India Fertility Services Market Size, Share, Trends and Forecast by Cause of Infertility, Procedure, Service, End-User, and Region, 2026-2034

India Fertility Services Market Size, Share, Trends & Forecast (2026-2034)

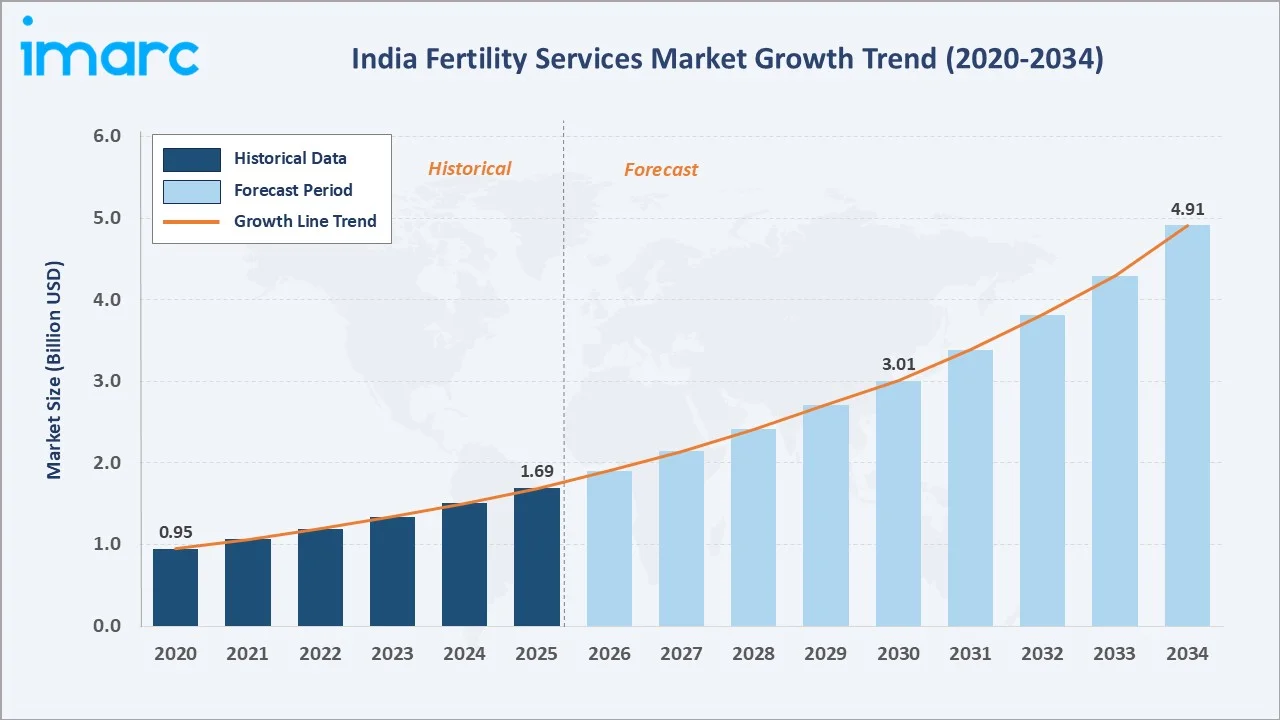

The India fertility services market reached USD 1.69 Billion in 2025 and is projected to reach USD 4.91 Billion by 2034, growing at a CAGR of 12.20% during 2026-2034. Expanding infertility awareness, rising lifestyle-linked health conditions, and improving access to assisted reproductive technologies (ART) are the central forces behind this growth. Delayed marriage and childbearing among urban professionals are significant structural drivers.

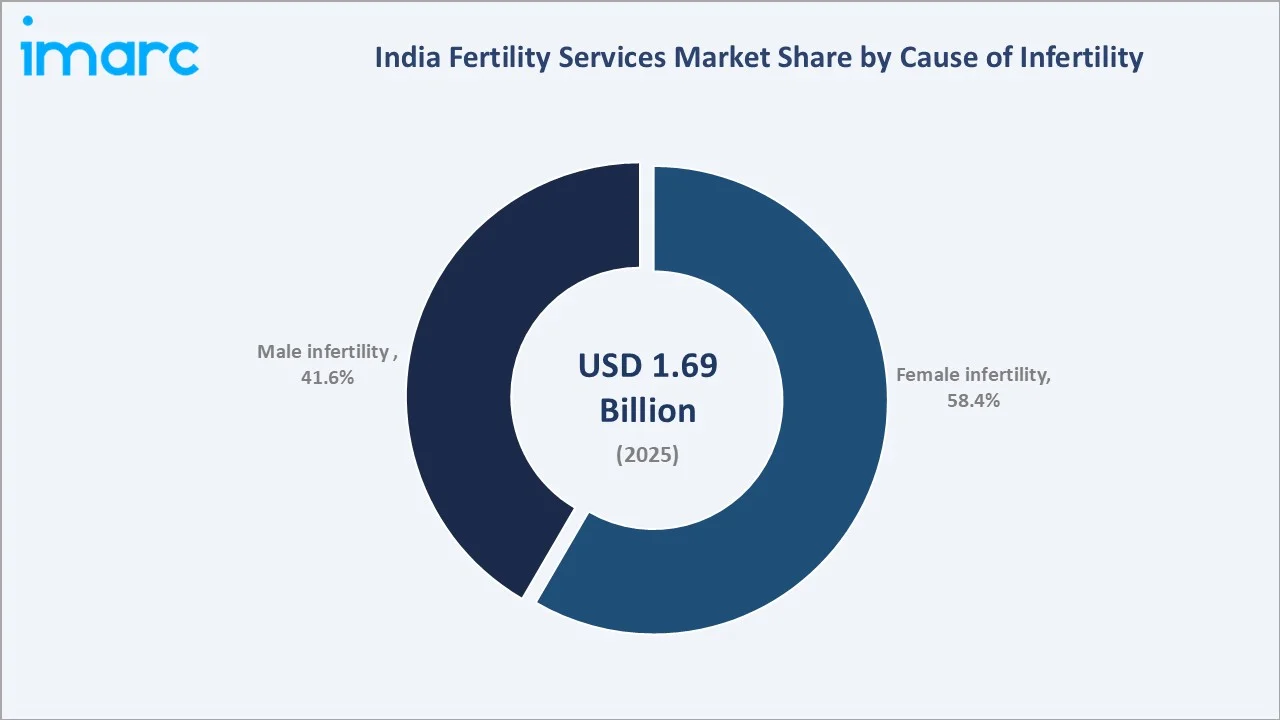

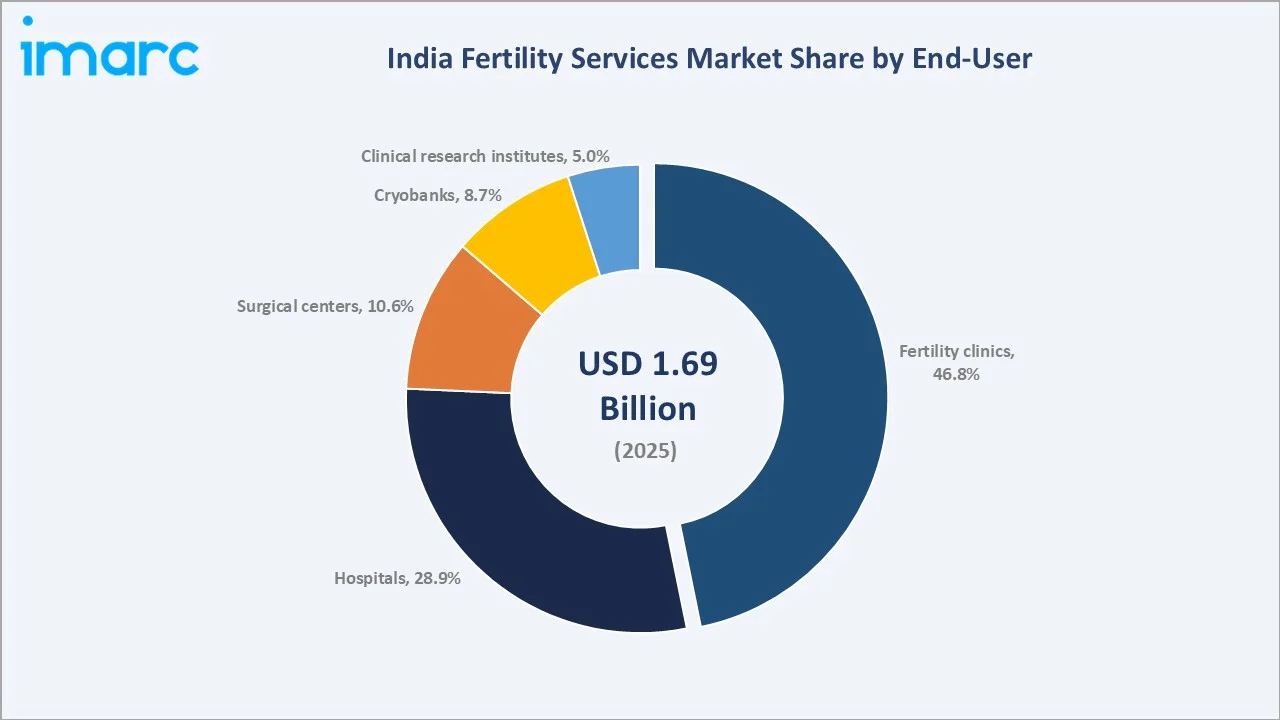

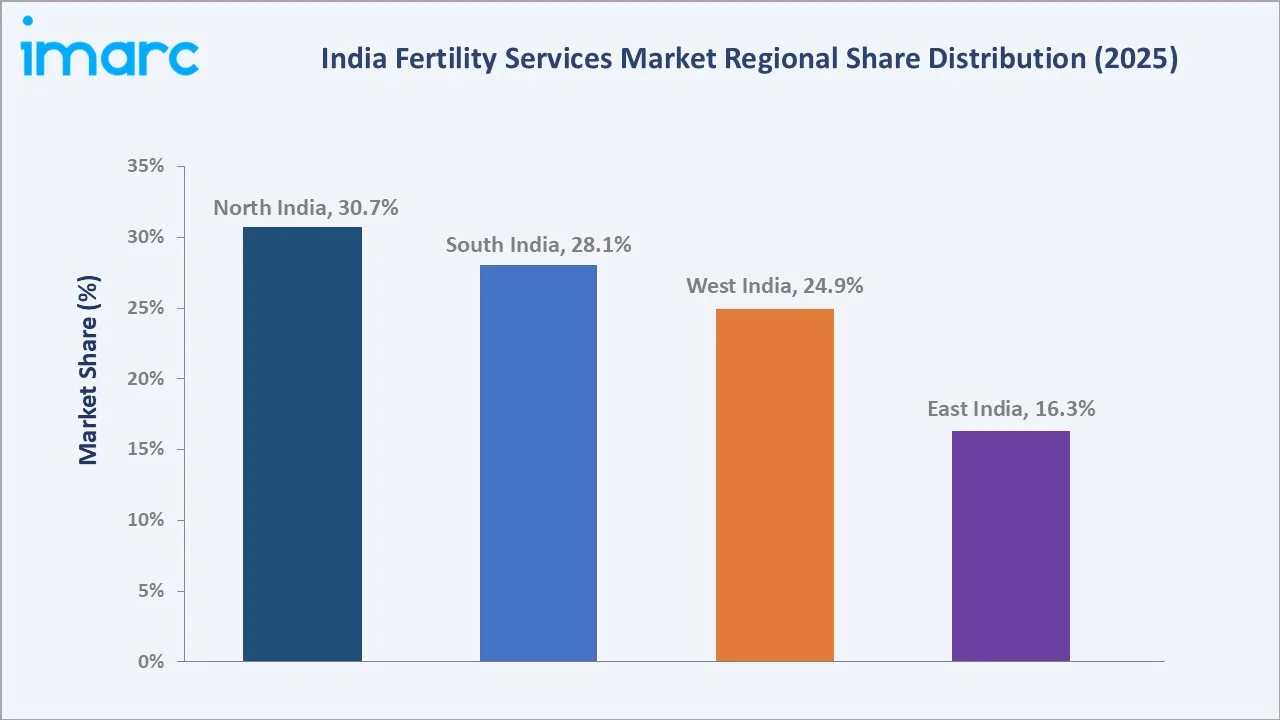

Fertility clinics lead end-user contribution at 46.8%, reflecting their specialized infrastructure advantage. Female infertility accounts for 58.4% of the market by cause. North India commands 30.7% regional share, driven by Metro-level hospital density. The market expanded from USD 0.95 Billion in 2020 to USD 1.69 Billion in 2025, anchored at USD 3.01 Billion in 2030.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 1.69 Billion |

|

Forecast Market Size (2034) |

USD 4.91 Billion |

|

CAGR (2026-2034) |

12.20% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Cause |

Female Infertility (58.4%, 2025) |

|

Leading End-User |

Fertility Clinics (46.8%, 2025) |

|

Leading Region |

North India (30.7%, 2025) |

To get more information on this market, Request Sample

The India fertility services market expanded from USD 0.95 Billion in 2020 to USD 1.69 Billion in 2025. Anchored at USD 3.01 Billion in 2030 and forecast to reach USD 4.91 Billion by 2034, the market reflects a structural shift in reproductive health awareness and ART adoption across urban and semi-urban India. India now performs an estimated 300,000-350,000 IVF cycles annually, yet the potential demand is 1-1.5 million, highlighting a significant and investable treatment gap.

Executive Summary

India fertility services market at USD 1.69 Billion in 2025 represents one of Asia's fastest-growing reproductive healthcare segments. A combination of rising infertility prevalence, delayed parenthood, growing awareness, and improving affordability of ART procedures are driving a consistent double-digit expansion. The National Family Health Survey (NFHS-5, 2019-21) noted a decline in Total Fertility Rate from 2.2 to 2.0, signaling a broader demographic shift that is simultaneously reflecting declining natural fertility.

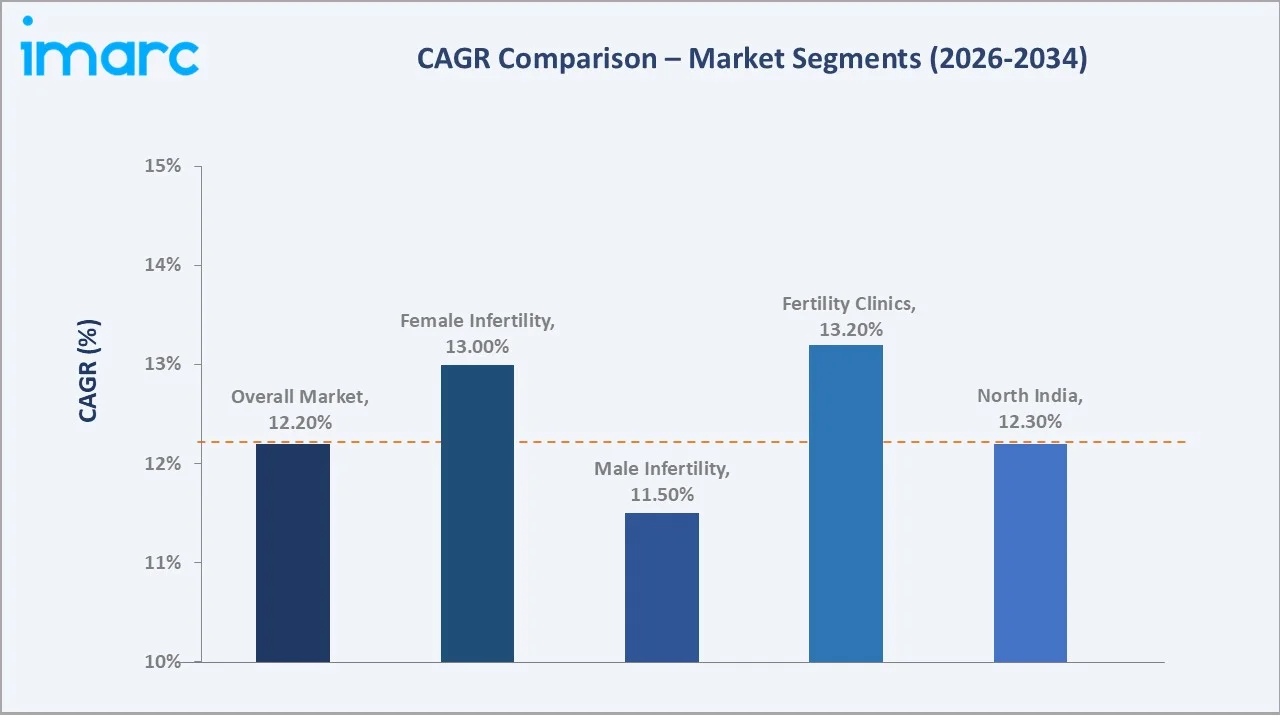

India's market is structurally distinguished by its vast and largely underpenetrated patient base. Approximately 10-15% of Indian couples experience infertility, yet ART utilization remains low relative to demand. Fertility clinics lead end-user share at 46.8% in 2025, owing to their specialized embryology labs and dedicated patient protocols. Female infertility drives 58.4% of the total cause-based market. The market is forecast to reach USD 4.91 Billion by 2034, at a 12.20% CAGR. North India leads regionally at 30.7% backed by Delhi-NCR's advanced hospital network.

Key Market Insights

|

Insight |

Data |

|

Leading Cause Segment |

Female Infertility - 58.4% share (2025) |

|

Leading End-User |

Fertility Clinics - 46.8% market share (2025) |

|

Leading Region |

North India - 30.7% share (2025) |

|

Market Opportunity |

Tier-2 city clinic expansion; AI-assisted ART; egg freezing adoption; male infertility diagnostics |

|

Key Growth Driver |

Rising infertility prevalence and increasing ART awareness among 25-40 age group |

- Female Infertility at 58.4%: PCOS, endometriosis, and blocked fallopian tubes are the primary contributors to female infertility in India. Delayed childbearing among urban working women has amplified diagnosis rates, sustaining the dominance of this segment.

- Fertility Clinics at 46.8%: Specialized clinics offer comprehensive IVF, IUI, ICSI, and cryopreservation under one roof. Their competitive success rate advantage over general hospitals makes them the preferred choice for patients seeking ART.

- North India at 30.7%: Delhi-NCR hosts a high concentration of accredited fertility clinics, with well-established referral networks. Regulatory clarity under the ART (Regulation) Act, 2021 has strengthened formal care pathways in this region.

- Hospitals at 28.9%: Multi-specialty hospitals increasingly integrate fertility units backed by gynecology, endocrinology, and urology departments. Hospital-grade infrastructure provides reassurance to complex infertility cases.

- South India at 28.1%: Bengaluru, Chennai, and Hyderabad show above-average fertility clinic density. The region benefits from a strong IT-sector workforce with higher health spending and awareness.

India Fertility Services Market Overview

India fertility services market encompasses diagnostic, medical, and procedural services designed to address male and female infertility through ART and related interventions. The ecosystem integrates pharmaceutical suppliers, advanced embryology laboratories, fertility clinics, hospital fertility units, cryobanks, and telemedicine platforms. Core procedures include IVF with and without ICSI, IUI, surrogacy, embryo freezing, and egg banking.

Macroeconomic forces shaping the market include rising disposable incomes across urban India, growing health insurance adoption, government regulation under the Assisted Reproductive Technology (Regulation) Act 2021 and the Surrogacy (Regulation) Act 2021 and increasing private equity investment in fertility chain consolidation. Medical tourism from South Asia and Southeast Asia adds an incremental demand layer to India's fertility hub cities.

Market Dynamics

To evaluate market opportunities, Request Sample

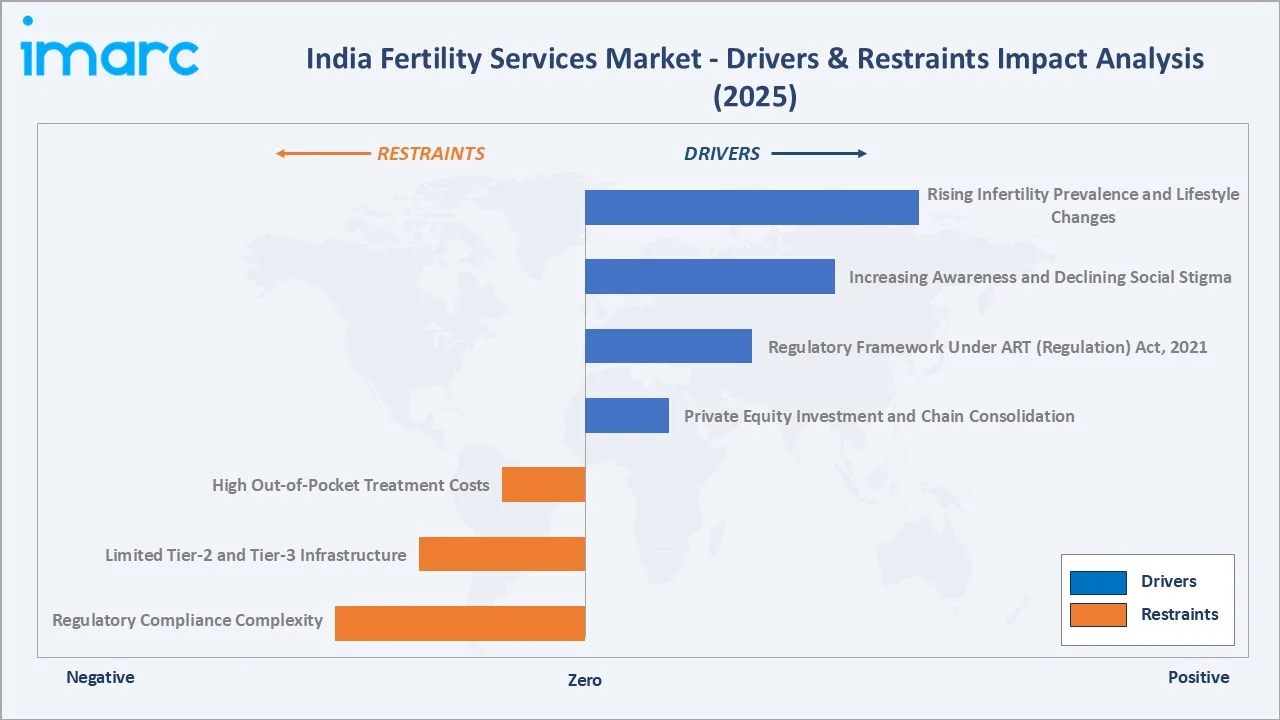

Market Drivers

- Rising Infertility Prevalence and Lifestyle Changes: An estimated 10-15% of Indian couples experience infertility, with lifestyle factors such as sedentary habits, stress, obesity, and environmental pollutants playing an increasing role. PCOS affects approximately 1 in 5 Indian women of reproductive age, per published clinical data. This structural rise in infertility cases directly expands the addressable market for fertility diagnostic and treatment services.

- Increasing Awareness and Declining Social Stigma: Media campaigns, digital health platforms, and celebrity disclosures around infertility treatment have materially reduced social stigma associated with ART in urban India. Fertility service adoption is highest among the 25-40 age group in metropolitan areas. Increased physician-patient open dialogue is translating into earlier diagnosis and treatment initiation.

- Regulatory Framework Under ART (Regulation) Act, 2021: The ART (Regulation) Act, 2021 established a formal licensing and oversight structure for fertility clinics and sperm banks in India. This regulatory clarity has improved institutional investor confidence and encouraged organized chain expansion. It has also raised quality standards, driving patients toward accredited providers and away from unregulated operators.

- Private Equity Investment and Chain Consolidation: Significant PE investment has flowed into India's fertility sector. In March 2026, Nova IVF acquired Craft Fertility for approximately USD 40 million, expanding its South India footprint. Consolidation is creating larger networks with standardized clinical protocols, improving both care quality and commercial scale.

Market Restraints

- High Out-of-Pocket Treatment Costs: A single IVF cycle in India costs between INR 1.5 lakh to INR 2.5 lakh, with multiple cycles often required. The majority of health insurance policies do not cover fertility treatment. This creates a significant affordability barrier, particularly for middle-income and semi-urban families, limiting ART penetration outside major cities.

- Limited Tier-2 and Tier-3 Infrastructure: Specialized fertility clinic infrastructure, embryology labs, and trained reproductive medicine specialists remain concentrated in Tier-1 cities. The shortage of trained ART specialists outside metro areas restricts care access for a significant proportion of the infertile population in smaller cities and rural areas.

Market Opportunities

- Egg Freezing and Fertility Preservation Services: Growing career-first priorities among urban Indian women are driving demand for elective egg freezing. Fertility preservation services are an emerging revenue stream for clinics, creating recurring patient relationships beyond immediate IVF cycles. In July 2025, Seeds of Innocence launched Asia's first Home IVF platform, combining virtual consultations with app-based monitoring, significantly improving accessibility in underserved regions.

- Male Infertility Diagnostics and Treatment Expansion: Male infertility constitutes 41.6% of the cause-based market, yet awareness and treatment-seeking remains lower than for female infertility. Expanding male fertility diagnostic services, andrology clinics, and ICSI treatments represents a commercially underdeveloped and high-growth opportunity within the overall market.

Market Challenges

- Regulatory Compliance Complexity: The ART Regulation Act and Surrogacy Regulation Act require multi-level registration, record-keeping, and reporting obligations. Compliance costs and administrative complexity are a barrier for smaller standalone fertility clinics, potentially creating market exit pressure among under-resourced operators and consolidating care among chain providers.

- Shortage of Trained Reproductive Medicine Specialists: India faces a structural shortage of trained reproductive endocrinologists and embryologists. The expansion of fertility clinic chains into Tier-2 cities is constrained by the limited talent pool. Training and talent retention remain critical bottlenecks for sustaining the market's double-digit growth trajectory.

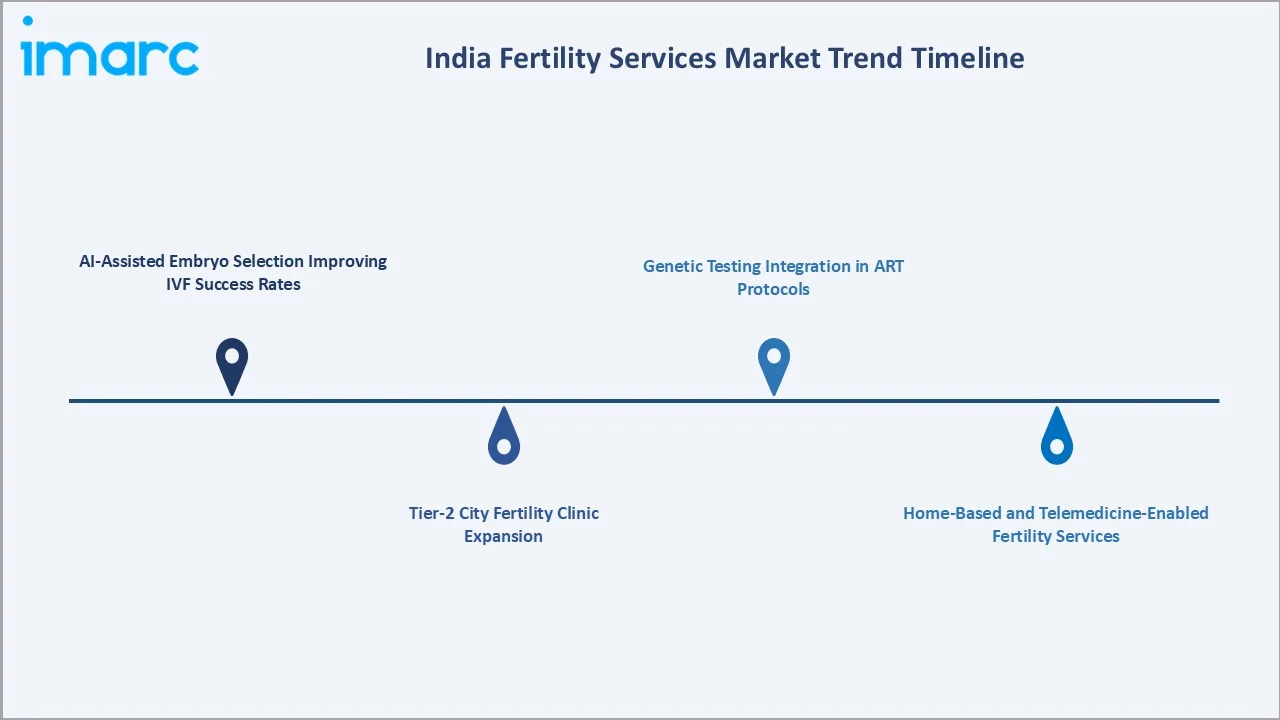

Emerging Market Trends

1. AI-Assisted Embryo Selection Improving IVF Success Rates

Artificial intelligence is being deployed in leading Indian fertility clinics for automated embryo grading, sperm morphology assessment, and predictive implantation scoring. AI-assisted selection reduces failed cycles and improves live birth rates. In 2025, India's top fertility centers reported live birth success rates of up to 50%-60% for women under 35, driven partly by AI integration.

2. Tier-2 City Fertility Clinic Expansion

Organized fertility chains are systematically expanding into Tier-2 cities including Jaipur, Lucknow, Coimbatore, and Indore. In January 2024, CK Birla Healthcare Pvt. Ltd. introduced a new fertility clinic in Meerut, Uttar Pradesh. The expansion is supported by a growing urban professional middle-class population with rising disposable incomes and fertility awareness.

3. Genetic Testing Integration in ART Protocols

Pre-implantation Genetic Testing (PGT) and Next Generation Sequencing (NGS) are increasingly integrated into IVF cycles in India. In February 2024, Kerala-based Sabine Hospital announced plans to install an NGS machine to detect genetic disorders in embryos. This trend improves IVF success rates and is particularly relevant for patients with recurrent implantation failure.

4. Home-Based and Telemedicine-Enabled Fertility Services

Digital health platforms are enabling remote fertility consultations, hormonal cycle monitoring via apps, and at-home hormone injections under physician supervision. Seeds of Innocence launched Asia's first Home IVF platform in July 2025, combining virtual care with at-home treatment delivery. This innovation is expected to expand ART access to Tier-3 cities and rural populations.

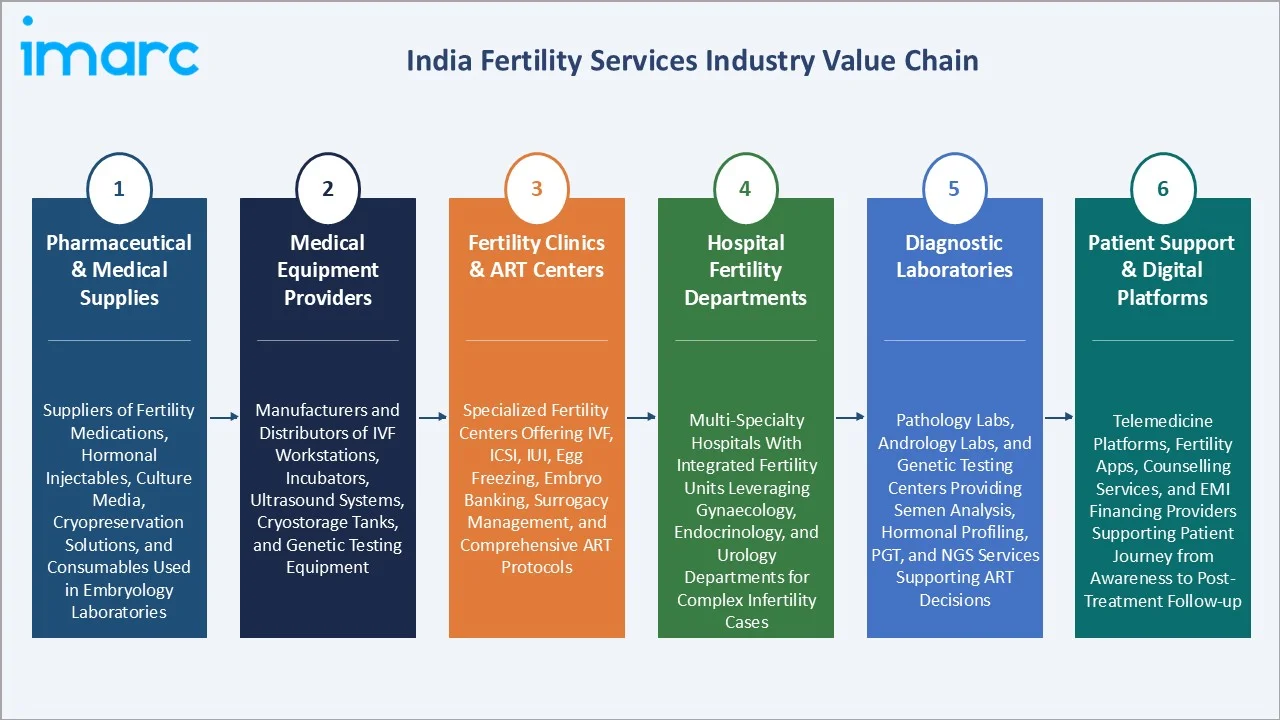

Industry Value Chain Analysis

India fertility services value chain encompasses multiple specialized stages, each contributing to the delivery of ART outcomes. The chain integrates pharmaceutical and equipment suppliers, clinical service providers, diagnostic laboratories, and patient support services into a highly regulated and quality-dependent ecosystem.

|

Stage |

Key Participants |

|

Pharmaceutical & Medical Supplies |

Suppliers of fertility medications, hormonal injectables, culture media, cryopreservation solutions, and consumables used in embryology laboratories |

|

Medical Equipment Providers |

Manufacturers and distributors of IVF workstations, incubators, ultrasound systems, cryostorage tanks, and genetic testing equipment |

|

Fertility Clinics & ART Centers |

Specialized fertility centers offering IVF, ICSI, IUI, egg freezing, embryo banking, surrogacy management, and comprehensive ART protocols |

|

Hospital Fertility Departments |

Multi-specialty hospitals with integrated fertility units leveraging gynaecology, endocrinology, and urology departments for complex infertility cases |

|

Diagnostic Laboratories |

Pathology labs, andrology labs, and genetic testing centers providing semen analysis, hormonal profiling, PGT, and NGS services supporting ART decisions |

|

Patient Support & Digital Platforms |

Telemedicine platforms, fertility apps, counselling services, and EMI financing providers supporting patient journey from awareness to post-treatment follow-up |

The diagnostic and pharmaceutical supply stage is the most commercially upstream node, with culture media quality, hormonal stimulation protocols, and genetic testing tools critically influencing IVF success rates and clinic differentiation strategies. The patient support and digital platforms layer is the fastest evolving stage, increasingly integrating AI-driven cycle monitoring and remote care delivery.

Technology Landscape in the India Fertility Services Industry

Assisted Reproductive Technology (ART) Protocols

IVF with ICSI is the dominant technology procedure in India's fertility services market, offering higher fertilization rates for male factor infertility. Conventional IVF represents approximately 45% of procedure volume (2025). Frozen embryo transfer (FET) cycles are growing rapidly, supported by improved cryopreservation protocols that allow multiple transfer attempts from a single stimulation cycle.

Genetic Testing Technologies

Pre-implantation Genetic Testing for Aneuploidies (PGT-A) and Next Generation Sequencing (NGS) are being integrated into premium IVF protocols across top fertility chains. These technologies screen embryos for chromosomal abnormalities, reducing miscarriage rates and improving successful implantation rates. Clinical adoption is expanding beyond Tier-1 cities as equipment costs decline.

Cryopreservation and Vitrification

Vitrification - ultra-rapid oocyte and embryo freezing - has replaced slow-freezing protocols in leading Indian fertility clinics, significantly improving post-thaw survival rates. This technology underpins the growth of egg freezing and embryo banking services. Cryobanks managing 8.7% of end-user market share directly depend on advanced vitrification infrastructure.

Digital Health and AI Integration

AI-based embryo grading platforms, app-based hormone monitoring, and telemedicine-enabled fertility consultations are being adopted by leading clinic chains. Seeds of Innocence's Home IVF platform (launched July 2025) exemplifies how digital health technology is extending ART access beyond physical clinic boundaries. The IHW-ISAR 6th National IVF Summit (July 2025) has focused specifically on using technology to expand access in Tier-2 and rural India.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Cause of Infertility |

Female Infertility |

58.4% |

2025 |

|

Procedure |

🔒 |

🔒 |

2025 |

|

Service |

🔒 |

🔒 |

2025 |

|

End-User |

Fertility Clinics |

46.8% |

2025 |

|

Region |

North India |

30.7% |

2025 |

By Cause of Infertility

Female infertility leads at 58.4% in 2025. PCOS, endometriosis, uterine abnormalities, and blocked fallopian tubes are the primary clinical drivers. The increasing prevalence of PCOS among Indian women aged 18-35, combined with delayed childbearing trends in metropolitan areas, sustains female infertility's dominant share. Male infertility at 41.6% is a commercially growing segment as awareness improves and male diagnostic services expand.

To access detailed market analysis, Request Sample

Male infertility is driven by declining sperm quality linked to environmental toxins, occupational stress, and lifestyle factors. The segment is commercially underpenetrated relative to its prevalence, presenting significant growth opportunity as andrology services and male fertility awareness programs expand across India.

By End-User

Fertility clinics lead end-user share at 46.8% in 2025, reflecting their specialized clinical advantage, higher IVF success rates versus general hospitals, and dedicated patient-centric care models. Hospitals follow at 28.9%, supported by multi-specialty infrastructure for complex clinical cases. Surgical centers at 10.6%, cryobanks at 8.7%, and clinical research institutes at 5.0% represent the remaining market.

Cryobanks at 8.7% are the fastest-growing end-user segment, driven by the expansion of egg freezing, embryo banking, and donor gamete banking services. Regulatory clarity under the ART Regulation Act, 2021 is supporting formal cryobank registration and operations, gradually formalizing what was previously a fragmented, poorly regulated storage landscape.

Regional Market Insights

|

Region |

Share (2025) |

Key Drivers & Characteristics |

|

North India |

30.7% |

Driven by Delhi-NCR's high fertility clinic concentration, strong referral networks, and above-average corporate health benefit adoption. |

|

South India |

28.1% |

Bengaluru, Chennai, and Hyderabad's IT-sector workforce creates premium fertility service demand. Strong private hospital networks and research institutes support advanced ART protocols. |

|

West India |

24.9% |

Mumbai's HNI concentration and Pune's growing medical infrastructure support premium fertility service demand. Medical tourism from international patients adds incremental revenue. |

|

East India |

16.3% |

Kolkata is the primary hub, with growing fertility awareness. The region is commercially underdeveloped but growing above national average CAGR from a lower penetration base. |

North India's 30.7% share reflects Delhi-NCR's role as India's premier medical hub for reproductive health. South India at 28.1% benefits from a highly educated, dual-income urban professional demographic. West India's 24.9% is supported by Mumbai's wealth concentration. East India's 16.3% represents the highest-growth potential region, with organized clinic expansion by Indira IVF, Nova IVF, and Apollo Fertility driving care access.

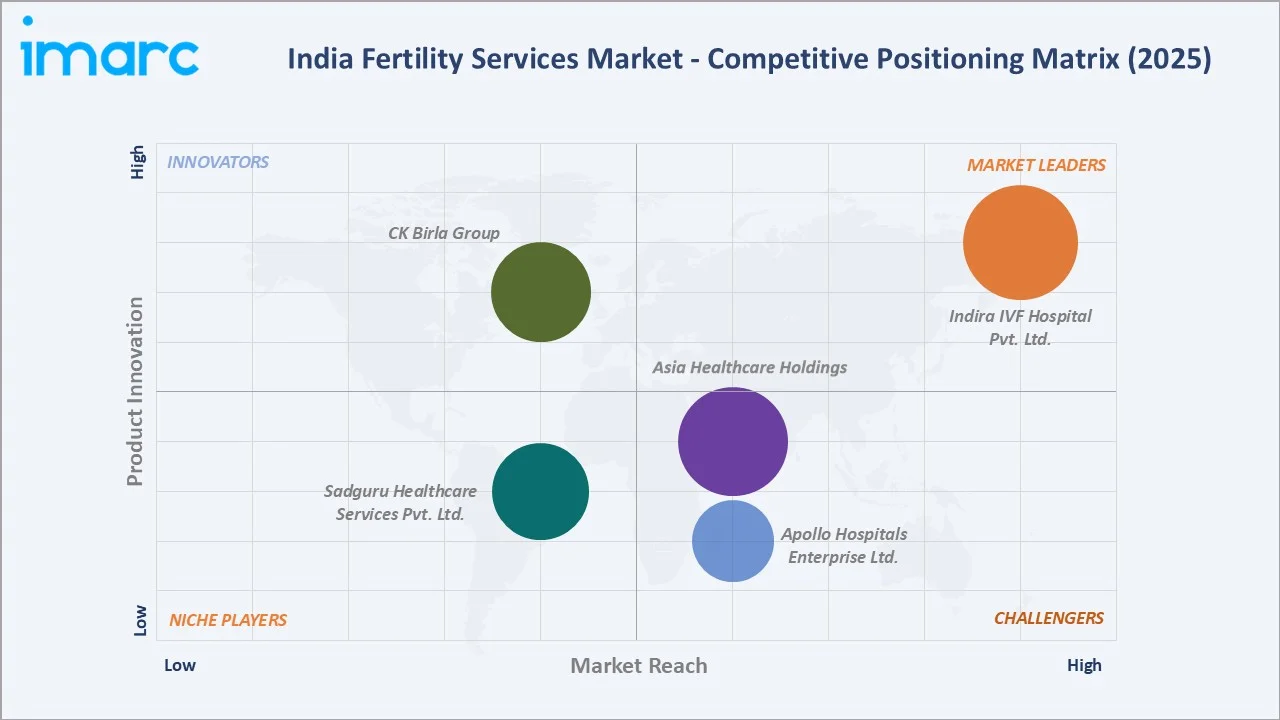

Competitive Landscape

India fertility services market is characterized by a combination of organized chain players, large hospital networks offering ART, and standalone specialty clinics. Consolidation through PE-backed acquisitions is accelerating. The market is dominated by Indira IVF and Nova IVF in the chain clinic segment, while Apollo Fertility and Birla Fertility & IVF represent hospital-group backed challengers.

|

Company |

Key Brands / Clinics |

Market Position |

Core Strength |

|

Indira IVF Hospital Pvt. Ltd. |

Indira IVF |

Market Leader |

Largest organized fertility clinic chain in India with 200+ centers across 20+ states |

|

Asia Healthcare Holdings |

Nova IVF Fertility |

Strong Challenger |

120+ centers across 70+ cities; PE-backed with strong South and West India presence |

|

Apollo Hospitals Enterprise Ltd. |

Apollo Fertility |

Strong Challenger |

Leverages Apollo Hospitals' pan-India brand trust and multi-specialty hospital infrastructure |

|

CK Birla Group |

Birla Fertility & IVF |

Innovator |

Rapidly expanding Tier-2 presence; Jan 2024 launched new clinic in Meerut, UP |

|

Sadguru Healthcare Services Pvt. Ltd. |

Oasis Fertility |

Niche Leader |

Specialized reproductive medicine focus with strong South India clinic network |

The competitive landscape's defining dynamic is consolidation through PE and strategic acquisitions. In March 2026, Nova IVF acquired Craft Fertility for USD 40 million, expanding its South India footprint. Indira IVF has confidentially refiled IPO papers with SEBI (December 2025, refiled 2026). Gaudium IVF & Women Health is also preparing draft papers, signaling IPO momentum across the sector.

Key Company Profiles

Indira IVF Hospital Private Limited

Indira IVF Hospital Private Limited is India's largest organized fertility clinic chain. The company operates 100+ fertility clinics across 80+ Indian cities, making it the most geographically distributed fertility services provider in India.

- Key Services: IVF, ICSI, IUI, egg freezing, embryo banking, surrogacy facilitation, and donor egg programs.

- Recent Developments: In April 2026, Indira IVF Hospital acquired a stake in Abha Surgy Healthcare for operating in the reproductive healthcare segment with a focus on fertility treatment and patient-centered care.

- Strategic Focus: Deepening Tier-2 and Tier-3 city penetration, maintaining the largest national clinic network, and IPO-readiness to fund accelerated expansion.

Asia Healthcare Holdings

Nova IVF Fertility, founded in 2011 and acquired by Asia Healthcare Holdings (AHH) in May 2019, operates 120+ centers across 70+ cities. The company was established in partnership with IVI (Instituto Valenciano de Infertilidad) of Spain, integrating international ART protocols into the Indian clinical environment.

- Key Services: IVF, ICSI, IUI, vitrification, PGT, andrology, embryo adoption, sperm donation.

- Recent Developments: In March 2026, Nova IVF acquired Craft Fertility for approximately USD 40 million, significantly expanding its South India clinic network.

- Strategic Focus: Pan-India chain consolidation through strategic acquisitions, expansion in South and West India, and standardization of clinical protocols across centers.

Market Concentration Analysis

India fertility services market is moderately fragmented at the national level, with a large number of standalone fertility clinics alongside organized chain players. The top five organized chains - Indira IVF, Nova IVF, Apollo Fertility, Birla Fertility, and Oasis Fertility - collectively account for an estimated 25-30% of the organized ART market by revenue in 2025.

Indira IVF commands the single largest individual share in the organized segment by clinic count and estimated patient volume. The broader market remains fragmented due to the large number of standalone gynecology practices and smaller fertility clinics operating outside organized chains. PE-backed consolidation is the primary force reducing market fragmentation, with Nova IVF's acquisition of Craft Fertility in March 2026 representing the market's most significant recent consolidation move at USD 40 million.

Market concentration is expected to increase over the forecast period as organized chains expand into Tier-2 and Tier-3 cities, regulatory compliance requirements raise the cost of independent operation, and IPO funding enables top chains to accelerate acquisition-driven growth.

Investment & Growth Opportunities

Highest Growth Segments

Cryobanks at 8.7% end-user share represent the fastest-growing end-user segment, driven by egg freezing and embryo banking adoption. Fertility preservation services are projected to grow at 15-20% CAGR through 2034 as elective egg freezing normalizes among urban professional women. Male infertility diagnostics and ICSI procedures represent the most underpenetrated sub-segment by clinical prevalence.

Emerging Investment Themes

- Tier-2 city organized fertility clinic expansion: Capturing the vast underserved fertility patient population in India's fast-urbanizing secondary cities through PE-backed chain models.

- Digital fertility platforms and Home IVF: Technology-enabled remote care models (as demonstrated by Seeds of Innocence's Home IVF launch in July 2025) that extend ART access beyond physical clinic geographies.

- Genetic testing integration: PGT and NGS services embedded within IVF protocols to improve success rates and command premium pricing. This is both a clinical differentiator and a revenue enhancement lever for leading chains.

- IPO-driven capital deployment: Indira IVF's and Gaudium IVF's public listing preparations signal that India's fertility sector is entering a capital markets phase that will fund aggressive network expansion through 2034.

Future Market Outlook (2026-2034)

India fertility services market is projected to grow from USD 1.69 Billion in 2025 to USD 4.91 Billion by 2034, delivering a 12.20% CAGR over the forecast period. The market's anchor value of USD 3.01 Billion in 2030 reflects a structural inflection driven by network expansion, technology adoption, and improving insurance coverage for fertility treatments.

Three structural forces define India fertility services market growth through 2034: accelerating IVF adoption driven by declining social stigma and increasing awareness across urban and semi-urban India; technology integration - AI, genetic testing, and digital health - improving success rates and expanding geographic access; and PE and public capital deployment through IPO-funded expansions of Indira IVF, Gaudium IVF, and competing chains.

The treatment gap - an estimated 1-1.5 million annual IVF demand versus 300,000-350,000 cycles performed in 2025 - is the market's most compelling structural growth indicator. As India's organized fertility infrastructure expands, this gap narrows, supporting sustained double-digit revenue growth through 2034.

Research Methodology

Primary Research

Primary research comprised structured interviews with India fertility services industry stakeholders including Medical Directors, Chief Embryologists, Fertility Clinic CEOs and Managing Directors, reproductive endocrinologists, and clinical research coordinators across North, South, West, and East India. Patient experience surveys from ART patients across Tier-1 and Tier-2 cities supplemented clinical perspectives.

Secondary Research

Secondary research encompassed India's ART Regulation Act 2021, Surrogacy Regulation Act 2021, NFHS-5 (2019-21) data from the Ministry of Health and Family Welfare, ICMR (Indian Council of Medical Research) fertility reports, company annual reports, PE transaction databases, and over 50 secondary sources including healthcare industry publications and regulatory filings. Company-sourced data from Indira IVF, Nova IVF, and Apollo Fertility press releases were cross-referenced.

Forecasting Models

Market revenue forecasts were developed using a bottom-up patient cohort model: India's infertile population by income segment, ART awareness rate, treatment conversion rate, and average revenue per ART cycle, aggregated across end-user categories. Regional growth differentials were modeled based on clinic network expansion projections and demographic income growth rates per region.

India Fertility Services Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Cause of Infertilities Covered | Male Infertility, Female Infertility |

| Procedures Covered | In Vitro Fertilization with Intracytoplasmic Sperm Injection (IVF with ICSI), Surrogacy, In Vitro Fertilization Without Intracytoplasmic Sperm Injection (IVF without ICSI), Intrauterine Insemination (IUI), Others |

| Services Covered | Fresh Non-Donor, Frozen Non-Donor, Egg and Embryo Banking, Fresh Donor, Frozen Donor |

| End-Users Covered | Fertility Clinics, Hospitals, Surgical Centers, Clinical Research Institutes, Cryobanks |

| Regions Covered | North India, South India, East India, West India |

| Companies Covered | Indira IVF Hospital Pvt. Ltd., Asia Healthcare Holdings, Apollo Hospitals Enterprise Ltd., CK Birla Group, Sadguru Healthcare Services Pvt. Ltd., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the India fertility services market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the India fertility services market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the India fertility services industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the India Fertility Services Market Report

India fertility services market reached USD 1.69 Billion in 2025. Rising infertility prevalence, ART awareness, and growing organized clinic networks are the primary growth drivers.

The market is projected to grow at 12.20% CAGR during 2026-2034, reaching USD 4.91 Billion by 2034, driven by expanding ART infrastructure, technology adoption, and PE-backed consolidation.

Female infertility leads at 58.4% in 2025. PCOS, endometriosis, and delayed childbearing among urban women are the primary contributing clinical factors.

Fertility clinics lead at 46.8% in 2025. Their specialized infrastructure, dedicated embryology expertise, and higher IVF success rates drive patient preference over hospitals.

North India leads at 30.7% in 2025, driven by Delhi-NCR's high clinic density, advanced medical infrastructure, and strong referral networks from corporate health programs.

Leading companies include Indira IVF Hospital Pvt. Ltd., Asia Healthcare Holdings, Apollo Hospitals Enterprise Ltd., CK Birla Group, and Sadguru Healthcare Services Pvt. Ltd., among others.

India fertility services market is projected to reach USD 3.01 Billion by 2030, supported by Tier-2 city clinic expansion, AI-assisted ART adoption, and rising female fertility preservation services.

The ART Regulation Act 2021 introduced formal licensing for fertility clinics and sperm banks. It has improved quality standards, institutional investor confidence, and organized chain expansion across India.

Top opportunities include Tier-2 city organized clinic expansion, digital fertility platforms and Home IVF services, genetic testing integration (PGT, NGS), and capital deployment through fertility chain IPOs.

Male infertility accounts for 41.6% of the market in 2025. It remains a commercially underpenetrated segment relative to its clinical prevalence, presenting significant growth potential as andrology awareness expands.

PE investment, regulatory compliance requirements, and scale economics are driving consolidation. Nova IVF's USD 40 million acquisition of Craft Fertility in March 2026 is a leading example.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)