India Facade Market Size, Share, Trends and Forecast by Product Type, Material, End User, and Region, 2026-2034

India Facade Market Size, Share, Trends & Forecast (2026-2034)

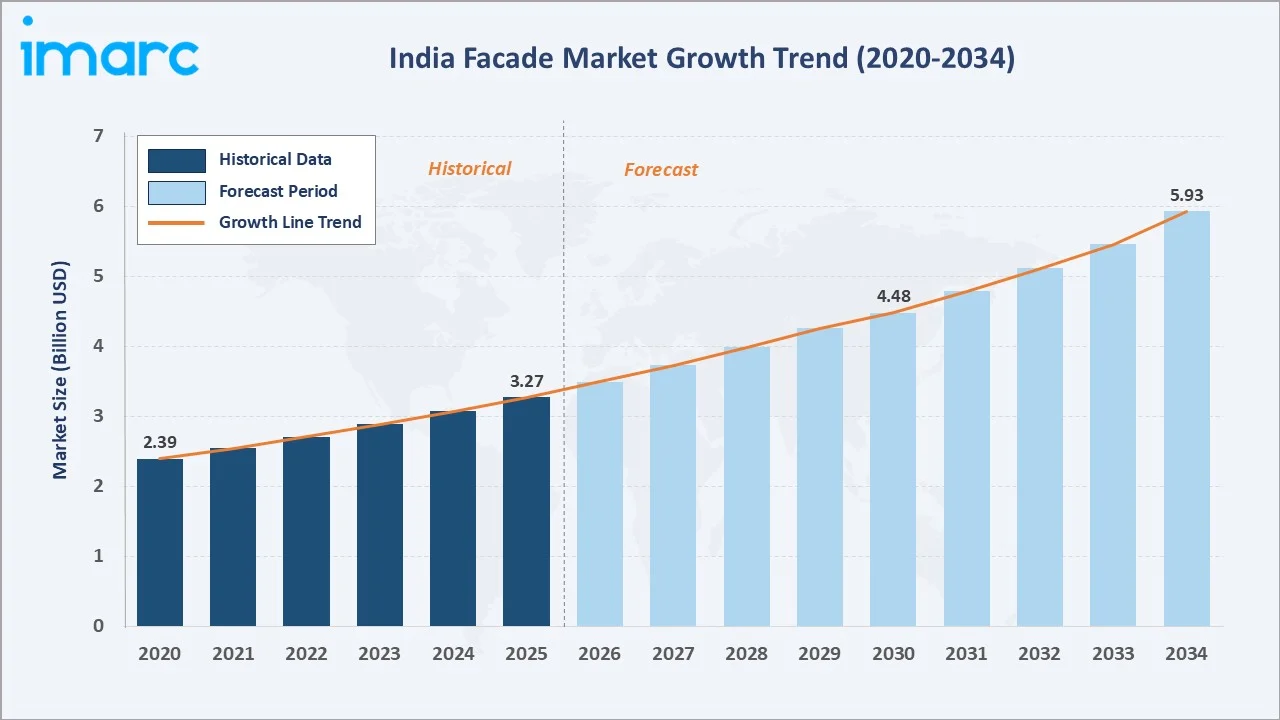

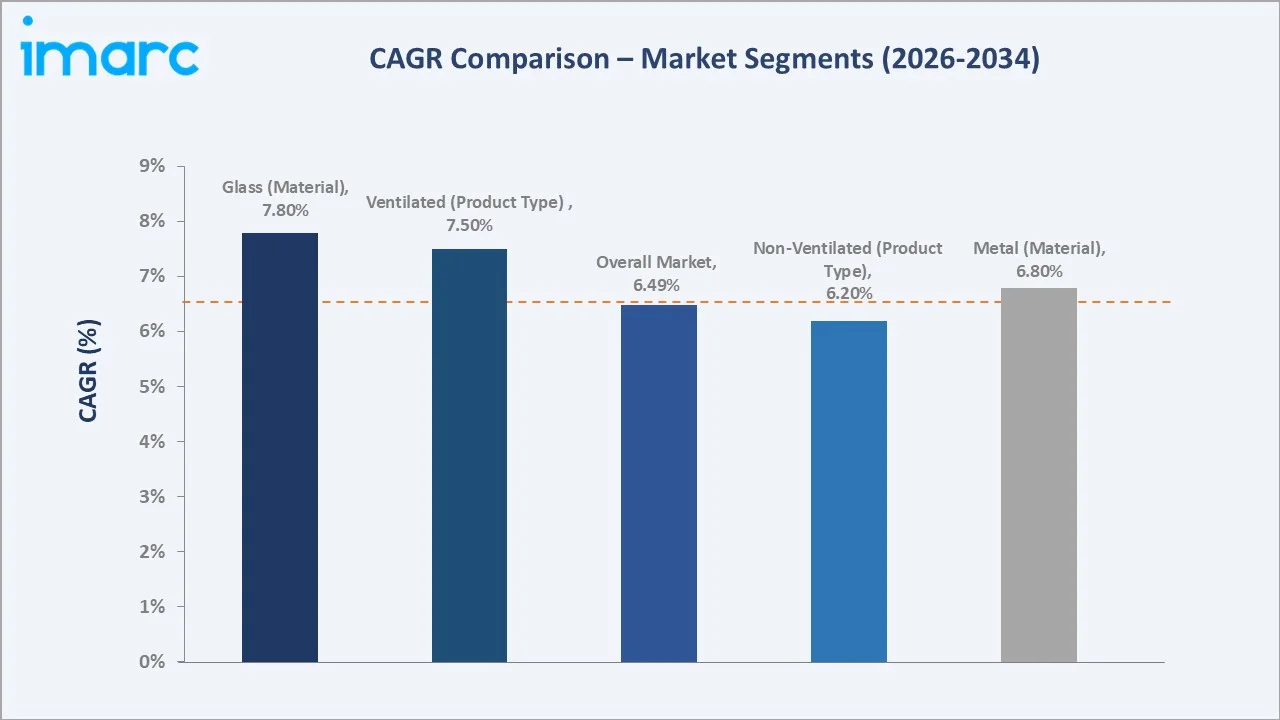

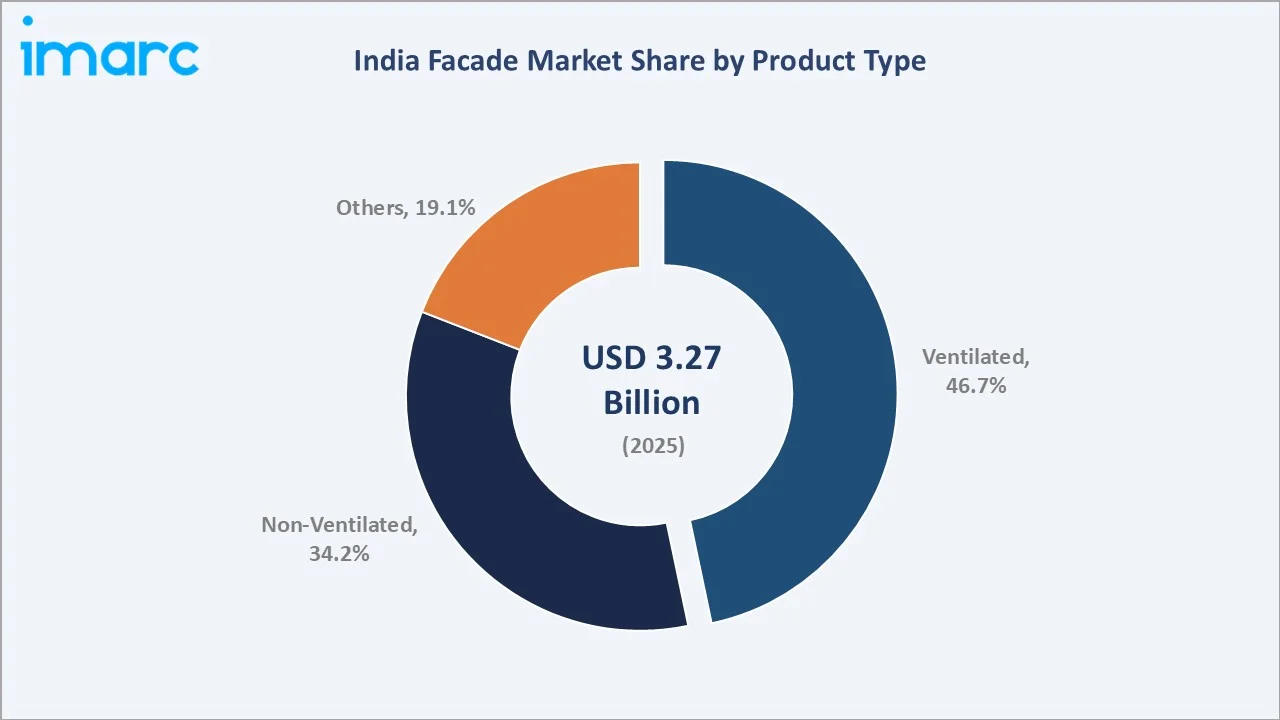

The India facade market reached USD 3.27 Billion in 2025 and is projected to reach USD 5.93 Billion by 2034, growing at a CAGR of 6.49% during 2026-2034. Rapid urbanization and the shift toward energy-efficient construction, the expansion of commercial real estate and IT parks, government-driven infrastructure programs including Smart Cities Mission and PMAY, growing adoption of green building standards, and technological advancements in facade systems are the primary growth catalysts.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 3.27 Billion |

|

Forecast Market Size (2034) |

USD 5.93 Billion |

|

CAGR (2026-2034) |

6.49% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

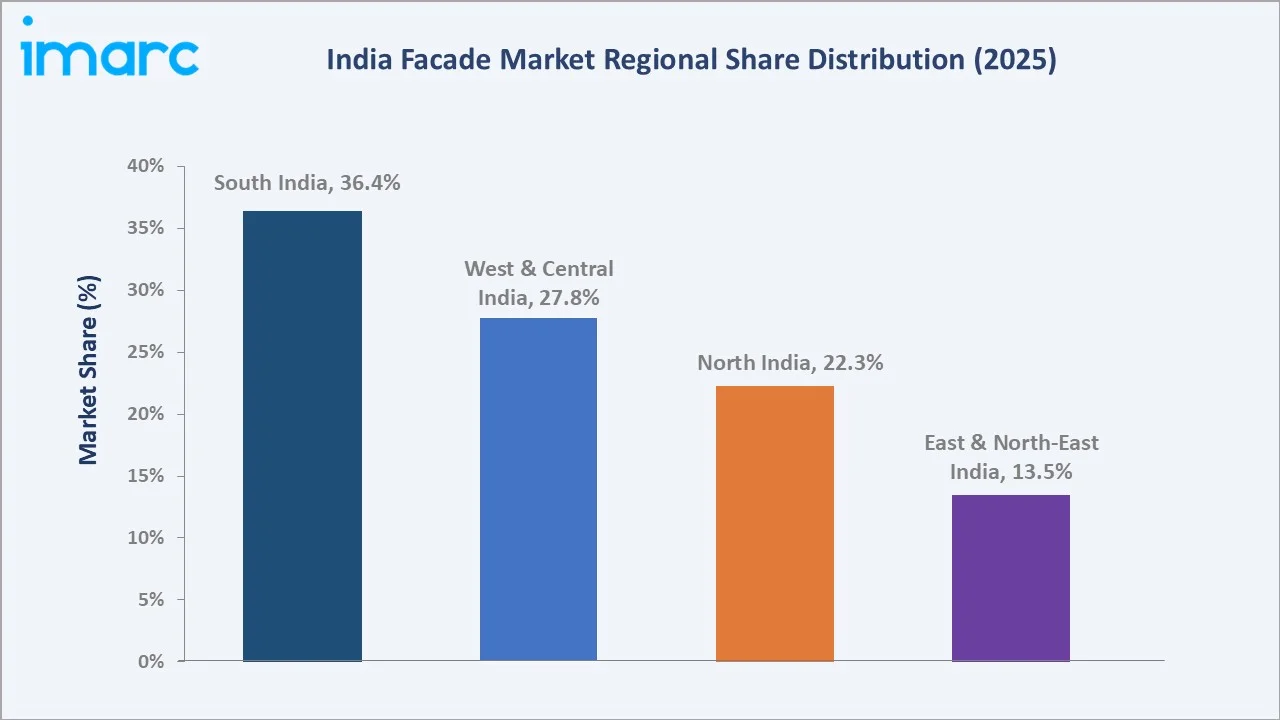

South India leads regionally, holding a 36.4% market share in 2025, anchored by Bengaluru, Hyderabad, and Chennai’s dense concentration of IT parks, commercial towers, and Special Economic Zones requiring high-performance facade systems. Ventilated facades command the dominant 46.7% product type share, driven by their superior thermal performance, adaptability to India’s diverse climatic zones, and alignment with green building certification standards such as IGBC and GRIHA.

To get more information on this market, Request Sample

India’s facade market is underpinned by three structural forces: urbanization driving high-rise residential and commercial tower construction requiring modern envelope systems, the green building movement mandating energy-efficient facades that reduce solar heat gain and HVAC loads, and the technology transition from conventional curtain walls to Building-Integrated Photovoltaic (BIPV) and intelligent facade systems that adapt dynamically to environmental conditions.

Executive Summary

The India facade market is experiencing steady, broad-based growth driven by the convergence of urban infrastructure expansion, sustainability mandates, and the modernization of India’s commercial real estate stock. The market was valued at USD 3.27 Billion in 2025 and is forecast to reach USD 5.93 Billion by 2034, growing at a CAGR of 6.49%.

Ventilated facades hold a 46.7% product type share, while glass dominates the material segment at 41.8%. South India leads regionally at 36.4%. Key players identified in the Saint-Gobain Group, Innovators, Kingspan Group, Schüco International KG, and Alfa Facade Systems Pvt. Ltd.

Key Market Insights

|

Insight |

Data |

|

Largest Product Type |

Ventilated – 46.7% share (2025) |

|

Fastest Growing Product Type |

Ventilated – ~7.5% CAGR driven by green building adoption |

|

Largest Material |

Glass – 41.8% share (2025) |

|

Fastest Growing Material |

Glass – ~7.8% CAGR driven by BIPV and curtain wall growth |

|

Leading Region |

South India – 36.4% share (2025) |

|

Top Companies |

Saint-Gobain Group, Innovators, Kingspan Group, Schüco International KG, and Alfa Facade Systems Pvt. Ltd. |

Key Analytical Observations Supporting the Above Data:

- Ventilated facades’ 46.7% share (2025) reflects their growing adoption in India’s premium commercial segment. In April 2024, Alstone launched a new range of ventilated fin louvers designed to enhance airflow and block direct sunlight, demonstrating active product innovation in this segment.

- Glass material’s 41.8% share (2025) reflects the dominance of glass curtain walls in India’s commercial office, IT park, and hospitality sectors. High-performance glass, including Low-E (low emissivity), double-glazed, and laminated safety glass, is the preferred facade material for buildings targeting IGBC Gold or Platinum certification.

- South India’s 36.4% share (2025) reflects the region’s concentration of Grade-A IT parks, SEZs, and commercial office developments in Bengaluru, Hyderabad, and Chennai that specify high-performance glass and aluminum facade systems as mandatory components of premium building envelopes.

- Non-ventilated facades’ 34.2% share (2025) reflects the widespread use of traditional wall cladding systems, including Aluminum Composite Panel (ACP) cladding, stone cladding, and external insulation composite systems, across the broader commercial and residential mid-market segment.

India Facade Market Overview

A facade is the exterior skin or envelope of a building, encompassing all external-facing systems including curtain walls, cladding, glazing systems, louvres, and sunshading elements. Facades serve the critical function of thermal insulation, solar radiation control, acoustic dampening, weatherproofing, and aesthetic articulation of the building exterior. In India, the market spans ventilated and non-ventilated facade systems manufactured from glass, aluminum and metal, natural stone, plastic composites, and specialty materials.

Macroeconomic drivers include India’s construction industry growing at 7.8% in real terms for 2024, making it one of the world’s fastest-growing construction markets; government investment of INR 111 Lakh Crore under the National Infrastructure Pipeline through 2020-2025, and the Ministry of Housing and Urban Affairs’ Smart Cities Mission driving construction of 100 smart cities requiring modern facade specifications.

Market Dynamics

To evaluate market opportunities, Request Sample

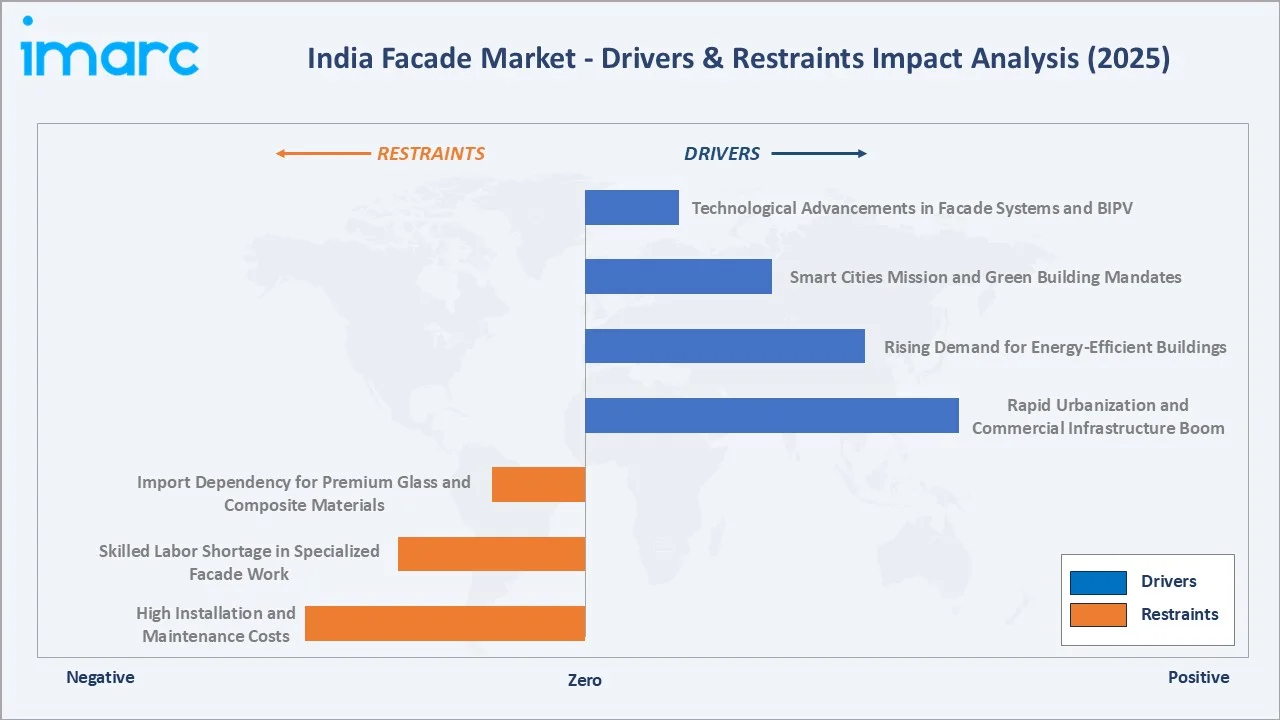

Market Drivers

- Rapid Urbanization and Commercial Infrastructure Boom: By 2030, Grade A office stock is expected to exceed the 1 billion sq. ft. mark, while annual demand and new supply are projected to reach 90-100 million sq. ft. and 75-85 million sq. ft., respectively.

- Rising Demand for Energy-Efficient Buildings: The Energy Conservation Building Code (ECBC) mandates thermal performance standards for commercial buildings that directly incentivize the specification of Low-E glass, double-glazed curtain walls, and insulated facade panels over conventional single-pane glazing.

- Smart Cities Mission and Green Building Mandates: India’s Smart Cities Mission investment of INR 2.05 lakh crore across 100 cities and GRIHA (Green Rating for Integrated Habitat Assessment) and IGBC rating requirements in smart city building codes are creating demand for ventilated facades, automated solar shading, and Building-Integrated Photovoltaic (BIPV) facade systems.

- Technological Advancements in Facade Systems and BIPV: The emergence of Building-Integrated Photovoltaic (BIPV) facades, which combine solar power generation with the weather protection function of conventional facades, represents a significant growth vector.

Market Restraints

- High Installation and Maintenance Costs: Premium ventilated facade systems with high-performance glass, aluminum framing, and sub-structure installation cost INR 1,200–2,500 per sq. ft., significantly higher than conventional paint or tile-finished exterior walls at INR 150–300 per sq. ft.

- Skilled Labor Shortage in Specialized Facade Work: Specialized facade installation requires trained facade engineers and installers that are in short supply in India. The shortage of qualified facade consultants and facade engineering contractors capable of managing complex projects extends project timelines and creates quality risks that developers seek to mitigate through value engineering to simpler systems.

- Import Dependency for Premium Glass and Composite Materials: India currently imports a significant proportion of premium facade glass and specialty composite panels from China, Europe, and the Middle East. INR depreciation and import duty fluctuations on flat glass create input cost volatility that squeezes facade contractor margins and compresses project budget certainty.

Market Opportunities

- BIPV Facade Integration for Commercial Buildings: The government’s net-zero building aspiration is creating demand for Building-Integrated Photovoltaic (BIPV) facade solutions that generate on-site renewable energy while serving as the building’s weather barrier. India’s strong solar irradiation (4–6 kWh/m²/day across most regions) makes BIPV facades economically attractive in premium commercial buildings.

- Residential High-Rise Tower Facade Premiumization: India’s luxury and premium residential segment, growing at 15–20% annually in cities like Mumbai, Delhi NCR, and Bengaluru, is increasingly specifying glass and aluminum facade systems that emulate commercial Grade-A aesthetics and deliver superior acoustic and thermal performance.

Market Challenges

- Counterfeiting of Aluminum Composite Panels (ACP): India’s ACP cladding market faces significant challenges from counterfeit and substandard Aluminum Composite Panels that imitate premium brands (Alstone, Alucomp, Alucobond) but use non-compliant polyethylene cores that do not meet fire resistance standards.

- Fragmented Project Delivery and Facade Contractor Capacity: India’s facade installation market remains fragmented, with hundreds of small and mid-sized facade contractors operating at the project level without the engineering, BIM (Building Information Modelling), and quality management capabilities required for complex curtain wall systems.

Emerging Market Trends

1. Building-Integrated Photovoltaic (BIPV) Facades

Pilot studies indicate that wall-mounted BIPV systems can generate around 30-40 kWh per sq. m. annually, meeting nearly 15-20% of a cluster’s daytime energy requirements. Pilot BIPV installations in Hyderabad’s HITEC City and Bengaluru’s IT campuses are demonstrating the technology’s commercial viability at India’s electricity tariff levels, which have been rising 5–8% annually.

2. Smart and Adaptive Facade Systems

Smart facade systems incorporating electrochromic glazing and automated external louvres, and double-skin facade configurations are being adopted by premium commercial developments seeking LEED Platinum or WELL Building Standard certification. In 2025, the Zak World of Facades India hosted its 155th edition in New Delhi, focusing on intelligent facade systems, reflecting the industry’s growing engagement with adaptive technologies.

3. Green Building Certification-Driven Facade Specification

Under IGBC, there are 4,363 registered projects covering more than 4.71 billion sq. ft., along with 1,257 certified and fully functional existing projects. Under GRIHA, around 1,000 projects have been registered, covering approximately 40 million sq. m. Green building rating systems award significant credits for facade-related measures including window-to-wall ratio optimization and daylight autonomy metrics, creating a certification-driven demand pull for high-performance ventilated facade systems and Low-E glass.

4. Natural Stone and Terracotta Facade Revival

A growing counter-trend to glass-dominant commercial facades is the revival of natural stone and terracotta cladding in premium residential and civic architecture that seeks to express regional identity and biophilic design sensibilities. Natural stone quarrying in Rajasthan (granite, marble) and South India (black granite, Kota stone) provides competitive domestic supply, while terracotta rainscreen panels from European manufacturers including Terreal and Cotto d’Este are gaining traction in India’s premium institutional and hospitality building segments.

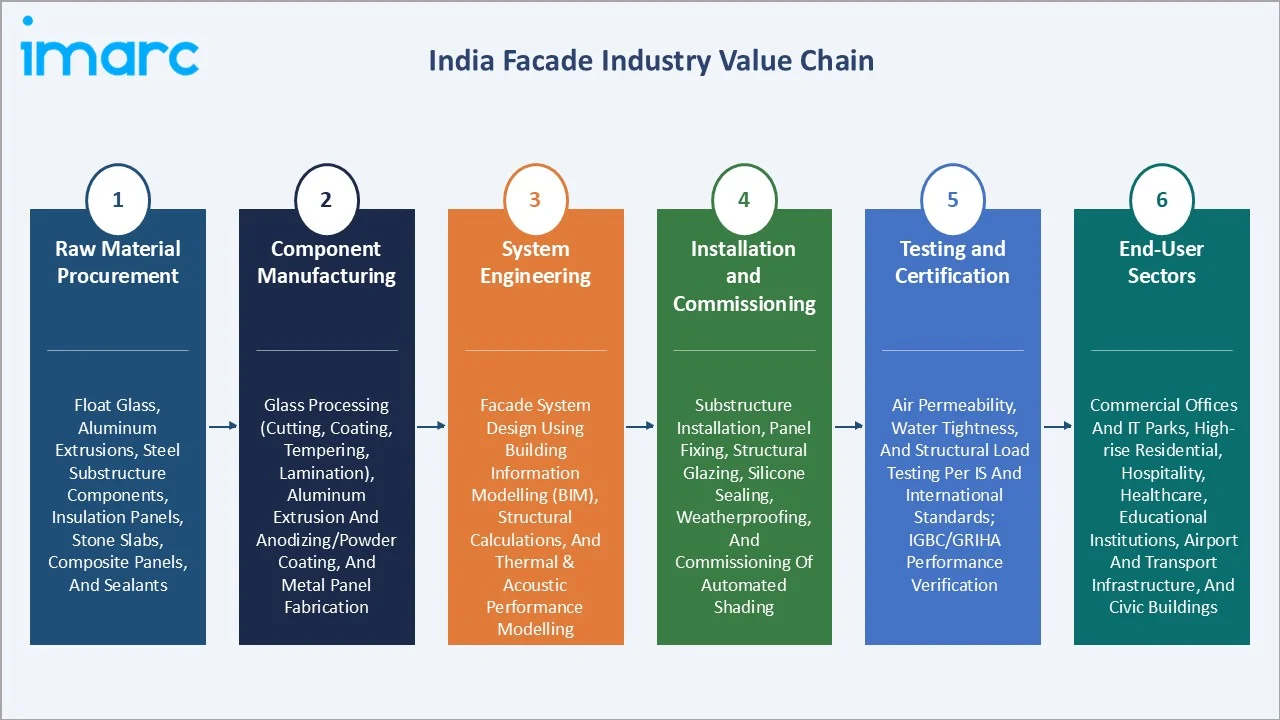

Industry Value Chain Analysis

The India facade value chain spans raw material procurement through building commissioning and post-installation maintenance, with each stage characterized by specific technical competencies and quality management requirements.

|

Stage |

Description |

|

Raw Material Procurement |

Float glass, aluminum extrusions, steel substructure components, insulation panels, stone slabs, composite panels, and sealants |

|

Component Manufacturing |

Glass processing (cutting, coating, tempering, lamination), aluminum extrusion and anodizing/powder coating, and metal panel fabrication |

|

System Engineering |

Facade system design using Building Information Modelling (BIM), structural calculations, and thermal & acoustic performance modelling |

|

Installation and Commissioning |

Substructure installation, panel fixing, structural glazing, silicone sealing, weatherproofing, and commissioning of automated shading |

|

Testing and Certification |

Air permeability, water tightness, and structural load testing per IS and international standards; IGBC/GRIHA performance verification |

|

End-User Sectors |

Commercial offices and IT parks, high-rise residential, hospitality, healthcare, educational institutions, airport and transport infrastructure, and civic buildings |

Technology Landscape in the India Facade Industry

High-Performance Glass Systems

Glass is the dominant facade material in India’s premium commercial segment at 41.8% market share, with the market progressively upgrading from basic clear float glass to high-performance variants. Low-E (low emissivity) coated glass reduces solar heat gain by 50–60% versus clear glass, directly reducing HVAC cooling loads in India’s high-irradiation climate.

Aluminum Extrusion Systems for Curtain Wall and Cladding

Thermal-break aluminum profiles, incorporating polyamide inserts that interrupt the metallic heat conduction path, achieve 40–60% better thermal performance than standard aluminum profiles, enabling ECBC compliance without transitioning to alternative framing materials. Schüco International’s system profiles represent the benchmark for precision German engineering in the premium Indian facade market.

BIM-Enabled Facade Engineering

BIM Level 2 adoption enables facade engineers to simulate thermal performance, daylighting, structural loads, and constructability in a single digital model before fabrication begins, reducing design errors, rework costs, and construction delays. International facade contractors and progressive Indian companies, including Innovators, are deploying BIM-enabled parametric facade design platforms that accelerate shop drawing production and enable mass customization of panel geometries.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product Type |

Ventilated |

46.7% |

2025 |

|

Material |

Glass |

41.8% |

2025 |

|

End User |

🔒 |

🔒 |

2025 |

|

Region |

South India |

36.4% |

2025 |

By Product Type

Ventilated facades dominate the India market with a 46.7% share in 2025. Ventilated systems create a deliberate air cavity between the outer cladding panel and the thermal insulation layer applied to the building structure, enabling natural convection that removes solar heat and moisture from the cavity. This approach delivers superior thermal performance, enhanced moisture management, and extended facade lifespan relative to non-ventilated alternatives.

To access detailed market analysis, Request Sample

Non-ventilated facades at 34.2% encompass direct-fix cladding systems where panels are bonded or mechanically fastened directly to the structural substrate or insulation without an air gap. This category includes Aluminum Composite Panel (ACP) cladding (the most widely used mid-market facade system in India), EIFS (External Insulation and Finish System), and conventional masonry cladding systems.

By Material

Glass holds the largest material share at 41.8% in 2025, reflecting its dominance as the facade material of choice for India’s premium commercial, IT park, and hospitality building segments. Glass curtain walls, from stick-built and semi-unitized systems to fully unitized high-rise curtain walls, are specified by architects seeking transparent, aesthetically aspirational building envelopes that maximize natural daylighting and communicate modernity.

Metal (predominantly aluminum) holds a 23.6% material share, encompassing aluminum composite panels, aluminum cassette and tray panels, and corrugated aluminum rainscreen cladding. Stones at 14.7% include granite, marble, sandstone, and limestone cladding panels, popular in institutional and premium residential projects for their natural aesthetics and durability.

Regional Market Insights

South India’s market leadership (36.4%, 2025) is anchored by Bengaluru’s position as India’s technology capital with 150+ million sq. ft. of operational IT park space, Hyderabad’s HITEC City and Gachibowli growth corridors, and Chennai’s OMR technology corridor, all generating sustained demand for high-performance glass and metal facade systems in Grade-A commercial towers.

|

Region |

Share (2025) |

Key Growth Drivers |

|

South India |

36.4% |

Largest concentration of Grade-A IT parks and SEZs requiring high-performance glass curtain walls; strong IGBC green building adoption; Technology corridor driving sustained commercial construction |

|

West & Central India |

27.8% |

Premium commercial real estate and high-rise residential towers; Maharashtra’s PCMC and Navi Mumbai IT corridors; commercial and industrial construction under the Delhi-Mumbai Industrial Corridor project |

|

North India |

22.3% |

Commercial office expansion; stone quarrying proximity driving natural stone cladding; government and institutional infrastructure construction across the National Capital Region |

|

East & North-East India |

13.5% |

Emerging commercial real estate growth; industrial and hospitality construction; emerging tourism infrastructure and government building programs |

West and Central India at 27.8% is the second-largest facade market, driven by Mumbai’s ongoing premium high-rise residential and commercial construction, the Bandra-Kurla Complex (BKC) and Navi Mumbai airport-linked development corridor, and Gujarat’s significant industrial and commercial infrastructure buildout in Ahmedabad’s GIFT City and Vadodara’s Alembic City.

Competitive Landscape

India’s facade market is characterized by a combination of multinational material suppliers (Saint-Gobain Group, Kingspan Group, Schüco International KG) with strong brand recognition and technical support networks, and domestic facade engineering and installation companies with deep local project execution expertise.

|

Company Name |

Brand Name |

Market Position |

Core Strength |

|

Saint-Gobain Group |

Saint-Gobain Glass |

Market Leader |

Global glass technology leadership; comprehensive Low-E, solar control, and self-cleaning glass ranges; strong architect and facade consultant specification network |

|

Innovators |

Innovators |

Market Leader |

One of India’s largest listed facade engineering and installation companies; BIM-enabled design capability; projects across IT parks, airports, and commercial towers |

|

Kingspan Group |

Kingspan Jindal |

Strong Challenger |

Insulated metal panel systems; energy-efficient building envelope leadership; Kingspan Group’s global sustainability credentials adapted for Indian building standards |

|

Schüco International KG |

Schüco |

Strong Challenger |

German-engineered premium aluminum curtain wall, window, and door systems; thermal-break technology; strong presence in premium commercial and institutional projects |

|

Alfa Facade Systems Pvt. Ltd. |

Alfa Facade Systems |

Challenger |

1,800+ projects delivered covering 10M sq. ft.; strong relationships with marquee developers |

Key Company Profiles

Saint-Gobain Group

Saint-Gobain Group operates Saint-Gobain Glass India, one of the world’s largest manufacturers of construction materials and high-performance glass. Saint-Gobain Glass India operates across three float glass manufacturing sites (at Sriperumbudur (Tamil Nadu), Bhiwadi (Rajasthan), Jhagadia (Gujarat), and adding more).

- Product Portfolio: SGG COOL-LITE solar control glass (SK series, KNT series), SGG PLANITHERM Low-E thermal insulating glass, SGG BIOCLEAN self-cleaning glass, SGG CLIMAPLUS insulated glass units, SGG SECURIT tempered safety glass, and SGG STADIP laminated glass.

- Recent Developments: In August 2025, Saint-Gobain commenced construction of its seventh float glass line (raw material for façade) at Oragadam near Chennai to strengthen its manufacturing footprint in India.

- Strategic Focus: Solar control glass specification in ECBC-compliant commercial buildings; BIPV glass development for India’s green building market; expansion of float glass manufacturing capacity to reduce import dependency; architect and facade consultant educational programs.

Innovators

Innovators is one of India’s largest publicly listed facade engineering, fabrication, and installation companies. The company provides end-to-end facade solutions from design engineering and shop drawing production through material procurement and on-site installation across India.

- Product Portfolio: Unitized and semi-unitized curtain wall systems, stick curtain wall systems, structural glazing, ACP cladding and panel facade systems, aluminum windows and doors, louvre systems, and custom architectural facade engineering solutions.

- Recent Developments: In May 2026, Innovators secured an order worth INR 84.84 crore from Reliance Industries for the design, supply, and installation of façade works at the Anant Vilas project.

- Strategic Focus: BIM-enabled facade engineering for complex curtain wall projects; in-house aluminum extrusion and glass processing fabrication capacity to improve supply chain control; adoption of parametric design tools for custom geometric facade solutions.

Kingspan Group

Kingspan Group operates Kingspan Jindal Pvt. Ltd. through a joint venture with Jindal Mectec Pvt. Ltd. It manufactures insulated metal wall and roof panel systems at its facility in India. Kingspan Group is a global leader in high-performance insulation and building envelope solutions, and the India joint venture adapts its panel technology.

- Product Portfolio: Kingspan KS series insulated wall panels (PIR, mineral wool, and glass wool core options), Kingspan QuadCore insulated panels with enhanced fire performance, IPN QuadCore hidden-fix facade panels, and Kingspan Optimo composite facade systems for commercial applications.

- Recent Developments: In April 2024, Kingspan Jindal supplied around 50,000 m² of roofing and 15,000 m² of façade systems for the Noida International Airport project in Jewar, highlighting the rising adoption of high-performance insulated sandwich panels in large-scale Indian airport infrastructure developments.

- Strategic Focus: Kingspan’s global net-zero building materials commitment informing India-specific product development; pilot projects for Kingspan’s solar-integrated metal panel systems in India’s industrial sector.

Market Concentration Analysis

India’s facade market exhibits moderate fragmentation, with multinational material suppliers (Saint-Gobain Group, Kingspan Group, Schüco International KG) commanding premium specification share and a large number of domestic facade contractors, panel fabricators, and ACP distributors competing in the mid-market and mass commercial segments.

ACP cladding, the most widely used mid-market facade system, is served by over 30 domestic manufacturers and distributors, creating significant price competition in the INR 800–1,500 per sq. ft. commercial cladding segment. Premiumization toward ventilated systems and unitized curtain walls is progressively increasing average project specification values and shifting competitive dynamics toward technically capable players with engineering and installation competencies.

Investment & Growth Opportunities

Fastest Growing Segments

BIPV facade glass (~18–22% CAGR), smart electrochromic glazing (~15–18% CAGR), unitized curtain wall systems for high-rise towers (~9–10% CAGR), and natural stone cladding for premium residential (~8% CAGR) represent the highest-growth investment vectors through 2034. Together, these sub-categories address a combined incremental opportunity of approximately USD 800 Million–1 Billion within the India facade ecosystem by 2034.

Emerging Market Expansion

India’s rapidly expanding Tier-2 city commercial real estate – with Grade-A office projects emerging in cities including Coimbatore, Kochi, Jaipur, Indore, Bhubaneswar, and Chandigarh – represents an incremental facade market of approximately USD 500–700 Million by 2034. Entry strategies for facade suppliers targeting these emerging markets include dealer-fabricator networks, ACP distribution partnerships, and project-specific direct sales to Tier-2 city developers.

Venture and Institutional Investment Trends

- India’s National Infrastructure Pipeline (INR 111 Lakh Crore through 2025) includes 100 smart city projects, 100+ airport infrastructure upgrades, and national highway rest area development, all categories requiring modern facade specifications that create structured demand for advanced glass and metal envelope systems.

- IGBC and GRIHA green building certification adoption creates a structured specification pull for high-performance facade systems. Developers targeting IGBC Gold or above certification systematically invest in ventilated facades, Low-E glass, and external shading that deliver the energy performance credits required for rating achievement.

Future Market Outlook (2026-2034)

India’s facade market is positioned for sustained above-GDP growth through 2034. From a base of USD 3.27 Billion in 2025, the market is projected to reach USD 5.93 Billion by 2034, representing incremental value creation of USD 2.66 Billion at a CAGR of 6.49%. This trajectory is structurally supported by India’s construction sector’s sustained 7–8% annual growth and the green building movement’s systematic elevation of facade performance specifications.

By 2034, the India facade market will be characterized by greater BIPV integration, smart adaptive facade system adoption in premium commercial buildings, and the progressive displacement of conventional ACP cladding by fire-rated and certified ventilated facade systems following the enforcement of BIS fire safety standards.

Research Methodology

Primary Research

Primary research comprised structured interviews with over 110 industry participants in 2024–2025, including facade engineering companies, glass and panel manufacturers, aluminum extrusion producers, EPC contractors, real estate developers, facade consultants, and institutional investors with exposure to India’s construction materials sector.

Secondary Research

Secondary research encompassed company annual reports, IGBC and GRIHA certification databases, Ministry of Housing and Urban Affairs Smart Cities program reports, BIS (Bureau of Indian Standards) standards for glass and cladding, DGFT import-export data for glass and aluminum (HS Codes 7007, 7016, 7606), and industry publications including Facade Architecture, Construction World, and Architecture + Design India.

Forecasting Models

Market size estimations were derived using top-down and bottom-up forecasting, incorporating commercial and residential construction floor area data, facade intensity (USD/sq. ft.) by building category, material split projections by segment, and green building penetration rates. A base-case CAGR of 6.49% reflects consensus estimates validated against construction activity indicators from FY 2020 to FY 2025.

India Facade Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Ventilated, Non-Ventilated, Others |

| Materials Covered | Glass, Metal, Plastic and Fibres, Stones, Others |

| End Users Covered | Commercial, Industrial, Residential |

| Regions Covered | South India, North India, West and Central India, East and North East-India |

| Companies Covered | Saint-Gobain Group, Innovators, Kingspan Group, Schüco International KG, Alfa Facade Systems Pvt. Ltd., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the India facade market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the India facade market.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the India facade industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the India Facade Market Report

The India facade market reached USD 3.27 Billion in 2025 and is projected to reach USD 5.93 Billion by 2034.

The market is expected to grow at a CAGR of 6.49% during 2026-2034, driven by urbanization, commercial real estate expansion, green building mandates, and technological advancements in BIPV and smart facade systems.

South India leads with a 36.4% share in 2025, anchored by Bengaluru, Hyderabad, and Chennai’s large concentration of IT parks and Grade-A commercial office towers that specify high-performance glass and metal facade systems.

Ventilated facades hold the largest share at 46.7% in 2025, driven by their superior thermal performance, adaptability to India’s diverse climatic conditions, and alignment with green building certification requirements.

Glass holds the largest material share at 41.8%, reflecting its dominance in premium commercial curtain wall applications, IT parks, hospitality buildings, and high-rise residential towers seeking modern aesthetic and energy-efficient building envelopes.

Key players include Saint-Gobain Group, Innovators, Kingspan Group, Schüco International KG, and Alfa Facade Systems Pvt. Ltd.

Glass is growing at approximately 7.8% CAGR because of rising adoption of high-performance glass curtain walls in India’s premium commercial and IT park segment, and the premiumization of residential high-rise tower facades.

Key challenges include high installation and maintenance costs limiting mid-market penetration, skilled labor shortage for specialized facade installation, and the fragmented nature of India’s facade contractor market limiting complex system adoption.

BIPV facade glass manufacturing, smart electrochromic and adaptive facade systems, domestic float glass capacity expansion under Make in India, and premium residential high-rise curtain wall systems represent the highest-growth investment opportunities through 2034.

India’s green building movement is systematically elevating facade performance requirements by making window-to-wall ratio compliance, Low-E glass specification, and ventilated facade thermal performance essential components of achieving IGBC Gold/Platinum and GRIHA 4/5 star building certifications, directly driving market premiumization.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)