India Green Hydrogen Market Size, Share, Trends and Forecast by Technology, Application, Distribution Channel, and Region, 2026-2034

India Green Hydrogen Market Size, Share, Trends & Forecast (2026-2034)

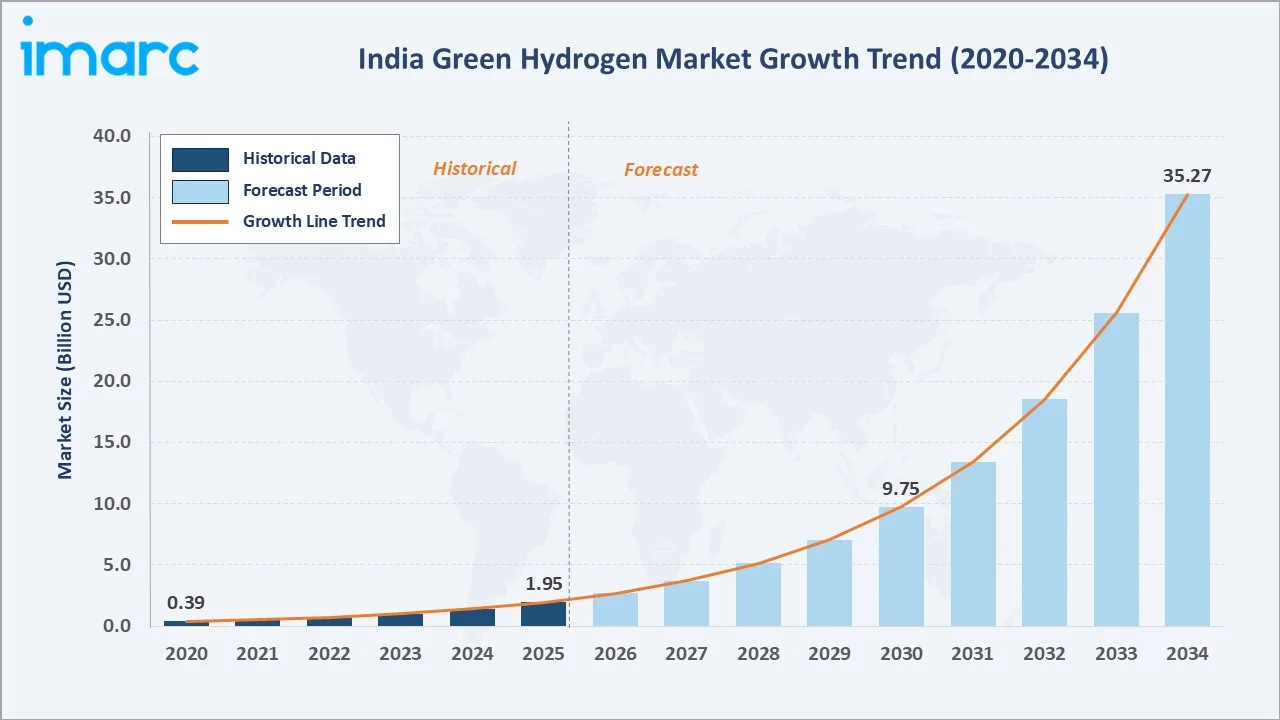

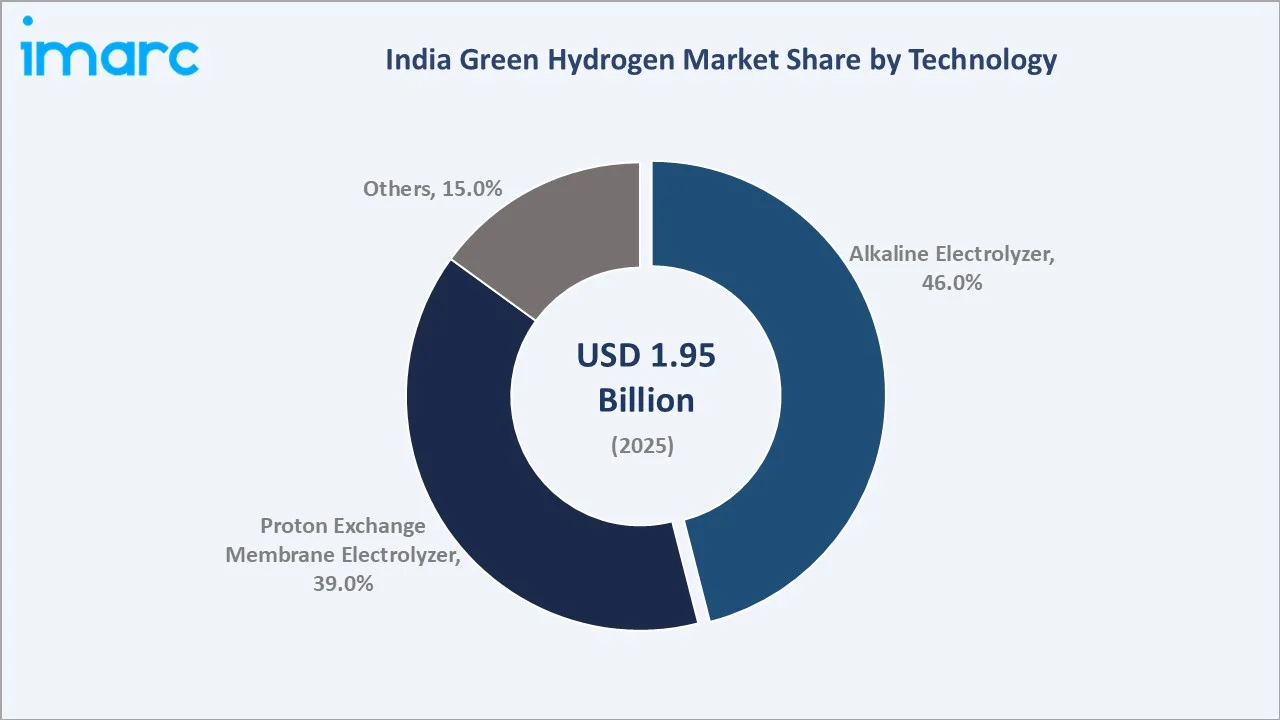

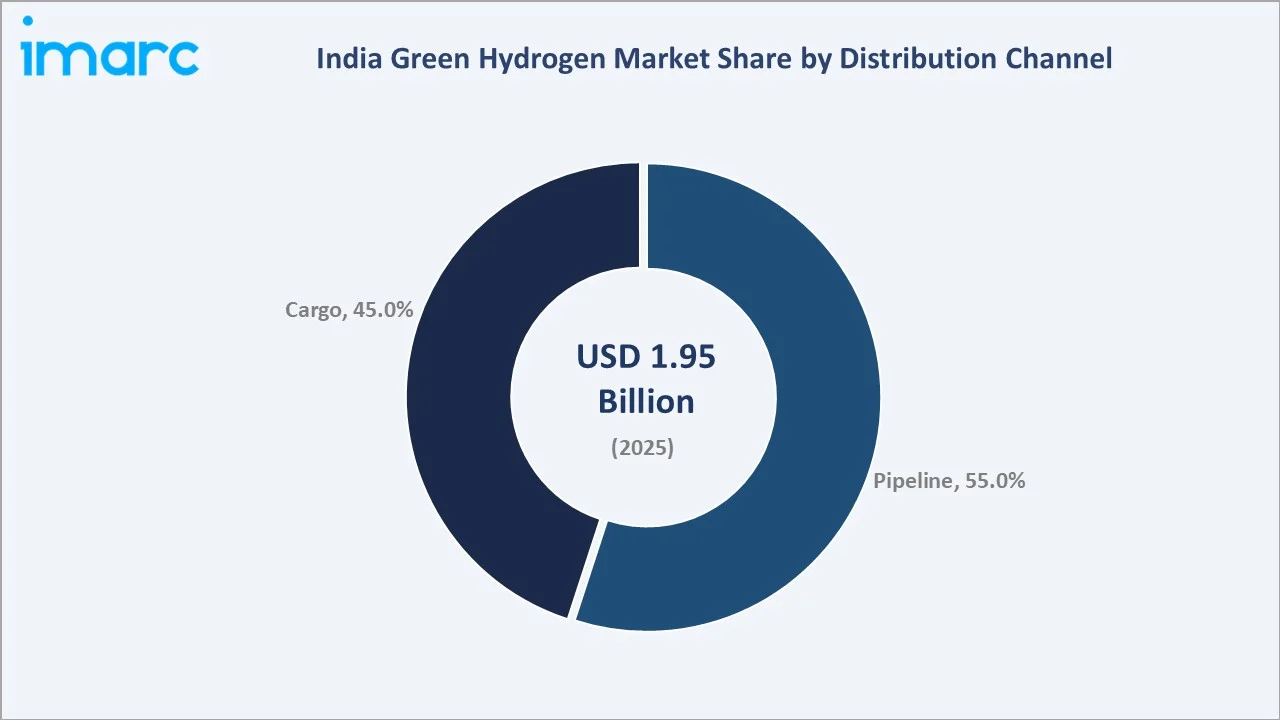

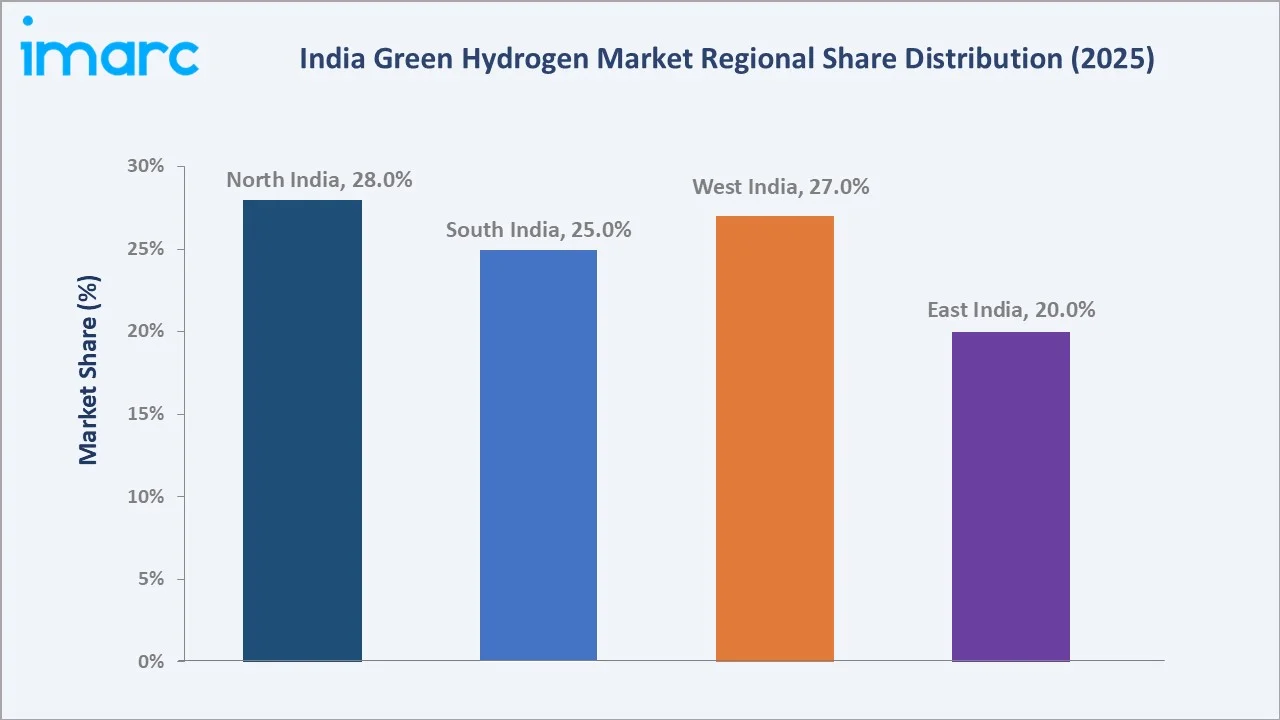

The India green hydrogen market reached USD 1.95 Billion in 2025 and is projected to reach USD 35.27 Billion by 2034, growing at a CAGR of 37.92% during 2026-2034. The market is driven by robust government policy under the National Green Hydrogen Mission (NGHM), falling renewable energy costs, and industrial decarbonisation demand across refining, fertilizers, steel, and heavy transport sectors. India has set an ambitious target of producing 5 Million Metric Tonnes (MMT) of green hydrogen annually by 2030, backed by a government outlay of INR 19,744 crore (approx. USD 2.4 Billion). Alkaline Electrolyzer dominates technology at 46.0% (2025). Pipeline leads distribution at 55.0%. North India commands 28.0% of national market share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 1.95 Billion |

|

Forecast Market Size (2034) |

USD 35.27 Billion |

|

CAGR (2026-2034) |

37.92% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Technology |

Alkaline Electrolyzer (46.0%, 2025) |

|

Leading Distribution Channel |

Pipeline (55.0%, 2025) |

|

Leading Region |

North India (28.0%, 2025) |

India green hydrogen market expanded from USD 0.39 Billion in 2020 to USD 1.95 Billion in 2025, anchored at USD 9.75 Billion in 2030, and forecast to reach USD 35.27 Billion by 2034. India's market is commercially unique among global green hydrogen markets, combining one of the world's most policy-driven clean energy transitions, a rapidly scaling electrolyzer manufacturing base, and a vast industrial decarbonisation demand from fertilizer, refining, and steel sectors representing captive replacement of existing grey hydrogen consumption estimated at approx. 6 MMT annually.

To get more information on this market, Request Sample

The PEM Electrolyzer segment grows fastest through India's hydrogen mobility program and the operational flexibility advantages of PEM systems for variable renewable energy integration. Cargo distribution grows above-market as decentralized hydrogen demand from refueling stations and industrial parks without pipeline access expands. South India is projected to grow fastest regionally, driven by the Andhra Pradesh Green Hydrogen Hub backed by USD 21.6 Billion investment under NTPC leadership.

Executive Summary

India green hydrogen market at USD 1.95 Billion in 2025 stands at the beginning of exponential commercial scale. India's National Green Hydrogen Mission (NGHM), approved in January 2023, targets 5 MMT annual green hydrogen production by 2030 with 125 GW dedicated renewable energy capacity, positioning India among the top three global green hydrogen producers within this decade. The market is commercially distinguished from other Asian green hydrogen markets by its extraordinary policy depth, private sector investment ambition exceeding USD 50 Billion in committed capital, and cost deflation trajectory in solar-powered electrolysis that makes India's green hydrogen production among the most competitive globally.

The market is projected to reach USD 35.27 Billion by 2034. Alkaline Electrolyzer at 46.0% leads through proven industrial maturity. Pipeline at 55.0% reflects infrastructure pathway dominance. North India leads regionally at 28.0%.

Key Market Insights

|

Insight |

Data |

|

Dominant Technology |

Alkaline Electrolyzer - 46.0% share (2025) |

|

Leading Distribution Channel |

Pipeline - 55.0% market share (2025) |

|

Leading Region |

North India - 28.0% share (2025) |

|

Market Opportunity |

Export hubs in Andhra Pradesh & Gujarat; green ammonia for Europe/Japan offtake; hydrogen refueling corridors for heavy transport; electrolyzer giga-factory investment |

Key Analytical Observations Supporting the Above Data:

- Alkaline Electrolyzer at 46.0%: The alkaline electrolyzer segment dominates due to its proven technology maturity, lower capital cost per MW compared to PEM alternatives, and proven suitability for large-scale continuous hydrogen production at refineries and fertilizer plants. Its established global supply chain and growing domestic manufacturing capability through NTPC Green Energy and Reliance New Energy further strengthen its position as India's primary near-term green hydrogen production technology.

- Pipeline at 55.0%: Pipeline distribution dominates due to the existing natural gas pipeline network operated by GAIL India and city gas distribution operators providing natural pathways for hydrogen blending at 5-20% concentrations. GAIL and Torrent Power are executing hydrogen blending pilots. Dedicated hydrogen pipeline corridors are under development for industrial clusters in Gujarat and Andhra Pradesh, sustaining pipeline's distribution leadership through 2034.

- North India at 28.0%: North India dominates regionally due to the concentration of major refinery demand centers (Mathura, Panipat), proximity to NGHM-supported hydrogen hub development, and Rajasthan's globally competitive solar irradiance enabling low-cost green hydrogen production. The region also benefits from strong industrial demand from fertilizer plants in Uttar Pradesh and Punjab, creating a high-volume captive green hydrogen offtake market.

India Green Hydrogen Market Overview

India green hydrogen market is commercially positioned at a critical strategic intersection: one of the world's most ambitious national clean energy missions, rapidly declining electrolysis and renewable energy costs, and industrial sectors facing mandatory decarbonisation under India's Nationally Determined Contributions (NDCs) committed at COP26. India has committed to achieving net-zero emissions by 2070 and reducing emissions intensity by 45% from 2005 levels by 2030, with green hydrogen identified as the cornerstone technology for hard-to-abate sectors across chemicals, steel, refining, and heavy transport.

India green hydrogen ecosystem integrates renewable energy developers, domestic electrolyzer manufacturers, industrial hydrogen consumers, distribution infrastructure operators, and export terminal developers into a complex and rapidly evolving industrial value chain. Macroeconomic factors driving this ecosystem include government SIGHT incentive scheme allocating production and manufacturing incentives to numerous companies, and private sector investment commitments from Reliance Industries Ltd., Adani Group, ACME Group, and Larsen & Toubro (L&T) creating a commercially credible scale trajectory.

Market Dynamics

To evaluate market opportunities, Request Sample

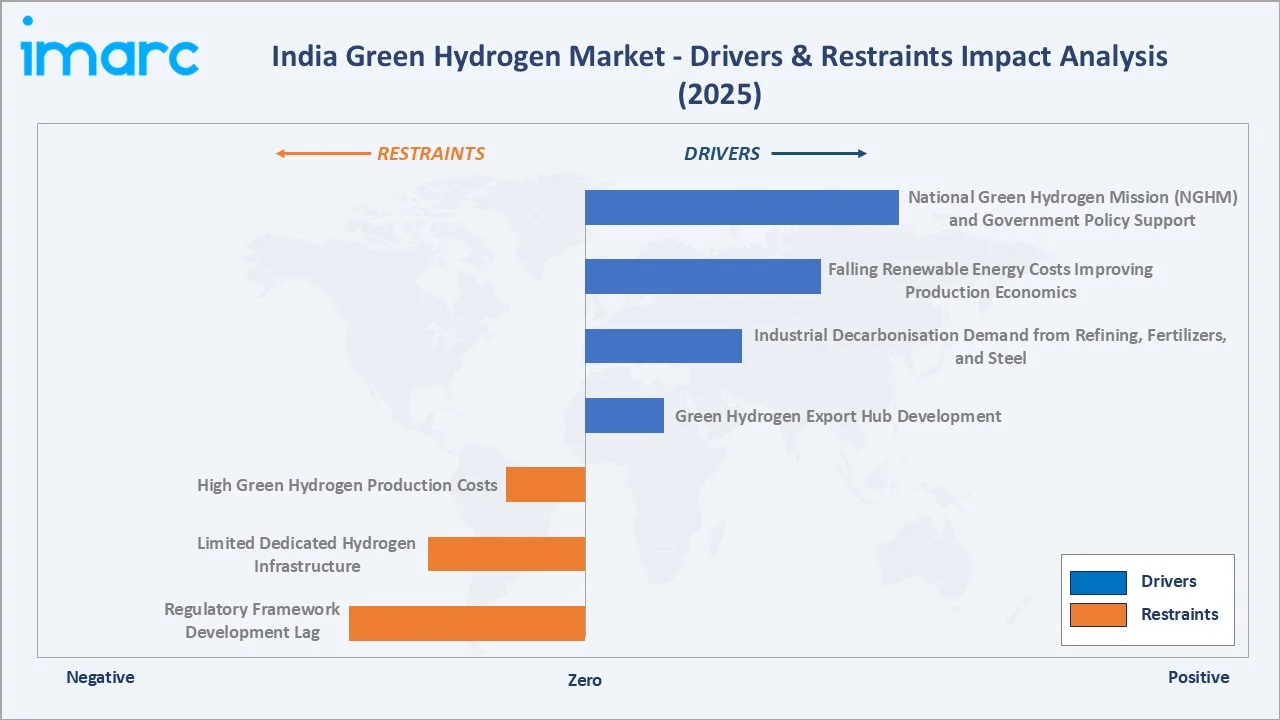

Market Drivers

- National Green Hydrogen Mission (NGHM) and Government Policy Support: The NGHM, approved by the Government of India with a financial outlay of INR 19,744 crore, targets 5 MMT per annum green hydrogen production and 125 GW dedicated renewable capacity by 2030. By January 2025, India announced its first dedicated green hydrogen hub in Andhra Pradesh backed by a USD 21.6 Billion investment, led by NTPC Green Energy Ltd. targeting 20 GW renewable capacity and 1,500 tonnes per day of green hydrogen production.

- Falling Renewable Energy Costs Improving Production Economics: India's solar tariffs have declined in recent auctions, directly improving green hydrogen production economics, as electricity represents 60-70% of total production cost. India's combination of globally competitive solar irradiance in Rajasthan and Gujarat with large-scale renewable procurement creates conditions for achieving the NGHM target of USD 1/kg green hydrogen production cost by 2030, versus the current USD 4-6/kg.

- Industrial Decarbonisation Demand from Refining, Fertilizers, and Steel: India's fertilizer industry consumes approximately 5-6 MMT of grey hydrogen annually, representing an immediate and high-volume replacement market for green hydrogen as production costs decline toward commercial viability. The steel sector is evaluating hydrogen-based direct reduced iron (DRI) technology as an emissions reduction pathway under Bureau of Energy Efficiency (BEE) mandates.

Market Restraints

- High Green Hydrogen Production Costs: Green hydrogen production costs remain at USD 4-6/kg in 2025, significantly above grey hydrogen at USD 1-2/kg, constraining near-term commercial offtake without policy subsidies. While SIGHT incentives partially bridge this gap, the cost differential requires sustained scale-up of both electrolyzer manufacturing and renewable energy deployment to achieve the government's USD 1/kg production cost target.

- Limited Dedicated Hydrogen Infrastructure: India's dedicated hydrogen storage, compression, and transport infrastructure remains nascent. Hydrogen blending in existing natural gas pipelines faces material compatibility and safety constraints limiting concentrations to 5-20%. Developing purpose-built hydrogen infrastructure requires capital investment estimated in hundreds of billions of dollars nationally, creating a near-term commercialization barrier for decentralized and mobility applications outside captive industrial clusters.

Market Opportunities

- Green Hydrogen Export Hub Development: India's geographic advantage in solar irradiance, coastal access, and low-cost land positions it as a globally competitive green hydrogen and green ammonia exporter to Japan, South Korea, and European Union markets, which have committed to large-scale clean hydrogen imports. Adani New Industries Ltd. plans to invest over USD 50 Billion over the next decade, targeting 1 MMT annual green hydrogen production capacity by 2030 primarily for export. ACME Group has secured long-term green ammonia export agreements with international buyers, establishing India's first export-grade green hydrogen derivative supply chain.

- Electrolyzer Manufacturing Localization and Cost Reduction: India's SIGHT scheme allocation of 3,000 MW electrolyzer manufacturing capacity to 15 domestic companies creates a structural opportunity for cost reduction through localization, reducing dependence on imported European and Chinese electrolyzers. In January 2026, Reliance Industries launched its first pilot low-cost electrolyzer manufacturing plant, targeting scalable production of modular electrolyzers designed to reduce green hydrogen production costs below USD 1/kg. L&T's electrolyzer manufacturing capability and technology partnerships with global OEMs further strengthen India's domestic supply chain development trajectory.

Market Challenges

- Regulatory Framework Development Lag: Comprehensive regulatory standards for hydrogen blending limits in pipelines, safety protocols for hydrogen storage and handling, and frameworks for cross-border green hydrogen trade remain in active development. The PNGRB (Petroleum and Natural Gas Regulatory Board) is developing hydrogen-specific pipeline regulations expected by 2026, but interim regulatory uncertainty creates project approval delays and investment risk for first-mover developers operating without settled compliance frameworks.

- Skilled Workforce Shortage in Electrolyzer Operations: India's green hydrogen industry faces a structural shortage of skilled professionals in electrolyzer operations, hydrogen safety management, fuel cell engineering, and high-purity hydrogen quality control. Industry-academia partnerships between IITs, NITs, and NGHM project developers are being established, but the workforce development timeline lags behind the rapid capacity deployment schedule, creating operational capability constraints for early commercial projects scaling through 2027-2028.

Emerging Market Trends

1. Electrolyzer Manufacturing Localization Creating India's Most Commercially Strategic Green Hydrogen Cost Advantage

India is rapidly developing domestic electrolyzer manufacturing capability that reduces import dependence and creates a structural cost advantage for Indian green hydrogen projects. The SIGHT scheme's allocation of 3,000 MW electrolyzer manufacturing capacity drives investment in local technology development and supply chain localization. In January 2026, Reliance Industries launched its pilot low-cost electrolyzer plant targeting modular production below USD 1/kg hydrogen cost. L&T, through international technology partnerships, is scaling PEM electrolyzer production for both domestic projects and potential export. This localization trend is India's most commercially significant green hydrogen cost deflation mechanism through 2030.

2. Hydrogen Blending in City Gas Distribution Networks Creating India's First Mass-Market Green Hydrogen Deployment Pathway

Hydrogen blending in city gas distribution (CGD) networks represents India's most commercially accessible near-term green hydrogen deployment pathway, leveraging existing pipeline infrastructure operated by GAIL India and CGD network operators. In August 2025, Torrent Power inaugurated Uttar Pradesh's first green hydrogen pilot plant in Gorakhpur, blending hydrogen with natural gas in its CGD network - India's first operational urban hydrogen blending project. KPI Green Energy commissioned a 1 MW green hydrogen plant in Bharuch in 2025, demonstrating distributed production viability. GAIL India is executing hydrogen blending pilots across multiple CGD zones, establishing the technical knowledge base and regulatory precedent for network-scale hydrogen integration through 2027.

3. Green Ammonia and Green Methanol Export Markets Creating India's Highest Near-Term Green Hydrogen Revenue Stream

Green ammonia, the most commercially ready green hydrogen derivative, represents India's highest near-term revenue opportunity from green hydrogen production, as international buyers in Japan, South Korea, and Europe seek long-term supply contracts at volumes India is uniquely positioned to fulfill. ACME Group secured international green ammonia export agreements, pioneering India's export-grade supply chain. Torrent Power committed INR 7,200 crore to establish a 100 KTPA green ammonia facility in Gujarat targeting European offtake buyers. The green methanol pathway for maritime fuel is gaining traction as global shipping decarbonisation mandates create additional demand channels for Indian green hydrogen derivatives.

4. Private Sector Mega-Investment Programs Transforming India's Green Hydrogen Market from Policy-Driven to Commercially-Driven

India's green hydrogen market is experiencing a structural transition from policy-driven early projects to commercially motivated mega-investment programs by India's largest industrial conglomerates. Adani Group's commitment to invest over USD 50 Billion over the next decade, with 1 MMT annual production target by 2030, represents the single largest private green hydrogen investment program globally by any Indian entity.

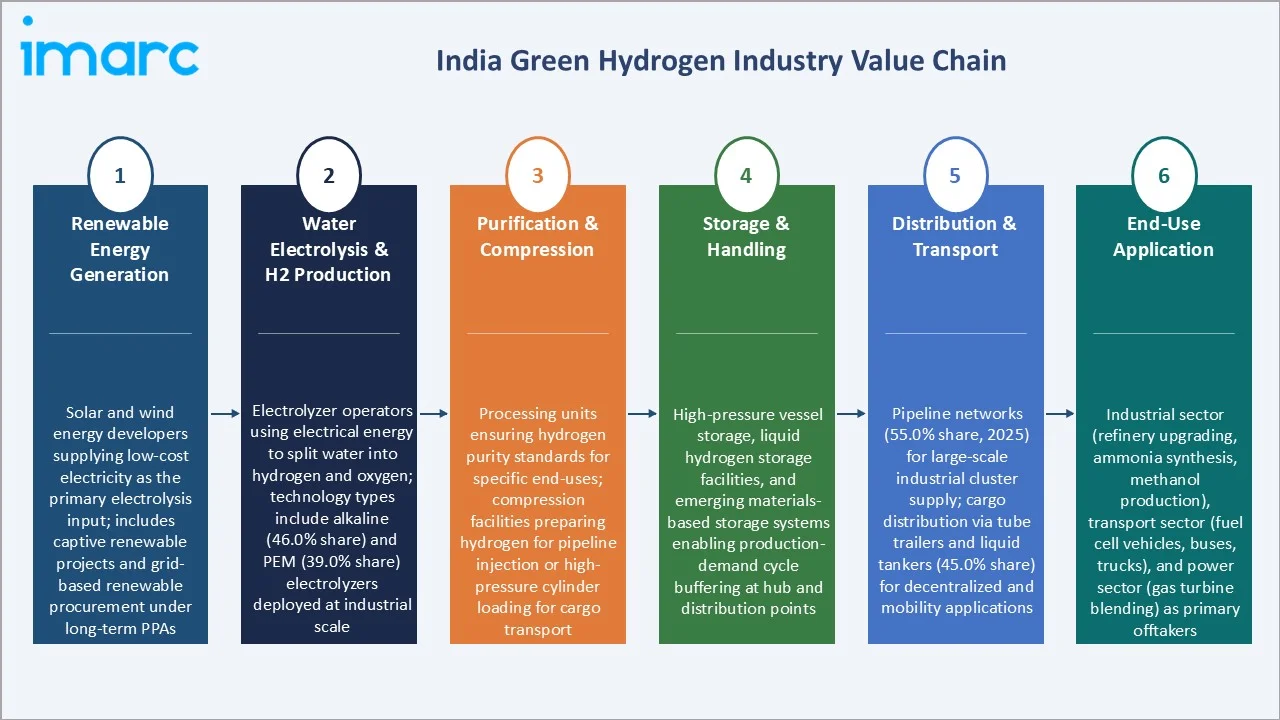

Industry Value Chain Analysis

India green hydrogen value chain is one of the most policy-shaped industrial value chains currently under construction in any emerging market. Each stage from renewable energy generation through final industrial or mobility application is being simultaneously developed through a combination of government mandates, SIGHT incentives, and private conglomerate investment, creating a unique parallel-development dynamic where upstream and downstream capabilities are scaling concurrently rather than sequentially.

|

Stage |

Key Participants |

|

Renewable Energy Generation |

Solar and wind energy developers supplying low-cost electricity as the primary electrolysis input; includes captive renewable projects and grid-based renewable procurement under long-term PPAs |

|

Water Electrolysis & H2 Production |

Electrolyzer operators using electrical energy to split water into hydrogen and oxygen; technology types include alkaline (46.0% share) and PEM (39.0% share) electrolyzers deployed at industrial scale |

|

Purification & Compression |

Processing units ensuring hydrogen purity standards for specific end-uses; compression facilities preparing hydrogen for pipeline injection or high-pressure cylinder loading for cargo transport |

|

Storage & Handling |

High-pressure vessel storage, liquid hydrogen storage facilities, and emerging materials-based storage systems enabling production-demand cycle buffering at hub and distribution points |

|

Distribution & Transport |

Pipeline networks (55.0% share, 2025) for large-scale industrial cluster supply; cargo distribution via tube trailers and liquid tankers (45.0% share) for decentralized and mobility applications |

|

End-Use Application |

Industrial sector (refinery upgrading, ammonia synthesis, methanol production), transport sector (fuel cell vehicles, buses, trucks), and power sector (gas turbine blending) as primary offtakers |

The electrolysis and production stage is India green hydrogen value chain's most commercially consequential investment stage in 2025, where domestic electrolyzer manufacturing capability under SIGHT incentives creates the foundational cost structure for the entire downstream value chain. With 15 companies awarded 3,000 MW of electrolyzer manufacturing capacity, India is building a domestic production capability that is projected to reduce electrolyzer capital cost by 40-60% through 2030, directly enabling the USD 1/kg green hydrogen production cost target of the NGHM.

Technology Landscape in the India Green Hydrogen Industry

Alkaline Electrolysis Technology

Alkaline electrolysis is the dominant green hydrogen production technology at 46.0% market share (2025), characterized by proven long-term operational reliability exceeding 80,000 hours, lower capital cost per MW (USD 500-900/kW in 2025) compared to PEM alternatives, and established suitability for large-scale continuous production at refineries, ammonia plants, and industrial hydrogen hubs. NTPC Green Energy has deployed advanced alkaline electrolyzer systems, including a 1.70 MW solar-powered alkaline electrolyzer with integrated battery energy storage at its pilot facility. The alkaline technology's robustness in continuous-operation industrial settings makes it India's preferred technology for the high-volume captive replacement of grey hydrogen in existing industrial facilities.

Proton Exchange Membrane (PEM) Electrolysis

PEM electrolyzer technology holds 39.0% market share (2025) and is growing at the fastest rate due to superior dynamic response capability enabling rapid ramp-up and ramp-down matching renewable energy intermittency, compact footprint, and high purity output (99.999%) suitable for fuel cell mobility and precision industrial applications. Siemens Energy and Cummins India are among the active PEM technology suppliers to Indian project developers.

Advanced Hydrogen Storage and Distribution Technologies

Pipeline distribution at 55.0% (2025) dominates India's green hydrogen transport infrastructure, leveraging the 18,400+ km natural gas transmission network operated by GAIL India as a co-transport medium for hydrogen blending. Research into liquid organic hydrogen carriers (LOHC) for long-distance and export transport is advancing through IIT-industry partnerships. The development of dedicated hydrogen pipeline corridors under NGHM infrastructure investment planning post-2026 will create a next-generation transport infrastructure layer for large-scale hub-to-industrial-cluster supply. KPI Green Energy's 1 MW Bharuch plant and Torrent Power's Gorakhpur blending project are establishing the operational knowledge base for scaling these distribution technologies through 2034.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Technology |

Alkaline Electrolyzer |

46.0% |

2025 |

|

Application |

Transport |

40.0% |

2025 |

|

Distribution Channel |

Pipeline |

55.0% |

2025 |

|

Region |

North India |

28.0% |

2025 |

By Technology

Alkaline Electrolyzer leads at 46.0% (2025). The segment serves India's largest near-term green hydrogen demand centers - fertilizer plants requiring continuous large-volume hydrogen supply, refinery upgrading applications, and green ammonia export projects where uninterrupted production is commercially essential. Alkaline's established global supply chain and growing domestic manufacturing under SIGHT incentives reinforce its dominant position through the medium-term forecast horizon.

To access detailed market analysis, Request Sample

Proton Exchange Membrane (PEM) Electrolyzer at 39.0% (2025) is the fastest-growing technology segment through India's expanding hydrogen mobility program, fuel cell vehicle adoption, and the operational flexibility advantages of PEM systems for variable solar and wind generation integration. Others (15.0%) includes Solid Oxide Electrolysis (SOE) at early pre-commercial stage and anion exchange membrane (AEM) systems in R&D phase at academic and national laboratory settings. SIGHT scheme technology-neutral incentive structure ensures all electrolyzer types benefit from production-side support, maintaining healthy technology diversity in India's green hydrogen production landscape.

By Distribution Channel

Pipeline leads at 55.0% (2025). India's existing natural gas transmission and city gas distribution network creates an immediate, low-capital-intensity pathway for green hydrogen transport through blending. The PNGRB is developing hydrogen-specific pipeline regulations targeting finalization in 2026, which will formalize the commercial and technical framework for higher-concentration hydrogen pipeline transport beyond current blending limits. Dedicated hydrogen pipeline corridors planned under NGHM for industrial hub supply in Gujarat and Andhra Pradesh will sustain pipeline's distribution dominance through 2034.

Cargo at 45.0% (2025) serves decentralized demand including hydrogen refueling stations, industrial parks without pipeline access, and export terminal loading operations. Compressed hydrogen tube trailers (200-500 bar) and cryogenic liquid hydrogen tankers are the primary cargo modalities currently deployed. IOC's planned hydrogen refueling station network and NTPC's hydrogen mobility projects in Leh drive near-term cargo distribution volume growth.

Regional Market Insights

|

Region |

Share (2025) |

Key India Green Hydrogen Market Drivers & Characteristics |

|

North India |

28.0% |

Driven by proximity to major refinery demand centers (Mathura, Panipat), Rajasthan's globally competitive solar irradiance for low-cost production, and NGHM-supported hydrogen hub development. High-volume captive offtake from fertilizer plants in Uttar Pradesh and Punjab anchors near-term commercial deployment. |

|

West India |

27.0% |

Gujarat's established petrochemical and chemical industrial base creates significant green hydrogen demand; Mundra and Kandla ports support export logistics; Torrent Power's 100 KTPA green ammonia project in Bharuch drives regional investment. Strong solar resource in Gujarat enables competitive production economics. |

|

South India |

25.0% |

Andhra Pradesh hosts India's first dedicated green hydrogen hub (USD 21.6 Billion, NTPC-led) targeting 1,500 TPD production; Tamil Nadu and Karnataka wind resources support competitive costs; Karnataka and Telangana's industrial base creates chemical and refinery demand. |

|

East India |

20.0% |

Jharkhand and Odisha's steel industry represents a strategic hydrogen-for-DRI demand center; JSW Group's hydrogen-for-steelmaking integration drives West Bengal and Odisha investment; Kolkata port enables export potential for green ammonia and green methanol derivatives. |

North India's 28.0% market leadership reflects the concentration of existing grey hydrogen consumption in large refineries at Mathura (IOC) and Panipat (IOC), which collectively represent India's largest single-location captive green hydrogen replacement market. Rajasthan's solar irradiance among the highest globally at 5.5-6.0 kWh/m2/day creates India's lowest-cost renewable electricity foundation for electrolyzer operation.

South India's 25.0% reflects the transformative scale of the Andhra Pradesh Green Hydrogen Hub, which is India's single largest green hydrogen investment commitment and will fundamentally reshape the regional distribution of production capacity through 2030. East India's 20.0% is the most commercially developing region, but projected to grow above national CAGR as JSW Group's steel sector hydrogen integration, Odisha's industrial investment, and West Bengal's port infrastructure create first-generation green hydrogen demand from sectors that have no near-term decarbonisation alternative to hydrogen.

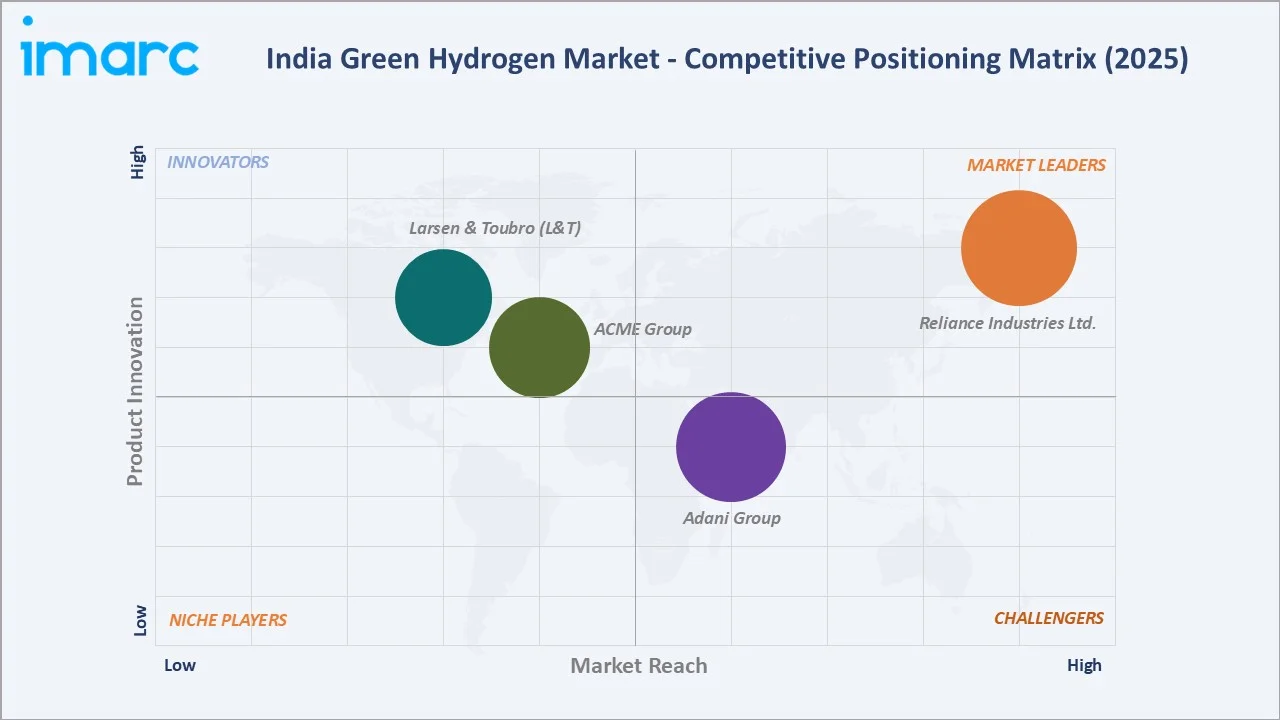

Competitive Landscape

India green hydrogen market competitive landscape exhibits moderate-to-high competitive intensity with major public sector undertakings (PSUs) and private conglomerates competing across the value chain. The market's early commercial stage means competitive differentiation is driven by access to renewable energy resources, electrolyzer technology partnerships, SIGHT incentive allocation, government project relationships, and industrial offtake contracts rather than purely by production scale or market share. Competition is intensifying as SIGHT incentive allocations create formal market entry points and NGHM mandates drive procurement programs across PSU refineries, fertilizer plants, and mobility infrastructure operators.

|

Company |

Key Brands / Subsidiary |

Market Position |

Core Strength |

|

Reliance Industries Ltd. |

Reliance New Energy Limited (RNEL) |

Market Leader |

5,000-acre Dhirubhai Ambani Green Energy Giga Complex, massive captive renewable energy, strategic global technology partnerships |

|

Adani Group |

Adani New Industries Limited (ANIL) |

Strong Challenger |

USD 50 Billion-decade commitment, 1 MTPA target by 2030, port infrastructure advantage |

|

ACME Group |

ACME Cleantech Solutions Private Limited |

Innovator |

Pioneer green ammonia export agreements; SIGHT production capacity allocation; international offtake secured with European and Asian buyers |

|

Larsen & Toubro (L&T) |

L&T Energy GreenTech (LTEG) |

Innovator |

EPC leadership for green H2 plants; SIGHT manufacturing capacity allocation |

The competitive landscape's most commercially significant dynamic is the PSU-private partnership model emerging as India's preferred green hydrogen project structure, where PSU credibility and government relationships combine with private capital efficiency and technology access. Apart from the private entities, some of the significant PSUs present in the India green hydrogen industry include, NTPC Limited, Indian Oil Corporation Limited (IOCL), Oil & Natural Gas Corporation (ONGC), GAIL (India) Limited, and others.

Key Company Profiles

Reliance Industries Ltd.

Reliance Industries Ltd., which operates in the sector through RNEL, is India's largest private sector company by market capitalization, with diversified operations spanning petrochemicals, refining, oil and gas exploration, retail, and telecommunications. Through its New Energy vertical, Reliance is executing a major clean energy pivot targeting 3 million tonnes of annual green hydrogen production by 2032 through integrated giga-factories combining renewable energy, electrolyzer manufacturing, and hydrogen storage.

- Key Initiatives: Giga-factory for solar module, electrolyzer, and battery manufacturing at Jamnagar, Gujarat; integration of captive solar and wind generation; hydrogen mobility solutions development

- Recent Developments: In August 2025, Reliance Industries announced during its 48th Annual General Meeting the target to reach a production capacity of 3 million tonnes of green hydrogen by 2032. The company plans to manufacture electrolysers in-house at its Dhirubhai Ambani Giga Energy Complex in Jamnagar, Gujarat.

- Strategic Focus: Become India's largest private green hydrogen producer by 2032; develop domestic electrolyzer manufacturing at giga-scale to create cost-competitive supply chain; target both domestic industrial offtake and global clean energy export markets.

Adani Group

Adani Group, through Adani New Industries Ltd. (ANIL), is one of India's most ambitious green hydrogen investors with a commitment exceeding USD 50 Billion in clean energy investment over the next decade. The group's integrated platform combining renewable energy, port infrastructure, and industrial operations creates a uniquely vertically-integrated green hydrogen and green ammonia export capability.

- Key Initiatives: Integrated renewable energy-to-hydrogen-to-ammonia production platform; SIGHT incentive allocations for both electrolyzer manufacturing and hydrogen production; port infrastructure at Mundra for export logistics

- Recent Developments: In June 2025, Adani New Industries (ANIL) commissioned country’s first off-grid 5MW green hydrogen pilot plant in Gujarat. The plant is powered by 100% solar energy and integrated with a battery storage system.

- Strategic Focus: Develop India as a cost-competitive green hydrogen and green ammonia export hub; integrate hydrogen production into existing Adani Group ports, energy, and industrial infrastructure; leverage conglomerate scale for vertically-integrated cost advantage.

ACME Group

ACME Group is a leading Indian renewable energy company that has emerged as India's pioneer in the green ammonia export value chain. The company has secured international offtake agreements, SIGHT production capacity allocations, and positioned itself as the first-mover in commercial-scale green hydrogen derivative exports, establishing India's earliest revenue-generating export green hydrogen project track record.

- Key Initiatives: Green hydrogen-to-ammonia conversion projects targeting international export markets; secured SIGHT incentive scheme production capacity; developed long-term offtake partnerships with European and Asian buyers

- Strategic Focus: Pioneer India's green ammonia export industry and establish first-mover advantage in international long-term offtake relationships; leverage captive renewable energy assets to maximize production cost competitiveness; scale toward 1 MTPA green ammonia capacity.

Market Concentration Analysis

India green hydrogen market is currently characterized by moderate-to-high fragmentation at the project development stage, with no single company commanding dominant production market share in 2025 as most capacity remains in pilot or early commercial phase. The top players - Reliance Industries Ltd., Adani Group, ACME Group, and Larsen & Toubro (L&T)- collectively represent the overwhelming majority of SIGHT incentive allocations and committed capital, though numerous companies hold SIGHT production allocations totaling 862,000 MTPA, creating a deliberately distributed market development structure by government design.

Market concentration is evolving through two structural forces operating simultaneously: PSU anchor demand consolidation, where NTPC and IOC's large-scale industrial projects create concentrated production centers at refinery and hub locations, and private conglomerate investment competing for the same renewable energy and industrial off-taker relationships in an emerging market where first-mover position is commercially decisive. Consolidation is expected in electrolyzer manufacturing as technology scale effects and cost deflation favor larger integrated producers, while green hydrogen distribution infrastructure will consolidate around GAIL India's pipeline network dominance and Adani Ports' export terminal advantage. The SIGHT scheme's allocation across numerous companies reflects the government's deliberate strategy of avoiding single-company dependence while ensuring commercially credible market development scale.

Investment & Growth Opportunities

Highest Growth Segments

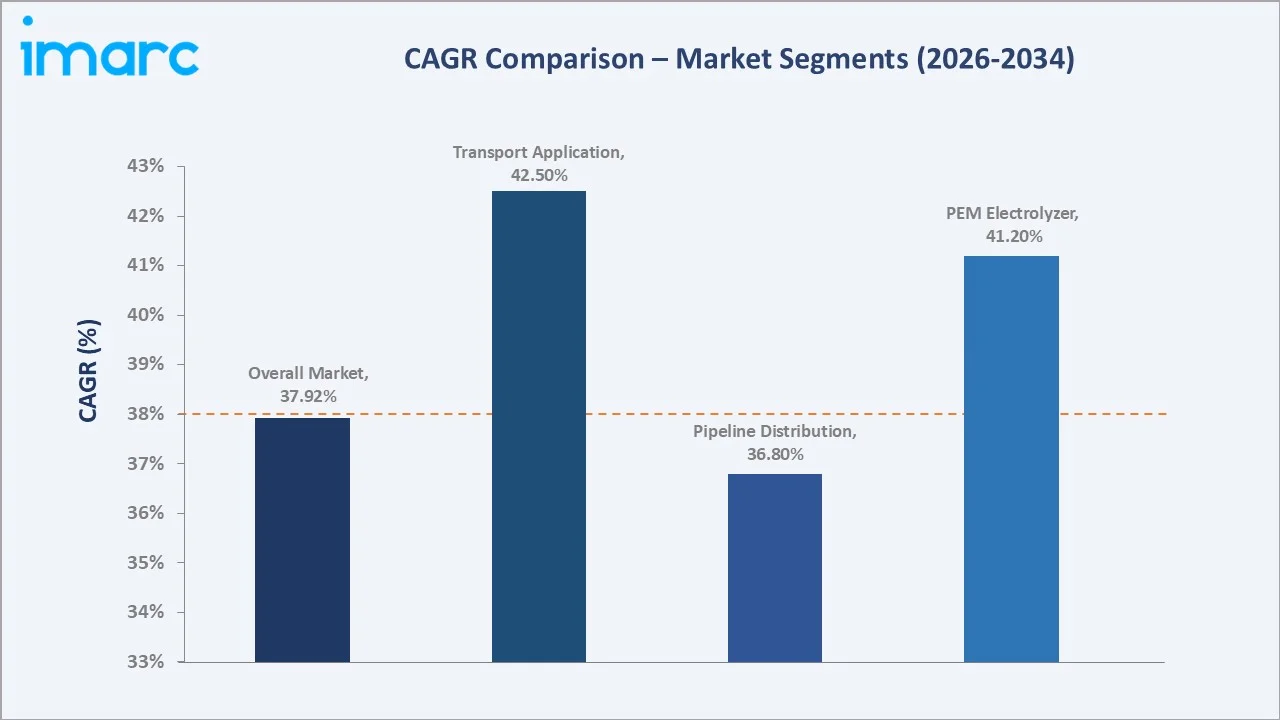

Transport application (~42% CAGR through hydrogen fuel cell commercial vehicle adoption), PEM electrolyzer technology (~41% CAGR through mobility and variable renewable integration demand), green ammonia derivative exports (~45-50% CAGR from early base), and South India regional market (~40%+ CAGR through Andhra Pradesh hub development) represent India's highest-growth green hydrogen investment vectors through 2034. Electrolyzer manufacturing localization under SIGHT scheme represents the highest-return manufacturing investment given SIGHT incentive support and India's cost deflation trajectory toward globally competitive domestic electrolyzer production costs.

Emerging Investment Opportunities

India's certified green hydrogen derivative market - green ammonia and green methanol for maritime and chemical applications - growing at above-50% CAGR from early 2025 base, represents the highest near-term revenue opportunity for investors with international offtake relationship access. Hydrogen storage technology - particularly liquid organic hydrogen carriers (LOHC) and advanced high-pressure vessel manufacturing - presents an early-stage but strategically essential investment as India scales toward export-grade hydrogen volumes requiring specialized carrier solutions. Hydrogen safety equipment, monitoring systems, electrolyzer maintenance services, and specialized engineering capabilities represent infrastructure-adjacent investment opportunities with lower capital intensity and earlier cash flow generation than primary production projects.

Investment Themes

- Electrolyzer Giga-factory Investment: Domestic electrolyzer manufacturing at gigawatt scale reduces import dependence and creates India's green hydrogen cost advantage; Reliance and L&T are leading this investment theme with SIGHT support, creating technology partnership, joint venture, and supply chain investment opportunities for international electrolyzer OEMs seeking India market access.

- Green Hydrogen Export Terminal Infrastructure: Port-integrated green ammonia and green methanol production facilities in Gujarat (Mundra/Kandla) and Andhra Pradesh (Krishnapatnam/Gangavaram) targeting 25-year offtake contracts with European and Asian energy importers; Adani Group and ACME provide investable platform structures for international institutional capital seeking India green hydrogen exposure.

Future Market Outlook (2026-2034)

India green hydrogen market is projected to grow from USD 1.95 Billion in 2025 to USD 35.27 Billion by 2034, delivering a 37.92% CAGR over the forecast period. The market's anchor value of USD 9.75 Billion in 2030 represents the NGHM milestone year - when India targets 5 MMT annual green hydrogen production capacity, significant export hub operationalization, and hydrogen mobility infrastructure deployment at national scale. This trajectory positions India alongside Germany, Australia, and Chile as a tier-one global green hydrogen economy, with India uniquely combining the world's largest domestic industrial decarbonisation demand market with globally competitive solar-powered production economics.

Three structural forces define India green hydrogen market growth through 2034. Policy depth and multi-decade continuity: NGHM's cross-ministry coordination structure, SIGHT financial incentives, and India's international climate commitments create investment certainty that provides commercial foundation for long-term project financing at scale. Cost trajectory compounding: India's solar cost deflation, electrolyzer localization under SIGHT, and production scale-up collectively drive production costs from USD 4-6/kg in 2025 toward USD 1-2/kg by 2030, unlocking industrial and export demand at commercial scale. Export market creation: Japan's hydrogen import strategy, Europe's REPowerEU clean hydrogen import targets, and South Korea's hydrogen economy roadmap create structured international demand that India's geography and cost position uniquely enable it to serve.

Research Methodology

Primary Research

Primary research comprised structured interviews with India green hydrogen industry stakeholders, including project development leads at NTPC Green Energy, Reliance New Energy, and ACME Group; electrolyzer technology providers and international OEM representatives; government officials from MNRE, MoPNG, and DPIIT; and policy analysts covering India's NGHM framework. Industrial buyer surveys were conducted with refinery procurement managers, fertilizer plant operations heads, and mobility fleet decision-makers across North, West, South, and East India.

Secondary Research

Secondary research encompassed NGHM policy documents and SIGHT scheme allocation data from MNRE; Ministry of Petroleum and Natural Gas hydrogen policy publications; PNGRB regulatory consultation documents; company annual reports and investor presentations from NTPC, Reliance Industries, GAIL India, and IOC; and SIGHT incentive award notifications. International sources included IEA Global Hydrogen Review 2024, IRENA Green Hydrogen Cost Outlook, Hydrogen Council Hydrogen Insights, and COP28 NDC hydrogen commitment documentation. Over 60 secondary sources reviewed.

Forecasting Models

Market revenue forecasts were developed using a bottom-up electrolyzer deployment model: MW of installed electrolyzer capacity by year multiplied by capacity utilization factor and conversion efficiency, yielding tonnes of green hydrogen production, priced at projected production cost curves derived from solar LCOE forecasts and electrolyzer capital cost deflation trajectories benchmarked against IRENA and BloombergNEF modelling. Demand-side validation used industrial sector decarbonisation models for refining, fertilizer, steel, and transport sectors benchmarked against NGHM production targets and SIGHT capacity allocation schedules.

India Green Hydrogen Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Technologies Covered | Proton Exchange Membrane Electrolyzer, Alkaline Electrolyzer, Others |

| Applications Covered | Power Generation, Transport, Others |

| Distribution Channels Covered | Pipeline, Cargo |

| Regions Covered | North India, South India, East India, West India |

| Companies Covered | Reliance Industries Ltd., Adani Group, ACME Group, Larsen & Toubro (L&T), etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Green Hydrogen Market Report

India green hydrogen market reached USD 1.95 Billion in 2025, driven by NGHM policy support, falling solar tariffs below INR 2/kWh, and growing industrial decarbonisation demand across refining, fertilizers, and steel sectors.

India green hydrogen market grows at 37.92% CAGR during 2026-2034, driven by NGHM mandates, SIGHT incentives, USD 50+ Billion private sector investment, and expanding export hub development targeting Japan and European offtake.

Alkaline Electrolyzer leads at 46.0% (2025) through proven operational maturity, lower capital cost, and suitability for large-scale continuous industrial hydrogen production at refineries and ammonia synthesis plants.

India green hydrogen market is projected to reach USD 9.75 Billion by 2030, the NGHM milestone year targeting 5 MMT annual production capacity and significant export hub operationalization in Andhra Pradesh and Gujarat.

Pipeline leads at 55.0% (2025), leveraging India's existing 18,400+ km natural gas network for hydrogen blending and dedicated industrial cluster corridors under NGHM infrastructure development post-2026.

North India leads with 28.0% (2025), driven by major refinery demand centers in Mathura and Panipat, Rajasthan's competitive solar costs, and NGHM-supported hydrogen hub proximity for captive industrial offtake.

India green hydrogen market is projected to reach USD 35.27 Billion by 2034, growing at 37.92% CAGR through electrolyzer capacity expansion, production cost deflation to USD 1-2/kg, and export market development.

Leading companies include Reliance Industries Ltd., Adani Group, ACME Group, and Larsen & Toubro (L&T), among others, competing across production, manufacturing, and distribution segments.

Primary drivers include NGHM policy framework, solar tariffs below INR 2/kWh enabling low-cost production, SIGHT scheme incentivizing numerous companies, industrial decarbonisation mandates, and export market demand from Europe and Japan.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)