India Food Additives Market Size, Share, Trends and Forecast by Type, Application, and Region, 2026-2034

India Food Additives Market Size & Forecast:

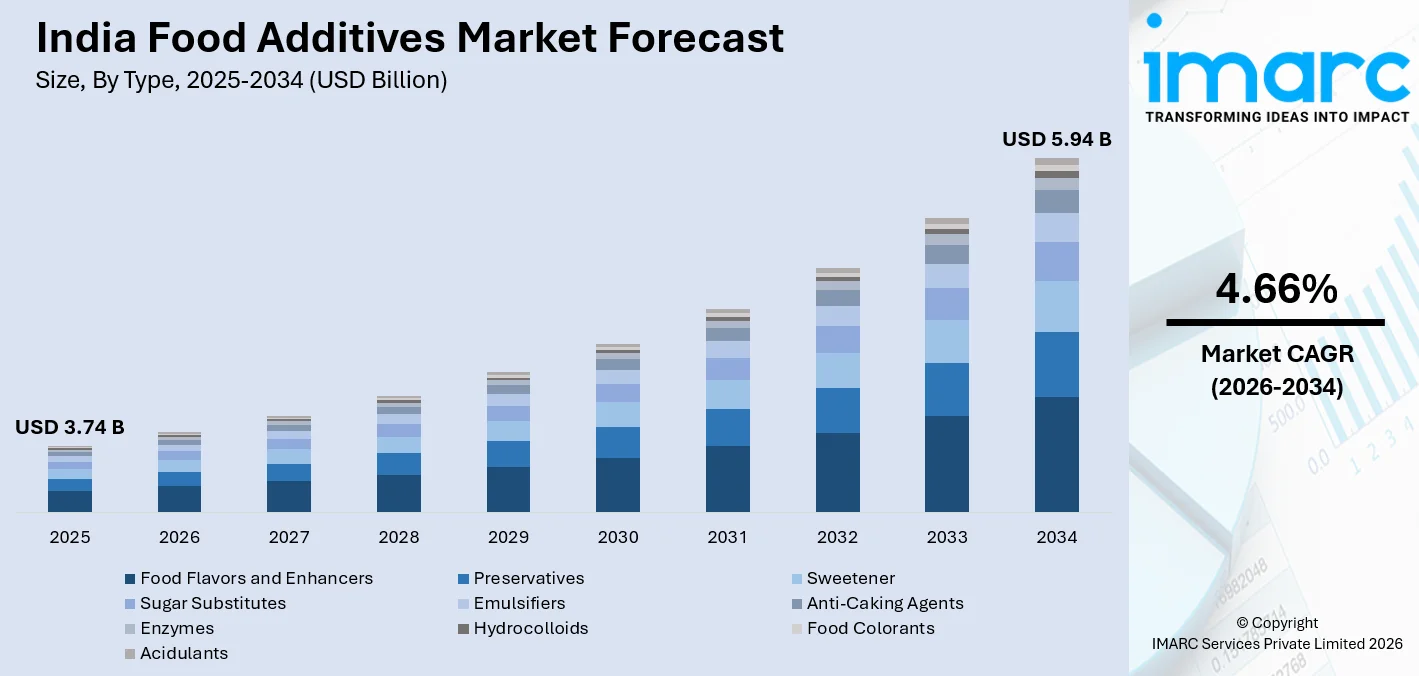

India food additives market size, valued at USD 3.74 Billion in 2025 and is projected to reach USD 5.94 Billion by 2034, growing at a CAGR of 4.66% from 2026-2034. The market is gaining strong momentum driven by the rapid expansion of India's food and beverage processing industry, rising urbanization, and the growing penetration of packaged and convenience foods across urban and semi-urban markets. Government-backed initiatives such as the Production Linked Incentive Scheme for Food Processing are accelerating investments in food manufacturing infrastructure.

To get more information on this market Request Sample

India Food Additives Industry Analysis — Key Insights

- Food Flavors and Enhancers lead the type segment with a 40.0% share in 2025- its dominance reflects the breadth of applications spanning packaged snacks, ready-to-drink beverages, dairy products, and confectionery that rely on consistent and differentiated flavor delivery.

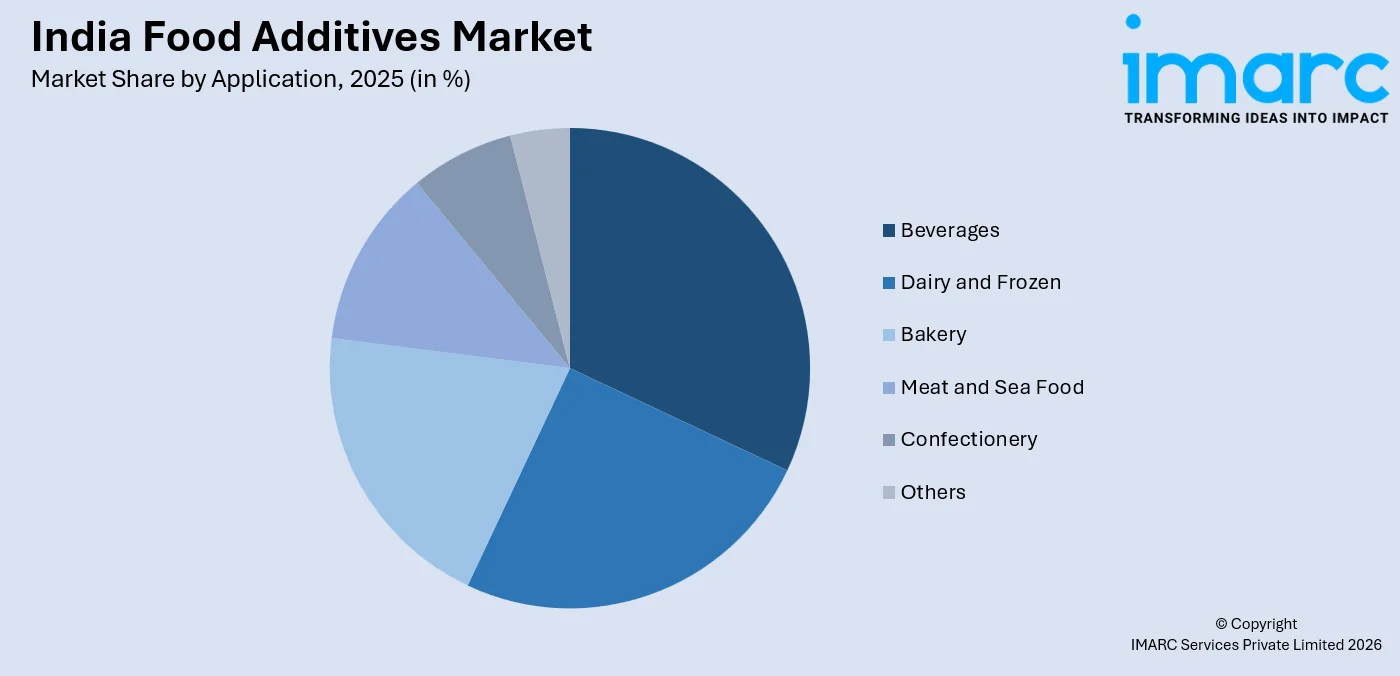

- Beverages account for 25.0% of application in 2025- the explosive growth of packaged beverage consumption across carbonated, energy, and flavored dairy product categories, combined with modern trade and quick-commerce expansion, underpins this segment's leading position.

- West and Central India leads regionally at 30.0% in 2025- Maharashtra and Gujarat's dense concentration of food processing, pharmaceutical ingredient, and beverage manufacturing facilities positions this region as the primary driver of national additive demand.

India Food Additives Market Trends and Dynamic 2026:

Market Trends

Accelerating Demand for Natural and Clean-Label Food Additives

India food additives market growth is being shaped by a fundamental shift in consumer preferences toward natural and clean-label ingredients. Urban millennials and health-conscious consumers are actively seeking products reformulated with plant-derived preservatives, natural colorants, and enzyme-based alternatives to synthetic additives. In August 2024, FSSAI issued revised guidelines clarifying usage and labeling requirements for natural colorants in packaged foods, creating compliance pathways that are accelerating the transition from synthetic to botanical colorant solutions across India's food manufacturing sector.

Specialty Flavor Innovation Driving Premiumization Across Food Categories

India's growing middle class and rapid urbanization are accelerating premiumization across packaged food and beverage categories, generating strong demand for specialty and exotic flavor profiles. From fusion-inspired snacks to international cuisine flavors in ready-to-eat meals, manufacturers are investing in differentiated solutions to capture aspirational consumers. In January 2025, Kurkure and Ching’s Secret collaborated to launch a Schezwan Chutney-flavored Masala Munch snack, specifically targeting the needs of India's domestic snacking industry.

FSSAI Regulatory Evolution Reshaping Additive Compliance Standards

India's food regulatory framework is undergoing significant evolution as FSSAI pursues alignment with Codex Alimentarius and international food safety benchmarks. Revised permissible additive limits, updated approved lists, and enhanced documentation requirements are compelling manufacturers across multiple processing categories to audit formulations and source compliant inputs. In January 2025, FSSAI published updated permitted food additive lists for emulsifiers, sweeteners, and preservatives, driving processors to accelerate compliance-driven reformulation across their product portfolios.

- Expansion of Functional and Fortified Food Products: Rising consumer demand for immunity-boosting, protein-enriched, and nutritionally fortified foods is increasing the use of stabilizers, micronutrients, and enzyme-based additives in processed food formulations.

- Growth of Processed and Convenience Food Consumption: Increasing adoption of ready-to-eat meals, frozen snacks, and instant food products across urban households is driving higher demand for preservatives, flavor enhancers, and shelf-life extending additives.

- Rapid Expansion of Food Processing and Export-Oriented Manufacturing: Government-backed food processing clusters, rising export demand for packaged foods, and investments in modern processing facilities are expanding additive consumption across India’s food manufacturing supply chain.

Growth Drivers

PLI Scheme and Government Investment in Food Processing

India's Production Linked Incentive Scheme for Food Processing Industries has emerged as a transformative catalyst for food manufacturing capacity expansion. With a total outlay of INR 10,900 crore, the scheme incentivizes processors to invest in plant upgrades, new facility construction, and product diversification. In January 2026, the Ministry of Food Processing Industries confirmed that over 169 companies had received PLI approvals for food processing operations, with combined projected investments exceeding INR 9,207 Crore. This rapid scaling of food manufacturing capacity directly amplifies demand for additives across preservative, flavoring, emulsifier, and functional ingredient categories.

Urbanization and Evolving Consumer Dietary Patterns

India's rapid urbanization is fundamentally reshaping food consumption, as packaged, convenient, and processed food categories are all intensive consumers of food additives. Ministry of Statistics & Programme Implementation on Household Consumption Expenditure Survey: 2023-24 stated that the share of beverages and processed food in rural household consumption expenditure increased slightly from 9.62% in 2022–23 to 9.84% in 2023–24, maintaining its position as the largest contributor among food categories.

Expansion of Organized Food Retail and E-Commerce Channels

The rapid growth of organized food retail and food e-commerce in India is fundamentally expanding the market for packaged food products, generating strong pull-through demand for food additives. Modern trade formats, supermarkets, hypermarkets, convenience stores, and quick-commerce platforms are expanding rapidly across urban and Tier 2 markets. In July 2025, Reliance Retail announced opened 2,659 new stores in FY25, creating substantial new demand for packaged products and, consequently, driving incremental food additive consumption throughout the Indian supply chain.

- Clean Label and Natural Ingredient Shift: Growing health awareness is pushing manufacturers to replace synthetic additives with plant-based colors, natural preservatives, and clean-label flavor enhancers.

- Growth of Functional and Fortified Foods: Rising demand for protein-enriched, probiotic, and nutritionally fortified foods is increasing the use of functional additives such as stabilizers, enzymes, and micronutrient blends.

- Expansion of Ready-to-Eat and Convenience Food Segments: Increasing consumption of frozen meals, instant snacks, and ready-to-cook products is accelerating the demand for preservatives, texture enhancers, and shelf-life extending additives across food processing operations.

Market Restraints

Complex and Evolving Regulatory Environment: India's food additive regulatory framework, administered by FSSAI, involves frequent amendments to permissible additive lists, usage levels, and labeling requirements. The need for food processors to continuously monitor regulatory changes and update formulations creates operational complexity and raises compliance costs, particularly for small and medium manufacturers that may lack dedicated in-house regulatory expertise and compliance resources.

Consumer Skepticism Toward Synthetic and Artificial Additives: Growing health consciousness among India's urban population is generating resistance to synthetic and artificial food additives, pressuring manufacturers to pursue costly and technically complex clean-label reformulation strategies. Digital health media and consumer scrutiny of ingredient labels have amplified this dynamic, restricting growth potential for conventional synthetic additive categories and increasing formulation costs for food manufacturers across India.

Supply Chain Vulnerabilities for Specialty Additive Inputs: India's reliance on imports for certain specialty food additive raw materials, including high-purity enzymes, specific hydrocolloids, and specialty flavor compounds, creates vulnerability to global supply chain disruptions and currency volatility. The cold chain and technical handling requirements for some additive categories add logistical complexity and cost, constraining manufacturers' ability to maintain consistent product quality and reliable delivery schedules.

India Food Additives Market Segmentation Analysis:

| Segment | Leading Category | Market Share | Year |

|---|---|---|---|

|

Type |

Food Flavors and Enhancers |

40.0% |

2025 |

|

Application |

Beverages |

25.0% |

2025 |

|

Region |

West and Central India |

30.0% |

2025 |

Type Insights

Food Flavors and Enhancers – 40.0% Market Share (2025) | Leading Type

Food flavors and enhancers led the India food additives market by type, reflecting their high usage in applications spanning packaged snacks, instant noodles, ready-to-drink beverages, confectionery, and dairy products. India's processed food manufacturing base is among the fastest-growing in Asia, with domestic manufacturers investing heavily in product innovation and retail-ready formats.

|

Segment Breakdown Food Flavors and Enhancers (40.0%), Preservatives, Sweetener, Sugar Substitutes, Emulsifiers, Anti-Caking Agents, Enzymes, Hydrocolloids, Food Colorants, Acidulants |

Application Insights

Access the comprehensive market breakdown Request Sample

Beverages- 25.0% Market Share (2025) | Leading Application

Beverages held the leading application share in the India food additives market, underpinned by the explosive growth of India's packaged beverage industry across carbonated soft drinks, fruit-based beverages, energy drinks, and flavored dairy products. Each category relies extensively on additives, including flavors, acidulants, sweeteners, and preservatives, to achieve consistent taste profiles, extended shelf life, and regulatory compliance. In April 2024, PepsiCo announced plans to invest INR 12.66 billion (approximately USD 151.70 million) to establish a new flavor manufacturing facility in Ujjain, Madhya Pradesh, India, reflecting sustained investment momentum in India's packaged beverage sector and the central role beverages play in driving food additives demand.

|

Segment Breakdown Beverages (25.0%), Dairy and Frozen, Bakery, Meat and Sea Food, Confectionery, Others |

Regional Insights

West and Central India- 30.0% Market Share (2025) | Largest Region

West and Central India led the regional breakdown, anchored by Maharashtra and Gujarat, two of India's most industrialized states with a significant concentration of food processing, pharmaceutical, and beverage manufacturing facilities. Mumbai serves as the primary import gateway for specialty additives, while Pune and Ahmedabad host large-scale food manufacturing plants that are major consumers of emulsifiers, flavors, and preservatives. The region's well-developed port infrastructure, logistics network, and proximity to both raw material suppliers and end-user industries make it the most accessible market for additive suppliers.

|

Metric

|

Details

|

|---|---|

| Market Share in 2025 | 30.0% |

| Major States | Maharashtra, Gujarat, Madhya Pradesh |

| Key Growth Driver | Concentration of food processing, beverage manufacturing, and pharmaceutical ingredient production facilities |

| Outlook | Largest market |

|

Regional Breakdown West and Central India (30.0%), North India, South India, East and Northeast India |

North India:

North India is a significant market for food additives, driven by the region's large-scale wheat processing, dairy, and packaged food manufacturing industries. Uttar Pradesh, Punjab, and Haryana are among India's largest agricultural processing states, generating strong demand for preservatives, emulsifiers, and flavor additives. In February 2025, the Uttar Pradesh government announced the establishment of 97 new food processing industries, under the Central Sector Pradhan MantriKisan SAMPADA Yojana (PMKSY) Scheme, with a total project cost of INR 1953.17 crore.

|

Metric

|

Details

|

|---|---|

| Major States | Uttar Pradesh, Punjab, Haryana, Rajasthan, Delhi |

| Key Growth Driver | Expansion of wheat milling and dairy processing industries, rising packaged food manufacturing, and government-backed food processing investments |

| Outlook | Major agro-processing and packaged food manufacturing |

South India:

South India hosts a dynamic food additives market underpinned by the region's strong food processing, seafood export, and beverage manufacturing base. Karnataka, Tamil Nadu, and Andhra Pradesh host significant processing clusters spanning spice processing, seafood export facilities, and beverage plants.

|

Metric

|

Details

|

|---|---|

| Major States | Tamil Nadu, Karnataka, Andhra Pradesh, Telangana, Kerala |

| Key Growth Driver | Strong seafood exports, beverage manufacturing expansion, spice processing clusters, investments in integrated food processing hubs |

| Outlook | Mature food processing ecosystem supporting steady growth |

East and Northeast India:

East and Northeast India represent an emerging market for food additives, supported by growing organized food retail penetration and expanding food processing investment. West Bengal and Odisha are significant seafood and rice processing centers, generating baseline additive demand. India's Act East Policy and northeast-focused investment incentives are attracting food processing companies to the region. In March 2026, the first-ever Food Corporation of India (FCI) food grain cargo train reached Sairang Railway Station (Mizoram) on March 3, 2026, carrying approximately 25,900 quintals of rice from Punjab across 42 wagons.

|

Metric

|

Details

|

|---|---|

| Major States | West Bengal, Odisha, Assam, Tripura, Meghalaya |

| Key Growth Driver | Expansion of rice and seafood processing, rising organized food retail penetration, grain infrastructure development |

| Outlook | Increasing food manufacturing activity and gradual growth in additive consumption |

Market Outlook (2026-2034)

What is the future outlook of the India food additives market?

India food additives market is expected to sustain steady growth through 2034.

India food additives market is positioned for consistent expansion over the forecast period, supported by the rapid growth of the food processing industry, rising consumption of packaged and convenience foods, and increasing urbanization. Expanding organized retail, quick-commerce platforms, and evolving consumer preferences for ready-to-eat and functional food products are strengthening demand for preservatives, flavor enhancers, emulsifiers, and stabilizers. At the same time, the continued development of food processing clusters, export-oriented manufacturing, and government initiatives such as PM Kisan Sampada Yojana is further expected to support additive consumption across India’s food manufacturing ecosystem through 2034.

India Food Additives Market — Leading Key Players:

India's food additives market features a competitive mix of global specialty ingredient companies and domestic manufacturers. International players leverage R&D expertise, global manufacturing networks, and established relationships with multinational food brands operating in India, while domestic players compete on cost efficiency, local formulation knowledge, and distribution reach across India's fragmented food processing landscape. Key competitive dimensions include product innovation, FSSAI compliance expertise, technical service capabilities, and application support.

| Company | Leading Brands | Highlights |

|---|---|---|

|

Cargill, Incorporated |

Cargill Food Ingredients, PURIS, SimPure |

Major global supplier of food ingredients and additives; strong presence in starches, sweeteners, and texturizers; expanding clean-label ingredient portfolio for processed food manufacturers. |

|

BASF SE |

Nutrilife, Isobionics, Verdessence | Global leader in food additives and specialty ingredients; focuses on vitamins, carotenoids, and natural flavor solutions; expanding sustainable and biotechnology-based additive solutions for food and beverage manufacturers. |

|

Kerry Group PLC |

Kerry Taste & Nutrition, Tastesense, EmulsiFibre | Leading taste and nutrition solutions provider; strong expertise in flavor systems, functional ingredients, and clean-label technologies supporting food processing and beverage industries. |

Some of the other key players in the market include Ingredion Incorporated, DSM-Firmenich AG, Tata Chemicals Limited, etc.

Latest Development & News:

- In November 2025, the Food Safety and Standards (Import) First Amendment Regulations, 2025, issued by the Food Safety and Standards Authority of India, updated the 2017 import regulations to improve the method of analysis and reporting for imported food products. The amendment mandates the use of approved analytical methods and requires notified laboratories to issue signed analysis reports (FORM-2) within five days of receiving samples, enhancing efficiency, transparency, and compliance in food import testing.

- In April 2025, Godrej Industries’ Chemicals Business finalized the acquisition of the Food Additives division of Savannah Surfactants Limited in Goa, adding approximately 5,200 MTPA of manufacturing capacity to its operations. This acquisition strengthens Godrej’s specialty chemicals portfolio and broadens its offerings for the global food and beverage industry.

- In March 2025, Cargill presented its comprehensive portfolio of food ingredient innovations at AAHAR 2025 in Delhi-NCR, showcasing solutions designed for snacks, bakery, confectionery, dairy, and ice cream segments. The company introduced several new products, including pectin alternatives, bake-stable fillings, and trans fat-free vanaspati, while also conducting live demonstrations and R&D sessions to highlight ingredient innovations tailored to India’s evolving food industry.

India Food Additives Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Preservatives, Sweetener, Sugar Substitutes, Emulsifiers, Anti-Caking Agents, Enzymes, Hydrocolloids, Food Flavors and Enhancers, Food Colorants, Acidulants |

| Applications Covered | Dairy and Frozen, Bakery, Meat and Sea Food, Beverages, Confectionery, Others |

| Regions Covered | North India, West and Central India, South India, East and Northeast India |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the India food additives market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the India food additives market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the India food additives industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the India Food Additives Market Report

India food additives market was valued at USD 3.74 Billion in 2025.

India food additives market is anticipated to reach a value of USD 5.94 Billion by 2034.

Food flavors and enhancers held the largest type share of 40.0%, driven by their extensive application across packaged snacks, beverages, confectionery, and dairy products requiring consistent and differentiated flavor delivery.

Some of the major players in India food additives market include Cargill, Incorporated, BASF SE, Kerry Group PLC, Ingredion Incorporated, DSM-Firmenich AG, and Tata Chemicals Limited.

The West and Central India are currently leading India's food additives market, accounting for a share of 30.0%, owing to Maharashtra and Gujarat's dense concentration of food processing, beverage manufacturing, and pharmaceutical ingredient production facilities.

Key growth drivers include the PLI Scheme for Food Processing spurring manufacturing investment, rapid urbanization expanding packaged food consumption, organized retail and e-commerce growth driving demand, FSSAI regulatory evolution encouraging compliant additive adoption, and India's growing food export competitiveness requiring internationally benchmarked additive standards.

Major challenges include FSSAI's complex and frequently updated regulatory requirements, raising compliance costs, growing consumer skepticism toward synthetic additives, driving costly clean-label reformulation, and supply chain vulnerabilities for imported specialty additive raw materials, creating cost and quality management pressures for domestic manufacturers.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)