India Elevator and Escalator Market Size, Share, Trends and Forecast by Type, Service, End Use, and Region, 2026-2034

India Elevator and Escalator Market Size, Share, Trends & Forecast (2026-2034)

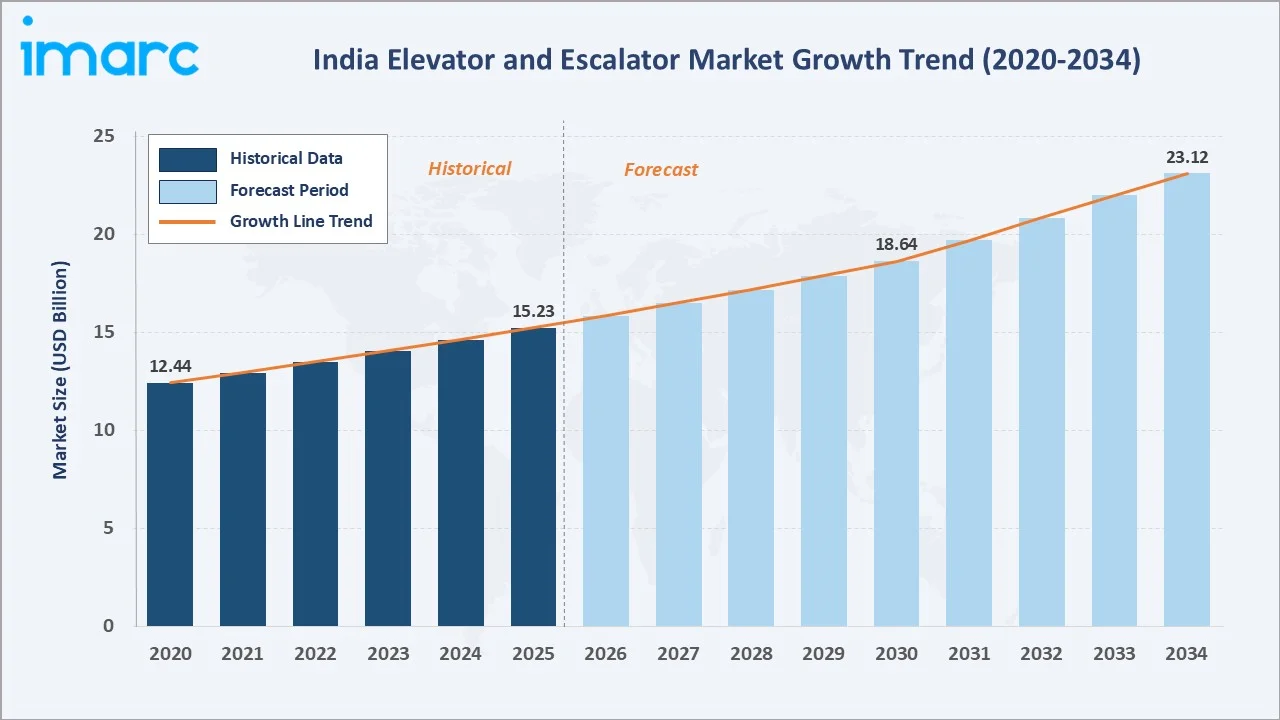

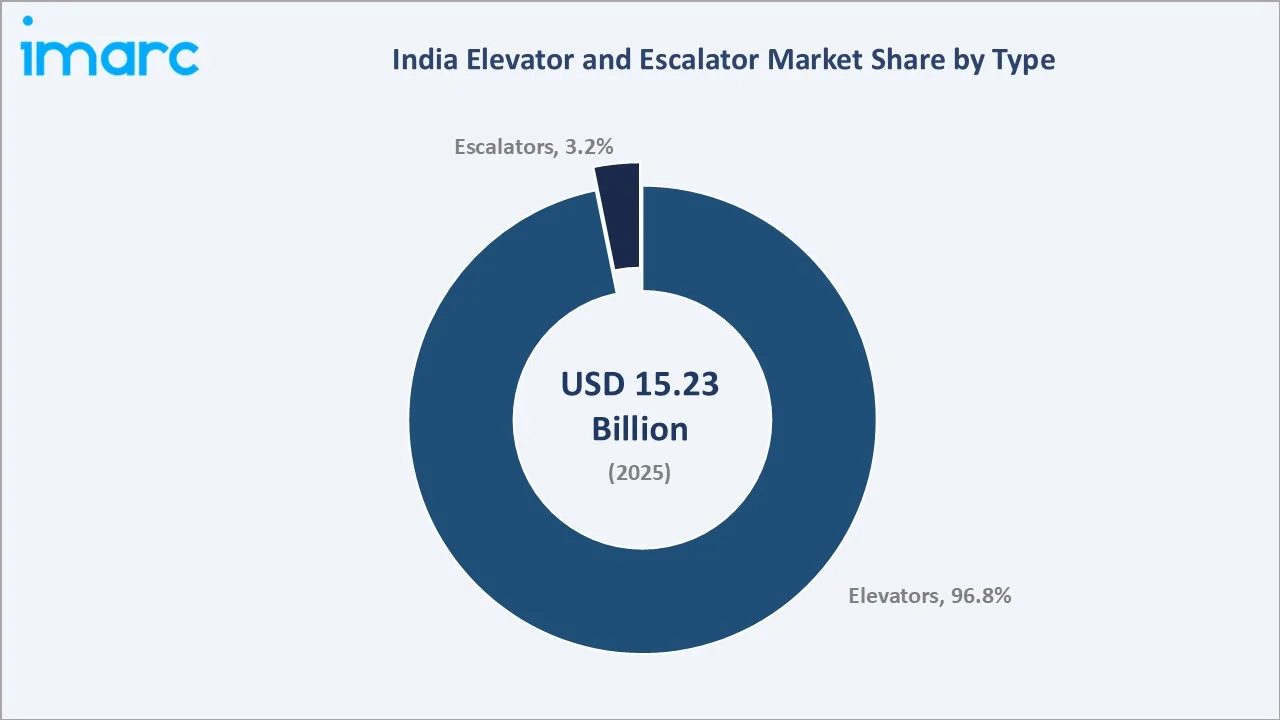

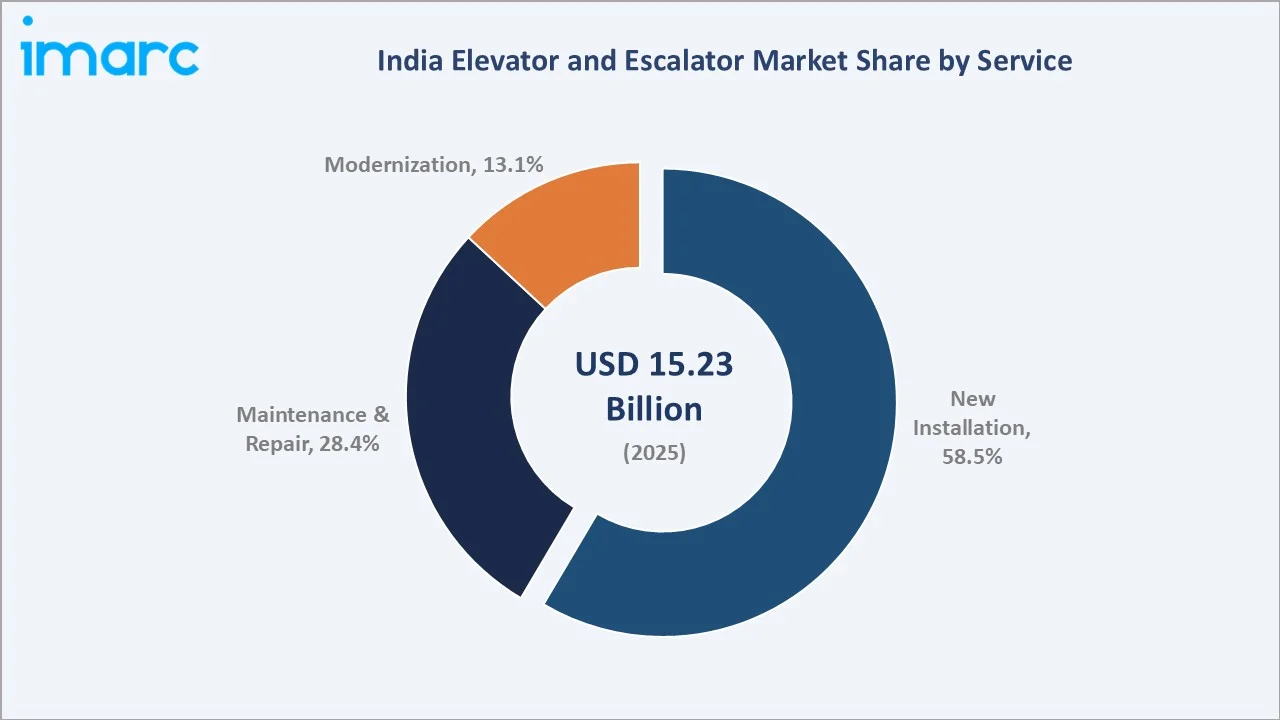

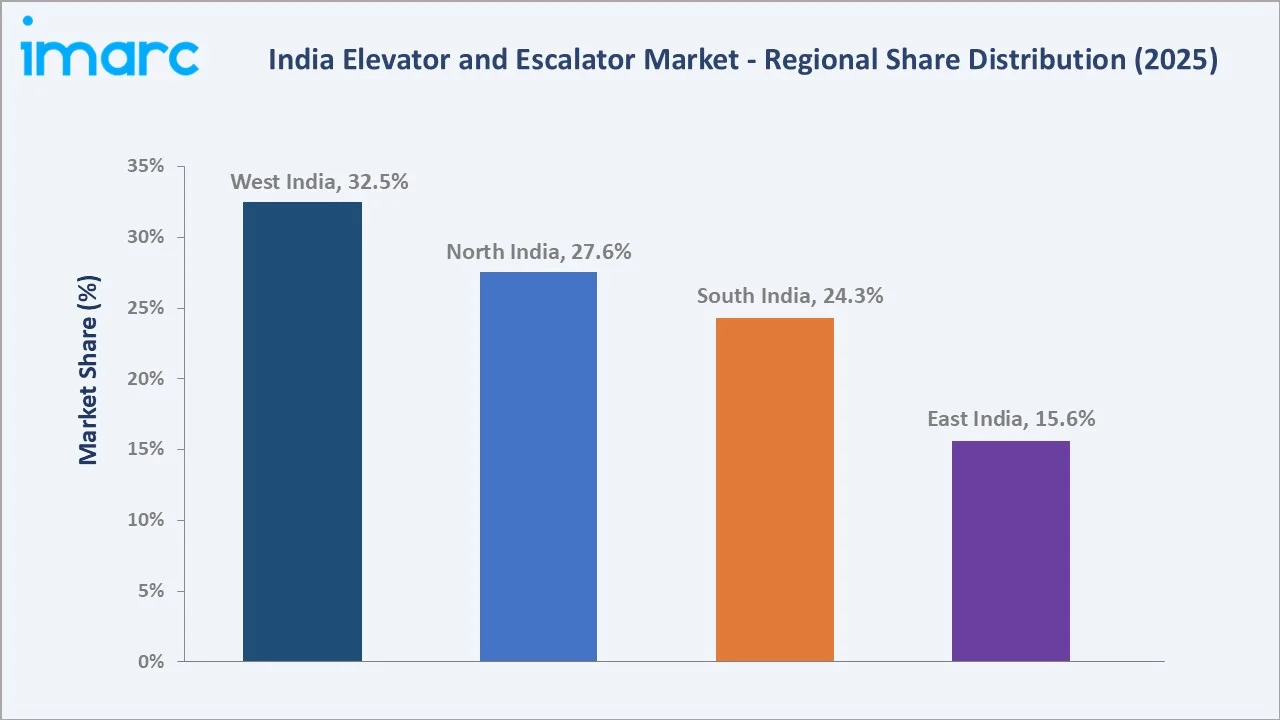

The India elevator and escalator market size was valued at USD 12.44 Billion in 2020 and reached USD 15.23 Billion in 2025. The market is projected to reach USD 18.64 Billion by 2030 and USD 23.12 Billion by 2034, growing at a CAGR of 4.13% during 2026-2034. Growth is driven by rapid urbanization, metro rail expansion, smart city investments, and rising demand for high-rise residential and commercial complexes. Elevators dominate with a 96.8% share in 2025, while New Installations contribute 58.5% of the service mix. West India leads with a 32.5%.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 15.23 Billion |

|

Forecast Market Size (2034) |

USD 23.12 Billion |

|

CAGR (2026-2034) |

4.13% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

West India (32.5% share, 2025) |

|

Fastest Growing Region |

South India |

|

Leading Type Segment |

Elevators (96.8%, 2025) |

|

Leading Service Segment |

New Installation (58.5%, 2025) |

The chart below illustrates India elevator and escalator market growth from 2020 to 2034, supported by sustained demand from real estate construction, metro rail rollouts, and modernization activity across cities.

To get more information on this market, Request Sample

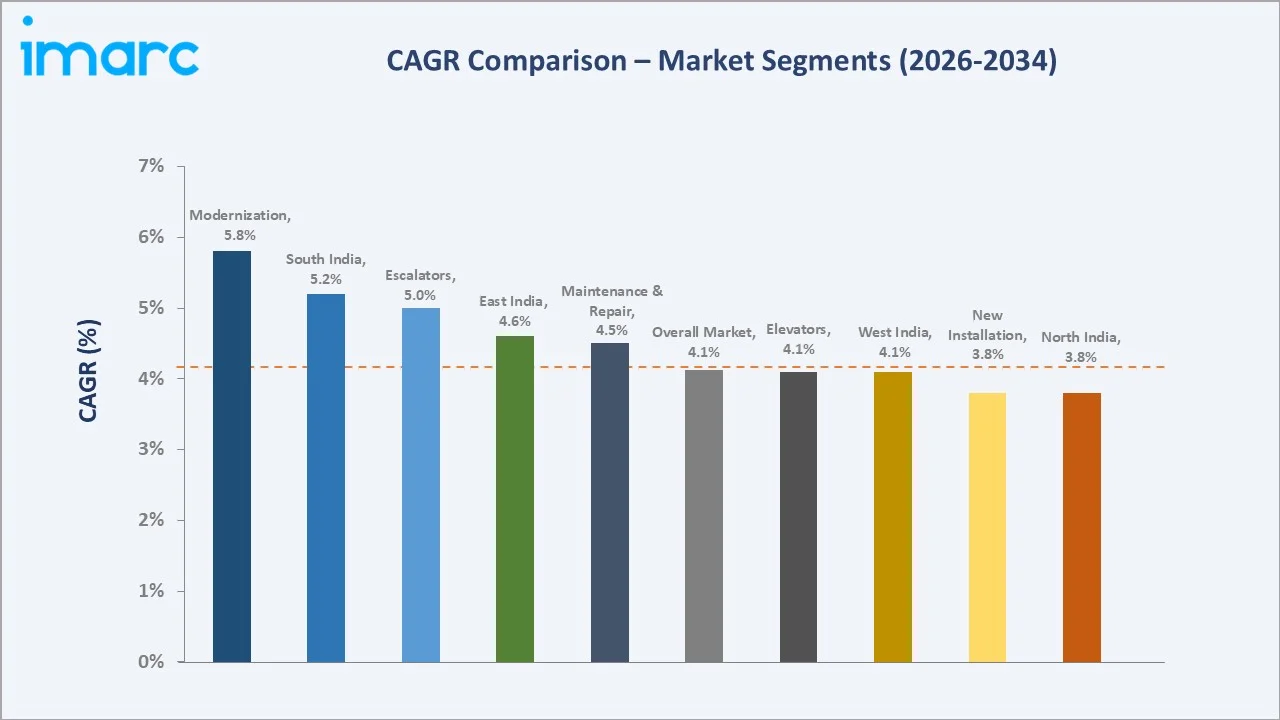

CAGR analysis indicates that elevators and the new installation service segment will lead growth through 2034, supported by ongoing infrastructure activity across Tier-1 and Tier-2 cities.

Executive Summary

The India elevator and escalator market is undergoing structural expansion, driven by accelerating urbanization, vertical real estate development, and metro rail investments. Valued at USD 15.23 Billion in 2025, the market is projected to reach USD 23.12 Billion by 2034, expanding at a CAGR of 4.13%, supported by Smart Cities Mission funding, growing high-rise housing stock, and rising service contract penetration.

Elevators dominate the type segment with a 96.8% share in 2025, while escalators contribute 3.2%, primarily concentrated in metros, malls, and airports. Within services, new installation leads at 58.5% in 2025, supported by ongoing residential and commercial construction. Maintenance and repair contribute 28.4%, while modernization holds 13.1% as building owners upgrade aging units to current safety norms.

Regionally, West India leads with a 32.5% share in 2025, anchored by Mumbai and Pune real estate. North India follows at 27.6%, supported by Delhi-NCR. South India holds 24.3% and is the fastest-growing region, propelled by Bengaluru and Chennai metro projects. East India contributes 15.6%, with Kolkata leading demand.

Key Market Insights

|

Insight |

Data |

|

Largest Type Segment |

Elevators – 96.8% share (2025) |

|

Smaller Type Segment |

Escalators – 3.2% share (2025) |

|

Leading Service Segment |

New Installation – 58.5% share (2025) |

|

Second Service Segment |

Maintenance and Repair – 28.4% (2025) |

|

Leading Region |

West India – 32.5% (2025) |

|

Fastest Growing Region |

South India – metro & IT hub demand |

|

Top Companies |

KONE Corporation, Otis Elevator Company (I). Ltd., Schindler, Johnsonlifts, Mitsubishi Elevator India Pvt Ltd, and Hitachi Lift India Pvt. Ltd. |

|

Forecast CAGR (2026–2034) |

4.13% |

Key Analytical Observations Supporting The Data Above:

- Elevators’ 96.8% share in 2025 reflects their universal use across residential apartments, offices, hospitals, and metro stations, where vertical movement of people is essential.

- Escalators at 3.2% in 2025 remain niche, concentrated in airports, shopping malls, and metro rail. Metro projects in Bengaluru, Hyderabad, and Mumbai are the main demand pockets.

- New Installation at 58.5% in 2025 highlights India’s strong construction pipeline, with millions of new housing units and large commercial developments added every year.

- West India’s 32.5% share reflects dense commercial and residential construction in Mumbai, Pune, Ahmedabad, and Surat, supported by leading developers and builder associations.

- South India’s position as fastest growing region is underpinned by metro rail expansion in Bengaluru and Chennai, IT park construction, and rapid urbanization in Tier-2 cities.

- Global majors KONE, Otis, and Schindler, along with Johnson Lifts, dominate the competitive landscape and collectively account for most of the new installation revenue in 2025.

India Elevator and Escalator Market Overview

Elevators and escalators are vertical and inclined transportation systems designed to move people and goods across multi-storey buildings, transit hubs, and public infrastructure. The Indian ecosystem includes raw material suppliers, component manufacturers, OEMs, EPC contractors, builders, service providers, and end users.

Applications span residential towers, IT parks, shopping malls, hospitals, hotels, metro stations, and airports. Macroeconomic drivers include India’s urbanization rate, expected to cross 40% by 2030, growing real estate investment of more than USD 5 Billion annually, government-led infrastructure push, and rising disposable incomes fueling premium high-rise demand.

Market Dynamics

To evaluate market opportunities, Request Sample

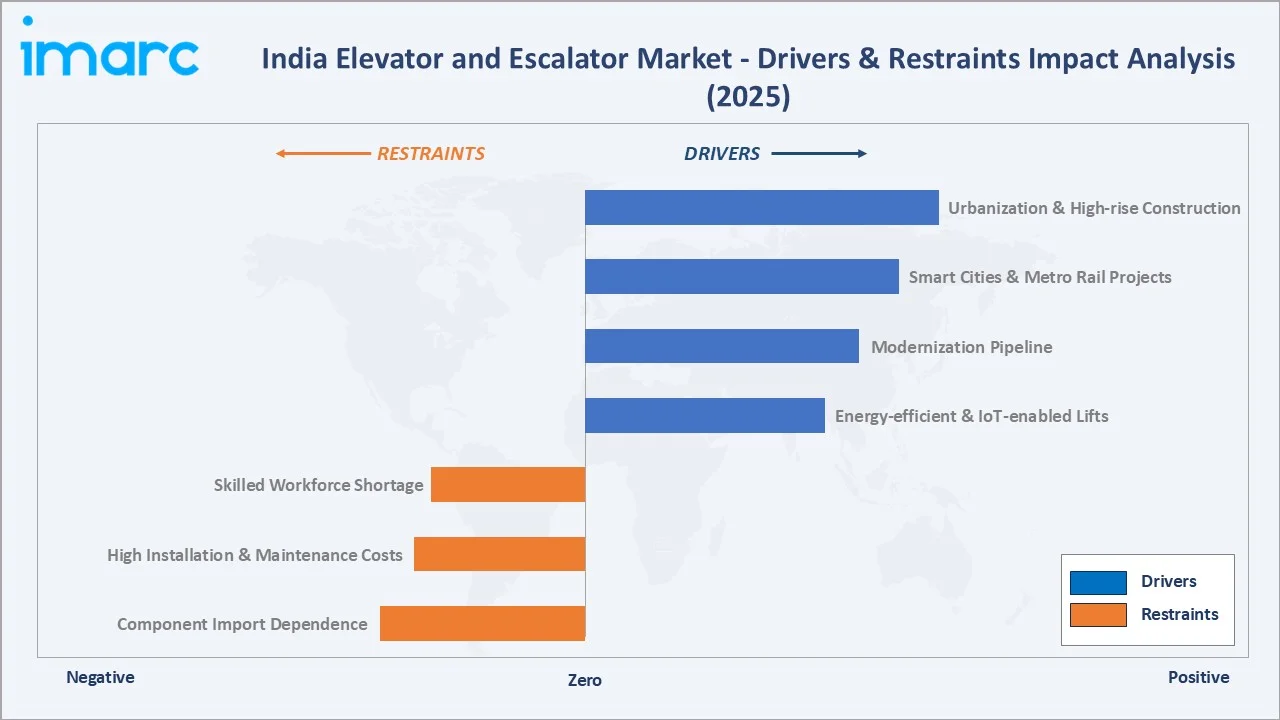

Market Drivers

- Rapid Urbanization and High-rise Construction: India’s urban population is projected to reach 600 million by 2030. Mumbai Metropolitan Region will see 34 per cent growth in skyscrapers, with over 40 floors, each requiring multiple elevators.

- Smart Cities Mission and Metro Rail Expansion: The 94% of the total 8,067 projects under Smart Cities Mission have been completed, with ₹1.64 lakh crore invested, while operational metro length crossed 1,000 km in 2025. Each metro station typically deploys multiple escalators and elevators.

- Rising Demand for Energy-efficient and IoT-enabled Lifts: Building owners are adopting regenerative drives, MRL elevators, and IoT-enabled systems to reduce energy use and improve efficiency. Regenerative technologies alone can save around 20–35% energy, while smart systems enable monitoring, predictive maintenance, and optimized performance.

- Expanding Modernization Pipeline: Elevator modernization in India is rising due to aging infrastructure, urbanization, and safety compliance needs. With elevators typically lasting 20–30 years, upgrading controllers, drives, and systems improves efficiency and aligns with building codes, driving strong modernization demand growth.

Market Restraints

- High Installation and Maintenance Costs: Elevator installation costs vary widely based on type, capacity, and technology, often making advanced systems expensive for smaller developers. High ongoing maintenance and servicing costs further increase lifecycle expenses, limiting adoption in price-sensitive Tier-2 and Tier-3 markets.

- Component Import Dependence: India’s elevator industry depends on imported components such as advanced control systems, drives, and precision parts. This reliance exposes manufacturers to currency fluctuations and global supply chain disruptions, as seen during recent logistics constraints and semiconductor shortage.

- Skilled Workforce Shortage: The elevator sector faces a shortage of trained installation and maintenance technicians in India. Limited availability of certified professionals affects service quality and timely maintenance, posing challenges for OEMs as demand for elevators and escalators continues to grow.

Market Opportunities

- Tier-2 and Tier-3 City Expansion: Rapid urbanization and housing demand in Tier-2 and Tier-3 cities such as Jaipur, Lucknow, and Coimbatore are driving mid-rise construction. This creates strong demand for cost-effective elevators, offering growth opportunities for value-focused OEMs in emerging urban markets.

- Government Mandated Modernization: State-level regulations such as Maharashtra Lift Act mandate stricter safety compliance and periodic inspections. These rules are encouraging upgrades of aging systems, generating sustained demand for modernization services and aftermarket maintenance contracts.

- Senior Living and Healthcare Demand: India’s senior population is projected to reach 194 million by 2031. Senior living projects and tier-1 hospitals are driving demand for advanced safety, hygiene, and accessibility features.

Market Challenges

- Long Approval and Permitting Timelines: Elevator approvals in India require inspections and licensing by state authorities, often causing project delays. While timelines vary by state, regulatory procedures and compliance requirements can slow installation and commissioning, impacting project completion schedules.

- Margin Compression in Maintenance: Competition from independent service providers and unorganized contractors is intensifying in India’s elevator maintenance market. This pricing pressure is reducing margins for OEMs, particularly in smaller cities, where cost-sensitive customers often prioritize low-cost annual maintenance contracts over branded services.

- Safety Incidents and Regulatory Scrutiny: Rising elevator safety concerns in India have led to stricter inspections and enforcement of safety norms under the Bureau of Indian Standards and state regulations. Compliance requirements, including safety devices and regular audits, are increasing operational costs for operators.

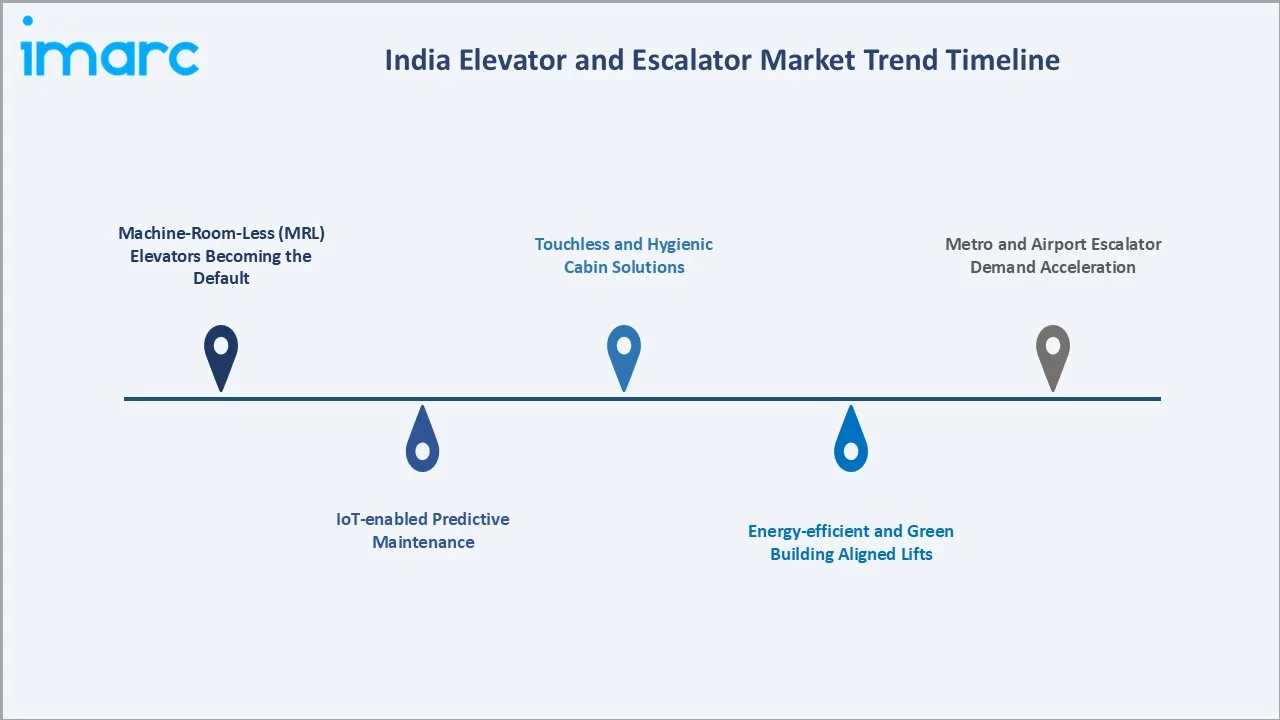

Emerging Market Trends

1. Machine-Room-Less (MRL) Elevators Becoming the Default

Machine-room-less (MRL) elevators are increasingly preferred in urban India due to space efficiency and lower energy consumption. While exact share varies by project, MRL systems dominate new mid- and high-rise installations, offering reduced footprint, flexible design, and improved efficiency compared to conventional traction elevators.

2. IoT-enabled Predictive Maintenance

OEMs such as KONE Corporation, Otis Worldwide Corporation, and Schindler Group deploy IoT-enabled platforms for remote monitoring and predictive maintenance. These systems improve uptime, enable real-time diagnostics, and reduce service disruptions, enhancing lifecycle efficiency and maintenance planning across elevator portfolios.

3. Touchless and Hygienic Cabin Solutions

Post-COVID-19, demand for touchless elevator technologies such as mobile-based controls, voice commands, and antimicrobial surfaces has increased, particularly in healthcare and commercial buildings. OEMs introduced digital and contactless solutions to improve safety, hygiene, and user confidence in shared mobility infrastructure.

4. Energy-efficient and Green Building Aligned Lifts

Energy-efficient elevators with regenerative drives, LED lighting, and standby modes are increasingly specified in green buildings. These features significantly reduce power consumption and support certification standards such as Indian Green Building Council and Leadership in Energy and Environmental Design, widely adopted in India’s commercial real estate sector.

5. Metro and Airport Escalator Demand Acceleration

Expansion of metro rail and airport infrastructure in India is driving escalator demand. India’s metro network is expected to reach 2,000 km by 2030, while projects led by Airports Authority of India and metro rail corporations require large-scale deployment of heavy-duty escalators.

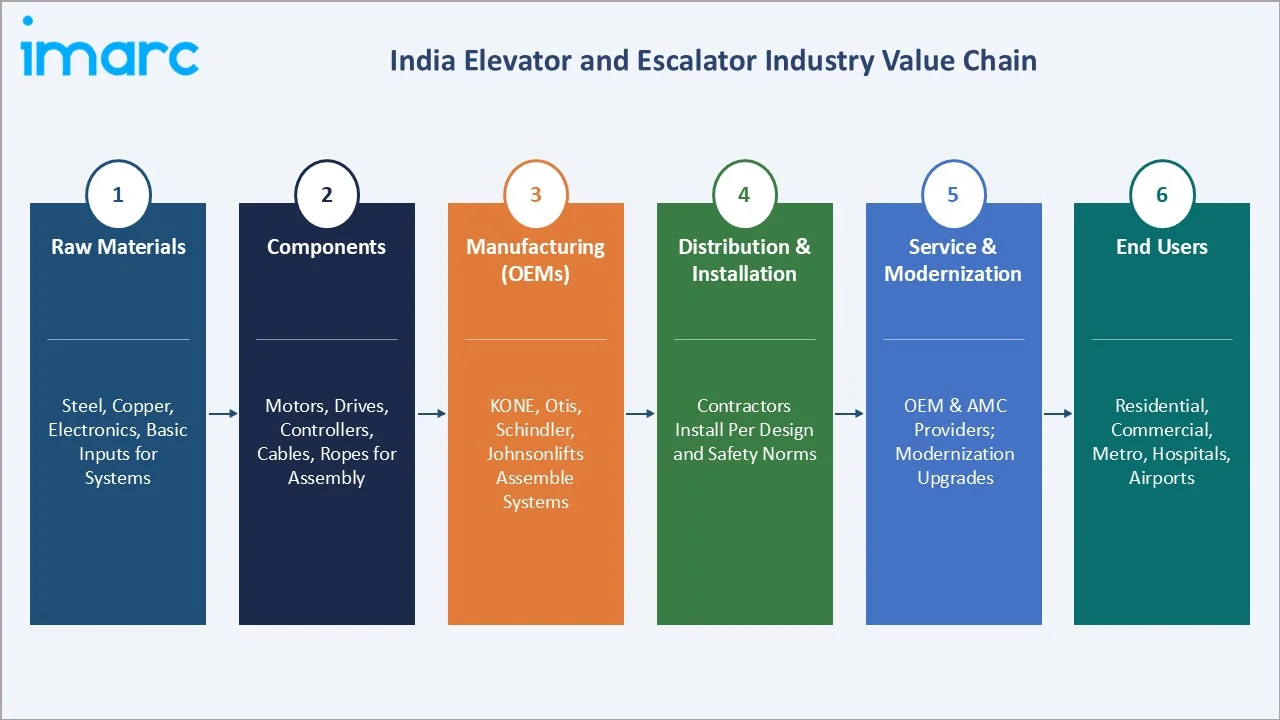

Industry Value Chain Analysis

The India elevator and escalator value chain comprises six interconnected stages, each with distinct margin structures, technology requirements, and competitive dynamics across the industrial ecosystem.

|

Stage |

Key Players / Examples |

|

Raw Materials |

Basic inputs like steel, copper, and electronics are sourced to produce elevator and escalator systems |

|

Components |

Specialized components including motors, drives, controllers, cables, and ropes are manufactured for assembly into systems |

|

Manufacturing (OEMs) |

Components are assembled into complete elevators and escalators, integrating mechanical, electrical, and software systems efficiently |

|

Distribution & Installation |

Finished systems are distributed through contractors and installed at sites following design and safety specifications |

|

Service & Modernization |

Maintenance services ensure operational efficiency, while modernization upgrades improve performance, safety, and extend equipment lifecycle |

|

End Users |

Elevators and escalators are used across residential, commercial, and infrastructure buildings for efficient vertical transportation |

Tier-1 OEMs capture the highest value by integrating manufacturing, installation, and lifetime service. Service contracts often deliver higher margins than new equipment sales, making installed-base scale a critical competitive moat.

Technology Landscape in the Industry

Drive and Motor Technology

Permanent-magnet synchronous gearless motors are widely adopted in modern elevators due to higher efficiency, smoother operation, and reduced maintenance. Compared to geared systems, they significantly lower energy consumption and improve ride quality, making them standard in premium and high-rise installations.

Materials Innovation

Innovations in materials such as high-strength steel ropes and lightweight components reduce elevator weight and energy consumption. Technologies like KONE UltraRope enable longer travel distances and improved efficiency, supporting high-rise building development globally, including in India.

Smart Connectivity and IoT

Cloud-connected elevator systems enable real-time monitoring and predictive maintenance. Platforms like KONE 24/7 Connected Services and Otis ONE enhance uptime, reduce unexpected failures, and support data-driven maintenance planning across elevator portfolios.

Automation and Destination Control

Destination control systems optimize elevator usage by grouping passengers based on destinations, improving traffic flow and reducing waiting times. These systems are increasingly deployed in commercial buildings, IT parks, and mixed-use developments to enhance efficiency and passenger experience.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Type | Elevators | 96.8% | 2025 |

| Service | New Installation | 58.5% | 2025 |

| End Use | Residential | 67.8% | 2025 |

| Region | West India | 32.5% | 2025 |

By Type

Elevators dominate the India market with a 96.8% share in 2025, driven by their universal application in residential, commercial, healthcare, and hospitality buildings. Demand is anchored by ongoing high-rise construction across Mumbai, Bengaluru, Delhi-NCR, and Hyderabad, supported by RERA-led project formalization.

To access detailed market analysis, Request Sample

Escalators contribute 3.2% in 2025, with demand concentrated in airports, metro rail networks, and large-format retail. Bengaluru, Mumbai, Hyderabad, and Chennai metro projects are the largest single demand pockets, with each station typically requiring multiple escalators.

By Service

New installation leads the service segment with a 58.5% share in 2025, reflecting India’s strong real estate pipeline and metro project rollouts. Builders typically order elevators in bulk during the structural completion phase, making this the largest revenue pool for OEMs.

Maintenance and repair hold 28.4% in 2025, anchored by long-term AMCs that offer recurring revenue across the installed base. Modernization, at 13.1%, is the fastest growing service line, driven by aging lift stock and stricter state safety regulations.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

West India |

32.5% |

Mumbai & Pune high-rise pipeline, MMR metro expansion, Gujarat industrial corridors, premium real estate demand |

|

North India |

27.6% |

Delhi-NCR commercial hubs, Noida & Gurugram office towers, Chandigarh tri-city growth, expanding metro rail |

|

South India |

24.3% |

Bengaluru & Hyderabad IT parks, Chennai metro, Kochi infrastructure, fastest-growing residential demand |

|

East India |

15.6% |

Kolkata residential & retail expansion, Bhubaneswar smart city projects, growing Tier-2 city construction |

West India commands the largest 32.5% share in 2025, anchored by Mumbai’s vertical real estate landscape, Pune’s IT-led commercial growth, and Gujarat’s industrial belt. The Mumbai Metropolitan Region alone accounts for the highest density of skyscrapers in India.

North India follows with 27.6% in 2025, driven by Delhi-NCR’s commercial real estate, Noida’s IT and data center construction, and the expanding Delhi Metro footprint. South India at 24.3% is the fastest-growing region, fueled by metro rail rollout in Bengaluru and Chennai, alongside large Hyderabad tech park developments. East India holds 15.6% in 2025, with growth concentrated in Kolkata’s residential redevelopment and Bhubaneswar’s smart city investments. Tier-2 cities such as Patna, Ranchi, and Guwahati are emerging as new demand pockets supported by hospital, hotel, and retail construction over the forecast period.

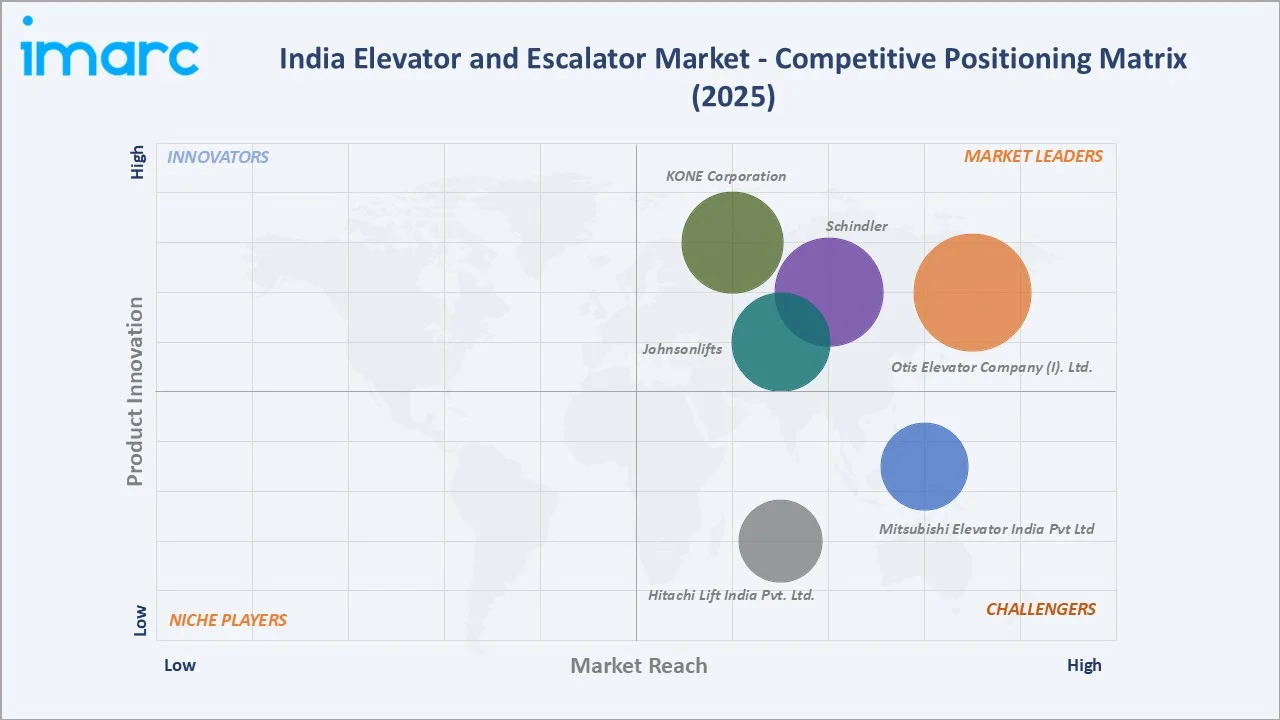

Competitive Landscape

|

Company Name |

Key Brand |

Market Position |

Core Strength |

|

KONE Corporation |

KONE |

Leader |

Energy-efficient MRL portfolio, IoT services |

|

Otis Elevator Company (I). Ltd. |

Otis, Gen2, Otis Robust, Gen3 Edge, Gen2 Life |

Leader |

Global scale, premium high-rise installations |

|

Schindler |

Schindler |

Leader |

Metro & airport escalator strength |

|

Johnsonlifts |

Nextra, Sukranti, Enduronic |

Leader |

Largest Indian OEM, deep distribution |

|

Mitsubishi Elevator India Pvt Ltd |

Mitsubishi, NEXIEZ |

Challenger |

Reliability, premium commercial focus |

|

Hitachi Lift India Pvt. Ltd. |

Hitachi |

Challenger |

Japanese engineering, hospital & metro |

The India elevator and escalator market combines global leaders with strong domestic challengers. KONE Corporation, Otis Elevator Company (I). Ltd., Schindler, and Johnsonlifts together account for most of the new installation revenue in 2025, leveraging large installed bases, strong brand recall, and pan-India service networks supporting premium and mid-segment projects.

Key Company Profiles

KONE Corporation

KONE Corporation, headquartered in Finland, operates in India through KONE Elevator India Private Limited, with a strong base in Chennai. The company supports urban infrastructure through manufacturing, R&D, and service operations, catering to residential, commercial, and infrastructure projects across metro and emerging cities.

- Product & Service Portfolio: KONE offers elevators, escalators, and moving walks, along with maintenance, modernization, and digital solutions such as 24/7 Connected Services and DX-class smart elevators for residential, commercial, and infrastructure applications.

- Recent Developments: In 2026, KONE Corporation announced an agreement to combine with TK Elevator in a €29.4 billion deal. The merged entity will strengthen global service, modernization, and digital capabilities, with €20.5 billion revenue and enhanced innovation and maintenance network scale.

- Strategic Focus: KONE focuses on digitalization, energy-efficient solutions, and expanding local manufacturing and R&D capabilities in India to support urbanization and smart building ecosystems.

Otis Elevator Company (I). Ltd.

Otis Elevator Company (I). Ltd., a subsidiary of Otis Worldwide Corporation, operates manufacturing and engineering facilities in Bengaluru. With a long presence in India, Otis serves residential, commercial, infrastructure, and transit segments, supported by an extensive service network across metropolitan and emerging urban markets.

- Product & Service Portfolio: Otis offers Gen2, Gen3, and SkyRise elevators, escalators and moving walks, alongside maintenance, modernization, and digital solutions such as the Otis ONE IoT platform and SkyBuild construction elevators.

- Recent Developments: In 2025, Otis Worldwide Corporation announced expansion of manufacturing capacity in India, its fastest-growing market, while advocating stricter safety regulations. The company also highlighted rising modernization demand and focus on affordability, energy efficiency, and safety across its expanding operations in over 800 cities.

- Strategic Focus: Otis focuses on expanding connected services, increasing modernization penetration, and strengthening service network density to drive recurring revenue and long-term customer retention in India.

Schindler

Schindler in India, a subsidiary of Schindler Group, operates manufacturing facilities in Pune and a nationwide service network. Headquartered in Mumbai, the company serves residential, commercial, and infrastructure sectors, with strong participation in metro rail and airport mobility projects across India’s expanding urban landscape.

- Product & Service Portfolio: Schindler offers elevator ranges such as 3300, 5500, and 7000, escalators including 9300 and 9700, along with maintenance, modernization, and digital solutions like Schindler Ahead for remote monitoring and predictive servicing.

- Recent Developments: In 2026: Schindler India Private Limited launched a new range of customizable elevator interiors featuring diverse materials, colours, and themed designs. The rollout enables architects and developers to integrate aesthetics with functionality, enhancing passenger experience while maintaining performance, reliability, and design flexibility in modern buildings.

- Strategic Focus: Schindler focuses on infrastructure-led growth, digital service platforms, and high-rise residential solutions, strengthening its position in metro, airport, and urban development projects across India.

Market Concentration Analysis

The India elevator and escalator market is moderately concentrated. The top players, KONE Corporation, Otis Elevator Company (I). Ltd., Schindler, and Johnsonlifts, collectively account for an estimated 60–65% of new installation revenue in 2025, supported by manufacturing scale, brand strength, and pan-India service networks.

Fragmentation increases at the regional and Tier-2 level. Independent service providers and smaller OEMs such as Express Lifts, Omega, and Blue Star compete on price and proximity, particularly in maintenance contracts for older mid-rise buildings.

Consolidation is visible in-service contracts, with leading OEMs targeting bolt-on acquisitions of regional service firms to expand installed base coverage. Stricter safety norms and IoT investment requirements are progressively tilting market share towards organized OEMs through the forecast period.

Investment & Growth Opportunities

Fastest-Growing Segments

Modernization is a major growth driver in India’s elevator market due to aging installations and tightening safety regulations. While exact installed base figures vary, a significant portion of elevators require upgrades to controls, drives, and safety systems. Escalator demand is also rising strongly, supported by metro rail expansion, airport development under Airports Authority of India, and growth in retail infrastructure across urban centres.

Emerging Geographic Markets

Tier-2 and Tier-3 cities such as Indore, Lucknow, and Coimbatore are witnessing strong construction growth. Increasing urbanization, rising incomes, and expansion of residential and commercial real estate are creating new demand for elevator installations, positioning these cities as major future growth markets in India.

Strategic and Venture Investment Trends

Investments are increasing in digital elevator solutions, including IoT-enabled monitoring, predictive maintenance, and smart building integration. Global OEMs are also expanding manufacturing and R&D capabilities in India to support domestic demand and position the country as a cost-effective export and sourcing hub.

Future Market Outlook (2026-2034)

The India elevator and escalator market forecast points to sustained expansion from USD 15.23 Billion in 2025 to USD 23.12 Billion by 2034, at a CAGR of 4.13%. Growth will be powered by urbanization, metro rollouts, smart city investments, and a structural pipeline of modernization activity.

Three transformations will reshape the market through 2034. Connected, IoT-enabled elevators will become default in metro projects, predictive maintenance will displace reactive servicing, and energy-efficient gearless drives will dominate new installations. Together, these shifts will improve safety, lower lifecycle costs, and elevate user experience.

By 2034, India’s elevator and escalator industry is expected to evolve into a digitally integrated, service-oriented business model. OEMs investing in digital platforms, Tier-2 distribution, and modernization capabilities are best positioned to capture incremental value.

Research Methodology

Primary Research

Primary research included structured interviews with senior executives at leading OEMs (KONE Corporation, Otis Elevator Company (I). Ltd., Schindler, Johnsonlifts, Mitsubishi Elevator India Pvt Ltd, and Hitachi Lift India Pvt. Ltd.), procurement heads at large real estate developers, metro rail authorities, hospital facility managers, and independent lift service contractors across India.

Secondary Research

Secondary inputs include OEM annual reports, Ministry of Housing and Urban Affairs publications, Smart Cities Mission data, state lift inspectorate notifications, real estate research from Knight Frank and JLL, and industry trade media covering construction and infrastructure.

Forecasting Models

Forecasts were built using a combination of top-down macro indicators (GDP, urbanization, real estate value) and bottom-up unit-level estimates by city, building type, and service category. Scenario analysis was applied across base, optimistic, and conservative assumptions.

India Elevator and Escalator Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Elevators, Escalators |

| Services Covered | New Installation, Maintenance and Repair, Modernization |

| End Uses Covered |

|

| Regions Covered | North India, South India, East India, West India |

| Companies Covered | KONE Corporation, Otis Elevator Company (I). Ltd., Schindler, Johnsonlifts, Mitsubishi Elevator India Pvt Ltd, Hitachi Lift India Pvt. Ltd., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Elevator and Escalator Market Report

The India elevator and escalator market reached USD 15.23 Billion in 2025, supported by urbanization, high-rise construction, metro rail rollouts, and growing modernization activity across major Indian cities.

The market is projected to reach USD 23.12 Billion by 2034, growing at a CAGR of 4.13% during 2026-2034, driven by metro expansion, smart city projects, and rising premium high-rise demand.

Elevators lead with a 96.8% share in 2025, supported by their universal application across residential towers, offices, hospitals, hotels, and government buildings across India’s rapidly urbanizing cities.

New installation dominates with a 58.5% share in 2025, supported by the strong residential pipeline, metro rail station rollouts, and large commercial and IT park construction across Tier-1 cities.

West India leads with a 32.5% share in 2025, anchored by Mumbai high-rise residential, Pune commercial real estate, and Gujarat’s expanding industrial corridors and Tier-2 city construction.

South India is the fastest-growing region, propelled by Bengaluru and Chennai metro rail expansion, Hyderabad IT park construction, and Kochi infrastructure development through the forecast period.

Leading companies include KONE Corporation, Otis Elevator Company (I). Ltd., Schindler, Johnsonlifts, Mitsubishi Elevator India Pvt Ltd, and Hitachi Lift India Pvt. Ltd.

Key drivers include rapid urbanization, smart city investments, expanding metro rail networks, rising high-rise construction, modernization of legacy elevator stock, and adoption of energy-efficient and IoT-enabled lifts.

Escalators account for 3.2% of the market in 2025, with demand concentrated in metro stations, airports, and large-format retail across Bengaluru, Mumbai, Hyderabad, Chennai, and Delhi-NCR.

Residential is the largest end-use segment, driven by mid-rise and high-rise housing across metros and Tier-2 cities, followed by commercial offices, hospitals, hotels, and metro rail networks.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)