~22.1% CAGR through e-commerce logistics demand; Tata Ace EV and Mahindra Treo Zor growing alongside platform economics.

Emerging Investment Opportunities

- EV Charging Infrastructure for Commercial Vehicles: India's commercial vehicle charging network is underbuilt relative to fleet electrification targets. Depot charging solutions and highway fast-charging stations for trucks and buses represent INR 25,000-30,000 crore investment opportunity through 2030.

- Battery Recycling and Second-Life Battery Applications: India's first-generation electric bus fleet - deployed from 2017-2022 - will begin reaching end-of-battery-life cycles by 2027-30. Battery recycling and second-life energy storage applications present a growing addressable market.

- EV Financing Platforms for Fleet Operators: NBFCs and fintech platforms offering EV-specific financing products - including residual value guarantees and battery replacement coverage - can unlock SME fleet adoption in Tier-2 and Tier-3 cities.

Future Market Outlook (2026-2034)

India's electric commercial vehicles market is projected to grow from USD 6.28 Billion in 2025 to USD 44.55 Billion by 2034, delivering a 23.59% CAGR. The market anchor value of USD 18.11 Billion by 2030 reflects the structural transition from subsidised adoption to economics-driven adoption, as battery costs reach below USD 75/kWh by 2028-30 making EVs cost-competitive with diesel CVs without government incentives.

Three structural forces will define the market through 2034: first, institutional demand from India's STU electrification creating baseload EV bus demand through PM eBus Sewa and successor schemes; second, e-commerce structural growth creating private-sector LCV EV demand that is incentive-independent; and third, HCV electrification entering commercial deployment phase by 2028-30 as battery range and payload constraints are resolved, representing the highest-value market expansion vector.

Technological disruption risks include hydrogen fuel cell commercial vehicles displacing BEV in long-haul heavy freight by 2030 if FCEV costs decline faster than expected. India's NTPC and ONGC hydrogen pilot programmes, targeting 50 hydrogen refuelling stations by 2027, represent early infrastructure for this potential transition. Competitive risks include Chinese EV OEM market entry as India evaluates its vehicle import policy, and potential supply chain disruptions in lithium and cobalt critical minerals.

Research Methodology

Primary Research

Primary research comprised structured interviews with India electric commercial vehicles industry stakeholders, including fleet operators, STU procurement officials, ECV OEM representatives, battery technology providers, charging infrastructure developers, and EV financing platforms across North, South, West, and East India. Consumer survey data was gathered from 150+ fleet operators across LCV, bus, and medium commercial vehicle segments.

Secondary Research

Secondary research encompassed India EV policy documents (PM E-Drive, PM eBus Sewa, PLI ACC Scheme), Ministry of Road Transport & Highways vehicle registration data (Vahan Dashboard), FADA retail sales data, company annual reports (Tata Motors, Olectra Greentech, Ashok Leyland), investor presentations, press releases, and third-party market intelligence databases. Over 60 secondary sources were reviewed.

Forecasting Models

Market revenue forecasts were developed using a bottom-up approach: vehicle segment unit volume projections multiplied by average selling prices per segment (LCV, bus, HCV), with BEV/PHEV/FCEV propulsion mix applied to each vehicle type. Unit volume projections integrate government procurement pipeline data, private fleet electrification announcements, and battery cost curve assumptions. A top-down cross-validation using India's total commercial vehicle market size and ECV penetration rate benchmarked against comparable markets (China, Europe) was applied.

India Electric Commercial Vehicles Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Vehicle Types Covered | Light Commercial Vehicle (LCV), Heavy Commercial Vehicle (HCV), Buses |

| Propulsion Types Covered | Battery Electric Vehicle (BEV), Plug in Hybrid Vehicle (PHEV), Fuel Cell Electric Vehicle (FCEV) |

| Battery Capacities Covered | <50kwh, 50-150 kwh,>150kwh |

| End Users Covered | Logistics, Last Mile Delivery |

| Regions Covered | North India, South India, East India, West India |

| Companies Covered | Tata Motors Limited, Megha Engineering & Infrastructures Limited (MEIL), Ashok Leyland, Mahindra & Mahindra Ltd, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the India electric commercial vehicles market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the India electric commercial vehicles market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the India electric commercial vehicles industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the India Electric Commercial Vehicles Market Report

The India electric commercial vehicles market reached USD 6.28 Billion in 2025, driven by PM E-DRIVE subsidies, PM eBus Sewa, TCO advantages, and expanding e-commerce logistics demand across urban centres.

The India electric commercial vehicles market grows at 23.59% CAGR during 2026-2034, reaching USD 44.55 Billion by 2034, supported by policy mandates, battery cost declines, and institutional bus procurement.

Light Commercial Vehicles (LCVs) lead at 52.0% (2025), driven by e-commerce last-mile delivery demand and the TCO advantage of EVs in short-range intra-city logistics applications.

Battery Electric Vehicles (BEV) dominate at 82.0% (2025), reflecting mature technology, urban charging infrastructure alignment, and the strongest government incentive coverage under PM E-DRIVE and state EV policies.

North India leads at 30.0% (2025) through Delhi's comprehensive Switch Delhi EV policy, high freight corridor density on NH-44 and NH-48, and concentrated state transport undertaking procurement.

The market was USD 2.18 Billion in 2020. It is projected to reach USD 18.11 Billion by 2030, reflecting a 3x expansion from 2025 as bus fleet electrification and HCV pilots scale commercially.

Leading companies include Tata Motors Limited, Megha Engineering & Infrastructures Limited (MEIL), Ashok Leyland, and Mahindra & Mahindra Ltd, among others.

Battery Electric Vehicles hold 82.0% of propulsion share in 2025, with the BEV segment projected to grow at approximately 26.4% CAGR through 2034 as infrastructure expands and battery costs fall.

Key drivers include PM E-DRIVE and PM eBus Sewa government policies, declining battery costs (down ~18% in 2024), e-commerce logistics demand, BaaS financing models, and increasing OEM product portfolios.

India awarded its largest-ever electric bus tender for 10,900 buses in December 2025 under PM eBus Sewa, representing approximately USD 1.2+ Billion in procurement and covering deployments across multiple Indian cities.

The market is projected to reach USD 18.11 Billion by 2030, driven by STU electrification completion, growing HCV EV deployment, BaaS model scaling, and India's 30% EV penetration target by 2030.

Top opportunities include EV charging infrastructure for commercial vehicles, BaaS financing platforms, HCV electrification technology, battery recycling businesses, and depot charging solutions for state transport undertakings.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)