India Government Cloud Market Size, Share, Trends and Forecast by Component, Deployment Model, Service Model, Application, and Region, 2026-2034

India Government Cloud Market Summary:

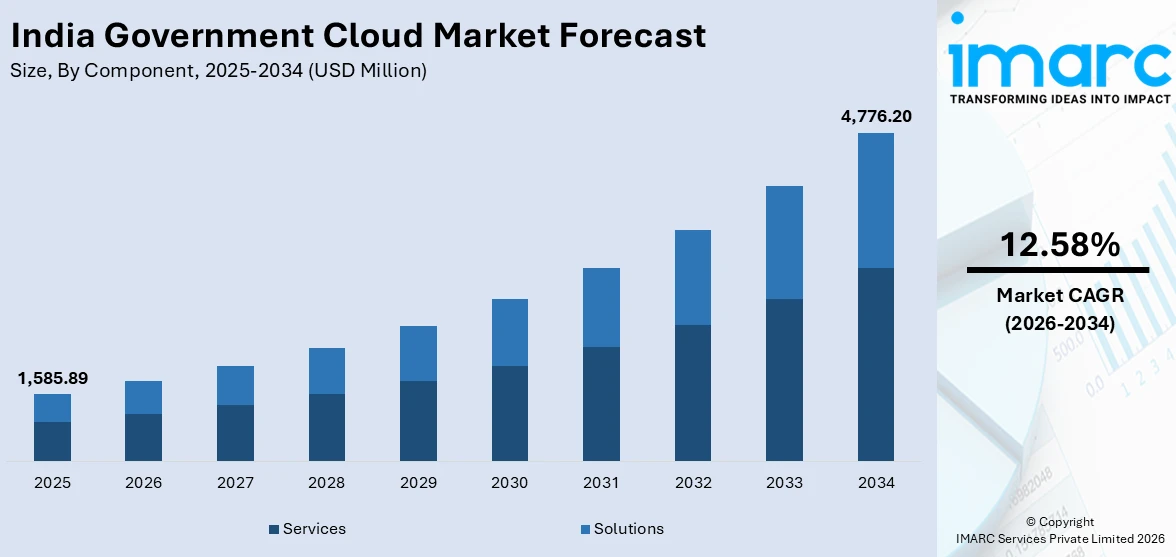

The India government cloud market size was valued at USD 1,585.89 Million in 2025 and is projected to reach USD 4,776.20 Million by 2034, growing at a compound annual growth rate of 12.58% from 2026-2034.

India's government cloud market is expanding as federal and state administrations increasingly migrate public services to cloud platforms. Demand is driven by the national push for e-governance, the proliferation of citizen-facing digital services, and the adoption of secure, scalable IT infrastructure aligned with national digital transformation agendas. Rising needs for operational efficiency and interoperability across government departments continue to propel the India government cloud market share.

Key Takeaways and Insights:

- By Component: Services dominate the market with a share of 56.0% in 2025, attributed to rising government demand for managed services, cloud consulting, technical support, and system integration to enable seamless digital transformation across central and state departments.

- By Deployment Model: Private cloud leads the market with a share of 41.0% in 2025, owing to heightened data sovereignty mandates, regulatory compliance requirements, and the need for dedicated, secure cloud environments that allow government agencies to maintain full control over sensitive citizen data.

- By Service Model: Infrastructure as a Service prevails the market with a share of 38.0% in 2025, driven by government agencies' need for scalable virtual compute, networking, and storage resources without incurring large capital expenditures on physical data center infrastructure.

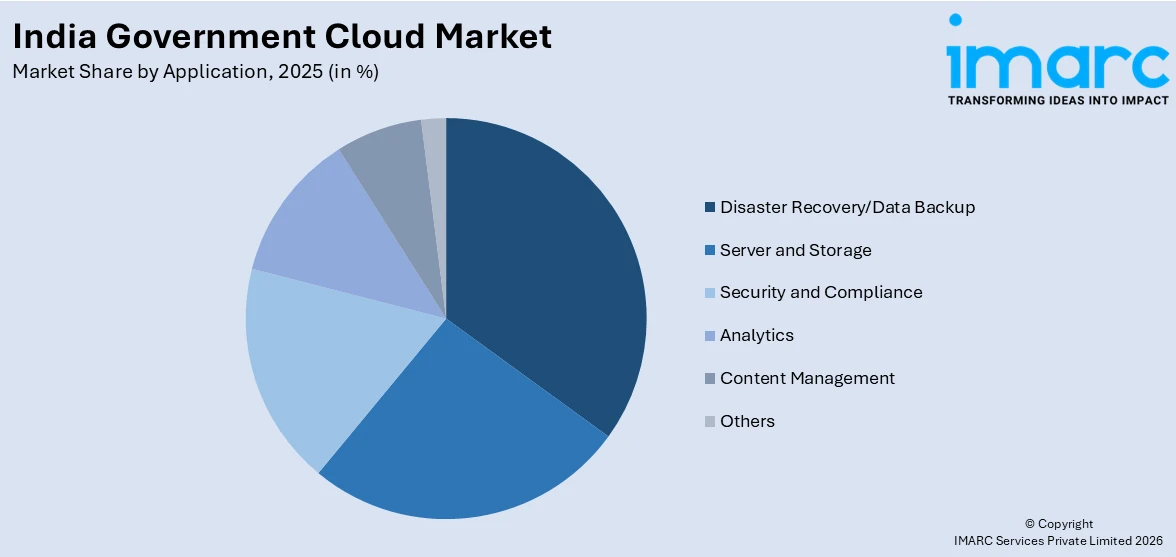

- By Application: Disaster recovery/data backup holds the largest segment with a market share of 28.0% in 2025, reflecting critical government imperatives around business continuity, data resilience, and the protection of sensitive public records against system outages, cyberattacks, and unforeseen disruptions.

- By Region: North India represents the largest region with 36.0% share in 2025, driven by the concentration of central government ministries, major public sector enterprises, and national data center corridors in the Delhi NCR and National Capital Territory region.

- Key Players: Key players drive the India government cloud market by offering secure, MeitY-compliant cloud infrastructure and managed services tailored for public sector use. Their investments in sovereign cloud platforms, government-specific compliance certifications, and strategic partnerships with national agencies accelerate digital governance transformation and broaden cloud adoption across central and state government departments.

To get more information on this market Request Sample

India's government cloud market is experiencing robust momentum fueled by transformative national programs and the accelerating digitalization of public sector operations across central and state agencies. The GI Cloud initiative, widely known as MeghRaj, continues to serve as the foundational infrastructure for e-governance across India. As of December 2025, over 2,170 central and state ministries and departments have hosted applications on the platform, underscoring the extensive scale of government-led cloud adoption. Managed by the National Informatics Centre under MeitY, MeghRaj supports a comprehensive range of service models, including IaaS, PaaS, and SaaS, enabling government entities to modernize their IT infrastructure efficiently and at scale. Complementing domestic cloud initiatives, global technology players are channeling substantial capital into Indian cloud infrastructure, reinforcing the country's position as a rapidly maturing government cloud hub. National programs such as Digital India and IndiaAI are generating sustained demand for secure, high-capacity cloud services capable of supporting AI-driven public service delivery, further strengthening this market's overall growth trajectory and creating compelling long-term opportunities across the value chain.

India Government Cloud Market Trends:

Surge in Hybrid Cloud Adoption Across Government Agencies

India's government agencies are rapidly embracing hybrid cloud architectures that seamlessly combine private and public cloud environments. This shift allows departments to maintain sensitive citizen data within secure, government-controlled private clouds while leveraging the scalability of public cloud platforms for non-sensitive workloads. The approach enables greater operational flexibility, improved resource utilization, and enhanced service continuity. Driven by evolving data sovereignty regulations and the need for interoperable digital infrastructure, hybrid cloud is increasingly becoming the preferred deployment model across India's public sector.

AI and Advanced Analytics Integration in Public Sector Cloud Platforms

Government cloud platforms in India are increasingly being enhanced with artificial intelligence and advanced analytics capabilities, enabling more intelligent and data-driven public service delivery. Ministries and departments are leveraging AI-powered cloud services to process large volumes of citizen data, automate administrative workflows, and improve decision-making in areas such as healthcare, taxation, and public welfare. This integration is transforming traditional e-governance models, making government operations more responsive, efficient, and predictive across central and state levels.

Growing Emphasis on Data Sovereignty and Localized Cloud Infrastructure

A defining trend shaping India's government cloud market is the intensifying focus on data sovereignty and the development of localized cloud infrastructure. Government mandates increasingly require that sensitive public-sector data remain within national boundaries, driving agencies to prioritize domestically hosted cloud solutions certified under regulatory frameworks such as STQC. This trend is prompting cloud service providers to expand their Indian data center presence, resulting in a more robust, sovereign, and compliance-ready cloud ecosystem specifically tailored for government workloads.

Market Outlook 2026-2034:

India's government cloud market is positioned for sustained and accelerating growth during the forecast period, underpinned by continued policy momentum, expanding digital public infrastructure, and deepening cloud adoption across government functions. The convergence of ambitious national programs, escalating cybersecurity awareness, and the integration of AI into public service delivery is expected to drive significant investment in cloud infrastructure across central and state government entities. Government agencies are expected to increasingly prioritize private and hybrid cloud deployments to balance data sovereignty requirements with the operational flexibility that modern cloud environments offer. Infrastructure modernization, disaster recovery planning, and AI-enabled analytics are anticipated to remain critical investment areas. Collectively, these drivers will create a compelling long-term growth environment for cloud service providers catering to India's expanding public sector digital agenda. The market generated a revenue of USD 1,585.89 Million in 2025 and is projected to reach a revenue of USD 4,776.20 Million by 2034, growing at a compound annual growth rate of 12.58% from 2026-2034.

India Government Cloud Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

|

Component |

Services |

56.0% |

|

Deployment Model |

Private Cloud |

41.0% |

|

Service Model |

Infrastructure as a Service |

38.0% |

|

Application |

Disaster Recovery/Data Backup |

28.0% |

|

Region |

North India |

36.0% |

Component Insights:

- Solutions

- Services

Services dominate with a market share of 56.0% of the total India government cloud market in 2025.

The dominance of the services segment in India's government cloud market reflects the expansive and evolving needs of public sector organizations as they navigate complex cloud adoption journeys. Government departments increasingly rely on a wide spectrum of managed services, including cloud migration support, technical consulting, system integration, and ongoing managed operations, to transition legacy IT environments onto modern cloud platforms. These services play a critical role in bridging the gap between existing government infrastructure and the advanced cloud capabilities required for digital service delivery, ensuring smooth transitions while minimizing operational disruption and compliance risk.

The services segment also encompasses a diverse range of professional offerings specifically designed for the government context, including cloud strategy consulting, application rationalization, cloud-native application development, and specialized training programs for government IT personnel. As government agencies across India expand their digital infrastructure to support citizen-facing portals, tax systems, health records management, and public safety platforms, demand for expert services that enable secure, compliant, and efficient cloud operations continues to grow. The ongoing emphasis on cloud-first procurement strategies across ministries further reinforces the leading position of services within the broader market landscape.

Deployment Model Insights:

- Hybrid Cloud

- Private Cloud

- Public Cloud

Private cloud leads with a share of 41.0% of the total India government cloud market in 2025.

Private cloud's commanding position in India's government cloud market stems from the unique security, compliance, and sovereignty requirements that characterize the public sector. Government agencies routinely handle vast quantities of sensitive citizen information, classified administrative data, and critical national infrastructure records, all of which demand the highest levels of protection. Private cloud environments offer dedicated computing resources that remain under full government control, significantly reducing the risk of unauthorized access and ensuring adherence to India's rigorous data localization mandates. The architecture supports robust access management, audit trails, and stringent security controls that are essential for government operations.

MeghRaj, India's national government cloud under the National Informatics Centre, exemplifies the private cloud model in practice, providing dedicated computing resources exclusively for central and state government ministries. The platform's architecture allows departments to maintain complete data sovereignty while benefiting from cloud-like elasticity and on-demand service provisioning. Regulatory frameworks established by MeitY, including mandatory STQC certification for cloud service providers, further reinforce private cloud adoption by ensuring that all government cloud environments meet internationally recognized security standards. As digital governance expands across more departments, the demand for secure, government-exclusive private cloud environments is expected to remain strong.

Service Model Insights:

- Infrastructure as a Service

- Platform as a Service

- Software as a Service

Infrastructure as a Service prevails the market with a 38.0% share of the total India government cloud market in 2025.

Infrastructure as a Service occupies the leading position in India's government cloud service model landscape by providing public sector organizations with on-demand access to scalable virtual compute, networking, and storage resources without the burden of owning or managing physical data center infrastructure. Government agencies rely on IaaS to deploy critical applications, host e-governance portals, and support large-scale data processing workloads. This model enables ministries to rapidly provision resources in response to surges in citizen demand, such as during national election registration campaigns, tax filing seasons, or large-scale welfare disbursement exercises, without requiring pre-planned capital investments.

The adoption of IaaS within India's government cloud market is further propelled by the national GI Cloud initiative under MeghRaj, which provides IaaS capabilities to ministries and departments through the National Informatics Centre's data center infrastructure. By eliminating the need for department-specific hardware procurement, the IaaS model significantly reduces total IT ownership costs while enabling faster application deployment timelines. It also underpins critical government functions such as disaster recovery provisioning, hybrid cloud integration, and the scaling of national digital public infrastructure platforms, positioning IaaS as the indispensable foundation of India's e-governance cloud strategy.

Application Insights:

Access the comprehensive market breakdown Request Sample

- Server and Storage

- Disaster Recovery/Data Backup

- Security and Compliance

- Analytics

- Content Management

- Others

Disaster recovery/data backup represents the leading segment with a 28.0% share of the total India government cloud market in 2025.

Disaster recovery and data backup applications hold the largest share in India's government cloud market, reflecting the critical importance that public sector agencies place on ensuring the continuity of essential services and the protection of vast volumes of citizen data. Government systems must remain resilient against a broad spectrum of threats including cyberattacks, natural disasters, infrastructure failures, and unplanned outages that could disrupt the delivery of critical public services. Cloud-based disaster recovery solutions enable agencies to replicate workloads across geographically distributed data centers, ensuring rapid failover and minimal service interruption in the event of a primary system failure.

The growing adoption of disaster recovery solutions in India's government sector is closely linked to the escalating frequency and sophistication of cyber threats targeting public sector IT infrastructure, alongside the heightened scrutiny that government agencies face for maintaining service availability. Cloud-based disaster recovery platforms enable agencies to meet stringent recovery time objectives and recovery point objectives mandated by government cybersecurity and IT continuity policies. The MeghRaj platform, operated by the National Informatics Centre, supports disaster recovery capabilities for ministries through its distributed data center network, exemplifying the government's commitment to resilient, cloud-backed public sector operations.

Regional Insights:

- North India

- South India

- East India

- West India

North India comprises the largest region with a 36.0% share of the total India government cloud market in 2025.

North India holds the dominant position in India's government cloud market, primarily driven by the concentration of central government ministries, parliamentary institutions, and major public sector enterprises in the Delhi National Capital Region. The region hosts India's primary national data center corridors managed by the National Informatics Centre, which serves as the nerve center of the MeghRaj platform and provides cloud services to a vast network of central government departments.

Beyond the national capital, North India encompasses key technology hubs such as Noida and Gurugram, which attract substantial IT infrastructure investment and host several MeitY-empaneled cloud service providers. The region's well-developed digital connectivity, availability of skilled IT talent, and robust regulatory oversight make it the preferred location for sovereign cloud deployments serving government agencies. These structural advantages are expected to sustain North India's overall market leadership throughout the forecast period.

Market Dynamics:

Growth Drivers:

Why is the India Government Cloud Market Growing?

Government-Led Digital Transformation Initiatives

India's government cloud market is fundamentally propelled by a comprehensive suite of national digital transformation initiatives that mandate the modernization of public sector IT infrastructure. The Digital India program serves as the cornerstone of this transformation, establishing a policy framework that encourages all central and state government agencies to adopt cloud-first strategies for service delivery. Under this initiative, ministries are actively transitioning from legacy, siloed IT environments to centralized cloud platforms that enable greater agility, interoperability, and cost efficiency. The GI Cloud initiative, MeghRaj, operationalized through the National Informatics Centre, provides the technical backbone for this transition, offering a comprehensive portfolio of cloud services including infrastructure, platform, and software services to government departments across India. National programs such as IndiaAI, Smart Cities Mission, and the National e-Governance Plan further amplify cloud adoption by creating demand for scalable, secure, and citizen-centric digital services. These initiatives collectively drive the procurement of cloud solutions across departments responsible for healthcare delivery, education management, taxation, welfare disbursement, and public safety. The emphasis on integrated digital public infrastructure and interoperable government platforms is generating consistent, long-term demand for government cloud services, making policy-driven digital transformation the most powerful and enduring growth catalyst in this market.

Escalating Demand for Data Sovereignty and Secure Cloud Infrastructure

India's public sector is experiencing unprecedented pressure to protect sensitive citizen data and critical national information assets, making data sovereignty and security among the most compelling growth drivers for the government cloud market. Regulatory frameworks established by MeitY mandate that government data be stored and processed within India's geographic boundaries, effectively requiring agencies to procure cloud services from certified, domestically hosted providers. This mandate has significantly accelerated investment in sovereign cloud infrastructure, driving the development of purpose-built government cloud environments certified under internationally recognized security standards. The increasing frequency and complexity of cyberattacks targeting government digital systems has further intensified the urgency of deploying robust, cloud-based security architectures. Government agencies are investing in cloud environments that incorporate advanced encryption, identity and access management, and real-time threat monitoring to safeguard sensitive public data. The Personal Data Protection framework and evolving cybersecurity policies reinforce the regulatory imperative for secure cloud adoption, creating a durable and growing market for government cloud security solutions. As digital governance platforms expand their reach to rural and underserved communities, ensuring the security and integrity of cloud-hosted citizen data becomes an increasingly critical and non-negotiable strategic priority for Indian government agencies operating at federal, state, and local levels.

Rising Need for Operational Efficiency and Citizen-Centric Service Delivery

India's government cloud market is being propelled by the mounting imperative to modernize public service delivery, reduce operational costs, and meaningfully enhance the experience of hundreds of millions of citizens interacting daily with government platforms. Cloud adoption enables government agencies to consolidate fragmented IT systems, eliminate redundant infrastructure, and streamline workflows across departments, resulting in significant improvements in administrative efficiency and service quality. By transitioning to shared, centralized cloud environments, ministries can redirect resources previously consumed by hardware maintenance and IT management toward higher-value public service priorities. The proliferation of citizen-facing digital platforms, including online tax portals, health management systems, benefit disbursement applications, and e-procurement portals, is generating sustained demand for scalable, high-performance cloud infrastructure capable of handling peak citizen transaction volumes. Cloud environments deliver the elasticity required to accommodate wide fluctuations in service demand, ensuring consistent performance and availability even during periods of high citizen engagement. Additionally, the integration of artificial intelligence and data analytics capabilities within government cloud platforms is enabling agencies to deliver more personalized, proactive, and efficient citizen services, further reinforcing cloud adoption as an indispensable strategic necessity across India's entire public sector administration.

Market Restraints:

What Challenges the India Government Cloud Market is Facing?

Data Security and Cybersecurity Vulnerabilities

Government cloud environments in India remain exposed to evolving and sophisticated cybersecurity threats, including ransomware attacks, data breaches, and advanced persistent threats targeting public sector IT systems. Ensuring robust security across diverse cloud environments is operationally demanding, as government agencies must implement comprehensive encryption, identity management, and continuous monitoring protocols. The rapidly shifting threat landscape requires ongoing security investment and specialized expertise, placing considerable strain on government IT budgets and cloud management teams already navigating complex multi-cloud architectures and stringent regulatory requirements.

Legacy IT Infrastructure and Migration Complexity

A significant barrier to government cloud adoption in India is the extensive base of legacy IT systems and applications that many ministries and departments continue to operate. Migrating outdated, monolithic government applications to cloud environments involves substantial technical complexity, extended timelines, and considerable financial investment. Many legacy systems were built on proprietary architectures not designed for cloud compatibility, requiring costly re-engineering or complete application redevelopment before migration can occur, slowing the overall pace of government cloud modernization across central and state departments.

Shortage of Cloud-Skilled Talent in the Public Sector

India's government cloud market faces a persistent shortage of cloud-skilled IT professionals within the public sector. Government agencies often struggle to attract and retain technologists with expertise in cloud architecture, security, and operations due to highly competitive compensation packages offered by the private technology sector. This talent gap impedes the effective design, deployment, and management of government cloud environments, creating operational vulnerabilities and slowing the adoption of advanced cloud capabilities such as AI integration, multi-cloud management, and cloud-native application development across ministries and departments.

Competitive Landscape:

India's government cloud market features a competitive landscape shaped by a blend of domestic public sector IT organizations, MeitY-empaneled cloud service providers, and global technology players operating within India's data localization framework. The National Informatics Centre anchors the government side, providing the foundational MeghRaj platform and engaging private cloud vendors through open tendering processes. Certified cloud service providers operate within a stringent regulatory framework established by MeitY and audited by the STQC Directorate, ensuring compliance with international security standards including ISO 27001 and ISO 27017. Competition among providers centers on the quality of sovereign cloud infrastructure, government-specific security certifications, technical support capabilities, and pricing competitiveness within the empanelment framework. Domestic providers hold competitive advantages through established government relationships and deep familiarity with regulatory requirements, while global providers leverage technological sophistication and broad service portfolios. The market is expected to remain moderately concentrated, with ongoing new entrant activity as additional cloud providers pursue MeitY empanelment to access India's growing public sector cloud opportunity.

Recent Developments:

- In December 2025, the Ministry of Electronics and Information Technology mandated the migration of approximately 12.68 lakh official government email accounts to a cloud-hosted platform by Zoho, an Indian technology provider. The contract enforced strict data sovereignty requirements, with primary and disaster-recovery data centers located within India and an explicit prohibition on replicating data outside national borders, reinforcing the government's commitment to sovereign cloud infrastructure.

- In January 2025, Amazon Web Services announced plans to invest approximately USD 8.3 Billion in cloud infrastructure within the AWS Asia-Pacific Mumbai Region in Maharashtra, aiming to significantly expand cloud computing capacity in India. The investment was projected to contribute USD 15.3 Billion to India's GDP and sustain over 81,300 full-time positions in the local data center supply chain by 2030, reinforcing India's position as a strategic cloud hub for public and private sector deployments.

India Government Cloud Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Components Covered | Solutions, Services |

| Deployment Models Covered | Hybrid Cloud, Private Cloud, Public Cloud |

| Service Models Covered | Infrastructure as a Service, Platform as a Service, Software as a Service |

| Applications Covered | Server and Storage, Disaster Recovery/ Data Backup, Security and Compliance, Analytics, Content Management, Others |

| Regions Covered | North India, South India, East India, West India |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Government Cloud Market Report

The India government cloud market size was valued at USD 1,585.89 Million in 2025.

The India government cloud market is expected to grow at a compound annual growth rate of 12.58% from 2026-2034 to reach USD 4,776.20 Million by 2034.

Services dominated the market with a share of 56.0%, driven by growing government demand for managed services, cloud consulting, and system integration to support digital transformation across central and state government departments.

Key factors driving the India government cloud market include the Digital India initiative, rising demand for data sovereignty, expanding e-governance platforms, increasing cybersecurity requirements, and the need for scalable cloud infrastructure to support citizen-centric public service delivery.

Major challenges include cybersecurity vulnerabilities, complex legacy IT migration processes, shortage of cloud-skilled public sector talent, regulatory compliance complexities, and uneven digital infrastructure development across different Indian states and regions.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade