India Electric Scooter Market Size, Share, Trends and Forecast by Drive, Battery, Product, Battery Fitting, End Use, and Region, 2026-2034

India Electric Scooter Market Size, Share, Trends & Forecast (2026-2034)

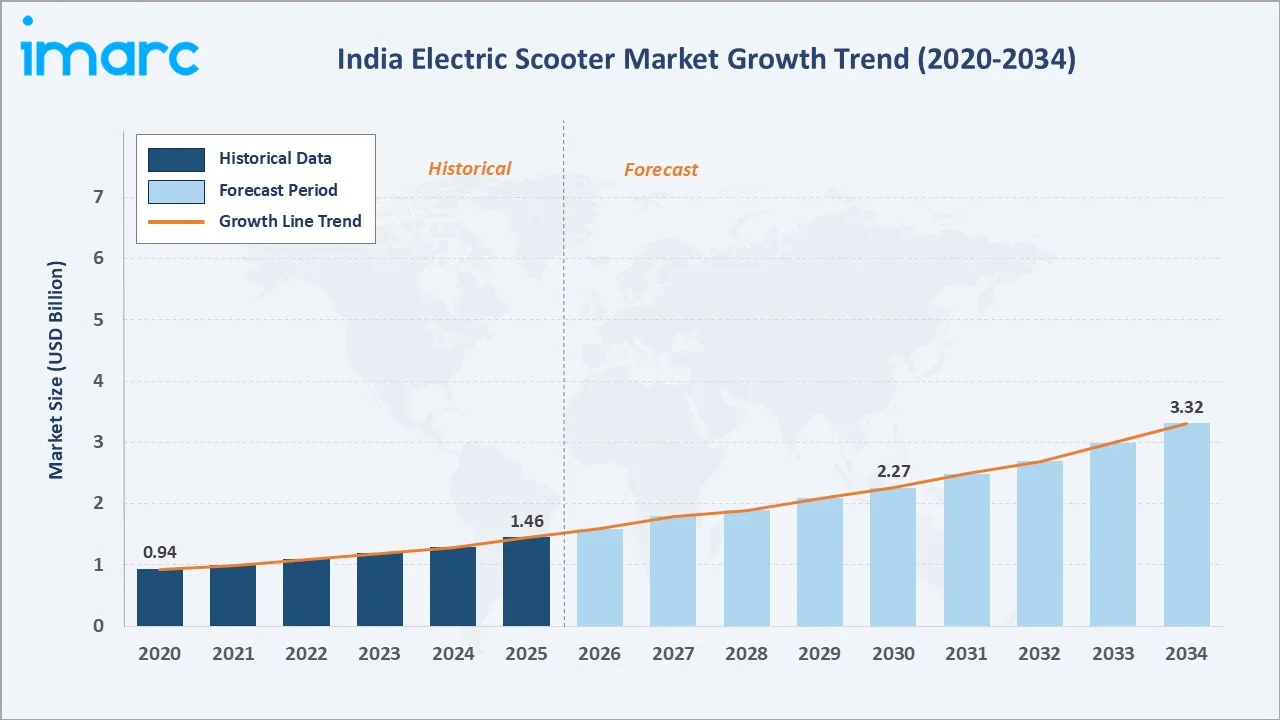

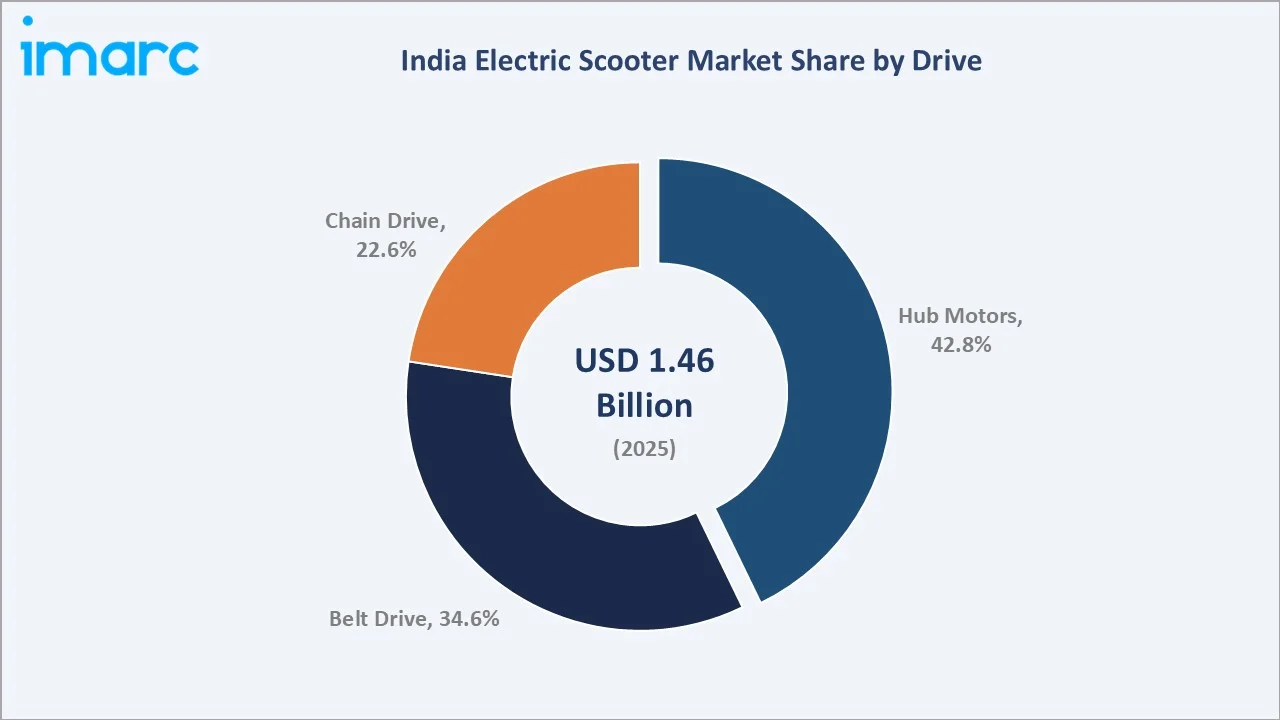

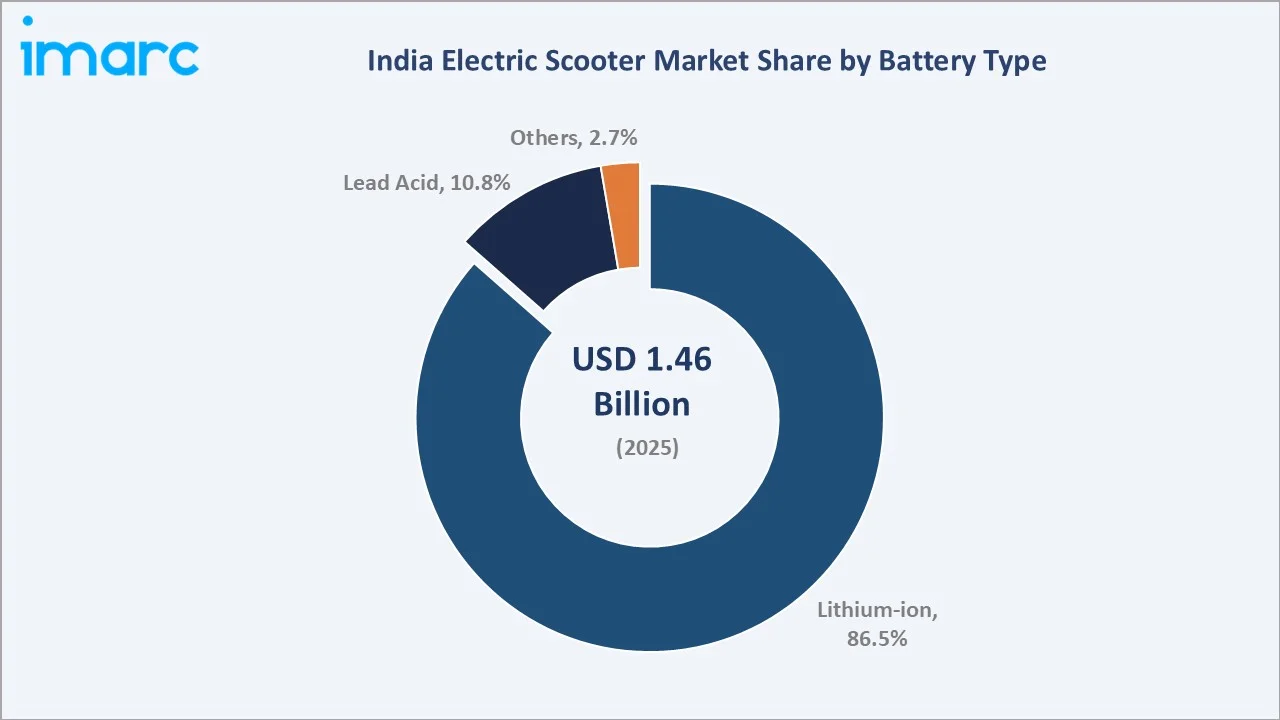

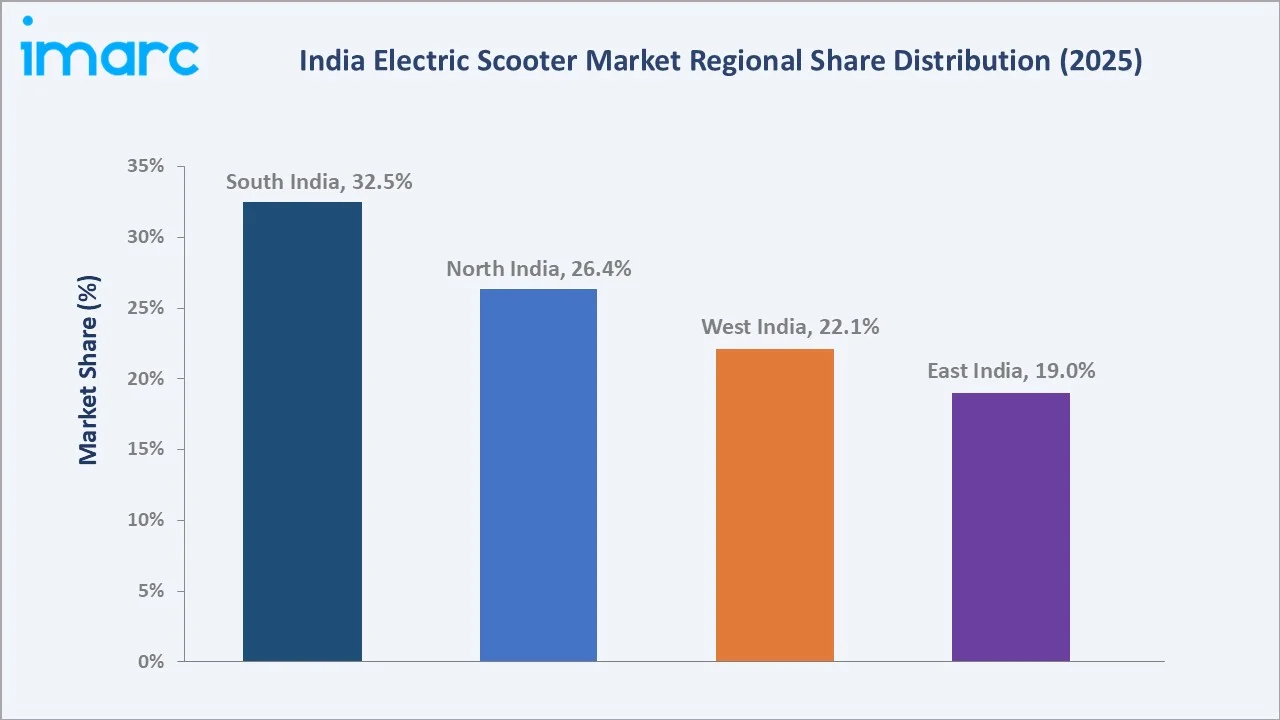

The India electric scooter market was valued at USD 1.46 Billion in 2025 and is projected to reach USD 3.32 Billion by 2034, expanding at a CAGR of 9.22% during 2026-2034. Growth is anchored by the Phase-II of the FAME Scheme with an outlay of Rs. 10,000 Crore supported 10 lakh e-2 Wheelers by 2024, rising petrol prices driving TCO superiority of EVs, PLI scheme-driven domestic battery manufacturing, and India’s ambitious EV penetration targets. Hub Motors dominate drive type at 42.8%, Lithium-Ion leads battery chemistry at 86.5%, and South India commands 32.5% regional market share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 1.46 Billion |

|

Forecast Market Size (2034) |

USD 3.32 Billion |

|

CAGR (2026-2034) |

9.22% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Region |

South India (32.5%, 2025) |

|

Fastest Growing Region |

East India (CAGR ~10.5%, 2026-2034) |

The India electric scooter market growth expanded from USD 0.94 Billion in 2020 to USD 1.46 Billion in 2025. Anchored at USD 2.27 Billion in 2030, the forecast is to USD 3.32 Billion by 2034. India’s e-2W sector sold a record 1.28 million units in 2025, with legacy players TVS Motor, Bajaj Auto, Ather Energy, and Hero MotoCorp logging best-ever retails.

To get more information on this market, Request Sample

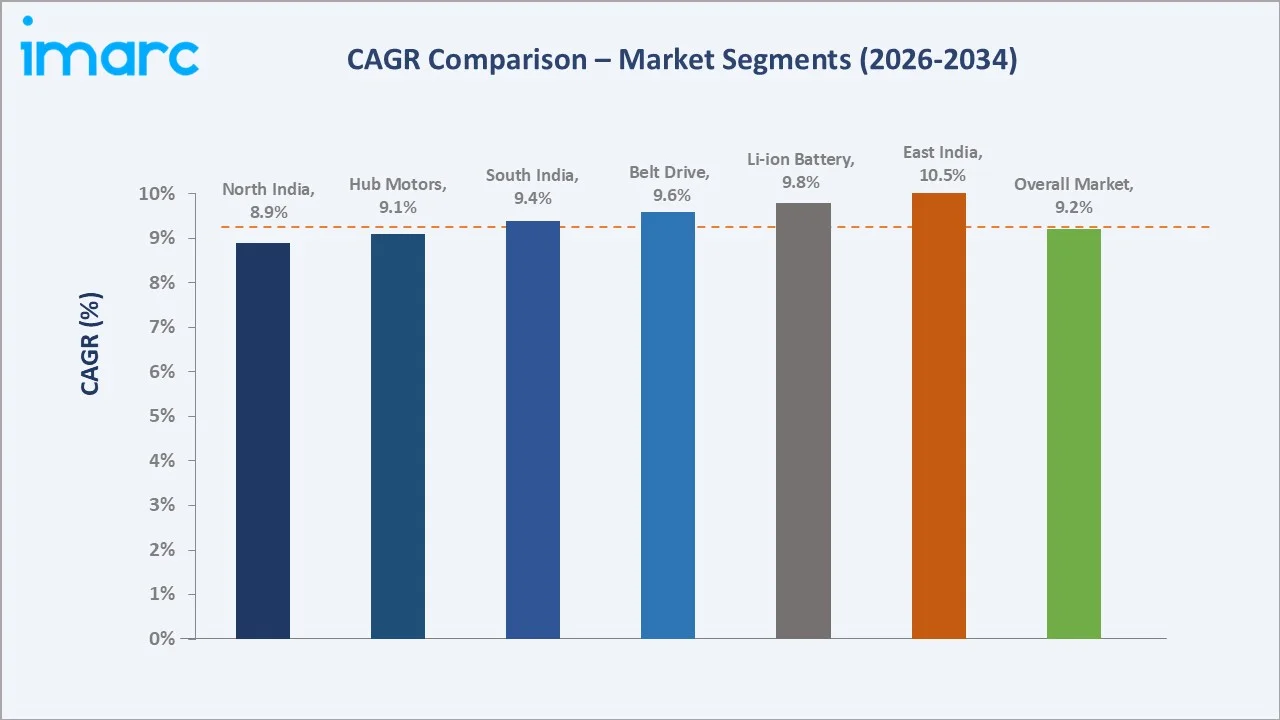

The CAGR across key segments. East India at ~10.5% CAGR grows fastest regionally, reflecting UDAN-inspired lower-tier city aspirational demand and state-level EV incentives from West Bengal, Odisha, and Bihar targeting EV registration fee waivers. Lithium-ion battery at ~9.8% CAGR dominates as the PLI Advanced Chemistry Cell scheme targets 50 GWh domestic manufacturing capacity, progressively reducing import dependency and cell costs.

Executive Summary

The India electric scooter market grew from USD 0.94 Billion in 2020 to USD 1.46 Billion in 2025, driven by FAME II subsidy activation, Ola Electric’s disruptive market entry that demonstrated mass-market EV scooter commercial viability, the industry-shaking 2022 battery fire incidents that triggered AIS-156 safety standard enforcement creating a quality floor, and India’s sustained petrol price elevation that made EV running cost economics undeniable to the aspirational Indian consumer. India’s electric scooter market is at an inflection point in 2025: the government’s transition from FAME II to EMPS 2024, combined with PLI Scheme-funded domestic Li-ion cell production scaling, signals the government’s commitment to a market where the subsidy dependency model transitions toward manufacturing competitiveness as the primary growth enabler.

Hub motors lead drive type at 42.8% as the default powertrain for mass-market EV scooters, where hub motor’s simplicity, lower cost, and instant torque at the wheel meet India’s urban commute requirements. Lithium-ion’s 86.5% dominance reflects India’s near-complete market transition from lead-acid to Li-ion, enabled by FAME II’s Li-ion battery requirement for subsidy eligibility, with the remaining 10.8% lead-acid serving the price-sensitive entry segment. South India’s 32.5% regional lead reflects the manufacturing cluster concentration of Ola, Ather, TVS, and Ampere in Tamil Nadu and Karnataka, creating the world’s most concentrated EV scooter production geography in a single Indian state pair.

Key Market Insights

|

Insight |

Data |

|

Dominant Drive |

Hub Motors – 42.8% revenue share (2025) |

|

Dominant Battery |

Lithium-Ion – 86.5% revenue share (2025) |

|

Leading Region |

South India – 32.5% share (2025) |

|

Fastest Growing Region |

East India (CAGR ~10.5%, 2026-2034) |

Key Analytical Observations Supporting the Above Data:

- Hub motors at 42.8% as India’s default mass-market EV drivetrain: Hub motor’s structural cost advantage makes it the default choice for EV scooters priced low. Ola Electric’s S1 X, India’s highest-volume single EV scooter model in FY2025, uses hub motor architecture to achieve its price point.

- Lithium-ion at 86.5% having transformed India’s EV scooter market quality floor: India’s rapid Li-ion transition was primarily catalysed by the FAME II scheme’s Li-ion battery eligibility requirement, manufacturers seeking the FAME II subsidy were compelled to adopt Li-ion from lead-acid within 12‐18 months.

- South India at 32.5% as India’s EV scooter manufacturing and adoption capital: Tamil Nadu alone hosts Ola Electric Future Factory, Ather Energy Hosur, TVS Motor Company Hosur, and Ampere Vehicles Coimbatore, collectively representing India’s domestic EV scooter manufacturing capacity in a single state.

India Electric Scooter Market Overview

India’s electric scooter market encompasses electric-motor-powered two-wheeled personal mobility vehicles for urban and semi-urban use, primarily in the 0.5–10 kW power range with 50–250 km stated range. The market spans a full spectrum from entry-level lead-acid hub-motor scooters through mid-tier lithium-ion hub-motor models to premium belt-drive high-performance models. Commercial EV scooters for last-mile delivery represent a high-growth sub-segment driven by India’s gig delivery workers’ fuel cost sensitivity.

Applications span personal daily commuting (30‐60 km), commercial last-mile delivery (Zomato, Swiggy, BigBasket fleet procurement), shared mobility, campus and gated community transport, and emerging rural connectivity. India’s macroeconomic context, petrol retail price stabilising in metro cities, EMPS 2024’s INR 10,000 per vehicle incentive, PLI-funded domestic battery manufacturing scaling, creates a structural cost and policy environment where EV scooter TCO is approaching and in urban high-mileage use cases has already achieved breakeven versus equivalent ICE scooters on a 3–4 year ownership cost basis.

Market Dynamics

To evaluate market opportunities, Request Sample

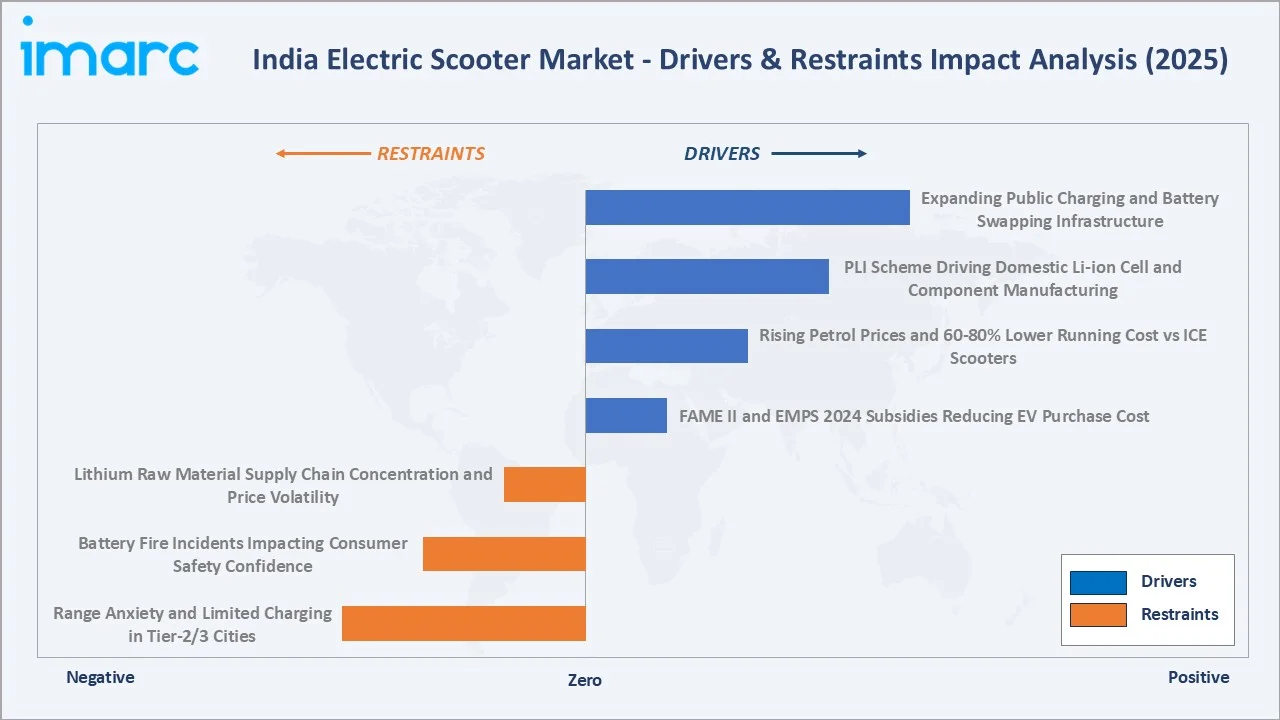

Market Drivers

- FAME II and EMPS 2024 Subsidies Reducing EV Purchase Cost: Ministry of Heavy Industries’ FAME II (Faster Adoption and Manufacturing of Hybrid and Electric Vehicles) Phase II scheme set up over 2,877 EV charging stations across 25 states.

- Rising Petrol Prices and 60-80% Lower Running Cost vs ICE Scooters: India’s average petrol retail price of INR 100–107/litre creates a stark cost differential versus EV scooters’ INR 0.15–0.25 per km electricity cost.

- PLI Scheme Driving Domestic Li-ion Cell and Component Manufacturing: India’s Production-Linked Incentive (PLI) Scheme for Advanced Chemistry Cell Battery Storage (INR 18,100 crore outlay) and PLI Scheme for Automobile and Auto Components (INR 25,938 crore) collectively fund the most critical supply chain dependency India’s EV industry must resolve, its near-total reliance on Chinese Li-ion cell imports.

- Expanding Public Charging and Battery Swapping Infrastructure: India’s public EV charging points grew to 12,146, creating a parallel range solution for consumers unwilling to wait for charging.

Market Restraints

- Range Anxiety and Limited Charging in Tier-2/3 Cities: Despite India’s urban EV adoption progress, 70%+ of India’s 1.5 million annual EV scooter sales are concentrated in 10‐15 top metros where charging access, service networks, and consumer EV awareness are relatively developed.

- Battery Fire Incidents Impacting Consumer Safety Confidence: Since November 14, 2022, a total of 23,865 electric vehicle-related accidents have been reported across various states over the past three years. During the same period, 26 incidents of fires involving electric vehicles were also recorded.

Market Opportunities

- Commercial and Gig Economy EV Fleet Transition: India’s 12 million gig delivery workers collectively represent India’s most compelling commercial EV fleet conversion opportunity.

- EV Scooter Export as India’s Emerging Two-Wheeler Export Segment: According to SIAM data, total two-wheeler exports increased by 21.4% in FY25, reaching 4,197,517 units, up from 3,458,416 units in FY24 is beginning to incorporate EV scooters.

Market Challenges

- Lithium Raw Material Supply Chain Concentration and Price Volatility: India’s electric scooter battery supply chain is highly dependent on Chinese lithium-ion cell imports, creating geopolitical supply risk and currency exposure that translates directly into electric scooter pricing volatility.

- Policy Uncertainty: Subsidy Scheme Transition Disruptions: India’s EV subsidy history demonstrates structural policy uncertainty: FAME I transitioned to FAME II with a 6-month gap in FY2019; FAME II lapsed in March 2024 before EMPS 2024.

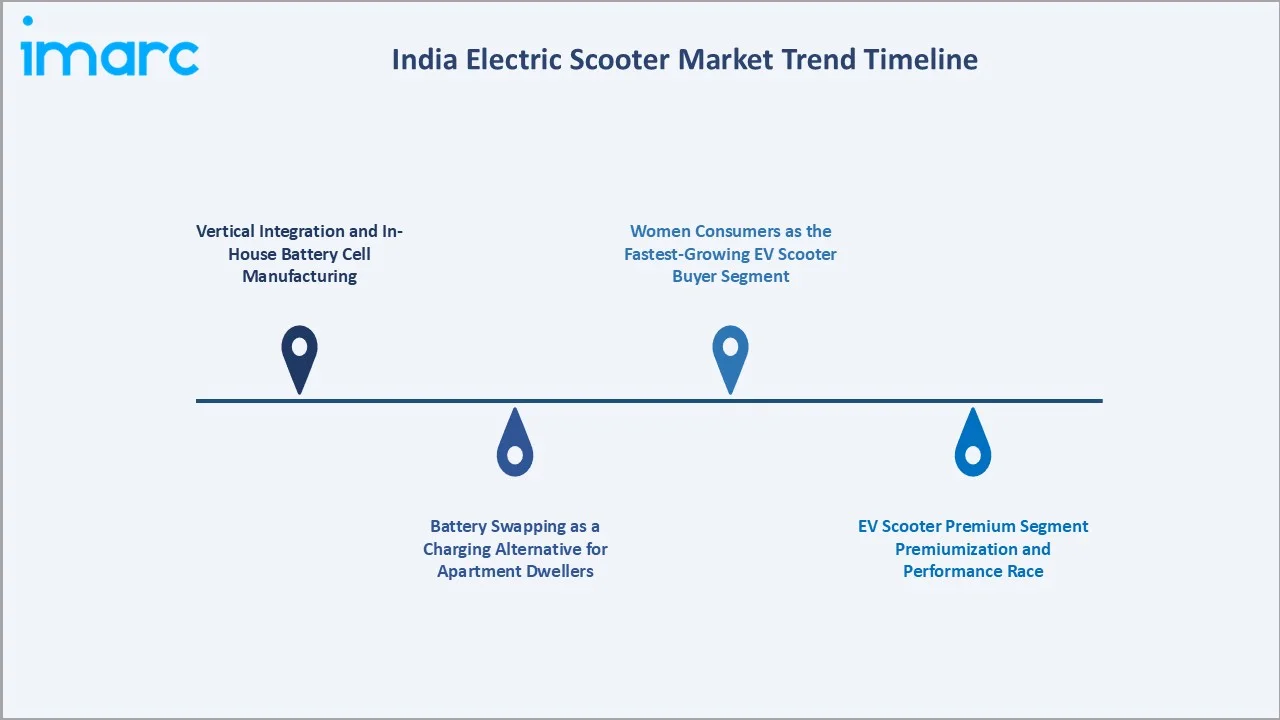

Emerging Market Trends

1. Vertical Integration and In-House Battery Cell Manufacturing

Ola Electric’s Cell Technologies Gigafactory, India’s first 4680 cylindrical cell Gigafactory for EV 2-wheelers, represents the most strategically significant development in India’s EV scooter industry since the FAME II scheme.

2. Battery Swapping as a Charging Alternative for Apartment Dwellers

India’s dense urban apartment culture creates a structural charging barrier that battery swapping uniquely addresses, demonstrating the disruptive pricing model that swappable EV scooters enable versus fixed-battery alternatives.

3. EV Scooter Premium Segment Premiumization and Performance Race

India’s premium EV scooter segment is experiencing a performance escalation unprecedented in India’s 2-wheeler history. This performance superiority is becoming India’s premium EV scooter segment’s primary appeal for the affluent urban consumer who previously owned performance ICE scooters.

4. Women Consumers as the Fastest-Growing EV Scooter Buyer Segment

India’s EV scooter market is exhibiting a striking gender adoption pattern: women buyers who historically purchased conventional Honda Activa and TVS Jupiter, India’s #1 and #2 best-selling ICE scooters, are disproportionately transitioning to EV scooters.

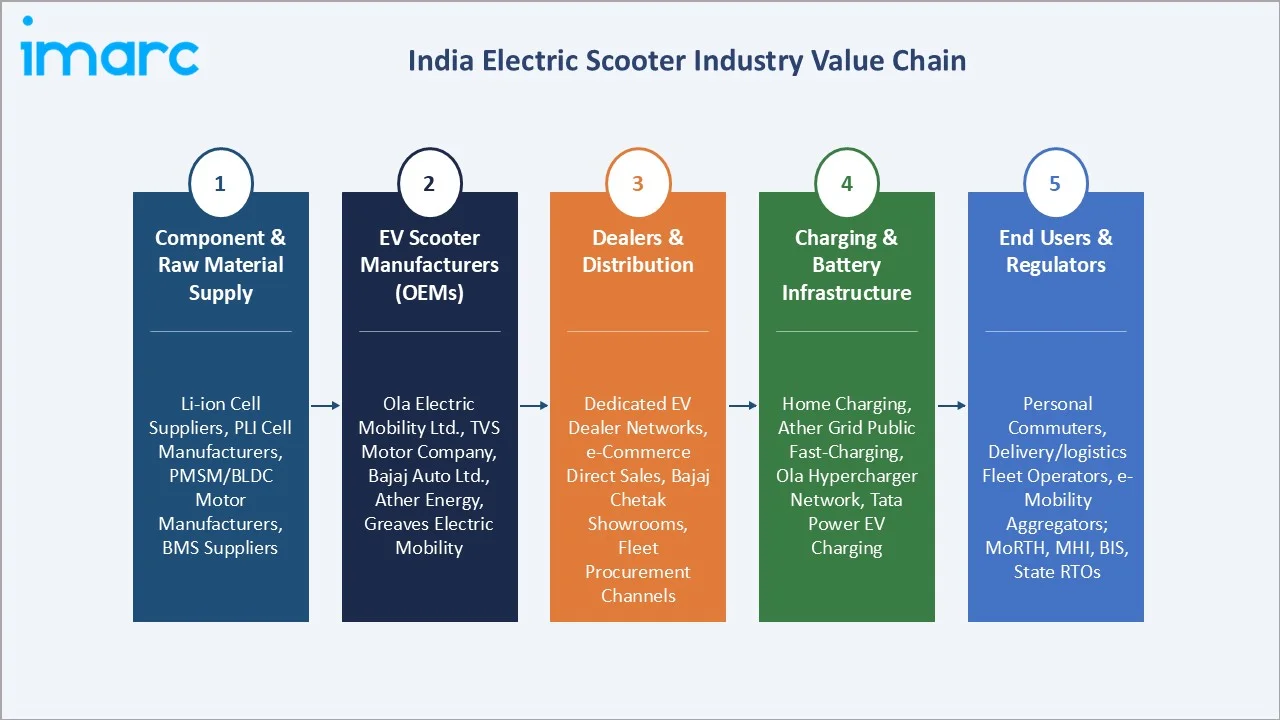

Industry Value Chain Analysis

India’s electric scooter value chain integrates Li-ion cell supply, battery pack assembly, motor and controller manufacturing, scooter assembly, dealer distribution, and end-user ownership, supported by charging infrastructure.

|

Stage |

Key Participants |

|

Component & Raw Material Supply |

Lithium-ion cell suppliers, Indian cell manufacturers under PLI, PMSM/BLDC motor manufacturers, Permanent magnet suppliers, Battery management system (BMS) suppliers |

|

EV Scooter Manufacturers (OEMs) |

Ola Electric Mobility Ltd., TVS Motor Company, Bajaj Auto Ltd., Ather Energy, and Greaves Electric Mobility Limited. |

|

Dealers & Distribution |

Dedicated EV dealer networks; e-commerce direct sales; Bajaj Chetak exclusive showrooms; traditional ICE dealer EV transition; fleet procurement channels |

|

Charging & Battery Infrastructure |

Home charging, Ather Grid public fast-charging network, Ola Hypercharger network, Tata Power EV charging |

|

End Users & Regulators |

Personal commuters, delivery/logistics fleet operators, e-mobility aggregators; MoRTH, MHI, BIS, State RTOs |

Battery pack constitutes 35‐45% of total EV scooter manufacturing cost, making it the dominant cost component and the primary focus of PLI investment. Motor and controller together represent 15‐20% of the cost, with an increasing domestic manufacturing share. Frame and body at 20‐25% leverage India’s established ICE scooter component supply chain, with domestic content already achieved.

Technology Landscape in the India Electric Scooter Industry

Battery Technology: From NMC to LFP Transition

India’s EV scooter battery chemistry is evolving from NMC (Nickel Manganese Cobalt, used by Ather and early Ola models) toward LFP (Lithium Iron Phosphate), driven by LFP’s inherently safer thermal profile and 20‐30% lower cell cost.

Motor Technology: PMSM Efficiency and Regenerative Braking

Permanent Magnet Synchronous Motors (PMSM) have become India’s standard high-performance EV scooter motor, replacing older BLDC (Brushless DC) motors in the premium segment.

Charging Technology: AC vs DC Fast Charging Evolution

India’s EV scooter charging ecosystem offers 3 levels: Level 1 standard 5A household socket, Level 2 dedicated 15A/3.3 kW wall box charger (2–4 hours), and Level 3 fast charging. The industry’s interoperability challenge is being addressed by BEE’s EV Charging Standard IS 17017-2, mandating a unified CCS2 connector for public fast chargers.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Drive | Hub Motors | 42.8% | 2025 |

| Battery | Lithium Ion | 86.5% | 2025 |

| Product | Standard | 72.5% | 2025 |

| Battery Fitting | Fixed | 76.0% | 2025 |

| End Use | Personal | 75.5% | 2025 |

| Region | South India | 32.5% | 2025 |

By Drive

Hub motors lead at 42.8% as the dominant drive system for India’s high-volume mass-market EV scooter segment. Hub motor’s key advantage, integration of motor, reduction gear, and brake drum within the wheel hub eliminating frame-mounted motor, chain/belt transmission, and associated maintenance, delivers the lowest total cost of ownership for India’s urban commuter.

To access detailed market analysis, Request Sample

Belt drive at 34.6% captures the aspirational premium segment where TVS, Bajaj, and Ather compete on performance, range, and brand prestige. Chain drive at 22.6% maintains presence in the budget segment and rural markets where chain drive’s field-repairable design (chain replacement available at any local mechanic) and lowest manufacturing cost extend market access to areas beyond OEM service network reach.

By Battery

Lithium-ion dominates at 86.5%, having displaced lead-acid through a combination of regulatory mandate (FAME II subsidy eligibility requiring Li-ion), consumer preference for 100+ km range that only Li-ion enables, and rapidly declining Li-ion pack prices. Lead acid at 10.8% persists in the ultra-budget EV scooter segment serving India’s most price-constrained consumers in Tier-3 cities, Tier-4 towns, and rural markets where a 40‐60 km range is sufficient for daily needs.

Others at 2.7% encompasses sodium-ion prototypes at the pilot stage, nickel-metal hydride (NiMH) in legacy models, and hybrid solid-state Li-ion in the R&D phase.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

South India |

32.5% |

Tamil Nadu hosts India’s densest EV manufacturing cluster, Ola Electric’s Future Factory, TVS Company (Hosur), Ather Energy (Hosur), and others, creating co-location advantages where proximity to manufacturing reduces logistics cost and enables rapid dealer network servicing |

|

North India |

26.4% |

Delhi NCR’s extreme air quality crisis is creating India’s most policy-driven EV push, driving the market in the region |

|

West India |

22.1% |

Maharashtra’s Maharashtra EV Policy 2021, India’s most financially generous state EV subsidy creating Mumbai and Pune’s outperforming EV adoption relative to the state population |

|

East India |

19.0% |

Kolkata’s historically high dependency on traditional cycle-rickshaws and e-rickshaws creating the foundation for electric 2-wheeler adoption normalisation, as electric mobility is already deeply embedded in everyday East India transport culture |

South India’s 32.5% leadership is both structural and self-reinforcing: Tamil Nadu and Karnataka’s manufacturing concentration creates a talent ecosystem that generates continuous product innovation disproportionately aligned with South India’s urban consumer preference for tech-forward premium EV scooters. Yulu's 22500 shared EVs have crossed 1 billion km in Bengaluru and its consumer base’s established technology adoption culture creates India’s richest test market for EV feature experimentation.

North India’s 26.4% is policy-amplified beyond its economic fundamentals. In Delhi, EV penetration has grown from under 3% in 2020 to nearly 14% in 2025, driving the market growth in the region. West India’s 22.1% with Maharashtra’s MEVP 2021 demonstrates that state-level financial incentives can accelerate adoption beyond what geography and income would predict.

Competitive Landscape

India’s electric scooter market exhibits high concentration among the top-3 manufacturers: Ola Electric, TVS Motor Company, and Bajaj Auto Chetak collectively commanding 58‐72% of India’s EV scooter market revenue by value.

|

Company Name |

Brand / Product Line |

Market Position |

Core Strength |

|

Ola Electric Mobility Ltd. |

Ola S1 Pro+ 3rd Gen, Ola S1 Pro 3rd Gen, Ola S1 X+ 3rd Gen |

Strong Challenger |

Bengaluru-headquartered Ola Electric operates India’s largest dedicated EV scooter manufacturing facility and Gigafactory |

|

TVS Motor Company |

iQube, iQube ST |

Market Leader |

Chennai-headquartered TVS Motor Company is India’s one of the largest 2-wheeler companies by volume, with iQube as its premium EV scooter platform |

|

Bajaj Auto Ltd. |

Chetak C2501, Chetak 3001, Chetak 3501, Chetak 3502, Chetak 3503 |

Market Leader |

Pune-headquartered Bajaj Auto launched the Chetak EV as a premium heritage-brand revival |

|

Ather Energy |

Ather 450X, Ather Rizta, Ather 450 Apex |

Strong Challenger |

Bengaluru-headquartered Ather Energy is India’s most technologically sophisticated premium EV scooter company |

|

Greaves Electric Mobility Limited |

Ampere Nexus, Ampere Magnus Grand, Ampere Reo 80, Ampere Magnus G Max, Ampere Magnus Neo |

Established |

Greaves Electric Mobility serves both consumer and fleet/commercial EV segments. |

Ather Energy at 10‐15% volume share with a premium price point delivers 15‐20% of total market revenue. This top-4 accounting for 75‐85% of industry revenue is unusually concentrated for an emerging technology market, reflecting Ola’s disruptive scale and TVS’s/Bajaj’s institutional dealer advantage over newer entrants.

Key Company Profiles

Ola Electric Mobility Ltd.

Ola Electric is prominent player in India electric scooter market with a high domestic volume share and the world’s most ambitious EV 2-wheeler manufacturing scale-up plan.

- Product Portfolio: Ola S1 Pro+ 3rd Gen, Ola S1 Pro 3rd Gen, Ola S1 X+ 3rd Gen.

- Recent Developments: In April 2026, Ola Electric launched its new S1 X+ electric scooter with a 5.2 kWh battery pack, priced at an introductory 1,29,999.

- Strategic Focus: Cell Technologies Gigafactory scaling to commercial production, creating an in-house Li-ion cell supply that eliminates import dependency and delivers cost advantage per scooter; MoveOS software platform as long-term revenue diversification through app subscriptions, fleet management SaaS, and OTA feature monetisation.

TVS Motor Company

TVS Motor Company is one of India’s largest 2-wheeler companies with iQube as its flagship EV scooter platform.

- Product Portfolio: iQube, iQube ST, iQube S, Orbiter V1, Orbiter V2

- Recent Developments: In March 2026, TVS Motor Company launched the Orbiter V1 electric scooter, pricing it from ₹49,999 under a new Battery-as-a-Service (BaaS) model.

- Strategic Focus: iQube ST performance leadership maintenance through torque vectoring and advanced motor control R&D; dealer network advantage monetization by expanding iQube to 500+ exclusive EV service centres by 2026 as tier-2 and tier-3 city service is TVS’s structural moat vs Ola and Ather.

Bajaj Auto Ltd.

Bajaj Auto Ltd. launched the Chetak EV as India’s earliest premium EV scooter from an established OEM, betting on the heritage equity of the original Chetak to command a premium positioning in India’s nascent EV market.

- Product Portfolio: Chetak C2501, Chetak 3001, Chetak 3502, Chetak 3503, Chetak 3501

- Recent Developments: In January 2026, Bajaj Auto launched its brand-new Chetak C25 electric scooter. The Bajaj Chetak C25 E-Scooter has a neo-tribe vibe, sleek design and a new look.

- Strategic Focus: Chetak C2501/C25 volume scaling to compete with Ola S1 X using Bajaj’s lower manufacturing cost base vs Ola’s greenfield overhead; subscription financing model expansion as a consumer acquisition channel for buyers unwilling to take ownership risk.

Market Concentration Analysis

India’s electric scooter market is highly concentrated with Ola Electric, TVS Motor Company, and Bajaj Auto Chetak controlling approximately 58–72% of total market volume in FY2025. Including Ather Energy creates a top-4 accounting for 75–85% of industry revenue by value, with Ather’s premium price point contributing 15‐20% of revenue from 10‐15% of volume.

This concentration is unusually high for an emerging technology market and stems from three structural factors: Ola Electric’s disruptive Gigafactory capacity enabling price points that smaller manufacturers cannot achieve; TVS and Bajaj’s established dealer network providing service reach that EV-only startups require years and capital to replicate; and FAME II/EMPS subsidy administration’s compliance complexity acting as an effective barrier that eliminated 15‐20 smaller EV manufacturers between 2022 and 2024 whose products failed certification or were found in subsidy fraud investigations.

Investment & Growth Opportunities

Fastest Growing Segments

Belt drive (~9.6% CAGR), lithium-ion battery (~9.8% CAGR), East India region (~10.5% CAGR), commercial/fleet EV segment (~15‐18% CAGR), and Li-ion cell manufacturing (~35‐40% CAGR from very small 2025 base as PLI investments scale) represent India’s electric scooter market’s highest-growth investment vectors.

Emerging Technology and Policy Opportunities

Domestic Li-ion cell manufacturing; battery swapping infrastructure; sodium-ion battery commercialisation; V2G (Vehicle-to-Grid) integration for smart grid demand response.

- Listed equity investment opportunities: Ola Electric Mobility Ltd., TVS Motor Company, Bajaj Auto Ltd., Greaves Electric Mobility.

- Private investment opportunities: Ather Energy Pvt. Ltd., Simple Energy Pvt. Ltd., River Mobility Pvt. Ltd.; Ola Cell Technologies.

Future Market Outlook (2026-2034)

The India electric scooter market is entering its most consequential growth phase. From USD 1.46 Billion in 2025, the market will reach USD 3.32 Billion by 2034, at a sustained 9.22% CAGR that reflects the systematic convergence of economic, policy, and technology forces that will make EV scooter ownership the rational default choice for India’s urban 2-wheeler buyer by 2030.

This growth trajectory is anchored by three incontrovertible structural drivers: India’s aspiring middle class is encountering the most favourable EV scooter economics in India’s history as PLI-funded domestic cell production progressively closes the upfront cost premium gap between EV and ICE scooters; India’s government has demonstrated across 6 years of FAME I, FAME II, and EMPS 2024 that EV scooter adoption is a priority that transcends electoral cycles and party politics, the subsidy commitment may shift from demand incentives toward manufacturing competitiveness support (PLI, production credits) but the directional policy commitment to EV 2-wheeler adoption is irreversible; and India’s 12 million gig economy delivery workers represent a captive commercial conversion market where Zomato’s, Swiggy’s, and BigBasket’s 100% EV fleet commitments by 2030 create a minimum high commercial EV scooter demand floor that provides market stability through retail demand cycles.

Research Methodology

Primary Research

Primary research included 110+ structured interviews with Indian electric scooter industry stakeholders in 2025, comprising OEM commercial and engineering directors, EV dealer operators across South India, North India, West India, and East India markets, fleet procurement managers at Zomato, Swiggy, and Shadowfax, battery technology specialists at ISRO LEOS and IIT Madras electrochemistry labs, FAME II and EMPS 2024 implementation officers at Ministry of Heavy Industries, and independent EV industry analysts.

Secondary Research

Secondary research encompassed VAHAN national vehicle registration database (FAME II EV registration data, state-wise EV penetration), SMEV (Society of Manufacturers of Electric Vehicles) monthly retail data, MHI FAME II disbursement reports, ARAI (Automotive Research Association of India) type approval database, BIS mandatory certification registry, annual reports of listed EV-related companies, IMARC automotive intelligence database, and state EV policy implementation reports. Over 120 secondary sources reviewed.

Forecasting Models

IMARC’s Bottom-Up and Top-Down dual estimation methodology was applied. Bottom-Up aggregates India electric scooter demand by drive type, battery type, and region, weighted by OEM production capacity expansion schedules, battery cost learning curve projections, government incentive continuation probability, and petrol price trajectory modeling. Top-Down validates against India’s overall two-wheeler market volume, EV penetration trajectory from peer market benchmarks, and manufacturer-disclosed capacity and sales guidance.

India Electric Scooter Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Drives Covered | Belt Drive, Chain Drive, Hub Motors |

| Batteries Covered | Lead Acid, Lithium Ion, Others |

| Products Covered | Standard, Folding, Self-Balancing, Maxi, Three Wheeled |

| Battery Fittings Covered | Detachable, Fixed |

| End Uses Covered | Personal, Commercial |

| Regions Covered | North India, South India, East India, West India |

| Companies Covered | Ola Electric Mobility Ltd., TVS Motor Company, Bajaj Auto Ltd., Ather Energy, Greaves Electric Mobility Limited, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Electric Scooter Market Report

The India electric scooter market was valued at USD 1.46 Billion in 2025 and is projected to reach USD 3.32 Billion by 2034.

The India electric scooter market is forecast to grow at a CAGR of 9.22% during 2026-2034, driven by FAME II/EMPS subsidy economics, rising petrol prices, PLI domestic battery manufacturing, and expanding charging infrastructure.

Hub Motors lead with 42.8% revenue share (2025), driven by hub motor’s lower manufacturing cost enabling competitive pricing at the mass-market segment where Ola S1 X and Ampere lead volume.

Lithium-ion dominates with 86.5% share (2025), enabled by FAME II Li-ion eligibility requirement, 2–3× higher energy density enabling 100+ km range, and declining import prices.

South India leads with 32.5% revenue share (2025), anchored by Tamil Nadu and Karnataka’s EV manufacturing cluster hosting Ola Electric, Ather Energy, TVS Motor, and Ampere Vehicles.

Key companies include Ola Electric Mobility Ltd., TVS Motor Company, Bajaj Auto Ltd., Ather Energy, and Greaves Electric Mobility Limited.

Key drivers include FAME II/EMPS 2024 subsidies reducing purchase cost, creating high annual EV running cost savings, PLI Scheme domestic cell manufacturing scaling, expanding Ather Grid/Ola Hypercharger charging networks, and gig economy commercial fleet conversion.

Key trends include Ola Cell Technologies’ 4680 Gigafactory cell production, software-defined MoveOS/AtherStack connected platforms, battery swapping, Belt drive premium segment growth, women consumers as fastest-growing buyer segment, and commercial fleet EV conversion.

Key challenges include range anxiety and limited charging in Tier-2/3 cities, upfront premium vs ICE scooters, battery fire incident consumer safety concern, EV subsidy policy uncertainty (FAME II fraud crisis, EMPS transition disruptions), and NBFC EV loan interest rates at 12‐15% vs 8‐10% for ICE models.

Top opportunities include PLI Li-ion cell manufacturing, battery swapping infrastructure, Ather Energy pre-IPO, commercial fleet EV scooters, sodium-ion battery R&D, V2G grid integration services, and EV scooter export to Southeast Asia and Africa markets.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)