India Electronic Warfare Market Size, Share, Trends and Forecast by Product, Equipment, Capacity, Platform, and Region, 2026-2034

India Electronic Warfare Market Summary:

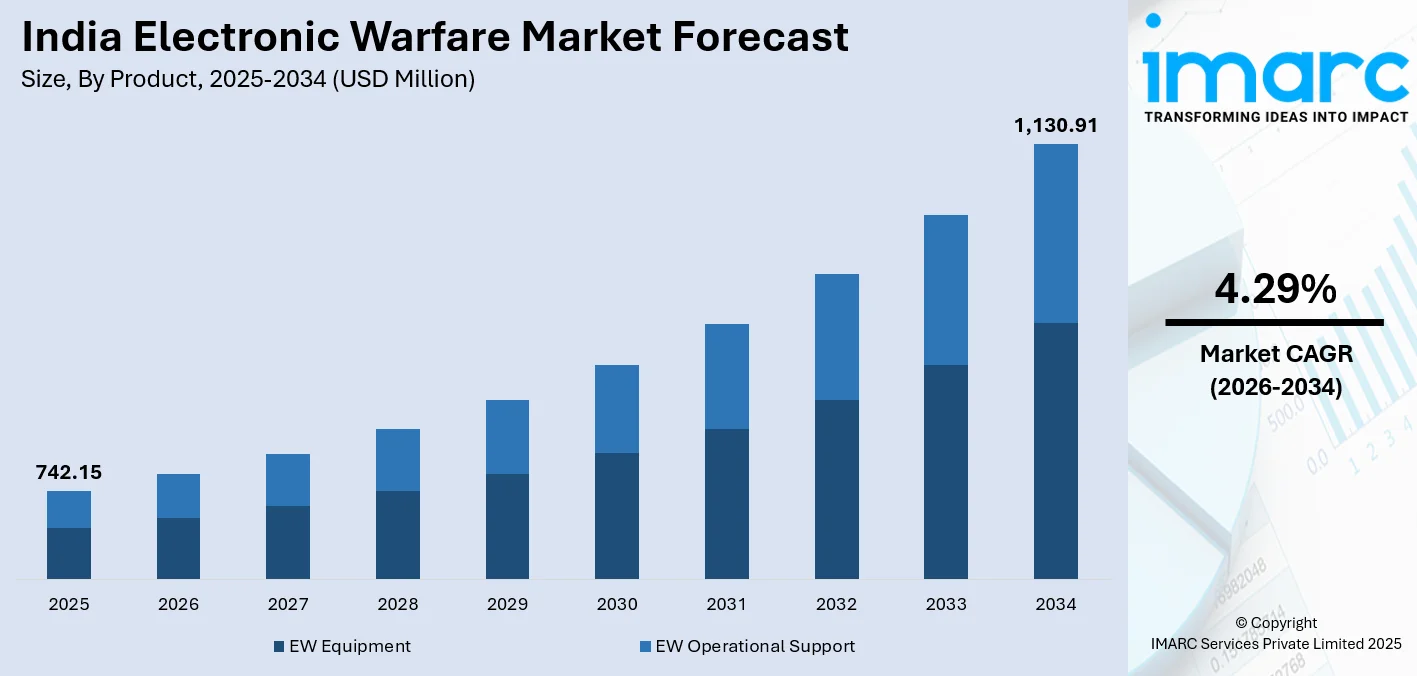

The India electronic warfare market size was valued at USD 742.15 Million in 2025 and is projected to reach USD 1,130.91 Million by 2034, growing at a compound annual growth rate of 4.29% from 2026-2034.

The India electronic warfare market is driven by rising geopolitical threats along sensitive borders and the urgent need to modernize military capabilities across all branches of the armed forces. Growing investments in indigenous defense technologies, government-backed indigenization programs, and expanding defense budgets are supporting sustained adoption across land, naval, airborne, and space platforms. These converging dynamics continue to reshape the India electronic warfare market share.

Key Takeaways and Insights:

- By Product: EW equipment dominates the market with the share of 74.5% in 2025, reflecting strong demand for active defense hardware deployed to detect, disrupt, and neutralize electromagnetic threats across all military platforms.

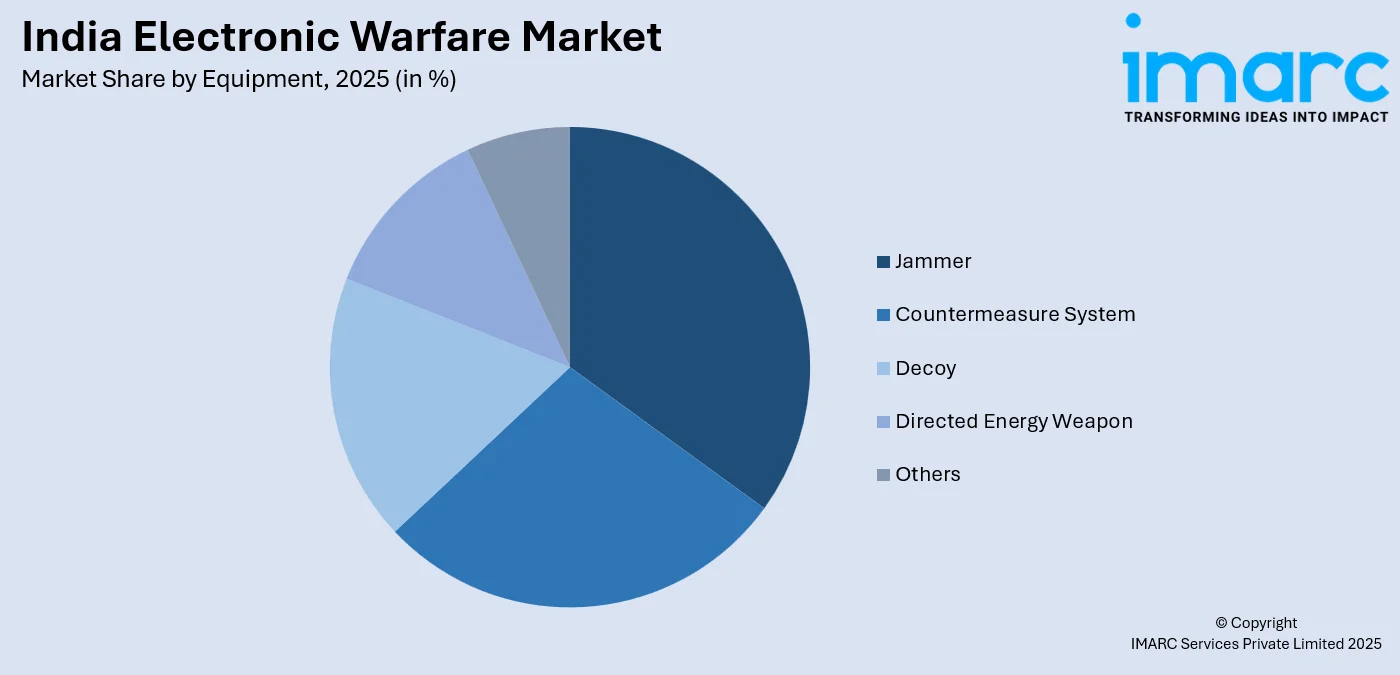

- By Equipment: Jammer leads the market with a share of 32.5% in 2025, driven by the growing requirement to disrupt adversarial communication and navigation systems in modern conflict scenarios across multiple operational theaters.

- By Capacity: Electronic support represents the largest segment with a market share of 36.8% in 2025, enabling armed forces to gather critical intelligence and maintain situational awareness across complex and evolving electromagnetic threat environments.

- By Platform: Land dominates the market with a share of 34.5% in 2025, supported by consistent demand for ground-based electronic warfare systems along extensive and strategically sensitive border regions.

- By Region: North India leads the market with a share of 31.5% in 2025, driven by its strategic proximity to disputed borders that require robust electronic surveillance, countermeasure, and disruption capabilities.

- Key Players: The India electronic warfare market features a competitive mix of public sector enterprises and private defense firms focused on developing indigenous solutions, securing government contracts, and expanding technology portfolios across multiple platforms.

To get more information on this market Request Sample

The India electronic warfare market is advancing rapidly as the country modernizes its armed forces to address growing multidimensional threats. Persistent border tensions, increasing digital warfare capabilities of adversaries, and the strategic imperative to reduce import dependency have driven substantial investments in indigenous electronic warfare development. For instance, in April 2025, Bharat Electronics Limited (BEL) signed a ₹2,210-crore contract with India’s Ministry of Defence to supply an indigenous Electronic Warfare (EW) Suite for Mi-17 V5 helicopters of the Indian Air Force, incorporating radar warning receivers, missile approach warning systems, and counter-measure dispensing systems to enhance aircraft survivability. The government's emphasis on Atmanirbhar Bharat has catalyzed collaboration between defense research institutions, public sector undertakings, and private manufacturers. Modernization programs spanning land, airborne, naval, and space platforms are creating sustained procurement demand. The proliferation of unmanned aerial systems, combined with evolving cyber-electronic warfare integration, is expanding the operational scope of EW systems.

India Electronic Warfare Market Trends:

Growing Indigenization of Electronic Warfare Capabilities

India's defense modernization strategy places significant emphasis on developing electronic warfare capabilities through domestic channels. Research institutions, public sector undertakings, and private industry partners collaborate to design and produce sophisticated systems tailored to national operational requirements. For instance, in February 2026, Amitec Electronics inaugurated a dedicated electronic warfare manufacturing facility at the Aligarh node of the Uttar Pradesh Defence Industrial Corridor with an investment of around ₹330 crore, aimed at strengthening domestic EW design and production capabilities. This indigenization drive reduces foreign technology dependency while building long-term industrial capacity and accelerating development timelines. The establishment of defense testing facilities for electronic warfare and the transfer of critical technology to domestic manufacturers are reinforcing self-reliance across India's defense electronics ecosystem.

Integration of Artificial Intelligence into EW Platforms

The incorporation of artificial intelligence into electronic warfare platforms is transforming how India's armed forces detect, classify, and counter electromagnetic threats. AI-enabled systems facilitate faster signal analysis, automated threat identification, and adaptive jamming responses, significantly improving situational awareness and operational response times. For instance, in July 2024, the Ministry of Defence approved several AI-enabled defence projects under the Innovations for Defence Excellence (iDEX) initiative, including solutions focused on electronic warfare signal intelligence and spectrum monitoring for the Indian Armed Forces. This technological integration enhances the operational effectiveness of both legacy and next-generation platforms deployed across multiple domains, driving adoption of software-defined EW architectures and supporting India electronic warfare market growth.

Expansion of Electronic Warfare Across Multi-Domain Platforms

India's electronic warfare capabilities are expanding beyond traditional land-based applications to encompass naval vessels, airborne platforms, and emerging space-based systems. This multi-domain approach reflects strategic recognition that modern conflicts require coordinated electronic operations across all operational environments. For instance, in March 2023, the Government of India approved the establishment of the Indian Air Force’s Integrated Air Command and Control System (IACCS) expansion under the Ministry of Defence to strengthen network-centric warfare capabilities, integrating sensors, electronic warfare inputs, and real-time battlefield data across air defence platforms. Investment in platform-specific EW suites and joint operational architectures is enabling more integrated and effective electromagnetic spectrum management, positioning India's armed forces for comprehensive electronic superiority in complex threat environments.

Market Outlook 2026-2034:

The India electronic warfare market is poised for significant revenue expansion through the forecast period, supported by continued government commitment to defense modernization and indigenization. The market's revenue trajectory reflects growing procurement of advanced jammers, electronic support measures, and countermeasure platforms across land, airborne, naval, and space domains. Increasing border security imperatives and rising adversarial electronic capabilities are reinforcing procurement urgency. The progressive integration of artificial intelligence directed energy systems, and satellite-based electronic warfare solutions is expected to unlock high-value growth opportunities, strengthening India's emergence as a globally competitive defense electronics manufacturing hub. With a strong order pipeline and expanding domestic industrial base, the market's long-term outlook remains highly positive. The market generated a revenue of USD 742.15 Million in 2025 and is projected to reach a revenue of USD 1,130.91 Million by 2034, growing at a compound annual growth rate of 4.29% from 2026-2034.

India Electronic Warfare Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

|

Product |

EW Equipment |

74.5% |

|

Equipment |

Jammer |

32.5% |

|

Capacity |

Electronic Support |

36.8% |

|

Platform |

Land |

34.5% |

|

Region |

North India |

31.5% |

Product Insights:

- EW Equipment

- EW Operational Support

The EW equipment dominates with a market share of 74.5% of the total India electronic warfare market in 2025.

EW equipment commands the dominant share of the India electronic warfare market, reflecting the fundamental importance of active hardware in modern defense operations. These systems encompass the full spectrum of electromagnetic tools deployed across military platforms to detect, disrupt, and neutralize adversarial threats. As India accelerates military modernization, the consistent prioritization of hardware procurement over support services reinforces sustained demand across land, airborne, naval, and space platforms, positioning EW Equipment as the primary market contributor.

The growing complexity of threat environments has further elevated demand for sophisticated EW hardware solutions, prompting large-scale procurement programs across all military branches. Defense budgets are increasingly directed toward advanced radar warning systems, jamming platforms, countermeasure dispensing systems, and electronic intelligence sensors. The alignment of government indigenization initiatives with armed forces modernization requirements has strengthened the procurement pipeline for EW equipment, ensuring this segment maintains its leadership position throughout the forecast period.

Equipment Insights:

Access the comprehensive market breakdown Request Sample

- Jammer

- Countermeasure System

- Decoy

- Directed Energy Weapon

- Others

The jammer leads with a share of 32.5% of the total India electronic warfare market in 2025.

Jammer dominates the Equipment segment of the India electronic warfare market, driven by the critical operational role these systems play in disrupting adversarial communications, radar functions, and navigation networks. Deployed across ground vehicles, aircraft, and naval vessels, jammers provide armed forces with the ability to degrade enemy situational awareness and impair coordinated offensive operations. Growing investment in next-generation jamming technologies, supported by government-funded development programs, continues to reinforce the segment's position as the leading equipment category.

The proliferation of unmanned aerial systems, advanced guided munitions, and sophisticated satellite navigation infrastructure among regional adversaries has amplified demand for high-performance jamming capabilities. India's armed forces are prioritizing deployments along sensitive border regions where signal disruption directly influences operational outcomes. The transition toward software-defined, broadband jamming architectures capable of targeting multiple frequency ranges simultaneously is further expanding the scope and value of jammer procurement across India's defense modernization programs.

Capacity Insights:

- Electronic Protection

- Electronic Support

- Electronic Attack

The electronic support dominates with a market share of 36.8% of the total India electronic warfare market in 2025.

Electronic Support commands the leading position within the Capacity segment, reflecting the foundational role passive intelligence-gathering capabilities play in modern military operations. These systems intercept, identify, and locate adversarial electromagnetic emissions without revealing the operator's presence, providing decision-makers with critical intelligence before and during engagements. India's armed forces depend heavily on electronic support measures for comprehensive threat awareness across sensitive borders, reinforcing consistent procurement of sensors, signal analysis platforms, and spectrum monitoring assets across multiple operational domains.

The evolution of India's threat environment has intensified operational reliance on electronic support capabilities that provide persistent, real-time insights into adversarial radar and communication infrastructure. Advanced signal exploitation technologies integrated with electronic support platforms enable faster and more accurate identification of hostile emitters, informing both defensive responses and offensive planning. Growing requirements for joint operational intelligence sharing across army, navy, and air force commands are further driving adoption of interoperable electronic support systems capable of functioning seamlessly across multi-domain operational architectures.

Platform Insights:

- Land

- Naval

- Airborne

- Space

The land leads with a share of 34.5% of the total India electronic warfare market in 2025.

Land represent the largest segment within the India electronic warfare market, underpinned by the country's extensive terrestrial border security requirements spanning multiple strategically sensitive theaters. Ground-deployed electronic warfare systems support army brigades, divisions, and corps with battlefield intelligence, signal disruption, and countermeasure capabilities essential to modern land operations. The ongoing modernization of India's ground forces, combined with the progressive induction of advanced battlefield surveillance systems, ensures sustained procurement demand for land-based electronic warfare solutions throughout the forecast period.

The high operational tempo maintained across India's land borders necessitates robust and field-deployable electronic warfare infrastructure capable of performing reliably in diverse geographical and climatic conditions. Investments in mobile and vehicle-mounted EW platforms that provide flexibility for rapid redeployment across operational theaters are intensifying. Integration of land-based electronic warfare systems with broader battlefield management networks is enhancing their operational value, enabling real-time intelligence sharing and coordinated electromagnetic operations that multiply the effectiveness of ground force deployments in contested environments.

Regional Insights:

- North India

- West and Central India

- South India

- East and Northeast India

North India exhibits a clear dominance with a 31.5% share of the total India electronic warfare market in 2025.

North India holds the largest regional share of the electronic warfare market, driven by the concentration of strategically vital military commands, air force stations, and forward-deployed army formations along some of India's most sensitive security corridors. The region's proximity to disputed territories requiring persistent electronic surveillance, countermeasure readiness, and signal disruption capability directly translates into high-priority procurement activity. Sustained government investment in border infrastructure and operational modernization programs continues to reinforce North India's leadership position across all electronic warfare platform categories.

The density of defense research facilities, testing ranges, and defense manufacturing support infrastructure in the northern region further strengthens its market contribution by enabling rapid development cycles and streamlined procurement logistics. Growing requirements for integrated multi-layered EW coverage along the region's strategic frontiers are driving demand for advanced systems capable of operating across land, airborne, and emerging space domains simultaneously. As India continues prioritizing defense preparedness in high-stakes border regions, North India is expected to maintain its dominant share throughout the forecast period.

Market Dynamics:

Growth Drivers:

Why is the India Electronic Warfare Market Growing?

Escalating Geopolitical Tensions and Border Security Imperatives

India's strategic environment is defined by persistent security challenges along its northern and western borders, creating sustained and non-negotiable demand for advanced electronic warfare capabilities. The presence of technologically sophisticated adversaries possessing modern radar systems, communication networks, and electronic attack capabilities has compelled India's armed forces to continuously upgrade their EW posture. Electronic warfare systems provide critical decision-making advantages through intelligence collection, signal disruption, and countermeasure deployment in operationally demanding environments. The recognition that electromagnetic spectrum dominance is a prerequisite for operational success has elevated electronic warfare from a supporting role to a central component of India's broader defense strategy, driving sustained procurement across land, airborne, naval, and emerging space domains, ensuring continued government prioritization of EW investments.

Government-Led Indigenization and Rising Defense Budgets

India's commitment to building a self-reliant defense industrial base through programs including Atmanirbhar Bharat and Make in India is a powerful catalyst for electronic warfare market growth. In 2025, the Indian Air Force issued a Request for Information (RFI) for 100 advanced ASPJ electronic warfare pods under its Super Sukhoi upgrade project, signaling an active push toward strengthening indigenous EW capabilities. The government has directed increasing proportions of the defense modernization budget toward domestic procurement, effectively channeling demand toward indigenous manufacturers and collaborative development programs. Defense Industrial Corridors in Uttar Pradesh and Tamil Nadu provide infrastructure that supports private sector participation in electronic warfare production. Positive indigenization lists restricting imports across hundreds of defense product categories further stimulate domestic market activity.

Adoption of Artificial Intelligence, Directed Energy, and Advanced Sensing Technologies

The integration of advanced technologies into electronic warfare systems is expanding capabilities and creating new procurement requirements across India's armed forces. In 2025, India successfully tested a 30 kW laser‑based directed energy weapon (DEW) system developed by the Defence Research and Development Organisation (DRDO), demonstrating its ability to disable drones and other aerial threats and showcasing a significant step toward indigenous directed energy capabilities. Artificial intelligence enables adaptive signal classification, automated threat response, and cognitive jamming that significantly improve system effectiveness compared to legacy platforms. Directed energy weapons offer speed-of-light engagement against drones, missiles, and communication infrastructure at lower per-engagement costs, driving growing interest from all defense services.. Advanced radar technologies, software-defined radio architectures, and multi-spectral sensing capabilities are enabling more comprehensive and resilient electromagnetic spectrum operations.

Market Restraints:

What Challenges the India Electronic Warfare Market is Facing?

Technological Complexity and High Development Costs

Developing advanced electronic warfare systems requires deep expertise in signal processing, semiconductor design, and system integration that demands significant research and manufacturing investment. High development costs combined with extended deployment timelines create financial and scheduling pressures for government agencies and industry partners alike. Persistent gaps in certain critical technology domains necessitate continued reliance on international collaborations, introducing procurement complexity and constraining the pace at which India can independently develop and field next-generation electronic warfare capabilities aligned with evolving operational requirements.

Electromagnetic Spectrum Management Challenges

Modern electronic warfare operations require precise coordination of electromagnetic spectrum usage to prevent interference between friendly systems and ensure operational effectiveness. Growing congestion from both military and civilian sources complicates mission planning and system deployment in contested environments. The absence of fully integrated spectrum management frameworks across India's joint forces adds operational complexity, potentially limiting the seamless employment of electronic warfare assets and reducing the coordinated effectiveness of multi-domain electromagnetic operations during complex military engagements.

Supply Chain Vulnerabilities and Import Dependencies

Despite significant indigenization progress, India's electronic warfare sector remains dependent on imported components including advanced semiconductors, specialized sensors, and high-frequency electronic subsystems. Global supply chain disruptions can delay procurement timelines and increase system costs, creating operational readiness risks for the armed forces. Developing robust domestic supply chains for critical electronic components requires sustained long-term investment and extended development periods, representing an ongoing structural challenge for India's defense electronics sector during its transition toward comprehensive self-sufficiency.

Competitive Landscape:

The India electronic warfare market features a competitive structure centered around government-owned defense enterprises, defense research institutions, and a growing private sector ecosystem. Public sector undertakings play a dominant role through established manufacturing capabilities, long-standing relationships with armed forces, and capacity for large-scale government contracts. Defense research laboratories contribute critical technology through indigenous systems and technology transfer agreements that enable industry-scale production. Private companies, including startups and MSMEs, are participating through innovation frameworks and procurement programs that actively encourage domestic solutions. Competition is intensifying as the government diversifies procurement sources and expands indigenization frameworks. Companies are differentiating through platform-specific expertise, software-defined architectures, multi-domain integration capabilities, and comprehensive lifecycle support services that provide strong value propositions to defense customers, reflecting India's transition toward a mature and self-reliant defense electronics industrial base.

Recent Developments:

- In February 2026, Defence Research and Development Organisation (DRDO) awarded a ₹30.01-crore contract to Unistring Tech Solutions, a subsidiary of Zen Technologies, to develop an advanced electronic warfare system. The project aims to strengthen India’s indigenous defence electronics capabilities and supports the government’s Atmanirbhar Bharat and Make-in-India initiatives focused on reducing reliance on imported EW technologies.

India Electronic Warfare Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Products Covered | EW Equipment, EW Operational Support |

| Equipments Covered | Jammer, Countermeasure System, Decoy, Directed Energy Weapon, Others |

| Capacities Covered | Electronic Protection, Electronic Support, Electronic Attack |

| Platforms Covered | Land, Naval, Airborne, Space |

| Regions Covered | North India, West and Central India, South India, East and Northeast India |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Electronic Warfare Market Report

The India electronic warfare market size was valued at USD 742.15 Million in 2025.

The India electronic warfare market is expected to grow at a compound annual growth rate of 4.29% from 2026-2034 to reach USD 1,130.91 Million by 2034.

EW Equipment dominates India's electronic warfare market, driven by accelerating military modernization and sustained hardware procurement across land, airborne, naval, and space platforms to detect, disrupt, and neutralize adversarial threats.

Key factors driving the India electronic warfare market include escalating border security imperatives, rising defense budgets, government indigenization mandates under Atmanirbhar Bharat, artificial intelligence integration, growing multi-domain platform requirements, and sustained procurement across land, airborne, naval, and space operational domains.

Major challenges include high system development costs, technological complexity in critical electronic subsystems, electromagnetic spectrum management constraints, supply chain dependencies on imported semiconductor components, and extended timelines for delivering indigenously developed electronic warfare capabilities to operational deployment readiness.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)