India Electric Two-Wheeler Market Size, Share, Trends and Forecast by Vehicle Type, Battery Type, Voltage Type, Peak Power, Battery Technology, Motor Replacement, and Region, 2026-2034

India Electric Two-Wheeler Market Size, Share, Trends & Forecast (2026-2034)

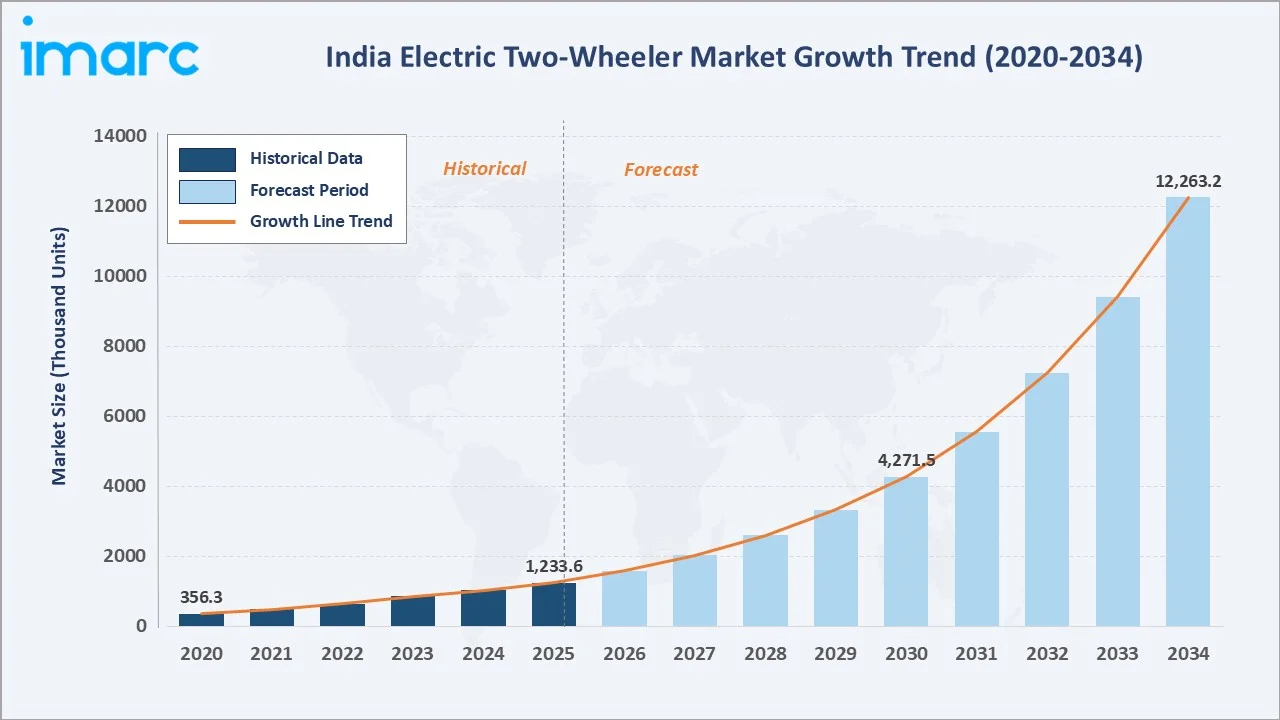

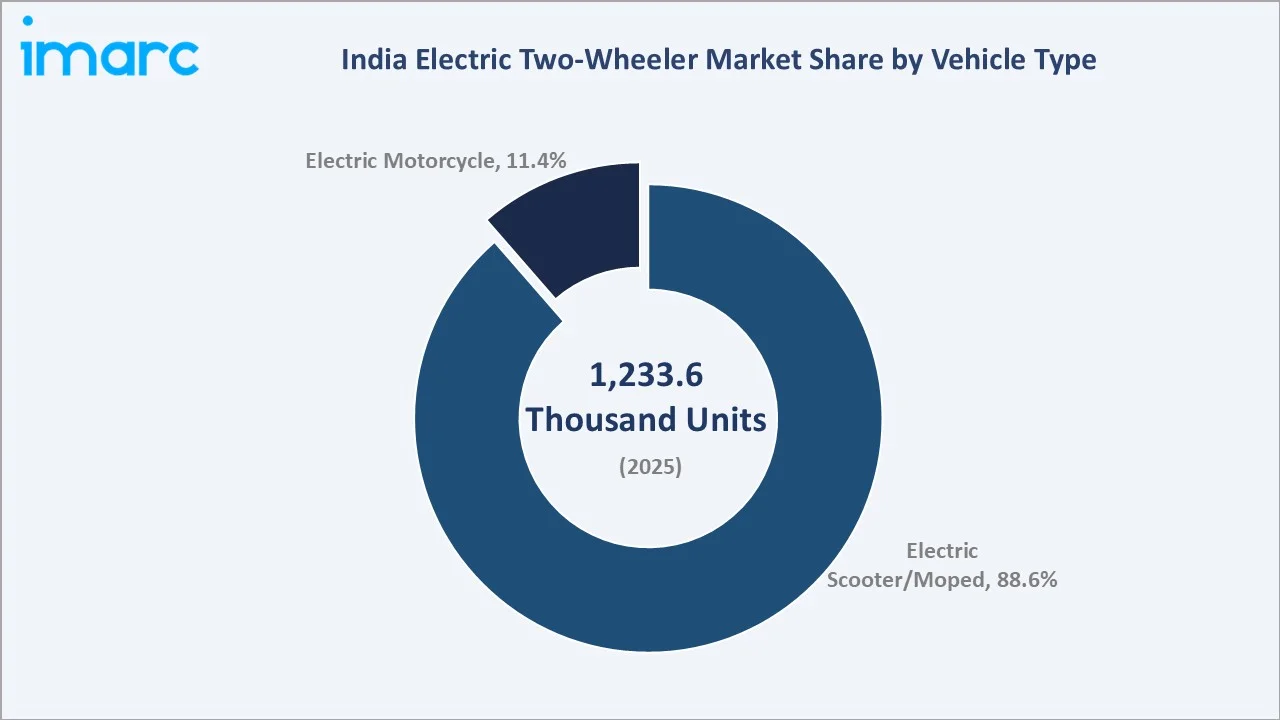

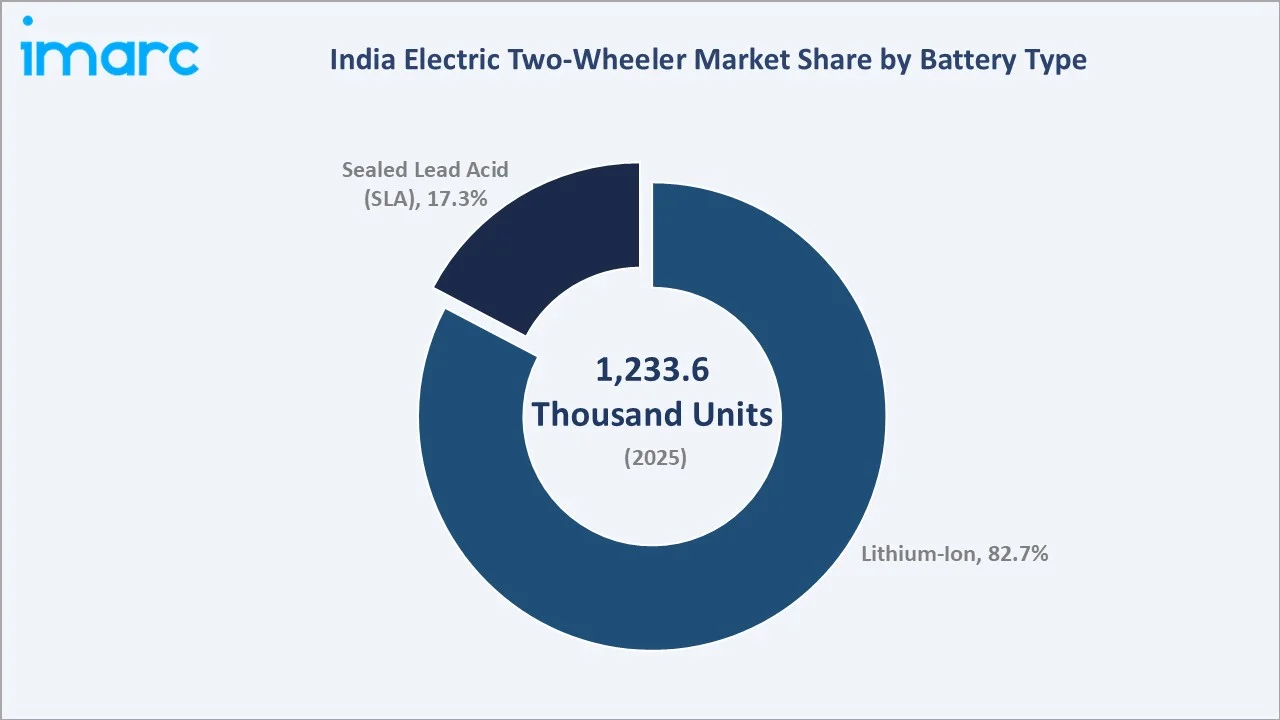

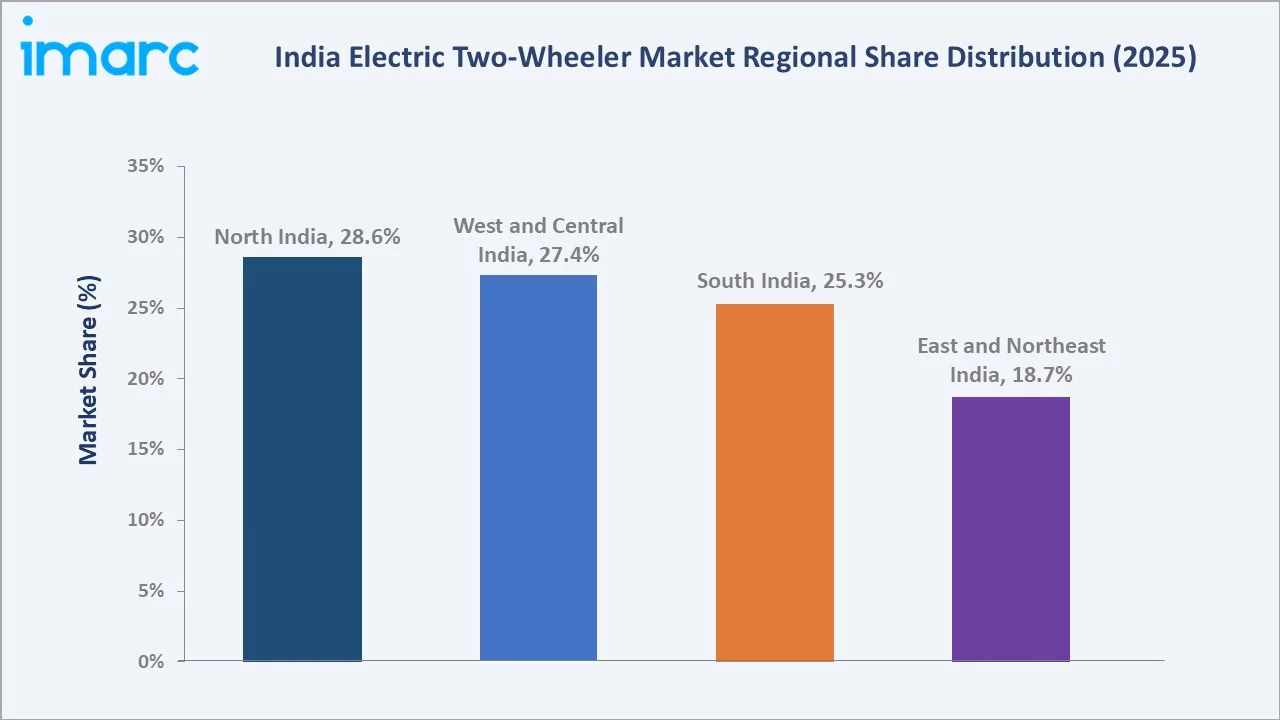

The India electric two-wheeler market size reached 1,233.6 Thousand Units in 2025 and is projected to touch 12,263.2 Thousand Units by 2034, exhibiting a CAGR of 28.20% during the forecast period 2026-2034. Rising fuel costs, expanding FAME-II and state-level subsidies, rapid lithium-ion battery localization, and growing urban pollution concerns are accelerating the India electric two-wheeler market growth. Electric scooters and mopeds dominate with 88.6% share in 2025, while lithium-ion batteries account for 82.7% of total demand. North India leads the country with 28.6% revenue share in 2025, followed closely by West and Central India at 27.4%.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

1,233.6 Thousand Units |

|

Forecast Market Size (2034) |

12,263.2 Thousand Units |

|

CAGR (2026-2034) |

28.20% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

North India (28.6% share, 2025) |

|

Fastest Growing Region |

South India (~30% CAGR) |

|

Leading Vehicle Type |

Electric Scooter/Moped (88.6%, 2025) |

|

Leading Battery Type |

Lithium-Ion (82.7%, 2025) |

The India electric two-wheeler market trajectory from 2020 through 2034 highlights a sharp acceleration phase, with volumes expanding nearly tenfold over the forecast horizon. Government incentives, falling battery prices, and urban mobility electrification are jointly powering this growth curve.

To get more information on this market, Request Sample

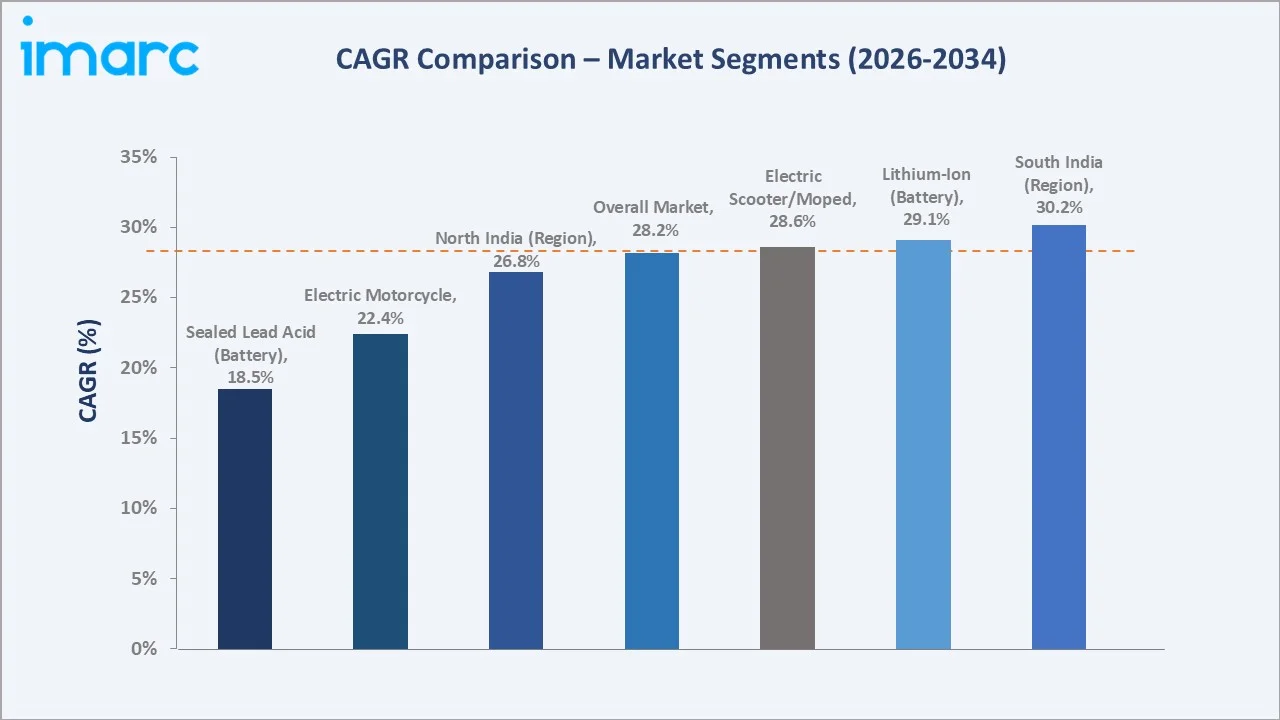

Segment-level CAGR analysis reveals that lithium-ion batteries, electric scooters, and South India are the fastest accelerating sub-segments. Each is positioned to outpace the overall market average through 2034.

Executive Summary

The India electric two-wheeler market is undergoing a structural transformation, shifting from an early-adopter niche to a mainstream urban mobility category. Valued at 1,233.6 Thousand Units in 2025, the market is forecast to reach 12,263.2 Thousand Units by 2034 at a CAGR of 28.20%. Falling lithium-ion cell prices, FAME-II disbursements, and state-level demand incentives are anchoring this expansion.

Electric scooters and mopeds command 88.6% share in 2025, driven by their suitability for short urban commutes and lower price points compared with motorcycles. The electric motorcycle segment, holding 11.4%, is gaining traction in performance and inter-city use cases. Lithium-ion batteries dominate at 82.7% share in 2025, while sealed lead acid retains 17.3% in entry-level rural and low-speed segments.

North India leads with 28.6% revenue share in 2025, propelled by Delhi-NCR demand and state EV policies in Uttar Pradesh and Punjab. West and Central India follows at 27.4%, anchored by Maharashtra and Gujarat. The India electric two-wheeler market outlook stays robust as charging infrastructure, swappable battery networks, and OEM model expansion converge through 2034.

Key Market Insights

|

Insight |

Data |

|

Largest Vehicle Type |

Electric Scooter/Moped – 88.6% share (2025) |

|

Second Vehicle Type |

Electric Motorcycle – 11.4% share (2025) |

|

Largest Battery Type |

Lithium-Ion – 82.7% share (2025) |

|

Second Battery Type |

Sealed Lead Acid (SLA) – 17.3% share (2025) |

|

Leading Region |

North India – 28.6% revenue share (2025) |

|

Top Companies |

TVS Motor Company, Bajaj Auto Ltd, Hero MotoCorp Ltd, Ather Energy, Ola Electric Mobility Ltd. |

|

Forecast Volume (2034) |

12.26 Million Units |

Key Analytical Observations Supporting the Above Data:

- Electric Scooter/Moped's 88.6% dominance in 2025 reflects the segment's price advantage, with most models priced between INR 80,000 and INR 1,50,000, and its alignment with last-mile and short-commute use cases across Tier-1 and Tier-2 cities.

- Electric Motorcycles' 11.4% share is rising as performance brands such as Ultraviolette F77 and Revolt RV400 expand their dealership footprint, supported by growing acceptance of higher peak-power configurations above 7 kW.

- Lithium-Ion's 82.7% majority in 2025 is underpinned by improving cycle life, declining cell costs (down nearly 14% year-over-year in 2024), and PLI scheme support for Advanced Chemistry Cell (ACC) manufacturing within India.

- North India's 28.6% lead is driven by Delhi’s draft EV Policy 2.0 introduces a strong push toward clean mobility, offering full road tax and registration fee exemptions for electric vehicles priced up to ₹30 lakh, Uttar Pradesh's per-vehicle subsidy, and last-mile delivery fleet electrification are also some other drivers for North Region.

- India's overall E2W penetration in total two-wheeler sales reached approximately 6.3% in 2025, the rapid mainstreaming of battery-electric drivetrains.

- Forecast trajectory projects nearly 10X volume growth through 2034, with 2030 acting as an inflection point at 4,271 Thousand Units, after which scale economics, swappable batteries, and PLI-led local cell capacity unlock the steepest expansion phase.

India Electric Two-Wheeler Market Overview

Electric two-wheelers are battery-powered scooters, mopeds, and motorcycles designed for personal mobility, short commutes, and last-mile commercial use. The Indian market spans entry-level low-speed scooters (under 25 km/h, license-exempt) to high-speed scooters and performance motorcycles equipped with lithium-ion batteries, smart connectivity, and regenerative braking.

The industry operates at the intersection of automotive, energy storage, and digital mobility. Growth is anchored by macroeconomic factors such as petrol price volatility (INR 95-105/litre in 2025), urbanization, last-mile delivery e-commerce, and government policy thrust through FAME-II, state-level subsidies, GST reduction (from 12% to 5%), and PLI schemes for ACC battery manufacturing.

Market Dynamics

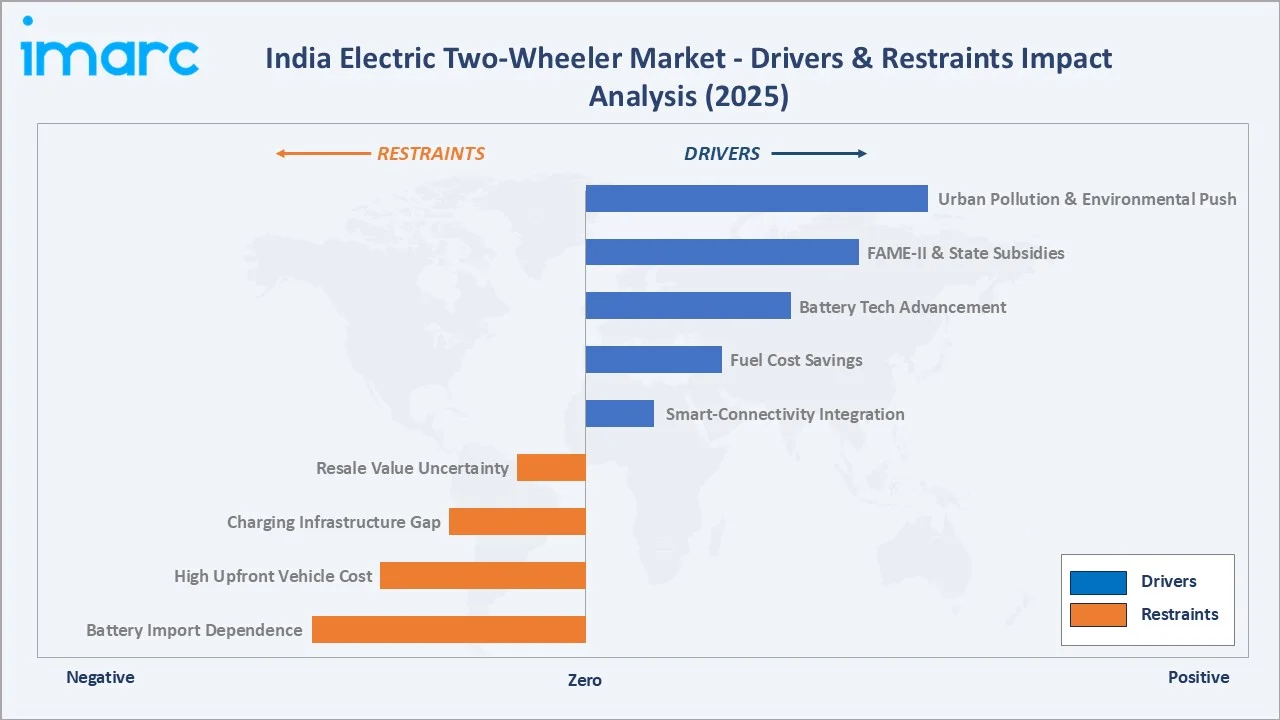

The India electric two-wheeler market is shaped by a balanced interplay of accelerators and headwinds. Drivers include policy incentives, fuel cost arbitrage, and rapid technology localization, while restraints stem from charging infrastructure gaps and battery import dependence.

To evaluate market opportunities, Request Sample

Market Drivers

- FAME-II and State EV Subsidies: The Government of India's FAME-II scheme, with an outlay of INR 10,000 crore, has supported over 16 lakh electric two-wheelers through 2025. State policies in Maharashtra, Delhi, Gujarat, and Tamil Nadu offer additional per-kWh demand incentives ranging from INR 5,000 to INR 15,000, materially lowering on-road prices for buyers.

- Fuel Cost Savings and TCO Advantage: With petrol priced near INR 100/litre in 2025 and electricity cost equivalents of approximately INR 0.20-0.30/km, electric scooters deliver running cost savings of 70-80% versus conventional ICE counterparts. The total cost of ownership crossover has now compressed to approximately 18-22 months for typical urban commuters.

- Battery Technology Advancement: Lithium-ion cell costs in India have fallen to approximately USD 115/kWh in 2025, down from over USD 160/kWh in 2021. Improved energy density (above 200 Wh/kg in latest packs) and 1,500-2,000 cycle life are extending real-world ranges to 100-160 km per charge in mainstream electric scooters.

- Urban Pollution and Sustainability Push: Air quality concerns in Delhi-NCR, Mumbai, Bengaluru, and Kolkata are driving city-led EV adoption mandates. Electric mobility is emerging as a critical solution to India’s pollution challenge, with the transport sector contributing nearly one-third of urban air pollution. EV adoption is accelerating, supported by government programs such as the FAME scheme, which has an outlay of ₹10,000 crore, alongside production-linked incentives to boost domestic manufacturing.

Market Restraints

- Charging Infrastructure Gap: Public charging stations in India totaled approximately 26,000 as of mid-2025, against an estimated need of 4-5 lakh by 2030. Range anxiety remains a key barrier for tier-2/3 city consumers and inter-city motorcycle use.

- High Upfront Vehicle Cost: Despite subsidies, electric scooters typically carry a 25-40% premium over comparable ICE models, restricting affordability for price-sensitive buyers in semi-urban and rural India.

- Battery Import Dependence: India still imports over 70% of lithium-ion cells, primarily from China and South Korea. Currency volatility and cell pricing cycles directly impact OEM margins and end-consumer pricing.

Market Opportunities

- Battery-Swap Networks for Commercial Fleets: Battery swapping networks led by Battery Smart and SUN Mobility have scaled significantly across India, primarily catering to electric two- and three-wheelers. The model is increasingly being adopted in last-mile delivery and shared mobility, where minimizing downtime and improving vehicle utilization are critical.

- Tier-2 and Tier-3 City Expansion: Emerging urban centers such as Lucknow, Indore, Jaipur, Coimbatore, and Bhubaneswar are witnessing strong acceleration in electric vehicle adoption, with significantly higher year-on-year growth compared to traditional metro markets. This trend reflects rising demand in Tier II and III cities, supported by improving charging infrastructure, affordability of EV models, and increasing use in commercial mobility segments.

- PLI Scheme for ACC Manufacturing: The Production Linked Incentive scheme of INR 18,100 crore for advanced chemistry cells is enabling Reliance, Ola, Rajesh Exports, and Hyundai to set up gigafactories targeting 50 GWh of cumulative capacity by 2030.

Market Challenges

- Subsidy Phase-Out Risk: FAME-II demand incentives are phasing down, with the scheme set to be replaced by the Electric Mobility Promotion Scheme (EMPS) and PM E-DRIVE. Transition periods can compress OEM volumes if policy bridges are delayed.

- Fire Safety and Quality Compliance: Battery thermal runaway incidents in 2022-2023 prompted AIS-156 amendments. Continued compliance with strict cell-pack-vehicle testing protocols raises certification costs for smaller manufacturers.

- Resale Value Uncertainty: Used electric two-wheeler resale markets remain underdeveloped, with buyers concerned about residual battery health. This depresses trade-in value and lengthens consumer purchase deliberation periods.

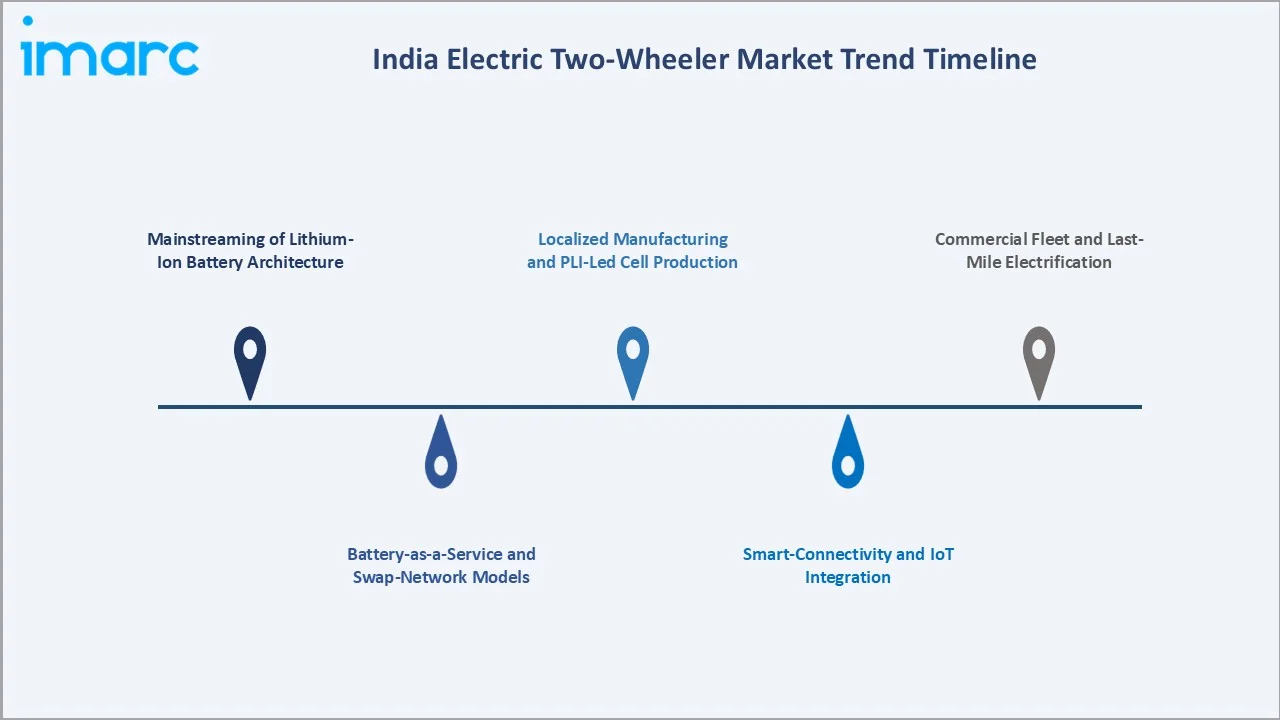

Emerging Market Trends

The Indian electric two-wheeler landscape is being reshaped by five powerful trends that span product, infrastructure, and business model innovation.

1. Mainstreaming of Lithium-Ion Battery Architecture

Lithium-ion batteries account for the majority of electric two-wheeler sales in India, driven by their higher energy density, longer lifecycle, and growing adoption in high-speed scooters. While low-cost lead-acid variants still exist in entry-level segments, the market is rapidly transitioning toward lithium-ion as the dominant battery technology. LFP (lithium iron phosphate) chemistry is gaining preference over NMC for its superior thermal safety, longer cycle life of 2,000+ cycles, and price competitiveness.

2. Battery-as-a-Service and Swap-Network Models

Battery-swapping networks are separating battery ownership from the vehicle, significantly reducing upfront purchase costs for consumers. Companies such as SUN Mobility, Battery Smart, Bounce Infinity, and Honda are expanding their presence across multiple cities, supporting the growth of electric mobility through scalable swapping infrastructure.

3. Smart-Connectivity and IoT Integration

Mainstream models from Ola, Ather, TVS iQube, and Bajaj Chetak now offer in-built 4G connectivity, smartphone pairing, GPS tracking, and OTA software updates. The shift mirrors smartphone-style product cycles, with annual feature releases driving repeat consumer engagement.

4. Localized Manufacturing and PLI-Led Cell Production

Under the PLI scheme, Reliance New Energy, Ola Electric, and Rajesh Exports are building gigafactories targeting 50+ GWh capacity by 2030. Battery localization is expected to deliver meaningful cost reductions and reduce reliance on imported cells, particularly from China, over the next few years, although estimates vary across sources.

5. Commercial Fleet and Last-Mile Electrification

Quick-commerce and food delivery operators including Zomato, Swiggy, Zepto, and Blinkit are deploying electric scooters at scale. Commercial fleet adoption is forecast to grow at 35-40% CAGR through 2030, driven by fleet TCO advantages and ESG mandates.

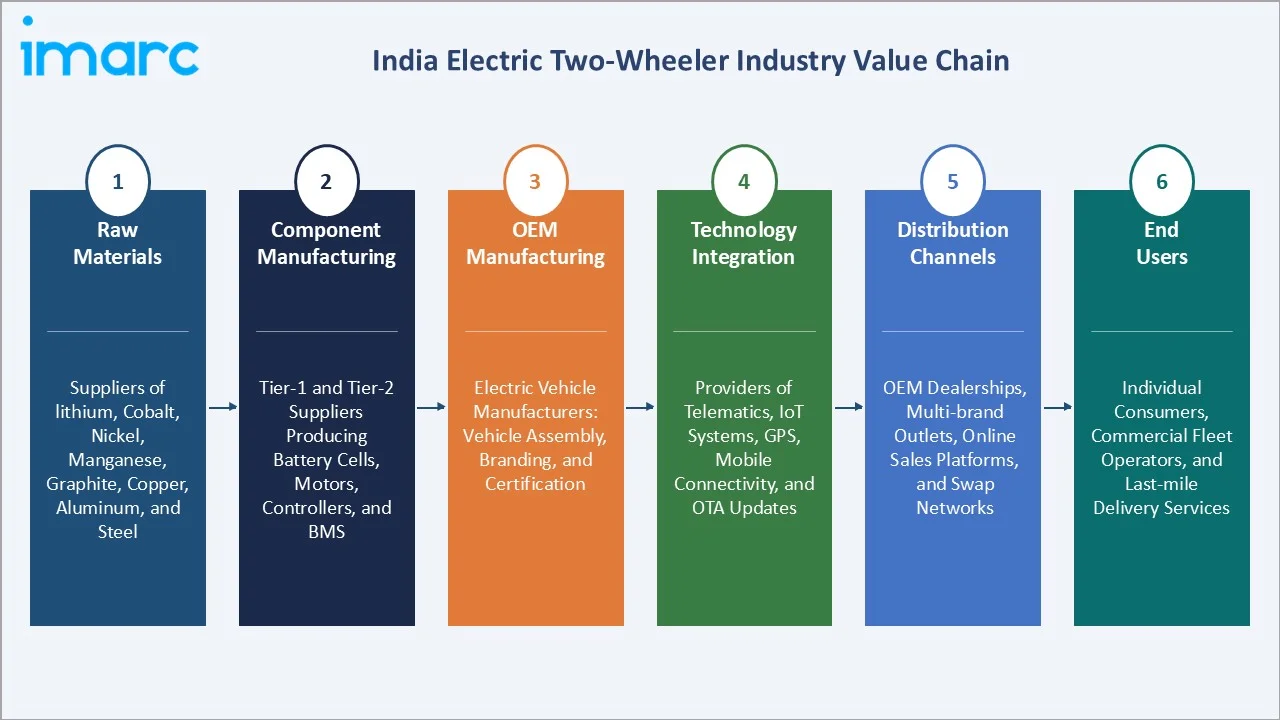

Industry Value Chain Analysis

The India electric two-wheeler value chain spans six integrated stages from raw materials through end-consumer delivery. Each stage carries distinct margin dynamics and strategic importance, with OEMs and battery cell manufacturers capturing the majority of long-term value.

|

Value Chain Stage |

Key Participants / Description |

|

Raw Materials |

Suppliers of lithium, cobalt, nickel, manganese, graphite, copper, aluminum, and steel, with a significant share sourced through imports from global mining hubs |

|

Component Manufacturing |

Tier-1 and Tier-2 suppliers producing battery cells, motors, controllers, battery management systems (BMS), and charging components, supported by both domestic manufacturing and imports |

|

OEM Manufacturing |

Electric vehicle manufacturers responsible for vehicle assembly, branding, certification, and market positioning |

|

Technology Integration |

Providers of telematics, IoT systems, GPS, mobile connectivity, over-the-air updates, and data analytics platforms integrated into vehicles |

|

Distribution Channels |

OEM-exclusive dealerships, multi-brand retail outlets, online sales platforms, and battery-swapping or charging network touchpoints |

|

End Users |

Individual consumers, commercial fleet operators, last-mile delivery services, shared mobility platforms, and government or institutional buyers |

OEMs and battery cell manufacturers retain the largest value share, while distribution and technology integrators are emerging as high-growth tiers. Battery-swap operators, in particular, are creating an entirely new monetization layer by separating battery ownership from vehicle ownership.

Technology Landscape in the India Electric Two-Wheeler Industry

Battery Technology

Lithium-ion battery packs dominate the Indian market in 2025, with LFP and NMC being the two principal chemistries. Energy densities have reached 180-220 Wh/kg, supporting practical ranges of 100-160 km on a full charge. Cell-to-pack design and modular swappable architectures are emerging as the next innovation frontier.

Materials Innovation

Advanced cell chemistries including LFP, sodium-ion (in pilot phase), and silicon-anode lithium-ion are entering the Indian R&D pipeline. PLI-supported gigafactories will localize advanced chemistry cell production by 2027, reducing import dependency from over 70% in 2025 to under 50% by 2028.

Smart Connectivity and IoT

Connected features such as GPS navigation, geofencing, ride analytics, anti-theft alerts, and over-the-air software updates are now widely integrated into mid- to premium electric scooters. These capabilities, enabled through advanced software platforms and smartphone connectivity, are increasingly standard in higher-priced models, enhancing both user experience and vehicle security.

Automation and Charging Infrastructure

Fast-charging compatibility (DC chargers reducing 0-80% charge time to 50-60 minutes) and AI-driven battery management systems are advancing rapidly. Battery-swap automation, with stations capable of completing full swaps within 90 seconds, is enabling continuous fleet operations for delivery and ride-hailing players.

Market Segmentation Analysis

IMARC Group provides analysis of key trends in each segment of the India electric two-wheeler market, with forecasts at country and regional levels from 2026 to 2034. Per the data inputs, this section focuses on vehicle type and battery type segments.

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Vehicle Type | Electric Scooter/Moped | 88.6% | 2025 |

| Battery Type | Lithium-Ion | 82.7% | 2025 |

| Voltage Type | 🔒 | 🔒 | 2025 |

| Peak Power | 🔒 | 🔒 | 2025 |

| Battery Technology | 🔒 | 🔒 | 2025 |

| Motor Replacement | 🔒 | 🔒 | 2025 |

| Region | North India | 28.6% | 2025 |

By Vehicle Type

Electric scooters and mopeds dominate India’s electric two-wheeler market, accounting for the overwhelming majority of sales and significantly outpacing electric motorcycles. Demand is propelled by short urban commute use cases, lower upfront prices ranging between INR 80,000 and INR 1,50,000, and broad model availability from Ola, TVS, Bajaj, Hero, Ather, and Ampere. License-exempt low-speed scooters (under 25 km/h) account for a sizeable entry-level base, while high-speed scooters with 70-100 km/h top speeds dominate urban premium segments.

To access detailed market analysis, Request Sample

Electric Motorcycles account for 11.4% of vehicle type demand in 2025. The segment is driven by performance-focused models such as Ultraviolette F77, Revolt RV400, and Tork Kratos, targeting urban enthusiasts and inter-city commuters. Average selling prices in the motorcycle segment fall between INR 1,50,000 and INR 4,50,000, supporting higher per-unit margins for OEMs and dealers alike.

By Battery Type

Lithium-ion is the dominant battery type at 82.7% of 2025 market share. Adoption is propelled by improving energy density, falling cell costs (USD 115/kWh in 2025), longer cycle life of 1,500-2,000 cycles, and FAME-II eligibility criteria favoring lithium-based packs. LFP chemistry is gaining preference for its thermal safety and price advantage, while NMC continues in higher-performance configurations.

Sealed Lead Acid (SLA) batteries hold 17.3% of the 2025 market, primarily in entry-level low-speed scooters and price-sensitive rural segments. SLA's lower upfront cost (USD 60-70/kWh) sustains its niche, though declining lithium-ion prices and shorter SLA cycle life of 300-500 cycles are gradually compressing this segment's share through the forecast period.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

North India |

28.6% |

Delhi EV Policy, UP per-vehicle subsidy, last-mile delivery boom, NCR pollution mandates |

|

West and Central India |

27.4% |

Maharashtra EV Policy 2021, Gujarat industrial cluster, Mumbai-Pune commercial fleet electrification |

|

South India |

25.3% |

Karnataka EV Policy, Tamil Nadu manufacturing hub (Hosur), Hyderabad smart city, Kerala fleet adoption |

|

East and Northeast India |

18.7% |

West Bengal e-rickshaw ecosystem cross-pull, Odisha EV Policy 2021, Assam state-level subsidies |

North India commands 28.6% share in 2025, anchored by Delhi-NCR, Uttar Pradesh, Haryana, and Punjab. Delhi's EV Policy targets 25% of all new vehicle registrations to be electric by 2024, and Uttar Pradesh's per-vehicle subsidy of up to INR 5,000 has driven sharp uptake. The region also benefits from being the largest e-commerce delivery cluster, with quick-commerce companies aggressively electrifying rider fleets.

West and Central India holds 27.4%, led by Maharashtra and Gujarat. Maharashtra's EV Policy 2021 targets 10% of all new registrations to be electric, while Gujarat hosts major OEM clusters including Hero MotoCorp, TVS, and component suppliers. Pune and Mumbai are leading metro EV adopters, with over 90,000 registrations recorded in FY 2024-25.

South India accounts for 25.3%, driven by Karnataka, Tamil Nadu, Telangana, Andhra Pradesh, and Kerala. Karnataka was the first Indian state to launch an EV policy in 2017, and Tamil Nadu is the country's largest two-wheeler manufacturing hub, hosting TVS, Royal Enfield, and Ola's Futurefactory in Hosur. East and Northeast India represents 18.7%, with West Bengal, Odisha, Bihar, Assam, and Jharkhand showing accelerating EV uptake. Odisha's EV Policy 2021 and Assam's per-kWh subsidies are anchoring growth.

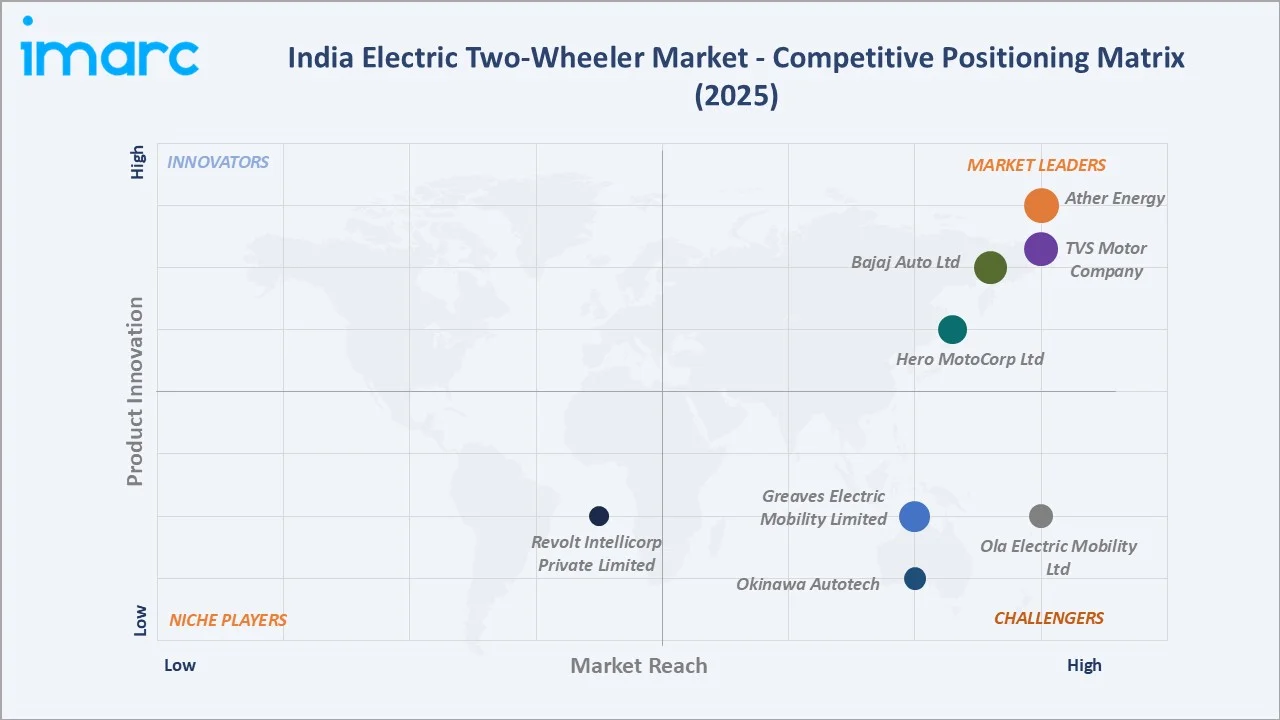

Competitive Landscape

|

Company Name |

Key Brand / Platform |

Market Position |

Core Strength |

|

TVS Motor Company |

TVS iQube, TVS X, Orbiter |

Leader |

Legacy distribution, dealership depth, R&D capability |

|

Bajaj Auto Ltd |

Bajaj Chetak |

Leader |

Premium positioning, design heritage, Pune-Aurangabad manufacturing |

|

Hero MotoCorp Ltd |

Hero Vida V1, Vida V2 |

Leader |

Largest 2W distribution network, Halol facility, brand trust |

|

Ather Energy |

Ather 450, 450S, Rizta |

Leader |

Premium tech, FastCharge network, Bengaluru-led innovation |

|

Ola Electric Mobility Ltd |

Ola S1 Pro, S1 Air, S1 X |

Challenger |

Vertically integrated, Futurefactory scale, direct-to-consumer model |

|

Greaves Electric Mobility Limited |

Ampere |

Challenger |

Affordable mass-market focus, rural retail penetration |

|

Okinawa Autotech |

Okinawa Praise, Ridge+ |

Challenger |

North India volumes, multi-segment model portfolio |

|

Revolt Intellicorp Private Limited |

Revolt RV400, RV1+ |

Emerging |

Electric motorcycle specialist, AI-powered features |

The India electric two-wheeler competitive landscape is moderately fragmented, with OEMs competing on platform innovation, dealership expansion, after-sales service, battery warranty terms, and price positioning. Strategic moves include Ola's IPO in August 2024 (valuing the company at over USD 4 billion), TVS' partnership with BMW Motorrad, and Bajaj's continued Chetak expansion across India.

Key Company Profiles

Ola Electric Mobility

Ola Electric Mobility is India's leading electric two-wheeler manufacturer, headquartered in Bengaluru, Karnataka. Founded in 2017 and listed on Indian stock exchanges in August 2024, Ola operates one of the world's largest electric two-wheeler factories, the Futurefactory in Krishnagiri, Tamil Nadu.

- Product & Platform Portfolio: Ola's portfolio includes the S1 Pro, S1 Air, and S1 X family of electric scooters, alongside the upcoming Roadster motorcycle series. The company is also vertically integrating with in-house battery cell manufacturing.

- Recent Developments: In 2026, Ola Electric has advanced its vertical integration strategy with the development of its in-house lithium iron phosphate battery cell, which is set to be integrated into its vehicles from the next quarter. The company’s gigafactory in Krishnagiri is simultaneously scaling up production capacity, reflecting its focus on building a full-stack EV and energy ecosystem while improving cost efficiency and accelerating adoption.

- Strategic Focus: Ola is pursuing vertical integration across cells, motors, and software, alongside expansion of its Roadster motorcycle line and store network beyond 1,000 outlets across India.

TVS Motor Company

TVS Motor Company, headquartered in Chennai, Tamil Nadu, is one of India's largest two-wheeler manufacturers and a leader in the electric scooter segment. Founded in 1978, TVS exports to over 80 countries and has a strong R&D base in Hosur.

- Product & Platform Portfolio: TVS' electric portfolio includes the iQube series (iQube, iQube S, iQube ST) and the upcoming TVS X premium electric scooter, complemented by the company's broader ICE two-wheeler range.

- Recent Developments: In April 2026, Hyundai Motor Company and TVS Motor Company have entered into a joint development agreement to co-develop and commercialize electric three-wheelers tailored for India’s last-mile mobility needs. The partnership combines Hyundai’s global design and R&D capabilities with TVS Motor’s expertise in electric platforms, manufacturing, and local market understanding to deliver scalable and sustainable mobility solutions.

- Strategic Focus: TVS is leveraging its dealership depth across 100,000+ touchpoints, partnering with BMW Motorrad on electric two-wheelers, and scaling iQube as a flagship platform.

Bajaj Auto Limited

Bajaj Auto Limited, headquartered in Pune, Maharashtra, is among India's most iconic two-wheeler manufacturers. Founded in 1945, Bajaj operates manufacturing facilities in Aurangabad, Pune, and Pantnagar, and exports to over 70 countries globally.

- Product & Platform Portfolio: Bajaj's electric flagship is the Bajaj Chetak electric scooter, available in Premium, Urbane, and Tecpac variants. The portfolio is expected to expand into electric motorcycles and three-wheelers.

- Recent Developments: In 2026, Bajaj Auto is evaluating the establishment of a new manufacturing facility outside Maharashtra to scale up production of its Chetak electric scooter. The company is exploring options such as expanding its Pantnagar plant in Uttarakhand or setting up a greenfield unit in southern India, as it looks to support growing EV demand and diversify its production footprint.

- Strategic Focus: Bajaj is positioning Chetak as a premium aspirational electric scooter, leveraging design heritage, KTM/Triumph synergies, and an expanding sub-INR 1 lakh entry variant for mass-market reach.

Market Concentration Analysis

The India electric two-wheeler market exhibits moderate concentration. The top five players - TVS Motor Company, Bajaj Auto Ltd, Hero MotoCorp Ltd, Ather Energy, Ola Electric Mobility Ltd - collectively accounted for approximately 78-82% of registered electric two-wheeler volumes in 2025. The remaining share is distributed across Ampere, Hero Electric, Okinawa, Revolt, Pure EV, and a long tail of regional players.

The market is going through a clear consolidation phase. Sub-scale players are losing share as compliance, R&D, and dealership investment requirements rise. Simultaneously, established legacy two-wheeler OEMs (TVS, Bajaj, Hero) are leveraging existing distribution moats to gain rapidly on early movers. This dual dynamic is intensifying competition through 2034, with smaller brands likely to either consolidate, exit, or be acquired.

Investment & Growth Opportunities

Fastest-Growing Segments

Electric scooters remain the highest-volume growth segment, projected to expand at approximately 28.6% CAGR through 2034. Electric motorcycles, while smaller in absolute terms, are scaling at a faster pace as performance brands capture urban premium and inter-city commuter segments. Lithium-ion battery-powered models are projected to expand share to over 95% by 2030.

Emerging Market Expansion

Tier-2 and Tier-3 cities including Lucknow, Indore, Coimbatore, Jaipur, Bhubaneswar, and Visakhapatnam are showing 35-50% year-on-year EV adoption growth. Rural India represents a longer-term opportunity as low-speed, license-exempt scooters priced under INR 1 lakh gain traction. Last-mile delivery, ride-hailing, and shared mobility fleets jointly represent over 1.5 lakh annual unit demand by 2028.

Venture and Strategic Investment Trends

India’s electric vehicle ecosystem is witnessing strong capital inflows, with automakers alone investing around US$ 10 billion in 2025 toward EVs, batteries, and manufacturing. In parallel, the auto component industry is expected to see US$ 2.9–3.5 billion in investments in FY26, following US$ 1.7–2.3 billion in FY25, reflecting accelerating capacity expansion across the EV value chain. Ola Electric's IPO (August 2024) and Ather Energy's IPO (May 2025) marked watershed moments for public market access. Battery-swap operators, charging infrastructure platforms, and ACC cell manufacturers are emerging as the next high-growth investment themes through 2030.

Future Market Outlook (2026-2034)

The India electric two-wheeler market forecast projects volumes to expand from 1,233.6 Thousand Units in 2025 to 12,263.2 Thousand Units by 2034, at a CAGR of 28.20%. North India will retain regional leadership while South India is projected as the fastest-growing region. Lithium-ion battery dominance will continue, with share crossing 95% by 2030.

Three structural shifts will reshape the India electric two-wheeler market through 2034. Local cell manufacturing under PLI will reduce import dependence below 50% by 2028. Battery-swap and battery-as-a-service models will lower upfront vehicle prices by 30-40%, accelerating mass-market and rural adoption. Smart-connectivity and OTA software updates will mature scooters into platform-style mobility devices, with annual feature releases driving consumer engagement.

Research Methodology

Primary Research

Primary research included structured interviews conducted in 2024-2025 with India electric two-wheeler ecosystem stakeholders, including OEM product managers, battery cell suppliers, dealership operators, fleet procurement leads, charging infrastructure providers, and policy experts. Primary insights validated market sizing, segmentation estimates, and policy impact assessments.

Secondary Research

Secondary sources include VAHAN registration data, FAME-II disbursement records, SIAM and FADA industry reports, OEM annual reports and investor presentations, NITI Aayog policy publications, Ministry of Heavy Industries notifications, RBI economic data, and trade publications such as AutoCar Professional and Mobility Outlook.

Forecasting Models

Market sizing and growth projections were derived using a combination of top-down and bottom-up approaches, incorporating GDP growth, urbanization rates, fuel price trajectories, FAME/EMPS/PM E-DRIVE policy outlays, and OEM capacity expansion plans. Scenario analyses (base, optimistic, and conservative) were conducted to incorporate policy and macroeconomic uncertainty.

India Electric Two-Wheeler Market Report Coverage

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Thousand Units |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Vehicle Types Covered | Electric Scooter/Moped, Electric Motorcycle |

| Battery Types Covered | Lithium-Ion, Sealed Lead Acid (SLA) |

| Voltage Types Covered | <48V, 48-60V, 61-72V, 73-96V, >96V |

| Peak Powers Covered | <3 kW, 3-6 kW, 7-10 kW, >10 kW |

| Battery Technologies Covered | Removable, Non-Removable |

| Motor Replacements Covered | Hub Type, Chassis Mounted |

| Regions Covered | North India, West and Central India, South India, East and Northeast India |

| Companies Covered | TVS Motor Company, Bajaj Auto Ltd, Hero MotoCorp Ltd, Ather Energy, Ola Electric Mobility Ltd, Greaves Electric Mobility Limited, Okinawa Autotech, Revolt Intellicorp Private Limited, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the India electric two-wheeler market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the India electric two-wheeler market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the India electric two-wheeler industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the India Electric Two-Wheeler Market Report

The India electric two-wheeler market reached 1,233.6 Thousand Units in 2025, driven by FAME-II subsidies, fuel cost savings, lithium-ion battery localization, and rapidly rising urban demand for clean mobility.

The market is projected to reach 12,263.2 Thousand Units by 2034, growing at a CAGR of 28.20% during 2026-2034, supported by policy continuity, charging infrastructure expansion, and fleet electrification.

Electric scooters and mopeds lead with 88.6% share in 2025, driven by lower upfront cost, ideal urban commute use cases, and broad model availability from Ola, TVS, Bajaj, Hero, and Ather.

Lithium-ion batteries account for 82.7% of the market in 2025, propelled by improving energy density, falling cell costs to USD 115/kWh, longer cycle life, and FAME-II eligibility favoring lithium chemistries.

North India dominates with 28.6% share in 2025, anchored by Delhi-NCR, Uttar Pradesh's per-vehicle subsidy, robust last-mile delivery demand, and accelerating commercial fleet electrification by quick-commerce players.

Key drivers include FAME-II and state EV subsidies, rising petrol prices near INR 100/litre, lithium-ion cost declines, urban pollution concerns, last-mile delivery electrification, and PLI-supported domestic battery cell manufacturing.

Major players include TVS Motor Company, Bajaj Auto Ltd, Hero MotoCorp Ltd, Ather Energy, Ola Electric Mobility Ltd, Greaves Electric Mobility Limited, Okinawa Autotech, Revolt Intellicorp Private Limited.

FAME-II, with a INR 10,000 crore outlay, has subsidized over 16 lakh electric two-wheelers through 2025, lowering on-road prices and accelerating buyer adoption across both personal and commercial fleet segments.

Key restraints include charging infrastructure gaps with only 25,000 public stations in 2025, high upfront vehicle costs, battery import dependence above 70%, and continued range anxiety in inter-city use cases.

Electric two-wheelers reached approximately 6.1% penetration of total Indian two-wheeler sales in 2025, up sharply from under 1% in 2021, reflecting structural mainstreaming of battery-electric drivetrains in urban India.

Key opportunities include battery-swap networks for fleet operators, Tier-2/Tier-3 city expansion, sub-INR 1 lakh affordable models, ACC cell manufacturing under PLI, and connected mobility software platforms.

South India is among the fastest-growing regions, advancing at approximately 30% CAGR through 2034, driven by Karnataka and Tamil Nadu manufacturing clusters, Telangana smart city programs, and Kerala's commercial fleet adoption.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)