India Foundry Equipment Market Size, Share, Trends and Forecast by Equipment Type, Foundry Process, Application, and Region, 2026-2034

India Foundry Equipment Market Summary:

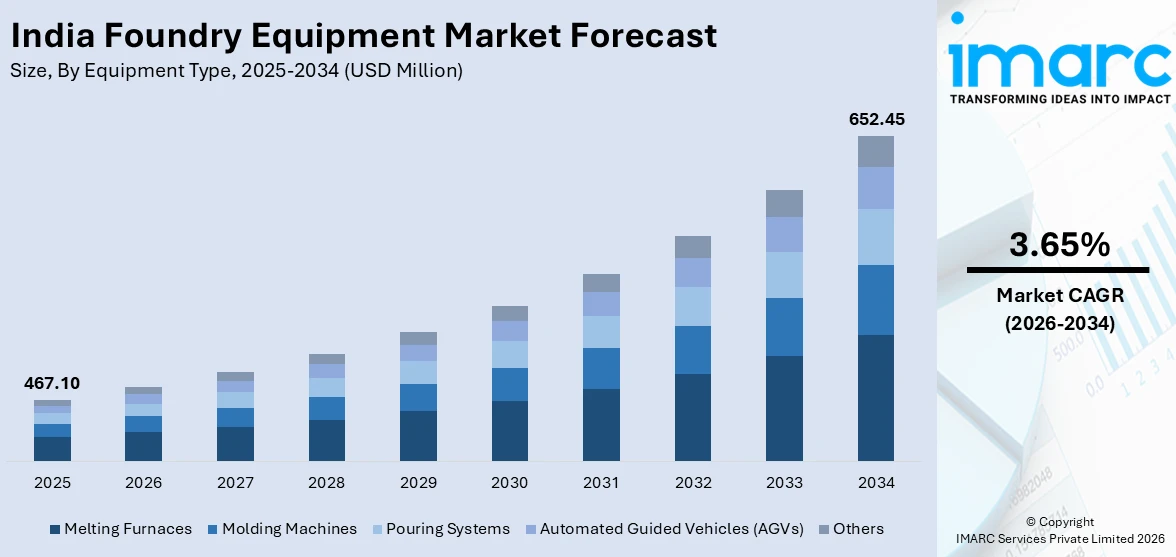

The India foundry equipment market size was valued at USD 467.10 Million in 2025 and is projected to reach USD 652.45 Million by 2034, growing at a compound annual growth rate of 3.65% from 2026-2034.

The India foundry equipment market is undergoing a transformative phase, fueled by rising industrial activity, a surging automotive sector, and rapid infrastructure expansion across the country. Government-backed manufacturing initiatives are catalyzing investments in modern casting technologies and equipment, while the accelerating adoption of electric vehicles is reshaping demand for high-precision, lightweight casting solutions. The ongoing integration of automation and digital tools across foundry operations is further redefining production efficiency, enabling manufacturers to deliver superior output quality while managing costs. These convergent forces are collectively reinforcing the India foundry equipment market share.

Key Takeaways and Insights:

- By Equipment Type: Melting furnaces dominate the market with a share of 48.0% in 2025, owing to their critical role as the foundational unit in virtually every casting operation. Coreless and channel-type induction furnaces are widely preferred across ferrous and non-ferrous applications for their superior energy efficiency and precise temperature control.

- By Foundry Process: Die casting leads the market with a share of 28.5% in 2025, driven by the growing demand for high-precision aluminum components in the automotive and industrial sectors. Its suitability for mass production of complex, thin-walled parts with excellent dimensional accuracy makes it the preferred process for EV structural components.

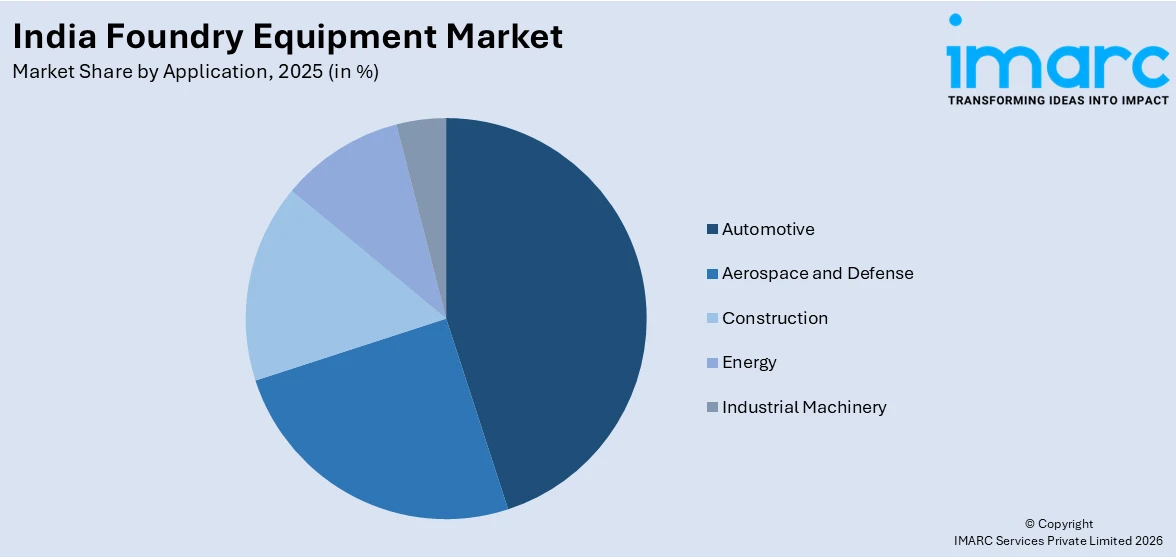

- By Application: Automotive represents the largest segment with a market share of 41.3% in 2025, underpinned by India's position as one of the world's largest vehicle producers and the deepening integration of foundry-made components across combustion and electric powertrain platforms.

- By Region: West India dominate the market with a share of 32.5% in 2025, anchored by the dense foundry and automotive manufacturing clusters across Gujarat and Maharashtra, supported by robust port connectivity and established OEM-supplier ecosystems.

- Key Players: The India foundry equipment market features a moderately fragmented competitive landscape, with domestic manufacturers such as Electrotherm (India) and Inductotherm India competing alongside global equipment majors. Players are increasingly differentiating through automation integration, energy efficiency, and aftersales service networks.

To get more information on this market Request Sample

The India foundry equipment market is positioned at the confluence of several powerful macro-economic trends. India’s foundry industry ranks among the largest globally, supporting a substantial workforce and a wide network of manufacturing units. Growth is being fueled by increased investment and modernization initiatives, as government programs focused on self-reliance and domestic manufacturing encourage upgrades to foundry infrastructure. These efforts are enhancing production capabilities, improving efficiency, and enabling the adoption of advanced technologies across casting operations, positioning India’s foundry sector for sustained expansion. For instance, in December 2024, Jaya Hind Industries Pvt Ltd installed India's largest 4,400-tonne high-pressure die-casting machine sourced from Bühler-Switzerland at its Urse plant near Pune, marking a milestone in domestic aluminum casting capability for electric vehicles and heavy-duty applications. The increasing prevalence of Industry 4.0 practices, including IoT-enabled furnace monitoring, digital twins, and AI-driven process optimization, is further widening the productivity gap between modernized facilities and legacy operations, creating sustained demand for next-generation foundry equipment.

India Foundry Equipment Market Trends:

Accelerating Shift Toward Energy-Efficient and Sustainable Foundry Equipment

Sustainability has emerged as a defining priority for India's foundry sector, driven by escalating energy costs and tightening environmental compliance requirements. Foundries are increasingly replacing legacy cupola furnaces with energy-efficient induction melting units that offer superior thermal control and substantially lower emissions. Sand reclamation systems and low-emission casting technologies are gaining traction as foundries seek to reduce raw material waste and carbon footprints. At IFEX 2025, Rhino Machines led a dedicated symposium on sustainable foundry practices, demonstrating how MSME-led innovation can drive meaningful progress in environmentally responsible manufacturing, signaling a broader sectoral commitment to green transformation.

Integration of Industry 4.0 Technologies Across Foundry Operations

Indian foundries are increasingly embedding Industry 4.0 technologies, including IoT-enabled real-time monitoring, AI-driven defect detection, digital twins, and predictive maintenance systems, into their casting workflows. These innovations are improving yield rates, reducing downtime, and enabling finer quality control across high-volume production lines. For instance, in March 2024, Godrej Tooling developed the Smart Connected Die Casting Die, a patented device that analyzes die parameters in real time to improve foundry efficiency, increasing die life by approximately 10% while reducing per-piece production costs by a similar margin. This indigenous solution underscores the growing emphasis on data-driven manufacturing intelligence within India's foundry equipment ecosystem.

Growing Demand for High-Pressure Die Casting Equipment Driven by EV Transition

India's accelerating electric vehicle adoption is triggering a fundamental shift in foundry equipment demand, particularly toward large-tonnage high-pressure die casting systems capable of producing complex aluminum structural components with tight dimensional tolerances. The replacement of multi-part assemblies with single-piece gigacastings for battery enclosures, motor housings, and chassis structures is compelling foundries to invest in advanced die casting machinery. For instance, in January 2025, Sundaram Clayton Limited established a new die casting facility in India to expand manufacturing capacity in response to surging automotive demand, reflecting the broader industry-wide pivot toward aluminum-intensive casting platforms aligned with EV powertrain requirements.

Market Outlook 2026-2034:

The India foundry equipment market is poised for sustained growth over the forecast period, supported by expanding automotive production, escalating infrastructure investment, and a government-led push toward domestic manufacturing self-sufficiency. Rising EV adoption will intensify demand for advanced die casting and melting systems capable of processing lightweight alloys at scale. Ongoing modernization of India's approximately 5,000 foundry units. the majority being MSMEs, will create recurring replacement and upgrade demand. The market generated a revenue of USD 467.10 Million in 2025 and is projected to reach a revenue of USD 652.45 Million by 2034, growing at a compound annual growth rate of 3.65% from 2026-2034.

India Foundry Equipment Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

|

Equipment Type |

Melting Furnaces |

48.0% |

|

Foundry Process |

Die Casting |

28.5% |

|

Application |

Automotive |

41.3% |

|

Region |

West India |

32.5% |

Equipment Type Insights:

- Molding Machines

- Melting Furnaces

- Pouring Systems

- Automated Guided Vehicles (AGVs)

- Others

Melting furnaces represent the largest share of 48.0% of the total India foundry equipment market in 2025.

Melting furnaces constitute the highest-value equipment category within India's foundry ecosystem, reflecting their indispensable role at the core of every metal casting operation. Induction melting furnaces, both coreless and channel-type, have become the technology of choice for a growing number of foundries due to their energy efficiency, precise temperature regulation, and lower emissions compared to conventional cupola and reverberatory furnaces. India's induction furnace manufacturing base is robust, with established players such as Electrotherm (India) and Inductotherm India producing a diverse capacity range from a few kilograms to over 60 tonnes. The Make in India initiative and PLI schemes have catalyzed further investment in domestic furnace production.

The prominence of melting furnaces is being strengthened by the growing use of scrap-based melting in foundries. Increased availability of clean ferrous and non-ferrous scrap allows operators to reduce reliance on primary raw materials while improving energy efficiency during melting. As scrap utilization rises, facilities are investing in larger-capacity, automated furnace systems to handle more flexible feedstock. With continued expansion in steel and non-ferrous casting production, demand for advanced melting furnace technology is expected to maintain strong growth, supporting efficiency, sustainability, and productivity improvements across India’s foundry sector.

Foundry Process Insights:

- Green Sand Casting

- Investment Casting

- Die Casting

- Permanent Mold Casting

- Centrifugal Casting

Die casting leads the market with a share of 28.5% of the total India foundry equipment market in 2025.

Die casting has become one of the fastest-growing foundry processes in India, driven by the rising need for precision aluminum components across automotive, consumer electronics, and industrial sectors. Its capability to produce complex, thin-walled parts with high dimensional accuracy and rapid production rates makes it ideal for EV structural assemblies, transmission housings, and electronic enclosures. The shift toward high-pressure die casting and consolidated casting strategies is encouraging foundries to invest in larger, heavy-tonnage machinery. This trend is significantly expanding domestic capacity for manufacturing large, lightweight aluminum components for advanced industrial and automotive applications.

The die casting equipment segment is also advancing through technological upgrades, including real-time process monitoring, automated mold temperature control, and vacuum-assisted casting for high-specification applications. Innovations in die design and monitoring are improving component quality, extending die life, and reducing production costs. As automotive manufacturers increasingly adopt electric vehicle platforms and shift toward lightweight aluminum castings to enhance efficiency and performance, the demand for sophisticated high-pressure and low-pressure die casting machines is expected to grow steadily, supporting modernization and productivity improvements across India’s foundry industry.

Application Insights:

Access the comprehensive market breakdown Request Sample

- Automotive

- Aerospace and Defense

- Construction

- Energy

- Industrial Machinery

Automotive represent the highest revenue share of 41.3% of the total India foundry equipment market in 2025.

The automotive sector remains the primary demand driver for foundry equipment in India, accounting for a substantial share of total casting consumption in the country. Foundry-manufactured components, including engine blocks, cylinder heads, transmission housings, brake components, and suspension parts, are integral to both internal combustion engine and electric vehicle platforms. India's growing position as a global automotive production hub, supported by the world's third-largest vehicle market and expanding OEM manufacturing bases, creates consistent demand for high-performance molding machines, induction furnaces, and die casting systems. Bharat Stage VI emission norms have additionally accelerated the shift toward precision cast components that deliver tighter tolerances and superior surface finishes across powertrain assemblies.

The transition to electric vehicles is transforming automotive casting requirements, driving higher demand for equipment capable of producing lightweight aluminum and magnesium structural components. As manufacturers increasingly adopt EV-specific designs, investments in high-pressure die-casting machines, energy-efficient induction furnaces, and precision molding systems are expanding to support the production of battery enclosures, chassis components, and other critical parts. The growing focus on aluminum-intensive castings for electric vehicles is expected to sustain strong demand for advanced foundry equipment in the automotive segment, reinforcing the market’s long-term growth trajectory.

Regional Insights:

- North India

- South India

- East India

- West India

West India exhibits a clear dominance with a 32.5% share of the total India foundry equipment market in 2025.

West India holds a strong position in the foundry equipment market due to the region’s high industrial concentration, particularly in Maharashtra and Gujarat. Maharashtra’s industrial corridors host a mix of automotive, defense, and heavy engineering manufacturers that rely heavily on precision casting and advanced foundry processes. These facilities require modern molding machines, die-casting systems, and sand handling equipment to maintain production efficiency and quality. The concentration of large-scale manufacturing operations, combined with ongoing industrial expansion, creates consistent demand for advanced foundry equipment and services in Western India, making it a key regional hub for market growth.

The petrochemical, chemical processing, electronics, and renewable energy manufacturing clusters in Gujarat serve as a great contribution to the demand for foundry equipment in West India. The high rate at which the state has embraced high-pressure die-casting, automated molding, and sand reclamation systems shows that it requires modern, efficient and environmentally compliant equipment. With the increasing regions demanding special machinery in foundries as companies upgrade to higher standards of productivity and quality, regional needs are increasing. Moreover, the close positioning with the suppliers, presence of skilled labor, and favorable state policies further make Western India a leading market in terms of investments in foundry equipment.

Market Dynamics:

Growth Drivers:

Why is the India Foundry Equipment Market Growing?

Expanding Automotive and Electric Vehicle Production

India's automotive sector is one of the most powerful catalysts for foundry equipment demand in the country. As the world's third-largest vehicle market and a key global production base, India's consistent growth in passenger car, commercial vehicle, and two-wheeler manufacturing translates directly into elevated demand for induction melting furnaces, high-pressure die casting machines, and precision molding systems. The transition toward electric mobility is adding a new dimension to this demand, as EV powertrain platforms require a fundamentally different casting mix, centered on aluminum structural components, battery enclosures, and motor housings, that necessitates larger-tonnage HPDC equipment and more sophisticated thermal management capabilities. Hindalco's Chakan plant shipped 10,000 EV battery enclosures to Mahindra Electric by December 2024, with annual capacity set to scale to 160,000 units by FY-2027. As Bharat Stage VI norms push further quality upgrades and EV penetration accelerates, foundries across India are upgrading to advanced equipment capable of meeting the exacting dimensional and material standards of next-generation automotive platforms.

Government Initiatives and Policy Support

India’s foundry equipment market is benefiting from multiple government initiatives aimed at strengthening domestic manufacturing and modernizing industrial capabilities. National programs promoting local production and industrial self-reliance are encouraging investment in advanced foundry infrastructure. At the same time, policy support for sectors such as automotive, defense, and capital goods is expanding manufacturing activity, which indirectly drives demand for casting and foundry technologies. Efforts to introduce Industry 4.0 practices are also encouraging foundries to adopt automated and digitally integrated equipment to improve productivity and efficiency. As a result, many foundries are transitioning from conventional casting systems to more advanced, high-pressure, and technology-driven manufacturing setups.

Rapid Infrastructure Development and Defense Manufacturing Expansion

India's sustained infrastructure investment cycle is creating significant complementary demand for foundry-produced components, ranging from structural steel castings and valve assemblies for water and energy systems to precision castings for railway and construction equipment. The National Infrastructure Pipeline (NIP) and major programs such as Pradhan Mantri Awas Yojana (PMAY) are driving construction sector growth that requires heavy machinery and structural castings at scale. Railway modernization, including Vande Bharat trainsets, metro rail expansion, and freight corridor development, demands specialized casting equipment for precision wheel and bogie components. Simultaneously, the government's push for indigenous defense manufacturing under Atmanirbhar Bharat is compelling foundries to invest in vacuum casting and investment casting equipment capable of meeting aerospace-grade specifications. These structural demand catalysts are expected to maintain a broad and diversified base of foundry equipment procurement across multiple industry verticals throughout 2026-2034.

Market Restraints:

What Challenges the India Foundry Equipment Market is Facing?

Volatility in Raw Material and Energy Costs

India's foundry equipment market faces significant headwinds from persistent raw material price volatility, particularly in aluminum, steel, and petroleum coke. Rising delivered prices for metallurgical coke, which surged following import quota reductions, have squeezed margins at cupola-based foundries, limiting their capacity to invest in new equipment. Energy cost unpredictability further complicates multi-year equipment procurement planning, especially for smaller MSME foundries that lack the hedging capabilities of larger integrated players.

Skilled Labor Shortage in Advanced Foundry Operations

The widespread adoption of advanced foundry equipment, including automation-integrated induction furnaces, robotics, and IoT-enabled molding systems, is constrained by an acute shortage of skilled technicians capable of operating and maintaining these sophisticated systems. India's foundry workforce is predominantly MSME-based, and the gap between available skills and the requirements of modern equipment remains a structural barrier to equipment upgrades, particularly in tier-2 manufacturing clusters away from major industrial hubs.

Stringent Environmental Regulations and Compliance Costs

Stricter environmental regulations, including tighter emission and effluent standards, are placing increasing financial pressure on foundries. Compliance with emerging international carbon regulations is also raising concerns for casting exporters serving global markets. Many foundries are required to upgrade to cleaner and more energy-efficient equipment to meet these standards. However, for smaller operators, the significant capital investment needed for such upgrades can slow modernization efforts and delay the adoption of advanced foundry equipment technologies.

Competitive Landscape:

The India foundry equipment market is characterized by a moderately fragmented competitive structure, with a mix of established domestic manufacturers, specialized regional players, and global equipment majors competing across equipment categories and price segments. Domestic players maintain strong competitive positions in induction furnace and sand processing equipment segments, benefiting from localized service networks, deep technical expertise, and competitive pricing tailored to India's predominantly MSME-dominated foundry base. Global equipment companies retain leadership in high-precision die casting machinery, advanced automation systems, and specialized casting equipment for aerospace and defense applications. Competitive differentiation is increasingly centered on energy efficiency credentials, automation integration, digital monitoring capabilities, and the quality of post-sales service and technical support networks. Strategic alliances, technology licensing agreements, and acquisitions are reshaping market positioning, with the market expected to see progressive consolidation as the technological complexity of foundry equipment requirements increases.

Recent Developments:

- December 2024: SMG Group completed the acquisition of Hunter Foundry Machinery Corporation, a leading global provider of matchplate molding machines, sand casting technology, and mold handling equipment. The acquisition is designed to strengthen Hunter's global footprint while preserving its established legacy and customer relationships in both domestic and international foundry markets.

- April 2024: Savelli Machinery India Pvt. Ltd. announced the installation of advanced foundry equipment at Gautam Casting Group's new plant in Rajkot, comprising a 40-ton-per-hour sand plant and a high-pressure flask molding line for producing tractor and earth-moving equipment castings. Additional installations were planned across Gujarat, Jamshedpur, and Mangalore to further expand India's sand reclamation and recycling capabilities.

India Foundry Equipment Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Equipment Types Covered | Molding Machines, Melting Furnaces, Pouring Systems, Automated Guided Vehicles (AGVs), Others |

| Foundry Processes Covered | Green Sand Casting, Investment Casting, Die Casting, Permanent Mold Casting, Centrifugal Casting |

| Applications Covered | Automotive, Aerospace and Defense, Construction, Energy, Industrial Machinery |

| Regions Covered | North India, South India, East India, West India |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Foundry Equipment Market Report

The India foundry equipment market size was valued at USD 467.10 Million in 2025.

The India foundry equipment market is expected to grow at a compound annual growth rate of 3.65% from 2026-2034 to reach USD 652.45 Million by 2034.

Melting furnaces dominated the India foundry equipment market with a share of 48.0% in 2025, driven by their critical role in metal casting operations, widespread adoption of energy-efficient induction technology, and the expanding scale of ferrous and non-ferrous casting activity across the country.

Key factors driving the India foundry equipment market include rapid expansion of the automotive sector and EV transition, government-backed manufacturing initiatives such as Make in India and PLI schemes, large-scale infrastructure development programs, increasing adoption of Industry 4.0 technologies, and growing export competitiveness of India's foundry sector.

Major challenges include raw material and energy cost volatility impacting foundry investment cycles, acute shortage of skilled technicians capable of operating advanced equipment, stringent environmental compliance requirements raising capital expenditure burdens, and the financial constraints facing the MSME-dominated foundry base in adopting modern casting technologies.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)