India Geosynthetics Market Size, Share, Trends and Forecast by Product, Type, Material, Application, and Region, 2026-2034

India Geosynthetics Market Summary:

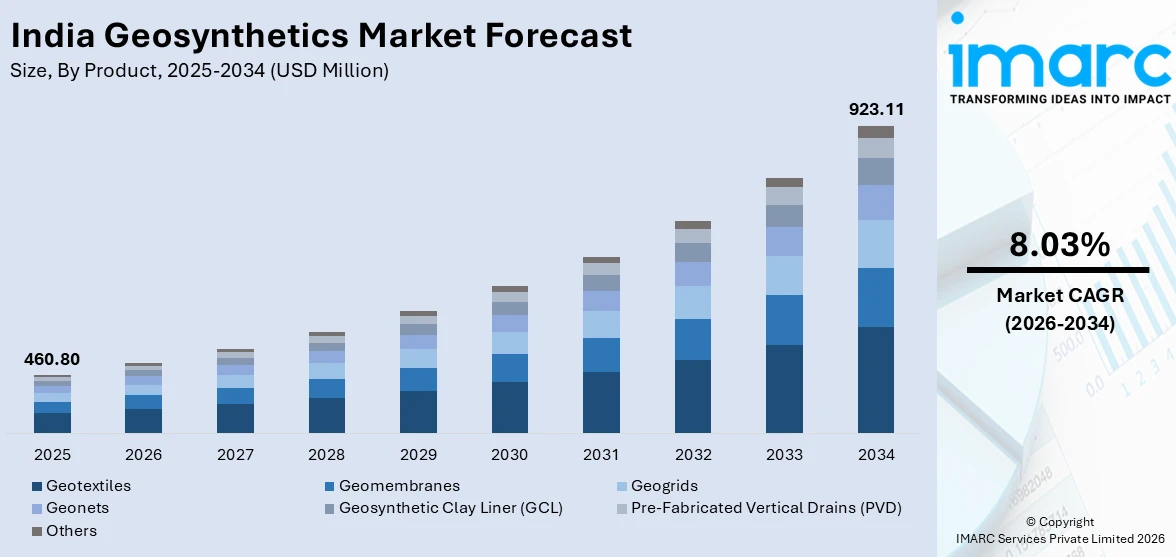

The India geosynthetics market size was valued at USD 460.80 Million in 2025 and is projected to reach USD 923.11 Million by 2034, growing at a compound annual growth rate of 8.03% from 2026-2034.

India's geosynthetics market is experiencing robust expansion, underpinned by the country's ambitious infrastructure modernisation agenda and intensifying demand for durable, performance-enhancing construction materials. Geosynthetics, encompassing geotextiles, geomembranes, geogrids, and related products, are increasingly embedded across transportation, water management, and environmental engineering projects. Growing awareness of sustainable construction practices, government-backed regulatory quality standards, and the country's rapid urbanisation are collectively widening the application landscape and reinforcing the India geosynthetics market share.

Key Takeaways and Insights:

- By Product: Geotextiles dominate the market with a share of 32% in 2025, reflecting their versatile utility across road construction, drainage, and soil erosion control applications throughout India.

- By Type: Non-woven lead the market with a share of 45% in 2025, owing to their superior filtration, drainage, and separation properties that make them the preferred choice across a broad spectrum of civil engineering applications.

- By Material: Polypropylene represents the largest material segment with a share of 30% in 2025, driven by its outstanding chemical resistance, cost efficiency, and widespread suitability across geotextile and geomembrane manufacturing.

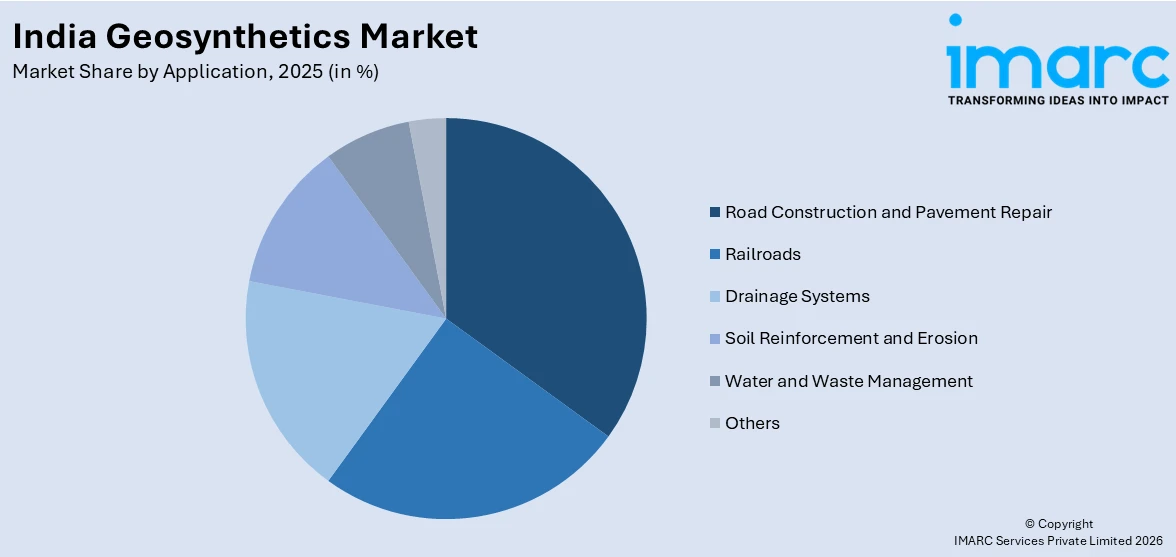

- By Application: Road construction and pavement repair represent the largest application segment with a share of 29% in 2025, supported by India's expansive national highway and rural road development programmes.

- Key Players: The India geosynthetics market features a competitive mix of domestic manufacturers and international participants offering a broad portfolio of geotextiles, geogrids, geomembranes, and composite solutions for construction and environmental applications.

To get more information on this market Request Sample

The India geosynthetics market is shaped by a convergence of government-driven infrastructure investment, advancing material technologies, and escalating environmental compliance requirements. Under the Bharatmala Pariyojana highway development scheme, thousands of kilometres of new roads and expressways are under construction, generating sustained demand for geotextile reinforcement and pavement separation layers. The national railway network expansion, including dedicated freight corridors and the 508-kilometre Mumbai-Ahmedabad high-speed rail project announced in 2024, is further amplifying geosynthetic consumption for track bed stabilisation and embankment reinforcement. Simultaneously, the Ministry of Textiles issued Quality Control Orders (QCOs) for geotextiles in October 2024, establishing mandatory performance standards that are elevating product quality benchmarks across the supply chain and encouraging broader adoption in critical infrastructure projects.

India Geosynthetics Market Trends:

Expansion of National Road and Highway Infrastructure Driving Geotextile Adoption

India's accelerating road infrastructure programmes, particularly the Bharatmala Pariyojana initiative targeting the development of over 26,000 kilometres of national highways, are generating substantial demand for geotextiles and geogrids used in subgrade stabilisation, pavement reinforcement, and drainage management. The Delhi-Mumbai Expressway, among the longest in the country, has incorporated geosynthetics for retaining wall construction and erosion control along its entire corridor. As road infrastructure budgets continue to expand, the integration of geosynthetics in pavement design is becoming standard engineering practice across state and national highway projects.

Rising Regulatory Standards Formalising Geosynthetic Quality Requirements

The Government of India has been steadily strengthening the regulatory framework governing geosynthetic materials to improve product quality and industry standards. Regulatory measures introduced by the Ministry of Textiles require geotextile products to comply with defined safety and performance specifications, helping standardize product quality and reduce the circulation of substandard materials in the market. These initiatives are also influencing procurement practices in infrastructure projects by encouraging stricter compliance requirements. In parallel, research institutions are receiving government support to enhance laboratory capabilities and promote innovation in technical textiles. Such efforts reflect a broader national focus on advancing research-driven development and improving the reliability of geosynthetic materials used in infrastructure and environmental applications.

Increasing Integration of Geosynthetics in Water and Waste Management Infrastructure

Water conservation and wastewater management projects across India are emerging as an important growth avenue for geomembranes and geosynthetic clay liners. In December 2024, the New Delhi Municipal Council announced the development of 139 modular rainwater harvesting pits, incorporating geosynthetic lining to prevent groundwater contamination. Geotube technology has recently been utilized for desilting drainage channels and supporting water treatment processes in urban areas. Such initiatives demonstrate the expanding role of geosynthetics beyond traditional applications in roads and railways. Increasingly, these materials are being adopted in urban water management and environmental infrastructure projects, highlighting their versatility and growing relevance across diverse engineering applications.

Market Outlook 2026-2034:

The India geosynthetics market is expected to witness steady expansion over the coming years, driven by the combined influence of large-scale infrastructure development, stricter environmental regulations, and growing awareness of advanced geosynthetic solutions. Public investment in transportation networks, water management systems, and urban infrastructure continues to create significant opportunities for the adoption of geosynthetic materials. At the same time, the increasing focus on sustainable construction practices and improved soil stabilization techniques is encouraging the wider use of geosynthetics across multiple engineering applications, supporting long-term growth across various product segments and end-use sectors. The market generated a revenue of USD 460.80 Million in 2025 and is projected to reach a revenue of USD 923.11 Million by 2034, growing at a compound annual growth rate of 8.03% from 2026-2034.

India Geosynthetics Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

| Product | Geotextiles | 32% |

| Type | Non-Woven | 45% |

| Material | Polypropylene | 30% |

| Application | Road Construction and Pavement Repair | 29% |

Product Insights:

- Geotextiles

- Geomembranes

- Geogrids

- Geonets

- Geosynthetic Clay Liner (GCL)

- Pre-Fabricated Vertical Drains (PVD)

- Others

Geotextiles dominate the India geosynthetics market with a share of 32% in 2025.

Geotextiles are the most widely deployed category within India's geosynthetics sector, reflecting their multifunctional utility across reinforcement, filtration, separation, and drainage applications. Their adoption spans road construction, railway track beds, coastal engineering works, and erosion protection projects. The Pradhan Mantri Gram Sadak Yojana rural roads programme has been a key demand driver, where both synthetic and natural-fibre geotextiles are specified for road subgrade stabilisation. Coir-based geotextiles, promoted by the government under PMGSY-III, have achieved considerable traction in rural road construction in southern states, offering biodegradability alongside adequate mechanical performance for low-traffic roads.

Geomembranes represent the second major product segment, primarily deployed in lining applications for landfills, reservoirs, canals, and industrial containment facilities. Their role in preventing groundwater contamination and ensuring hydraulic integrity in water storage infrastructure is gaining prominence as India expands its water resource management capacity. Geogrids are extensively used in soil reinforcement for highway embankments and railway track bed applications, where the Bharatmala expressway corridors and the dedicated freight railway corridors have been significant demand catalysts.

Type Insights:

- Woven

- Non-Woven

- Knitted

- Others

Non-Woven represent the largest share of 45% in the India geosynthetics market in 2025.

Non-woven geosynthetics account for the largest type segment, owing to their outstanding performance in drainage, filtration, and separation functions that are critical across a wide range of civil engineering applications in India. Their flexibility and compatibility with diverse installation conditions make them the preferred choice in road construction, railway subbase stabilisation, and erosion management. The manufacturing process for non-woven fabrics also lends itself to cost-effective large-volume production using polypropylene and polyester polymers, giving them a competitive price advantage over woven alternatives in tender-driven government infrastructure contracts.

Woven geosynthetics occupy a significant share within the market, particularly valued for their superior tensile strength and load-bearing capacity in demanding reinforcement applications such as steep slope stabilisation, retaining structures, and heavy-traffic embankments. Their structured construction provides predictable mechanical properties that are specified in high-performance engineering projects. Knitted geosynthetics, while a smaller segment, serve specialised applications including drainage composites and flexible containment systems where directional strength management is critical.

Material Insights:

- Polypropylene

- Polyester

- Polyethylene

- Polyvinyl Chloride

- Synthetic Rubber

- Others

Polypropylene leads the highest revenue share of 30% in the India geosynthetics material segment in 2025.

Polypropylene is the dominant raw material in the India geosynthetics market, prized for its combination of chemical resistance, hydrolytic stability, and cost-effective processability. It is the primary feedstock for non-woven geotextile manufacturing, directly connecting its dominance to the prevalence of non-woven product forms across Indian infrastructure projects. India's robust domestic polypropylene production capacity supports competitive raw material pricing for geosynthetic manufacturers, enabling cost-competitive product development for both domestic use and export. The material's UV resistance, when appropriately stabilised, further supports its suitability for Indian climatic conditions including high solar radiation and monsoon moisture exposure.

Polyester is the second major material segment, offering high tensile modulus and creep resistance that make it the preferred choice for applications requiring sustained long-term load-bearing performance, including reinforcement geogrids for highway embankments and retaining walls. Polyethylene, particularly high-density polyethylene (HDPE), dominates the geomembrane segment due to its impermeability, chemical inertness, and proven performance in landfill and water containment applications. Polyvinyl chloride (PVC) and synthetic rubber materials serve niche but important roles in tunnel waterproofing and specialised containment systems.

Application Insights:

Access the comprehensive market breakdown Request Sample

- Road Construction and Pavement Repair

- Railroads

- Drainage Systems

- Soil Reinforcement and Erosion

- Water and Waste Management

- Others

Road construction and pavement repair represent the leading application segment with a share of 29% of the total India geosynthetics market in 2025.

Road construction and pavement maintenance represent the largest application area for geosynthetics in India, supported by continued investment in highway and expressway development. Materials such as geotextiles and geogrids are widely used in road projects for functions including subgrade separation, subbase reinforcement, and asphalt interlayer stabilization. These applications help enhance pavement durability, improve load distribution, and reduce long-term maintenance requirements. In addition, the growing development of tunnels and complex highway infrastructure is increasing the use of geomembranes and other waterproofing geosynthetics, which play a critical role in protecting structures from water infiltration and ensuring long-term structural stability.

The railway sector is also emerging as a significant application area for geosynthetics as rail infrastructure expands and modernizes across the country. These materials are commonly used in track bed stabilization, embankment reinforcement, and drainage management to improve track durability and operational safety. Effective soil stabilization and moisture control are essential for maintaining the long-term performance of railway corridors. At the same time, rapid urbanization is increasing the need for improved drainage and waste management systems. Geomembranes and related geosynthetic solutions are therefore gaining wider adoption in landfill containment, wastewater treatment, and stormwater management projects.

Regional Insights:

- North India

- West and Central India

- South India

- East and Northeast India

North India’s geosynthetics demand is driven by extensive highway and expressway construction, railway corridor upgrades, and rapid urban infrastructure development. The region’s large transportation projects require geosynthetics for soil stabilization, reinforcement, and drainage management. Additionally, expanding industrial zones and increasing urbanization are strengthening the need for durable and cost-efficient civil engineering materials.

West and Central India’s market growth is supported by port-linked infrastructure development, industrial corridor projects, and the expansion of urban transportation systems. Major metropolitan areas in the region are witnessing continuous investments in metro rail networks, highways, and logistics infrastructure. These developments are increasing the use of geosynthetics for ground reinforcement, erosion control, and long-term infrastructure stability.

South India’s demand for geosynthetics is driven by road modernization projects, coastal protection initiatives, and investments in water resource management infrastructure. The region’s focus on strengthening transportation networks and addressing coastal erosion challenges is encouraging the adoption of geosynthetics for soil stabilization, slope protection, and efficient drainage systems.

East and Northeast India’s geosynthetics demand is rising due to improving connectivity projects and infrastructure development in difficult terrains. The region’s focus on flood management, railway expansion, and road construction in hilly and river-prone areas is increasing the use of geosynthetics for embankment reinforcement, erosion control, and enhanced drainage performance.

Market Dynamics:

Growth Drivers:

Why is the India Geosynthetics Market Growing?

Unprecedented Scale of National Infrastructure Investment

India's government has committed to one of the most expansive infrastructure investment programmes in the country's history, creating a powerful sustained demand catalyst for geosynthetics across all major product categories. The National Infrastructure Pipeline encompasses over 6,500 projects across roads, railways, ports, airports, urban infrastructure, and water management. Rising government expenditure on infrastructure development is significantly increasing demand for construction materials, including geosynthetics. Large-scale highway and transportation development programs require extensive use of geotextiles and geogrids for applications such as subgrade stabilization, slope protection, and effective drainage management. These materials play a crucial role in improving the durability and performance of modern road infrastructure. Continuous investment in transportation networks and civil engineering projects is providing long-term demand visibility for geosynthetic manufacturers while encouraging wider adoption of these materials across major infrastructure developments throughout the country.

Railway Network Modernisation and Dedicated Freight Corridor Expansion

India’s ongoing railway modernization is emerging as an important growth driver for the geosynthetics market, with applications that include track bed reinforcement, embankment stabilization, drainage management, and tunnel waterproofing. As rail networks expand and infrastructure upgrades accelerate, geosynthetic materials are increasingly being used to enhance structural stability and improve long-term performance. High-speed rail projects and major corridor developments require advanced geosynthetic solutions to address challenges such as soil settlement and load distribution. Additionally, freight corridor construction across diverse soil conditions is further increasing the demand for specialized reinforcement and drainage systems, making railway infrastructure a significant and independent contributor to geosynthetics adoption in India.

Tightening Environmental Regulations and Sustainable Construction Imperatives

Increasing environmental awareness within India’s regulatory and policy framework is expanding the application scope of geosynthetics beyond conventional civil construction. These materials are increasingly used in waste containment systems, water resource management projects, and environmental protection initiatives. Stricter waste management regulations are encouraging the use of engineered landfill liners that incorporate geomembranes and geosynthetic clay liners to prevent groundwater contamination. At the same time, research institutions are receiving government support to strengthen domestic innovation in technical textiles and geosynthetics. The promotion of biodegradable alternatives such as natural fiber-based geotextiles for rural infrastructure projects further reflects the growing emphasis on sustainable engineering solutions, encouraging wider adoption of geosynthetics in infrastructure development.

Market Restraints:

What Challenges the India Geosynthetics Market is Facing?

High Initial Material and Installation Costs Relative to Conventional Alternatives

Despite their superior long-term performance and lifecycle cost advantages, geosynthetics often carry higher upfront material costs compared to conventional construction alternatives such as gravel, stone, and compacted soil. In price-sensitive public procurement environments where tender selection is dominated by lowest-cost bidding, this initial cost premium can disadvantage geosynthetic specifications, particularly in smaller rural infrastructure projects where the long-term value proposition is not always fully appraised by procurement decision-makers.

Limited Technical Expertise and Skilled Workforce Availability

The effective deployment of geosynthetics requires specialised technical knowledge in product selection, quality assessment, installation procedures, and quality control monitoring. India currently faces a shortage of trained civil engineers and site supervisors with demonstrable geosynthetic expertise, particularly in Tier-2 and Tier-3 cities and rural infrastructure project sites. This skills deficit can result in suboptimal product installation, undermining the performance benefits of geosynthetics and creating risk aversion among project developers, thereby constraining market penetration in smaller and less technically sophisticated project segments.

Market Fragmentation and Prevalence of Substandard Products

India’s geosynthetics market features a fragmented supply structure with many small-scale domestic producers operating alongside larger national and international manufacturers. The presence of lower-quality, non-compliant products, particularly in geotextiles, has historically created concerns regarding performance reliability. Although new quality regulations aim to improve standards, consistent enforcement across the supply chain remains essential.

Competitive Landscape:

The India geosynthetics market features a moderately fragmented competitive landscape, comprising domestic manufacturers, international material specialists, and emerging regional producers operating across multiple product categories and pricing segments. Local manufacturers have developed strong capabilities in producing geotextiles and geomembranes, while global participants contribute advanced technologies in areas such as geogrids and geocomposites. Ongoing consolidation within the sector is gradually transforming competitive dynamics by creating more integrated solution providers with broader operational capabilities. At the same time, companies are increasingly differentiating themselves through technical support services, compliance with evolving quality standards, and reliable supply chains to meet the requirements of large-scale infrastructure and environmental projects.

Recent Developments:

- March 2025: Geotube desilting technology was deployed to clean 23 untapped drainage channels in Prayagraj ahead of the Maha Kumbh event, processing over 100 million litres of water daily and treating effluent before release into the Ganga river. This deployment highlighted geosynthetics' expanding role in urban water management and environmental remediation applications.

- October 2024: The Ministry of Textiles issued Quality Control Orders for geotextiles and related industrial textiles, establishing mandatory safety and performance standards for the sector. These QCOs are expected to significantly elevate product quality benchmarks across the domestic supply chain and align Indian geotextile specifications with international standards.

- June 2023: Hella Infra Market Private Limited (Infra.Market) completed the acquisition of Strata Geosystems (India) for approximately USD 110 million, creating a significantly strengthened geosynthetics manufacturing and engineering solutions platform and marking one of the largest consolidation transactions in the India geosynthetics sector.

India Geosynthetics Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Products Covered | Geotextiles, Geomembranes, Geogrids, Geonets, Geosynthetic Clay Liner (GCL), Pre-Fabricated Vertical Drains (PVD), Others |

| Types Covered | Woven, Non-Woven, Knitted, Others |

| Materials Covered | Polypropylene, Polyester, Polyethylene, Polyvinyl Chloride, Synthetic Rubber, Others |

| Applications Covered | Road Construction and Pavement Repair, Railroads, Drainage Systems, Soil Reinforcement and Erosion, Water and Waste Management, Others |

| Regions Covered | North India, West and Central India, South India, East and Northeast India |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Geosynthetics Market Research Report and Industry Forecast Report

The India geosynthetics market size was valued at USD 460.80 Million in 2025.

The India geosynthetics market is expected to grow at a compound annual growth rate of 8.03% from 2026-2034 to reach USD 923.11 Million by 2034.

Geotextiles held the largest product segment with a share of 32% in 2025, driven by their widespread adoption in road construction, drainage systems, erosion control, and railway track bed stabilisation across India's rapidly expanding infrastructure network.

Key factors driving the India geosynthetics market include the country's large-scale national infrastructure investment under the National Infrastructure Pipeline and Bharatmala Pariyojana, the rapid expansion of the railway network, growing environmental compliance requirements for waste containment, and the government's active policy support for sustainable construction materials including geotextile quality standardisation.

Major challenges include the higher upfront cost of geosynthetics compared to conventional construction materials, a shortage of trained technical personnel for proper installation and quality assurance, and market fragmentation characterised by the presence of substandard products from informal manufacturers that creates procurement uncertainty for large project developers.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)