India Electric Vehicle Market Size, Share, Trends and Forecast by Vehicle Type, Price Category, Propulsion Type, and Region, 2026-2034

India Electric Vehicle Market Size, Share, Trends & Forecast (2026-2034)

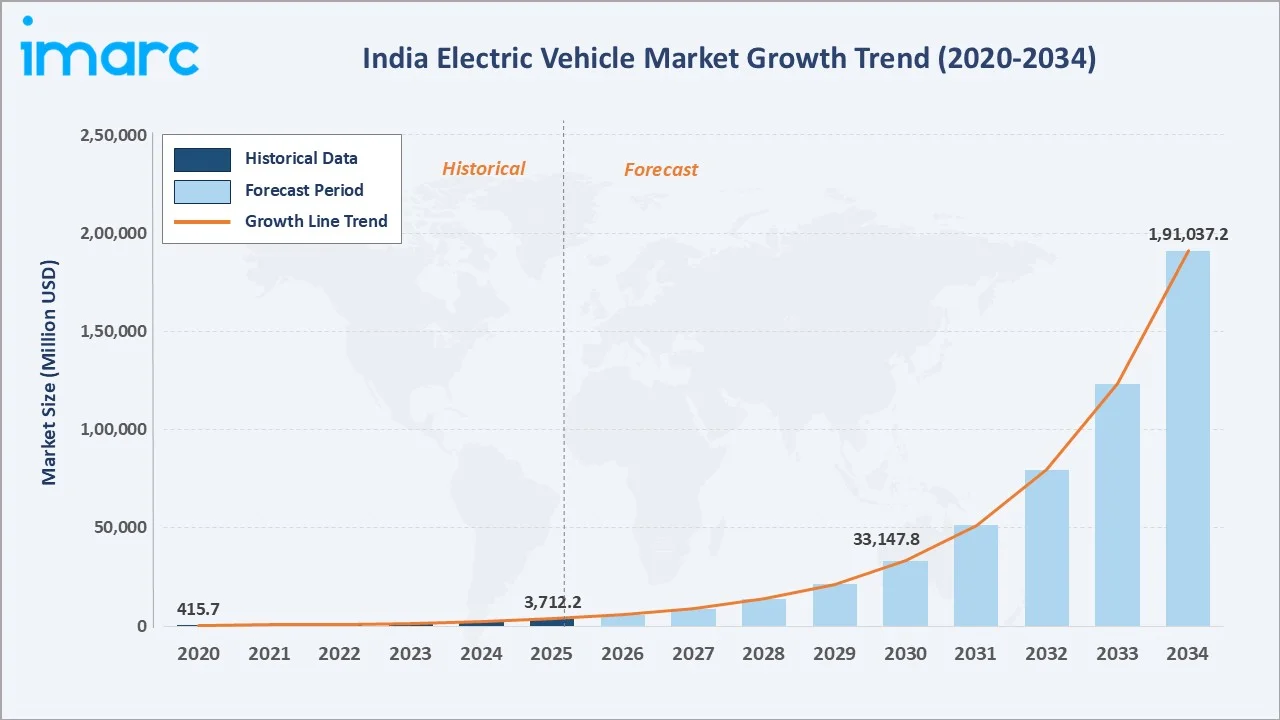

The India electric vehicle market size reached USD 3,712.2 Million in 2025 and is projected to reach USD 191,037.2 Million by 2034, exhibiting a CAGR of 54.94% during 2026-2034. Comprehensive government policy support through FAME India, PM E-DRIVE, and PLI schemes, combined with declining battery costs and rising conventional fuel prices, are the primary forces driving India EV market growth.

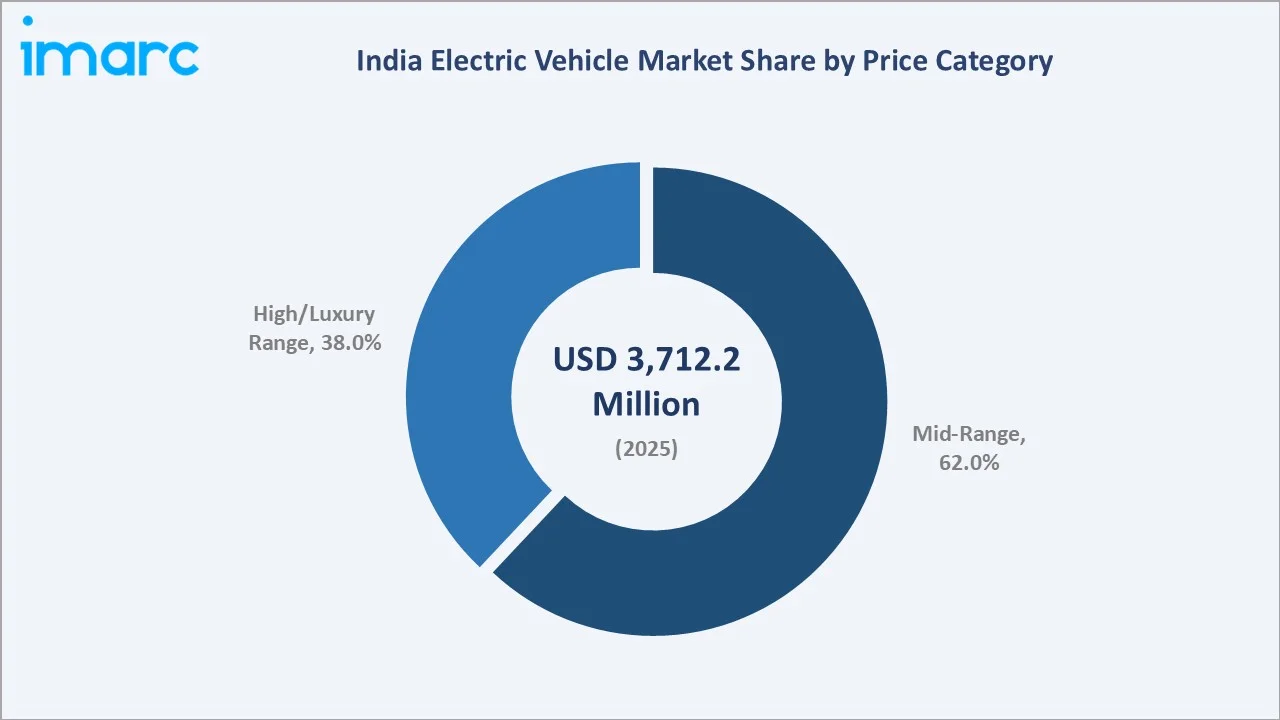

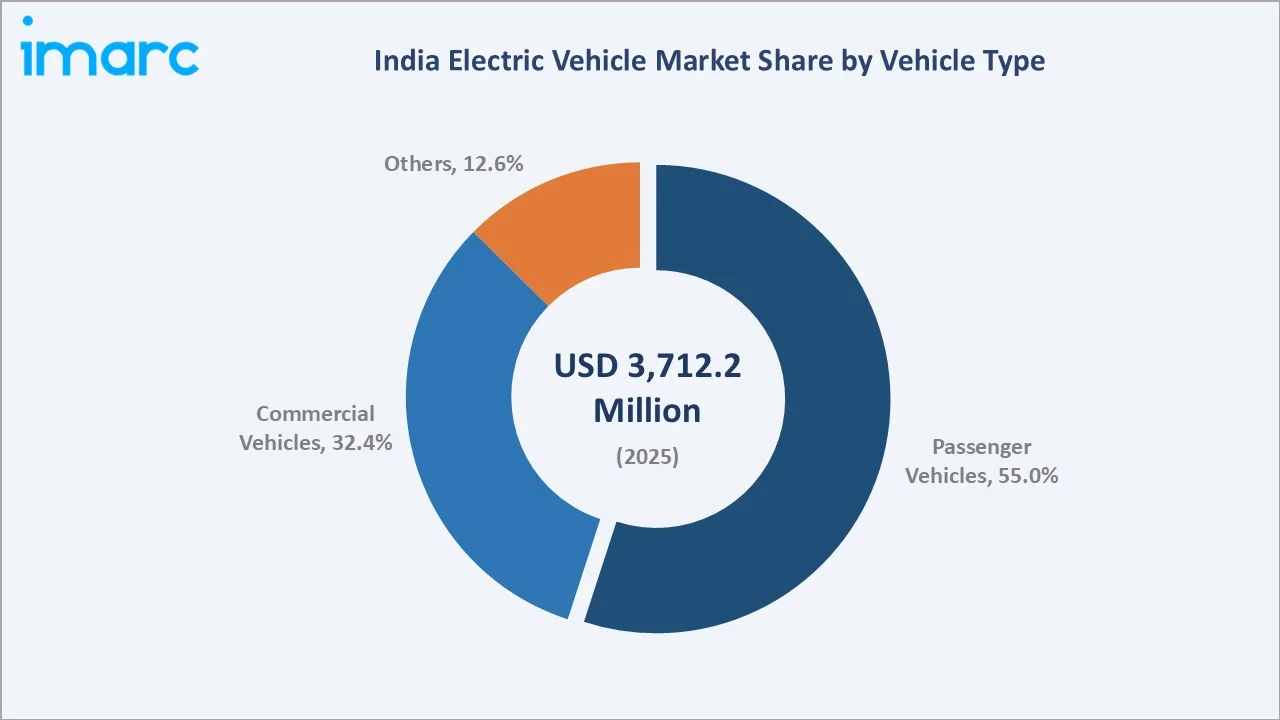

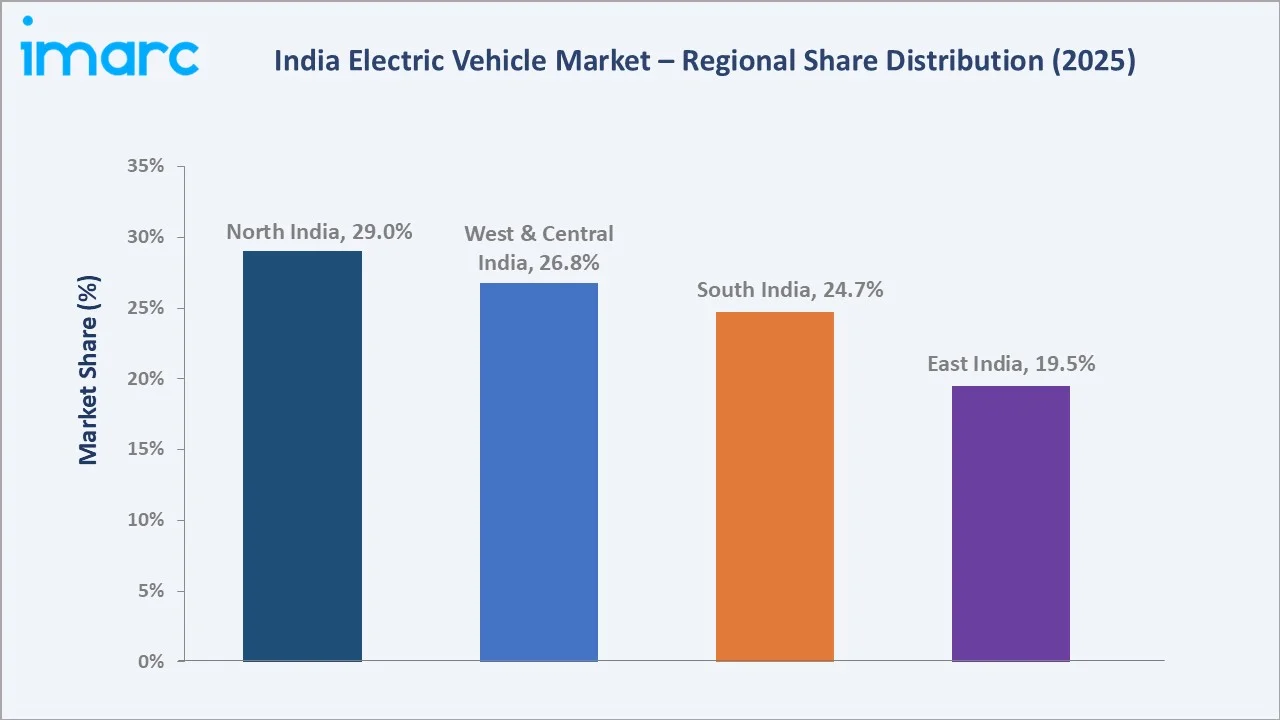

Mid-Range price category dominates at 62% in 2025, while Passenger Vehicles lead the vehicle type segment at 55%. North India commands a dominant 29% regional share in 2025, reflecting stringent emission norms and strong state-level EV policies across the Delhi NCR region.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 3,712.2 Million |

|

Forecast Market Size (2034) |

USD 191,037.2 Million |

|

CAGR (2026-2034) |

54.94% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Leading Price Category |

Mid-Range (62% share, 2025) |

|

Leading Vehicle Type |

Passenger Vehicles (55%, 2025) |

|

Largest Region |

North India (29% share, 2025) |

The India EV market growth trajectory from 2020 through 2034, with historical expansion to USD 3,712.2 Million in 2025, reflects accelerating policy-driven and consumer-led demand, while the forecast to USD 191,037.2 Million captures battery cost deflation, infrastructure build-out, and domestic manufacturing scale-up.

To get more information on this market, Request Sample

The CAGR trajectories across key price category, vehicle type, and regional sub-segments, with High/Luxury Range at ~62.5% CAGR and Commercial Vehicles at ~58.3% CAGR, are the fastest-growing categories within the India EV market analysis through 2034.

Executive Summary

The India electric vehicle market is on an exceptional growth trajectory from USD 3,712.2 Million in 2025 to USD 191,037.2 Million by 2034. EVs, encompassing battery electric vehicles (BEVs), plug-in hybrids (PHEVs), and hybrid electric vehicles (HEVs), serve passenger, commercial, and special-purpose mobility across urban and semi-urban India.

Mid-Range price category dominates at 62% in 2025, reflecting the cost-sensitive nature of the Indian consumer who prioritises total cost of ownership over premium features. Affordable pricing, combined with government subsidies, positions mid-range EVs as the primary volume driver for domestic OEMs, including Tata Motors, Ola Electric, and Hero Electric.

Passenger Vehicles command a 55% vehicle type share in 2025, driven by rising urban incomes, expanding charging infrastructure in metro regions, and the growing model availability from domestic and global OEMs. North India leads regional demand at 29%, anchored by Delhi NCR's stringent emission norms and strong state EV policies in Haryana, Uttar Pradesh, and Punjab.

Key Market Insights

|

Insight |

Data |

|

Leading Price Category |

Mid-Range – 62% share (2025) |

|

Second Price Category |

High/Luxury Range – 38% share (2025) |

|

Leading Vehicle Type |

Passenger Vehicles – 55% revenue share (2025) |

|

Second Vehicle Type |

Commercial Vehicles – 32.4% revenue share (2025) |

|

Leading Region |

North India – 29.0% revenue share (2025) |

|

Second Region |

West & Central India – 26.8% revenue share (2025) |

|

Top Companies |

Tata Motors Limited, Ola Electric Mobility Ltd., Mahindra &Mahindra Ltd., Ather Energy, Hero MotoCorp Ltd., TVS Motor Company, Bajaj Auto Ltd. |

Key Analytical Observations Supporting the Above Data:

- Mid-Range EV dominance at 62% in 2025 is driven by India’s price-sensitive market, where total cost of ownership matters more than acquisition price. FAME II subsidies and state-level incentives have made mid-range EVs viable for the middle-class buyer.

- Passenger Vehicles at 55% in 2025 lead because urban India’s daily commuting distances of 30–80 km are well within the 150–300 km range of affordable BEVs, and fleet operators’ fuel-cost savings justify the EV premium within 2–3 years.

- North India’s 29% dominance in 2025 reflects Delhi NCR’s BS-VI emission norm enforcement and the Delhi EV Policy’s direct incentives, combined with Haryana and UP automotive manufacturing clusters that drive both supply and adoption.

- West and Central India at 26.8% in 2025 is anchored by Maharashtra and Gujarat, India’s two largest automotive manufacturing states, hosting Tata Motors’ Pune facility and Ola Electric’s Future Factory in Krishnagiri, Tamil Nadu.

India Electric Vehicle Market Overview

An electric vehicle (EV) is a vehicle propelled by one or more electric motors drawing power from rechargeable battery packs, eliminating internal combustion engine dependence on fossil fuels. The India EV ecosystem integrates lithium-ion battery cell manufacturers, EV OEM assemblers, charging infrastructure operators, software and telematics providers, fleet operators, and diverse end-use segments spanning personal mobility, commercial logistics, public transit, and three-wheeler last-mile delivery.

India’s EV market architecture is distinct from other major economies: two- and three-wheelers account for the largest unit volume at lower price points, while passenger cars and commercial vehicles represent the highest revenue contribution. The government’s vision of 30% EV penetration across all vehicle categories by 2030 underpins the most ambitious policy incentive structure in the Asia-Pacific region outside China.

Market Dynamics

To evaluate market opportunities, Request Sample

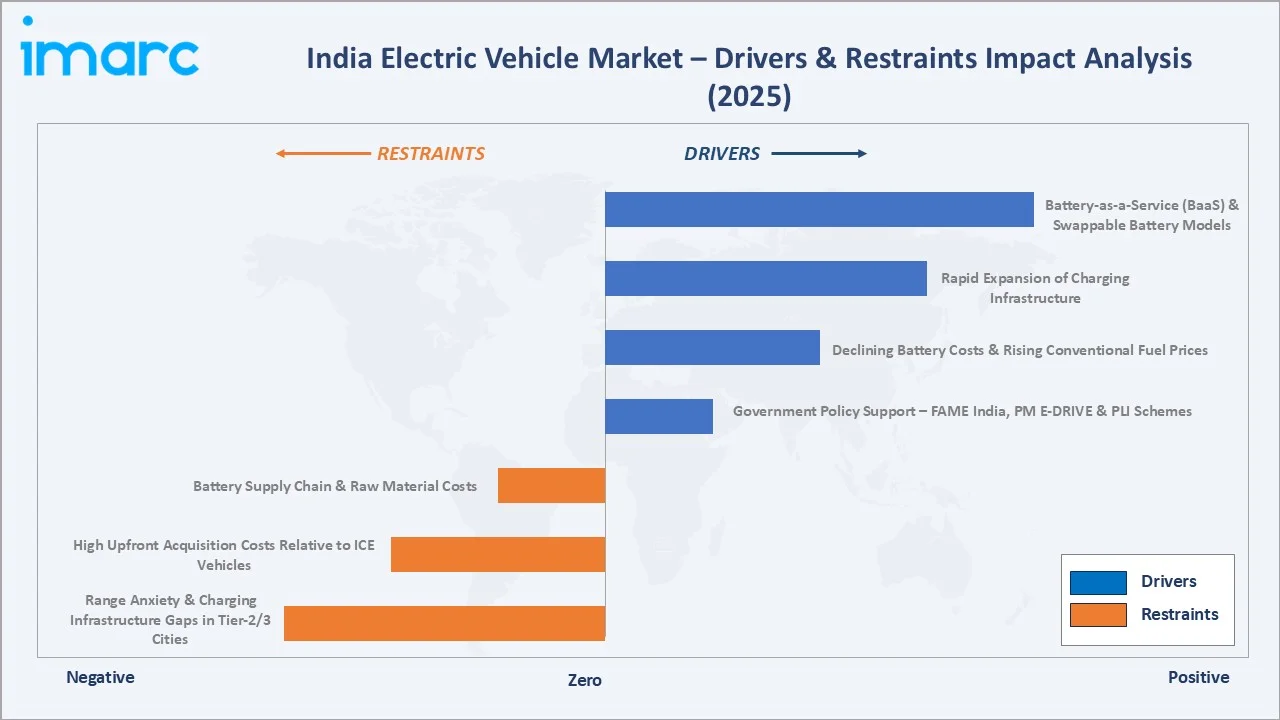

Market Drivers

- Government Policy Support – FAME India, PM E-DRIVE & PLI Schemes: The PM E-DRIVE scheme with INR 10,900 Crore allocation extended to March 2028 directly subsidises EV two-wheelers, three-wheelers, and buses. The PLI scheme for ACC battery storage worth INR 18,100 Crore anchors domestic battery manufacturing, reducing import dependency and enabling cost reduction for Indian OEMs.

- Declining Battery Costs & Rising Conventional Fuel Prices: Declining battery costs, coupled with rising prices of conventional fuels, are improving the overall cost competitiveness of electric vehicles. This shift is making EVs increasingly attractive for cost-conscious consumers, particularly in high-usage segments like two-wheelers and three-wheelers. It is also accelerating the transition from ICE vehicles to EVs, especially in urban and last-mile mobility use cases. As affordability improves, adoption is expected to scale further, supported by increasing consumer awareness and favorable operating economics.

- Rapid Expansion of Charging Infrastructure: India surpassed 29,000 public charging stations by August 2025, with Karnataka, Maharashtra, UP, and Delhi leading deployment. Tata Power, BPCL, and Ather Grid are investing in high-speed DC charger rollout across highways, malls, and corporate campuses, reducing range anxiety in key metropolitan corridors.

Market Restraints

- Range Anxiety & Charging Infrastructure Gaps in Tier-2/3 Cities: Outside the top 20 cities, charging infrastructure remains sparse. The median inter-station distance on national highways is still 120–150 km, creating hesitation among long-distance commuters and fleet operators considering EV transition in smaller urban centres.

- High Upfront Acquisition Costs Relative to ICE Vehicles: Despite subsidies, a comparable BEV costs 20–35% more upfront than its ICE equivalent in the passenger vehicle segment. For two-wheeler and three-wheeler segments, the price gap has narrowed but remains a barrier for sub-INR 1 Lakh buyers in rural and semi-urban markets.

Market Opportunities

- Electric Commercial Vehicle Fleet Electrification: India’s e-commerce logistics sector, processing over 10 million daily shipments, is actively transitioning last-mile delivery fleets to electric three-wheelers and light commercial vehicles. Companies including Amazon, Flipkart, Zomato, and Swiggy have announced 100% EV delivery targets, generating substantial order pipelines for domestic EV manufacturers.

- Battery-as-a-Service (BaaS) & Swappable Battery Models: Swap-based business models, pioneered by Sun Mobility and Gogoro, address range anxiety and upfront cost barriers by separating battery ownership from vehicle ownership. Battery Smart, a startup that targets commercial vehicles, has more than 1,400 swapping sites across 40 cities, enabling lower acquisition prices for two- and three-wheeler segments.

Market Challenges

- Domestic Battery Cell Manufacturing Gaps: India currently imports over 70% of its lithium-ion battery cells from China, South Korea, and Japan. Despite PLI incentives, large-scale domestic gigafactory production is not expected before 2027–2028, maintaining import dependency and exposing OEMs to currency and supply chain risks in the medium term.

- Charging Infrastructure Investment & Standardisation Gaps: Multiple competing charging standards, the absence of mandatory interoperability requirements, and high land and power costs in metro areas slow the pace of public charger deployment. Without a unified charging protocol, consumer confidence in charging availability remains constrained.

Emerging Market Trends

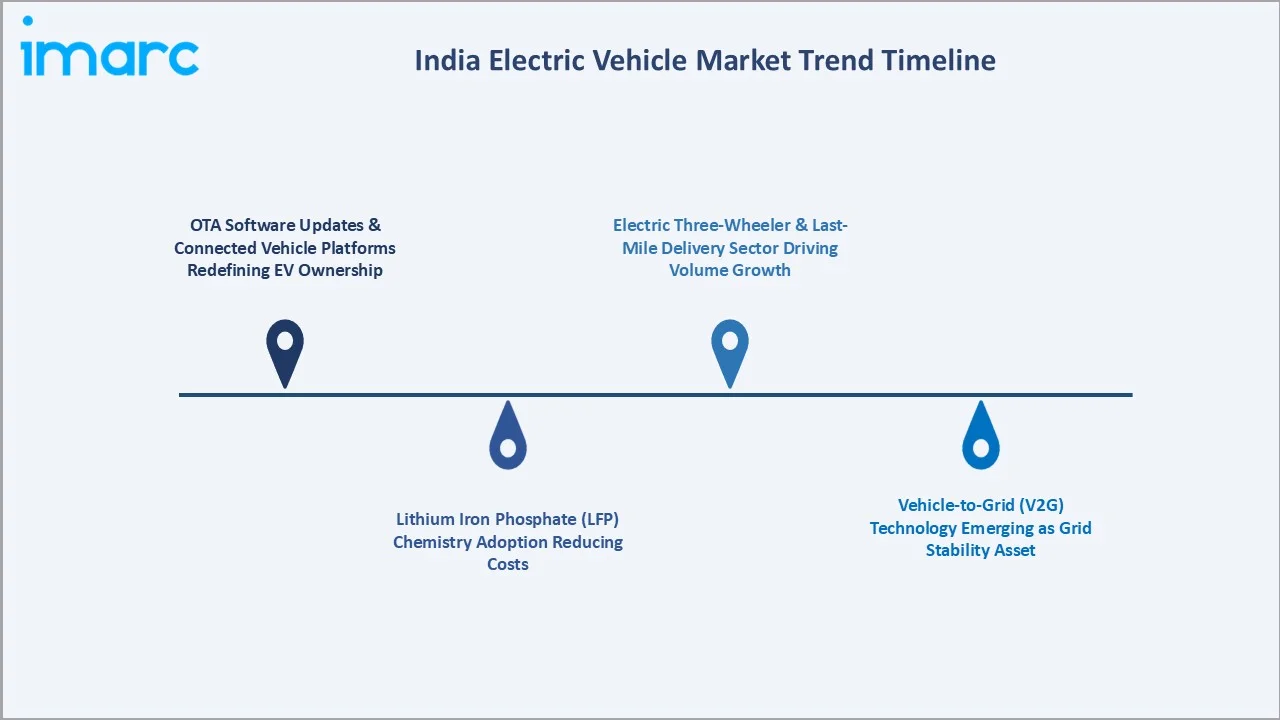

1. OTA Software Updates & Connected Vehicle Platforms Redefining EV Ownership

India’s EV-native OEMs — Ather Energy, Ola Electric, and Tata Motors’ EV division — have built software-defined vehicle architectures enabling over-the-air (OTA) performance, range, and feature updates. Ather’s AtherStack and Ola’s MoveOS platforms position India’s EV brands closer to Tesla’s connected-vehicle model than traditional ICE OEMs, creating recurring software revenue streams beyond the initial vehicle sale.

2. Lithium Iron Phosphate (LFP) Chemistry Adoption Reducing Costs

Indian EV OEMs are shifting from NMC to LFP battery chemistry, which offers lower cost per kWh, longer cycle life (2,000+ cycles), and superior thermal safety. BYD’s Blade Battery and CATL’s LFP exports to India have enabled domestic OEMs to offer improved warranty terms — up to 8 years/160,000 km — that are critical for commercial fleet adoption decisions.

3. Electric Three-Wheeler & Last-Mile Delivery Sector Driving Volume Growth

Electric three-wheelers represent the highest unit penetration rate in India’s EV market at approximately 53% of total three-wheeler sales in 2025. E-rickshaws and cargo three-wheelers serve over 7 million daily passenger and delivery trips in Indian cities. The economics are compelling: operators save approximately INR 200–250 per day in fuel costs, recovering the EV premium within 12–18 months.

4. Vehicle-to-Grid (V2G) Technology Emerging as Grid Stability Asset

India’s renewable energy integration challenges — managing 165 GW of solar and wind intermittency — are creating policy interest in V2G technology. CESL and Tata Power have initiated pilot V2G programs in Delhi and Mumbai, where EV fleet batteries can discharge stored energy back to the grid during peak demand, earning revenue for fleet operators while supporting grid stability.

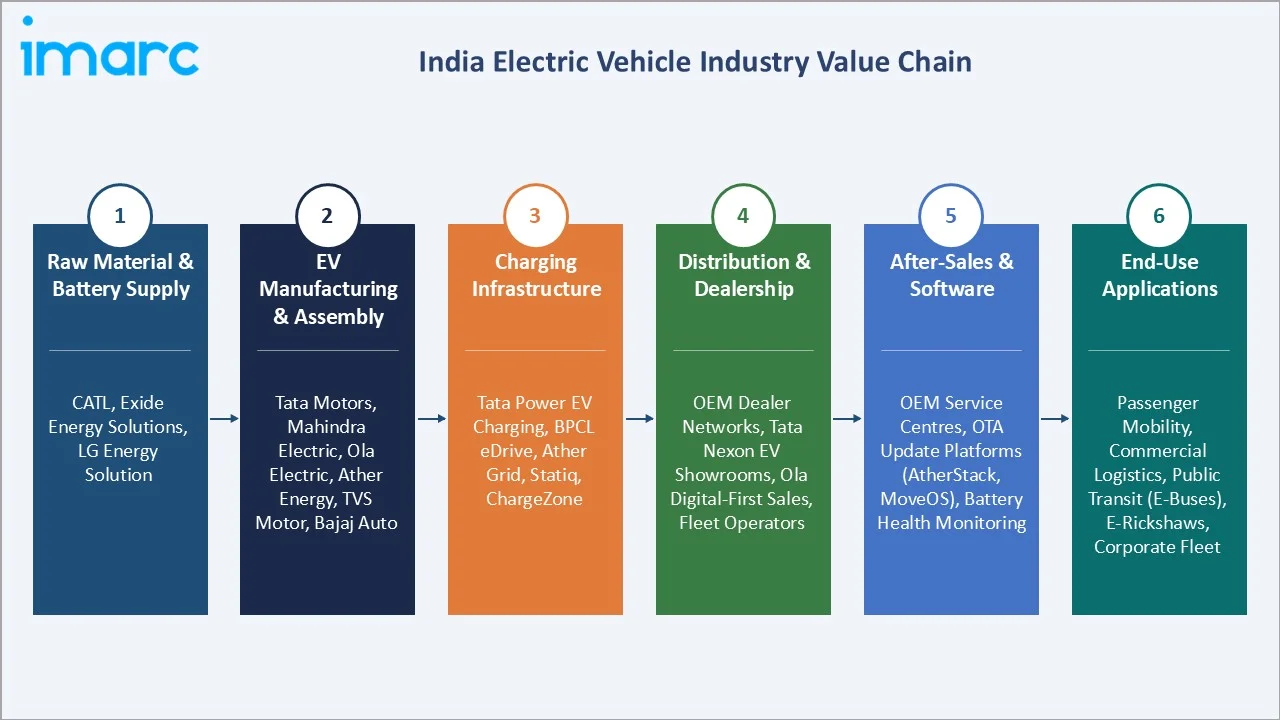

Industry Value Chain Analysis

The India EV value chain spans six stages from raw material and battery cell sourcing through end-use applications. Battery manufacturing and EV assembly capture the highest value-add margins, while charging infrastructure and after-sales software services generate recurring revenue that increasingly differentiates EV business models from traditional automotive.

|

Stage |

Key Players / Examples |

|

Raw Material & Battery Supply |

CATL, Exide Energy Solutions, LG Energy Solution |

|

EV Manufacturing & Assembly |

Tata Motors, Mahindra Electric, Ola Electric, Ather Energy, TVS Motor, Bajaj Auto |

|

Charging Infrastructure |

Tata Power EV Charging, BPCL eDrive, Ather Grid, Statiq, ChargeZone |

|

Distribution & Dealership |

OEM dealer networks, Tata Nexon EV showrooms, Ola digital-first sales, fleet operators |

|

After-Sales & Software |

OEM service centres, OTA update platforms (AtherStack, MoveOS), battery health monitoring |

|

End-Use Applications |

Passenger mobility, commercial logistics, public transit (e-buses), e-rickshaws, corporate fleet management |

Vertically integrated OEMs with in-house battery pack assembly capabilities, such as Tata Motors’ Pune EV manufacturing hub, achieve lower bill-of-materials cost than competitors dependent on third-party battery packs. This vertical integration provides a meaningful competitive advantage as battery costs remain the largest component of EV total cost.

Technology Landscape in the India EV Industry

Battery Technology: LFP vs. NMC Chemistry Evolution

Lithium Iron Phosphate (LFP) chemistry is progressively replacing NMC (Nickel Manganese Cobalt) in India’s mass-market EV segment due to superior thermal stability, longer cycle life, and 15–20% lower cost per kWh. CATL’s CTP (Cell-to-Pack) technology and BYD’s Blade Battery eliminate module-level packaging, improving energy density by 50% and enabling Indian OEMs to offer 300–400 km range at competitive price points.

Permanent Magnet Synchronous Motors & In-Wheel Drive Systems

PMSM (Permanent Magnet Synchronous Motor) technology, offering 92–95% efficiency versus 85–88% for induction motors, is the dominant powertrain architecture in Indian passenger EVs. In-wheel hub motor technology, deployed in Ather 450X and certain three-wheeler platforms, eliminates the differential and driveshaft, reducing mechanical complexity and improving packaging efficiency in compact urban EVs.

Advanced Driver Assistance & Vehicle-to-Everything (V2X) Connectivity

India’s EV-native OEMs are integrating ADAS Level 1–2 features — lane departure warning, automatic emergency braking, adaptive cruise control — as standard in premium segments above INR 15 Lakh. V2X connectivity enabling EV communication with traffic signals, charging stations, and grid operators is in pilot deployment through CESL’s Smart Mobility programs in Delhi and Bengaluru.

Fast Charging Technology: DC Fast Chargers & Ultra-Fast 350 kW Infrastructure

India’s charging infrastructure is transitioning from AC slow chargers (3.3–7 kW) to DC fast chargers (30–150 kW) capable of delivering 80% charge in 20–30 minutes. Tata Power and ChargeZone are deploying 60–150 kW CCS2-compliant DC fast chargers at highway corridors, commercial complexes, and residential societies. Ultra-fast 350 kW chargers are in early pilot deployment in India for commercial fleet applications.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Vehicle Type |

Passenger Vehicles |

55.0% |

2025 |

|

Price Category |

Mid-Range |

62.0% |

2025 |

|

Propulsion Type |

Battery Electric Vehicle |

48.0% |

2025 |

|

Region |

North India |

29.0% |

2025 |

By Price Category

The mid-range EV price category commands a 62.0% majority share in 2025, reflecting India’s price-elastic consumer base and the effectiveness of FAME II subsidies in making INR 7–15 Lakh EVs financially competitive with ICE alternatives on a total cost of ownership basis. Tata Nexon EV, Tata Tiago EV, MG ZS EV, and Ola S1 Pro populate this dominant segment.

To access detailed market analysis, Request Sample

High/luxury range EV category at 38.0% in 2025 is growing fastest at ~62.5% CAGR through 2034. Premium EVs (above INR 20 Lakh) benefit from disproportionately affluent early adopters seeking ADAS, panoramic roofs, and large battery packs. Hyundai Creta Electric, Kia EV6, BYD Atto 3, and Mahindra BE 6 compete in this rapidly expanding segment as India’s EV aspirations expand from mass-market to premium.

By Vehicle Type

Passenger Vehicles dominate the vehicle type segment at 55.0% in 2025, driven by urban India’s transition from shared mobility to personal EV ownership.

Commercial Vehicles at 32.4% in 2025 represent the second largest and fastest-growing vehicle type, driven by fleet operators’ total cost of ownership advantage in high-utilisation urban delivery and transit applications. Electric buses from JBM Auto, Olectra, and Tata Motors serve state transport undertakings across Mumbai, Delhi, Pune, and Bengaluru. Others (12.6%) encompass electric two-wheelers sold in volume and e-rickshaws driving mass rural electrification.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

North India |

29.0% |

Delhi NCR emission norms; Delhi EV Policy incentives; Haryana & UP automotive clusters; high metro EV adoption |

|

West & Central India |

26.8% |

Maharashtra’s Tata & Mahindra manufacturing; Gujarat renewable energy; Mumbai-Pune highway EV corridor |

|

South India |

24.7% |

Tamil Nadu’s Hyundai & Ola factories; Bengaluru tech adoption; Andhra Pradesh EV policy; Ather’s home market |

|

East India |

19.5% |

Emerging EV adoption in West Bengal; Odisha industrial corridor; e-rickshaw dominance in Bihar & Jharkhand |

North India’s 29.0% market dominance in 2025 is driven by Delhi’s Switch Delhi campaign and one of India’s most comprehensive EV policies, offering up to INR 1.5 Lakh purchase incentive for two-wheelers and INR 30,000 for e-rickshaws. The NCR’s existing CNG refuelling infrastructure has accelerated commercial operator migration toward EVs as a next-generation clean fuel alternative.

West and Central India at 26.8% in 2025 benefits from the convergence of India’s two largest automobile manufacturing states, Maharashtra (Tata Motors’ Pune complex) and Gujarat (Maruti Suzuki’s Hansalpur facility transitioning to EVs), with strong EV policy support. Maharashtra’s EV policy offers 100% road tax waiver and registration fee exemption, among the most generous incentive structures nationally.

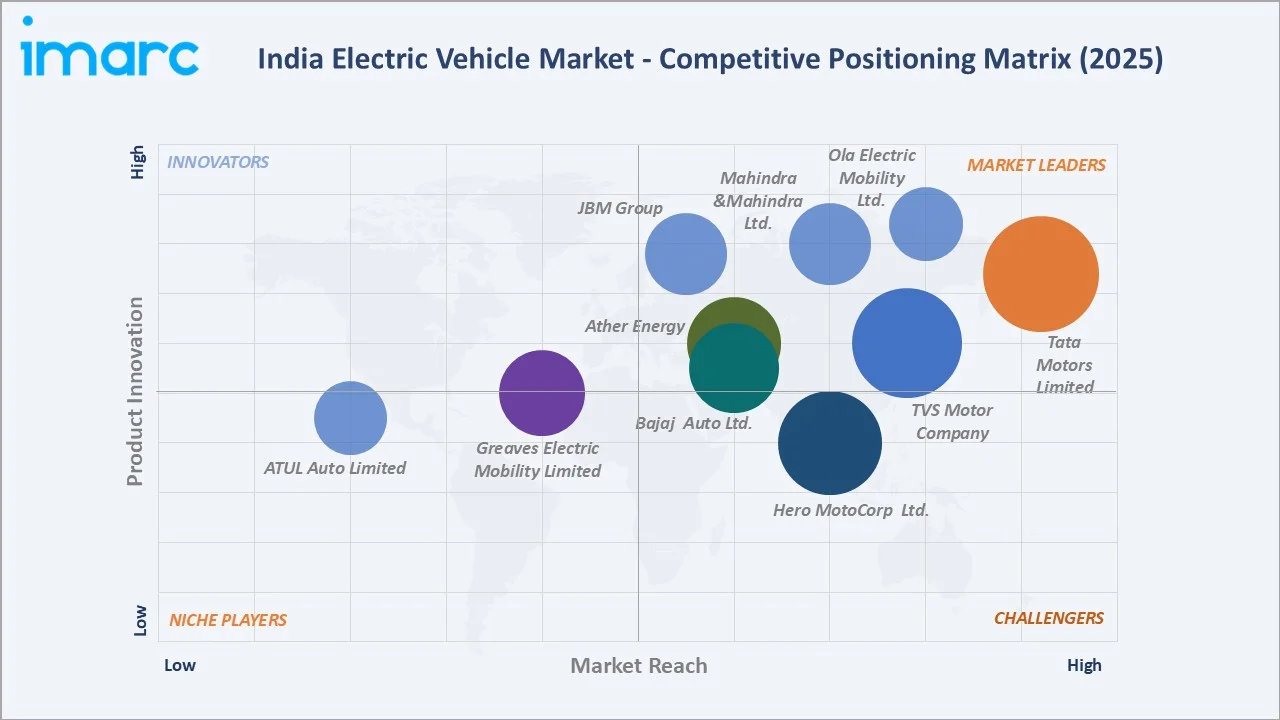

Competitive Landscape

The India electric vehicle market is moderately fragmented, with Tata Motors holding a commanding lead in the passenger EV segment, while the two-wheeler segment sees strong competition between Ola Electric, Ather Energy, Hero Electric, and TVS iQube. The commercial vehicle segment is contested by JBM Auto, Olectra Greentech, and Tata Motors.

|

Company Name |

Key Products |

Market Position |

Strategic Focus |

|

Tata Motors Limited |

Nexon EV, Tigor EV, Punch EV, Curvv EV |

Leader |

Passenger EV leader; broadest model range; TPEM subsidiary |

|

Ola Electric Mobility Ltd. |

S1 Pro, S1 Air, S1 X, S1 X+ |

Leader |

E-scooter leader; digital-first sales; Future Factory scale-up; MoveOS platform |

|

Mahindra&Mahindra Ltd. |

BE 6, XEV 9e |

Leader |

SUV-focused EV; INGLO platform; Volkswagen partnership; BE & XEV series |

|

Ather Energy |

450X, 450S, Rizta, Ather Grid |

Leader |

Premium e-scooter; AtherStack software; Ather Grid fast-charging; IPO 2025 |

|

Hero MotoCorp Ltd. |

Vida V2, Vida V1 Pro, Vida V2 Pro |

Challenger |

Mass-market e-scooters; Tier 2/3 city distribution; entry segment volume |

|

TVS Motor Company |

iQube, iQube S, iQube Electric |

Leader |

Connected e-scooter; SmartXonnect; Hosur manufacturing scale-up |

|

Bajaj Auto Ltd. |

Chetak 3001, 3501, 3502, 3503 |

Leader |

Retro-styled premium scooter; Pune facility; expanding tier-2 city presence |

|

Greaves Electric Mobility Limited |

Ampere Magnus, Zeal, Primus |

Emerging |

Mid-segment e-scooters; Ampere brand; focus on women urban commuters |

|

JBM Group |

Ecolife electric bus, Intercity EV |

Leader |

Electric bus leader; BEST/DTC/NMMT contracts; 200+ city bus deployments |

|

ATUL Auto Limited |

Atul Elite Plus, Atul RIK EV, Atul Energie |

Emerging |

Electric three-wheeler specialist; rural distribution; L5 category focus |

Key players include Tata Motors Limited, Ola Electric Mobility Ltd., Mahindra&Mahindra Ltd., Ather Energy, Hero MotoCorp Ltd., TVS Motor Company, Bajaj Auto Ltd., Greaves Electric Mobility Limited, JBM Group, ATUL Auto Limited, and others.

Key Company Profiles

Tata Motors Limited

Tata Motors, currently operating as Tata Motors Passenger Vehicles, is India’s largest electric vehicle manufacturer. The company’s EV portfolio spans multiple segments and price points, built on dedicated EV platforms.

- Product Portfolio: Offers Nexon EV, Tigor EV, Punch EV, and Curvv EV, among others, for passenger electric vehicles in India.

- Recent Developments: In September 2025, Tata Motors strengthened its EV ecosystem by enabling access to over 25,000 public charging stations for electric small commercial vehicles across India. These chargers are strategically deployed across more than 150 cities, particularly around key logistics hubs, to support last-mile delivery operations.

- Strategic Focus: Tata’s EV strategy leverages its vertically integrated model — battery pack assembly at Pune, motor manufacturing through Tata AutoComp — to maintain cost leadership in the volume segment while expanding premium SUV offerings targeting the growing High/Luxury Range category.

Ola Electric Mobility Ltd.

Ola Electric is India’s one of the leading electric two-wheeler manufacturers, disrupting the traditional dealership model through direct-to-consumer digital sales. The company’s Future Factory in Krishnagiri, Tamil Nadu, is one of the world’s largest single-location electric two-wheeler manufacturing facilities.

- Product Portfolio: Offers S1 Pro, S1 Air, S1 X, and S1 X+ electric scooters in India.

- Recent Developments: In March 2025, Ola Electric received ₹73.7 crore in incentives under the government’s Production Linked Incentive (PLI) scheme, becoming the first two-wheeler manufacturer in India to qualify for the program. The incentive is linked to the company’s eligible sales and compliance with localization requirements.

- Strategic Focus: Ola’s strategy focuses on manufacturing scale and software differentiation through MoveOS, creating an ecosystem of connected scooters with OTA updates, predictive maintenance, and integrated payment features that traditional ICE OEMs cannot replicate.

Mahindra &Mahindra Ltd.

Mahindra Electric Mobility, a subsidiary of Mahindra & Mahindra, is India’s premier electric SUV manufacturer, pivoting from its legacy e20 platform to the all-new INGLO electric architecture, targeting the premium EV segment.

- Product Portfolio: Offers BE 6 and XEV 9e electric SUVs built on the INGLO BEV platform for India’s electric vehicle market.

- Recent Developments: In March 2026, Mahindra’s EV charging arm entered a strategic partnership with Hindustan Petroleum Corporation Limited (HPCL) to develop electric vehicle charging infrastructure across HPCL’s fuel stations nationwide. The new infrastructure will feature high-speed 180 kW chargers designed to offer quicker and more reliable charging, enhancing user convenience.

- Strategic Focus: Mahindra’s EV strategy differentiates through premium platform architecture and performance specifications, targeting High/Luxury Range buyers willing to pay for domestic technology rather than imported EVs, while leveraging INGLO platform scalability for future variants.

Ather Energy

Ather Energy, founded by IIT Madras alumni Tarun Mehta and Swapnil Jain, is India’s pioneer in premium connected electric scooters. Based in Bengaluru, Ather is renowned for its AtherStack software-defined vehicle architecture and the Ather Grid fast-charging network. The company completed its IPO in 2025.

- Product Portfolio: Offers 450X, 450S, and Rizta electric scooters plus Ather Grid fast-charging network infrastructure in India.

- Recent Developments: In August 2024, Ather Energy signed a strategic MoU with Amara Raja Advanced Cell Technologies to develop and source lithium-ion battery cells for its electric two-wheelers. The collaboration focuses on producing advanced chemistry cells, including NMC and LFP, tailored to Ather’s specific requirements. These battery cells will be manufactured domestically at Amara Raja’s upcoming gigafactory in Telangana, supporting localization and reducing dependence on imports.

- Strategic Focus: Ather’s strategy centres on software differentiation through AtherStack — delivering OTA updates, smart navigation, and battery health optimisation — creating a premium connected mobility ecosystem that commands a 15–20% pricing premium over comparable hardware-spec competitors.

Market Concentration Analysis

The India electric vehicle market is moderately fragmented at the national level, with Tata Motors holding the dominant position in passenger EVs while the two-wheeler segment is contested among four to five leading players. No single company holds more than 37–40% of total India EV market revenue across all segments, and new entrants continue to emerge across segments.

Consolidation in the two-wheeler EV segment is accelerating as larger OEMs with manufacturing scale and distribution networks — TVS Motor, Bajaj Auto, Hero MotoCorp — enter the segment with growing investment. The commercial EV segment is more concentrated, with JBM Auto and Olectra holding majority shares in the electric bus tender market, supported by CESL’s aggregated procurement model that favours large-scale manufacturers.

Investment & Growth Opportunities

Fastest-Growing Segments

High/Luxury Range EVs at ~62.5% CAGR through 2034 is the highest-growth price category, driven by premium SUV launches from Mahindra, Kia, Hyundai, and BYD targeting India’s 50 million affluent households. Commercial Vehicles at ~58.3% CAGR represent the broadest-based growth opportunity, supported by government e-bus procurement and corporate fleet electrification mandates.

Emerging Markets within India

East India at ~52% CAGR is the fastest-growing domestic region for electric vehicles through 2034. West Bengal’s Singur and Odisha’s Kalinganagar industrial corridors are attracting EV component manufacturing investment, while Bihar and Jharkhand’s rapidly growing e-rickshaw markets represent a 5-million-unit addressable opportunity by 2030.

Venture & Investment Trends

Private equity and venture capital investment in India’s EV ecosystem exceeded USD 2 Billion in 2024, targeting battery technology startups, charging network operators, and EV fleet management platforms. Battery recycling and second-life applications are an emerging investment theme: India will generate approximately 50,000 tonnes of spent EV batteries annually by 2030. Government PLI incentives and green financing from multilateral agencies including ADB and IFC are channelling capital toward domestic gigafactory development.

Future Market Outlook (2026-2034)

The India electric vehicle market is forecast to expand from USD 3,712.2 Million in 2025 to USD 191,037.2 Million by 2034 at a CAGR of 54.94%, adding approximately USD 187 Billion in incremental annual market value over the forecast period. This exceptional growth trajectory reflects India’s position as the world’s most rapidly electrifying major automotive market.

Three structural forces will shape the India EV industry through 2034. First, battery cost convergence with ICE vehicles — expected around 2028–2030 for passenger vehicles — will eliminate the subsidy dependency that currently limits mass-market adoption. Second, the PLI-supported domestic gigafactory ecosystem, led by Amara Raja, Exide Energy, and Reliance Industries’ battery ventures, will reduce import dependency from 70% to below 30% by 2030. Third, the government’s 30% EV penetration target by 2030 will sustain policy tailwinds across purchase incentives, charging infrastructure grants, and commercial fleet mandates through the entire forecast period.

Research Methodology

Primary Research

Primary research encompassed over 45 structured interviews in 2024–2025 with India EV industry stakeholders, including senior commercial managers at Tata Motors’ TPEM division, Ola Electric, and Ather Energy; fleet procurement managers at CESL, BEST, and DTC; battery technology engineers at Amara Raja and Exide Energy; and FAME scheme administrators at MoHI. Primary data validated market sizing, vehicle type and price segment shares, regional demand estimates, and technology adoption timelines.

Secondary Research

Key secondary sources include Ministry of Heavy Industries Annual Reports, SIAM EV Data, VAHAN registration database, IEA Global EV Outlook 2025, CESL EV procurement data, Niti Aayog India EV Policy Papers, TERI EV Charging Infrastructure reports, State EV Policy documents (Delhi, Maharashtra, Gujarat, Tamil Nadu), and trade publications including Autocar India, ET Auto, and The Economic Times Energy Supplement.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models, incorporating India’s GDP growth trajectory, EV penetration rate curves, battery cost deflation models, and historical VAHAN registration evolution patterns. Scenario analysis across base, optimistic, and conservative cases was performed to account for policy continuity risks and macroeconomic volatility.

India Electric Vehicle Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD, ‘000 Units |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Vehicle Types Covered | Passenger Vehicles, Commercial Vehicles, Others |

| Price Categories Covered | Mid-Range, High/Luxury Range |

| Propulsion Types Covered | Battery Electric Vehicle, Hybrid Electric Vehicle, Plug-In Hybrid Electric Vehicle |

| Regions Covered | North India, West and Central India, South India, East India |

| Companies Covered | Tata Motors Limited, Ola Electric Mobility Ltd., Mahindra&Mahindra Ltd., Ather Energy, Hero MotoCorp Ltd., TVS Motor Company, Bajaj Auto Ltd., Greaves Electric Mobility Limited, JBM Group, ATUL Auto Limited, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Electric Vehicle Market Report

The India electric vehicle market reached USD 3,712.2 Million in 2025, reflecting accelerating policy support, declining battery costs, and rising consumer adoption across two-wheelers, passenger vehicles, and commercial segments.

The market is projected to reach USD 191,037.2 Million by 2034, growing at a CAGR of 54.94% during 2026-2034, driven by battery cost convergence, PLI-supported domestic manufacturing, and expanding charging infrastructure.

Mid-Range EV category leads with 62.0% share in 2025, reflecting India’s cost-sensitive consumer base and the effectiveness of FAME II subsidies in making INR 7–15 Lakh EVs financially competitive with ICE equivalents on total cost of ownership.

Passenger Vehicles lead at 55.0% in 2025, driven by urban EV adoption across sedans, hatchbacks, and SUVs, supported by an expanding charging network in metro cities and growing model availability from domestic and global OEMs.

North India commands the dominant 29.0% market share in 2025, driven by Delhi NCR’s stringent emission norms, the Delhi EV Policy’s direct purchase incentives, and automotive manufacturing clusters across Haryana and Uttar Pradesh.

High/Luxury Range EVs are the fastest-growing price category at ~62.5% CAGR through 2034, driven by premium SUV launches from Mahindra, Hyundai, Kia, and BYD targeting India’s affluent urban household segment.

Leading companies include Tata Motors Limited, Ola Electric Mobility Ltd., Mahindra &Mahindra Ltd., Ather Energy, Hero MotoCorp Ltd., TVS Motor Company, Bajaj Auto Ltd., Greaves Electric Mobility Limited, JBM Group, ATUL Auto Limited, and others.

Key applications include urban personal commuting, e-commerce last-mile delivery logistics, public transit electric bus fleets, e-rickshaw passenger services, corporate employee transport, and ride-sharing fleet electrification across metro and Tier-1 cities.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)