India Fraud Detection and Prevention Market Size, Share, Trends and Forecast by Component, Application, Organization Size, Vertical, and Region, 2026-2034

India Fraud Detection and Prevention Market Summary:

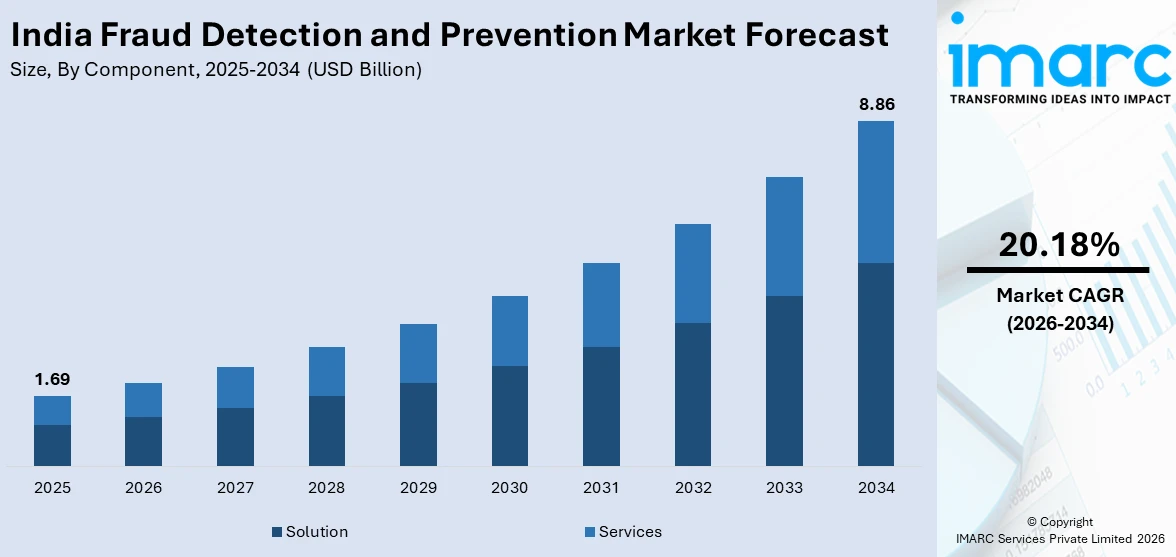

The India fraud detection and prevention market size was valued at USD 1.69 Billion in 2025 and is projected to reach USD 8.86 Billion by 2034, growing at a compound annual growth rate of 20.18% from 2026-2034.

The India fraud detection and prevention market is gaining strong momentum as the country undergoes rapid digital transformation across banking, e-commerce, and government services. Surging digital payment volumes, rising sophistication of cyber threats, and increasingly stringent regulatory mandates from bodies such as the Reserve Bank of India are driving organizations to invest in advanced fraud mitigation technologies. The growing integration of artificial intelligence (AI) and machine learning into real-time monitoring platforms is further expanding India fraud detection and prevention market share.

Key Takeaways and Insights:

- By Component: Solution dominates the market with a share of 59% in 2025, driven by enterprises prioritizing integrated software platforms for real-time fraud analytics, identity verification, and automated threat response.

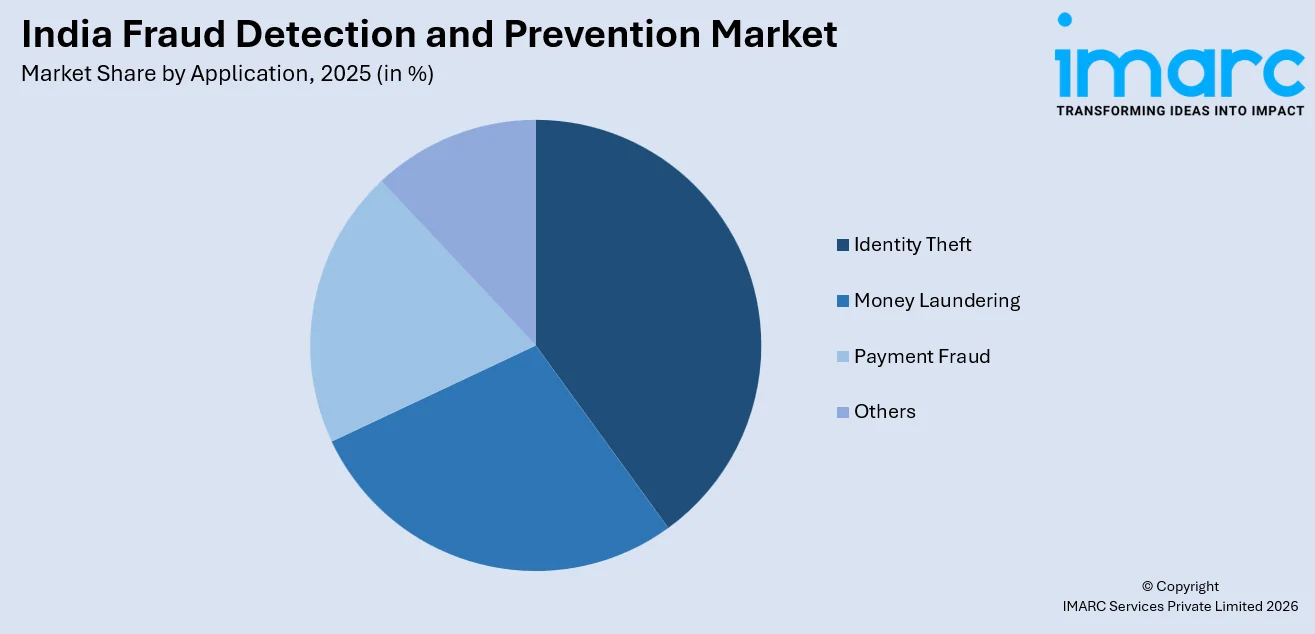

- By Application: Identity theft leads the market with a share of 25% in 2025, as surging data breaches and digital identity vulnerabilities compel organizations to deploy advanced authentication and identity protection tools.

- By Organization Size: Large enterprises hold the largest share at 73% in 2025, reflecting their extensive transaction volumes, complex digital ecosystems, and greater regulatory compliance obligations requiring robust fraud prevention infrastructure.

- By Vertical: BFSI accounts for the highest revenue share of 33% in 2025, as banking and financial institutions handle vast digital transaction flows and face heightened regulatory scrutiny for fraud risk management.

- By Region: North India represents the leading segment with a 30% share in 2025, supported by the concentration of major financial institutions, technology companies, and government infrastructure in the National Capital Region and surrounding states.

- Key Players: The India fraud detection and prevention market features intense competition among global technology firms, domestic fintech innovators, and specialized cybersecurity providers, all investing in artificial intelligence capabilities, strategic partnerships, and platform expansion to strengthen their market positioning.

To get more information on this market Request Sample

India’s fraud detection and prevention market is developing rapidly with increases in digital payments infrastructure and cyber attacks sophistication. There is a significant rise in the Unified Payments Interface, mobile banking facilities, and digital transactions with the evolution of e-commerce services. As the monetary loss from cyber attacks is increasing enormously, various business organizations, government bodies, and financial sectors are adopting AI-powered fraud detection systems to mitigate financial fraud. For example, the Reserve Bank Innovation Hub launched its “MuleHunter.AI” concept using advanced AI and machine learning technologies to detect and disable mule bank accounts that are involved in financial fraud activities, especially with two public sector banks in December 2024. Moreover, regulations, awareness regarding data privacy issues, and extensive collaborations between the public and private sectors are playing critical roles in boosting the market.

India Fraud Detection and Prevention Market Trends:

Rising Adoption of AI and Machine Learning in Fraud Analytics

Organizations in India are also using artificial intelligence and machine learning technologies to detect fraud. These technologies can analyze large amounts of data to detect patterns of fraud that other systems might miss. For example, in June 2025, Google announced the Safety Charter in India, enabling the expansion of AI-based fraud detection and scam prevention in the country through device-based detection and financial app partnerships. This increasing use of intelligent automation is thus contributing to the growth of the India fraud detection and prevention market.

Expansion of Real-Time Digital Payment Security Solutions

As online transactions through UPI-based systems crossed 185.8 billion in FY 2024-25, recording a 41.7% yearly increase, the need to monitor online fraud payments has gained momentum. Various financial bodies are employing an adaptive security solution to monitor online fraud payments. For example, in 2025, the Department of Telecommunications launched the Financial Fraud Risk Indicator scheme, which has since been able to prevent cyber fraud losses of approximately INR 660 Crore across over 1,000 banks and financial institutions.

Growing Focus on Network-Level Fraud Prevention

Telecommunications providers and technology companies are embedding fraud detection directly into network infrastructure rather than relying solely on endpoint-based protection. This approach blocks threats at the source before they reach end-users. For instance, in May 2025, Bharti Airtel launched the world's first network-based solution to detect and block malicious links across all communication channels in real time. By September 2025, Airtel's AI-powered anti-fraud initiatives had resulted in a 68.7% reduction in financial losses on its network, as validated by the Indian Cyber Crime Coordination Centre.

Market Outlook 2026-2034:

India's fraud detection and prevention market is positioned for sustained expansion, underpinned by the country's accelerating digital economy, regulatory tightening, and growing cybersecurity awareness. The market generated a revenue of USD 1.69 Billion in 2025 and is projected to reach a revenue of USD 8.86 Billion by 2034, growing at a compound annual growth rate of 20.18% from 2026-2034. Continued investment in AI-driven analytics, biometric authentication, and cross-institutional intelligence-sharing platforms is expected to strengthen fraud resilience and unlock new revenue opportunities across India's evolving digital landscape.

India Fraud Detection and Prevention Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Component |

Solution |

59% |

|

Application |

Identity Theft |

25% |

|

Organization Size |

Large Enterprises |

73% |

|

Vertical |

BFSI |

33% |

|

Region |

North India |

30% |

Component Insights:

- Solution

- Services

Solution dominates with a market share of 59% of the total India fraud detection and prevention market in 2025.

Solution segment represents the largest share of the India Fraud Detection and Prevention Market, driven by the rapid digitalization of financial and commercial activities across the country. Organizations are increasingly adopting advanced fraud detection solutions to combat the rising volume and sophistication of fraudulent transactions associated with digital payments, mobile banking, e-commerce, and online services. These solutions typically integrate technologies such as artificial intelligence (AI), machine learning (ML), big data analytics, and real-time transaction monitoring, enabling proactive identification and prevention of fraud. Fraud detection solutions help enterprises analyze large volumes of structured and unstructured data to detect unusual patterns, behavioral anomalies, and high-risk activities in real time. This capability is especially critical in sectors such as banking, financial services and insurance (BFSI), retail, telecom, and government, where transaction volumes are high and regulatory compliance is stringent.

By automating fraud detection processes, organizations can significantly reduce financial losses, minimize false positives, and enhance operational efficiency. Additionally, the growing adoption of cloud-based and scalable fraud prevention platforms is supporting wider deployment across large enterprises as well as small and medium-sized businesses in India. Regulatory initiatives promoting digital payments and data security further encourage investment in robust fraud detection solutions. As fraud techniques continue to evolve, the demand for intelligent, adaptive, and integrated fraud prevention solutions is expected to remain strong, reinforcing the Solution segment’s dominance in the Indian market.

Application Insights:

Access the comprehensive market breakdown Request Sample

- Identity Theft

- Money Laundering

- Payment Fraud

- Others

Identity theft leads with a share of 25% of the total India fraud detection and prevention market in 2025.

Identity theft is the leading application segment, driven by the rapid expansion of digital identities and online transactions across the country. With the widespread adoption of mobile banking, e-wallets, UPI payments, and e-commerce platforms, individuals increasingly share sensitive personal and financial information online, making identity theft a major concern for organizations and consumers alike. Fraudsters use techniques such as phishing, social engineering, data breaches, and account takeover to impersonate legitimate users and gain unauthorized access to accounts. The growing use of Aadhaar-based verification, digital onboarding, and remote KYC processes has further increased the need for robust identity theft detection solutions.

To address this, organizations are deploying advanced technologies including biometric authentication, behavioral analytics, device fingerprinting, and AI-driven identity verification. These tools help detect suspicious activities in real time, reduce false identities, and prevent unauthorized transactions before financial losses occur. Industries such as banking, financial services and insurance (BFSI), telecom, e-commerce, and government are at the forefront of adopting identity theft prevention solutions due to strict regulatory requirements and high reputational risk. As cybercriminals continue to develop more sophisticated methods, the demand for advanced identity theft detection and prevention solutions is expected to remain strong. This makes identity theft the most critical and dominant application segment in India’s fraud detection and prevention market.

Organization Size Insights:

- Small and Medium Enterprises

- Large Enterprises

Large enterprises exhibit a clear dominance with a 73% share of the total India fraud detection and prevention market in 2025.

Large enterprises hold the largest share in the market due to their extensive digital infrastructure, high transaction volumes, and greater exposure to complex fraud risks. These organizations operate across multiple channels, online banking, mobile applications, enterprise systems, and third-party platforms, making them prime targets for sophisticated fraud schemes such as identity theft, payment fraud, and money laundering. As a result, large enterprises prioritize advanced fraud detection and prevention solutions to safeguard financial assets and sensitive data.

These solutions enable centralized monitoring across business units and geographies, allowing faster detection and response to fraudulent activities. Another key factor contributing to their market dominance is the early adoption of emerging technologies, including cloud-based solutions, behavioral biometrics, and predictive analytics. Large enterprises also maintain dedicated cybersecurity and risk management teams, ensuring continuous optimization of fraud detection systems. As digital transformation accelerates and fraud techniques become more advanced, large enterprises are expected to remain the primary contributors to revenue growth in India’s fraud detection and prevention market.

Vertical Insights:

- BFSI

- Government and Defense

- Healthcare

- IT and Telecom

- Manufacturing

- Retail and E-Commerce

- Others

BFSI leads with a share of 33% of the total India fraud detection and prevention market in 2025.

The banking, financial services, and insurance (BFSI) sector leads the market due to its high exposure to financial risks and its central role in the country’s digital economy. The rapid growth of online banking, mobile wallets, UPI transactions, credit cards, and digital lending platforms has significantly increased transaction volumes, making the BFSI sector a prime target for fraud activities such as identity theft, payment fraud, account takeover, and money laundering.

Additionally, stringent regulatory and compliance requirements imposed by authorities such as the Reserve Bank of India (RBI) further drive the adoption of robust fraud management systems. Financial institutions must ensure data security, transaction transparency, and customer protection, making fraud prevention a strategic priority rather than an optional investment. As digital financial services continue to expand across urban and rural India, the BFSI sector is expected to maintain its dominant position in the fraud detection and prevention market.

Regional Insights:

- North India

- West and Central India

- South India

- East and Northeast India

The North India exhibits a clear dominance with a 30% share of the total India fraud detection and prevention market in 2025.

North India accounts for the largest share of the market, supported by its strong economic activity, high concentration of financial institutions, and rapid adoption of digital technologies. Major metropolitan and commercial hubs such as Delhi NCR, Chandigarh, Noida, Gurugram, and Jaipur host a large number of banks, financial service providers, fintech companies, e-commerce firms, and corporate headquarters, all of which generate high volumes of digital and financial transactions. This concentration significantly increases the demand for advanced fraud detection and prevention solutions.

The region has witnessed accelerated growth in digital payments, mobile banking, online retail, and digital lending, which has also led to a rise in fraud attempts including identity theft, payment fraud, and cyber-enabled financial crimes. To counter these threats, organizations in North India are increasingly investing in AI- and machine learning, based fraud detection systems, real-time monitoring tools, and identity verification technologies. Additionally, North India benefits from a strong technology ecosystem and access to skilled IT and cybersecurity professionals, enabling faster adoption and implementation of advanced fraud prevention platforms. Government initiatives promoting digital governance and cashless transactions further contribute to market growth in the region. As enterprises continue to scale digital operations and regulatory oversight strengthens, North India is expected to maintain its leadership position in the India Fraud Detection and Prevention Market over the forecast period.

Market Dynamics:

Growth Drivers:

Why is the India Fraud Detection and Prevention Market Growing?

Surging Digital Transaction Volumes and Expanding Digital Economy

India's digital payments ecosystem has experienced unprecedented growth, with UPI alone processing more than 20 billion transactions worth over ₹24.85 Lakh Crore in August 2025, representing a major increase from the previous year and accounting for 83.4% of the country's total digital payment volume. This explosive expansion of digital commerce across banking, retail, insurance, and government services has vastly enlarged the potential attack surface for cybercriminals, compelling organizations to invest in advanced fraud detection and prevention infrastructure. As more people and businesses migrate to digital channels, the complexity and frequency of fraudulent activities have intensified. The sheer scale of transaction volumes requires automated, real-time monitoring capabilities that can process and analyze data at speed. This structural shift toward a digital-first economy is creating sustained, long-term demand for fraud detection solutions capable of scaling alongside India's evolving digital infrastructure.

Escalating Cybercrime Losses and Evolving Threat Landscape

The financial toll of cybercrime in India has reached alarming levels, with cybercriminals responsible for losses exceeding INR 22,842 crore in 2024, marking a substantial increase from previous years. The number of reported financial cyber fraud incidents surpassed 20 lakh cases in 2024, reflecting the growing sophistication of fraudsters who increasingly leverage artificial intelligence, deepfake technology, and social engineering tactics to evade traditional security measures. This escalating threat environment is compelling organizations across all sectors to strengthen their fraud prevention capabilities with advanced technologies. Enterprises are recognizing that legacy rule-based systems are no longer sufficient against modern attack vectors, driving adoption of adaptive, AI-powered detection platforms that can evolve alongside emerging fraud patterns and protect against both known and novel threats.

Strengthening Regulatory Mandates and Compliance Requirements

The Indian regulatory landscape for fraud prevention has become increasingly rigorous, with the Reserve Bank of India introducing comprehensive directives that mandate financial institutions to implement robust cybersecurity and fraud risk management frameworks. In July 2024, the RBI issued its Master Directions on Cyber Resilience and Digital Payment Security Controls for non-bank payment system operators, establishing stringent requirements for risk assessments, incident reporting, and security controls. Additionally, the Digital Lending Directions issued in 2025 consolidated regulatory requirements for digital lending platforms, mandating enhanced data security, transparency, and cybersecurity measures. These evolving compliance obligations are driving significant investments in fraud detection and prevention solutions, as non-compliance carries the risk of substantial penalties, operational restrictions, and reputational damage for regulated entities across the financial services landscape.

Market Restraints:

What Challenges the India Fraud Detection and Prevention Market is Facing?

Shortage of Skilled Cybersecurity Professionals

India faces a significant shortage of trained cybersecurity professionals capable of managing, deploying, and optimizing advanced fraud detection systems. The limited availability of skilled data scientists, AI engineers, and fraud analysts restricts the ability of organizations, particularly smaller enterprises, to fully leverage the potential of sophisticated prevention technologies, thereby slowing market adoption.

High Implementation Costs for Advanced Solutions

The deployment of comprehensive fraud detection and prevention platforms requires substantial upfront investment in technology infrastructure, software licensing, integration services, and ongoing maintenance. For small and medium enterprises operating with constrained budgets, these costs represent a significant barrier to adoption, limiting the market's penetration across India's vast and diverse business landscape.

Integration Challenges with Legacy Systems

Many Indian enterprises, particularly in the banking and government sectors, continue to operate on legacy IT infrastructure that lacks compatibility with modern AI-driven fraud detection solutions. Integrating advanced platforms with outdated systems is technically complex, time-consuming, and costly, creating implementation delays and limiting the effectiveness of newly deployed fraud prevention technologies.

Competitive Landscape:

The India fraud detection and prevention market is characterized by dynamic competition among global technology corporations, specialized cybersecurity firms, and emerging domestic fintech companies. Market players are differentiating through investments in artificial intelligence (AI) capabilities, cloud-based delivery models, and strategic partnerships with financial institutions and regulatory bodies. Companies are expanding their product portfolios to offer end-to-end fraud management solutions that address identity verification, transaction monitoring, and compliance automation. Collaborative approaches, including data-sharing initiatives between industry participants and government agencies, are becoming increasingly important for strengthening collective fraud resilience across the ecosystem.

India Fraud Detection and Prevention Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Components Covered | Solution, Services |

| Applications Covered | Identity Theft, Money Laundering, Payment Fraud, Others |

| Organization Sizes Covered | Small and Medium-sized Enterprises, Large Enterprises |

| Verticals Covered | BFSI, Government and Defense, Healthcare, IT and Telecom, Manufacturing, Retail and E-Commerce, Others |

| Regions Covered | North India, West and Central India, South India, East and Northeast India |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Fraud Detection and Prevention Market Report

The India fraud detection and prevention market size was valued at USD 1.69 Billion in 2025.

The market is expected to grow at a compound annual growth rate of 20.18% from 2026-2034 to reach USD 8.86 Billion by 2034.

Solution, holding the largest revenue share of 59% in 2025, leads the India fraud detection and prevention market, driven by enterprise demand for integrated fraud analytics, authentication platforms, and automated compliance tools that deliver real-time protection across digital channels.

Key factors driving the India fraud detection and prevention market include surging digital transaction volumes, escalating cybercrime losses, strengthening regulatory mandates, growing AI and machine learning adoption, and increasing enterprise awareness around data privacy and security.

Major challenges include a shortage of skilled cybersecurity professionals, high implementation costs for advanced solutions, integration difficulties with legacy IT systems, data privacy concerns, and the rapidly evolving nature of fraud techniques.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)