India Genetic Testing Market Size, Share, Trends and Forecast by Type, Technology, Application, and Region, 2026-2034

India Genetic Testing Market Summary:

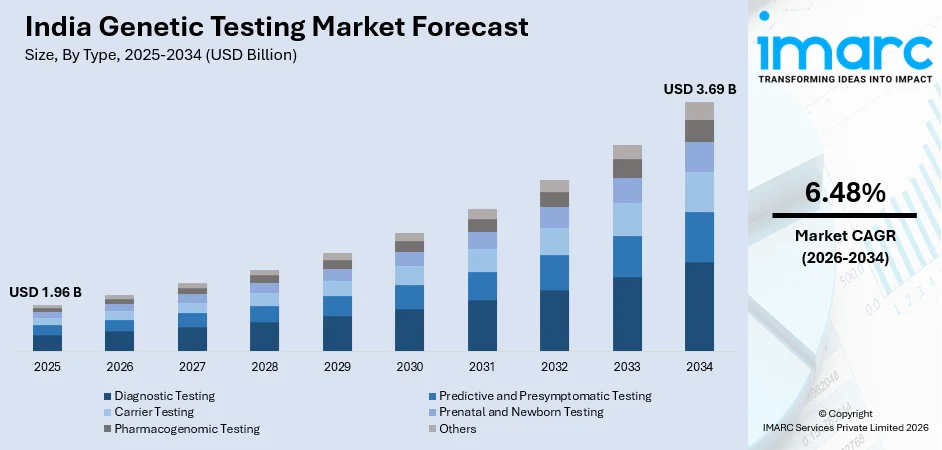

The India genetic testing market size was valued at USD 1.96 Billion in 2025 and is projected to reach USD 3.69 Billion by 2034, growing at a compound annual growth rate of 6.48% from 2026-2034.

The India genetic testing market is experiencing robust growth, fueled by rising awareness of hereditary diseases, growing cancer incidence, and expanding access to advanced molecular diagnostics. Increasing government initiatives promoting genomic research and the widespread adoption of prenatal and newborn screening programs are further stimulating demand. Technological advancements in next-generation sequencing (NGS) and declining test costs are collectively enhancing accessibility and broadening the market share.

Key Takeaways and Insights:

- By Type: Diagnostic testing dominates the market with a share of 60.0% in 2025, owing to its critical role in identifying genetic disorders and hereditary conditions, expanding clinical awareness, and strong physician recommendation rates driving consistent demand across healthcare settings.

- By Technology: Molecular testing leads the market with a share of 45.0% in 2025. This dominance is driven by its superior sensitivity and specificity, ability to detect diverse genetic mutations, and broad clinical applicability spanning oncology, infectious disease, and rare disorder diagnostics.

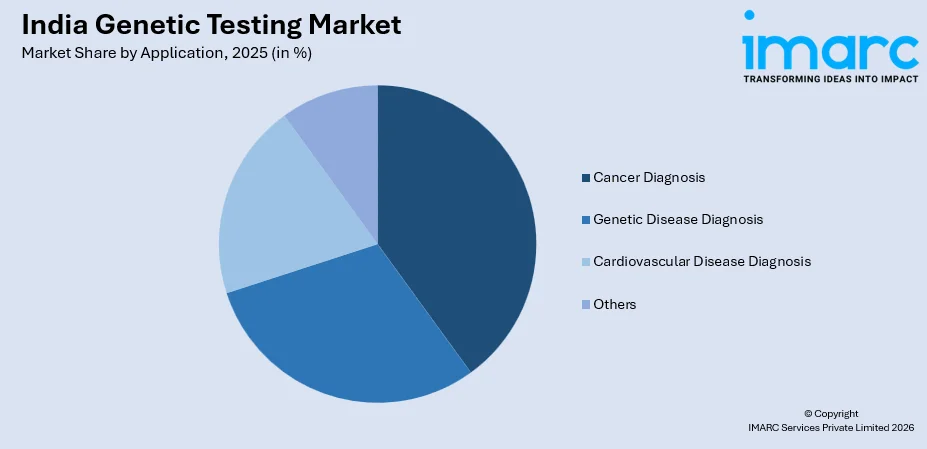

- By Application: Cancer diagnosis represents the largest segment with a market share of 35.0% in 2025, reflecting the rising burden of oncological conditions and growing clinical reliance on genetic profiling for personalized treatment strategies across major hospitals and cancer centers.

- By Region: North India comprises the largest region with 45.0% share in 2025, driven by the concentration of leading tertiary care hospitals and genomic diagnostic centers in Delhi, Chandigarh, and Lucknow, along with high patient footfall and strong physician awareness.

- Key Players: Key players in the India genetic testing market expand their presence by investing in advanced sequencing platforms, broadening test menus, forging hospital partnerships, and enhancing affordability through scalable laboratory networks that extend reach to tier-2 cities and underserved populations across the country.

To get more information on this market Request Sample

The India genetic testing market is positioned at a significant inflection point as the country's healthcare ecosystem undergoes rapid transformation, driven by the broad adoption of genomic medicine. The integration of genetic diagnostics into mainstream clinical practice has accelerated, propelled by increased physician awareness, evolving regulatory frameworks, and the expansion of accredited molecular diagnostic laboratories across urban and semi-urban regions. In February 2026, Genetic Wellness Testing, which was introduced by NuGenomics, an AI-powered wellness startup, was made available for INR 999. Demand is underpinned by the country's high burden of hereditary conditions. Genetic testing has consequently become central to clinical decision-making across oncology, cardiology, and reproductive medicine. The market is also benefiting from strong government support, with national programs targeting genomic surveillance of rare and non-communicable diseases. Infrastructure investments in reference laboratories, combined with rising consumer interest in preventive and personalized healthcare, are reinforcing steady long-term market expansion and continuously diversifying the expanding application base of genetic diagnostics across hospital networks and independent diagnostic centers throughout the country.

India Genetic Testing Market Trends:

Rising Adoption of NGS in Clinical Diagnostics

The widespread adoption of NGS is fundamentally reshaping India's genetic testing landscape. NGS platforms enable comprehensive genomic profiling at a fraction of earlier costs, facilitating simultaneous analysis of thousands of genes in a single test run. This is particularly transformative for rare disease diagnosis and oncology applications, where broad mutation panels are clinically essential. Under the Genome India Project, the Department of Biotechnology completed sequencing of over 10,000 whole genomes from diverse Indian population cohorts, as of February 2024, establishing a national genetic reference database and reinforcing institutional momentum for NGS adoption across the country.

Expansion of Prenatal and Newborn Genetic Screening Programs

Increasing awareness of congenital disorders and government-backed maternal health initiatives are driving rapid expansion of prenatal and newborn genetic screening across India. Cell-free fetal DNA testing and chromosomal microarray analysis are witnessing growing adoption among urban and peri-urban populations seeking early prenatal risk assessment. Improved awareness among expecting parents about early detection of chromosomal abnormalities is further encouraging uptake of advanced prenatal screening methods. Healthcare providers are increasingly recommending non-invasive screening tests as part of routine prenatal care for early risk identification.

Integration of Pharmacogenomics in Personalized Treatment Protocols

The convergence of pharmacogenomics with clinical oncology and cardiology is emerging as a critical trend in India genetic testing market. Healthcare systems are increasingly incorporating genetic testing into drug selection workflows to optimize therapeutic efficacy and minimize adverse reactions. India's premier oncology institutions have begun embedding tumor profiling panels into multidisciplinary treatment protocols for breast, lung, and colorectal cancers. The incidence of breast cancer among Indian women was expected to rise, attaining 5.6 Million DALYs by 2025.

Market Outlook 2026-2034:

The India genetic testing market is set for sustained expansion throughout the forecast period, underpinned by progressive integration of genomics into standard clinical care, growing public and private investment in diagnostic infrastructure, and rising consumer health consciousness. Advancements in artificial intelligence (AI)-driven genomic data interpretation and the proliferation of direct-to-consumer (D2C) testing platforms are poised to unlock new demand segments beyond traditional clinical settings. The market generated a revenue of USD 1.96 Billion in 2025 and is projected to reach a revenue of USD 3.69 Billion by 2034, growing at a compound annual growth rate of 6.48% from 2026-2034. Continued expansion of hospital-based genetic counseling services, government-funded genomic databases, and cross-sector collaborations with academic research institutions are expected to accelerate clinical adoption.

India Genetic Testing Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

|

Type |

Diagnostic Testing |

60.0% |

|

Technology |

Molecular Testing |

45.0% |

|

Application |

Cancer Diagnosis |

35.0% |

|

Region |

North India |

45.0% |

Type Insights:

- Predictive and Presymptomatic Testing

- Carrier Testing

- Prenatal and Newborn Testing

- Diagnostic Testing

- Pharmacogenomic Testing

- Others

Diagnostic testing dominates with a market share of 60.0% of the total India genetic testing market in 2025.

Diagnostic testing serves as the foundational pillar of India's genetic testing ecosystem, including tests intended to confirm or rule out suspected genetic disorders in people who exhibit symptoms. The pressing clinical demand for accurate etiological diagnosis across hospitals, specialty clinics, and reference laboratories is reflected in its significant market domination. The need for precise diagnostic confirmation is increasing due to the rising prevalence of inherited diseases and uncommon genetic abnormalities. Additionally, more accurate and efficient identification of genetic defects is being made possible by advancements in molecular diagnostic tools.

The considerable clinical efficacy of diagnostic testing in managing multigenerational familial health risks, especially in communities with a high proportion of consanguineous marriages, further supports the segment's dominance. Genetic diagnostic panels are being integrated into normal therapeutic pathways for chromosomal syndromes, metabolic illnesses, and neuromuscular disorders. The position of diagnostic testing as the cornerstone of India's genetic testing ecosystem has been reinforced by the increasing availability of comprehensive gene panels and whole-exome sequencing services through accredited laboratories, which offer quicker turnaround times, better interpretive accuracy, and greater clinical utility.

Technology Insights:

- Cytogenetic Testing and Chromosome Analysis

- Biochemical Testing

- Molecular Testing

- DNA Sequencing

- Others

Molecular testing leads with a share of 45.0% of the total India genetic testing market in 2025.

Molecular testing holds dominance in the India genetic testing market, driven by its unmatched ability to analyze DNA and RNA at the molecular level for the detection of inherited mutations and oncological alterations. Polymerase chain reaction (PCR) and NGS-based molecular assays are the most widely deployed platforms across clinical laboratories. The growing need for precise genomic insights in clinical decision-making is further accelerating the adoption of molecular diagnostics across healthcare institutions.

Molecular testing's dominance can also be attributed to its versatility in a wide range of clinical applications, such as somatic mutation detection in tumor tissues, pharmacogenomic profiling, and confirmation of hereditary diseases. Because of the technology's scalability, which ranges from focused single-gene assays to extensive multi-gene panels, laboratories may support both highly specialized clinical testing and standard diagnostic workflows. High-throughput molecular platforms have been gradually added to the infrastructure of healthcare facilities in India's major cities, allowing for quicker reporting cycles, lower test costs, and the clinical flexibility to treat complex multi-system genetic conditions that present in a variety of patient demographics.

Application Insights:

Access the comprehensive market breakdown Request Sample

- Cancer Diagnosis

- Genetic Disease Diagnosis

- Cardiovascular Disease Diagnosis

- Others

Cancer diagnosis exhibits a clear dominance with a 35.0% share of the total India genetic testing market in 2025.

Cancer diagnosis prevails the market, driven by the rapidly growing burden of oncological disease and the clinical imperative for molecular-level tumor characterization to guide targeted therapies. Genetic testing is integral to the standard of care at oncology centers across India's major cities, enabling identification of actionable mutations in BRCA1/2, EGFR, and ALK genes. GLOBOCAN projected that by 2040, cancer cases in India will rise to 2.08 Million, representing a 57.5% increase from 2020, underscoring the expanding demand for oncology-oriented genetic diagnostics.

Beyond initial diagnosis, genetic testing for cancer enables comprehensive risk stratification and surveillance planning for high-risk individuals with familial cancer syndromes. Clinical adoption is accelerating across hereditary breast and ovarian cancer programs, Lynch syndrome screening, and hereditary colorectal cancer protocols, with genetic counseling now embedded in multidisciplinary tumor boards at India's premier oncology institutions. The growing availability of liquid biopsy platforms for non-invasive tumor DNA analysis is further broadening the clinical scope of cancer-related genetic testing, extending access to patients across urban centers and emerging tier-2 cancer care facilities.

Regional Insights:

- North India

- West and Central India

- South India

- East and Northeast India

North India represents the leading region with a 45.0% share of the total India genetic testing market in 2025.

North India enjoys the leading position in the market, anchored by the dense concentration of premier academic medical centers, multi-specialty hospitals, and accredited reference laboratories in Delhi-NCR, Chandigarh, and Lucknow. The region benefits from a highly trained clinical workforce, robust diagnostic infrastructure, and strong patient awareness. The presence of leading medical universities and research institutes further strengthens the region’s capabilities in advanced genetic diagnostics. Additionally, higher healthcare expenditure and better access to specialized medical services are encouraging wider adoption of genetic testing across urban populations.

The region's dominance is further supported by strong institutional linkages between government teaching hospitals, private tertiary centers, and genomic research institutions, enabling seamless referral pathways for complex genetic workups. North India leads in genetic counseling program availability, with several hospitals in Delhi integrating dedicated genetics departments into clinical frameworks. This combination of clinical expertise, institutional capacity, and concentrated patient populations ensures North India's continued leadership across India's rapidly expanding genetic testing landscape.

Market Dynamics:

Growth Drivers:

Why is the India Genetic Testing Market Growing?

Increasing Burden of Genetic Disorders and Hereditary Diseases

India's disproportionately high burden of hereditary diseases represents a fundamental catalyst driving the genetic testing market forward. The country's unique demographic structure, characterized by elevated rates of consanguineous marriages in several regional communities, has resulted in high prevalence of autosomal recessive conditions, including thalassemia, sickle cell disease, hemophilia, and a wide range of lysosomal storage disorders. Compounding this is the rapidly growing elderly population, which is increasingly susceptible to late-onset genetic conditions, such as hereditary cancers, familial cardiomyopathies, and neurodegenerative disorders with strong genetic underpinnings. As per PIB, by 2036, the elderly population in India is expected to rise to approximately 230 Million, accounting for roughly 15% of the overall population. Pediatric healthcare institutions are expanding their genetic diagnostic capabilities to address congenital anomalies, inborn metabolic disorders, and syndromic presentations, where early genetic diagnosis directly informs treatment planning and family counseling. The healthcare system's growing recognition of the critical role of germline and somatic mutations in multi-system diseases has prompted broader integration of genetic testing into multidisciplinary clinical pathways.

Government Initiatives and National Genomic Programs

India's federal and state governments have intensified investments in genomic research and public health genomics as part of a broader national precision medicine agenda. Government-supported programs under the Indian Council of Medical Research and the Department of Biotechnology are directing investment towards genomic data infrastructure, bioinformatics capabilities, and clinical translation platforms. National newborn screening programs, expanded under the National Health Mission, have established standardized protocols for early identification of metabolic and genetic disorders across participating states. Policy frameworks, including rare disease management guidelines, are creating institutional mandates for genetic testing within public health systems. Initiatives to develop Centers of Excellence in genomics at academic institutions are strengthening India's research and clinical capacity, generating trained professionals and validated diagnostic pathways. Collectively, these government-led programs are establishing a policy-driven foundation for the sustained expansion of genetic testing demand across India.

Technological Advancements and Declining Cost of Genetic Testing

Rapid technological innovation has dramatically expanded the clinical accessibility and commercial viability of genetic testing in India. Progressive cost reduction in NGS platforms, driven by advances in sequencing chemistry, informatics software, and reagent efficiency, has brought comprehensive genomic analyses within reach of a substantially larger patient population. Benchtop sequencers and automated genetic analysis platforms have enabled mid-sized diagnostic laboratories to offer previously centralized tests, decentralizing access beyond major metropolitan reference facilities. Integration of AI in genomic data interpretation has significantly reduced the time and expertise required to generate clinically actionable reports, improving laboratory throughput and diagnostic efficiency. Cloud-based genomic databases and AI-powered variant classification tools are enabling smaller regional laboratories to deliver high-quality interpretations consistent with international standards.

Market Restraints:

What Challenges the India Genetic Testing Market is Facing?

Limited Awareness and Genetic Literacy Among the General Population

Despite growing urban awareness, a substantial proportion of India's population remains unfamiliar with the clinical significance and applications of genetic testing. Misconceptions about the implications of genetic diagnoses, concerns about genetic discrimination, and limited understanding of hereditary disease concepts among rural and semi-urban populations constrain proactive uptake. Healthcare provider education gaps also limit the frequency of genetic testing recommendations at primary and secondary care levels, significantly restricting referral volumes and slowing the penetration of genetic diagnostics into broader community health settings.

Shortage of Trained Genetic Counselors and Clinical Geneticists

India faces a critical shortage of qualified genetic counselors and clinical geneticists, constraining the effective delivery and clinical integration of genetic testing services. The limited number of accredited genetic counseling training programs at Indian universities means that demand for trained professionals significantly outpaces supply. This workforce gap reduces the capacity of hospitals to provide pre-test and post-test counseling, particularly in tier-2 cities and public health facilities where genetics expertise is most scarce, undermining comprehensive service delivery.

Regulatory and Ethical Concerns Surrounding Genetic Data

The management and protection of sensitive genetic information present growing regulatory and ethical challenges for the market. Concerns related to data privacy, informed consent, and potential misuse of genetic information can discourage individuals from undergoing testing. In addition, the absence of a fully standardized regulatory framework governing genetic data storage, sharing, and interpretation may create uncertainty among healthcare providers and diagnostic laboratories, slowing the adoption of advanced genetic testing solutions.

Competitive Landscape:

The India genetic testing market is characterized by a moderately fragmented competitive landscape, comprising large national reference laboratory networks, multi-specialty hospital-affiliated diagnostic centers, and a growing number of specialized genomic testing providers. Established laboratory chains leverage pan-India presence and accreditation credentials to capture significant institutional testing volumes, while boutique genomics laboratories compete on specialized offerings and clinical expertise. The market is also witnessing increasing participation from international genomic testing entities entering through partnership arrangements. Competitive strategies center on expansion of test menus, implementation of AI-powered interpretive platforms, and investment in direct-to-physician outreach. Quality accreditation serves as a key differentiator in hospital procurement decisions. Consolidation through mergers and laboratory network expansions is gradually reshaping the competitive hierarchy, with leading players pursuing scale advantages in sequencing infrastructure and bioinformatics capabilities.

India Genetic Testing Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Predictive and Presymptomatic Testing, Carrier Testing, Prenatal and Newborn Testing, Diagnostic Testing, Pharmacogenomic Testing, Others |

| Technologies Covered |

|

| Applications Covered | Cancer Diagnosis, Genetic Disease Diagnosis, Cardiovascular Disease Diagnosis, Others |

| Regions Covered | North India, West and Central India, South India, East and Northeast India |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Genetic Testing Market Research Report and Industry Forecast Report

The India genetic testing market size was valued at USD 1.96 Billion in 2025.

The India genetic testing market is expected to grow at a compound annual growth rate of 6.48% from 2026-2034 to reach USD 3.69 Billion by 2034.

Diagnostic testing dominated the market with a share of 60.0%, driven by its critical role in confirming hereditary conditions, high physician recommendation rates, and growing integration of comprehensive gene panels into multidisciplinary clinical pathways across India's tertiary care hospitals and specialty clinics.

Key factors driving the India genetic testing market include the rising burden of hereditary diseases, strong government investments in genomic research programs, rapid advancements in NGS, and growing integration of genetic diagnostics into oncology, reproductive medicine, and rare disease clinical pathways.

Major challenges include limited genetic literacy among the general population, high costs of advanced genetic tests, insufficient insurance reimbursement coverage, and a shortage of trained genetic counselors and clinical geneticists constraining comprehensive service delivery across India.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)