India Electric Motor Market Size, Share, Trends and Forecast by Motor Type, Voltage, Rated Power, Magnet Type, Weight, Speed, Application, and Region, 2026-2034

India Electric Motor Market Summary:

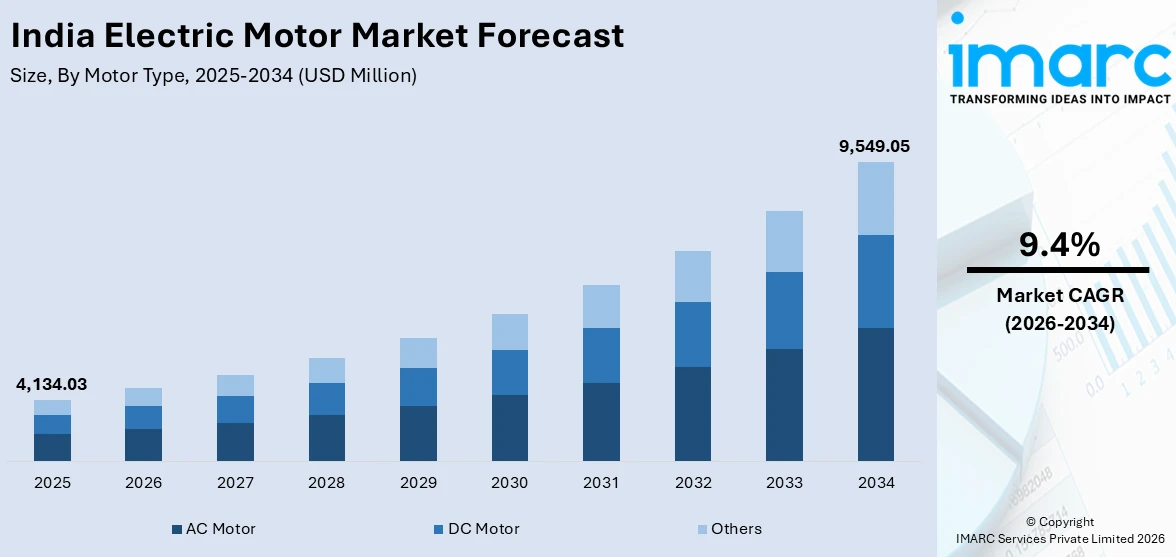

The India electric motor market size was valued at USD 4,134.03 Million in 2025 and is projected to reach USD 9,549.05 Million by 2034, growing at a compound annual growth rate of 9.4% from 2026-2034.

The market is driven by accelerating industrialization, government-backed energy efficiency mandates, and the rapid expansion of electric mobility across the country. Growing adoption of automated manufacturing systems, widespread deployment of motors in infrastructure and renewable energy applications, and deepening urbanization are reinforcing demand across diverse end-use sectors. The proliferation of modern HVAC installations, smart city developments, and expanding transportation electrification continue to strengthen India's position within the India electric motor market share.

Key Takeaways and Insights:

- By Motor Type: AC motor dominates the market with a share of 53.4% in 2025, driven by versatility, wide availability across power ratings, and extensive deployment in industrial machinery and HVAC applications across the country.

- By Voltage: Low voltage electric motors lead the market with a share of 67.5% in 2025, owing to leading role in industrial automation, consumer appliances, commercial systems, and general manufacturing operations nationwide.

- By Rated Power: Integral horsepower motors represent the largest segment with a market share of 56.2% in 2025, driven by heavy industries, large-scale manufacturing plants, and commercial infrastructure projects across India.

- By Magnet Type: Ferrite dominates the market with a share of 52.8% in 2025, owing to its affordability and reliable magnetic performance across general industrial and consumer-grade motor applications throughout the country.

- By Weight: Medium weight motors represent the market with a share of 42.5% in 2025, driven by deployed across industrial machinery, transportation equipment, and commercial HVAC systems in India.

- By Speed: Medium speed motors lead the market with a share of 38.5% in 2025, owing to manufacturing facilities, conveyor systems, and process industries requiring balanced operational speed and torque.

- By Application: Industrial machinery represents the largest segment with a market share of 32.5% in 2025, driven by India's rapidly expanding manufacturing base, industrial automation upgrades, and smart factory deployments.

- By Region: West and Central India leads the market with a share of 27.4% in 2025, owing to dense industrial clusters in Maharashtra and Gujarat with significant manufacturing and infrastructure presence.

- Key Players: The India electric motor market features established domestic and global manufacturers competing on energy efficiency ratings, product diversification, and technological innovation, while leveraging strategic partnerships and expanding distribution networks to consolidate their market positioning.

To get more information on this market Request Sample

The India electric motor market is expanding robustly, supported by a confluence of industrial modernization, policy-driven electrification, and broadening application diversity. Increasing government emphasis on energy conservation is compelling industries to transition toward higher-efficiency motor technologies across manufacturing, utilities, and commercial facilities. In September 2025, ABB India announced an investment of over ₹140 crore to expand and modernize its low-voltage motors manufacturing facility in India while introducing IE5 ultra-premium efficiency motors designed for industries such as cement, metals, textiles, and pharmaceuticals. The rapid scaling of India's electric vehicle (EV) sector is generating significant demand for specialized traction and auxiliary motor systems. Industrial automation adoption under smart manufacturing frameworks is expanding motor deployment across precision motion control, robotics, and high-speed production equipment. Additionally, sustained infrastructure investment in water management, metro rail, and renewable energy installations is extending the addressable market for electric motors.

India Electric Motor Market Trends:

Transition Toward High-Efficiency Motor Technologies

The progressive shift toward energy-efficient motor technologies represents a defining India electric motor market trend reshaping procurement and manufacturing standards across industrial sectors. Regulatory frameworks mandating higher efficiency classifications are compelling industries to replace legacy motor installations with advanced alternatives that deliver measurable reductions in energy consumption. In December 2025, Siemens Limited approved the sale of its low-voltage motors and geared motors business in India to Innomotics India Private Limited for about INR 2,200 crore, strengthening the country’s industrial motor ecosystem and aligning operations with global motor and drive technologies. Manufacturers are responding by integrating optimized winding materials, superior magnetic designs, and improved thermal management systems into their product portfolios.

Integration of Smart Motors with Industrial IoT Platforms

The convergence of electric motors with industrial digital ecosystems is driving a fundamental evolution in how motors are deployed, monitored, and maintained across India. Smart motors equipped with embedded sensors enable continuous operational monitoring, supporting predictive maintenance strategies that reduce unplanned downtime and extend service intervals. As per sources, ABB introduced the ABB Ability™ Smart Sensor for low-voltage motors, enabling wireless monitoring of vibration, temperature, speed, and other parameters through cloud analytics to support predictive maintenance in industrial facilities. Connectivity with automated control architectures allows seamless synchronization between motor performance and broader production workflows.

Electrification of Transportation and EV Ecosystem Expansion

India's accelerating transition to electric mobility is generating substantial new demand streams for traction motors, drivetrain systems, and auxiliary motor components across two-wheelers, three-wheelers, buses, and passenger vehicles. Permanent magnet synchronous and switched reluctance motor architectures are gaining prominence due to their superior power density and efficiency characteristics suited to EV applications. In October 2025, India recorded a milestone with more than 2.34 lakh electric vehicles sold in a single month across two-wheelers, three-wheelers, passenger vehicles, and commercial vehicles, reflecting rapid expansion of EV adoption and supporting demand for traction motor technologies. Growing government investment in public transport electrification and charging infrastructure is reinforcing downstream motor procurement.

Market Outlook 2026-2034:

The India electric motor market is poised for sustained expansion throughout the forecast period, driven by deepening industrialization, accelerating electric vehicle adoption, and growing infrastructure investments across the country. Increasing government emphasis on energy efficiency, expanding renewable energy installations, and the rapid proliferation of industrial automation are broadening application diversity across sectors. Rising urbanization, smart manufacturing transitions, and the electrification of transportation are reinforcing long-term demand, positioning the market for consistent and broadly supported revenue growth across all major segments. The market generated a revenue of USD 4,134.03 Million in 2025 and is projected to reach a revenue of USD 9,549.05 Million by 2034, growing at a compound annual growth rate of 9.4% from 2026-2034.

India Electric Motor Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

|

Motor Type |

AC Motor |

53.4% |

|

Voltage |

Low Voltage Electric Motors |

67.5% |

|

Rated Power |

Integral Horsepower Motors |

56.2% |

|

Magnet Type |

Ferrite |

52.8% |

|

Weight |

Medium Weight Motors |

42.5% |

|

Speed |

Medium Speed Motors |

38.5% |

|

Application |

Industrial Machinery |

32.5% |

|

Region |

West and Central India |

27.4% |

Motor Type Insights:

- AC Motor

- Induction AC Motor

- Synchronous AC Motor

- DC Motor

- Brushed DC Motor

- Brushless DC Motor

- Others

AC motor dominates with a market share of 53.4% of the total India electric motor market in 2025.

AC motors command the largest share of India's electric motor market owing to their operational reliability, wide availability across diverse power ratings, and seamless compatibility with existing industrial electrical infrastructure. Their ability to efficiently handle variable power outputs makes them indispensable across manufacturing facilities, HVAC installations, water management systems, and commercial buildings. The simplicity of construction and reduced maintenance requirements compared to DC motor alternatives further enhance their appeal among both large industrial operators and smaller commercial establishments.

Within the AC motor segment, induction motor variants remain the dominant choice for general-purpose industrial applications due to their robustness and cost-effectiveness. Synchronous AC motors are gaining ground in precision manufacturing and high-efficiency industrial processes where speed accuracy is critical. Growing regulatory pressure to upgrade installed motor fleets to higher efficiency ratings is expanding replacement demand within the segment, while renewable energy installations and expanding water infrastructure projects are broadening AC motor adoption into new application categories.

Voltage Insights:

- Low Voltage Electric Motors

- Medium Voltage Electric Motors

- High Voltage Electric Motors

Low voltage electric motors lead with a share of 67.5% of the total India electric motor market in 2025.

Low voltage motors account for the substantial majority of India's electric motor consumption, driven by their extensive deployment across consumer appliances, commercial HVAC systems, light industrial machinery, and agricultural pump applications. Their compatibility with standard electrical grid infrastructure, ease of installation, and broad availability across diverse power ranges establish them as the default specification for most general industrial and commercial motor requirements. According to reports, CG Power and Industrial Solutions Limited inaugurated a 4200 sq. m manufacturing facility in Ahmednagar, Maharashtra, to produce smart low-voltage motors ranging from 75 kW to 1000 kW, strengthening domestic motor production capacity.

The diverse application base of low voltage motors spanning pumps, fans, conveyors, blowers, compressors, and material handling systems ensures persistent demand across multiple industry verticals. Automation trends are accelerating in robotics and precision manufacturing machinery, where variable-frequency drives enable energy-efficient speed and torque regulation. Government-backed infrastructure programs covering smart city development, water supply modernization, and metro expansion are driving large-scale procurement, while deepening industrialization across tier-II and tier-III cities continues to broaden the segment's market base.

Rated Power Insights:

- Fractional Horsepower Motors

- Fractional Horsepower (< 1/8) Motors

- Fractional Horsepower (1/8 - 1/2) Motors

- Fractional Horsepower (1/2 - 1) Motors

- Integral Horsepower Motors

- Integral Horsepower (1 - 5) Motors

- Integral Horsepower (10 - 50) Motors

- Integral Horsepower (50 - 100) Motors

- Integral Horsepower (>100) Motors

Integral horsepower motors exhibit a clear dominance with a 56.2% share of the total India electric motor market in 2025.

Integral horsepower motors command most of the rated power segment owing to their critical role across heavy industrial applications including large-scale manufacturing equipment, industrial compressors, pumps, and processing machinery. Their capacity to deliver sustained power output under demanding operational conditions makes them indispensable across energy, chemicals, textiles, metals, and automotive production sectors. India's infrastructure expansion and ongoing industrial capacity additions are driving consistent procurement, particularly as facilities upgrade equipment to meet modern efficiency standards and evolving production requirements.

Higher-rated integral horsepower motors are increasingly specified for energy-intensive manufacturing processes incorporating variable-frequency drives for precision speed regulation and energy management. The transition toward higher efficiency-class motors within this segment is gaining momentum as industrial operators prioritize energy cost reduction and regulatory compliance simultaneously. Renewable energy installations, water treatment infrastructure, data centers, and large commercial facilities represent growing application areas, creating new sustained demand for high-reliability integral horsepower motor systems across India's diversifying industrial landscape.

Magnet Type Insights:

- Ferrite

- Neodymium (NdFeB)

- Samarium Cobalt (SmCo5 and Sm2Co17)

Ferrite leads with a market share of 52.8% of the total India electric motor market in 2025.

Ferrite magnets dominate India's electric motor market owing to their significant cost advantage relative to rare-earth alternatives, widespread domestic availability, and adequate magnetic performance across general industrial and consumer motor applications. Resistance to corrosion and demagnetization under standard operating conditions makes ferrite suitable for motors deployed in pumps, fans, appliances, and light industrial machinery. Manufacturers favor ferrite-based motors in cost-sensitive segments where performance requirements do not necessitate premium rare-earth magnet systems, supporting mass-market motor production across multiple application categories.

Despite growing interest in rare-earth magnets for high-performance applications, ferrite retains its dominant position owing to structural cost pressures in consumer appliances, agricultural equipment, and general industrial motors. Rare-earth supply chain vulnerabilities and import dependency are motivating manufacturers to innovate within ferrite motor technology to achieve improved performance without compromising cost competitiveness. This ongoing technological refinement supports continued ferrite market leadership across mainstream industrial motor segments, reinforcing its position as the preferred magnet material throughout the forecast period.

Weight Insights:

- Low Weight Motors

- Medium Weight Motors

- High Weight Motors

Medium weight motors dominate with a market share of 42.5% of the total India electric motor market in 2025.

Medium weight motors occupy the critical operational middle ground between compact lightweight units and heavy-duty industrial motors, making them ideally suited for a broad range of applications including conveyor systems, industrial fans, pumps, and standard manufacturing equipment. Their balanced physical profile enables versatile installation across both fixed industrial environments and mobile or semi-portable equipment configurations. India's manufacturing-oriented economy generates consistent demand for medium weight motors, particularly across automotive assembly, food processing, pharmaceutical production, and packaging industries.

As India expands its industrial capacity under production-linked incentive programs and foreign investment attraction initiatives, demand for medium weight motors grows proportionately with manufacturing facility expansions. Compatibility with standard drive and control systems reduces integration complexity and total procurement costs for industrial operators. Increasing deployment in commercial HVAC installations, water management systems, and waste treatment infrastructure further deepens demand across the segment, while advancements improving power density within medium weight designs help manufacturers meet escalating efficiency standards without compromising manageable physical specifications.

Speed Insights:

- Ultra-High-Speed Motors

- High-Speed Motors

- Medium Speed Motors

- Low Speed Motors

Medium speed motors lead with a share of 38.5% of the total India electric motor market in 2025.

Medium speed motors serve as the operational backbone of India's industrial motor market, powering conveyors, compressors, centrifugal pumps, industrial fans, and general manufacturing machinery across the most prevalent industrial application categories. Their alignment with standard process requirements across manufacturing sectors including steel, cement, chemicals, food and beverages, and textiles makes them the most widely specified motor speed category. Variable-frequency drives paired with medium speed motors enable efficient operational speed regulation and energy consumption management across complex industrial workflows.

India's deepening industrialization and expanding industrial corridor development are sustaining robust demand for medium speed motors, particularly as manufacturing capacity additions drive large-scale equipment installations. Their growing integration with industrial IoT monitoring platforms enables real-time performance analytics and condition-based maintenance, adding technology-driven demand from digitally progressive manufacturing operators. Expanding commercial and residential HVAC deployments across accelerating urban construction programs are further reinforcing medium speed motor procurement, ensuring sustained segment leadership throughout the forecast period.

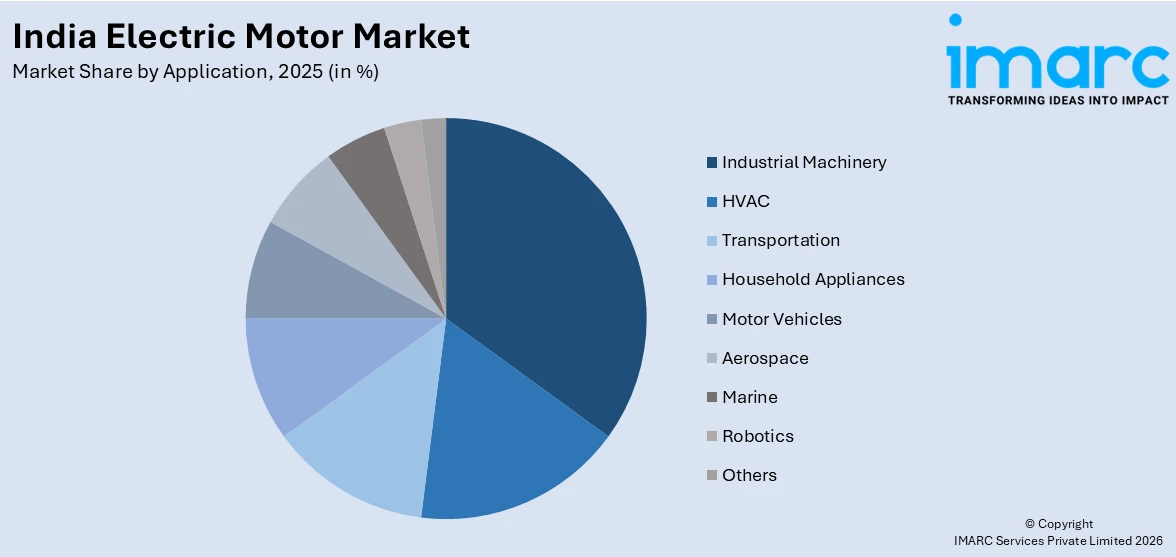

Application Insights:

Access the comprehensive market breakdown Request Sample

- Industrial Machinery

- HVAC

- Transportation

- Household Appliances

- Motor Vehicles

- Aerospace

- Marine

- Robotics

- Others

Industrial machinery exhibits a clear dominance with a 32.5% share of the total India electric motor market in 2025.

Industrial machinery represents the primary demand driver for electric motors in India, encompassing machine tools, material handling systems, industrial mixers, crushers, presses, and automated production line equipment across diverse manufacturing sectors. India's expanding manufacturing base, underpinned by government industrial policy frameworks and rising export demand, consistently widens the installed base of industrial motors. As per sources, Toyota Kirloskar Auto Parts secured approval under the Government of India’s PLI scheme for two electric vehicle trans-axle components, becoming the first auto component manufacturer receiving incentives for advanced automotive technologies.

The industrial machinery segment is benefiting from India's growing investments across capital goods, automotive manufacturing, specialty chemicals, and pharmaceuticals, all of which require reliable and energy-efficient motor solutions at scale. Replacement demand is expanding as industrial operators upgrade legacy motor installations to higher efficiency-class units in response to regulatory mandates and operational cost pressures. Growing industrial clusters and special economic zones in key manufacturing states are driving greenfield equipment investments, while deepening automation penetration ensures the India electric motor market outlook for industrial machinery applications remains strongly positive throughout the forecast period.

Regional Insights:

- North India

- West and Central India

- South India

- East and Northeast India

West and Central India dominates with a market share of 27.4% of the total India electric motor market in 2025.

West and Central India dominates the regional electric motor market, anchored by the dense industrial concentration across Maharashtra and Gujarat. These states host extensive automotive manufacturing clusters, chemical processing facilities, petrochemical complexes, and textile industries that collectively generate sustained demand for diverse motor types and power ratings. Gujarat's position as a leading investment destination, supported by progressive industrial policy and renewable energy development programs, has attracted substantial manufacturing capacity that reinforces the region's leadership in motor procurement.

Maharashtra's well-developed infrastructure, port connectivity, and skilled workforce further reinforce its prominence in motor-intensive industrial activity across the western and central corridor. The concentration of large-scale engineering industries, pharmaceutical manufacturers, and food processing units across both states creates diversified and resilient demand streams for electric motors spanning multiple application categories. Growing industrial investments in Madhya Pradesh and adjoining states are additionally expanding the regional demand base, ensuring West and Central India maintains its leading position throughout the forecast period.

Market Dynamics:

Growth Drivers:

Why is the India Electric Motor Market Growing?

Expanding Industrialization and Manufacturing Investments

India's rapidly expanding industrial base is a primary growth driver for the electric motor market, as rising manufacturing activity across automotive, chemicals, textiles, pharmaceuticals, and food processing sectors increases motor procurement at scale. In May 2025, Schaeffler India inaugurated a ₹330 crore manufacturing facility in Shoolagiri, Tamil Nadu to produce automotive powertrain and electrified transmission components, supporting local supply chains for industrial and EV markets. Government-led programs promoting domestic production and attracting foreign manufacturing investments are deepening industrial capacity across established and emerging corridors. Growing industrial cluster development in multiple states is generating consistent demand for motors across diverse power ratings and application categories, reinforcing the market's upward trajectory.

Rising Urbanization and Infrastructure Development

Accelerating urbanization across India is driving sustained demand for electric motors through expanding residential construction, commercial building installations, and large-scale public infrastructure projects. Metro rail networks, airports, water supply systems, and smart city initiatives collectively require motors across pumping, ventilation, escalation, and material handling applications. Growing tier-II and tier-III city development is broadening geographic demand distribution, while rising urban population density intensifies the need for reliable HVAC, water management, and building automation systems, all of which depend fundamentally on electric motor technologies.

Agricultural Modernization and Rural Electrification

India's ongoing agricultural modernization and rural electrification programs are generating growing demand for electric motors in irrigation pumping, crop processing, and cold storage applications across rural and peri-urban areas. Government initiatives supporting pump replacement with energy-efficient motor-driven systems are expanding procurement beyond traditional urban industrial markets. According to reports, in 2025, 9,42,189 standalone solar agricultural pumps had been installed in India under the PM-KUSUM scheme, supporting irrigation electrification and energy-efficient pump deployment across rural regions. Rising agricultural productivity targets, increasing mechanization of farming operations, and improving rural electricity access are collectively broadening the addressable market for electric motors, creating a significant and structurally supported demand stream that complements established industrial and commercial application sectors.

Market Restraints:

What Challenges the India Electric Motor Market is Facing?

High Initial Cost of Premium-Efficiency Motors

The elevated acquisition cost of motors meeting advanced efficiency classifications remains a significant barrier for cost-sensitive small and medium-sized enterprises across India's fragmented industrial base. While higher-efficiency motors deliver measurable long-term operational savings, the substantial upfront investment deters adoption among buyers lacking favorable financing options or clear payback period visibility, slowing the overall efficiency upgrade transition across price-prioritized industrial procurement segments.

Dependence on Imported Raw Materials and Components

India's electric motor manufacturing sector faces structural vulnerabilities from reliance on imported raw materials including rare-earth magnets, high-grade copper, and specialized electrical steel. Global commodity price volatility in these critical inputs directly impacts domestic manufacturing costs, compressing producer margins and creating pricing instability. Limited domestic rare-earth production capacity further intensifies supply chain exposure, particularly as demand for permanent magnet motor technologies expands alongside EV adoption nationwide.

Market Fragmentation and Low-Cost Import Competition

India's electric motor industry remains highly fragmented, with numerous small and medium manufacturers operating alongside established global players, creating inconsistencies in product quality standards and intensifying price competition. The sustained availability of low-cost motor imports exerts significant downward pricing pressure on domestic producers, while smaller manufacturers struggle to invest in research, efficiency certification, and technology upgrades necessary to compete as regulatory standards and end-user performance expectations continue to rise.

Competitive Landscape:

The India electric motor market is characterized by a dynamic and competitive landscape shaped by the presence of well-established global manufacturers and strong domestic players competing across efficiency standards, product breadth, and technological innovation. Competition is sustained by continuous investment in energy-efficient motor development, digital integration capabilities, and adherence to progressively stringent Bureau of Energy Efficiency regulatory mandates. Market participants are differentiating through diversified product portfolios spanning AC, DC, and permanent magnet motor categories that address the full spectrum of industrial, commercial, and mobility applications. Strategic manufacturing expansions, aftersales service network development, and technology partnerships with automation and drive system providers are critical competitive levers shaping market positioning across India.

Recent Developments:

- In November 2025, Nidec Corporation began production at its Orchard Hub campus in Hubli-Dharwad, Karnataka. The 50-acre facility manufactures EV traction motors, high-efficiency industrial motors, generators, and energy storage systems, strengthening India’s domestic electric motor manufacturing ecosystem and supporting the country’s electrification and advanced industrial production capabilities.

India Electric Motor Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Motor Types Covered |

|

| Voltages Covered | Low Voltage Electric Motors, Medium Voltage Electric Motors, High Voltage Electric Motors |

| Rated Powers Covered |

|

| Magnet Types Covered | Ferrite, Neodymium (NdFeB), Samarium Cobalt (SmCo5 and Sm2Co17) |

| Weights Covered | Low Weight Motors, Medium Weight Motors, High Weight Motors |

| Speeds Covered | Ultra-High-Speed Motors, High-Speed Motors, Medium Speed Motors, Low Speed Motors |

| Applications Covered | Industrial Machinery, HVAC, Transportation, Household Appliances, Motor Vehicles, Aerospace, Marine, Robotics, Others |

| Regions Covered | North India, West and Central India, South India, East and Northeast India |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Electric Motor Market Report

The India electric motor market size was valued at USD 4,134.03 Million in 2025.

The India electric motor market is expected to grow at a compound annual growth rate of 9.4% from 2026-2034 to reach USD 9,549.05 Million by 2034.

AC motor holds the largest position in the India electric motor market, driven by its operational reliability, cost-effectiveness, and versatile applicability across industrial machinery, HVAC systems, manufacturing facilities, and commercial infrastructure throughout the country.

Key factors driving the India electric motor market include rapid industrialization, expanding EV adoption, government energy-efficiency mandates, rising industrial automation investments, infrastructure development programs, renewable energy expansion, and smart manufacturing transitions across diverse industrial sectors.

Major challenges include high upfront costs of premium-efficiency motors, dependence on imported rare-earth materials, market fragmentation, competition from low-cost imports, technical integration complexities in smart motor deployments, and inconsistent quality standards across India's fragmented domestic manufacturing base.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)