India Haircare Market Size, Share, Trends and Forecast by Product Type, Distribution Channel, and Region, 2026-2034

India Haircare Market Summary:

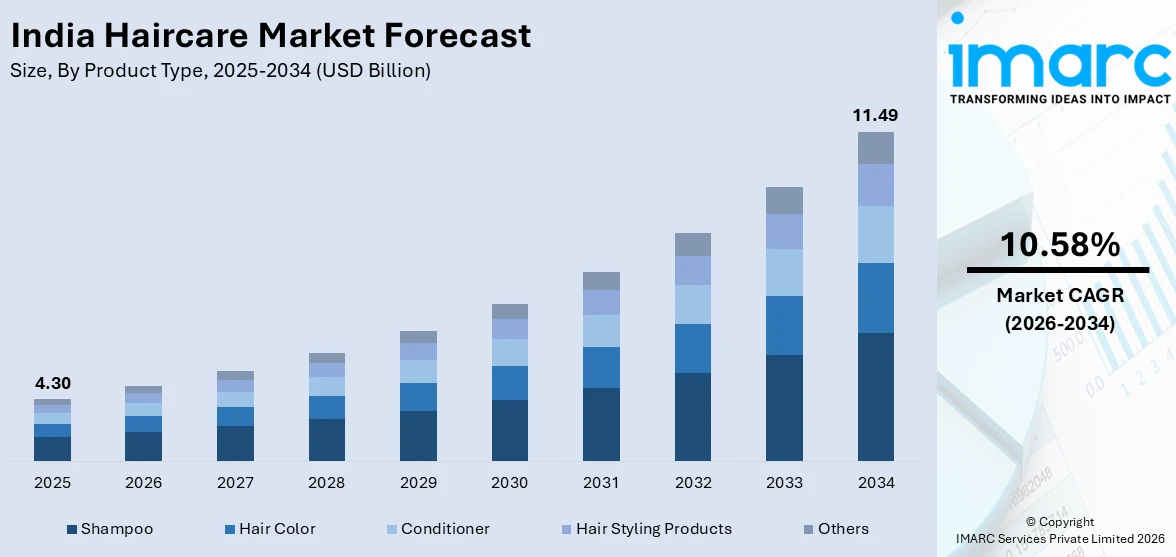

The India haircare market size was valued at USD 4.30 Billion in 2025 and is projected to reach USD 11.49 Billion by 2034, growing at a compound annual growth rate of 10.58% from 2026-2034.

The India haircare market is experiencing robust expansion driven by rising consumer consciousness around personal grooming and hair health. Growing disposable incomes, rapid urbanization, and an expanding middle class are fueling demand for premium, specialized, and natural haircare solutions. The increasing influence of social media platforms and digital beauty content is reshaping consumer purchasing behavior across urban and rural markets. Additionally, the cultural affinity toward Ayurvedic and herbal formulations continues to strengthen product innovation, positioning India as a dynamic hub for diverse haircare offerings and bolstering the India haircare market share.

Key Takeaways and Insights:

- By Product Type: Shampoo dominates the market with a share of 45.0% in 2025, driven by its essential role in daily grooming routines and the growing availability of specialized formulations addressing diverse hair concerns.

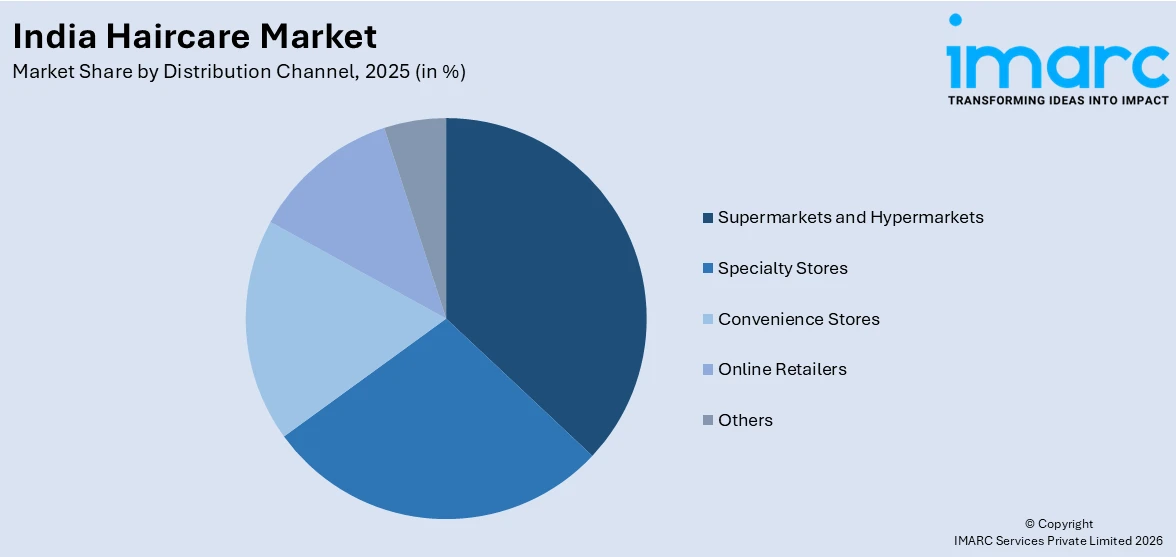

- By Distribution Channel: Supermarkets and hypermarkets lead the market with a share of 37.0% in 2025, supported by one-stop shopping convenience, broad product assortments, and attractive promotional offers appealing to price-conscious consumers.

- By Region: West and Central India represent the largest segment with a market share of 33.0% in 2025, fueled by strong purchasing power in metropolitan centers, well-established retail infrastructure, and high consumer awareness of premium haircare products.

- Key Players: The India haircare market features a moderately competitive landscape characterized by a mix of established multinational corporations and emerging domestic players. Companies are leveraging Ayurvedic positioning, digital marketing strategies, and product innovation to capture evolving consumer preferences across diverse price segments.

To get more information on this market Request Sample

The India haircare market is advancing as consumer preferences evolve toward scientifically formulated and naturally derived products. Urbanization across tier-2 and tier-3 cities is broadening the consumer base, while digital platforms are enabling new brands to reach wider audiences through direct-to-consumer models. The convergence of traditional Ayurvedic wisdom with modern cosmetic science is creating a distinctive product innovation ecosystem. For instance, in February 2024, Tata Elxsi collaborated with Dabur International to revamp the Vatika Haircare range, introducing eco-conscious packaging that reduces plastic use by 15% per pack and greenhouse gas emissions by 20%, demonstrating the industry’s commitment to sustainability-led growth. The expanding salon culture and growing male grooming segment further reinforce long-term market momentum, while government support through AYUSH initiatives continues to encourage natural product development and formulation standardization.

India Haircare Market Trends:

Rising Demand for Natural and Ayurvedic Haircare Solutions

Indian consumers are increasingly shifting toward natural, organic, and Ayurvedic haircare formulations, moving away from chemical-based products due to heightened awareness of ingredient safety and long-term hair health. Herbal ingredients such as amla, bhringraj, hibiscus, and onion oil are gaining widespread acceptance across age groups. This cultural alignment with traditional wellness practices is driving brands to develop plant-based solutions and clean beauty offerings. For instance, in October 2024, Dabur India Limited finalized a merger agreement with Sesa Care Private Limited, acquiring a 51% stake for Rs 12.59 Crore to strengthen its position in the Ayurvedic haircare category, reflecting the industry’s strategic focus on herbal product portfolios.

Premiumization and Science-Driven Formulations

The market is witnessing a decisive shift from basic cleansing products toward advanced treatment-led value growth, with consumers increasingly investing in specialized formulations offering targeted solutions for damage repair, scalp health, and hair strength. Premium and professional-grade products are gaining traction particularly in metropolitan markets where consumers prioritize ingredient quality and proven efficacy over price considerations. For instance, in September 2025, K Formula launched India’s first peptide-based molecular haircare brand, debuting with a six-step peptide repair ritual priced between Rs 700 and Rs 1,500, reflecting the India haircare market growth toward science-backed innovation.

Skinification of Haircare and Scalp-Centric Routines

The concept of treating the scalp as an extension of skin is fundamentally reshaping haircare routines in India. Consumers are adopting multi-step regimens incorporating scalp exfoliating scrubs, hydrating tonics, and barrier repair oils, moving beyond traditional one-product approaches. This trend is driven by growing awareness of the connection between scalp health and overall hair quality, influenced by dermatological education and digital beauty content. For instance, in August 2024, Mamaearth launched its Kerala Thaali hair care range, featuring hibiscus, shikakai, and amla through a partnership with Reliance Retail across the southern market, exemplifying the fusion of regional botanical traditions with modern scalp-care science.

Market Outlook 2026-2034:

The India haircare market is poised for sustained growth over the forecast period, driven by deepening consumer engagement with personal wellness, expanding digital commerce infrastructure, and continuous product innovation across natural and premium categories. The convergence of Ayurvedic heritage with advanced cosmetic science positions the market for accelerated value creation, while rising rural penetration and organized retail expansion broaden the accessible consumer base. Additionally, the increasing influence of social media trends and professional salon culture is further stimulating demand for specialized and high-performance haircare solutions. The market generated a revenue of USD 4.30 Billion in 2025 and is projected to reach a revenue of USD 11.49 Billion by 2034, growing at a compound annual growth rate of 10.58% from 2026-2034.

India Haircare Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

|

Product Type |

Shampoo |

45.0% |

|

Distribution Channel |

Supermarkets and Hypermarkets |

37.0% |

|

Region |

West and Central India |

33.0% |

Product Type Insights:

- Shampoo

- Hair Color

- Conditioner

- Hair Styling Products

- Others

Shampoo dominates with a market share of 45.0% of the total India haircare market in 2025.

Shampoo remains the cornerstone of India’s haircare industry, serving as an essential daily grooming product across urban and rural demographics. Its dominance is underpinned by the wide spectrum of formulations available, addressing specific concerns such as dandruff control, hair fall prevention, dryness management, and scalp sensitivity. The segment has evolved significantly from basic cleansing solutions to ingredient-centric products incorporating herbal, organic, and sulfate-free compositions. The affordability of sachet formats has enabled deep penetration into rural markets, making shampoo accessible across all economic segments.

Product innovation continues to drive segment growth, with brands introducing specialized variants targeting specific hair types and climate conditions. The rising popularity of herbal shampoos featuring ingredients like amla, bhringraj, shikakai, and neem reflects the broader consumer shift toward natural formulations. Additionally, the emergence of anti-pollution and scalp-health shampoos responds to growing urban environmental concerns. Premium shampoo variants with advanced technologies, such as keratin-infused and peptide-based formulations, are capturing market share in metropolitan markets where consumers seek salon-quality results at home.

Distribution Channel Insights:

Access the comprehensive market breakdown Request Sample

- Supermarkets and Hypermarkets

- Specialty Stores

- Convenience Stores

- Online Retailers

- Others

Supermarkets and hypermarkets lead with a share of 37.0% of the total India haircare market in 2025.

Supermarkets and hypermarkets maintain their position as the dominant distribution channel for haircare products in India, driven by their extensive geographic reach, comprehensive product assortments, and the one-stop shopping convenience they offer to consumers. These large-format retail establishments provide exposure to multiple brands and product categories under a single roof, enabling consumers to compare options and take advantage of promotional offers, bundle deals, and private-label alternatives. Their strategic locations in urban and suburban areas ensure accessibility to a broad consumer base, while organized in-store merchandising enhances product visibility and impulse purchases.

The trend of the steady growth of organized retail chains in the areas of tier-2 and 3 cities reinforces the status of the offline channel dominance in the Indian haircare market. Top retailers are also improving store format, developing super-sized beauty shops, and providing in-store consultations to elevate the shopping experience. The old and new trade outlets remain central to the distribution of FMCGs as they are supported by the high level of consumer trust and accessibility. The personal care category is the aspect of purchase that supermarkets and hypermarkets continue to dominate, with most individuals enjoying judging the packaging, fragrance, and texture of the product in person before making a purchase.

Regional Insights:

- North India

- West and Central India

- South India

- East and Northeast India

West and Central India represents the largest share at 33.0% of the total India haircare market in 2025.

West and Central India commands the leading position in the haircare market, anchored by the strong purchasing power of metropolitan centers such as Mumbai, Pune, and Ahmedabad. The region enjoys a well-developed modern retail system, such as high concentrations of supermarkets, hypermarkets, and specialty beauty shops that guarantee extensive product supply. The State of Maharashtra, which is the economic giant of the region, is a major proportion of the Indian FMCG environment that is characterized by the focal consumer demand and established retail channels. The urbanization factors and high levels of cosmopolitan and diverse lifestyles promote the high uptake of international and premium haircare brands. The availability of contemporary trade outlets, specialty beauty shops, and a strong presence of e-commerce indicate even further development of innovative and high-value haircare products within the state.

The region’s diverse consumer base encompasses both mass-market and premium segments, creating opportunities across the pricing spectrum. The presence of Bollywood and the entertainment industries in Mumbai significantly influences beauty and grooming trends, amplifying consumer interest in professional-grade and trendsetting haircare products. Additionally, the expanding salon culture and growing direct-to-consumer brand presence in the region contribute to sustained demand for innovative haircare solutions, from Ayurvedic formulations to science-backed treatments.

Market Dynamics:

Growth Drivers:

Why is the India Haircare Market Growing?

Expanding E-Commerce and Digital Distribution Channels

The rapid expansion of e-commerce platforms and digital retail infrastructure is transforming how Indian consumers discover and purchase haircare products. Online retail channels offer unparalleled product variety, competitive pricing, and the convenience of doorstep delivery, making specialized and premium haircare products accessible to consumers in smaller cities and rural areas. Digital platforms are enabling emerging direct-to-consumer brands to scale rapidly without the overhead costs associated with traditional distribution. Social media-driven product discovery and influencer marketing are reshaping purchasing decisions, particularly among younger demographics. Beauty e-commerce sales in India recorded approximately 39% of total sales between June and November 2024, demonstrating the channel’s growing importance. For instance, in January 2025, Mermade Hair, an Australian hair styling company, partnered with Tira, Reliance Retail’s omnichannel beauty platform, to launch its complete product collection in India, illustrating the increasing role of digital platforms in facilitating international brand entry into the Indian market.

Rising Urbanization and Consumer Grooming Awareness

India’s rapid urbanization is playing a pivotal role in driving haircare market expansion by enlarging the addressable consumer base and reshaping grooming preferences. The urban consumers are generally more brand-conscious, more experimental, and more demanding in terms of specialized solutions that address their concerns of hair fall, hair damage repair, and scalp health. The expanding middle class, because of rising income levels, is changing consumption habits towards basic hygiene items to holistic hair wellness regimes. Big urban centers are the major demand centers, and the new store format and online shopping platforms further stimulate the use of high-quality and value-added haircare products.

Government Support for Natural and Ayurvedic Product Innovation

Strong government support through policy frameworks and financial incentives is catalyzing innovation in the natural and Ayurvedic haircare segment. The promotion of traditional medicine systems through dedicated ministries and certification standards is building institutional foundations that encourage product development and quality assurance across the herbal haircare category. Programs supporting medicinal plant cultivation, entrepreneurship development in the AYUSH sector, and manufacturing standardization are creating a favorable ecosystem for natural haircare brands. The Union Budget 2025-26 increased the allocation for the Ministry of AYUSH to INR 3,992.90 Crore from INR 3,497.64 Crore in the previous year, demonstrating sustained policy commitment to traditional wellness industries. Additionally, India holds 7.3 million hectares under organic cultivation including aromatic and medicinal plants as reported by APEDA, ensuring a robust supply base for natural ingredients used in haircare formulations.

Market Restraints:

What Challenges the India Haircare Market is Facing?

Counterfeit and Unregulated Product Proliferation

The prevalence of counterfeit and unregulated haircare products poses a significant challenge to market growth and consumer safety. Spurious products undermine branded offerings through aggressive pricing, creating consumer confusion and eroding brand equity investments. Enforcement actions across Kerala, Maharashtra, and Telangana throughout 2024 revealed extensive networks of counterfeit cosmetics and unlicensed imports. Rural and semi-urban markets remain particularly vulnerable to counterfeit penetration due to limited regulatory oversight.

Rural Distribution Infrastructure Limitations

Fragmented distribution networks in rural India continue to restrict market penetration despite representing significant untapped demand. Infrastructure constraints including inadequate road connectivity, limited organized retail presence, and fragmented supply chains increase distribution costs and reduce product accessibility. These logistical challenges make it difficult for brands to ensure consistent product availability and freshness in remote areas, constraining the overall addressable market.

Intense Price Competition and Margin Pressures

Heightened competition among multinational corporations, domestic FMCG players, and emerging direct-to-consumer brands is intensifying pricing pressures across the haircare market. The need to maintain competitive pricing while investing in product innovation, quality ingredients, and marketing creates margin challenges, particularly for mid-tier brands. The dominance of price-sensitive consumer segments and the proliferation of private-label alternatives further compress profit margins across the value chain.

Competitive Landscape:

The India haircare market features a moderately concentrated competitive landscape characterized by balanced competition between established multinational corporations and agile domestic players. Leading multinationals leverage extensive distribution networks, brand equity, and research capabilities to maintain market leadership, while domestic companies capitalize on consumer insights, Ayurvedic positioning, and regional preferences. Emerging direct-to-consumer brands are disrupting traditional market dynamics through digital-first strategies, customized formulations, and social media engagement. Companies are focusing on premiumization, sustainable packaging, ingredient transparency, and product portfolio diversification to strengthen market positioning and capture evolving consumer preferences across urban and rural segments.

Recent Developments:

- In May 2025, Hindustan Unilever introduced Nexxus in India, expanding its portfolio in the prestige and professional beauty segment. The launch features Protein Transfusion Technology, which delivers proteins and lipids to the hair cortex for damage repair, strengthening hair and improving smoothness from the first application.

- In February 2025, Karmic Beauty launched a luxury haircare line featuring up to 91.8% naturally derived ingredients, including USDA-certified organic Moroccan Argan Oil and 92% pure hydrolysed keratin. The brand holds ECOCERT and IFRA certifications and emphasizes sustainability through eco-friendly packaging.

India Haircare Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Shampoo, Hair Color, Conditioner, Hair Styling Products, Others |

| Distribution Channels Covered | Supermarkets and Hypermarkets, Specialty Stores, Convenience Stores, Online Retailers, Other |

| Regions Covered | North India, West and Central India, South India, East and Northeast India |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Haircare Market Report

The India haircare market size was valued at USD 4.30 Billion in 2025.

The India haircare market is expected to grow at a compound annual growth rate of 10.58% from 2026-2034 to reach USD 11.49 Billion by 2034.

Shampoo held the largest revenue share of 45.0% in 2025, driven by its essential role in daily grooming routines, versatile formulations addressing diverse hair concerns, and deep penetration across both urban and rural markets through affordable sachet formats.

Key factors driving the India haircare market include expanding e-commerce infrastructure, rising urbanization and disposable incomes, growing demand for natural and Ayurvedic formulations, increasing influence of social media on grooming behavior, and supportive government policies promoting traditional wellness industries.

Major challenges include the proliferation of counterfeit and unregulated products, fragmented rural distribution infrastructure, intense price competition compressing profit margins, regulatory compliance complexities, and the need to balance affordable pricing with quality innovation.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)