India Foodtech Market Size, Share, Trends and Forecast by Component, Application, Industry, and Region, 2026-2034

India Foodtech Market Summary:

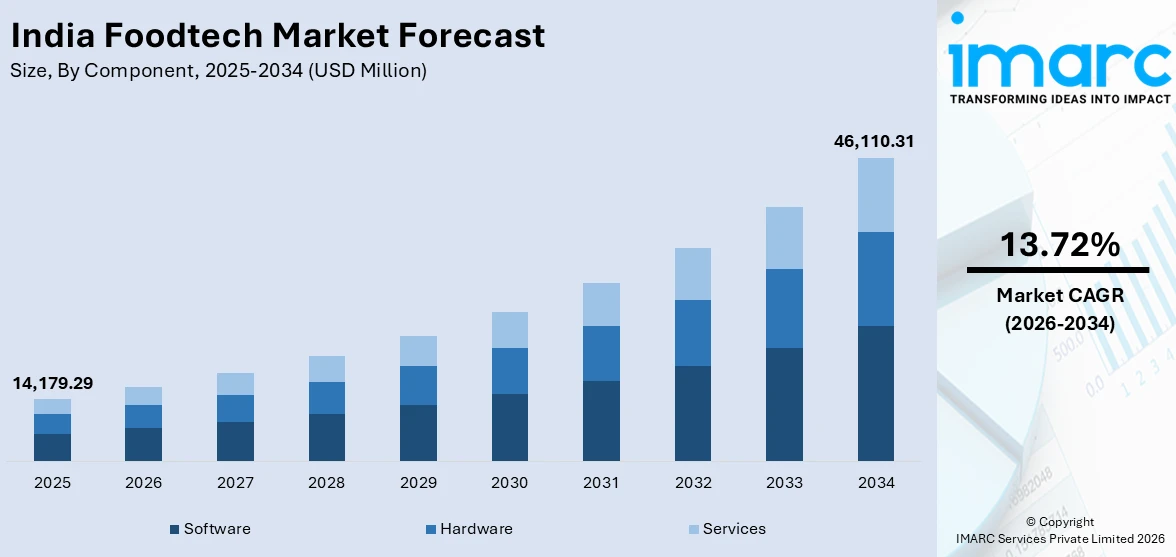

The India foodtech market size was valued at USD 14,179.29 Million in 2025 and is projected to reach USD 46,110.31 Million by 2034, growing at a compound annual growth rate of 13.72% during 2026-2034.

India's foodtech sector is experiencing robust growth, propelled by accelerating digital adoption, a rapidly urbanizing population, and a surge in consumer demand for convenience-driven food solutions. The proliferation of cloud kitchens, artificial intelligence (AI)-powered delivery platforms, and internet of things (IoT)-enabled food processing technologies is transforming how food is prepared, distributed, and consumed across the country. Rising smartphone penetration, growing disposable incomes, and strong government support for food processing modernization are further reinforcing growth, expanding the India foodtech market share.

Key Takeaways and Insights:

- By Component: Software leads the market with a revenue share of 42.3% in 2025, driven by the widespread adoption of AI-powered platforms, demand forecasting tools, and cloud-based restaurant management systems that are transforming operational efficiency across the food ecosystem.

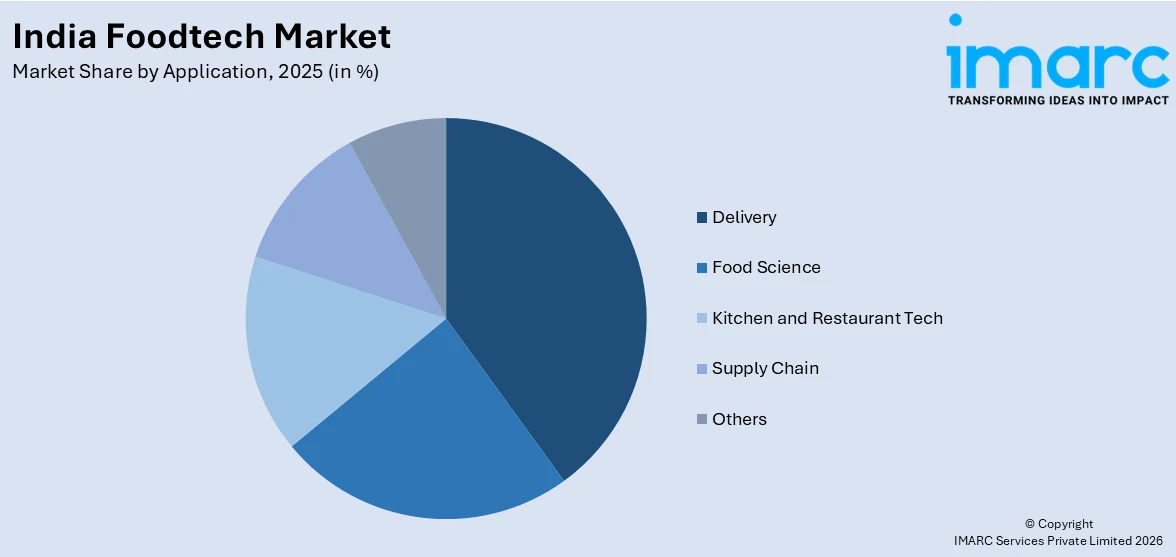

- By Application: Delivery dominates the India foodtech market with a 38.9% share in 2025, reflecting the massive consumer shift toward on-demand food ordering enabled by hyperlocal platforms, quick-commerce models, and algorithm-driven logistics optimization.

- By Industry: Dairy products holds the largest industry share at 24.6% in 2025, underpinned by rising demand for tech-enabled cold chain logistics, automated processing, and IoT-driven quality control in one of India's largest agricultural sub-sectors.

- By Region: South India accounts for the highest regional share at 31.8% in 2025, supported by its dense urban population, high digital literacy, and the strong presence of foodtech hubs in Bengaluru, Hyderabad, and Chennai.

- Key Players: The India foodtech market features intense competition among leading digital platforms, cloud kitchen operators, and food processing technology providers, with major players expanding delivery networks, deepening AI integration, and forging partnerships to consolidate market presence.

To get more information on this market Request Sample

The foodtech sector in India is undergoing a transformation due to the convergence of digital innovation and the changing lifestyles of consumers. Consumers in urban areas are increasingly using food delivery apps, cloud kitchen brands, and intelligent grocery platforms, while the food processing industry is embracing automation, IoT sensors, and blockchain technology for quality assurance and supply chain transparency. South India is the most dynamic region, driven by its vibrant startup ecosystem and tech-friendly consumer base. Major government outlays in food park development and cold chain infrastructure are expanding market accessibility. India saw a major boost in agri foodtech investment in 2024, which grew by 215 percent to reach $2.6 billion, as per the latest Global Agrifoodtech Investment Report 2025 from venture capital firm AgFunder. During the year, the global agri foodtech industry showed signs of a recovery in 2024, raising $16 billion in investment, which marked only a 4 percent decline from 2023.

India Foodtech Market Trends:

Rise of AI-Powered Quick Commerce and Hyperlocal Delivery

Quick commerce is changing the face of food delivery in India, with key players competing to reduce delivery times to less than 15 minutes. In October 2024, Swiggy, a leading food delivery company, rolled out its 10-minute food delivery service, Bolt, in six cities including Hyderabad, Mumbai, and Delhi, in collaboration with the country's leading quick-service restaurants like KFC and McDonald's. In December 2024, Magicpin, the third-largest food delivery app in India, announced its quick delivery service, magicNOW, which is a new 15-minute food delivery service that is currently being tested in key Indian cities and urban areas. magicNOW aims to deliver fast food in a 1.5 km to 2 km radius to ensure that the food is fresh and of high quality. It will be available in Bengaluru, Hyderabad, Mumbai, Chennai, Delhi-NCR, and Pune.

Cloud Kitchen Expansion and Virtual Brand Proliferation

Cloud kitchens have emerged as a defining structural shift in the Indian foodtech industry, allowing the operation of multiple virtual restaurants from a single kitchen at a very low cost. Today, India has over 20,000 cloud kitchens, with Delhi-NCR and Bengaluru being the main hubs. Rebel Foods, with over 350 kitchens in 70 cities, clocking 2.5 lakh orders every day as of early 2025, is one such example of scalability. The use of AI-based demand forecasting and supply chain analysis in these kitchens is further increasing profitability and accuracy of orders.

Technology-Led Transformation of Dairy and Food Processing

The Indian dairy industry, which is one of the biggest in the world, is also embracing cutting-edge food technology such as automated pasteurization, IoT-based quality analysis, and cold chain upgradation. In October 2025, Prime Minister Narendra Modi virtually dedicated a Rs. 76.5 crore milk powder plant at Indore in the state of Madhya Pradesh, which is a major public sector investment in the dairy industry. Secondly, Amul also announced the setting up of what would be the world’s largest curd manufacturing unit in Kolkata.

Market Outlook 2026-2034:

India's foodtech market is positioned for sustained, high-momentum growth over the forecast period, underpinned by the convergence of advanced digital technologies, policy-driven food processing modernization, and a structural shift in consumer food behavior. The market generated a revenue of USD 14,179.29 Million in 2025 and is projected to reach a revenue of USD 46,110.31 Million by 2034, growing at a compound annual growth rate of 13.72% from 2026-2034. The expanding footprint of cloud kitchens, AI-powered delivery platforms, and IoT-integrated food processing facilities will be central to this expansion. Rising investments under the Production-Linked Incentive (PLI) Scheme and the Pradhan Mantri Kisan Sampada Yojana are expected to catalyze food processing capacity at scale, while improving cold chain connectivity across Tier II and III cities will broaden market access for both technology providers and consumers.

India Foodtech Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Component |

Software |

42.3% |

|

Application |

Delivery |

38.9% |

|

Industry |

Dairy Products |

24.6% |

|

Region |

South India |

31.8% |

Component Insights:

- Hardware

- Software

- Services

Software dominates with a market share of 42.3% of the total India foodtech market in 2025.

Software solutions are at the forefront of India's foodtech transformation, enabling seamless integration between order management, delivery optimization, customer engagement, and supply chain coordination. Platforms powered by machine learning and AI enable predictive demand forecasting, dynamic pricing, and personalized recommendations that significantly enhance user retention and operational margins. Restaurant management software, cloud-based ERP tools for food manufacturers, and IoT middleware for dairy and cold chain monitoring are all witnessing strong adoption. The proliferation of mobile-first platforms has made sophisticated software solutions accessible to both large aggregators and smaller cloud kitchen operators.

Enterprise-grade SaaS platforms designed for food processing companies are enabling manufacturers to digitize quality control, production scheduling, and regulatory compliance workflows. In July 2023, FarMart introduced Saudabook, India's first ERP solution specifically designed for the food processing industry, extending its FarMartOS platform to processors nationwide. This underscores the growing demand for purpose-built software across India's diverse food sector. As businesses scale and data-driven decision-making becomes essential, the software segment is expected to retain its dominant position throughout the forecast period.

Application Insights:

Access the comprehensive market breakdown Request Sample

- Food Science

- Kitchen and Restaurant Tech

- Delivery

- Supply Chain

- Others

Delivery leads with a share of 38.9% of the total India foodtech market in 2025.

In the India foodtech market, delivery is the largest and fastest-growing segment, driven by rapid urbanization, rising disposable incomes, and changing consumer lifestyles. The widespread adoption of smartphones and affordable internet has accelerated the use of online food delivery platforms, making convenience a key factor in consumer decision-making. Major players have transformed the foodservice landscape by connecting restaurants, cloud kitchens, and customers through technology-enabled logistics networks. The growth of quick commerce and hyperlocal delivery models has further strengthened this segment.

Consumers increasingly prefer doorstep delivery due to busy work schedules, traffic congestion in metropolitan cities, and the expanding variety of cuisines available online. Features such as real-time order tracking, digital payments, AI-based recommendations, and subscription models have enhanced user experience and customer retention. Additionally, tier-2 and tier-3 cities are emerging as high-growth markets, supported by expanding logistics infrastructure and increasing digital penetration. Overall, the delivery segment continues to dominate the India foodtech market due to its scalability, technological innovation, and strong consumer demand for convenience and variety.

Industry Insights:

- Fish, Meat, and Seafood

- Fruits and Vegetables

- Grain and Oil

- Dairy Products

- Beverages

- Bakery and Confectionery

- Others

Dairy products exhibit a clear dominance with a 24.6% share of the total India foodtech market in 2025.

In the market, dairy products represent the largest segment, supported by strong domestic consumption, cultural dietary preferences, and a well-established production ecosystem. India is one of the world’s largest milk producers, with organized and cooperative networks playing a vital role in procurement and distribution. Companies have built extensive cold-chain and processing infrastructure, enabling large-scale supply of milk and value-added dairy products across urban and rural markets.

The segment includes milk, curd, butter, ghee, paneer, cheese, and flavored dairy beverages. Rising urbanization, growing middle-class income, and increasing demand for protein-rich diets have fueled consumption. Foodtech innovations such as automated milk collection systems, IoT-enabled cold storage monitoring, AI-driven demand forecasting, and digital supply chain management have significantly improved quality control and efficiency. The rapid expansion of online grocery platforms and quick commerce has further strengthened dairy distribution, ensuring faster doorstep delivery and improved product freshness. Additionally, increasing demand for premium and health-oriented products, such as lactose-free milk, probiotic yogurt, and organic dairy, has created new growth avenues.

Regional Insights:

- North India

- South India

- East India

- West India

South India leads with a share of 31.8% of the total India foodtech market in 2025.

In the market, South India holds the largest regional share, driven by strong urban infrastructure, high digital adoption, and a well-developed food processing ecosystem. Major metropolitan cities such as Bengaluru, Chennai, and Hyderabad serve as key technology and startup hubs, fostering innovation in food delivery, cloud kitchens, and supply chain solutions. The region’s robust IT sector and tech-savvy population have accelerated the adoption of app-based food ordering and digital payment systems.

South India also has a strong dairy, poultry, seafood, and spice production base, supporting food processing and value-added product development. The presence of organized retail chains and efficient cold-chain infrastructure has strengthened distribution networks across urban and semi-urban areas. Additionally, a large working professional population and growing middle class contribute to high demand for convenience foods and online delivery services. Foodtech companies benefit from supportive state policies, startup incubators, and investment activity concentrated in cities like Bengaluru. Furthermore, the popularity of diverse regional cuisines, such as South Indian, coastal seafood, and quick-service formats, drives continuous innovation in menu offerings and delivery models.

Market Dynamics:

Growth Drivers:

Why is the India Foodtech Market Growing?

Rapid Urbanization and Evolving Consumer Lifestyles

India's accelerating urbanization is fundamentally reshaping food consumption patterns and driving structural demand for technology-enabled food services. With the urban population surpassing 461 million in 2024 and growing at approximately 2.3% annually, India's cities are generating increasing demand for convenience-oriented, time-saving food solutions. Dual-income households, longer working hours, and a growing young professional demographic are shifting preferences toward on-demand delivery, processed foods, and digital ordering platforms. Urban consumers increasingly prioritize variety, speed, and personalization, creating fertile ground for both food delivery platforms and food processing technology companies to expand their offerings and user bases.

Government Policy Initiatives and Institutional Support

A robust policy environment is a critical enabler of India's foodtech market growth. The Government of India has introduced several targeted programs that are directly accelerating investment in food processing technology, cold chain infrastructure, and innovation. In July 2025, the Union Cabinet approved an additional outlay of Rs. 1,920 crore under the Pradhan Mantri Kisan Sampada Yojana (PMKSY), bringing the total allocation to Rs. 6,520 crore. This includes Rs. 1,000 crore specifically for establishing 50 multi-product food irradiation units, directly supporting processing technology modernization.

Expanding Digital Infrastructure and Smartphone Penetration

India's unparalleled digital infrastructure expansion is a foundational driver of foodtech market growth, enabling both demand-side adoption and supply-side efficiency. As of late 2024, India had 886 million internet users, with 85.5% of households owning at least one smartphone and 99.5% of youth using UPI-based digital payments. These foundations allow food delivery platforms to reach consumers in virtually every urban and peri-urban geography, while food processors and distributors leverage digital tools for real-time inventory management, order tracking, and customer engagement.

Market Restraints:

What Challenges the India Foodtech Market is Facing?

High Operational Costs and Thin Profit Margins

Despite robust revenue growth, many foodtech companies in India operate under significant margin pressure. Customer acquisition costs remain elevated as platforms compete aggressively through discounts and promotional offers. High logistics costs, including rider incentives, fuel, vehicle maintenance, and last-mile technology, strain unit economics, particularly in Tier II and III cities where average order values are lower. Revenue-sharing agreements with restaurant partners, order cancellations, and refund liabilities further compound profitability challenges, requiring strategic realignment from growth-first to profit-oriented models.

Cold Chain and Last-Mile Logistics Infrastructure Gaps

Despite progress, India's cold chain infrastructure remains inadequate relative to the scale of its food production and distribution needs. Post-harvest losses continue to affect perishable categories including dairy, meat, seafood, and fresh produce, limiting the effectiveness of food technology investments. Geographic diversity, congested urban environments, and underdeveloped road networks in semi-urban areas complicate last-mile delivery reliability. These gaps constrain the geographic expansion of temperature-sensitive foodtech solutions and remain a persistent challenge for market participants.

Regulatory Compliance and Food Safety Enforcement Complexity

India's food safety and regulatory environment, governed primarily by the Food Safety and Standards Authority of India (FSSAI), is evolving rapidly but introduces compliance complexity for technology-driven food businesses. Inconsistent enforcement, frequent policy updates, and the challenge of applying uniform standards across India's diverse, fragmented food sector create operational uncertainty. Foodtech startups and food processing companies often face elevated compliance costs, particularly as new regulations around labeling, genetically modified ingredients, and digital commerce emerge, potentially slowing technology adoption among smaller operators.

Competitive Landscape:

The India foodtech market exhibits a dynamic and increasingly concentrated competitive environment, with major digital platforms commanding dominant market positions alongside a rich ecosystem of emerging startups. Moreover, major players collectively account for the majority of platform-to-consumer food delivery volumes, continuously diversifying into quick commerce, cloud kitchen infrastructure, and AI-driven personalization. Apart from this, food processing technology companies, SaaS providers, and agri-food startups are intensifying competition through targeted innovation, strategic partnerships, and geographic expansion into underpenetrated Tier II and III markets.

Recent Developments:

- In July 2025, ITC Ltd, a diversified conglomerate, is broadening its reach into sectors like food-tech, wellness, sustainable packaging, and agri-tech platforms as part of its comprehensive ‘ITC Next’ strategy.

India Foodtech Market Report Coverage:

|

Report Features |

Details |

|

Base Year of the Analysis |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Units |

Million USD |

|

Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

|

Components Covered |

Hardware, Software, Services |

|

Applications Covered |

Food Science, Kitchen and Restaurant Tech, Delivery, Supply Chain, Others |

|

Industries Covered |

Fish, Meat, and Seafood, Fruits and Vegetables, Grain and Oil, Dairy Products, Beverages, Bakery and Confectionery, Others |

|

Regions Covered |

North India, South India, East India, West India |

|

Customization Scope |

10% Free Customization |

|

Post-Sale Analyst Support |

10-12 Weeks |

|

Delivery Format |

PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Foodtech Market Report

The India foodtech market size was valued at USD 14,179.29 Million in 2025.

The India foodtech market is expected to grow at a compound annual growth rate of 13.72% from 2026-2034 to reach USD 46,110.31 Million by 2034.

Software segment leads with a 42.3% market share in 2025, driven by strong demand for AI-enabled delivery platforms, cloud-based restaurant management tools, and demand forecasting solutions that are transforming India's food ecosystem.

Key growth factors include rapid urbanization and lifestyle changes, rising smartphone adoption and digital infrastructure, government support through PLI schemes and PMKSY, the proliferation of cloud kitchens, expansion of quick commerce, and increasing AI integration across delivery and food processing operations.

Major challenges include high operational costs and thin delivery margins, inadequate cold chain and last-mile logistics infrastructure in semi-urban areas, complex and evolving food safety regulatory requirements, and intense competition leading to unsustainable discounting strategies among market participants.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade