India Engineering Plastics Market Size, Share, Trends and Forecast by Type, Application, and Region, 2026-2034

India Engineering Plastics Market Size, Share, Trends & Forecast (2026-2034)

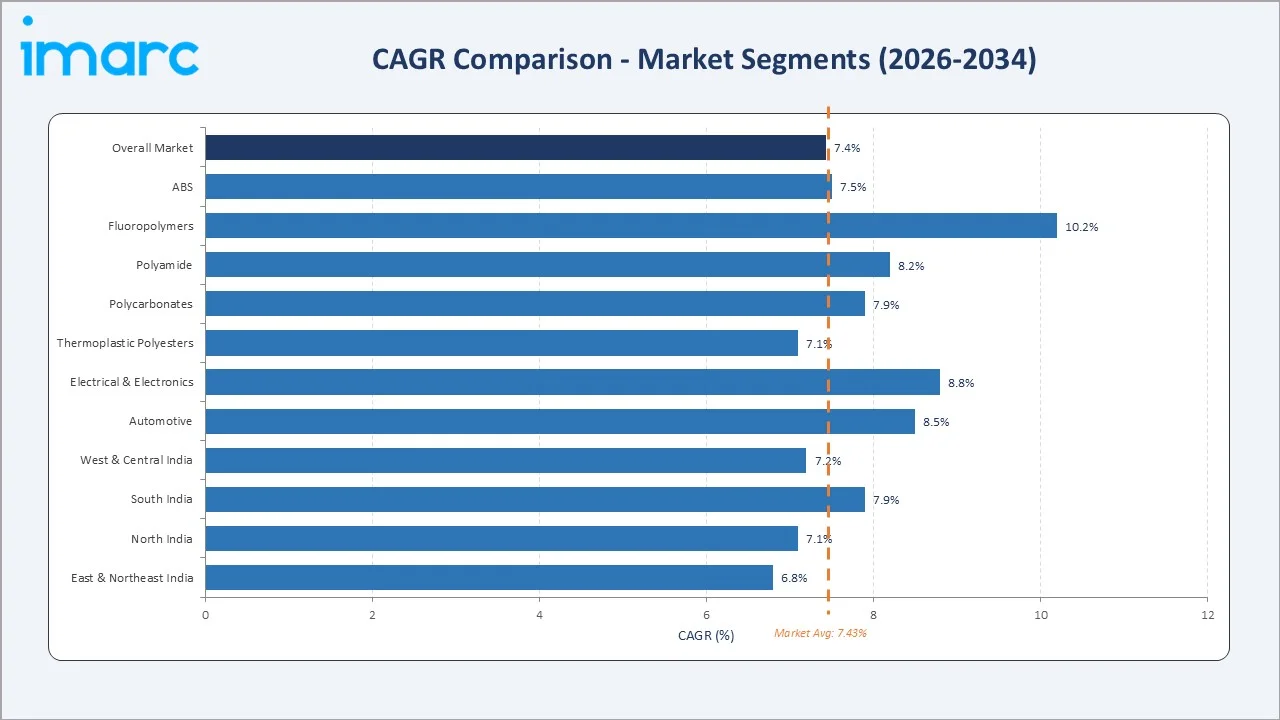

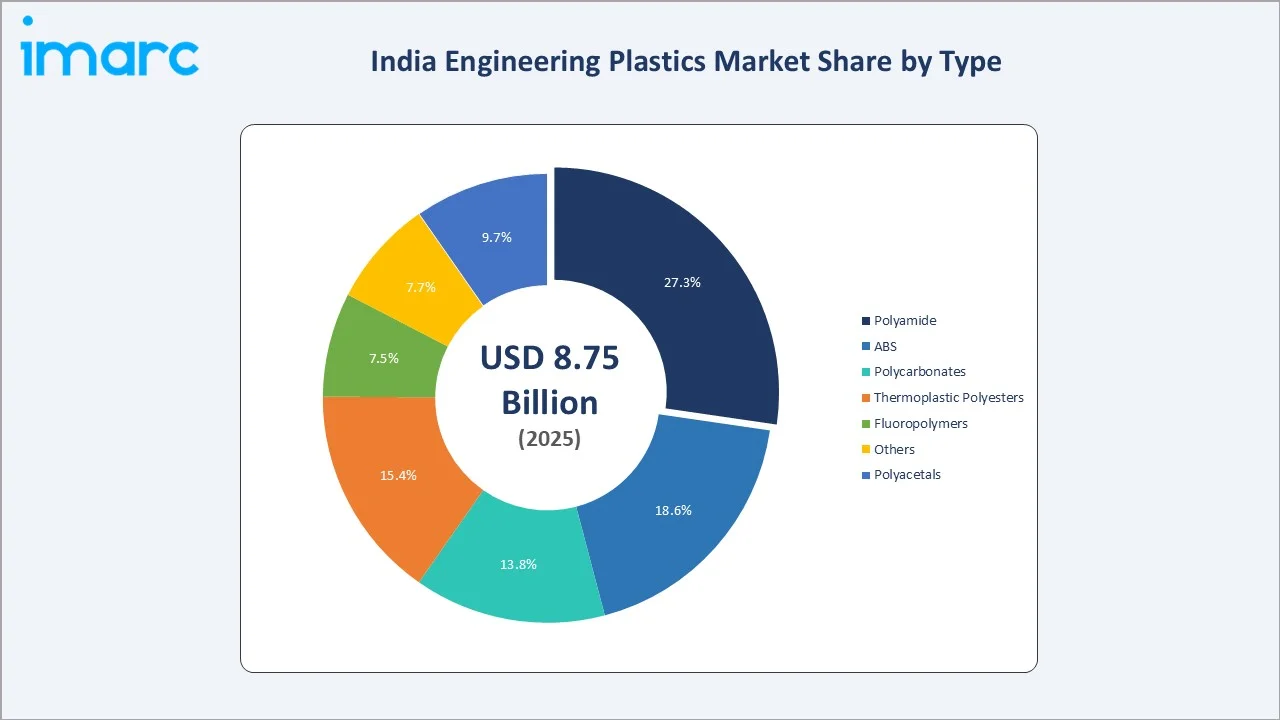

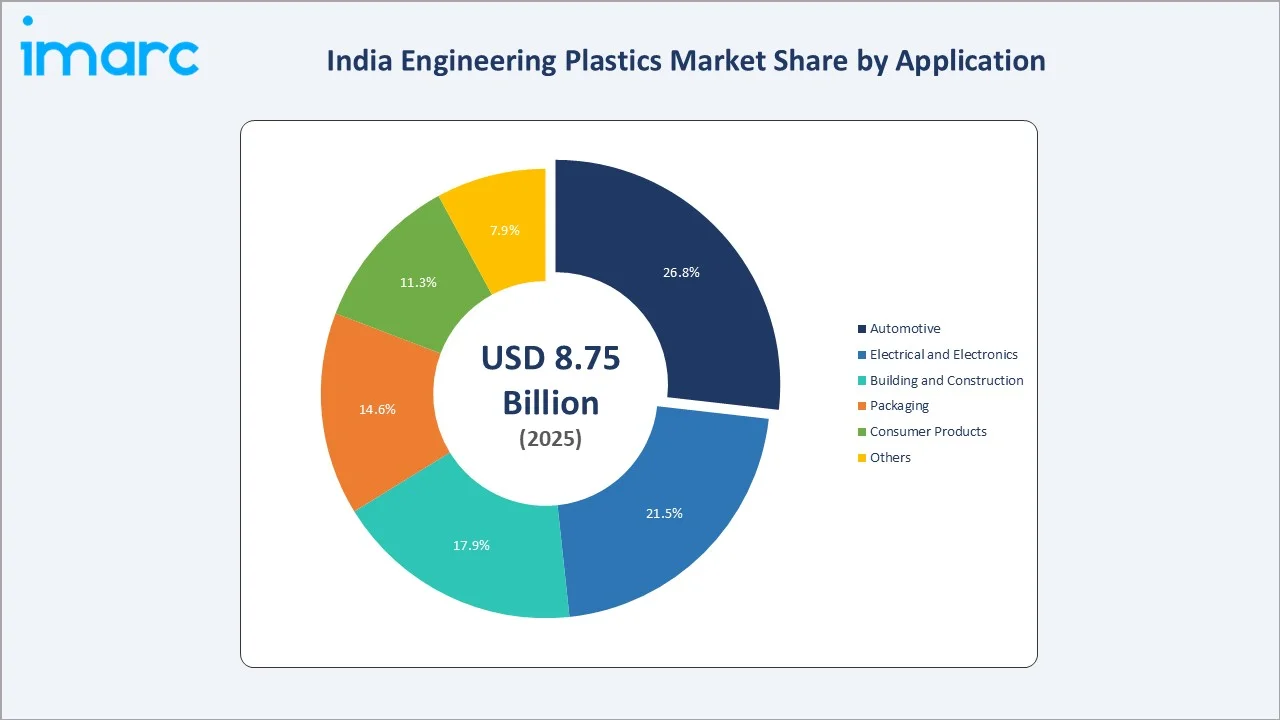

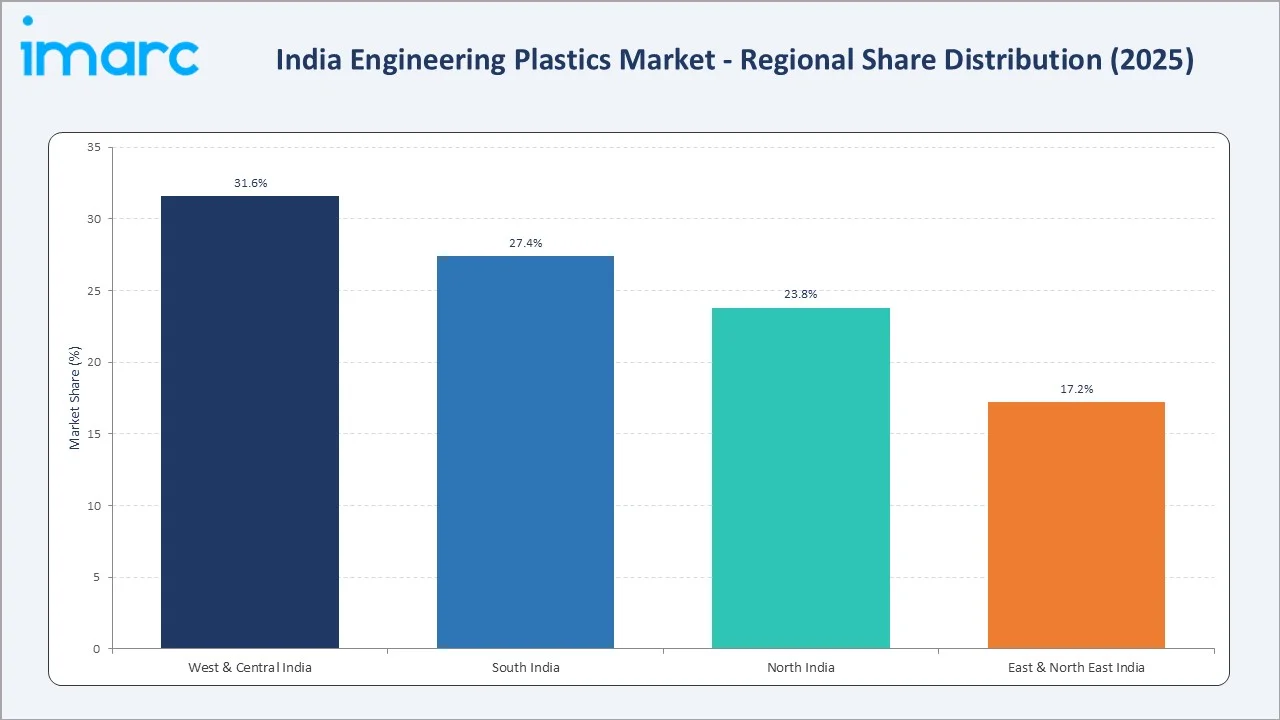

The India engineering plastics market size was valued at USD 8.75 Billion in 2025 and is projected to reach USD 16.67 Billion by 2034, at a CAGR of 7.43% during 2026-2034. Rapid industrialization, expanding automotive production, rising electronics manufacturing, and the government's Make in India initiative collectively fuel engineering plastics market growth. Polyamide leads with a 27.3% type share in 2025, while automotive is the dominant application at 26.8%. West and Central India account for the largest regional share at 31.6% in 2025, anchored by Maharashtra's industrial clusters.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 8.75 Billion |

|

Forecast Market Size (2034) |

USD 16.67 Billion |

|

CAGR (2026-2034) |

7.43% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

West & Central India (31.6% share, 2025) |

|

Fastest Growing Region |

South India |

|

Leading Type Segment |

Polyamide (27.3%, 2025) |

|

Leading Application Segment |

Automotive (26.8%, 2025) |

To get more information on this market, Request Sample

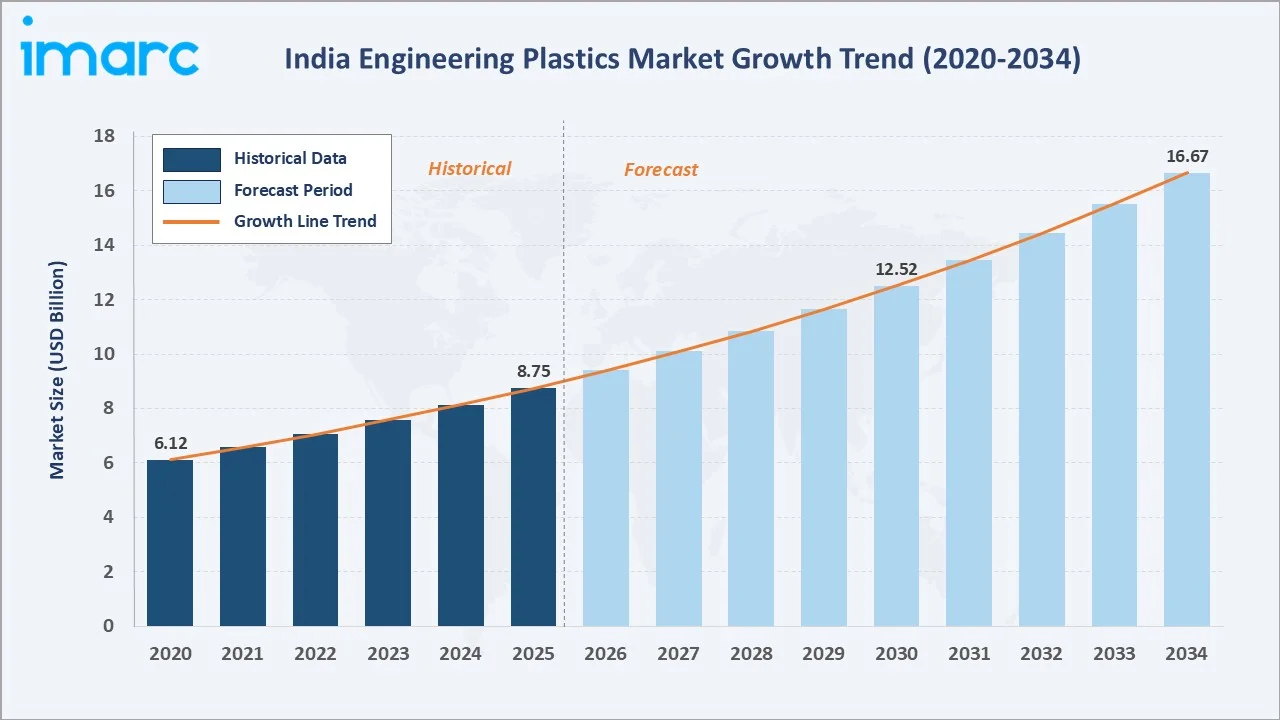

The chart shows the growth of India’s engineering plastics market from 2020 to 2034, with both past performance and future projections driven by strengthening national strategies and increased investment initiatives.

The chart shows steady growth from USD 6.12 Billion in 2020 to USD 8.75 Billion in 2025, with faster expansion expected through 2034, driven by post-pandemic recovery, PLI-led manufacturing, EV adoption, and semiconductor growth.

Executive Summary

India’s engineering plastics market is rapidly transforming, driven by rising automotive output, expanding electronics manufacturing, and strong infrastructure investment. Valued at USD 8.75 Billion in 2025, the market is projected to reach USD 16.67 Billion by 2034, reflecting a robust CAGR of 7.43%, supported by PLI schemes and the Make in India initiative boosting domestic manufacturing demand.

Polyamide leads the market with a 27.3% Market Share in 2025, driven by high heat resistance, strength, and lightweight properties for automotive and electronics uses. ABS follows with an 18.6% Market Share, supported by its cost-efficiency in consumer products. Automotive remains the largest application with a 26.8% Market Share in 2025, fueled by localization and EV initiatives from manufacturers like Tata Motors, Maruti Suzuki, and Hyundai Motor India.

West and Central India leads with a 31.6% Market Share in 2025, driven by Maharashtra’s Pune–Nashik automotive corridor and Gujarat’s chemical hub. South India follows with a 27.4% Market Share, supported by Tamil Nadu’s automotive clusters and Karnataka’s electronics base. Future growth will be driven by bio-based polymers, recycled engineering plastics, and smart material integration through 2034.

Key Market Insights

|

Insight |

Data |

|

Largest Type Segment |

Polyamide – 27.3% share (2025) |

|

Second Type Segment |

ABS – 18.6% share (2025) |

|

Leading Application Segment |

Automotive – 26.8% share (2025) |

|

Second Application Segment |

Electrical & Electronics – 21.5% share (2025) |

|

Largest Region |

West & Central India – 31.6% revenue share (2025) |

|

Fastest Growing Region |

South India – 27.4% share (2025) |

|

Top Companies |

BASF, SABIC, Covestro AG, LG Chem, Lanxess, Dupont |

|

Market Opportunity |

EV component localization, bio-based engineering plastics |

Key Analytical Observations Supporting the Above Data:

- Polyamide holds a 27.3% Market Share in 2025, driven by rising automotive demand for lightweight, heat-resistant components in engine bays, connectors, and structural parts under India’s vehicle lightweighting mandates.

- ABS at 18.6% serves high-growth consumer electronics and appliance segments where impact resistance and surface finish quality are primary selection criteria for domestic and export-oriented manufacturers.

- Automotive's 26.8% application share in 2025 underscores India's position as the world's third-largest automobile market, with increasing polymer content per vehicle driven by fuel efficiency and safety regulation compliance.

- Electrical and Electronics at 21.5% is driven by India's smartphone assembly boom under the PLI scheme, with manufacturers including Foxconn, Samsung, and Tata Electronics scaling domestic production volumes significantly.

- West and Central India's 31.6% share is anchored by Maharashtra and Gujarat's combined industrial base, hosting automotive OEMs, specialty chemical manufacturers, and export-oriented polymer processing clusters.

- South India is the fastest-growing region, driven by Tamil Nadu’s expanding EV and auto-component manufacturing, along with rising electronics and defence investments in Karnataka and Andhra Pradesh since 2022.

India Engineering Plastics Market Overview

Engineering plastics are high-performance polymers with superior mechanical, thermal, and chemical resistance compared to commodity plastics. They are widely used in automotive, electrical & electronics, industrial machinery, and consumer applications. In India, the value chain includes petrochemical raw material suppliers, polymer manufacturers, compounders, processors, and OEM end-users across multiple industrial regions.

Engineering plastics are widely used in automotive components, EV battery parts, electrical & electronics (including PCBs), medical devices, packaging, and construction. Strong economic growth, government PLI schemes, and rising investments in automotive and electronics manufacturing are supporting demand growth in India.

Market Dynamics

To evaluate market opportunities, Request Sample

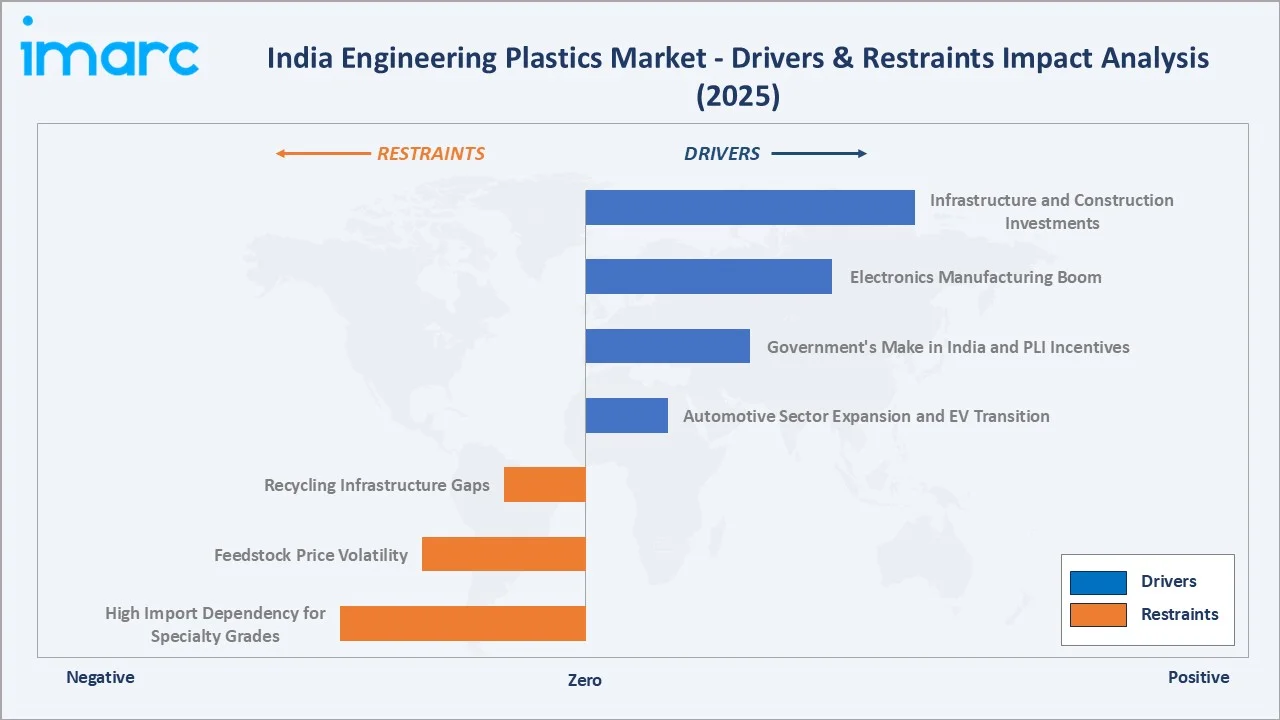

Market Drivers

- Automotive Sector Expansion and EV Transition: India’s automobile production exceeded 4.5 million units in FY2024. Increasing lightweighting and EV adoption are driving higher engineering plastics usage, as manufacturers replace metal components with durable polymer alternatives.

- Government's Make in India and PLI Incentives: India’s PLI schemes, with ~INR 1.97 trillion outlay, promote domestic manufacturing in automotive, electronics, and chemicals, boosting engineering plastics demand across components, devices, and industrial equipment production.

- Electronics Manufacturing Boom: India’s electronics production surpassed USD 100 billion in FY2024, driven by PLI-led smartphone manufacturing, increasing demand for engineering plastics like ABS and polycarbonate in consumer electronics applications.

- Infrastructure and Construction Investments: India’s National Infrastructure Pipeline, with over USD 1.4 trillion investment, supports construction growth, increasing demand for engineering plastics in piping systems, electrical fittings, and durable construction materials.

Market Restraints

- High Import Dependency for Specialty Grades: India relies on imports for advanced engineering plastic grades due to limited domestic production, exposing the market to supply disruptions, foreign exchange fluctuations, and price volatility in global markets.

- Feedstock Price Volatility: Engineering plastics depend on petrochemical feedstocks linked to crude oil prices, making resin costs highly volatile and impacting margins for processors during periods of sharp fluctuations in global oil prices.

- Recycling Infrastructure Gaps: India recycles around one-third of plastic waste, with limited infrastructure for engineering plastics. EPR regulations under Plastic Waste Management Rules increase compliance costs and operational challenges for manufacturers.

Market Opportunities

- Electric Vehicle Component Localization: India’s rapidly growing EV market creates strong demand for engineering plastics in battery housings, motor parts, and charging systems, supporting localization of high-performance polymer components across the automotive value chain.

- Bio-Based and Recycled Engineering Plastics: Sustainability requirements from global OEMs are increasing demand for recycled and bio-based engineering plastics, encouraging domestic manufacturers to invest in circular production technologies and environmentally compliant material solutions.

- Medical Device Manufacturing Growth: India’s expanding medical device market is driving demand for high-performance engineering plastics used in surgical instruments and diagnostic equipment, supported by increasing domestic manufacturing and healthcare infrastructure development.

Market Challenges

- Skilled Processing Workforce Shortage: India faces a shortage of skilled polymer processing professionals, impacting product quality, innovation, and scalability, particularly in high-performance engineering plastics applications requiring specialized technical expertise and advanced manufacturing capabilities.

- Intense Competition from China: Chinese manufacturers offer cost-competitive engineering plastics due to scale and supply chain efficiencies, creating pricing pressure and limiting margin expansion for Indian producers in both domestic and export markets.

- Regulatory Complexity on Plastic Use: India’s evolving plastic regulations, including single-use plastic bans and EPR requirements, create compliance challenges, with varying state-level implementation adding complexity to operations and supply chain planning for manufacturers.

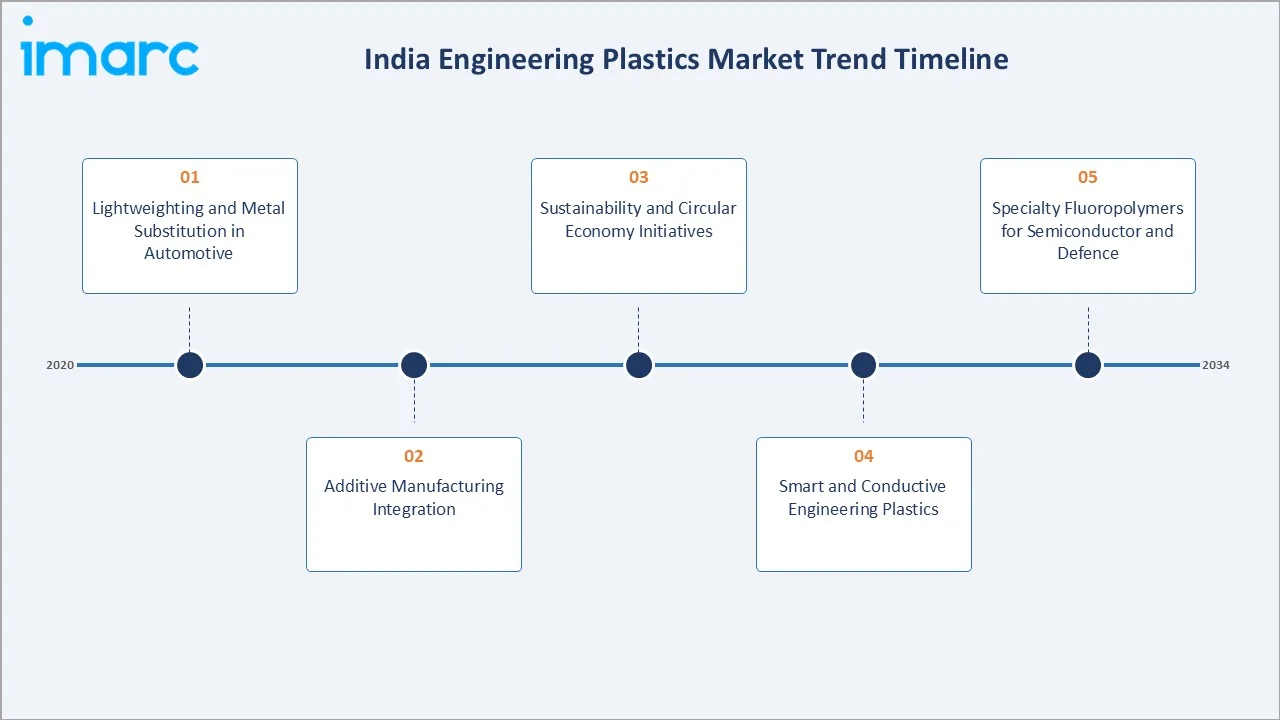

Emerging Market Trends

1. Lightweighting and Metal Substitution in Automotive

Automotive lightweighting under fuel efficiency and emission norms is accelerating metal-to-plastic substitution, increasing demand for high-performance engineering plastics in structural, under-the-hood, and interior automotive applications.

2. Additive Manufacturing Integration

Growing adoption of additive manufacturing in India is increasing demand for engineering plastics such as polyamide, ABS, and PEEK, supporting applications in aerospace, medical prototyping, and industrial tooling.

3. Sustainability and Circular Economy Initiatives

Global chemical companies are investing in recycled and circular engineering plastics in India, driven by sustainability goals and OEM requirements, promoting adoption of chemically recycled materials and closed-loop production systems.

4. Smart and Conductive Engineering Plastics

Demand for conductive engineering plastics is rising in electronics and defence applications, supporting EMI shielding, anti-static uses, and advanced components requiring enhanced electrical and functional material properties.

5. Specialty Fluoropolymers for Semiconductor and Defence

India’s semiconductor and defence initiatives are driving demand for high-performance fluoropolymers used in cleanroom systems, chemical handling, and advanced electronics manufacturing requiring high purity and thermal resistance.

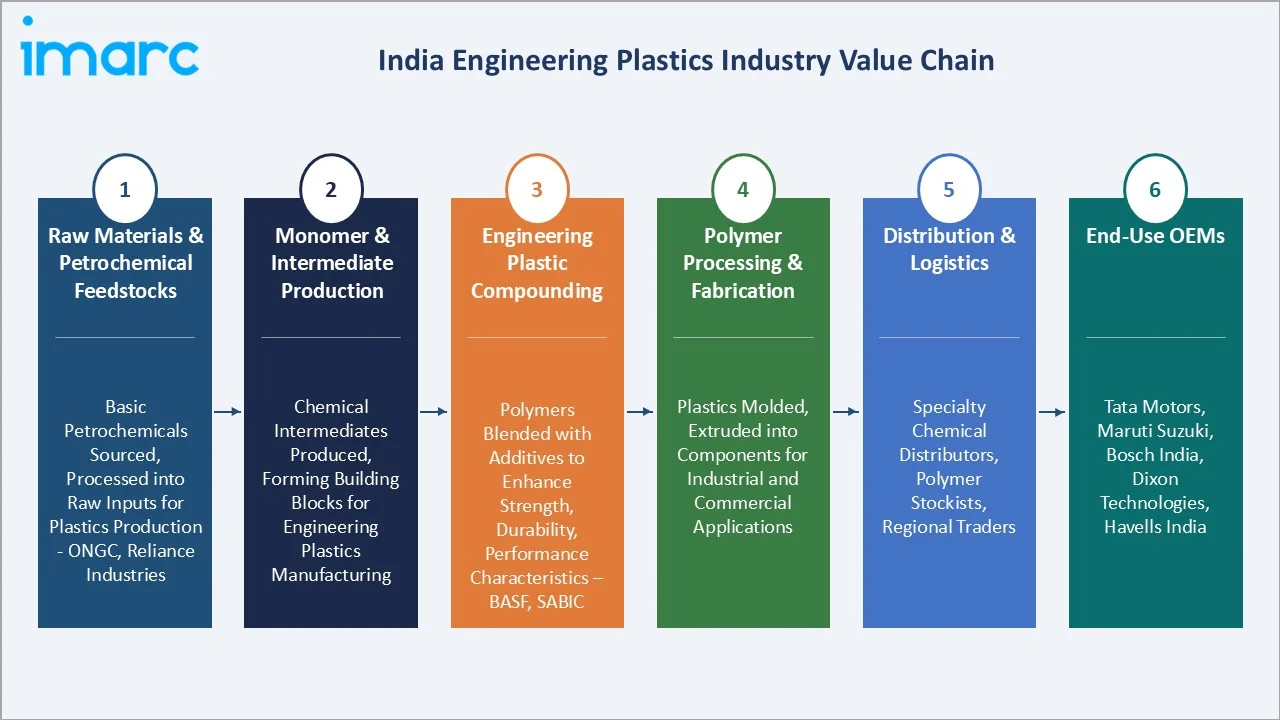

Industry Value Chain Analysis

India’s engineering plastics value chain covers six stages, from petrochemical feedstocks to OEM applications, with each stage characterized by distinct competition levels and margin profiles.

|

Stage |

Key Players / Examples |

|

Raw Materials & Petrochemical Feedstocks |

ONGC, Reliance Industries, Indian Oil Corporation, Borealis (imports) |

|

Monomer & Intermediate Production |

GAIL, Deepak Nitrite, GNFC, imported caprolactam and diamine suppliers |

|

Engineering Plastic Compounding |

BASF India, Covestro India, Lanxess India, RTP Company, Celanese |

|

Polymer Processing & Fabrication |

Siyaram Polymers, Hitech Plastic, Ester Industries |

|

Distribution & Logistics |

Specialty chemical distributors, polymer stockists, regional traders |

|

End-Use OEMs |

Tata Motors, Maruti Suzuki, Bosch India, Dixon Technologies, Havells India |

Global compounders and specialty polymer manufacturers hold the highest value position in the chain, commanding premium pricing for performance-engineered grades. Domestic processors and distributors operate in more competitive, price-sensitive segments.

Technology Landscape in the Engineering Plastics Industry

Advanced Polymer Compounding Technologies

Advanced compounding technologies, including twin-screw extrusion, enable precise incorporation of reinforcements such as glass fibers and fillers, enhancing performance, processing efficiency, and application suitability of engineering plastics.

Recycling and Circular Material Technologies

Chemical and mechanical recycling technologies for engineering plastics are gaining traction, driven by sustainability goals and EPR regulations, supporting development of circular materials and reducing dependence on virgin polymer production.

Smart and Functional Engineering Plastics

Functional engineering plastics with conductive, anti-static, and high-strength properties are increasingly used in automotive, electronics, and defence applications, enabling advanced performance features such as EMI shielding and structural durability.

Bio-Based Polymer Development

Bio-based engineering plastics derived from renewable feedstocks are gaining adoption, offering lower carbon footprints and supporting sustainability initiatives across industries including automotive, packaging, and medical device manufacturing.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Type |

Polyamide |

27.3% |

2025 |

|

Application |

Automotive |

26.8% |

2025 |

|

Region |

West and Central India |

31.6% |

2025 |

By Type

To access detailed market analysis, Request Sample

Polyamide holds a dominant 27.3% type share in 2025, driven by strong mechanical properties, heat resistance, and wide use in automotive and electrical sectors. Glass-fiber reinforcement enhances stiffness, wear resistance, and durability for demanding industrial and underhood applications.

ABS accounts for 18.6% of the type of mix in 2025, primarily serving India's booming consumer electronics and appliance manufacturing sectors. ABS demand grew approximately 14% in 2024 supported by the PLI scheme for IT hardware, wearables, and white goods. Thermoplastic Polyesters at 15.4% are gaining traction in sustainable packaging and construction profiles as manufacturers seek halogen-free flame-retardant material solutions.

By Application

Automotive holds a commanding 26.8% application share in 2025, India is the world’s third-largest automobile market, producing over 4.3 million passenger vehicles in FY2024. Engineering plastic usage per vehicle is steadily increasing, driven by lightweighting trends and growing electric vehicle adoption.

Electrical and Electronics at 21.5% in 2025 is expanding rapidly, propelled by India's semiconductor ambitions and PLI-driven mobile device assembly growth. Dixon Technologies, Tata Electronics, and Foxconn India are scaling operations, creating sustained demand for Polycarbonate, ABS, and thermally conductive Polyamide compounds. Building and Construction at 17.9% benefits from the National Infrastructure Pipeline and smart city projects driving thermoplastic profiles, electrical conduit, and specialty fitting demand.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

Regulatory Impact |

Major Companies |

|

West & Central India |

31.6% |

Maharashtra, Gujarat industrial clusters; Pune-Nashik automotive corridor |

Make in India incentives; SEZ expansions |

Reliance, BASF India, Covestro India |

|

South India |

27.4% |

Tamil Nadu EV and auto components; Karnataka electronics and defence |

EV policy incentives; PLI electronics investments |

Hyundai India, Bosch India, Samsung India |

|

North India |

23.8% |

NCR industrial belt; UP and Haryana manufacturing clusters |

DMIC corridor; Yamuna Expressway industrial zone |

Maruti Suzuki, Hero MotoCorp, Dixon Technologies |

|

East & North East India |

17.2% |

West Bengal chemical industry; Odisha metals linkages |

NE industrial development policy 2024 |

Haldia Petrochemicals |

West and Central India commands a 31.6% revenue share in 2025, supported by Maharashtra’s strong automotive and plastics manufacturing base and Gujarat’s large petrochemical hubs like Dahej, with Maharashtra contributing a significant share to India’s plastics processing capacity.

South India at 27.4% in 2025 is supported by Tamil Nadu’s automotive and EV manufacturing hubs and Karnataka’s strong electronics ecosystem, with additional industrial development in Andhra Pradesh. North India at 23.8% is driven by the established Delhi-NCR automotive belt and Uttar Pradesh’s growing electronics manufacturing ecosystem supported by industrial corridor initiatives.

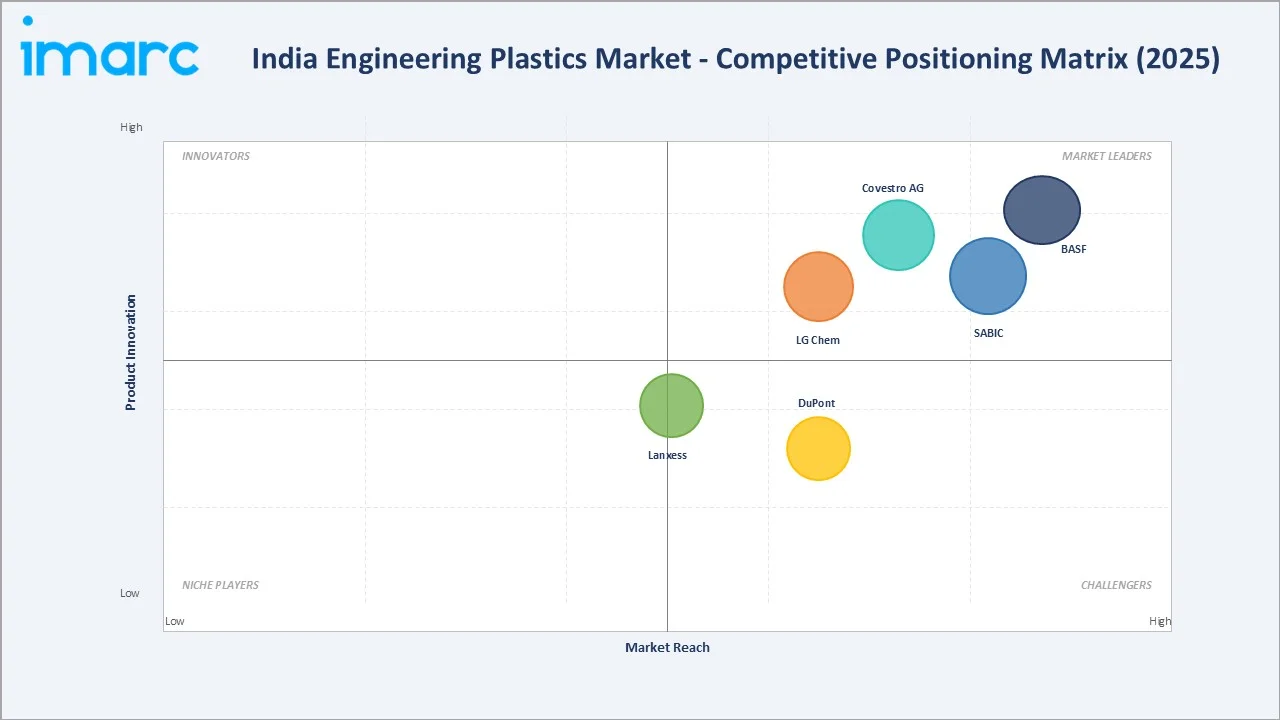

Competitive Landscape

|

Company Name |

Key Brand / Platform |

Market Position |

Core Strength |

|

BASF |

Ultramid / Ultradur |

Leader |

Broad PA and PBT portfolio, strong auto-sector relationships |

|

SABIC |

Noryl |

Leader |

Polycarbonate and PPO blends, global scale, auto and E&E |

|

Covestro AG |

Makrolon |

Leader |

Polycarbonate specialization, sustainability focus |

|

LG Chem |

LUPOY / LUPOS |

Leader |

ABS leadership, diversified polymer grades for electronics |

|

Lanxess |

Durethan |

Challenger |

Engineering PA and PBT grades for automotive and E&E |

|

DuPont |

Zytel / Delrin |

Challenger |

Polyamide and Polyacetal leadership, precision applications |

The India engineering plastics market is led by global chemical multinationals including BASF, SABIC, Covestro, and LG Chem, alongside a growing ecosystem of regional compounders and specialty polymer distributors. BASF India reported net revenues of approximately Euro 2.4 billion in FY2024 across all business segments, with engineering plastics representing a significant growth driver.

Key Company Profiles

BASF

BASF SE, headquartered in Ludwigshafen, Germany, is the world’s leading chemical producer, with strong engineering plastics operations in India. The company operates multiple manufacturing and R&D sites, supplying high-performance polymers to automotive, electrical, and industrial sectors.

- Product & Service Portfolio: BASF offers engineering plastics including Ultramid (PA), Ultradur (PBT), Ultraform (POM), Ultrason (PES/PSU/PPSU), and Elastollan (TPU), serving automotive, electrical & electronics, and industrial applications.

- Recent Developments: In May 2024: BASF SE announced a major expansion of its engineering plastics production in India, increasing Ultramid (PA) and Ultradur (PBT) compounding capacity at Panoli (Gujarat) and Thane (Maharashtra) facilities by over 40%. The expansion supports rising demand from automotive and electrical sectors, with additional capacity expected by H2 2025.

- Strategic Focus: BASF focuses on localized production, sustainable and high-performance engineering plastics, and advanced materials tailored for automotive electrification, lightweighting, and electronics applications in India.

Covestro AG

Covestro AG, headquartered in Leverkusen, Germany, is a leading global manufacturer of high-performance polymers. In India, it operates multiple production and innovation sites, supplying polycarbonates, polyurethanes, and specialty materials to automotive, electronics, healthcare, and industrial sectors.

- Product & Service Portfolio: Covestro offers engineering plastics including Makrolon (polycarbonate), Bayblend (PC blends), along with polyurethanes and specialty raw materials for coatings, adhesives, and elastomers used across automotive, electronics, healthcare, and industrial applications.

- Recent Developments: In 2025, Covestro introduced advanced polycarbonate glazing and lightweight material solutions for next-generation mobility, supporting EV design through improved transparency, weight reduction, and integration of electronic components.

- Strategic Focus: Covestro focuses on circular economy-driven polymer innovation, lightweight and high-performance materials for EVs and electronics, and expanding sustainable polycarbonate applications through advanced recycling and localized solutions.

LG Chem

LG Chem Ltd., headquartered in Seoul, is a global leader in petrochemicals and advanced materials, supplying engineering plastics such as ABS and polycarbonate. The company serves India through exports and local operations targeting electronics, automotive, and appliance manufacturing sectors.

- Product & Service Portfolio: LG Chem offers engineering plastics including LUPOY (polycarbonate and PC blends), LUPOS (reinforced ABS/SAN), ABS resins, and specialty PC/ABS compounds for automotive, electronics, and industrial applications.

- Recent Developments: In August 2024 – LG Chem Ltd. announced the development of a PFAS-free flame-retardant PC/ABS material made with over 50% recycled plastics, achieving the highest UL94 V-0 rating. The material reduces carbon emissions by approximately 46% and is designed for applications in electronics, EV chargers, and industrial equipment.

- Strategic Focus: LG Chem focuses on expanding sustainable engineering plastics, localizing production in India, and strengthening its position in electronics, automotive, and EV material solutions through advanced polymer technologies.

Market Concentration Analysis

The India engineering plastics market exhibits a moderately concentrated structure at the specialty and premium grade level, with BASF, Covestro, SABIC, LG Chem, and Lanxess collectively accounting for an estimated 40–50% of the organized engineering plastics supply market in 2025. Global leaders command significant pricing authority in high-performance segments such as glass-reinforced Polyamide, optical Polycarbonate, and specialty PBT grades, where domestic alternative production remains limited.

Market fragmentation is high in the mid-market compounding segment, with numerous regional players and ABS processors competing on price. This reflects India’s dual structure, where global firms cater to premium OEM supply chains, while local and regional players serve cost-sensitive domestic manufacturing demand.

Consolidation is increasing as global specialty chemical companies expand manufacturing in India, reducing reliance on imports. Investments like BASF’s Dahej expansion and Covestro’s Pune compounding facility highlight local value addition strategies, while EPR compliance and sustainability reporting requirements are intensifying pressure on smaller compounders lacking circular material capabilities.

Investment & Growth Opportunities

Fastest-Growing Segments

Fluoropolymers are expected to witness strong growth, supported by India’s semiconductor and defence initiatives. The India Semiconductor Mission (USD 10 billion incentive) is likely to boost demand for high-purity materials like PTFE and PVDF. EV battery and thermal management applications are also emerging as key growth areas for high-performance engineering plastics. High-temperature Polyamide, Polycarbonate compounds, and PPS grades capable of meeting EV thermal management requirements at operating temperatures of 120–150°C are seeing accelerated qualification testing across India's major automotive OEMs.

Emerging Market Expansion

East and Northeast India present growth opportunities due to supportive industrial policies and rising investments in electronics and pharmaceuticals. Government initiatives like the North East Industrial Development Scheme (NEIDS) are encouraging regional manufacturing expansion, though exact market share figures vary across sources.

Venture & Strategic Investment Trends

Investment activity is increasing in areas like chemical recycling, bio-based polymers, and specialty compounding. Policy initiatives such as the draft National Chemical Policy aim to promote innovation and domestic manufacturing, supporting long-term growth, though specific investment figures remain indicative.

Future Market Outlook (2026-2034)

The India engineering plastics market is projected to expand from USD 8.75 Billion in 2025 to USD 16.67 Billion by 2034, at a CAGR of 7.43%. Growth is supported by automotive electrification, electronics manufacturing, and infrastructure initiatives like the National Infrastructure Pipeline. Per-capita consumption is expected to rise steadily, though exact figures vary across sources.

Technological advancements such as bio-based polymers, chemical recycling, and conductive engineering plastics are expected to reshape the market. Polyamide is likely to remain dominant, while specialty grades like fluoropolymers and polycarbonate show strong growth potential. South India is gaining share, driven by expanding automotive and electronics manufacturing clusters..

India's engineering plastics import-to-domestic production ratio is expected to improve as global multinationals expand local compounding capacity and domestic chemical manufacturers invest in upstream monomer production. This structural improvement in supply chain localization will support both cost competitiveness and supply security for downstream OEM customers, reinforcing India's position as a high-growth engineering plastics market of global significance through 2034.

Research Methodology

Primary Research

Primary research included structured interviews and discussions with industry executives, procurement managers, polymer engineers, OEM material specification teams, and chemical distributors across 14 key industry sectors. Over 60 primary interactions were conducted across automotive, electronics, packaging, construction, and specialty industrial end-user categories to validate market sizing, segmentation trends, and competitive dynamics.

Secondary Research

Secondary research encompassed analysis of company annual reports, regulatory filings, trade association publications, customs import-export data from the Ministry of Commerce, CHEMEXCIL industry statistics, PLEXCONCIL (Plastics Export Promotion Council) trade data, and industry conference proceedings. International trade data for HS codes 3901–3914 covering engineering plastic polymer categories were systematically analyzed for volume and value benchmarking.

Forecasting Models

Market forecasting employs a hybrid bottom-up and top-down approach, integrating macroeconomic scenario modeling, end-use industry production outlook analysis, historical CAGR trend extrapolation, and capacity expansion pipeline tracking. Sensitivity analysis across crude oil price, GDP growth, and automotive production scenarios was conducted to test forecast robustness across a range of plausible economic conditions through 2034.

India Engineering Plastics Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Polyamide, ABS, Thermoplastic Polyesters, Polycarbonates, Polyacetals, Fluoropolymers, Others |

| Applications Covered | Packaging, Building and Construction, Electrical and Electronics, Automotive, Consumer Products, Others |

| Regions Covered | North India, West and Central India, South India, East and Northeast India |

| Companies Covered | BASF, SABIC, Covestro AG, LG Chem, Lanxess, DuPont, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the India engineering plastics market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the India engineering plastics market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the India engineering plastics industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the India Engineering Plastics Market Report

The India engineering plastics market was valued at USD 8.75 Billion in 2025, reflecting consistent growth driven by automotive, electronics, and construction sector demand.

The market is projected to grow at a CAGR of 7.43% during 2026-2034, reaching USD 16.67 Billion by 2034, driven by industrial expansion.

Polyamide leads the market with a 27.3% share in 2025, driven by its superior mechanical and thermal properties for automotive and industrial applications.

Automotive is the largest application at 26.8% in 2025, supported by India's vehicle production scale and growing EV component material requirements.

West and Central India leads with a 31.6% revenue share in 2025, anchored by Maharashtra's automotive clusters and Gujarat's petrochemical manufacturing base.

Key drivers include India's automotive expansion, PLI-driven electronics manufacturing, EV transition programs, infrastructure investment, and the Make in India initiative.

Major companies include BASF, SABIC, Covestro AG, LG Chem, Lanxess, and DuPont.

Fluoropolymers and specialty Polycarbonate grades are the fastest-growing types, driven by semiconductor manufacturing and EV battery application demand through 2034.

India is among the world’s largest automobile markets, with rising EV adoption and increasing use of lightweight materials supporting engineering plastics demand. EVs typically use higher polymer content than ICE vehicles, though exact percentages vary across studies.

Companies are investing in chemical recycling, bio-based polymer grades, and EPR compliance programs. BASF, Covestro, and Lanxess are commercializing recycled engineering plastic grades in India by 2025–2026.

The market is projected to reach USD 16.67 Billion by 2034 at a 7.43% CAGR, supported by strong industrial demand, EV transition, and semiconductor manufacturing expansion.

Key challenges include high import dependency for specialty grades, petrochemical feedstock price volatility, skilled workforce shortages, and compliance complexity under evolving EPR regulations.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)