India Erectile Dysfunction Market Size, Share, Trends and Forecast by Treatment Type, Drug Type, Mode of Administration, Age Group, End User, and Region, 2026-2034

India Erectile Dysfunction Market Summary:

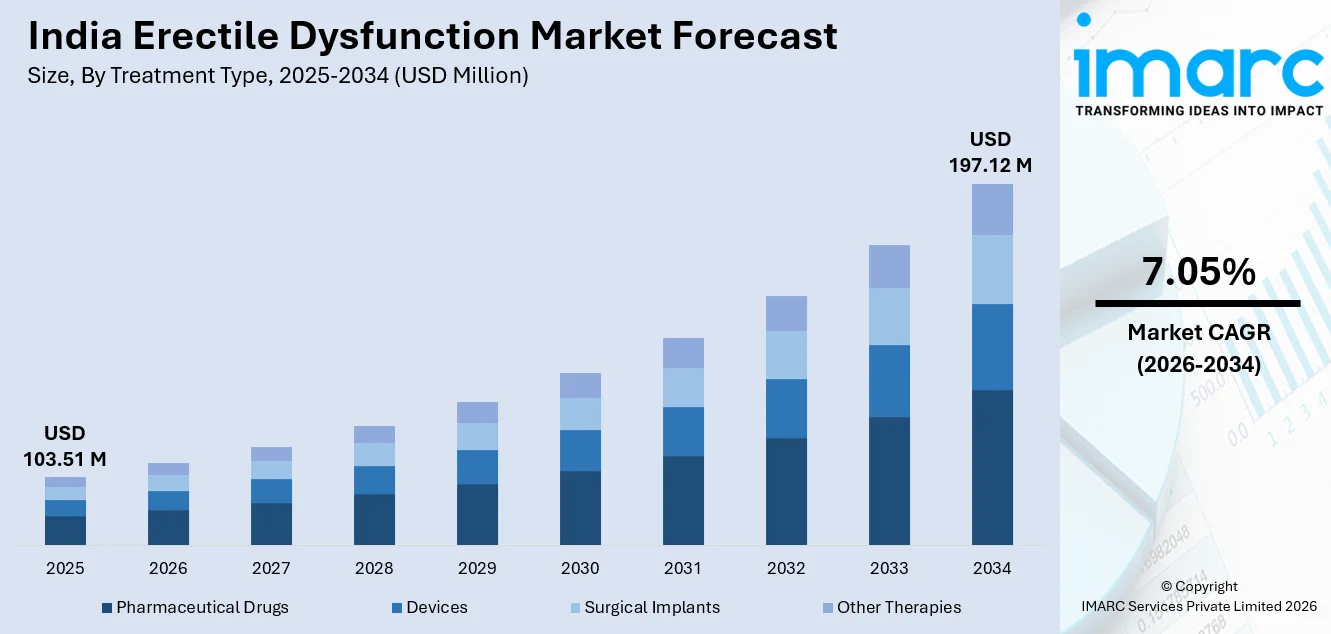

The India erectile dysfunction market size was valued at USD 103.51 Million in 2025 and is projected to reach USD 197.12 Million by 2034, growing at a compound annual growth rate of 7.05% from 2026-2034.

India's erectile dysfunction market is expanding as rising prevalence of lifestyle diseases, growing geriatric demographics, and increasing awareness of sexual health solutions reshape treatment-seeking behavior. The proliferation of telemedicine platforms is eliminating traditional access barriers, while organized retail pharmacy networks enhance product availability. Expanding government healthcare initiatives and digital health infrastructure are further strengthening patient identification pathways, supporting sustained growth across the India erectile dysfunction market share.

Key Takeaways and Insights:

- By Treatment Type: Pharmaceutical drugs dominate the market with a share of 69.8% in 2025, owing to the widespread availability of affordable generic phosphodiesterase type 5 inhibitors that offer proven clinical efficacy and convenient oral administration for erectile dysfunction management across India.

- By Drug Type: Sildenafil leads the market with a share of 44.6% in 2025. This dominance is driven by its established clinical track record, extensive generic availability from Indian pharmaceutical manufacturers, and strong physician familiarity with prescribing protocols.

- By Mode of Administration: Oral leads the market with a share of 78.3% in 2025, owing to patient preference for non-invasive treatment options that offer ease of use, rapid onset of action, and proven therapeutic outcomes across diverse age demographics.

- By Age Group: 50-59 years is the leading segment in the market with a share of 32.7% in 2025, reflecting the strong correlation between advancing age, cumulative exposure to chronic comorbidities, and progressive vascular deterioration that significantly elevates erectile dysfunction prevalence.

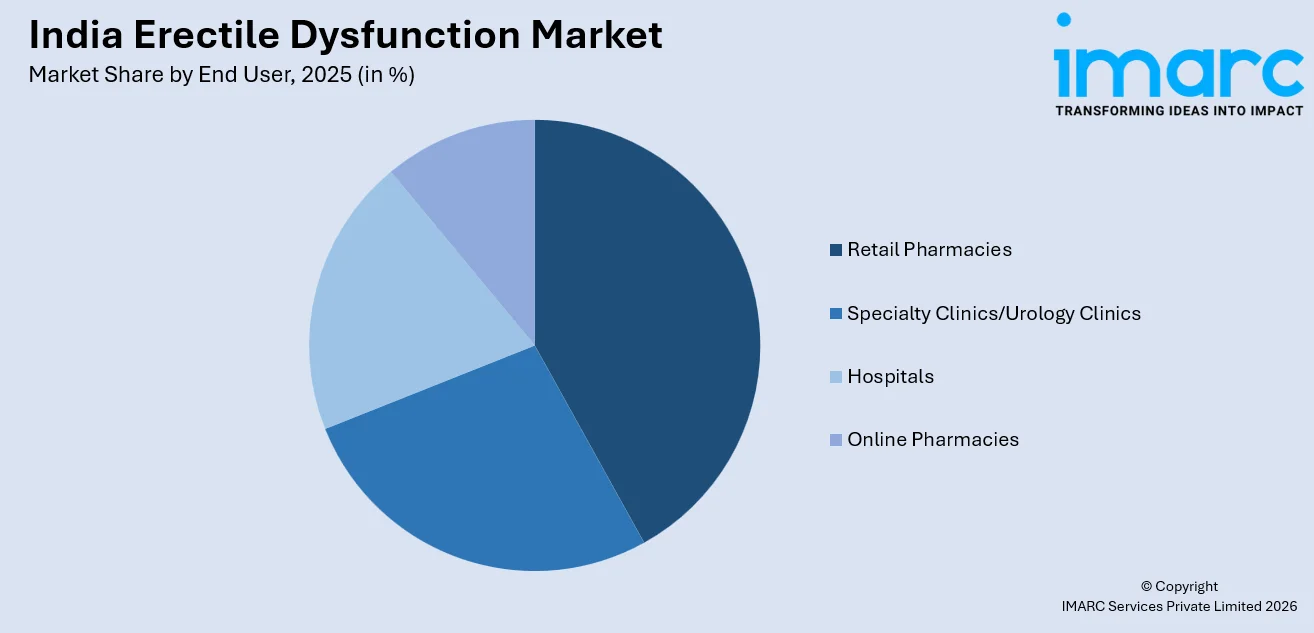

- By End User: Retail pharmacies reign the market with a share of 41.9% in 2025, driven by widespread geographic distribution, ease of access without prior appointments, and the growing organized pharmacy segment that ensures consistent product availability nationwide.

- By Region: North India comprises the largest region with 34.8% share in 2025, driven by higher population density, concentration of tertiary healthcare facilities, and greater prevalence of metabolic disorders across the densely urbanized states of Uttar Pradesh, Delhi, and Haryana.

- Key Players: The market is competitive, led by major pharma brands and strong generics, with intense price-based competition across retail and online pharmacies. Companies differentiate through faster-acting formulations, discreet packaging, teleconsult platforms, and wider distribution. Awareness campaigns and doctor engagement also shape brand preference.

To get more information on this market Request Sample

India's erectile dysfunction market is shaped by the convergence of demographic transitions, chronic disease burden expansion, and digital health infrastructure development. The pharmaceutical segment remains the primary revenue contributor, supported by India's position as the world's largest producer of generic medicines, which ensures affordable access to phosphodiesterase type 5 inhibitors across income groups. Telemedicine platforms are emerging as critical distribution channels, reducing stigma-related barriers to treatment initiation. In January 2025, Bengaluru-based male reproductive health platform Raaz raised USD 1 Million in pre-seed funding led by Fireside Ventures and Campus Fund, having served over 5,000 users since its 2024 launch with three-fold growth within three months. The aging population trajectory and rising diabetes prevalence are creating a sustained expansion of the addressable patient pool, positioning India as a high-growth opportunity within the global erectile dysfunction treatment landscape.

India Erectile Dysfunction Market Trends:

Proliferation of telemedicine platforms addressing male sexual health

India is witnessing rapid expansion of digital health platforms specifically targeting erectile dysfunction and male sexual health, removing geographic and psychological barriers to treatment. These platforms integrate teleconsultations, personalized treatment programs, and discreet medication delivery. As of mid-2025, the government's eSanjeevani platform facilitated approximately 372 million remote consultations with around 220,000 nationwide providers, demonstrating the scale at which digital health infrastructure is bridging urban-rural care gaps and supporting the India erectile dysfunction market growth.

Destigmatization of sexual health through celebrity-driven consumer brands

India's erectile dysfunction treatment landscape is undergoing cultural transformation as direct-to-consumer brands leverage celebrity endorsements and digital marketing to normalize conversations around sexual health. Bold Care, backed by Ranveer Singh, raised USD 5 Million in Series A funding in February 2025, led by Rainmatter and other investors. Founded in 2020, it offers ED and PE solutions, completed over 30 lakh orders, and surpassed INR 100 Crore ARR in December 2024. The brand's viral marketing campaigns and multi-platform distribution across quick-commerce channels are reducing societal taboos surrounding erectile dysfunction treatment.

Expansion of organized retail pharmacy networks

India’s retail pharmacy sector is steadily shifting from fragmented, unorganized outlets toward more consolidated, technology-driven chain networks. Organized pharmacy players are expanding their footprint through digital prescription verification, advanced inventory management, and integrated online ordering platforms. These developments are improving medicine availability, enhancing consumer convenience, and supporting discreet access to erectile dysfunction treatments. As pharmacy chains strengthen distribution reach and digital capabilities, the market is becoming more structured, competitive, and accessible across urban and semi-urban areas.

Market Outlook 2026-2034:

The India erectile dysfunction market is positioned for sustained expansion over the forecast period, driven by the intersection of rising chronic disease prevalence, demographic aging, and accelerating digital health adoption. According to PIB, India is experiencing a significant demographic shift, with the population aged 60 and above expected to more than double, rising from 100 million in 2011 to 230 million by 2036. The deepening penetration of telemedicine platforms and organized retail pharmacy chains is expected to significantly improve treatment accessibility, particularly in tier-two and tier-three cities where specialist availability remains limited. Growing investment in direct-to-consumer sexual health brands, combined with progressive destigmatization of erectile dysfunction through mainstream marketing campaigns, is expected to drive higher treatment-seeking rates. Furthermore, government healthcare expansion under Ayushman Bharat and increasing coverage for senior citizens are creating supportive frameworks for patient identification and management. The market generated a revenue of USD 103.51 Million in 2025 and is projected to reach a revenue of USD 197.12 Million by 2034, growing at a compound annual growth rate of 7.05% from 2026-2034.

India Erectile Dysfunction Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Treatment Type |

Pharmaceutical Drugs |

69.8% |

|

Drug Type |

Sildenafil |

44.6% |

|

Mode of Administration |

Oral |

78.3% |

|

Age Group |

50-59 Years |

32.7% |

|

End User |

Retail Pharmacies |

41.9% |

|

Region |

North India |

34.8% |

Treatment Type Insights:

- Pharmaceutical Drugs

- Devices

- Surgical Implants

- Other Therapies

Pharmaceutical drugs dominate with a market share of 69.8% of the total India erectile dysfunction market in 2025.

Pharmaceutical drugs constitute the primary treatment modality for erectile dysfunction in India, driven by the widespread availability of affordable generic formulations manufactured by domestic pharmaceutical companies. India's position as the world's largest producer of generic medicines ensures cost-effective access to phosphodiesterase type 5 inhibitors, including sildenafil, tadalafil, and vardenafil, which represent the first-line pharmacological intervention recommended by clinical guidelines. According to data from the India Brand Equity Foundation, India's pharmaceutical sector stood at INR 4,71,295 crore, approximately USD 55 Billion, in 2025, underscoring the manufacturing base supporting erectile dysfunction drug production and distribution nationwide.

The erectile dysfunction market in India shows its strongest market segment through its pharmaceutical drug sales which reflect both physician prescribing patterns and patient preference for oral medications as their most noninvasive treatment choice. The rise of digital health startups has increased this trend because they provide users with confidential telemedicine services and quick access to prescription medications. Online platforms create a safe environment for men to order products while making it easy to obtain items which leads to higher demand for prescription erectile dysfunction medications in urban areas.

Drug Type Insights:

- Sildenafil (Viagra, generics)

- Tadalafil (Cialis, generics)

- Vardenafil (Levitra, Staxyn)

- Avanafil (Stendra)

- Others

Sildenafil leads with a share of 44.6% of the total India erectile dysfunction market in 2025.

Sildenafil maintains its market dominance in India's erectile dysfunction drug sector because it demonstrates proven clinical effectiveness which doctors know well and Indian drugmakers produce multiple generic versions of the medication. The molecule which was first created as Viagra has obtained clinical proof through many years of testing and after its patent protection ended it became available at cheaper prices through domestic production of generic drugs.

Sildenafil maintains its dominant position in India because the country possesses a strong generic pharmaceutical manufacturing system that enables manufacturers to produce drugs at prices which meet international standards. Indian manufacturers supply sildenafil formulations across multiple dosage strengths including tablets oral jellies and combination products with dapoxetine for patients experiencing concurrent premature ejaculation.

Mode of Administration Insights:

- Oral

- Injectable

- Topical

- Transurethral

Oral is the largest segment, accounting for 78.3% of the total India erectile dysfunction market in 2025.

Oral administration maintains its overwhelming dominance in India's erectile dysfunction treatment landscape, reflecting patient preference for non-invasive, convenient, and discreetly administered medication formats. Phosphodiesterase type 5 inhibitors in tablet form represent the most widely prescribed first-line therapy, offering predictable onset times, established safety profiles, and ease of self-administration without clinical supervision.

The oral segment's dominance in India is further strengthened by continuous innovation in drug delivery formats, including orodispersible films, chewable tablets, and sublingual formulations designed to improve onset speed and patient convenience. Indian pharmaceutical companies are actively developing novel oral formulations that address specific patient needs, including those with swallowing difficulties or those requiring faster therapeutic action.

Age Group Insights:

- 40-49 years

- 50-59 years

- 60-69 years

- 70+ years

50-59 years holds the largest share at 32.7% of the total India erectile dysfunction market in 2025.

The 50-59 years age group represents the largest treatment-seeking demographic in India's erectile dysfunction market, reflecting the cumulative impact of age-related vascular deterioration, chronic disease burden, and hormonal changes on sexual function. This cohort experiences significantly elevated erectile dysfunction prevalence as metabolic conditions, particularly type 2 diabetes and hypertension, reach peak incidence levels during the fifth decade of life. A meta-analysis of studies conducted in India reported that approximately 60.57% of men with diabetes experience erectile dysfunction.

Market demand in the 50–59 age group is rising due to better health awareness, a greater openness to consult medical professionals, and higher spending capacity than younger consumers. Individuals in this bracket are more proactive about managing age-related health concerns, including erectile dysfunction. They increasingly rely on a mix of conventional healthcare providers and digital platforms, using teleconsultations and online pharmacies to access treatments discreetly and conveniently, strengthening overall market growth.

End User Insights:

Access the comprehensive market breakdown Request Sample

- Specialty Clinics/Urology Clinics

- Hospitals

- Online Pharmacies

- Retail Pharmacies

Retail pharmacies accounts for the highest revenue at 41.9% of the total India erectile dysfunction market in 2025.

Retail pharmacies remain the main distribution channel for erectile dysfunction medications in India due to their wide geographic reach and strong community presence. Consumers are accustomed to purchasing prescription medicines from trusted neighborhood chemists, making pharmacies a convenient and familiar access point. These outlets also offer immediate product availability and pharmacist guidance, which supports treatment adherence. Their established supply chains and relationships with pharmaceutical companies further strengthen their position in the market.

The growing consolidation of India's pharmacy retail sector through organized chains is enhancing the erectile dysfunction treatment experience by ensuring standardized product availability, professional dispensing practices, and integration with digital prescription systems. Apollo Pharmacy, MedPlus, and Wellness Forever are expanding their store networks across metropolitan and tier-two cities, bringing consistent access to erectile dysfunction medications.

Region Insights:

- North India

- South India

- West India

- East India

North India exhibits a clear dominance with a 34.8% share of the total India erectile dysfunction market in 2025.

North India leads the erectile dysfunction market owing to its substantial population base, higher concentration of tertiary healthcare facilities, and elevated prevalence of metabolic risk factors including diabetes and hypertension across densely urbanized states. According to the 2023 Census population projections, Uttar Pradesh has an estimated population of 235.7 million, making it the most populous state in India and accounting for 16.5% of the nation’s total population. The region benefits from well-established pharmaceutical distribution networks across Uttar Pradesh, Delhi, Haryana, and Punjab, ensuring robust medication availability.

In addition, rising health awareness and expanding digital healthcare adoption across major northern cities are supporting treatment uptake. Urban centers such as Delhi and Lucknow have seen growth in telemedicine platforms and online pharmacies, enabling discreet consultations and home delivery of medications. Private hospital chains and specialty clinics are also expanding men’s health services, improving diagnosis rates. Strong physician networks and aggressive pharmaceutical marketing across the region further reinforce North India’s leading position in the erectile dysfunction market.

Market Dynamics:

Growth Drivers:

Why is the India Erectile Dysfunction Market Growing?

Rising diabetes increasing the patient pool

India's rapidly escalating diabetes burden is emerging as a primary catalyst for erectile dysfunction market growth, given the well-established pathophysiological link between type 2 diabetes and erectile dysfunction. Diabetic men face a three to four times higher risk of developing erectile dysfunction compared to non-diabetic individuals, owing to diabetes-induced endothelial dysfunction, neuropathy, and vascular impairment. As diagnostic screening expands through government health programs and private healthcare initiatives, the identification of previously undetected diabetic patients is expected to substantially enlarge the addressable patient population seeking erectile dysfunction treatment. The International Diabetes Federation projects India's diabetic population to reach 134 million by 2045, indicating a sustained long-term growth trajectory for associated comorbidity treatments.

Aging population increasing age-related incidence

India's demographic transition toward an aging population structure is creating a progressively larger patient base for erectile dysfunction treatment, as sexual dysfunction prevalence increases significantly with advancing age. The country's elderly population aged 60 years and above currently stands at approximately 153 million and is projected to surge to 347 Million by 2050, representing an increase over the coming decades. Clinical studies conducted across Indian populations indicate that erectile dysfunction prevalence rises from approximately 8.6% among men aged 26-30 years to 27.6% among those aged 51-60 years, demonstrating the strong age-prevalence correlation. The Government of India's announcement in October 2024 extending Ayushman Bharat PMJAY free treatment benefits of up to INR 5 Lakh per year to approximately 6 crore senior citizens aged 70 years and above further enhances healthcare access for elderly populations, indirectly supporting improved identification and management of erectile dysfunction.

Digital health infrastructure improving treatment access

India’s expanding digital health ecosystem is reducing long-standing barriers to erectile dysfunction treatment by enabling remote consultations, electronic prescriptions, and discreet home delivery of medications. Government-backed digital health initiatives have strengthened nationwide infrastructure, supporting smoother patient identification and improved access to healthcare services. Telemedicine platforms are playing a key role in connecting individuals with qualified providers, especially for sensitive conditions where stigma often limits in-person visits. The growing integration of online consultations with pharmacy delivery networks is creating more private, convenient, and continuous treatment pathways across urban and rural areas.

Market Restraints:

What Challenges the India Erectile Dysfunction Market is Facing?

Social stigma limiting treatment seeking

Despite rising awareness efforts and the growth of digital health platforms, strong social stigma around sexual health continues to limit treatment-seeking behavior in India’s erectile dysfunction market. Many men remain reluctant to consult healthcare professionals due to shame, embarrassment, and long-standing cultural taboos. This hesitation leads to widespread underdiagnosis and delayed treatment, preventing patients from accessing effective therapies. As a result, market expansion is constrained, even as medical solutions and access channels continue to improve across the country.

Price sensitivity and limited insurance coverage restricting treatment affordability

India’s largely out-of-pocket healthcare system creates affordability barriers for long-term erectile dysfunction treatment, especially among middle- and lower-income groups. Although generic medicines are cheaper than branded options, the recurring nature of therapy can still impose a significant financial burden for price-sensitive consumers. Access is further limited by the lack of insurance support, as most policies do not cover sexual health medications. Reduced purchasing power among older adults, who are most affected by erectile dysfunction, also restricts sustained treatment uptake.

Fragmented healthcare infrastructure limiting specialist accessibility in rural areas

India’s healthcare infrastructure is still largely concentrated in urban areas, creating major access gaps for patients in rural and semi-urban regions. Many smaller pharmacies operate without consistent inventory systems or standardized dispensing practices, which can affect the availability of sensitive medications. Rural communities also face shortages of trained urologists and men’s health specialists, with expertise mostly limited to metropolitan cities and state capitals. This uneven distribution delays diagnosis and restricts access to appropriate erectile dysfunction treatment for large sections of the population.

Competitive Landscape:

The India erectile dysfunction market features a competitive landscape characterized by established generic pharmaceutical manufacturers, emerging direct-to-consumer digital health brands, and multinational pharmaceutical companies with localized distribution networks. Market participants compete on formulation innovation, pricing strategies, and distribution channel expansion across retail, hospital, and online pharmacy segments. Strategic investments in telemedicine integration, celebrity-endorsed marketing campaigns, and quick-commerce partnerships are reshaping competitive dynamics, while India's favorable regulatory environment for generic drug manufacturing continues to attract new entrants seeking to capture growing demand.

Recent Developments:

- In August 2025, Viatris launched the “EmpowerED for Life” campaign, led by its India & Access Markets division, to address erectile dysfunction stigma and encourage men to seek professional care. The initiative highlights ED as an indicator of conditions like diabetes and cardiovascular disease, using education, digital outreach, and healthcare partnerships to expand awareness and access to safe treatment.

- In May 2025, Erecticare Pro Systems partnered with urologist Niall Dickson to introduce Alma Duo shockwave therapy for erectile dysfunction in Uttar Pradesh. Developed by Alma Lasers, the FDA Class I LI-ESWT device improves blood flow through six 15-minute sessions over three weeks. Treatment is drug-free, needle-free, and costs roughly USD 1,500–USD 3,000.

India Erectile Dysfunction Market Report Coverage:

|

Report Features |

Details |

|

Base Year of the Analysis |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Units |

Million USD |

|

Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

|

Treatment Types Covered |

Pharmaceutical Drugs, Devices, Surgical Implants, Other Therapies |

|

Drug Types Covered |

Sildenafil (Viagra, generics), Tadalafil (Cialis, generics), Vardenafil (Levitra, Staxyn), Avanafil (Stendra), Others |

|

Modes of Administration Covered |

Oral, Injectable, Topical, Transurethral |

|

Age Groups Covered |

40-49 years, 50-59 years, 60-69 years, 70+ years |

|

End Users Covered |

Specialty Clinics/Urology Clinics, Hospitals, Online Pharmacies, Retail Pharmacies |

|

Regions Covered |

North India, South India, West India, East India |

|

Customization Scope |

10% Free Customization |

|

Post-Sale Analyst Support |

10-12 Weeks |

|

Delivery Format |

PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Erectile Dysfunction Market Report

The India erectile dysfunction market size was valued at USD 103.51 Million in 2025.

The India erectile dysfunction market is expected to grow at a compound annual growth rate of 7.05% from 2026-2034 to reach USD 197.12 Million by 2034.

Pharmaceutical drugs dominated the market with a share of 69.8%, driven by widespread availability of affordable generic phosphodiesterase type 5 inhibitors manufactured by India's extensive domestic pharmaceutical production base.

Key factors driving the India erectile dysfunction market include rising diabetes prevalence expanding the patient pool, rapid demographic aging amplifying age-related incidence, and government digital health infrastructure improving treatment accessibility.

Major challenges include persistent social stigma suppressing treatment-seeking behavior, price sensitivity and limited insurance coverage restricting affordability, fragmented healthcare infrastructure limiting rural specialist access, cultural taboos preventing open health discussions, and geographic maldistribution of healthcare resources.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)