India Frozen Finger Chips Market Size, Share, Trends and Forecast by End Use and Region, 2026-2034

India Frozen Finger Chips Market Size, Share, Trends & Forecast (2026-2034)

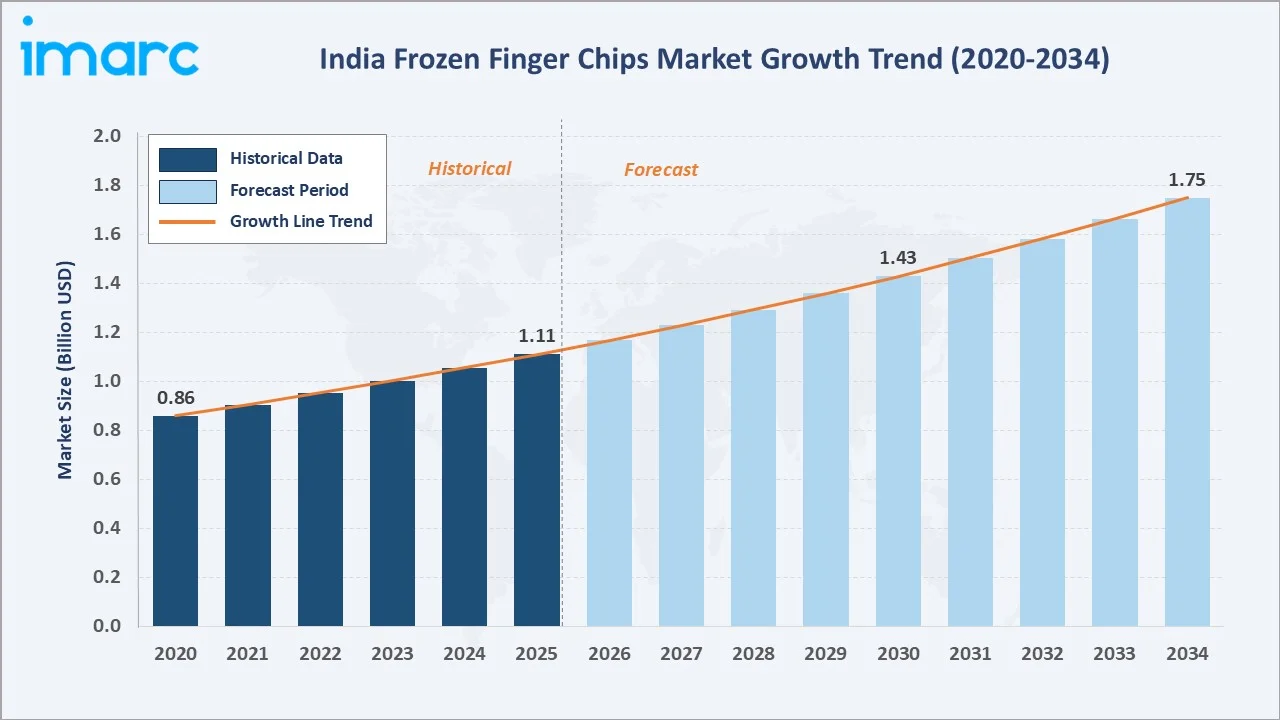

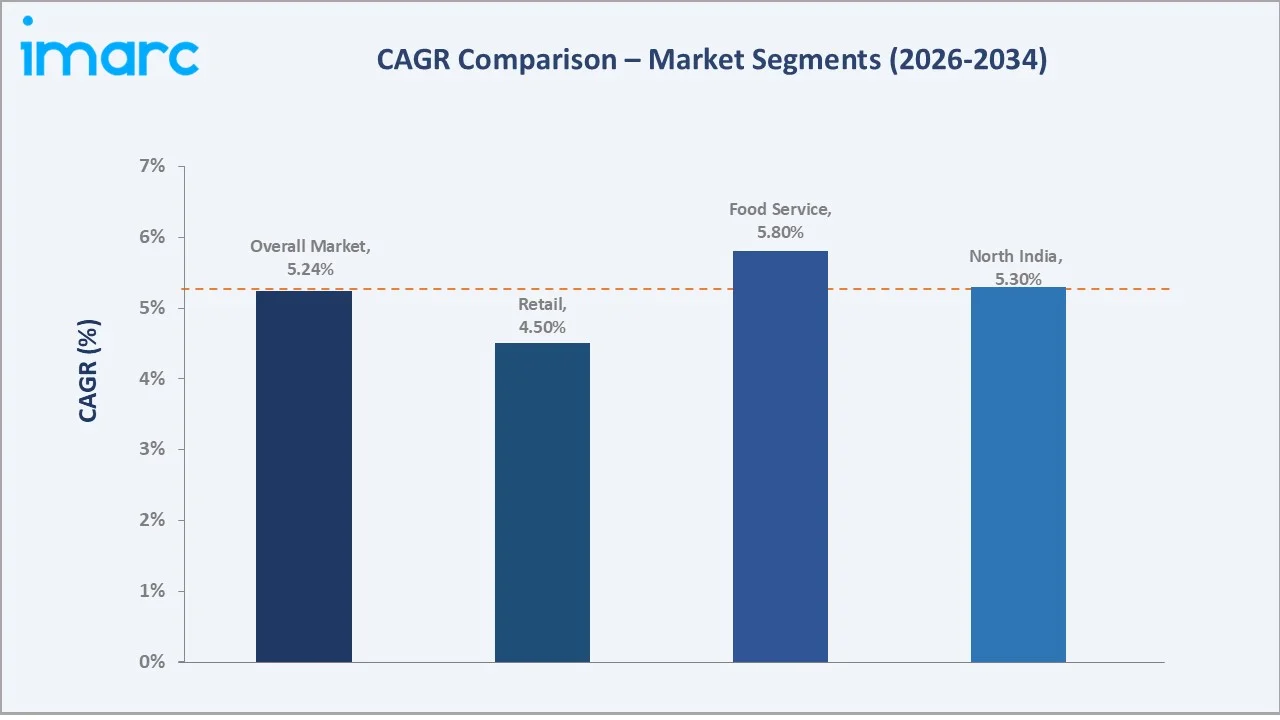

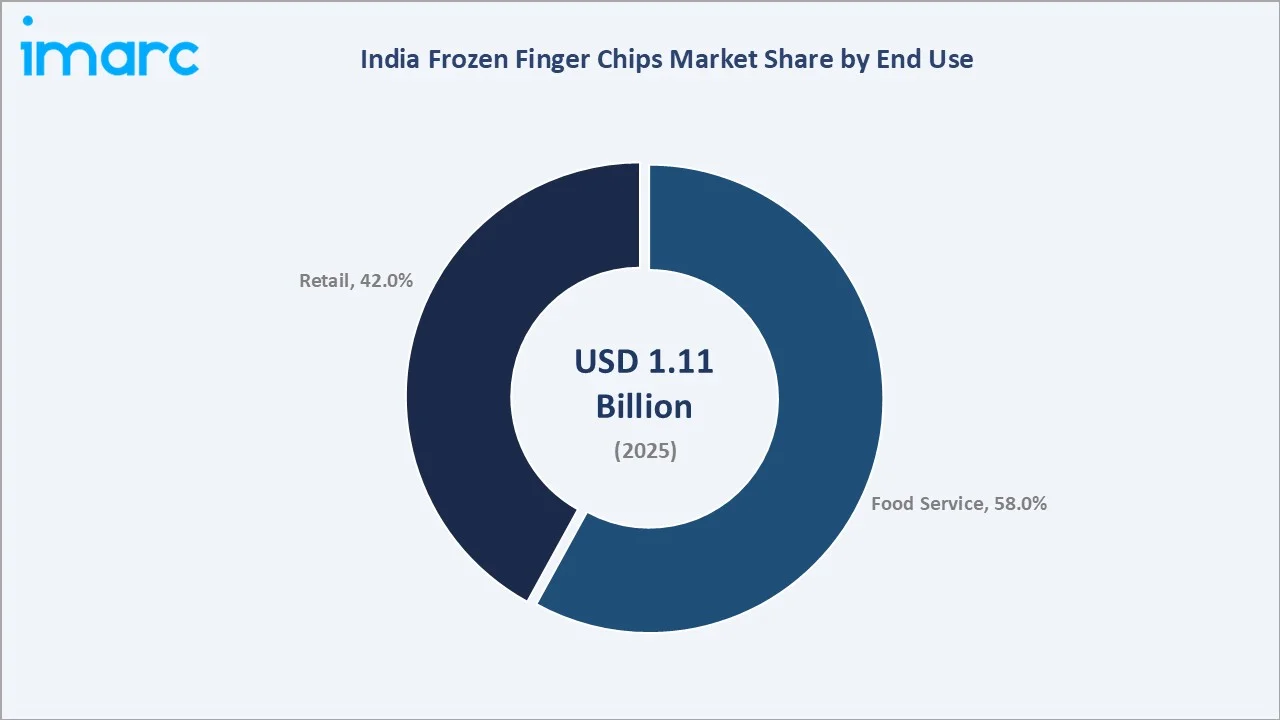

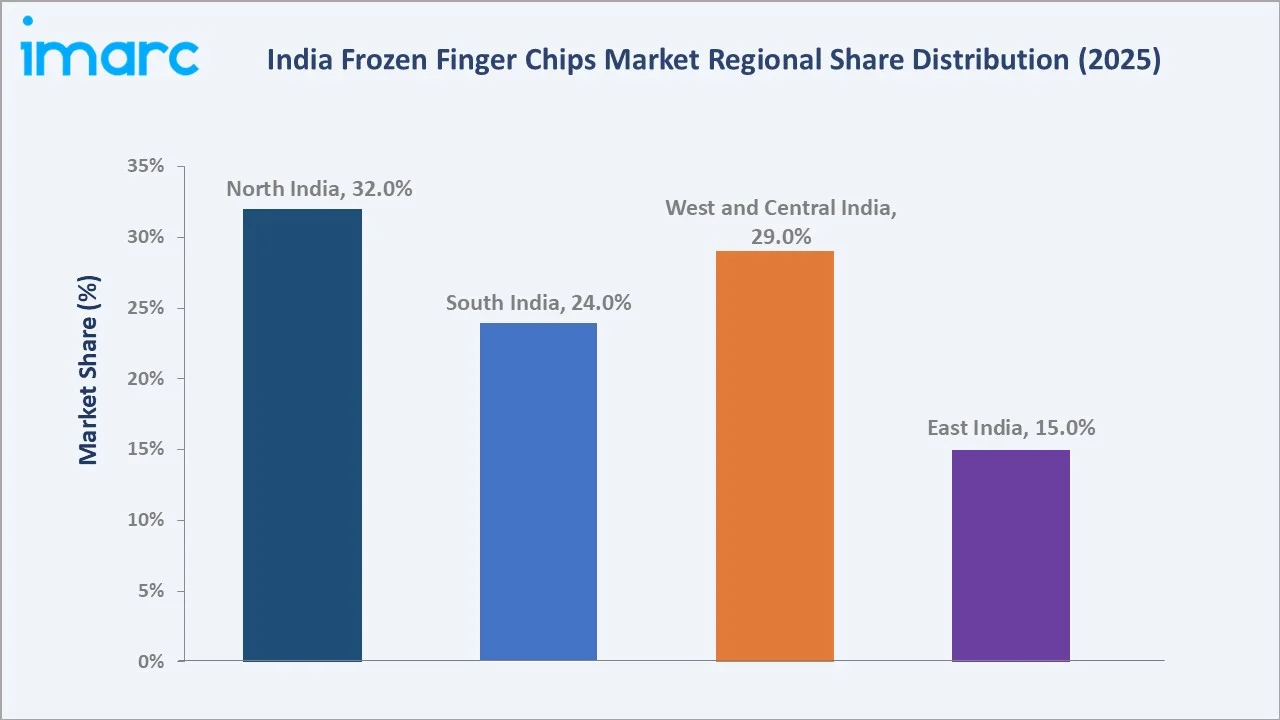

The India frozen finger chips market size was valued at USD 1.11 Billion in 2025 and is projected to reach USD 1.75 Billion by 2034, growing at a compound annual growth rate (CAGR) of 5.24% during 2026-2034. Rapid urbanization, expanding quick-service restaurant (QSR) networks, and growing demand for convenient ready-to-cook snack products are the primary growth drivers. The food service segment dominates with a 58.0% share in 2025, supported by bulk procurement from hotel chains and QSR operators. North India leads regionally at 32.0%, reflecting dense QSR infrastructure and evolving snacking habits among urban consumers.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 1.11 Billion |

|

Forecast Market Size (2034) |

USD 1.75 Billion |

|

CAGR (2026-2034) |

5.24% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant End Use |

Food Service (58.0%, 2025) |

|

Leading Region |

North India (32.0%, 2025) |

The India frozen finger chips market expanded from USD 0.86 Billion in 2020 to USD 1.11 Billion in 2025, anchored at USD 1.43 Billion in 2030, and is forecast to reach USD 1.75 Billion by 2034. The market is commercially distinct, combining a large food service demand base driven by standardized QSR procurement with a rapidly growing retail segment fueled by modern trade expansion and online grocery adoption. In 2023-24, India exported approximately 135,877 tons of frozen French fries valued at INR 1,478.73 Crores, underscoring the domestic processing sector's scale and global competitiveness.

To get more information on this market, Request Sample

The food service segment, commanding 58.0% of the market in 2025, is the primary demand anchor. Cloud kitchen proliferation and online meal delivery aggregator growth have amplified this structural dependency on frozen potato products for foodservice operators seeking operational efficiency. The retail segment, at 42.0%, benefits from expanding organized retail footprints and consumer shift toward frozen convenience foods.

Executive Summary

The India frozen finger chips market at USD 1.11 Billion in 2025 represents one of the most commercially dynamic segments of the country's rapidly evolving processed food industry. The market is commercially distinguished by its dual demand structure, where institutional foodservice procurement from QSR chains, hotels, and cloud kitchens coexists with rapidly growing consumer retail demand through organized supermarkets and e-commerce grocery channels. The market is projected to reach USD 1.75 Billion by 2034 at a 5.24% CAGR.

Food service dominates at 58.0% in 2025. This segment is driven by standardized quality requirements of QSR operators, consistent bulk procurement practices, and the rapid geographic expansion of branded restaurant chains into tier-two and tier-three cities. In 2023, Jubilant FoodWorks announced plans to open 250 new Domino's stores in India with a capital investment of INR 900 Crore, directly amplifying frozen potato product procurement volumes. The retail segment at 42.0% is expanding as cold chain infrastructure improves and consumers increasingly adopt frozen convenience foods for home consumption.

North India leads regionally at 32.0%, supported by the highest QSR outlet density and robust cold chain connectivity. Government initiatives including the Production Linked Incentive (PLI) Scheme for food processing and the Pradhan Mantri Kisan Sampada Yojana are accelerating domestic manufacturing capacity and cold storage infrastructure development, creating a structurally favorable investment environment for frozen food manufacturers through the forecast period.

Key Market Insights

|

Insight |

Data |

|

Dominant End Use |

Food Service - 58.0% share (2025) |

|

Leading Region |

North India - 32.0% market share (2025) |

|

Fastest Growing Region |

East India (~5.6% CAGR, 2026-2034) |

|

Market CAGR |

5.24% (2026-2034) |

|

Market Opportunity |

QSR expansion into Tier-2 cities; cold chain modernization; online food delivery channel growth; healthier frozen snack formulations |

Key Analytical Observations Supporting the Above Data:

- Food Service at 58.0%: The segment's dominance is driven by standardized quality demands of QSR chains and bulk procurement efficiencies. Rapid expansion of international and domestic QSR brands into tier-2 cities is creating new demand pockets for frozen finger chips (2025).

- Retail at 42.0%: Growing organized retail penetration, expanding e-commerce grocery channels, and evolving consumer preference for convenient home meal solutions collectively drive retail segment demand across urban and semi-urban markets.

- North India at 32.0%: The region benefits from the highest QSR outlet concentration, developing cold storage infrastructure, and strong urban consumer adoption of Western-style snacking habits in cities like Delhi-NCR, Chandigarh, and Lucknow.

- East India at 15.0%: The most commercially underpenetrated region with above-average growth potential as improving cold chain networks, rising disposable incomes, and expanding modern retail reach urban consumer segments in Kolkata and Bhubaneswar.

- PLI Scheme Impact: Government support through Production Linked Incentive schemes covering ready-to-cook foods is attracting manufacturing investments, with McCain Foods committing INR 4,000 Crore for a greenfield plant in Madhya Pradesh in July 2025.

- Export Competitiveness: India exported approximately 135,877 tons of frozen French fries valued at INR 1,478.73 Crores in 2023-24, demonstrating domestic processing sector's scale and global cost-competitiveness.

India Frozen Finger Chips Market Overview

The India frozen finger chips market is positioned at the intersection of rapid urbanization, evolving snacking culture, and expanding institutional foodservice demand. Frozen finger chips - primarily potato-based products processed through blanching, frying, and flash-freezing, have transitioned from niche imported specialty products to mainstream consumer and foodservice staples. The product ecosystem spans straight-cut, crinkle-cut, waffle-cut, and specialty formats tailored for distinct consumer and operational requirements.

The market's commercial structure is supported by domestic processing facilities concentrated in Gujarat, Maharashtra, Madhya Pradesh, and Punjab. Cold chain logistics infrastructure - encompassing refrigerated warehousing, temperature-controlled transportation, and last-mile distribution - forms the critical operational backbone enabling market penetration from metropolitan centers to emerging urban clusters. According to the Economic Survey 2023-24, over 40% of India's population will reside in urban areas by 2030, creating structural demand growth for convenient ready-to-cook food products including frozen finger chips.

Market Dynamics

To evaluate market opportunities, Request Sample

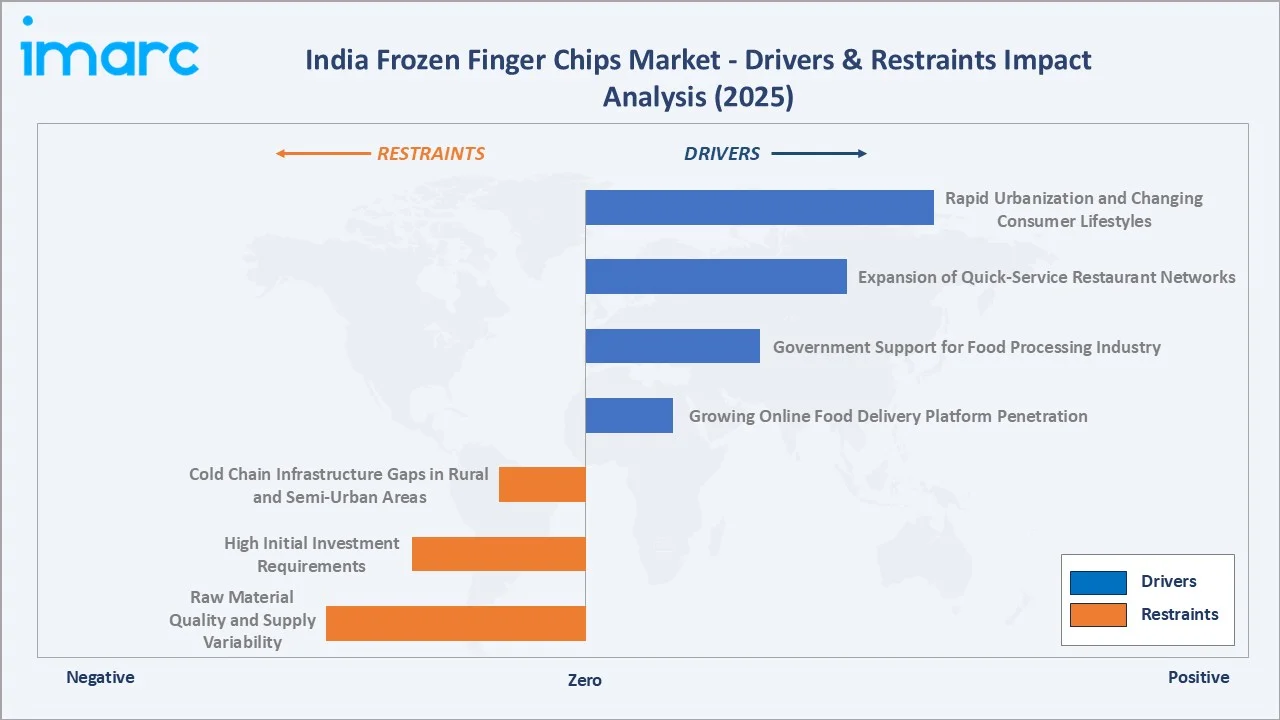

Market Drivers

- Rapid Urbanization and Changing Consumer Lifestyles: India's accelerating urbanization is reshaping food consumption patterns. Over 40% of India's population will live in urban areas by 2030, per the Economic Survey 2023-24. Nuclear families, longer work schedules, and reduced home-cooking time are collectively driving demand for quick-preparation food products. Urban consumers influenced by global food culture increasingly seek branded snacking experiences, positioning frozen finger chips as a primary beneficiary of this lifestyle transition.

- Expansion of Quick-Service Restaurant Networks: The aggressive geographic expansion of QSR chains creates the primary institutional demand channel for frozen finger chips. Jubilant FoodWorks announced plans to open 250 new Domino's stores across India with a capital investment of INR 900 Crore. International and domestic QSR brands are extending into tier-2 and tier-3 cities, creating standardized bulk procurement requirements that favor established frozen potato processors. In May 2025, Devyani International Ltd. launched the first New York Fries outlet in India at Mumbai Airport, signaling further premium snack format expansion.

- Government Support for Food Processing Industry: The Production Linked Incentive (PLI) Scheme for food processing, covering ready-to-cook and ready-to-eat products including frozen finger chips, provides financial incentives to domestic manufacturers. The Pradhan Mantri Kisan Sampada Yojana specifically targets cold chain infrastructure development. In July 2025, McCain Foods announced its largest-ever India investment, INR 4,000 Crore for a greenfield plant in Madhya Pradesh, partially facilitated by the favorable policy environment.

- Growing Online Food Delivery Platform Penetration: Online food delivery aggregators are amplifying foodservice demand by enabling QSR brands and cloud kitchens to serve broader consumer segments. Cloud kitchen operations specifically benefit from frozen finger chips for menu flexibility without significant incremental infrastructure. The exponential growth of app-based food ordering has created consistent incremental demand that supplements traditional dine-in procurement volumes.

Market Restraints

- Cold Chain Infrastructure Gaps in Rural and Semi-Urban Areas: Despite ongoing development, inadequate cold storage and refrigerated transportation in rural and tier-3 markets limits product accessibility. Insufficient cold chain connectivity results in quality degradation, higher wastage rates, and constrained market penetration beyond established urban centers.

- High Initial Investment Requirements: Establishing frozen finger chips processing facilities requires substantial capital investment in processing equipment, blast-freezing systems, cold storage, and specialized distribution infrastructure. High energy costs for continuous refrigeration and the capital intensity of scaling operations create significant barriers for small and mid-sized domestic manufacturers.

- Raw Material Quality and Supply Variability: Processing-grade potato varieties with high dry matter content (required for optimal texture and yield in frozen products) face limited large-scale cultivation in India. Seasonal variability, erratic monsoon patterns, and climate-related crop stress create supply chain uncertainties for manufacturers reliant on consistent high-quality potato raw material.

Market Opportunities

- Tier-2 City QSR Expansion and Retail Modernization: The rapid expansion of QSR chains into tier-2 and tier-3 cities presents the most commercially significant near-term opportunity. Each new QSR outlet creates recurring standardized procurement demand. Simultaneously, organized retail expansion in these markets is creating new consumer touchpoints for frozen finger chips retail SKUs.

- Online Grocery and E-Commerce Channel Growth: The exponential growth of online grocery platforms is creating a new high-growth distribution channel for frozen food products. Digital grocery penetration enables brands to reach consumers beyond physical retail footprints, with efficient direct delivery expanding the addressable consumer base for frozen finger chips retail products.

Market Challenges

- Intense Price Competition from Unorganized Sector: Unorganized local fresh potato snack vendors and informal food stalls compete on price with frozen finger chips, particularly in price-sensitive semi-urban and rural markets where cold chain infrastructure remains underdeveloped. Maintaining competitive price positioning while sustaining product quality and cold chain integrity presents ongoing operational challenges.

- Energy Cost Pressures for Cold Storage Operations: Continuous refrigeration requirements for frozen food processing, storage, and distribution create significant energy cost exposure. Fluctuating electricity tariffs and reliance on diesel backup power in areas with unreliable grid supply pressure operating margins for manufacturers and logistics providers throughout the frozen food supply chain.

Emerging Market Trends

1. Premium and Specialty Finger Chip Formats Creating Differentiated Value

The market is witnessing growing demand for premium and specialty frozen finger chip formats including waffle cuts, steak cuts, seasoned varieties, and loaded fries. Consumer willingness to pay premiums for differentiated snacking experiences is enabling manufacturers and QSR operators to improve per-unit revenue. Devyani International's New York Fries launch at Mumbai Airport in May 2025 exemplifies the premium format trend in the India frozen finger chips market growth trajectory.

2. Cold Chain Infrastructure Development Unlocking New Geographies

Accelerating cold chain development, with DP World inaugurating a 110,000 sq. ft. temperature-controlled warehouse in Navi Mumbai in May 2025, is enabling systematic geographic expansion of frozen finger chip distribution into tier-2 and tier-3 markets. This infrastructure development trend is structurally expanding the addressable market beyond established metropolitan centers, creating new revenue pools for manufacturers.

3. Healthier Frozen Snack Formulations Attracting Health-Conscious Consumers

Health-conscious consumer segments are driving demand for reduced-fat, air-fried compatible, baked, and fortified frozen finger chip variants. Manufacturers are investing in reformulation efforts and new product development to capture the growing wellness-focused snacking sub-segment within the broader frozen potato category.

4. Contract Farming and Farm-to-Factory Integration

Leading manufacturers are investing in structured contract farming programs to secure consistent supply of processing-grade potato varieties. These programs improve raw material quality, reduce supply chain uncertainty, and provide farmers with technical support for adopting high-yield processing-grade varieties, creating a more stable and quality-assured raw material pipeline.

5. E-Commerce and Direct-to-Consumer Retail Adoption

Online grocery platforms are becoming increasingly important distribution channels for branded frozen finger chip products. Digital retail enables manufacturers to reach consumers in geographies underserved by organized physical retail, while providing real-time demand data that supports inventory management and production planning efficiency improvements.

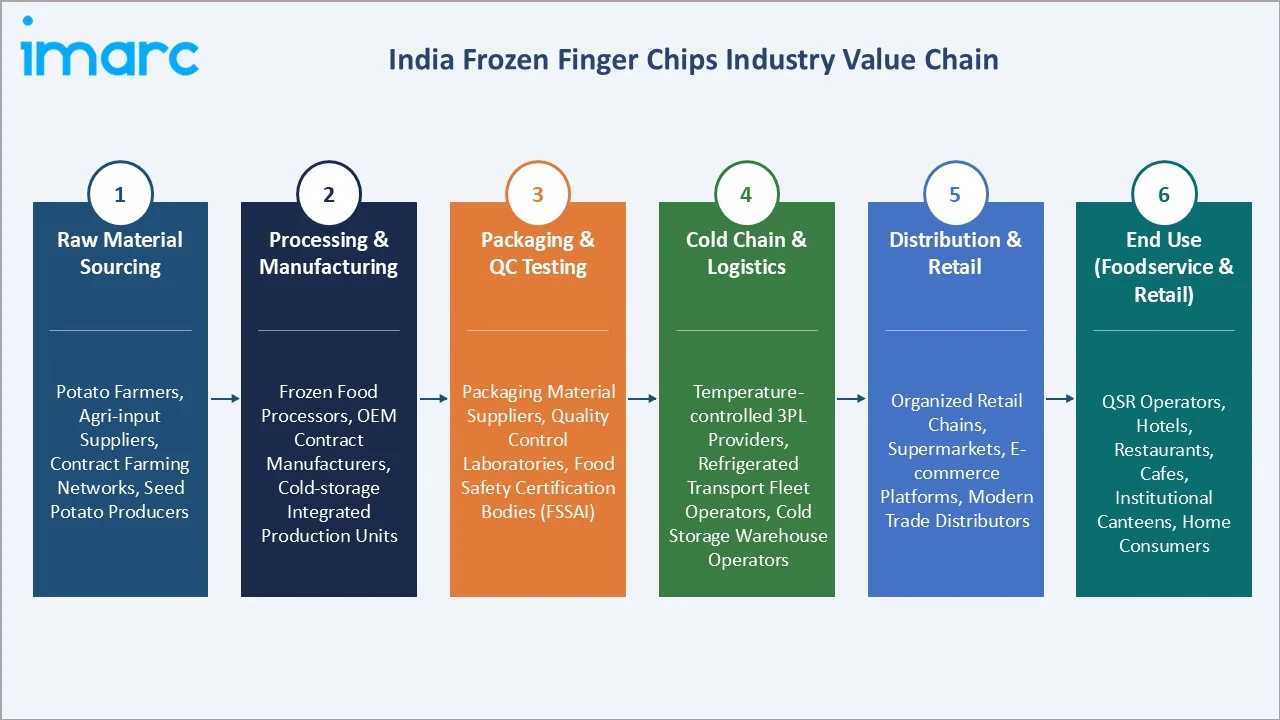

Industry Value Chain Analysis

The India frozen finger chips value chain integrates agricultural inputs, processing operations, cold chain logistics, and multi-channel distribution. The chain's commercial structure creates a distinct market dynamic where domestic value addition and processing capabilities increasingly compete on quality and price with imported frozen potato products.

|

Stage |

Key Participants |

|

Raw Material Sourcing |

Potato farmers, agri-input suppliers, contract farming networks, seed potato producers |

|

Processing & Manufacturing |

Frozen food processors, OEM contract manufacturers, cold-storage integrated production units |

|

Packaging & QC Testing |

Packaging material suppliers, quality control laboratories, food safety certification bodies (FSSAI) |

|

Cold Chain & Logistics |

Temperature-controlled 3PL providers, refrigerated transport fleet operators, cold storage warehouse operators |

|

Distribution & Retail |

Organized retail chains, supermarkets, e-commerce platforms, modern trade distributors |

|

End Use (Foodservice & Retail) |

QSR operators, hotels, restaurants, cafes, institutional canteens, home consumers |

The processing and manufacturing stage is commercially the most capital-intensive, requiring integrated blast-freezing facilities, food-grade water treatment systems, and FSSAI-compliant quality controls. Cold chain logistics - spanning refrigerated warehousing and temperature-controlled transportation - represents the most operationally critical stage, where infrastructure gaps directly constrain market penetration geography.

Technology Landscape in the India Frozen Finger Chips Industry

Processing and Freezing Technologies

Individual Quick Freezing (IQF) technology represents the standard for modern frozen finger chips production, enabling rapid freezing of individual pieces to preserve texture, color, and nutritional quality. Advanced IQF systems with tunnel-belt and spiral configurations are deployed at large-scale facilities. McCain Foods' INR 4,000 Crore greenfield investment in Madhya Pradesh will incorporate state-of-the-art processing automation including computer-vision-based quality sorting systems.

Cold Chain Automation and Monitoring

IoT-enabled temperature monitoring systems and automated cold storage management platforms are transforming cold chain reliability. Real-time temperature tracking across storage and transportation ensures product integrity. Cloud-based supply chain visibility platforms enable manufacturers to monitor product conditions from production to point-of-sale, reducing rejection rates and improving distribution efficiency.

Product Innovation and Reformulation

Manufacturers are investing in food science-driven reformulation to develop lower-fat, lower-acrylamide, and high-fiber frozen finger chip variants. Air-fry optimized formulations with modified surface coatings achieve the crispy texture of oil-fried products with significantly reduced fat absorption, addressing health-conscious consumer preferences without compromising sensory appeal.

Sustainable Packaging and Water-Efficient Processing

Environmental sustainability is emerging as a technology investment priority. Manufacturers are developing recyclable and compostable packaging materials for frozen food products. Water recycling systems in potato processing facilities significantly reduce freshwater consumption per ton of output. Energy-efficient refrigeration technologies including ammonia-based systems and solar-assisted cold storage are gaining adoption among sustainability-focused processors.

Market Segmentation Analysis

The report covers the following market segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

End Use |

Food Service |

58.0% |

2025 |

|

Region |

North India |

32.0% |

2025 |

By End Use

Food service leads at 58.0% in 2025. The food service segment encompasses QSR chains, hotels, restaurants, cafes, institutional canteens, and cloud kitchen operators. These entities prefer frozen finger chips for their consistent quality, extended shelf life, ease of preparation, and operational efficiencies in high-volume environments. The Indian QSR market is projected to grow at a CAGR of 7.00% during 2025-2033, directly sustaining frozen potato product demand.

To access detailed market analysis, Request Sample

The retail segment at 42.0% benefits from expanding organized retail infrastructure, growing consumer familiarity with frozen food products, and improving home refrigeration penetration. Online grocery platforms are creating new distribution pathways for branded retail frozen finger chip products, accelerating segment growth in markets where physical organized retail is still developing.

Regional Market Insights

|

Region |

Share (2025) |

Key Market Drivers & Characteristics |

|

North India |

32.0% |

High concentration of QSR outlets, expanding mall culture, and robust cold chain connectivity support strong demand. |

|

West & Central India |

29.0% |

Strong food processing manufacturing base and growing organized retail networks drive broad market penetration. |

|

South India |

24.0% |

Rising urban middle class, expanding QSR footprint, and tech-savvy consumer base drive adoption of convenient frozen food products. |

|

East India |

15.0% |

Underpenetrated region with high growth potential; increasing urbanization and improving cold chain infrastructure fuel demand expansion. |

North India's 32.0% market leadership reflects Delhi-NCR's high QSR outlet density, strong cold chain connectivity linking processing hubs to end markets, and above-average urban consumer spending on branded food products. West & Central India's 29.0% is commercially anchored by Mumbai's large institutional foodservice market and Gujarat's proximity to processing facilities.

South India's 24.0% reflects Bengaluru's IT sector workforce driving QSR demand and Chennai's growing organized retail infrastructure. East India's 15.0% is the most commercially underdeveloped region, but growing above the overall market CAGR as Kolkata's organized retail expansion, increasing disposable incomes in Odisha, and infrastructure improvements in northeastern states create first-generation frozen food consumer demand from a comparatively lower base.

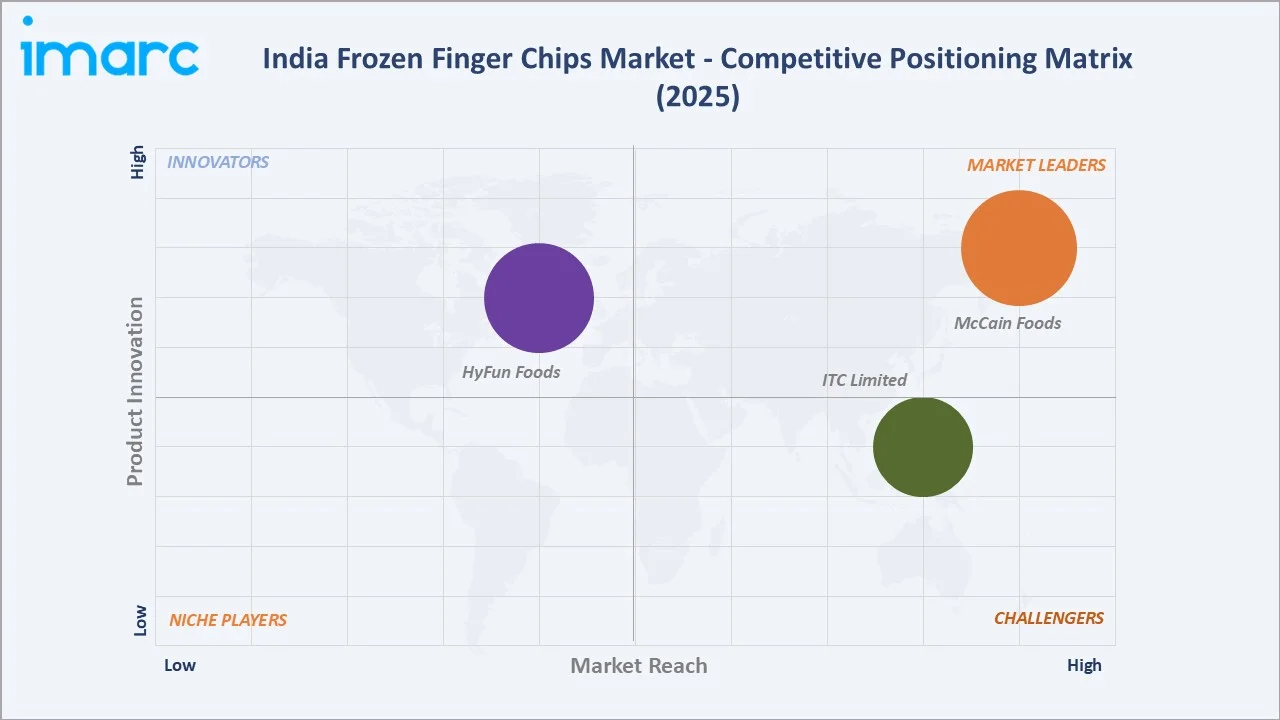

Competitive Landscape

The India frozen finger chips market exhibits moderate concentration, with McCain Foods commanding the dominant branded position through processing scale, QSR partnership depth, and brand equity. ITC Limited and Hindustan Unilever Ltd. are strong challengers leveraging extensive pan-India distribution networks and established consumer brand relationships. Competition is intensifying through capacity expansion, product innovation, and cold chain network investments.

|

Company |

Key Brands |

Market Position |

Core Strength |

|

McCain Foods |

McCain |

Market Leader |

Highly localized product portfolio, robust end-to-end supply chain, and strong B2B partnerships |

|

ITC Limited |

ITC Master Chef |

Strong Challenger |

Extensive distribution network and strong brand equity; leverages multi-category food platform. |

|

HyFun Foods |

HyFun |

Innovator |

Integrated system that combines scale with quality, traceability and sustainability |

The competitive landscape is evolving through two primary dynamics: the continued capacity expansion by established multinational processors deepening their processing scale advantages, and the emergence of organized domestic manufacturers investing in modern facilities supported by government PLI incentives. Distribution network strength - particularly the ability to serve tier-2 city QSR operators with consistent temperature-controlled supply - is emerging as the most commercially critical competitive differentiator.

Key Company Profiles

McCain Foods

McCain Foods, which operates McCain Foods (India) Pvt. Ltd., is the country's leading branded frozen potato processor and a dominant force in the India frozen finger chips market. The company supplies to all major QSR chains operating in India and maintains a strong branded retail presence through organized trade channels.

- Key Products: Straight-cut fries, waffle fries, crinkle-cut fries, and others.

- Recent Developments: In July 2025, McCain Foods announced its largest-ever India investment, a INR 4,000 Crore processing facility in Madhya Pradesh, significantly expanding domestic production capacity for French fries and expanding its product portfolio.

- Strategic Focus: Deepening QSR chain partnerships, expanding retail distribution in tier-2 markets, and investing in contract farming programs for processing-grade potato supply security.

ITC Limited

ITC Limited is a diversified conglomerate with a significant and growing presence in the India frozen finger chips market through its food processing division. The company leverages its extensive pan-India distribution network and strong agri-business capabilities to compete effectively in both foodservice and retail channels.

- Key Products: Crispy fries, piri piri fries, crinkle fries, and others.

- Recent Developments: In May 2026, ITC celebrated the “Journey of the Potato!” on the International Day of Potato. The company highlighted its Technico Agri Sciences, where scientists develop and nurture high vigor seed potatoes TECHNITUBER.

- Strategic Focus: Leveraging ITC's integrated agri-business for raw material procurement advantages and using its multi-category FMCG distribution network to drive frozen food retail penetration across urban and semi-urban markets.

Market Concentration Analysis

The India frozen finger chips market is moderately concentrated in the branded organized segment, with McCain Foods commanding an estimated 35-40% share of the organized branded market by value. The top players - McCain Foods, ITC Limited, and HyFun Foods - collectively account for approximately 60-65% of the organized market.

Market concentration dynamics are evolving through two opposing forces: the continued brand and distribution scale advantages of multinational processors deepening their market share in urban QSR supply, and the fragmentation created by domestic mid-sized processors supported by PLI incentives who are expanding capacity and competing in price-sensitive tier-2 markets and the retail segment. The unorganized sector, comprising local fresh-cut potato vendors and artisanal processors, maintains a structural presence, particularly in markets with underdeveloped cold chain infrastructure.

Investment & Growth Opportunities

Highest Growth Segments

The food service segment at 58.0% market share (2025) with an estimated CAGR of ~5.8% through QSR chain expansion represents the primary institutional demand investment opportunity. The East India region, growing above the 5.24% overall CAGR from a 15.0% base, represents the most commercially underpenetrated high-potential geographic opportunity. Online grocery retail distribution is expanding at an estimated 15-20% CAGR, creating a fast-growing channel opportunity for branded frozen finger chip manufacturers.

Emerging Investment Themes

Cold chain infrastructure investment in tier-2 and tier-3 city distribution networks represents the most commercially enabling investment for unlocking underpenetrated markets. Processing-grade potato contract farming programs in Gujarat, Madhya Pradesh, and Punjab create supply chain security investments with direct margin improvement benefits. PLI Scheme-supported greenfield processing facility investments offer government-incentivized capacity expansion opportunities.

Venture and Strategic Investment Priorities

- Tier-2 City Cold Storage Network Expansion: Investing in temperature-controlled warehouse capacity in Jaipur, Lucknow, Coimbatore, and Bhubaneswar unlocks direct access to fast-growing QSR markets and organized retail penetration in underserved geographies.

- Processing-Grade Potato Agri-Investment: Contract farming partnerships and agri-input financing for processing-grade potato varieties in established potato-growing districts create raw material supply security with cost structure advantages.

- Premium and Specialty Frozen Snack Formats: Investment in waffle-cut, loaded fries, and health-positioned low-fat variants target premium consumer segments willing to pay above-average prices, improving per-unit revenue and brand positioning.

- E-Commerce Frozen Food Platform Investment: Digital-first brands and e-commerce-optimized cold packaging solutions targeting online grocery consumers represent the highest-growth emerging distribution channel in the frozen finger chips retail segment.

Future Market Outlook (2026-2034)

The India frozen finger chips market is projected to grow from USD 1.11 Billion in 2025 to USD 1.75 Billion by 2034, delivering a 5.24% CAGR over the forecast period. The market's anchor value of USD 1.43 Billion in 2030 reflects a structural mid-point where QSR geographic expansion into tier-2 cities reaches critical mass and the retail segment matures in organized trade penetration.

Three structural forces define market growth through 2034: India's urbanization trajectory creating an expanding urban consumer base with higher disposable incomes and greater inclination toward convenient ready-to-cook snack products; the continued QSR chain expansion into geographically underserved tier-2 and tier-3 markets generating new institutional procurement demand; and the improvement of cold chain infrastructure enabling reliable product distribution from processing hubs to end markets across the country.

McCain Foods' INR 4,000 Crore greenfield manufacturing investment announced in July 2025 and government PLI scheme support are collectively building the processing capacity foundation for a significantly larger domestic market by 2034. Export market growth, with India already exporting INR 1,478.73 Crores of frozen French fries in 2023-24, will provide an additional revenue outlet for domestic processors, reinforcing the commercial viability of large-scale capacity investments through the forecast period.

Research Methodology

Primary Research

Primary research comprised structured interviews with India frozen finger chips industry stakeholders, including processing plant directors, supply chain managers, QSR procurement heads, organized retail category managers, cold chain logistics operators, and food industry analysts. Consumer survey data was collected across North, West & Central, South, and East India, covering food service consumption patterns and retail purchase behavior for frozen snack products.

Secondary Research

Secondary research encompassed India food processing export-import data from the Agricultural and Processed Food Products Export Development Authority (APEDA), company annual reports, FSSAI regulatory publications, Ministry of Food Processing Industries (MoFPI) policy documents, PLI scheme enrollment data, and industry association reports from the Frozen Food Industry Association of India. Over 50 secondary sources were reviewed and cross-referenced.

Forecasting Models

Market revenue forecasts were developed using a demand-side channel aggregation model: food service segment modeled through QSR outlet count growth multiplied by average frozen potato procurement per outlet; retail segment modeled through organized retail store count growth and per-store frozen food category offtake. Both segment models were calibrated against India's official food processing production data and APEDA export statistics to ensure macro-level consistency with government-published data.

India Frozen Finger Chips Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| End Uses Covered | Food Service, Retail |

| Regions Covered | North India, West and Central India, South India, East India |

| Companies Covered | McCain Foods, ITC Limited, HyFun Foods, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Frozen Finger Chips Market Report

The India frozen finger chips market size was valued at USD 1.11 Billion in 2025, driven by rapid urbanization, QSR chain expansion, and growing consumer demand for convenient ready-to-cook snack products across urban and semi-urban markets.

The India frozen finger chips market is expected to grow at a 5.24% CAGR during 2026-2034, reaching USD 1.75 Billion by 2034, sustained by QSR network expansion, improving cold chain infrastructure, and growing retail adoption of frozen convenience foods.

Food service dominates with a 58.0% share in 2025, driven by bulk procurement from QSR chains, cloud kitchens, hotels, and institutional canteens that rely on standardized frozen finger chips for operational efficiency and consistent product quality.

North India leads with a 32.0% share in 2025, supported by the highest QSR outlet concentration, robust cold chain connectivity, and high urban consumer adoption of Western-style snacking in cities like Delhi-NCR, Chandigarh, and Lucknow.

Key drivers include rapid urbanization and changing consumer lifestyles, QSR chain expansion into tier-2 cities, government PLI scheme support for food processing manufacturing, and rising online food delivery platform penetration creating new demand channels.

The India frozen finger chips market is projected to reach approximately USD 1.43 Billion by 2030, with QSR chains achieving significant tier-2 city penetration, organized retail cold chain infrastructure reaching critical mass, and the retail segment maturing across urban markets.

Leading companies include McCain Foods, ITC Limited, and HyFun Foods, among others competing across foodservice supply and organized retail channels.

Major challenges include cold chain infrastructure gaps in rural and semi-urban areas, high capital requirements for processing facility establishment, raw material quality and supply variability for processing-grade potato varieties, and energy cost pressures for continuous refrigeration operations.

Priority investment opportunities include tier-2 city cold storage infrastructure, processing-grade potato contract farming programs, PLI Scheme-supported greenfield processing facilities, premium specialty snack format development, and e-commerce frozen food distribution channel build-out.

The PLI Scheme for ready-to-cook foods including frozen products, Pradhan Mantri Kisan Sampada Yojana for cold chain development, and Make in India manufacturing incentives collectively support domestic processing capacity expansion and cold chain infrastructure investment throughout the supply chain.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade