India Generator Market Size, Share, Trends and Forecast by Fuel Type, Power Rating, Sales Channel, Design, Application, End User, and Region, 2026-2034

India Generator Market Summary:

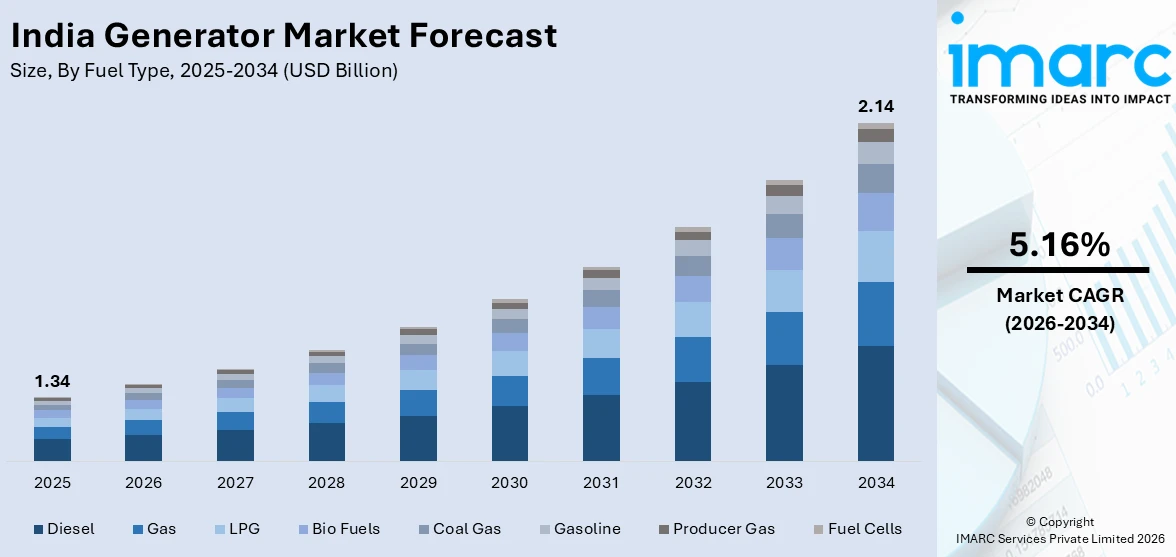

The India generator market size was valued at USD 1.34 Billion in 2025 and is projected to reach USD 2.14 Billion by 2034, growing at a compound annual growth rate of 5.16% from 2026-2034.

The market is driven by persistent electricity supply gaps, rapid industrialization, and escalating demand for uninterrupted power across critical sectors. Surging infrastructure investments under government programs, including smart city development and industrial corridor projects, are expanding the need for reliable standby and prime power solutions. The accelerating growth of data centers, healthcare facilities, and commercial real estate further underscores the indispensable role of generators in India's economic landscape, reinforcing their prominence and contributing to the India generator market share.

Key Takeaways and Insights:

- By Fuel Type: Diesel dominates the market with a share of 73.4% in 2025, driven by its high energy density, widespread fuel availability, cost-effectiveness, and an extensive service network across all end-user verticals.

- By Power Rating: 51–280 Kw leads the market with a share of 31.2% in 2025, owing to its mid-range capacity optimally serves commercial establishments, healthcare facilities, telecom towers, and medium-scale industries requiring dependable backup power.

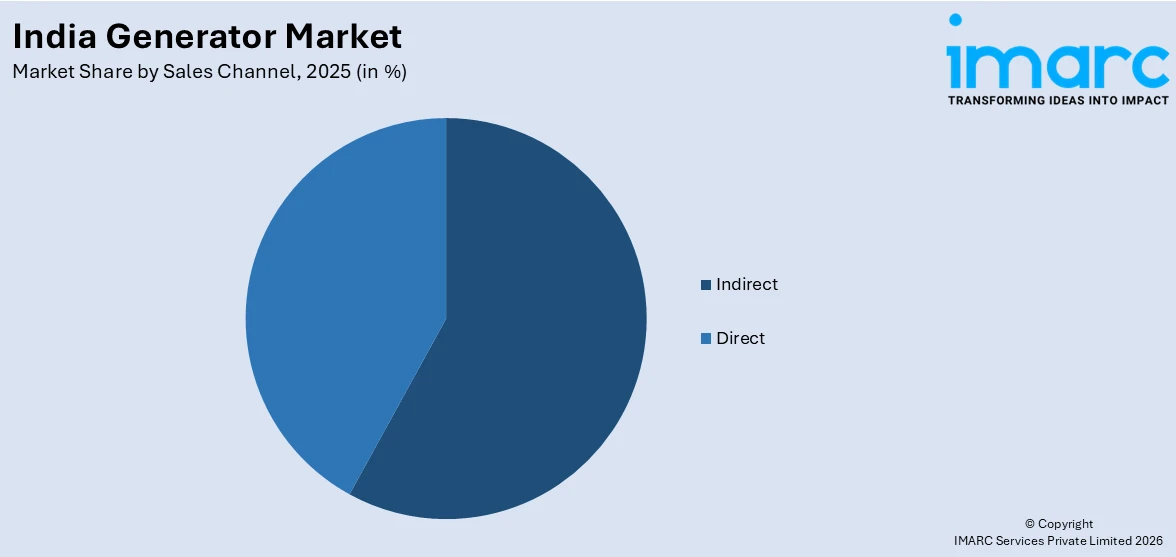

- By Sales Channel: Indirect represents the largest segment with a market share of 58.5% in 2025, driven by extensive dealer networks across Tier II and Tier III cities, enabling broader geographic reach and after-sales support.

- By Design: Stationary dominates the market with a share of 67.5% in 2025, owing to widespread adoption in commercial complexes, data centers, hospitals, and industrial facilities requiring permanently installed, high-capacity backup power solutions.

- By Application: Standby leads the market with a share of 51.8% in 2025, driven by critical emergency backup power needs across hospitals, data centers, and commercial facilities that cannot tolerate interruptions during grid failures.

- By End User: Commercial represents the largest segment with a market share of 34.5% in 2025, owing to by rapid expansion of IT parks, hospitality establishments, healthcare facilities, and data centers demanding highly reliable standby power systems.

- By Region: South India leads the market with a share of 28.5% in 2025, driven concentrated IT corridors, robust manufacturing activity, an expanding data center ecosystem, and higher commercial energy demand across the region's metropolitan hubs.

- Key Players: The India generator market is characterized by a moderately concentrated competitive landscape, with leading domestic and multinational manufacturers competing on technology differentiation, emission compliance, service network depth, and product range spanning portable to large industrial generator sets across fuel types.

To get more information on this market Request Sample

The India generator market is underpinned by a confluence of structural demand drivers spanning residential, commercial, and industrial domains. The persistent gap between electricity supply and demand, particularly in smaller cities and towns where voltage fluctuations remain endemic, continues to position generators as essential capital infrastructure across all economic segments. As per sources, Cummins India stated that approximately 40% of its power generation revenue during the September quarter was driven by demand from data centres, reflecting the sector’s growing reliance on reliable backup power amid digital expansion in the country. The country's accelerated investment in physical infrastructure, encompassing new airport terminals, metro rail corridors, smart industrial cities, and greenfield manufacturing clusters, has structurally elevated the need for reliable on-site power generation during both construction and operational phases. Simultaneously, the mandatory transition to more stringent emission standards has catalyzed a broad-based technology upgrade cycle, driving replacement demand for compliant generator sets across the installed base.

India Generator Market Trends:

Rising Adoption of IoT-Enabled and Smart Generator Systems

The India generator market is witnessing a significant structural shift toward intelligent, connected power systems as commercial and industrial end-users increasingly demand real-time operational visibility. IoT-enabled generators equipped with cloud-connected monitoring dashboards, predictive maintenance algorithms, and remote diagnostics are gaining traction across data centers, hospitals, and large commercial complexes. As per sources, Indian Industrial IoT solutions provider Trinetra TSense announced enhanced remote monitoring for multi‑brand generator sets, offering real‑time data on critical parameters such as fuel level, engine temperature, battery health, and runtime via web and mobile interfaces.

Transition Toward Cleaner Fuels and Hybrid Power Configurations

Growing environmental awareness, mandatory emission compliance requirements, and corporate sustainability commitments are accelerating the transition away from conventional diesel-only generators toward cleaner fuel alternatives and hybrid configurations. Gas-based generators powered by natural gas, LPG, and biogas are gaining considerable interest, particularly in urban areas where expanding city gas distribution networks reduce fuel logistics complexity. In April 2025, Green Power International reported that industries, commercial buildings, and residential societies across India were increasingly choosing gas gensets over diesel units to meet stricter emission norms and achieve operational efficiency, with several societies in Noida switching to gas‑based systems.

Surge in High-Capacity Generator Demand from Digital Infrastructure Expansion

The explosive expansion of data center infrastructure is creating a distinct high-value demand segment for large-capacity, high-reliability generator sets. As hyperscale operators and domestic cloud providers rapidly scale their footprints across the country, the requirement for mission-critical backup power systems capable of sustaining full operational load for extended periods has intensified. In November 2025, Digital Connexion, a joint venture of Reliance Industries, Brookfield, and Digital Realty, announced an $11 billion investment to build a 1 GW AI-native data centre campus in Andhra Pradesh, highlighting the surging demand for robust, redundant power systems in hyperscale facilities. Data centers typically specify redundant generator configurations, multiplying procurement volumes per facility.

Market Outlook 2026-2034:

The India generator market is poised for sustained expansion through the forecast period, supported by structural demand from infrastructure development, digital economy growth, and industrial modernization. The ongoing emission compliance transition continues to drive fleet replacement and technology upgrades across existing installations. Government-backed programs spanning industrial corridor development, smart city initiatives, and national infrastructure pipelines will generate multi-year generator procurement cycles. The proliferation of data centers, coupled with healthcare infrastructure expansion and rising commercial real estate activity, will sustain robust revenue growth across the forecast period. The market generated a revenue of USD 1.34 Billion in 2025 and is projected to reach a revenue of USD 2.14 Billion by 2034, growing at a compound annual growth rate of 5.16% from 2026-2034.

India Generator Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

|

Fuel Type |

Diesel |

73.4% |

|

Power Rating |

51–280 Kw |

31.2% |

|

Sales Channel |

Indirect |

58.5% |

|

Design |

Stationary |

67.5% |

|

Application |

Standby |

51.8% |

|

End User |

Commercial |

34.5% |

|

Region |

South India |

28.5% |

Fuel Type Insights:

- Diesel

- Gas

- LPG

- Bio Fuels

- Coal Gas

- Gasoline

- Producer Gas

- Fuel Cells

Diesel dominates with a market share of 73.4% of the total India generator market in 2025.

Diesel maintains an overwhelming dominance in India's generator market, owing to a combination of factors deeply embedded in the country's power infrastructure landscape. Diesel's high energy density, ready availability through an extensive retail fuel network spanning urban to rural geographies, established maintenance ecosystems, and proven performance across extreme climatic conditions collectively sustain its primacy. As per sources, Mahindra Powerol was recognised as India’s diesel genset manufacturer by volume, securing a 23.8% share of the diesel generator market and helping to drive cumulative industry sales of over 1,51,634 units.

The transition to more stringent emission standards has further driven a replacement wave, as operators upgrade aging generator sets to meet mandatory compliance requirements. New compliant models incorporate advanced electronic fuel injection systems, selective catalytic reduction, and diesel particulate filters, delivering substantially improved emission profiles without compromising performance. These technological advancements have reinforced diesel's competitive position, ensuring it remains the dominant fuel choice across all end-user segments while progressively addressing environmental concerns that had previously challenged its long-term market standing.

Power Rating Insights:

- Up To 50 Kw

- 51–280 Kw

- 281–500 Kw

- 501–2,000 Kw

- 2,001–3,500 Kw

- Above 3,500 Kw

51–280 Kw leads with a share of 31.2% of the total India generator market in 2025.

The 51–280 Kw commands the largest share of the Indian generator market, reflecting its alignment with the capacity requirements of the country's dominant demand segments. Commercial establishments, including hospitals, hotels, educational institutions, mid-scale manufacturing units, and telecom base stations, typically require generators in this range to meet their operational load profiles without the capital cost or installation complexity of higher-capacity units. The segment's versatility makes it the preferred choice for a wide cross-section of buyers across diverse industry verticals.

India's telecom infrastructure expansion, particularly network densification and rollout in semi-urban corridors, continues to drive steady demand for generators in this capacity band as tower operators require reliable backup power across thousands of sites nationwide. The segment also benefits from growing commercial real estate development in Tier II cities, where mid-range generators represent the optimal balance between operational reliability and investment efficiency. As India's commercial and industrial base continues to expand geographically, this segment is well-positioned to sustain its leading market position through the forecast period.

Sales Channel Insights:

Access the comprehensive market breakdown Request Sample

- Direct

- Indirect

Indirect exhibits a clear dominance with a 58.5% share of the total India generator market in 2025.

Indirect sales channels, encompassing authorized dealers, distributors, system integrators, and channel partners, account for the majority of generator sales in India, reflecting the critical importance of geographic reach, local market knowledge, and after-sales service capabilities. Most of the India's generator demand originates from Tier II and Tier III cities, industrial clusters, and semi-urban regions where manufacturers' direct sales teams cannot efficiently penetrate. Distributor networks provide crucial last-mile connectivity, enabling customers to access product demonstrations, financing options, and locally trusted maintenance support.

For mid-range commercial and residential buyers, the dealer relationship provides assurance on service continuity that is often as important as the product specification itself. Spare parts availability, technician proximity, and flexible payment arrangements offered through indirect channels address the practical concerns of buyers in geographies underserved by manufacturer-owned service infrastructure. As generator demand continues to expand into smaller cities and rural industrial clusters, the indirect channel's structural advantages in geographic coverage and customer relationship management are expected to sustain its dominant position through the forecast period.

Design Insights:

- Stationary

- Portable

Stationary leads with a market share of 67.5% of the total India generator market in 2025.

Stationary dominates the India generator market, underpinned by the large-scale procurement requirements of commercial real estate, data centers, hospitals, government facilities, and industrial plants that require permanently installed power backup systems. These units are typically integrated with automatic transfer switches, fuel storage systems, and building management infrastructure, creating complex installations that demand professional commissioning and ongoing maintenance. The emission compliance transition has particularly benefited the stationary segment, as institutional buyers replace older installed bases with compliant units featuring advanced emission controls and electronic monitoring interfaces.

Large commercial and industrial customers increasingly favor stationary generators with remote monitoring capabilities that allow facility teams to track runtime, fuel levels, and equipment health in real-time. The growing complexity of power backup requirements, particularly in data centers and healthcare facilities operating zero-tolerance uptime mandates, is driving demand for sophisticated stationary configurations with redundant systems and integrated power management platforms. As India's institutional infrastructure continues to expand, stationary generators with advanced technological features are expected to sustain their dominant market position through the forecast period.

Application Insights:

- Standby

- Prime and Continuous

- Peak Shaving

Standby dominates with a market share of 51.8% of the total India generator market in 2025.

Standby represents the core application in India's generator market, serving as emergency backup power systems that activate automatically upon grid failure and deactivate when utility power is restored. This segment encompasses the broadest cross-section of end-users, including residential societies, commercial establishments, hospitals, data centers, and government facilities, all of which deploy generators primarily as insurance against grid interruption. As per sources, King George Hospital in Visakhapatnam installed a 323 kVA mobile generator and expanded its existing backup capacity after a prolonged outage disrupted critical care services, underscoring the essential role of standby gensets in healthcare continuity.

Automatic transfer switch integration, remote monitoring, and extended fuel tank configurations are standard requirements in premium standby installations, reflecting the sophistication of institutional buyer specifications. The segment has benefited disproportionately from the emission compliance upgrade cycle as institutional buyers modernize their backup fleets across the installed base. Rising awareness of operational continuity risks among mid-market commercial buyers is further expanding the addressable standby segment beyond traditionally large institutional purchasers, creating new demand vectors in hospitality, retail, and organized logistics that are expected to sustain segment growth through the forecast period.

End User Insights:

- Utilities/Power Generation

- Oil and Gas

- Chemicals And Petrochemicals

- Mining and Metals

- Manufacturing

- Marine

- Construction

- Others

- Residential

- Commercial

- Healthcare

- It and Telecommunications

- Data Centers

- Others

Commercial leads with a share of 34.5% of the total India generator market in 2025.

The commercial end-user segment encompasses a highly diverse range of establishments, including IT parks, data centers, shopping malls, hotels, hospitals, educational institutions, banking facilities, and commercial office complexes, all of which share an exceptionally low tolerance for power disruption. India's commercial real estate sector has recorded robust expansion, with Grade-A office space additions in major metros, a recovering hospitality sector, and a healthcare infrastructure investment wave driven by government programs and private capital. Data centers represent the most rapidly growing sub-segment, creating outsized demand for high-capacity, redundant generator configurations with round-the-clock maintenance contracts.

The emission compliance transition has triggered a broad-based fleet upgrade across the commercial segment as operators replace legacy generator sets under regulatory and sustainability pressure. Rising corporate ESG commitments are additionally influencing procurement decisions toward cleaner, technology-enabled generator solutions with integrated performance monitoring. As India's services economy continues to expand and commercial infrastructure development extends into tier II and tier III cities, the commercial end-user segment is well-positioned to sustain its leading market position and drive above-average generator demand growth through the forecast period.

Regional Insights:

- North India

- South India

- East India

- West India

South India dominates with a market share of 28.5% of the total India generator market in 2025.

South India's leadership in the generator market is anchored by its disproportionate concentration of technology infrastructure, manufacturing excellence, and commercial activity relative to other regions. The region's IT and ITeS corridors host thousands of technology companies, data centers, and research facilities that collectively require among the highest per-capita backup power density in the country. The emergence of the region as a priority destination for artificial intelligence-optimized data center investment is creating a powerful and sustained demand generator for high-capacity backup power systems across multiple states.

The region's strong manufacturing base in automotive, textiles, and electronics, combined with a growing data center ecosystem and expanding port infrastructure, reinforces broad-based generator demand across industrial and commercial applications. Government-backed industrial corridor development and state-level incentive programs are attracting significant foreign and domestic manufacturing investment into the region, creating new demand nodes for both construction-phase and operational generator deployments. As South India continues to consolidate its position as India's technology and manufacturing powerhouse, its generator market leadership is expected to be sustained through the forecast period.

Market Dynamics:

Growth Drivers:

Why is the India Generator Market Growing?

Expanding Infrastructure Development and Urbanization

India's sustained infrastructure development program represents one of the most powerful structural demand drivers for the generator market. The country's ambitious investment in highways, airports, metro rail corridors, industrial parks, and smart city projects is creating multi-year procurement cycles for construction-phase generator deployments across geographies that are currently infrastructure-deficient. In December 2025, India’s flagship Production Linked Incentive (PLI) schemes across key sectors reported realized investments of approximately ₹02 lakh crore and generated, reflecting strong policy support that is catalysing new manufacturing capacity and allied infrastructure development.

Growing Demand from Healthcare and Critical Public Infrastructure

The rapid expansion of India's healthcare infrastructure, encompassing new hospital construction, diagnostic center proliferation, and government-backed public health facility upgrades, is creating a structurally significant and recurring demand source for reliable generator systems. Healthcare facilities operate with absolute zero tolerance for power interruption, making generator procurement a mandatory capital expenditure rather than a discretionary investment. Educational institutions, government administrative complexes, and emergency service facilities share similar power continuity requirements, collectively forming a stable and growing demand base across Tier II and Tier III cities.

Rising Commercial and Industrial Power Continuity Requirements

India's expanding services economy and industrial modernization are progressively elevating the cost of power interruption for commercial and industrial operators, making generator ownership an economic necessity across a widening range of business categories. Organized retail, hospitality, logistics, cold chain infrastructure, and financial services are sectors where even brief outages translate into significant revenue loss and reputational damage. As per sources, industrial clusters in Noida and Ghaziabad reported frequent power outages up to 7 hours, forcing manufacturers to halt production, incur material waste, and push firms to depend on expensive backup solutions to maintain output.

Market Restraints:

What Challenges the India Generator Market is Facing?

High Capital Costs and Compliance-Driven Price Increases

Increasingly stringent emission standards have elevated generator acquisition costs, with advanced after-treatment systems and electronic controls adding meaningful price premiums to compliant models. For price-sensitive small commercial and residential buyers, these cost increases present a meaningful adoption barrier, potentially driving deferred replacement cycles. Limited access to affordable financing in semi-urban markets further constrains demand realization among economically viable customer segments.

Competition from Renewable Energy and Battery Storage Alternatives

The decline in cost of rooftop solar and battery energy storage systems is progressively eroding generator demand in grid-connected residential and light-commercial segments. As solar-plus-storage solutions become economically competitive with generating total cost of ownership, a structural substitution risk is emerging. Government programs accelerating solar adoption are further compressing the addressable market for generators in certain urban and peri-urban geographies.

Operational Restrictions and Fuel Price Volatility

Diesel price volatility, driven by international crude oil markets and domestic taxation, creates operational cost uncertainty affecting generator utilization decisions among price-sensitive end-users. In certain urban jurisdictions, seasonal operating restrictions, mandatory technical requirements, and time-limited operational permits impose additional compliance burdens and installation complexity. Growing regulatory momentum around urban air quality is expected to intensify emission-related operational restrictions in densely populated commercial and residential zones.

Competitive Landscape:

The India generator market exhibits moderate competitive concentration, with the organized segment led by established domestic manufacturers and multinational corporations competing on emission compliance credentials, product range breadth, service network density, and technological differentiation. The mandatory emission compliance transition has consolidated competitive advantage among manufacturers possessing the engineering capability and capital resources to develop certified after-treatment systems. The competitive landscape is further shaped by growing demand for integrated power solutions combining generators with remote monitoring platforms, hybrid configurations, and renewable energy components, creating meaningful differentiation opportunities for technologically capable competitors while raising entry barriers for smaller regional players.

Recent Developments:

- In December 2025, Kirloskar Oil Engines unveiled India’s first hydrogen-engine genset, along with advanced multi-core power systems and high-power naval engines, focusing on green energy solutions for healthcare, real estate, data centers, and defense, marking a significant pivot toward sustainable and indigenous power technology.

- In March 2024, Recon Technologies Pvt Ltd, the authorised Mahindra Powerol GOEM partner, launched its CPCB IV+ diesel genset range up to 625 kVA in Hyderabad, featuring advanced after-treatment systems, remote monitoring, and emission compliance, aimed at industrial, commercial, and gas genset applications across Telangana and Andhra Pradesh.

India Generator Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Fuel Types Covered | Diesel, Gas, LPG, Bio Fuels, Coal Gas, Gasoline, Producer Gas, Fuel Cells |

| Power Ratings Covered | Up To 50 Kw, 51–280 Kw, 281–500 Kw, 501–2,000 Kw, 2,001–3,500 Kw, Above 3,500 Kw |

| Sales Channels Covered | Direct, Indirect |

| Designs Covered | Stationary, Portable |

| Applications Covered | Standby, Prime and Continuous, Peak Shaving |

| End Users Covered |

|

| Regions Covered | North India, South India, East India, West India |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Generator Market Report

The India generator market size was valued at USD 1.34 Billion in 2025.

The India generator market is expected to grow at a compound annual growth rate of 5.16% from 2026-2034 to reach USD 2.14 Billion by 2034.

Diesel held the largest share in the India generator market, driven by its high energy density, widespread fuel availability, cost-effectiveness over the operational lifecycle, and an extensive service and maintenance network supporting diverse end-user verticals.

Key factors driving the India generator market include persistent electricity supply gaps across urban and rural geographies, rapid expansion of data centers and digital infrastructure, large-scale government infrastructure investment programs, and mandatory emission compliance requirements accelerating fleet replacement cycles nationwide.

Major challenges facing the India generator market include rising product costs from emission compliance requirements, growing competition from renewable energy and battery storage alternatives, diesel price volatility, increasing urban operational restrictions on generator usage, and limited financing accessibility constraining demand in semi-urban markets.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)