India Engine Oils Market Size, Share, Trends and Forecast by Grade, Sales Channel, Engine Type, Vehicle Type, and Region, 2026-2034

India Engine Oils Market Summary:

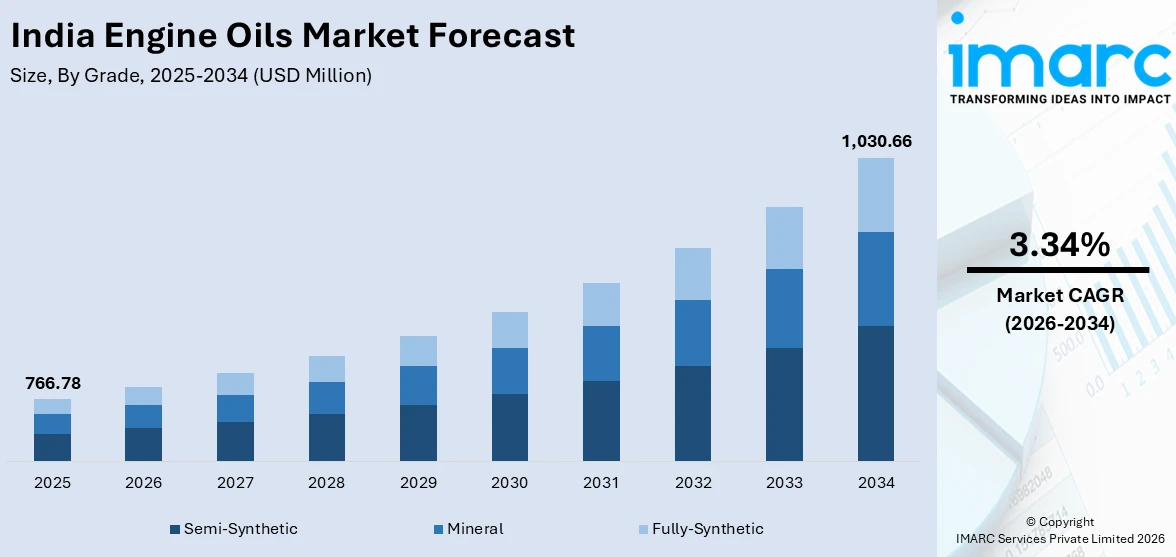

The India engine oils market size was valued at USD 766.78 Million in 2025 and is projected to reach USD 1,030.66 Million by 2034, growing at a compound annual growth rate of 3.34% from 2026-2034.

The market for engine oils in India is witnessing consistent growth fueled by rising vehicle ownership, increasing awareness among users regarding engine upkeep, and the continuing shift towards more advanced lubricant formulations. Strict emission standards and advancing engine technologies are driving the transition from traditional mineral oils to semi-synthetic and fully synthetic options. The increasing aftermarket demand, expanding digital distribution avenues, and premiumization trends in both passenger car and commercial vehicle segments are further contributing to the India engine oils market share.

Key Takeaways and Insights:

- By Grade: Semi-synthetic leads the market with a share of 40% in 2025, fueled by its ideal combination of performance attributes and cost efficiency that attracts budget-sensitive consumers in India.

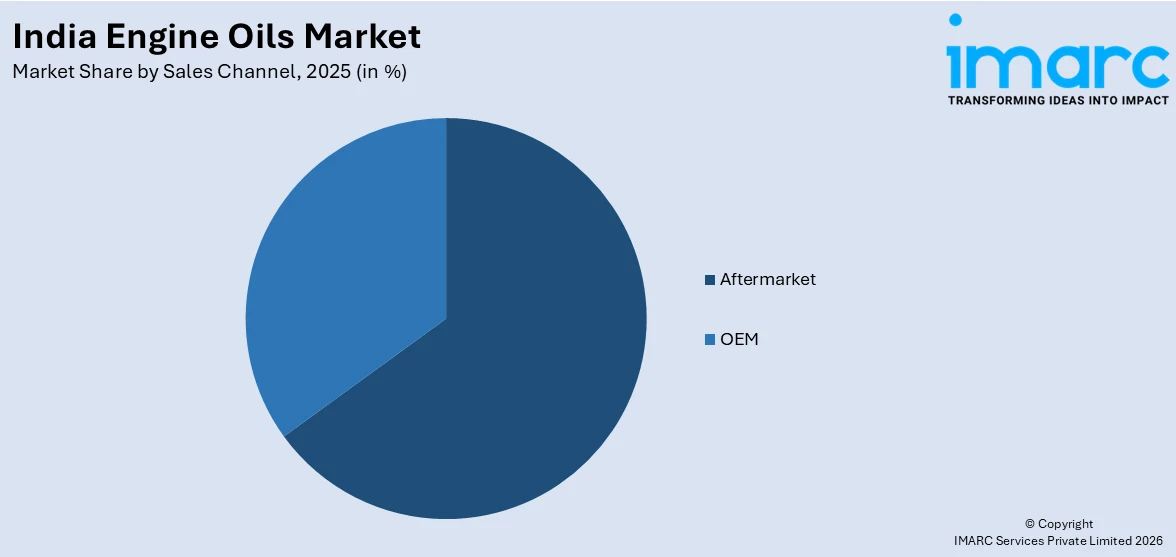

- By Sales Channel: Aftermarket dominates the market with a share of 65% in 2025, bolstered by widespread independent workshop networks, increasing vehicle maintenance awareness, and the growth of e-commerce distribution platforms.

- By Engine Type: Diesel represents the largest segment with a market share of 54% in 2025, highlighting India's significant commercial vehicle fleet and the ongoing prevalence of diesel engines in transportation and logistics industries.

- By Vehicle Type: Passenger cars lead the market with a share of 38% in 2025, driven by higher vehicle ownership, increasing disposable incomes, and a growing consumer preference for high-quality engine maintenance products.

- Key Players: The India engine oils market showcases fierce competition between established multinational firms and local oil marketing enterprises, with major players broadening their product offerings, enhancing distribution systems, and investing in innovative lubricant formulations to meet increasing demand.

To get more information on this market Request Sample

The India engine oils market is evolving rapidly, driven by the increasing vehicle ownership, the rising adoption of turbocharged and fuel-efficient engines, stricter emission regulations, and growing user awareness about engine longevity and maintenance cost optimization. Urbanization and expanding middle-class incomes are encouraging demand for premium and semi-synthetic lubricants that offer enhanced protection, thermal stability, and fuel efficiency. Additionally, the preference for locally produced, globally certified products is shaping purchasing decisions, as consumers seek reliable performance aligned with international standards. Technological advancements, including formulations tailored for modern passenger cars and hybrid engines, are further fueling market growth. Marketing strategies that emphasize performance, brand credibility, and aspirational value are also playing a key role in influencing consumer choices. For example, in 2025, Castrol India launched its enhanced MAGNATEC engine oils, meeting the latest global API SQ standard, providing superior wear protection, improved fuel efficiency, and full compatibility with India’s E20 fuel, reflecting these combined market-driving trends.

India Engine Oils Market Trends:

Premiumization and Performance-Oriented Branding

Premiumization is emerging as a powerful trend in the Indian engine oils market, driven by rising use preference and demand for enhanced vehicle performance. Lubricant brands are positioning products around measurable gains in power, responsiveness, and long-term protection, often supported by global marketing campaigns. The shift toward high-performance passenger cars is encouraging manufacturers to introduce advanced formulations aligned with the latest API standards. In 2025, Shell India upgraded its Helix Ultra range meeting API SQ norms and promoted it through a global campaign featuring Scuderia Ferrari drivers, highlighting performance gains and reinforcing a strong premium brand identity.

Increasing Strategic Distribution Partnerships

The expansion and optimization of distribution networks through strategic collaborations represent a key factor bolstering the growth of the India engine oils market. With rising demand for advanced lubricants across automotive and industrial applications, companies are increasingly entering partnerships to integrate technological expertise with well-established supply chain infrastructures. These alliances facilitate faster market penetration, broader geographic coverage, and enhanced accessibility of premium products to end users. Moreover, such arrangements enable international brands to effectively participate in India’s expanding lubricant consumption base. Illustrating this development, in 2024, Enso Oils & Lubricants entered into a partnership with G-Energy to distribute its advanced engine oils across the Indian market.

Growing OEM Approvals and Global Certifications

The India engine oils market is influenced by the increasing emphasis on obtaining global OEM approvals and certifications, which strengthen brand credibility and facilitate entry into premium automotive segments. Domestic lubricant manufacturers are aligning their formulations with rigorous international standards to enhance competitiveness against established multinational players and to build user confidence. Securing approvals from leading automobile manufacturers reflects proven product reliability, superior emission control, and optimized fuel efficiency. In 2024, EnerG Lubricants became the first Indian company to receive Mercedes-Benz MB 229.51 and MB 229.52 approvals for its G1 Xtreme Plus 5W-30 engine oil, further reinforced by its collaboration with GAT GmbH.

Market Outlook 2026-2034:

The India engine oils sector shows significant growth potential during the forecast period, supported by increasing vehicle ownership and changing requirements for engine technology. The market generated a revenue of USD 766.78 Million in 2025 and is projected to reach a revenue of USD 1,030.66 Million by 2034, growing at a compound annual growth rate of 3.34% from 2026-2034. This growth pattern indicates consistent market development as premiumization speeds up, aftermarket services rise, and regulatory structures promote the use of advanced lubricant formulations in commercial and passenger vehicle sectors across India.

India Engine Oils Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Grade |

Semi-Synthetic |

40% |

|

Sales Channel |

Aftermarket |

65% |

|

Engine Type |

Diesel |

54% |

|

Vehicle Type |

Passenger Cars |

38% |

Grade Insights:

- Mineral

- Semi-Synthetic

- Fully-Synthetic

Semi-synthetic dominates with a market share of 40% of the total India engine oils market in 2025.

Semi-synthetic leads the market due to its ability to provide an optimal combination of performance, reliability, and cost-effectiveness. It blends high-quality synthetic components with conventional mineral base oils, resulting in superior lubrication properties, improved viscosity stability, and extended drain intervals. Compared to mineral oils, semi-synthetic offers enhanced protection against engine wear, oxidation, and thermal breakdown, making it suitable for a wide range of vehicles under diverse operating conditions. Its affordability relative to fully synthetic oils further strengthens its appeal among consumers seeking long-term engine performance without incurring premium costs.

The leadership of semi-synthetic is reinforced by the increasing adoption of compact SUVs and turbocharged engines in India, which require higher thermal stability, improved oxidation resistance, and enhanced wear protection. As India’s middle-class population increasingly emphasizes fuel efficiency, engine longevity, and cost-effective maintenance, semi-synthetic emerges as the preferred choice for balancing quality and affordability. Serving as an intermediate solution between mineral and fully synthetic oils, it meets the performance requirements of modern engines while supporting sustained growth across urban and rural automotive service sectors nationwide.

Sales Channel Insights:

Access the comprehensive market breakdown Request Sample

- OEM

- Aftermarket

Aftermarket leads with a market share of 65% of the total India engine oils market in 2025.

Aftermarket holds the biggest market share owing to its extensive reach, accessibility, and ability to serve a diverse user base across urban and rural regions. It provides vehicle owners with a wide selection of products, including mineral, semi-synthetic, and fully synthetic oils, enabling informed choices based on engine type, performance requirements, and budget considerations. Aftermarket distribution channels, including independent automotive service centers, retail outlets, and online platforms, offer convenience and competitive pricing, making them particularly attractive for cost-conscious consumers. Their established presence and responsiveness to consumer demand further reinforce aftermarket’s dominant position in engine oil sales.

The prominence of aftermarket is further strengthened by the growing Indian automotive sector, including the rising adoption of compact SUVs, passenger vehicles, and modern turbocharged engines. Vehicle owners increasingly prioritize regular maintenance, engine longevity, and fuel efficiency, which drives demand for readily available and high-quality engine oils. Aftermarket channels efficiently address these needs, offering professional guidance, product availability, and post-sale support. By bridging the gap between manufacturers and end consumers, aftermarket sustains its leadership in engine oil sales, supporting both the growth of the automotive service industry and the evolving preferences of India’s expanding middle-class population.

Engine Type Insights:

- Gasoline

- Diesel

Diesel exhibits a clear dominance with a 54% share of the total India engine oils market in 2025.

Diesel dominates the market because of its widespread use in commercial vehicles, heavy-duty trucks, and passenger cars that demand high-performance lubrication. Diesel engine oil is formulated to meet stringent emission norms and maintain engine efficiency over extended drain intervals. Its ability to enhance fuel economy, reduce maintenance frequency, and extend engine life makes diesel the preferred engine type for both fleet operators and individual vehicle owners across India’s diverse automotive landscape. For instance, in 2024, Valvoline Cummins Pvt Ltd has launched All Fleet Pro, a CK-4 diesel engine oil designed to provide up to 20% extra engine protection for commercial vehicles. Engineered with a premium synthetic blend and advanced additives, it enhanced durability, reduced wear, and ensured compliance with modern emission systems like EGR, DPF, and SCR.

The dominance of diesel is further reinforced by India’s strong logistics, transportation, and industrial sectors, which rely heavily on diesel-powered vehicles for sustained operations. As vehicle owners and fleet managers increasingly prioritize reliability, fuel efficiency, and cost-effective maintenance, diesel engine oil emerges as the solution that addresses these operational requirements. Its performance advantages under high-load and long-distance driving conditions ensure consistent engine protection, while supporting compliance with evolving environmental standards. Consequently, diesel maintains a leading position in the engine oils market, meeting the needs of both urban and rural users as well as commercial enterprises nationwide.

Vehicle Type Insights:

- Passenger Cars

- Light Commercial Vehicles

- Heavy Commercial Vehicles

- Two Wheelers

Passenger cars dominate with a market share of 38% of the total India engine oils market in 2025.

Passenger cars represent the largest segment driven by their widespread ownership, diverse engine configurations, and increasing demand for performance and efficiency. These vehicles require oils that ensure optimal lubrication, thermal stability, and protection against wear, oxidation, and sludge formation under varying driving conditions. Engine oils for passenger cars are formulated to meet modern emission standards, enhance fuel economy, and extend service intervals, making them particularly suitable for urban and semi-urban usage. The growing preference for reliable and cost-effective maintenance further strengthens the position of passenger cars in driving engine oil usage across India’s expanding automotive sector.

The dominance of passenger cars is further supported by the rise of compact, mid-sized, and premium vehicles that demand advanced lubrication solutions. Owners increasingly prioritize engine longevity, fuel efficiency, and smooth performance, creating sustained demand for oils that balance affordability with high-quality protection. Engine oils tailored for passenger cars bridge the gap between conventional mineral oils and fully synthetic alternatives, providing a reliable choice for urban commuters, family vehicles, and personal transportation. Consequently, passenger cars remain a key driver of engine oil sales, shaping market trends and influencing product development across India’s automotive landscape.

Regional Insights:

- North India

- South India

- East India

- West India

North India constitutes an important part of the market owing to its populous urban areas, increasing passenger car ownership, and a rising number of commercial vehicles. The area's severe winters and diverse driving circumstances create a need for top-notch lubrication solutions. People emphasize engine durability, fuel efficiency, and affordable maintenance, which fosters substantial growth in both semi-synthetic and fully synthetic oils in urban and semi-urban regions.

South India enjoys advantages from its booming automotive sector, increasing ownership of SUVs and compact cars, and a robust logistics industry. Tropical climates and elevated engine load conditions require oils that offer excellent thermal stability and oxidation resistance. Growing user awareness regarding fuel efficiency, engine safeguarding, and periodic maintenance bolsters the use of semi-synthetic and synthetic oils in urban and rural service centers alike.

East India’s engine oils market is growing because of increasing passenger vehicle adoption, rise of commercial transport, and regional industrial activity. Semi-synthetic oils, offering balanced performance and affordability, are increasingly preferred, with independent service centers and retail outlets acting as key distribution channels across urban and emerging semi-urban regions.

West India contributes significantly to engine oil usage owing to its industrial hubs, dense urban populations, and high vehicle density. The region’s mix of passenger vehicles, SUVs, and commercial fleets drives demand for oils with enhanced thermal stability and engine protection. Rising awareness of maintenance schedules, fuel efficiency, and environmental standards supports steady growth in semi-synthetic and fully synthetic oil adoption throughout urban, semi-urban, and rural markets.

Market Dynamics:

Growth Drivers:

Why is the India Engine Oils Market Growing?

Growing Demand for Advanced Engine Protection Standards

A key trend driving the India engine oils market is the growing demand for lubricants that comply with advanced global performance standards. As passenger vehicles adopt turbocharged and gasoline direct injection technologies, the need for superior protection against LSPI, timing chain wear, and emission-related challenges is increasing. Individuals and OEMs alike are prioritizing oils that enhance fuel efficiency while ensuring compatibility with both modern and older engines. This is evident in 2025, when TotalEnergies Marketing India launched its new Quartz range certified to API SQ and ILSAC GF-7 standards. The oils offered up to 40% better LSPI protection, 20% improved timing chain wear protection, and enhanced fuel efficiency, while remaining backward compatible with older engines.

Rise in Domestic Innovation and Export Ambitions

The increasing focus on indigenous research and advanced formulation technologies is also shaping the market dynamics. Key lubricant players in India are investing in proprietary technologies to deliver high-performance synthetic oils tailored for diverse driving conditions, ranging from congested urban roads to extreme climates. This innovation-led approach not only enhances engine longevity and efficiency but also positions Indian brands for global expansion. The emphasis on synthetic and specialty lubricants reflects a move up the value chain within the automotive aftermarket. Illustrating this in 2025, Veedol Corporation launched SwiftPower and SynthGlide using advanced EstoBioLides Technology, with plans to explore export opportunities beyond the domestic market.

Expanding SUV and Hybrid Vehicle Segment

The rapid growth of SUVs, hybrids, and premium vehicles in India is catalyzing the demand for specialized engine oils tailored to higher load and performance requirements. These vehicles operate under more demanding conditions, requiring lubricants with enhanced strength, stability, and acceleration support. As people upgrade to technologically advanced cars, lubricant companies are introducing segment-specific products aligned with OEM recommendations. In 2024, Castrol India launched its EDGE range for SUVs and hybrids featuring PowerBoost Technology™, promising at least 30% improved performance. The launch combined innovative products with a 360-degree multimedia campaign, reinforcing Castrol’s leadership in advanced lubricants and premium automotive performance in India.

Market Restraints:

What Challenges the India Engine Oils Market is Facing?

Growing Electric Vehicle Adoption Reducing Conventional Lubricant Demand

The accelerating adoption of electric vehicles across two-wheeler, three-wheeler, and passenger car segments is gradually reducing traditional engine oil consumption. Electric powertrains eliminate the need for conventional engine oils, creating long-term volume headwinds for the lubricant industry. While the impact remains modest in the near term, the structural shift toward electrification poses a growing challenge to sustained market expansion.

Volatility in Crude Oil and Base Stock Prices Affecting Market Stability

India imports a significant portion of its base oil requirements, exposing domestic lubricant manufacturers to volatile global crude oil prices and exchange rate fluctuations. These supply-side uncertainties compress blender margins and create pricing instability that can affect product affordability and consumer purchasing patterns, particularly in price-sensitive rural and semi-urban markets.

Prevalence of Counterfeit and Substandard Products in Unorganized Markets

The widespread availability of counterfeit and substandard engine oils through unorganized distribution channels undermines market integrity and erodes user trust. These inferior products, often sold at significantly lower prices through informal workshops and roadside outlets, can damage engines and reduce the perceived value proposition of branded lubricants, hindering premiumization efforts.

Competitive Landscape:

The India engine oils market features a highly competitive landscape characterized by the coexistence of established multinational lubricant corporations, state-owned oil marketing companies, and emerging domestic manufacturers. Competition is driven by product innovation, brand strength, distribution reach, and strategic OEM partnerships that secure factory-fill supply agreements. Major international players leverage advanced additive technology and global brand recognition to capture premium synthetic segments, while domestic oil marketing companies utilize extensive retail networks spanning fuel stations, workshops, and rural outlets. The competitive dynamics are increasingly shaped by digital transformation, sustainability initiatives, and premiumization strategies as manufacturers invest in developing advanced BS-VI compliant formulations and expanding e-commerce capabilities to capture evolving user preferences across diverse geographic and vehicle segments.

Recent Developments:

- December 2025: Gulf Oil Lubricants India Ltd launched Gulf Syntrac, a fully synthetic motorcycle engine oil range aimed at premium and high-performance two-wheelers. Built on advanced ester technology and API SP compliant, it offered 11 SKUs across multiple viscosity grades, ensuring engine, gearbox, and wet clutch protection under demanding conditions.

- September 2025: Valvoline Cummins India launched the All Fleet Full Synthetic CK4, India’s first full synthetic CK4 engine oil for heavy-duty commercial vehicles. The oil offered 60% cleaner pistons, superior wear protection, and compatibility across BSIV and BSVI engines, ensuring reliable performance under extreme temperatures. Designed for modern after-treatment systems, it helped fleets reduce downtime, extend engine life, and maintain emissions compliance.

India Engine Oils Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Grades Covered | Mineral, Semi-Synthetic, Fully-Synthetic |

| Sale Channels Covered | OEM, Aftermarket |

| Engine Types Covered | Gasoline, Diesel |

| Vehicle Types Covered | Passenger Cars, Light Commercial Vehicles, Heavy Commercial Vehicles, Two Wheelers |

| Regions Covered | North India, South India, East India, West India |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Engine Oils Market Research Report and Industry Forecast Report

The India engine oils market size was valued at USD 766.78 Million in 2025.

The India engine oils market is expected to grow at a compound annual growth rate of 3.34% from 2026-2034 to reach USD 1,030.66 Million by 2034.

Semi-synthetic dominates the market with a revenue share of 40% in 2025, driven by their optimal balance of performance and affordability that appeals to India's broad user base seeking enhanced engine protection beyond conventional mineral oils.

Key factors driving the India engine oils market include rising premiumization, as people increasingly seek enhanced engine performance, protection, and longevity. Brands emphasize measurable benefits in power and responsiveness. For example, in 2025, Shell India upgraded Helix Ultra to API SQ standards, promoting it globally with a campaign featuring Scuderia Ferrari drivers.

Major challenges include growing electric vehicle adoption reducing conventional lubricant demand, volatility in crude oil and base stock prices affecting manufacturing costs and market stability, prevalence of counterfeit products in unorganized markets, and extended drain intervals in modern engines reducing replacement frequency.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)