India Enteral Feeding Formulas Market Size, Share, Trends and Forecast by Product, Stage, Application, End Use, and Region, 2026-2034

India Enteral Feeding Formulas Market Summary:

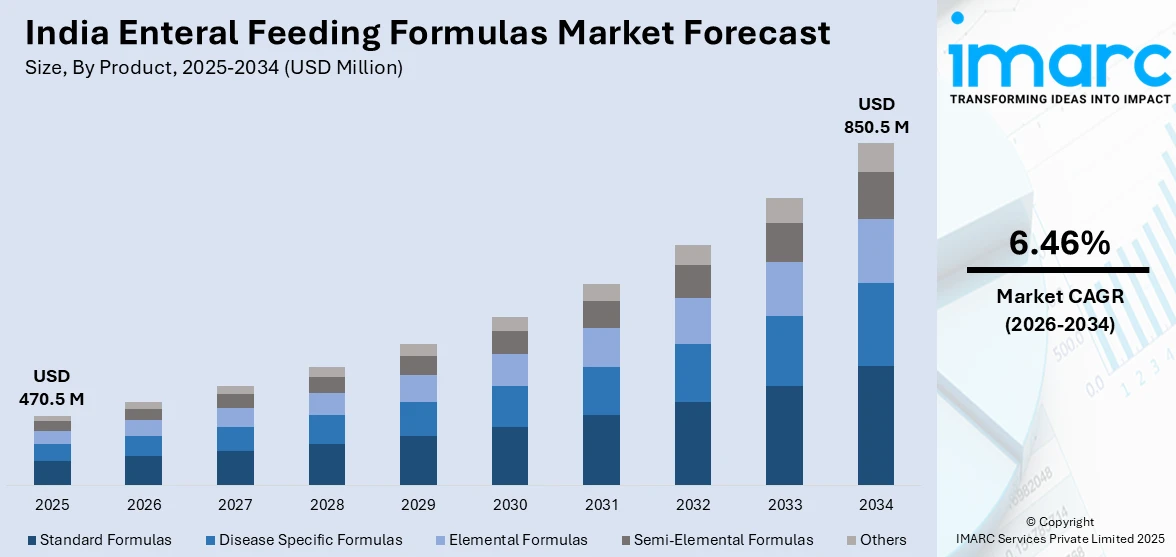

The India enteral feeding formulas market size was valued at USD 470.5 Million in 2025 and is projected to reach USD 850.5 Million by 2034, growing at a compound annual growth rate of 6.46% from 2026-2034.

The market is driven by the rising prevalence of chronic diseases requiring nutritional intervention, expanding geriatric population with swallowing difficulties, and growing awareness about clinical nutrition therapy across healthcare settings. Increasing hospital infrastructure development, improving healthcare expenditure, and the shift toward specialized disease-specific nutritional solutions are further propelling market expansion. The growing adoption of home-based enteral nutrition and advancements in formula compositions addressing diverse patient needs continue strengthening the India enteral feeding formulas market share.

Key Takeaways and Insights:

- By Product: Standard formulas dominate the market with a share of 44.2% in 2025, driven by versatile nutritional composition, cost-effectiveness, widespread availability across healthcare facilities, and physician prescription familiarity.

- By Stage: Adults lead the market with a share of 53.1% in 2025, owing to rising chronic illness burden, higher incidence of tube feeding conditions, and increasing critical care admissions.

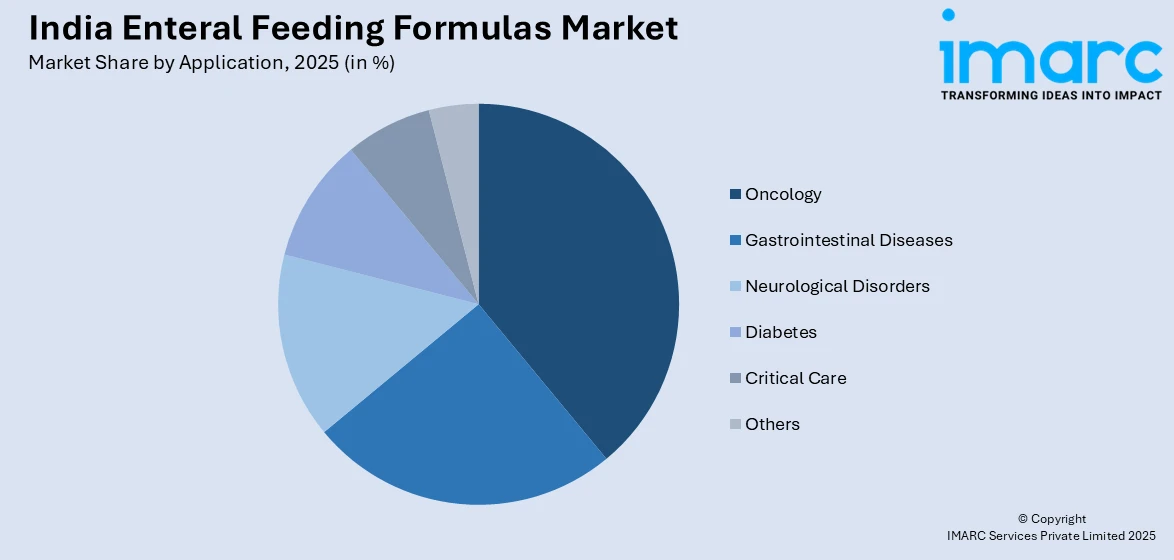

- By Application: Oncology represents the largest segment with a market share of 38.7% in 2025, driven by increasing cancer-related malnutrition, treatment-induced dysphagia, and the growing need for optimized nutritional support during therapy.

- By End Use: Hospitals dominate the market with a share of 46.5% in 2025, owing to centralized patient management, trained clinical nutrition teams, established procurement systems, and comprehensive monitoring infrastructure.

- By Region: West India leads the market with a share of 35.4% in 2025, driven by advanced tertiary care hospital concentration, higher healthcare spending, robust distribution networks, and specialized care centers.

- Key Players: The market exhibits moderately consolidated competition, with multinational nutrition corporations competing alongside domestic manufacturers. Participants emphasize product diversification, strategic distribution partnerships, and clinical education initiatives for positioning.

To get more information on this market Request Sample

The India enteral feeding formulas market is experiencing substantial growth momentum driven by multiple converging factors transforming the healthcare nutrition landscape. The expanding prevalence of chronic conditions including cancer, neurological disorders, and gastrointestinal diseases has created sustained demand for specialized nutritional interventions. In February 2025, Rela Hospital launched India’s first Centre for Intestinal Rehabilitation and Nutrition Support to provide integrated medical and nutritional therapies for complex gastrointestinal and intestinal failure cases, enhancing clinical nutrition capabilities. Moreover, India's demographic transition toward an aging population has amplified requirements for enteral nutrition support among elderly patients experiencing swallowing difficulties and reduced oral intake capabilities. Healthcare infrastructure modernization across tier-two and tier-three cities has improved access to clinical nutrition services previously concentrated in metropolitan areas. Rising physician awareness regarding malnutrition's impact on clinical outcomes has encouraged proactive nutritional screening and intervention protocols.

India Enteral Feeding Formulas Market Trends:

Expansion of Disease-Specific Nutritional Formulations

The market is witnessing significant advancement in specialized enteral formulas designed to address specific pathophysiological requirements of various medical conditions. Healthcare providers are increasingly adopting condition-targeted nutritional products that optimize metabolic responses in patients with diabetes, renal dysfunction, hepatic impairment, and respiratory conditions. These specialized formulations incorporate modified macronutrient ratios, specific fiber compositions, and tailored micronutrient profiles aligned with disease management protocols. The therapeutic nutrition approach enables clinicians to address underlying metabolic derangements while providing adequate caloric support, improving overall treatment outcomes and reducing complications associated with standard nutritional interventions.

Growing Adoption of Home Enteral Nutrition Programs

Healthcare systems across India are progressively implementing structured home enteral nutrition programs enabling patients to receive tube feeding outside hospital environments. This transition supports early hospital discharge while maintaining nutritional continuity for patients requiring long-term feeding support. In November 2025, the Indian Society of Parenteral and Enteral Nutrition (ISPEN) hosted its annual conference in Kolkata, featuring workshops and sessions to advance home and clinical enteral nutrition practices. Moreover, healthcare facilities are establishing dedicated nutrition support teams providing patient education, caregiver training, and remote monitoring services.

Integration of Ready-to-Use Feeding Systems

The market is experiencing growing preference for convenient ready-to-use enteral nutrition delivery systems requiring minimal preparation before administration. These pre-packaged feeding solutions reduce contamination risks associated with reconstitution processes and decrease nursing workload in clinical settings. In March 2024, Vygon India launched its Nutrisafe2 enteral feeding system designed to enhance safety and precision in neonatal feeding, addressing misconnections and improving clinical care delivery in NICUs across India. Healthcare facilities are transitioning toward closed-system feeding containers that maintain sterility throughout administration, enhancing patient safety and reducing infection-related complications.

Market Outlook 2026-2034:

The India enteral feeding formulas market revenue is projected to experience robust expansion throughout the forecast period, supported by increasing chronic disease burden and healthcare infrastructure development. Growing investments in specialized nutrition services, expanding insurance coverage for clinical nutrition products, and rising awareness among healthcare practitioners regarding malnutrition management will sustain market momentum. The revenue growth trajectory will be further strengthened by technological advancements in formula compositions, expanding home care adoption, and increasing penetration across semi-urban healthcare facilities seeking comprehensive nutritional intervention capabilities for diverse patient populations. The market generated a revenue of USD 470.5 Million in 2025 and is projected to reach a revenue of USD 850.5 Million by 2034, growing at a compound annual growth rate of 6.46% from 2026-2034.

India Enteral Feeding Formulas Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Product |

Standard Formulas |

44.2% |

|

Stage |

Adults |

53.1% |

|

Application |

Oncology |

38.7% |

|

End Use |

Hospitals |

46.5% |

|

Region |

West India |

35.4% |

Product Insights:

- Standard Formulas

- Disease Specific Formulas

- Elemental Formulas

- Semi-Elemental Formulas

- Others

Standard formulas dominate with a market share of 44.2% of the total India enteral feeding formulas market in 2025.

The standard formulas represent the foundational product category within India's clinical nutrition landscape, designed to meet general nutritional requirements of patients who are unable to consume adequate oral nutrition. These polymeric formulations contain intact proteins, carbohydrates, and fats in balanced proportions suitable for patients with functional gastrointestinal tracts. The formulations provide complete macro and micronutrient profiles enabling comprehensive nutritional support through tube feeding methods across diverse healthcare settings and patient populations.

The segment's market leadership stems from broad clinical applicability across diverse patient populations and healthcare environments nationwide. Standard formulas serve as first-line nutritional intervention for most patients initiating enteral feeding, with physicians transitioning to specialized products only when specific metabolic requirements emerge. Cost-effectiveness compared to disease-specific alternatives and widespread formulary inclusion across hospitals reinforce standard formula utilization as the predominant choice for routine nutritional support requirements.

Stage Insights:

- Adults

- Pediatric

Adults lead with a share of 53.1% of the total India enteral feeding formulas market in 2025.

Adult encompasses enteral nutrition requirements spanning young adults through elderly populations experiencing conditions necessitating tube feeding support. Adult enteral formulas are specifically calibrated to meet mature metabolic demands, incorporating appropriate protein concentrations, caloric densities, and micronutrient profiles aligned with adult physiological requirements across various disease states and clinical scenarios. The formulations address diverse nutritional needs arising from acute illnesses, chronic conditions, surgical recovery, and palliative care situations.

Segment dominance reflects the higher absolute prevalence of conditions requiring enteral nutrition among adult populations, including malignancies, stroke-related dysphagia, and progressive neurological disorders. The aging demographic profile in India has particularly expanded elderly patient requirements for enteral feeding support as geriatric populations experience increased vulnerability to malnutrition. Additionally, adults comprise the majority of critical care admissions and surgical patients requiring temporary nutritional support during recovery periods. The growing burden of chronic diseases among working-age populations further amplifies demand.

Application Insights:

Access the comprehensive market breakdown Request Sample

- Oncology

- Gastrointestinal Diseases

- Neurological Disorders

- Diabetes

- Critical Care

- Others

Oncology exhibits a clear dominance with a 38.7% share of the total India enteral feeding formulas market in 2025.

Oncology dominates enteral formula utilization driven by the significant nutritional challenges faced by cancer patients throughout their treatment journey. Malignancy-related cachexia, treatment-induced mucositis, and tumor-associated dysphagia create substantial requirements for alternative feeding routes when oral intake becomes compromised. Enteral nutrition supports patients undergoing chemotherapy, radiation therapy, and surgical interventions by maintaining adequate caloric intake during periods of compromised oral feeding capacity. The metabolic demands of malignancy combined with treatment side effects create complex nutritional requirements necessitating specialized support.

The oncology segment's leading position reflects cancer's growing prevalence across Indian populations and heightened clinical recognition of nutrition's role in treatment tolerance and outcomes. Oncology nutrition protocols increasingly emphasize early nutritional intervention to prevent severe malnutrition development before it compromises treatment delivery. Specialized oncology centers have established comprehensive nutritional support programs integrating enteral feeding as standard care components for appropriate patient populations. The connection between adequate nutrition and improved chemotherapy tolerance has driven systematic nutritional screening across cancer care pathways.

End Use Insights:

- Hospitals

- Long Term Care Facilities

- Home Care Settings

- Nursing Homes

Hospitals lead with a market share of 46.5% of the total India enteral feeding formulas market in 2025.

Hospitals represent the primary institutional setting for enteral nutrition initiation and management, equipped with specialized clinical nutrition teams, diagnostic capabilities, and monitoring infrastructure necessary for safe feeding tube placement and formula administration. Reflecting their central role in advanced clinical care, the India hospital market size was valued at USD 193.42 Billion in 2025 and is projected to reach USD 364.55 Billion by 2034, growing at a compound annual growth rate of 7.30% from 2026–2034, reinforcing the scale and capacity expansion of inpatient healthcare services. Inpatient settings enable comprehensive nutritional assessment, formula selection optimization, and complication management under professional supervision throughout the feeding initiation phase. The controlled environment allows healthcare teams to monitor patient tolerance, adjust feeding rates, and address complications promptly.

The segment dominance reflects the complexity of enteral nutrition initiation requiring medical oversight and the concentration of severely ill patients necessitating tube feeding within acute care environments. Tertiary care hospitals have developed specialized nutrition support services integrating clinical expertise in coordinated patient management approaches. Procurement systems and formulary management within hospitals facilitate consistent product availability and standardized nutritional protocols ensuring quality care delivery. The infrastructure investments in clinical nutrition departments have enhanced service capabilities across healthcare facilities.

Regional Insights:

- North India

- South India

- East India

- West India

West India dominates with a market share of 35.4% of the total India enteral feeding formulas market in 2025.

West India encompasses Maharashtra, Gujarat, Goa, and adjacent territories representing India's most economically developed region with advanced healthcare infrastructure supporting comprehensive clinical nutrition services. The region hosts numerous tertiary care hospitals, specialized cancer centers, and multispecialty facilities offering sophisticated enteral nutrition programs. Major metropolitan areas including Mumbai, Pune, and Ahmedabad concentrate significant healthcare capacity and specialist medical expertise attracting patients from surrounding regions. The industrial and commercial development has created populations with higher healthcare spending capacity and awareness regarding clinical nutrition benefits.

Regional market leadership stems from higher healthcare expenditure capacity, established pharmaceutical distribution networks, and concentration of corporate hospital chains emphasizing clinical nutrition programs as quality differentiators. West India's industrial development has attracted healthcare investments creating superior infrastructure for specialized services including enteral nutrition support across institutional and home care settings. The region's demographic profile includes substantial elderly populations within urban centers requiring nutritional intervention services as chronic disease prevalence increases. Additionally, the presence of medical education institutions has created trained workforce availability supporting clinical nutrition service expansion.

Market Dynamics:

Growth Drivers:

Why is the India Enteral Feeding Formulas Market Growing?

Rising Burden of Chronic Diseases Requiring Nutritional Support

India is experiencing an epidemiological transition characterized by increasing prevalence of chronic conditions creating sustained demand for clinical nutrition interventions. The growing incidence of malignancies across various organ systems has expanded patient populations requiring enteral feeding support during treatment and palliative care phases. In 2024, the India Association for Parenteral and Enteral Nutrition (IAPEN India) published a consensus guidance on nutritional management for paediatric cancer patients, emphasizing structured enteral nutrition strategies to address high rates of treatment-related malnutrition and support therapy tolerance in clinical practice, reflecting growing professional focus on integrated nutrition care in oncology.

Expanding Healthcare Infrastructure and Clinical Nutrition Services

India's healthcare sector is experiencing significant infrastructure development extending specialized services beyond metropolitan areas into tier-two and tier-three cities. Hospital networks such as Aster DM Healthcare have announced large expansion plans across India, adding thousands of beds and increasing clinical service access in emerging healthcare hubs in response to rising demand for comprehensive care, including nutrition support in inpatient settings. New hospital establishments increasingly incorporate clinical nutrition departments as essential service components recognizing nutrition's impact on patient outcomes. The expansion of intensive care unit capacity across healthcare facilities has created additional settings requiring enteral nutrition capabilities.

Growing Awareness of Malnutrition's Clinical Impact

Healthcare practitioners across India are demonstrating increased recognition of malnutrition's detrimental effects on treatment outcomes, complication rates, and recovery trajectories. Clinical evidence highlighting improved surgical outcomes, reduced infection rates, and shortened hospital stays among adequately nourished patients has encouraged proactive nutritional screening protocols, and a nationwide survey found that 81.5 % of surveyed hospitals in India already perform regular nutritional screening, reflecting growing clinical adoption of systematic malnutrition identification and intervention practices in healthcare settings. Professional medical associations have emphasized nutrition assessment as standard care components across various specialties. This awareness shift has transformed institutional approaches toward nutrition from supportive afterthought to integrated treatment element.

Market Restraints:

What Challenges the India Enteral Feeding Formulas Market is Facing?

Limited Awareness in Rural Healthcare Settings

Despite urban healthcare advancement, rural healthcare facilities across India often lack awareness regarding clinical nutrition benefits and enteral feeding protocols. Primary healthcare centers serving rural populations rarely possess trained personnel capable of identifying malnourished patients requiring nutritional intervention. This knowledge gap results in delayed referrals and missed opportunities for timely enteral nutrition initiation, limiting market penetration beyond established urban healthcare networks.

High Cost of Specialized Enteral Formulations

Specialized disease-specific enteral formulas command premium pricing that limits accessibility for economically disadvantaged patient populations. Many families face financial constraints preventing sustained procurement of appropriate enteral products, particularly for chronic conditions requiring long-term feeding support. Insurance coverage limitations for nutritional products further compound affordability challenges, restricting market expansion among price-sensitive patient segments.

Infrastructure Requirements for Home Enteral Nutrition

Successful home-based enteral feeding requires reliable supply chains, caregiver training programs, and monitoring systems that remain underdeveloped across many Indian regions. Patients discharged with enteral feeding requirements may face difficulties obtaining consistent product supplies and accessing troubleshooting support when complications arise. These infrastructure gaps discourage home enteral nutrition adoption and create preference for continued institutional care despite associated inconveniences.

Competitive Landscape:

The India enteral feeding formulas market demonstrates a moderately consolidated competitive structure characterized by established multinational corporations maintaining significant market presence alongside emerging domestic manufacturers. Market participants compete across multiple dimensions including product portfolio breadth, therapeutic specialization, distribution network coverage, and healthcare professional engagement programs. Leading players emphasize scientific differentiation through clinical research demonstrating product efficacy across specific patient populations. Distribution strategy represents a critical competitive element, with successful participants establishing relationships across hospital pharmacy systems, medical distributors, and emerging home care channels. Educational initiatives targeting physicians, dietitians, and nursing staff constitute important competitive tools for building brand preference and prescription loyalty.

India Enteral Feeding Formulas Market Report Coverage:

|

Report Features |

Details |

|

Base Year of the Analysis |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Units |

Million USD |

|

Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

|

Products Covered |

Standard Formulas, Disease Specific Formulas, Elemental Formulas, Semi-Elemental Formulas, Others |

|

Stages Covered |

Adults, Pediatric |

|

Applications Covered |

Oncology, Gastrointestinal Diseases, Neurological Disorders, Diabetes, Critical Care, Others |

|

End Uses Covered |

Hospitals, Long Term Care Facilities, Home Care Settings, Nursing Homes |

|

Regions Covered |

North India, South India, East India, West India |

|

Customization Scope |

10% Free Customization |

|

Post-Sale Analyst Support |

10-12 Weeks |

|

Delivery Format |

PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Questions Answered in This Report

The India enteral feeding formulas market size was valued at USD 470.5 Million in 2025.

The India enteral feeding formulas market is expected to grow at a compound annual growth rate of 6.46% from 2026-2034 to reach USD 850.5 Million by 2034.

Standard formulas held the largest market share, driven by their versatile nutritional composition suitable for diverse patient populations, cost-effectiveness compared to specialized alternatives, and widespread physician familiarity enabling confident prescription across healthcare settings.

Key factors driving the India enteral feeding formulas market include rising chronic disease prevalence requiring nutritional intervention, expanding healthcare infrastructure with clinical nutrition capabilities, growing physician awareness of malnutrition's impact on outcomes, and increasing adoption of home-based enteral nutrition programs.

Major challenges include limited clinical nutrition awareness in rural healthcare settings, high costs of specialized formulations restricting accessibility, underdeveloped home enteral nutrition infrastructure, inadequate insurance coverage for nutritional products, shortage of trained nutrition professionals, and inconsistent supply chain networks across regions.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: sales@imarcgroup.com

Client Testimonials

.webp)