India Foreign Exchange Market Size, Share, Trends and Forecast by Counterparty, Type, and Region, 2026-2034

India Foreign Exchange Market Size, Share, Trends & Forecast (2026-2034)

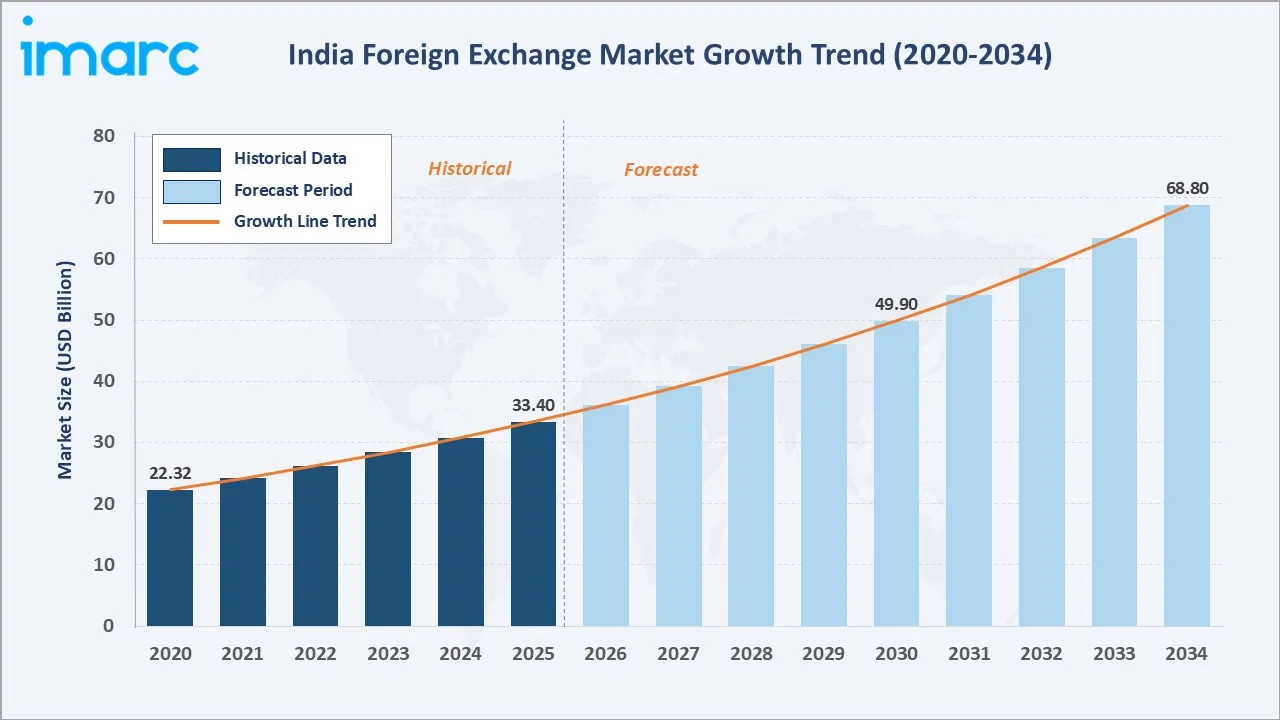

The India foreign exchange market size was valued at USD 33.40 Billion in 2025 and is projected to reach USD 68.80 Billion by 2034, exhibiting a CAGR of 8.4% during the forecast period 2026-2034. Robust cross-border trade flows, rising foreign direct investment (FDI) activity, and growing integration with global capital markets are the primary engines of growth.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 33.40 Billion |

|

Forecast Market Size (2034) |

USD 68.80 Billion |

|

CAGR (2026-2034) |

8.4% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

North India (34.0% share, 2025) |

|

Fastest Growing Region |

South India (~9.5% est. CAGR) |

|

Leading Counterparty |

Reporting Dealers (42.1%, 2025) |

|

Leading Type |

Currency Swap (40.3%, 2025) |

The chart below illustrates the India foreign exchange market growth trajectory from 2020 through 2034, contrasting historical expansion against a sustained forecast curve.

To get more information on this market, Request Sample

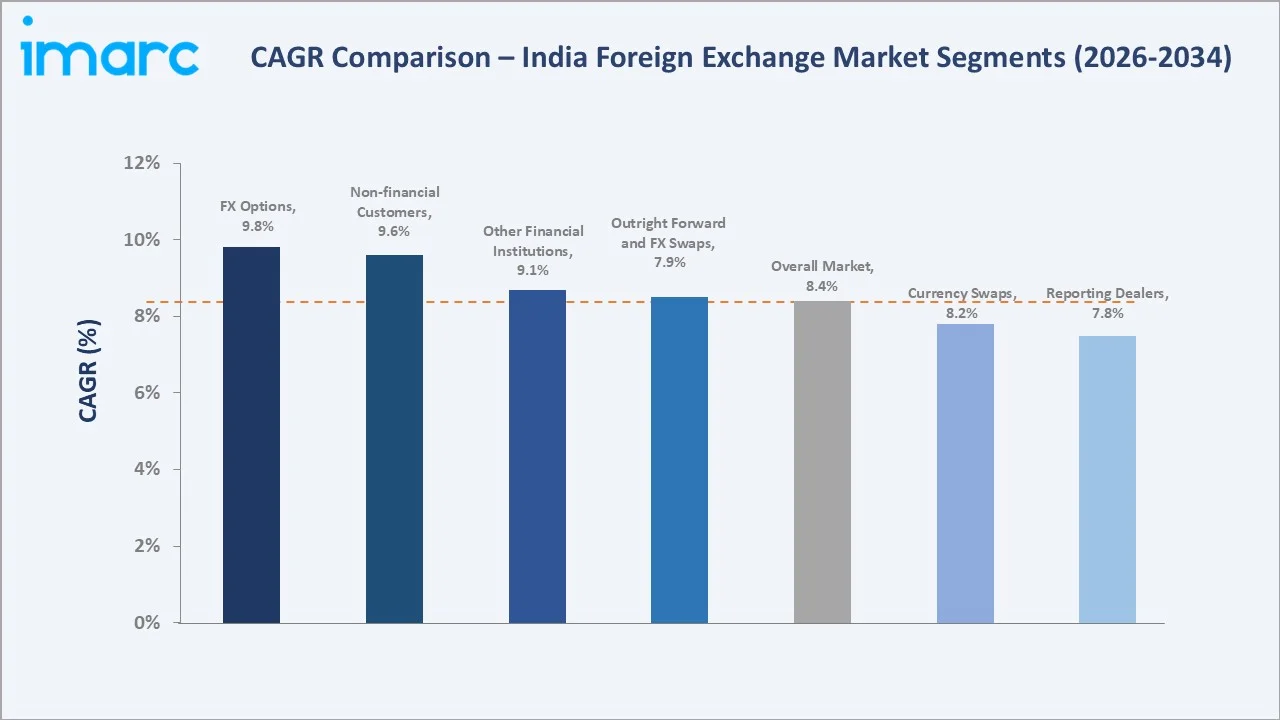

Segment-level CAGR comparisons highlight non-financial customers and FX options as the fastest-growing sub-categories within the India foreign exchange market forecast through 2034.

Executive Summary

The India foreign exchange market is undergoing significant structural expansion, driven by liberalizing regulatory policies, rising corporate globalization, and accelerating digital trading adoption. Valued at USD 33.40 Billion in 2025, the market is forecast to reach USD 68.80 Billion by 2034 at a CAGR of 8.4%. The Reserve Bank of India's (RBI) proactive monetary policy management, currency stabilization interventions, and progressive opening of the forex ecosystem continue to strengthen market depth and liquidity.

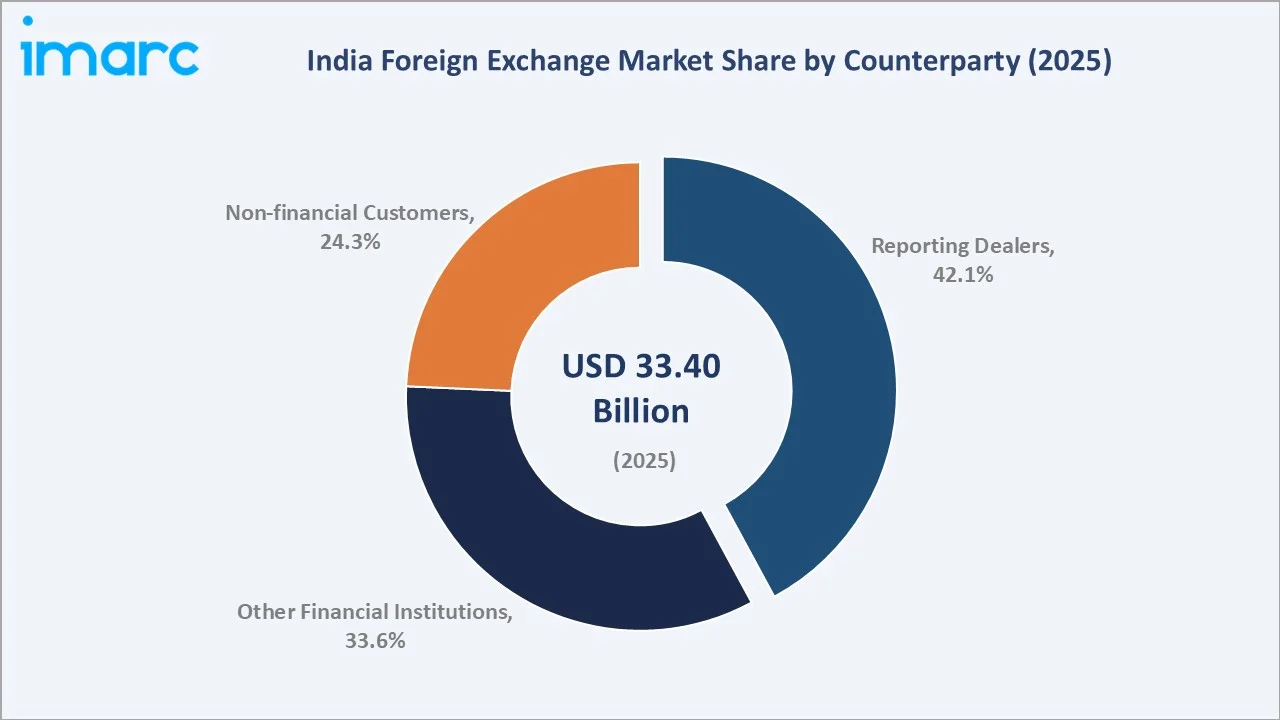

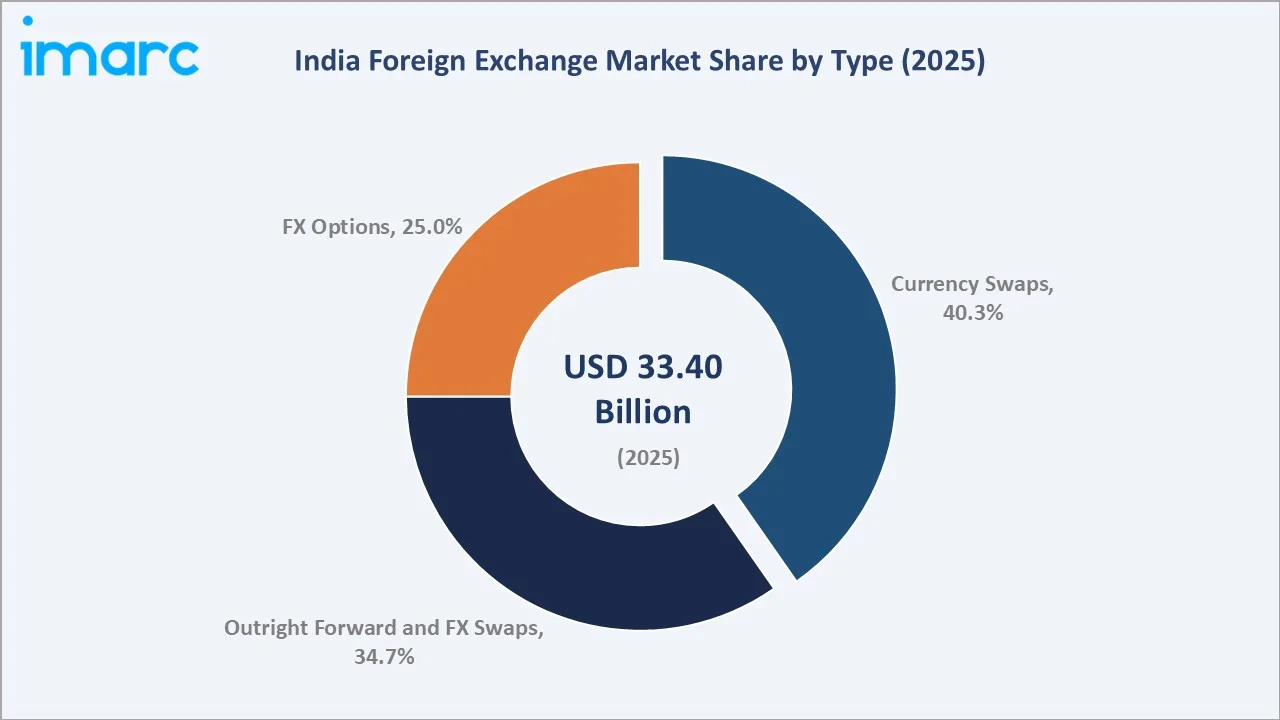

Reporting dealers represent the dominant counterparty segment at 42.1% in 2025, underpinned by their role as primary liquidity providers and execution agents for institutional and corporate clients. Currency swaps lead the type segmentation at 40.3%, reflecting robust hedging demand among Indian corporates managing cross-border financing and export receivables. Non-financial customers - importers, exporters, and retail participants - account for 24.3% and represent the fastest-growing counterparty cohort.

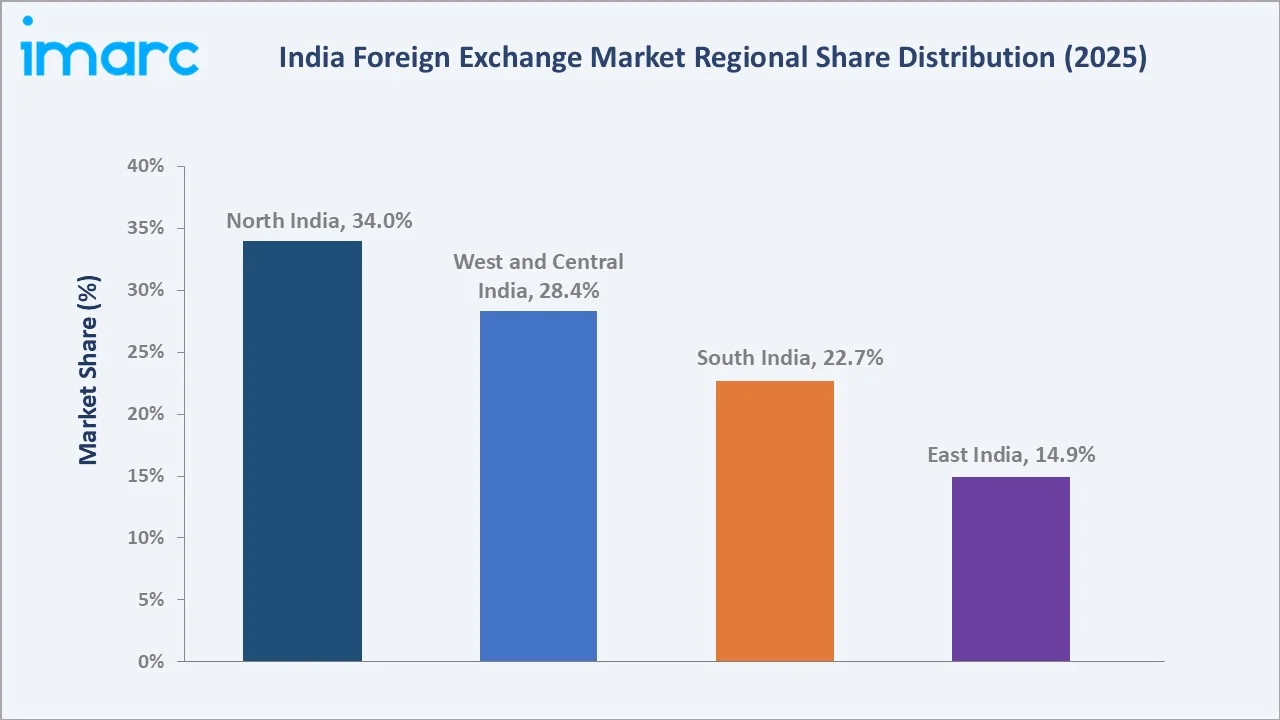

North India commands the largest regional share at 34.0%, anchored by the concentration of corporate headquarters and authorized dealers in New Delhi and NCR. West and Central India follows at 28.4%, reflecting Mumbai's stature as India's financial capital and primary interbank forex center. The India foreign exchange market outlook remains highly positive as digital platform penetration, NRI remittance growth, and India's expanding global trade footprint underpin sustained multi-year expansion through 2034.

Key Market Insights

|

Insight |

Data |

|

Largest Counterparty |

Reporting Dealers - 42.1% share (2025) |

|

Second Counterparty |

Other Financial Institutions - 33.6% (2025) |

|

Largest Type |

Currency Swap - 40.3% share (2025) |

|

Second Type |

Outright Forward & FX Swaps - 34.7% (2025) |

|

Leading Region |

North India - 34.0% revenue share (2025) |

|

Fastest Growing Counterparty |

Non-financial Customers (~9.6% est. CAGR) |

|

Top Companies |

State Bank of India, HDFC Bank Ltd., ICICI Bank, Axis Bank, Kotak Mahindra Bank, Standard Chartered Bank, and Yes Bank |

Key Analytical Observations Supporting The Above Data:

- Reporting Dealers' 42.1% dominance in 2025 reflects their critical role as interbank market makers, facilitating high-volume transactions for corporate, institutional investors, and offshore participants. Their operations are governed by strict regulatory authorization requirements, creating significant entry barriers and reinforcing the position of established players.

- Currency Swap's 40.3% share is driven by increasing demand from banks and corporates for long-term currency risk management solutions. These instruments are widely used for managing exposures related to external borrowings and cross-currency interest rate obligations, particularly across major currency pairs.

- Non-financial Customers at 24.3% represent a rapidly evolving segment, driven by increasing outbound investment activity by Indian corporates. This trend is generating growing demand for forex hedging solutions to manage currency risks associated with overseas investments and cross-border capital flows.

- North India's 34.0% regional dominance is anchored by the NCR, which serves as a key hub for public sector enterprises, multinational corporations, and government-linked financial institutions, generating consistently high and predictable forex transaction volumes.

- FX Options at 25.0% are gaining traction as Indian corporations adopt more advanced treasury and risk management practices. Companies are increasingly using both vanilla and structured option strategies to hedge asymmetric currency exposures arising from export contracts and long-term import obligations.

Global India Foreign Exchange Market Overview

The India foreign exchange (forex) market is a decentralized, over the counter (OTC) financial market for trading Indian Rupee (INR) against major global currencies, including the US Dollar (USD), Euro (EUR), British Pound (GBP), and Japanese Yen (JPY). The market operates through authorized dealers (primarily commercial banks), money changers, and electronic trading platforms under the regulatory oversight of the Reserve Bank of India (RBI) and the Foreign Exchange Management Act (FEMA), 1999.

The ecosystem comprises interbank spot and forward markets, currency derivatives traded on recognized exchanges such as National Stock Exchange of India and Bombay Stock Exchange, along with a rapidly expanding retail forex trading segment enabled by licensed brokers and digital platforms.

Market Dynamics

To evaluate market opportunities, Request Sample

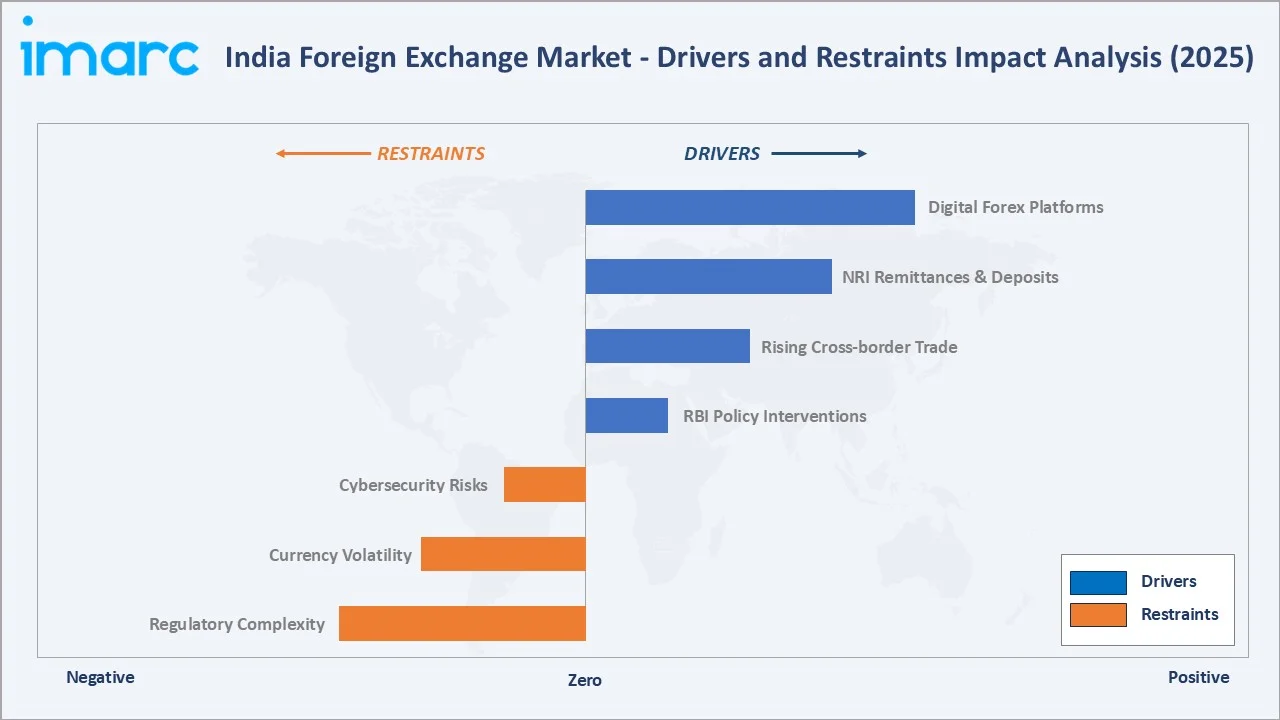

Market Drivers

- Rising Cross-Border Trade and FDI Flows: The cumulative value of merchandise exports during FY 2024-25 (April-March) was US$ 437.42 Billion, registering a growth of 0.08%. This scale of cross-border commerce generates structural forex demand for currency conversion, settlement, and hedging across all counterparty segments - from large exporters to mid-sized importers.

- Digital Forex Platform Proliferation: The expansion of mobile trading apps, seamless KYC processes, and real-time price feeds has dramatically lowered entry barriers for retail forex participants. This democratization is adding breadth and liquidity to a market traditionally dominated by institutional players and is a key contributor to non-financial customer segment growth.

- NRI Remittances and Deposit Inflows: India remains the world’s largest recipient of remittances, with strong growth in NRI deposits in recent periods. These inflows strengthen the forex supply side and play a key role in supporting overall currency stability.

- RBI Policy Interventions and INR Internationalization: The central bank’s progressive framework for rupee-based trade settlement is expanding the global use of the INR in cross-border transactions. This initiative is driving increased demand for hedging instruments and currency swaps linked to INR cross-currency pairs, supporting the development of a more diversified forex market ecosystem.

Market Restraints

- Regulatory Complexity and Compliance Burden: India's forex market operates under extensive FEMA and RBI regulations, including capital account restrictions, documentation requirements, and transaction limits. These compliance demands increase operational costs for smaller financial institutions and restrict product innovation compared to more liberalized global forex markets.

- INR Currency Volatility and External Macro Risks: The Indian rupee remains vulnerable to global risk-off sentiment, shifts in US monetary policy, and fluctuations in crude oil prices due to the country’s high import dependence. Periods of sharp currency depreciation tend to dampen corporate participation in the forex market while simultaneously increasing the cost of hedging exposures.

- Cybersecurity and Platform Risks in Digital Forex: The rapid growth of digital forex trading platforms has expanded the attack surface for cybersecurity threats. Regulatory lapses, platform outages, or fraud incidents can damage retail investor confidence and slow the democratization of forex market participation.

Market Opportunities

- INR-Denominated Trade Settlement Expansion: As of 2025, the central bank has expanded approval for INR-based trade settlement with multiple countries, with active transactions already taking place across key trading partners. This framework is generating structural demand for INR-denominated hedging instruments while also creating new revenue opportunities for authorized dealers and digital trading platforms.

- Growth of Retail Forex Participation: India’s young and digitally connected workforce represents a significant untapped opportunity in the retail forex segment. Improving regulatory clarity and the rise of mobile-first trading platforms are expected to accelerate retail participation, driving steady account growth and expanding the non-financial customer base over the coming years.

- Expansion into Tier-2 and Tier-3 City Markets: Currently, forex market activity is concentrated in metro centers. The expansion of authorized money changer networks and digital forex platforms into smaller cities, supported by Jan Dhan Yojana-linked financial inclusion, represents a multi-billion-dollar opportunity for market deepening.

Market Challenges

- Limited Depth in Long-Dated Derivatives: India's forex derivative market remains thin beyond 12-month tenors, limiting the ability of corporates to hedge long-dated currency exposures. This structural limitation constrains participation from infrastructure project developers and long-cycle exporters who require multi-year hedging solutions.

- Capital Account Convertibility Constraints: India maintains a partially convertible capital account, restricting certain cross-border capital flows. These restrictions limit India's integration with global forex markets and cap the depth of participation from foreign institutional investors and hedge funds.

Emerging Market Trends

1. Accelerating Digital Forex Platform Adoption

User-friendly mobile applications and seamless onboarding have democratized forex trading. A tech-savvy investor base is actively trading major INR pairs using advanced analytical tools and live price feeds, shifting market depth away from exclusive institutional dominance.

2. INR Internationalization and Cross-Currency Expansion

The central bank’s push toward INR-denominated trade settlement is creating new demand for INR cross-currency hedging instruments. This structural shift is expected to significantly expand the size of India’s forex market as bilateral trade in INR gains traction across emerging economies.

3. Surge in NRI Remittances and Deposit Growth

India sustained its position as the world's largest remittance recipient in 2024. NRI deposits rose to USD 158.94 Billion in outstanding balances by August 2024, representing a powerful structural forex supply driver that supports rupee stability and market liquidity.

4. Corporate Treasury Sophistication and Hedging Innovation

Indian corporations especially in IT services (USD 210 Billion estimated exports in FY25), pharmaceuticals, and manufacturing are developing sophisticated forex treasury strategies. Adoption of structured options, cross-currency swaps, and dynamic hedging programs is driving FX Options segment growth.

5. AI-Powered Forex Analytics and Algorithmic Trading

The integration of artificial intelligence and machine learning into forex price discovery, execution algorithms, and risk analytics is rapidly transforming India's institutional forex landscape. Leading banks and technology-enabled brokers are deploying AI-driven trading desks, compressing spreads and improving execution quality for corporate clients.

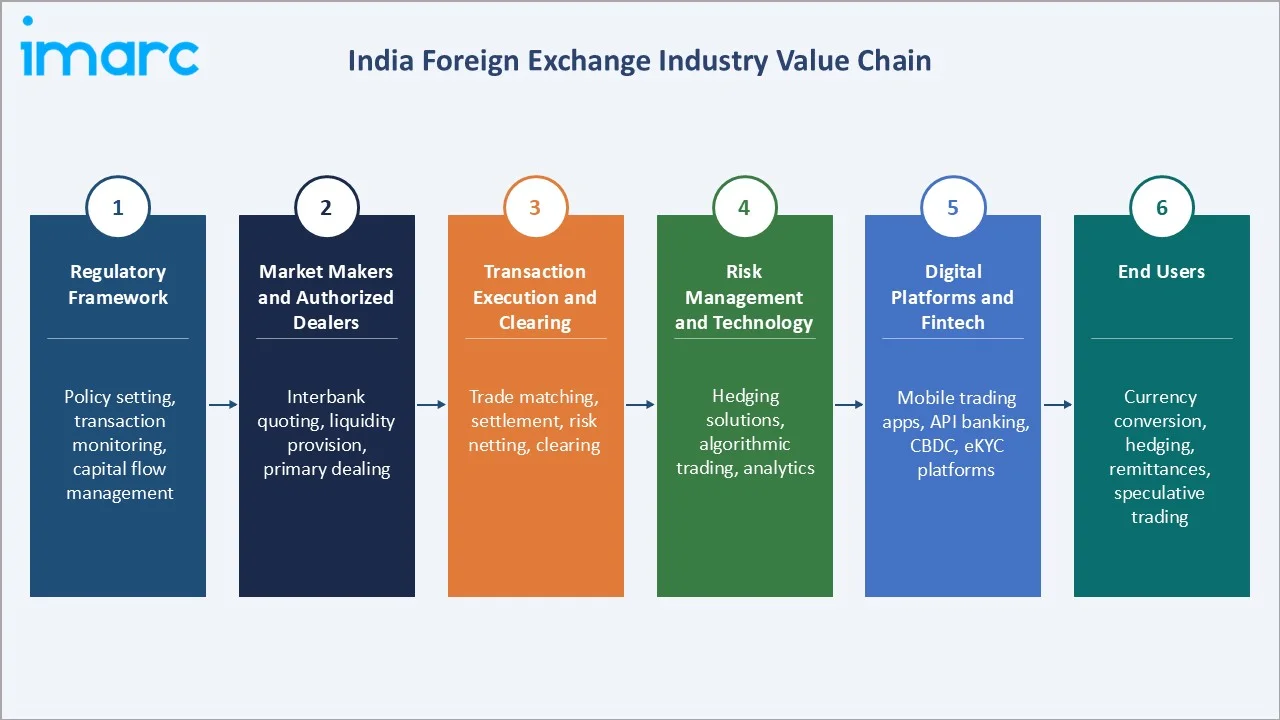

Industry Value Chain Analysis

The India foreign exchange industry value chain spans five integrated stages from regulatory oversight to end-user transaction execution. Each stage represents distinct competitive dynamics, technology investment requirements, and margin profiles relevant to the overall India foreign exchange market analysis.

|

Value Chain Stage |

Key Functions |

|

Regulatory Framework |

Policy setting, transaction monitoring, capital flow management |

|

Market Makers & Authorized Dealers |

Interbank quoting, liquidity provision, primary currency dealing |

|

Transaction Execution & Clearing |

Trade matching, settlement, risk netting, derivative clearing |

|

Risk Management & Technology |

Hedging solutions, algorithmic trading, portfolio analytics |

|

End Users |

Currency conversion, hedging, remittances, speculative trading |

The Clearing Corporation of India Ltd. (CCIL) plays a pivotal central counterparty role, guaranteeing settlement across the interbank forex market and significantly reducing counterparty credit risk. Technology vendors enabling real-time pricing, order management, and regulatory reporting are increasingly capturing strategic value as market infrastructure modernizes.

Technology Landscape in the India Foreign Exchange Industry

Electronic Trading Platforms and APIs

Multi-bank electronic trading platforms and bank-proprietary APIs are increasingly replacing traditional voice-based dealing for institutional and corporate clients. This shift toward electronic execution is enhancing market efficiency by tightening bid-ask spreads and enabling faster, more seamless transaction settlement.

Algorithmic and High-Frequency Trading

Algorithmic trading desks at major Indian and foreign banks are increasingly deploying quantitative models for currency arbitrage, multi-currency strategies, and systematic hedging execution. The introduction of a clearer regulatory framework for algorithmic trading in currency derivatives has further strengthened the operating environment, encouraging greater participation from technology-driven market players.

Digital KYC and Compliance Automation

The adoption of Aadhaar-linked eKYC, video-based customer verification, and automated AML/CFT monitoring systems is significantly reducing onboarding friction for retail forex participants. This digital infrastructure is acting as a key enabler for the growth of the non-financial customer segment, supporting its steady expansion over the long term.

Blockchain and Distributed Ledger Technology

Pilot programs for blockchain-based cross-border remittance settlement are underway between Indian banks and their international correspondent networks. RBI's exploration of a Central Bank Digital Currency (CBDC) - e-Rupee - represents a potential structural shift in how retail forex and cross-border payments are executed, with implications for market size metrics by 2028-2030.

AI-Powered Risk Analytics

Machine learning models for exchange rate forecasting, volatility surface calibration, and dynamic hedging ratio optimization are being deployed by leading corporate treasury teams. AI-driven risk dashboards are enabling real-time monitoring of forex exposure across multi-currency trade books, reducing operational risk and improving hedge effectiveness ratios.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Counterparty |

Reporting Dealers |

42.1% |

2025 |

|

Type |

Currency Swap |

40.3% |

2025 |

|

Region |

North India |

34% |

2025 |

By Counterparty

To access detailed market analysis, Request Sample

Reporting Dealers lead the India foreign exchange market counterparty segmentation with a 42.1% share in 2025. These entities - primarily scheduled commercial banks with RBI authorization - function as the primary liquidity backbone of the market, executing interbank trades, corporate currency purchases, and institutional hedging transactions.

By Type

Currency Swaps dominate the type segmentation at 40.3% share in 2025, driven by corporate demand for long-dated currency and interest rate risk management. Indian companies with external commercial borrowings (ECBs) denominated in USD and EUR routinely use cross-currency swaps to convert fixed foreign currency liabilities into INR-equivalent obligations, managing both exchange rate and interest rate exposure simultaneously.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

Major Centers |

|

North India |

34.0% |

Corporate HQs, PSUs, government financial entities, NCR concentration |

New Delhi, Gurugram, Noida |

|

West & Central India |

28.4% |

Interbank forex hub, stock exchange proximity, export-import financing |

Mumbai, Pune, Ahmedabad |

|

South India |

22.7% |

IT/ITES export revenues, pharma exports, growing NRI diaspora |

Bengaluru, Chennai, Hyderabad |

|

East India |

14.9% |

Port-driven trade finance, commodity exports, emerging industrial growth |

Kolkata, Bhubaneswar |

North India commands 34.0% of India's total forex market revenue in 2025. The National Capital Region (NCR) hosts the largest concentration of corporate headquarters, public sector undertakings (PSUs), and government-linked financial entities in the country. The presence of the Ministry of Finance, major state-owned banks' head offices, and the headquarters of India's largest conglomerates generates deep and consistent forex transaction volumes across all counterparty categories.

Competitive Landscape

|

Company Name |

Key Platform / Brand |

Market Position |

Core Strength |

|

State Bank of India |

SBI Forex / SBI Trade |

Leader |

Largest branch network, PSU client dominance, government forex mandates |

|

HDFC Bank Ltd. |

TradeOnNet, TradeXpress |

Leader |

Digital forex platform, premium corporate banking, superior technology |

|

ICICI Bank |

ICICI Trade Online / Forex |

Leader |

Retail and SME forex solutions, strong NRI banking franchise |

|

Axis Bank |

neo for corporates |

Leader |

Mid-market corporate focus, competitive forward rates, digital tools |

|

Kotak Mahindra Bank |

Kotak Neo |

Challenger |

Private banking forex, HNI solutions, digital-first positioning |

|

Standard Chartered Bank |

Straight2Bank |

Challenger |

Trade finance integration, cross-border banking, emerging market expertise |

|

Yes Bank |

Yes Forex |

Emerging |

Competitive retail forex rates, SME focus, digital platform investment |

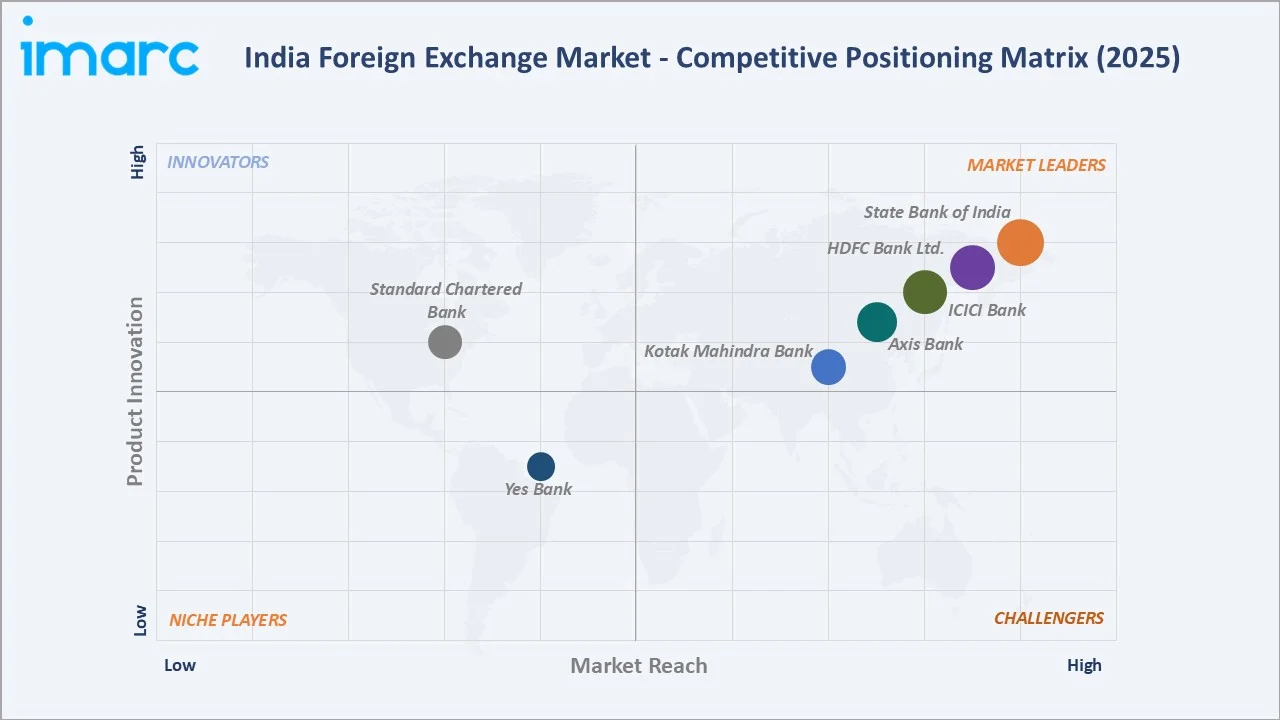

The India foreign exchange market's competitive landscape is dominated by a combination of large public sector banks and private sector banking giants. Competition is intensifying as fintech-enabled forex platforms challenge traditional bank relationships for retail and SME forex business.

Key Company Profiles

State Bank of India

State Bank of India is India’s largest public sector bank and a leading multinational financial services institution, headquartered in Mumbai. It operates as a government-owned entity and plays a central role in India’s banking and financial ecosystem.

- Product & Platform Portfolio: SBI's forex portfolio spans spot and forward contracts, cross-currency swaps, and structured hedging solutions. The SBI Trade Finance portal and SBI Forex digital platform serve import-export clients with competitive USD-INR, EUR-INR, and other major pair solutions.

- Recent Developments: In 2026, State Bank of India has taken a strategic step to strengthen India–Israel trade by enabling rupee-denominated settlement mechanisms, allowing transactions to be conducted directly in INR instead of traditional dollar-based routes. This move marks a significant advancement in the internationalization of the rupee, reducing dependency on intermediary currencies and lowering exchange-related risks for exporters and importers.

- Strategic Focus: SBI's strategy centers on leveraging its unmatched branch network to capture NRI remittance flows, expanding digital forex servicing for SME exporters, and strengthening its role in government-linked FDI and infrastructure project currency management.

HDFC Bank

HDFC Bank is one of India’s largest private sector banks, headquartered in Mumbai. It has grown into a leading financial services institution offering a wide range of banking and financial solutions across retail, corporate, and wholesale segments.

- Product & Platform Portfolio: HDFC Bank's forex services include real-time spot currency conversion, forward booking, cross-currency payments, and a comprehensive trade finance suite. Its digital platform offers live INR-USD rates, online forward contract booking, and integrated trade documentation management.

- Recent Developments: In 2023, HDFC Bank completed its landmark merger with HDFC Ltd., creating one of the largest financial institutions in India with an expanded balance sheet and customer base. The merger enhances cross-border transaction capabilities, boosting forex flows across remittances, NRI deposits, and corporate dealings while increasing demand for hedging and treasury services.

- Strategic Focus: HDFC Bank focuses on digital-first forex services for premium retail and NRI segments, building API-integrated forex solutions for corporate treasuries, and expanding its trade finance franchise as India's exports grow.

ICICI Bank

ICICI Bank is India's second-largest private sector bank. It maintains one of the strongest NRI banking franchises in India, with dedicated forex and remittance services serving the large Indian diaspora in the US, UK, UAE, and Canada.

- Product & Platform Portfolio: ICICI Bank offers a comprehensive forex product range through its Trade Online platform, covering documentary credits, bank guarantees, forward exchange contracts, and structured forex hedging solutions. Its Money2India remittance service is among India's largest NRI remittance channels.

- Recent Developments: In 2025, ICICI Bank Limited, in partnership with Visa Inc., has launched the Corporate Sapphiro Forex Card, strengthening its foreign exchange offerings for corporate clients. The multi-currency prepaid card enables efficient cross-border payments, competitive forex conversion, and streamlined expense management for international business travel.

- Strategic Focus: ICICI Bank's forex strategy emphasizes NRI financial solutions, SME export finance, and technology-led retail forex services, leveraging its strong brand presence in diaspora markets.

Market Concentration Analysis

The India foreign exchange market exhibits moderate-to-high concentration at the top tier. The top five authorized dealers - State Bank of India, HDFC Bank Ltd., ICICI Bank, Axis Bank, Kotak Mahindra Bank - collectively account for an estimated 55-65% of interbank forex transaction volumes in 2025. This concentration reflects the capital requirements, technology investments, and regulatory authorizations required to operate as an authorized dealer category-1 (AD-1) institution.

The market exhibits a dual-tier structure. At the wholesale interbank tier, a small number of large banks dominate through their treasury operations and direct RBI market access. At the retail and corporate service tier, the market is significantly more fragmented, with over 100 authorized dealers, thousands of money changers, and a growing number of fintech-licensed entities competing for SME and retail forex business.

Consolidation trends are emerging at the digital platform layer, where well-funded fintech companies are acquiring smaller forex service providers and licensed money changers to build pan-India distribution networks. Simultaneously, the RBI's progressive licensing of payment aggregators and cross-border payment service providers is introducing new non-bank competitors into segments previously dominated by commercial banks, particularly in the remittance and retail forex conversion segments.

Investment & Growth Opportunities

Fastest-Growing Segments

FX Options represent the fastest-growing type at an estimated 9.8% CAGR through 2034, driven by increasing corporate treasury sophistication and growing demand for asymmetric hedging solutions. Non-financial customers are the fastest-growing counterparty category at ~9.6% CAGR, fueled by India's accelerating outward FDI (nearly doubling to USD 6.8 Billion in April 2025) and expanding retail forex participation.

Emerging Market Expansion

Tier-2 and Tier-3 cities represent a significant untapped opportunity as digital forex platforms expand coverage beyond metro centers. India's manufacturing sector expansion under the Production-Linked Incentive (PLI) scheme across electronics, semiconductors, and textiles is creating new export-linked forex demand in industrial clusters in Gujarat, Tamil Nadu, and Uttar Pradesh.

INR Internationalization Investment Theme

The RBI's push for INR trade settlement and the long-term trajectory toward broader INR convertibility represents a structural investment theme for financial institutions. Banks and fintech platforms that build early infrastructure for INR cross-border payment corridors - particularly with the UAE, Russia, and ASEAN markets - are positioned to capture significant first-mover advantages as India's trade in INR scales from the current nascent base.

Venture and Strategic Investment Trends

Venture capital interest in Indian forex fintech has grown significantly, with players like Niyo, and EbixCash attracting growth capital to build technology-led forex distribution platforms. Corporate venture arms of major banks are co-investing in API banking infrastructure that enables seamless forex access for enterprise and SME treasury clients. AI-driven FX risk management platforms and CBDC-linked settlement infrastructure are emerging as key investment focus areas for 2025-2030.

Future Market Outlook (2026-2034)

The India foreign exchange market forecast projects robust value expansion from USD 33.40 Billion in 2025 to USD 68.80 Billion by 2034 at a CAGR of 8.4%. Three structural transformations will define this growth trajectory.

First, INR internationalization will progress meaningfully. As India's GDP moves toward the USD 7.3 Trillion range by 2030, its currency's international role will expand. Bilateral INR trade settlement agreements with 22 countries are a realistic scenario, creating new hedging demand streams and expanding market size beyond the traditional USD-INR dominated transaction mix.

Second, Digital platform disruption is set to democratize access to forex services, with mobile-first platforms, API-based banking, and AI-driven pricing transforming the market. These innovations are reducing transaction costs and improving pricing transparency, making forex services more accessible to SMEs, retail travelers, and individual investors who were previously underserved by traditional banking channels.

Third, the CBDC integration era will begin. The central bank’s e-Rupee CBDC, currently in the pilot phase, has the potential to significantly transform cross-border payment settlement over the coming years. CBDC-based forex transactions could lower costs, enable near real-time settlement, and enhance transparency through data-driven risk management capabilities.

Research Methodology

Primary Research

Primary research encompassed structured interviews conducted in 2024-2025 with India foreign exchange market stakeholders, including treasury heads at major authorized dealer banks, forex compliance officers, corporate CFOs managing multi-currency exposures, fintech platform executives, and senior RBI officials. Primary insights validated market sizing, segmentation estimates, and technology adoption timelines.

Secondary Research

Secondary sources include RBI Annual Reports, Monthly Forex Turnover Data (RBI), FEMA notifications, SEBI circulars on currency derivative trading, National Securities Depository Limited (NSDL) FII investment data, BIS Triennial Central Bank Survey (OTC forex turnover), World Bank remittance data, Ministry of Commerce export-import statistics, company annual reports, and leading financial publications including The Economic Times, Business Standard, and Mint.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models, incorporating India's GDP growth trajectory, trade openness indices, capital account liberalization pathways, digital platform adoption curves, and historical forex market evolution patterns. Scenario analysis (base, optimistic, and conservative cases) was performed to account for macroeconomic and policy uncertainty.

India Foreign Exchange Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Counterparties Covered | Reporting Dealers, Other Financial Institutions, Non-Financial Customers |

| Types Covered | Currency Swap, Outright Forward and Fx Swaps, Fx Options |

| Regions Covered | South India, North India, West and Central India, East India |

| Companies Covered | State Bank of India, HDFC Bank Ltd., ICICI Bank, Axis Bank, Kotak Mahindra Bank, Standard Chartered Bank, Yes Bank, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Foreign Exchange Market Report

The India foreign exchange market was valued at USD 33.40 Billion in 2025, driven by rising cross-border trade, increasing FDI flows, growing NRI remittances, and progressive RBI policy frameworks supporting broader market participation.

The market is projected to reach USD 68.80 Billion by 2034, growing at a CAGR of 8.4% during 2026-2034, supported by digital platform adoption, INR internationalization, and expanding corporate hedging demand.

Reporting Dealers lead with a 42.1% share in 2025, underpinned by their role as primary interbank liquidity providers, authorized currency dealers, and execution agents for institutional and corporate clients.

Currency Swaps lead with a 40.3% share in 2025, driven by corporate demand for cross-currency interest rate risk management, external commercial borrowing hedging, and RBI liquidity swap operations.

North India dominates with 34.0% share in 2025, anchored by the NCR's concentration of corporate headquarters, government-linked entities, and authorized dealer banking operations.

Key drivers include rising cross-border trade and FDI, digital forex platform proliferation, NRI remittance growth, RBI policy interventions, and the progressive push toward INR internationalization across 22+ trade partner countries.

Major players include State Bank of India, HDFC Bank Ltd., ICICI Bank, Axis Bank, Kotak Mahindra Bank, Standard Chartered Bank, and Yes Bank.

FX Options are the fastest-growing type at ~9.8% CAGR through 2034, while Non-financial Customers are the fastest-growing counterparty cohort at ~9.6% CAGR, reflecting growing corporate treasury sophistication and retail market democratization.

NRI deposits reached USD 158.94 Billion outstanding by August 2024, up significantly year-on-year. As the world's largest remittance recipient, India benefits from structural inflows that strengthen forex reserves and expand market liquidity.

The RBI functions as both regulator and active participant. It conducts USD/INR swap auctions for liquidity management, intervenes in spot markets to limit rupee volatility, and sets the policy framework through FEMA notifications and authorized dealer licensing.

The central bank’s approval of INR-based trade settlement with multiple countries is creating new demand for INR cross-currency hedging instruments. This shift is expanding the market’s total addressable size beyond the traditional USD-INR-dominated transaction base, supporting greater diversification in forex activity.

Key opportunities include digital forex platform investment, INR trade settlement corridor infrastructure, AI-powered treasury risk management solutions, CBDC-compatible payment infrastructure, and Tier-2/3 city market expansion through mobile-first distribution models.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade