India Frequency Converter Market Size, Share, Trends and Forecast by Type, End Use Industry, and Region, 2026-2034

India Frequency Converter Market Summary:

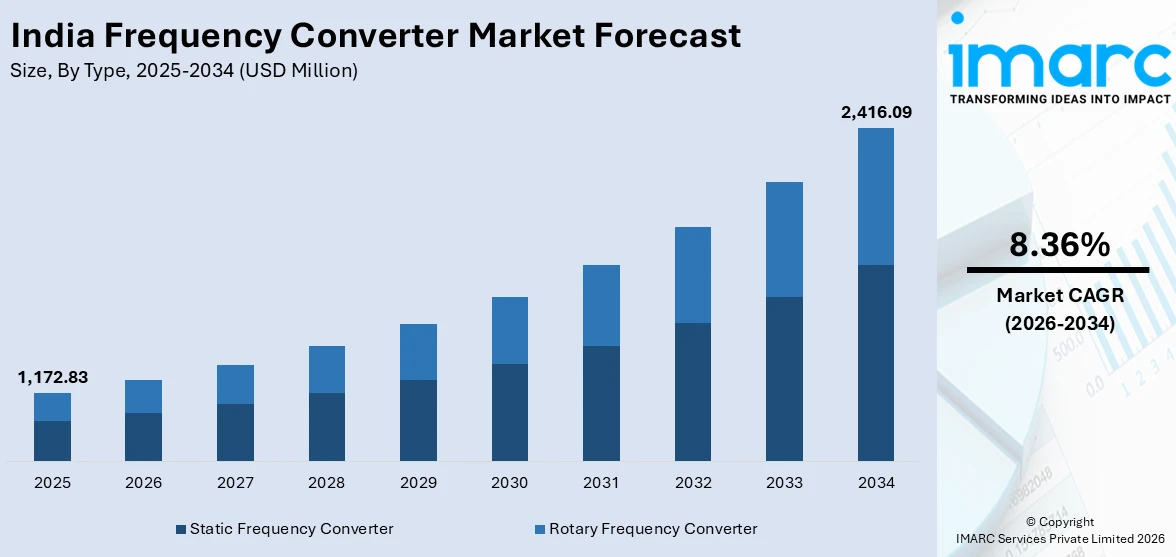

The India frequency converter market size was valued at USD 1,172.83 Million in 2025 and is projected to reach USD 2,416.09 Million by 2034, growing at a compound annual growth rate of 8.36% from 2026-2034.

The India frequency converter market is experiencing robust expansion driven by rapid industrialization, large-scale infrastructure modernization, and the country’s accelerating transition toward renewable energy integration. Growing investments in the power and energy sector, coupled with the expansion of aerospace and defense manufacturing capabilities, are fueling demand for advanced frequency conversion solutions. Additionally, the electrification of India’s railway network, the expansion of oil and gas exploration activities, and the increasing adoption of industrial automation technologies across manufacturing and process industries are strengthening the India frequency converter market share.

Key Takeaways and Insights:

- By Type: Static frequency converter dominates the market with a share of 60% in 2025, driven by its compact design, higher energy efficiency, lower maintenance requirements, and growing adoption across power systems and industrial automation applications.

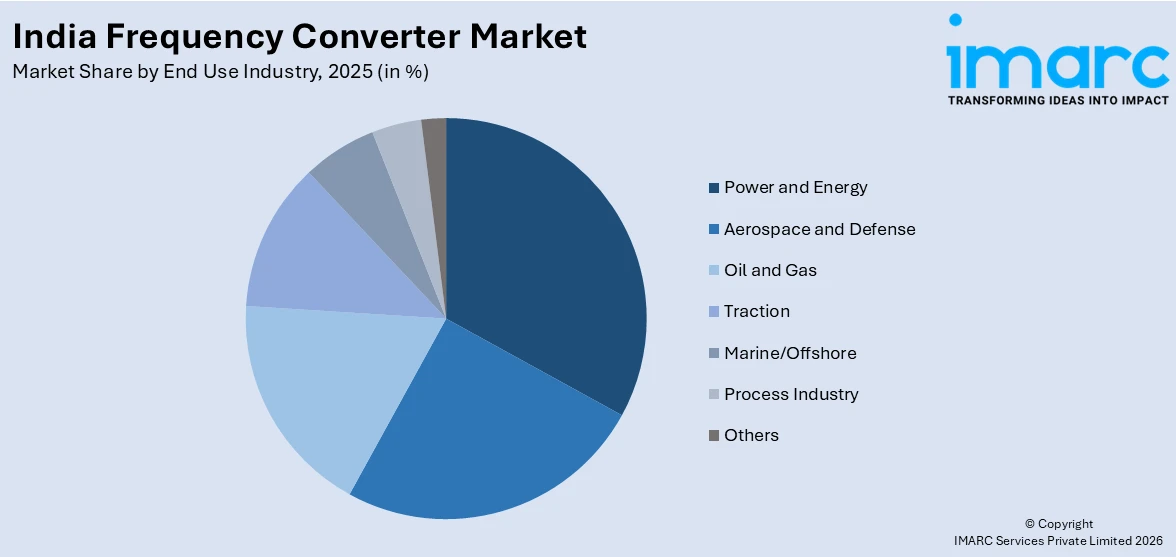

- By End Use Industry: Power and energy lead the market with a share of 33% in 2025, supported by massive investments in renewable energy integration, grid modernization, and the expansion of conventional and nuclear power generation infrastructure.

- Key Players: The India frequency converter market features a moderately competitive landscape with established multinational corporations competing alongside domestic manufacturers. Key players are focusing on expanding local manufacturing capabilities, investing in research and development, launching energy-efficient product lines, and forming strategic partnerships to strengthen their market positioning.

To get more information on this market Request Sample

The India frequency converter market is advancing on the back of large-scale investments in energy infrastructure, defense modernization, and industrial expansion. Frequency converters play a critical role in ensuring compatibility between different power frequency standards, optimizing motor speeds for energy efficiency, and enabling the seamless integration of variable renewable energy sources into the power grid. The country’s target of integrating 500 GW of renewable energy capacity by 2030 is generating significant demand for advanced power conversion equipment. For instance, in November 2024, the consortium of Hitachi Energy India and Bharat Heavy Electricals Limited was awarded a contract by Power Grid Corporation of India to design and execute a ±800 kV, 6,000 MW HVDC link to transmit renewable energy from Khavda in Gujarat to Nagpur in Maharashtra, spanning over 1,200 kilometers. This underscores the critical role of advanced frequency and power conversion technologies in India’s energy transition. The rising defense budget, near-complete railway electrification, and expanding offshore oil and gas exploration further contribute to the market’s sustained growth trajectory.

India Frequency Converter Market Trends:

Growing Integration of Renewable Energy Sources into the National Grid

India’s aggressive renewable energy expansion is driving substantial demand for frequency converters that enable grid synchronization of variable power outputs from solar and wind installations. Frequency converters serve as essential components in doubly-fed induction generators used in modern wind turbines and in grid-tie inverter systems for solar installations. As of November 2025, India’s total installed renewable energy capacity reached 253.96 GW, representing 51.5% of the country’s total electricity capacity. The Central Electricity Authority has reaffirmed the goal of integrating 600 GW of renewables by 2032, further driving India frequency converter market growth.

Accelerating Industrial Automation and Smart Manufacturing Adoption

India’s manufacturing sector is rapidly embracing Industry 4.0 technologies, creating heightened demand for frequency converters in motor control and process optimization applications. Variable frequency drives and static frequency converters play a crucial role in enabling accurate speed control, optimizing energy consumption, and extending the operational life of equipment in manufacturing and processing facilities. The increasing focus on industrial efficiency and automation has encouraged major technology providers to strengthen domestic production and assembly capabilities. This growing emphasis on localized manufacturing of power electronics reflects rising demand for advanced motor control and energy management solutions across India’s industrial landscape.

Expansion of Aerospace, Defense, and Railway Modernization Programs

India’s defense modernization and railway electrification programs are generating significant demand for specialized frequency conversion equipment used in ground power units, aircraft systems, and electric traction. The defense production value exceeded INR 1.27 lakh crore in FY 2023–24, while Indian Railways has electrified over 99.2% of its broad-gauge network by November 2025. In January 2025, Alstom was awarded a €144 million contract to supply traction components including converters, for 17 Vande Bharat Sleeper trainsets for Indian Railways’ Integral Coach Factory in Chennai.

Market Outlook 2026-2034:

The India frequency converter market is poised for sustained growth over the forecast period, driven by the convergence of renewable energy expansion, industrial automation adoption, and infrastructure modernization across multiple sectors. Continued government investments in power grid upgrades, the expansion of defense manufacturing under the Atmanirbhar Bharat initiative, and the development of high-speed rail corridors are expected to create sustained demand for advanced frequency conversion solutions. The market generated a revenue of USD 1,172.83 Million in 2025 and is projected to reach a revenue of USD 2,416.09 Million by 2034, growing at a compound annual growth rate of 8.36% from 2026-2034.

India Frequency Converter Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Type |

Static Frequency Converter |

60% |

|

End Use Industry |

Power and Energy |

33% |

Type Insights:

- Static Frequency Converter

- Rotary Frequency Converter

Static frequency converter dominates with a market share of 60% of the total India frequency converter market in 2025.

Static frequency converters have emerged as the preferred solution across multiple industries due to their superior energy efficiency, compact footprint, and minimal maintenance requirements compared to their rotary counterparts. These converters utilize solid-state power electronics to transform input frequencies without mechanical moving parts, resulting in greater reliability, lower noise levels, and faster response times. Their versatility makes them ideal for applications ranging from aerospace ground power units and defense testing equipment to renewable energy grid integration systems and industrial motor drives.

The growing adoption of silicon carbide and gallium nitride semiconductor technologies is further enhancing the performance and efficiency of static frequency converters. For instance, in December 2025, ABB completed its acquisition of Gamesa Electric’s power electronics business, adding wind converters, battery energy storage systems, and solar inverters to its portfolio, along with approximately 400 employees including key resources in India. This acquisition expanded ABB’s serviceable installed base of wind converters by approximately 46 GW, reinforcing the dominance of static conversion technologies in India’s evolving energy landscape.

End Use Industry Insights:

Access the comprehensive market breakdown Request Sample

- Aerospace and Defense

- Power and Energy

- Oil and Gas

- Traction

- Marine/Offshore

- Process Industry

- Others

Power and energy lead with a share of 33% of the total India frequency converter market in 2025.

The power and energy sector represents the leading end user of frequency converters in India, supported by ongoing grid modernization efforts, renewable energy integration, and expansion of generation infrastructure. Frequency converters play a vital role in aligning variable output from wind and solar installations with the fixed-frequency national grid. They are also widely used to enhance the performance and efficiency of pumps, fans, and compressors in power plants, ensuring stable and optimized operations across energy facilities.

Government-led initiatives aimed at strengthening green energy transmission networks and expanding high-voltage direct current infrastructure are further promoting the adoption of frequency conversion technologies. Large-scale transmission projects designed to transport renewable power across regions highlight the strategic importance of advanced power electronics. Such developments underscore the essential role of frequency and power conversion systems in supporting India’s evolving and increasingly renewable-focused energy framework.

Regional Insights:

- North India

- West and Central India

- South India

- East India

Growth in North India is supported by expanding industrial corridors, large-scale infrastructure projects, and rising investments in renewable energy installations. Manufacturing clusters, metro rail systems, and commercial developments are increasing demand for variable frequency drives and grid-connected converters. Additionally, modernization of power distribution networks and energy efficiency initiatives across industrial facilities contribute to steady adoption of advanced frequency conversion systems.

West and Central India benefit from strong industrialization, particularly in automotive, chemicals, oil & gas, and heavy engineering sectors. These industries require efficient motor control and power optimization solutions, driving frequency converter demand. The region’s growing renewable energy capacity, along with industrial automation upgrades and smart manufacturing initiatives, further accelerates deployment of advanced power electronics technologies.

South India’s well-established manufacturing base, data centers, and technology parks generate consistent demand for reliable power management systems. Expansion of wind and solar energy projects increases the need for grid-interfacing converters. Additionally, the presence of electronics manufacturing hubs and industrial automation adoption strengthens regional demand for high-performance frequency converters in both industrial and commercial applications.

In East India, industrial development in steel, mining, and power generation sectors fuels the need for robust motor control and energy-efficient conversion systems. Infrastructure modernization and expansion of renewable energy projects further support market growth. As regional industries upgrade legacy equipment and adopt automation technologies, demand for reliable and durable frequency converters continues to rise.

Market Dynamics:

Growth Drivers:

Why is the India Frequency Converter Market Growing?

Massive Renewable Energy Expansion and Grid Modernization

India’s ambitious renewable energy targets are creating unprecedented demand for frequency converters that facilitate the integration of variable-frequency power from wind and solar installations into the national grid. Frequency converters play an essential role in wind turbine generators and grid-connected systems by ensuring stable power output despite variations in input frequency. As India accelerates its transition toward clean energy, the integration of large-scale renewable projects has increased the need for advanced power conversion technologies. Strategic planning by energy authorities to accommodate expanding renewable capacity further reinforces the importance of efficient frequency regulation systems in maintaining grid reliability and operational stability. In 2024, Gujarat contributed 1,250 MW to India’s wind capacity additions, creating substantial demand for power electronic converters and inverters across the state’s expanding renewable energy infrastructure.

Rapid Industrialization and Growing Adoption of Automation Technologies

India’s manufacturing sector is undergoing a transformative shift toward automation and digitalization, driving significant demand for frequency converters used in motor speed control, process optimization, and energy management systems. Variable frequency drives, a key category of frequency converters, enable precise motor speed regulation that reduces energy consumption and extends equipment lifespan. The India industrial automation market size reached USD 8.2 Billion in 2025. Looking forward, IMARC Group expects the market to reach USD 16.7 Billion by 2034, exhibiting a growth rate (CAGR) of 8.17% during 2026-2034, reflecting strong adoption of automation solutions. For instance, in September 2024, the Government of Maharashtra approved an investment of INR 83,947 crore (approximately USD 10 billion) for a semiconductor fabrication plant joint venture between Tower Semiconductor and the Adani Group in Panvel, underscoring the scale of India’s industrial modernization that drives demand for advanced power electronics including frequency converters.

Defense Modernization and Railway Electrification Programs

Modernization efforts in India’s defense sector and the rapid electrification of its railway network are significantly boosting demand for specialized frequency conversion systems. In defense applications, converters are critical for aircraft ground support equipment, radar installations, communication systems, and precision testing platforms that require stable and controlled frequency output. Simultaneously, the continued expansion of electric rail infrastructure is increasing the need for advanced traction converters and onboard power systems. As high-speed and next-generation trainsets are introduced, reliable power conversion technology becomes essential for efficiency, safety, and performance. Together, these developments are reinforcing the strategic importance of frequency converters across mission-critical transportation and defense environments.

Market Restraints:

What Challenges the India Frequency Converter Market is Facing?

High Initial Investment and Total Cost of Ownership

The high initial investment of the advanced frequency conversion system, especially the high power of static converters based on silicon carbide and gallium nitride technologies, poses a great obstacle to small and medium enterprises. The capital cost involved is discouraging many prospective end users in process industries and smaller manufacturing processes, even though the benefits of such systems in the long term are in terms of energy savings and operational efficiencies.

Dependency on Imported Semiconductor Components

India’s frequency converter market remains significantly dependent on imported semiconductor devices and power electronic components, creating supply chain vulnerabilities and cost pressures. While the government has initiated semiconductor manufacturing through programs like the India Semiconductor Mission, domestic production capabilities for advanced power semiconductors remain limited, affecting lead times and pricing for frequency converter manufacturers.

Technical Complexity in Grid Integration and Standardization

The integration of frequency converters into India’s diverse and evolving power grid infrastructure presents technical challenges, including harmonic distortion, electromagnetic compatibility issues, and the need for compliance with varied regional standards. The absence of unified national standards for power quality and grid interconnection in some applications creates uncertainty for manufacturers and end users.

Competitive Landscape:

The India frequency converter market features a moderately competitive landscape characterized by a mix of established multinational corporations and emerging domestic manufacturers. Key players are differentiating themselves through investments in localized manufacturing, product innovation, and expanded service capabilities. Companies are focusing on developing energy-efficient solutions incorporating advanced wide-bandgap semiconductors, launching application-specific converter designs for renewable energy and traction, and strengthening after-sales service networks. Strategic partnerships between global technology leaders and Indian industrial conglomerates are accelerating technology transfer and localized production, supporting the government’s Atmanirbhar Bharat initiative while enabling companies to capture the growing demand across power, defense, and industrial automation segments.

Recent Developments:

- January 2026: ABB dispatched its first wind power converter in India following the acquisition of Gamesa Electric’s power electronics business in December 2025. The converter was manufactured and shipped from the company’s advanced Nelamangala facility in Bengaluru and delivered to a wind turbine OEM. This milestone marks a significant step in ABB’s expanded renewable energy portfolio and reinforces its strengthened commitment to advancing wind power solutions in India and global markets.

- August 2025: ABB India secured an order worth INR 173.55 crore from Siemens Gamesa Renewable Power, Chennai, for the manufacture and supply of 3.X wind turbine converters and electrical cabinets from its Nelamangala factory.

India Frequency Converter Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Static Frequency Converter, Rotary Frequency Converter |

| End Use Industries Covered | Aerospace and Defense, Power and Energy, Oil and Gas, Traction, Marine/Offshore, Process Industry, Others |

| Region Covered | North India, West and Central India, South India, East India |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Frequency Converter Market Report

The India frequency converter market size was valued at USD 1,172.83 Million in 2025.

The India frequency converter market is expected to grow at a compound annual growth rate of 8.36% from 2026-2034 to reach USD 2,416.09 Million by 2034.

Static frequency converter, holding the largest share of 60% in 2025, dominates the India frequency converter market due to its superior energy efficiency, compact design, lower maintenance needs, and growing adoption across renewable energy, aerospace, and industrial automation applications.

Key factors driving the India frequency converter market include massive renewable energy expansion and grid modernization, rapid industrialization and automation adoption, defense sector modernization, railway electrification programs, and growing offshore oil and gas exploration activities.

Major challenges include high initial investment costs for advanced converter systems, dependency on imported semiconductor components creating supply chain vulnerabilities, technical complexity in grid integration and standardization, and limited domestic manufacturing capabilities for advanced power semiconductors.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)