India HDPE Pipes Market Size, Share, Trends, and Forecast by Type, Application, and Region, 2026-2034

India HDPE Pipes Market Size, Share, Trends & Forecast (2026-2034)

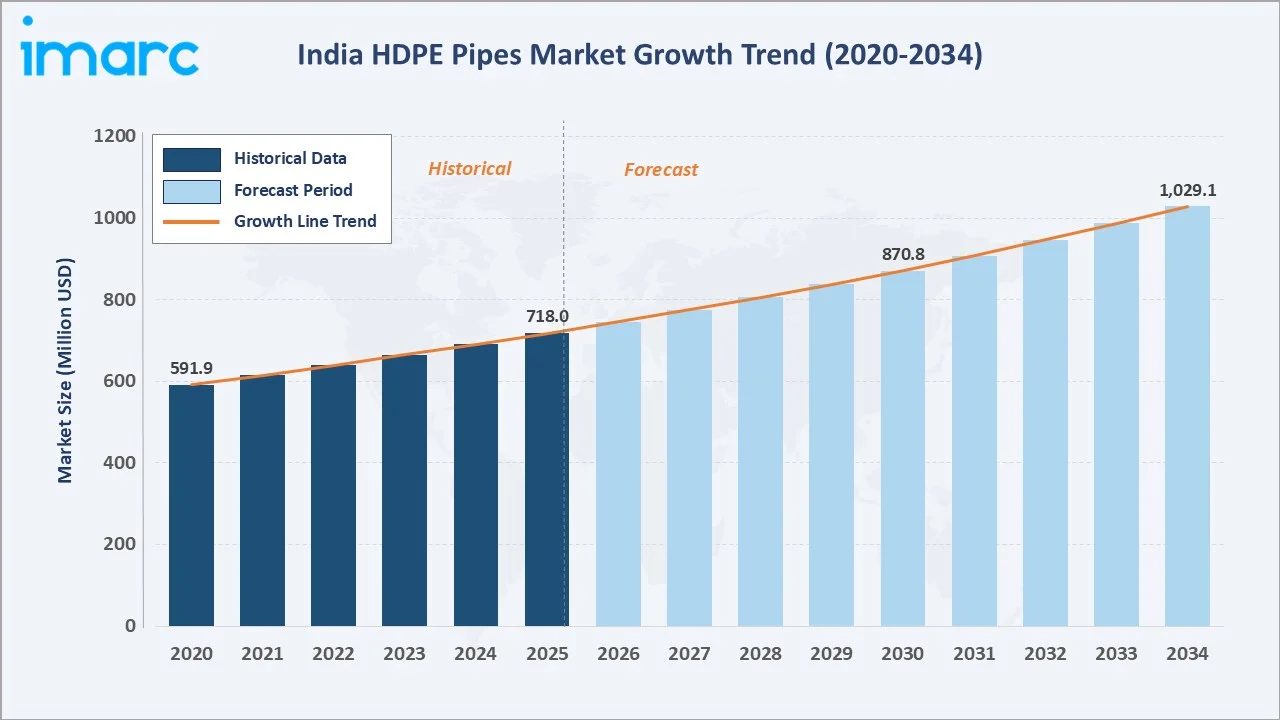

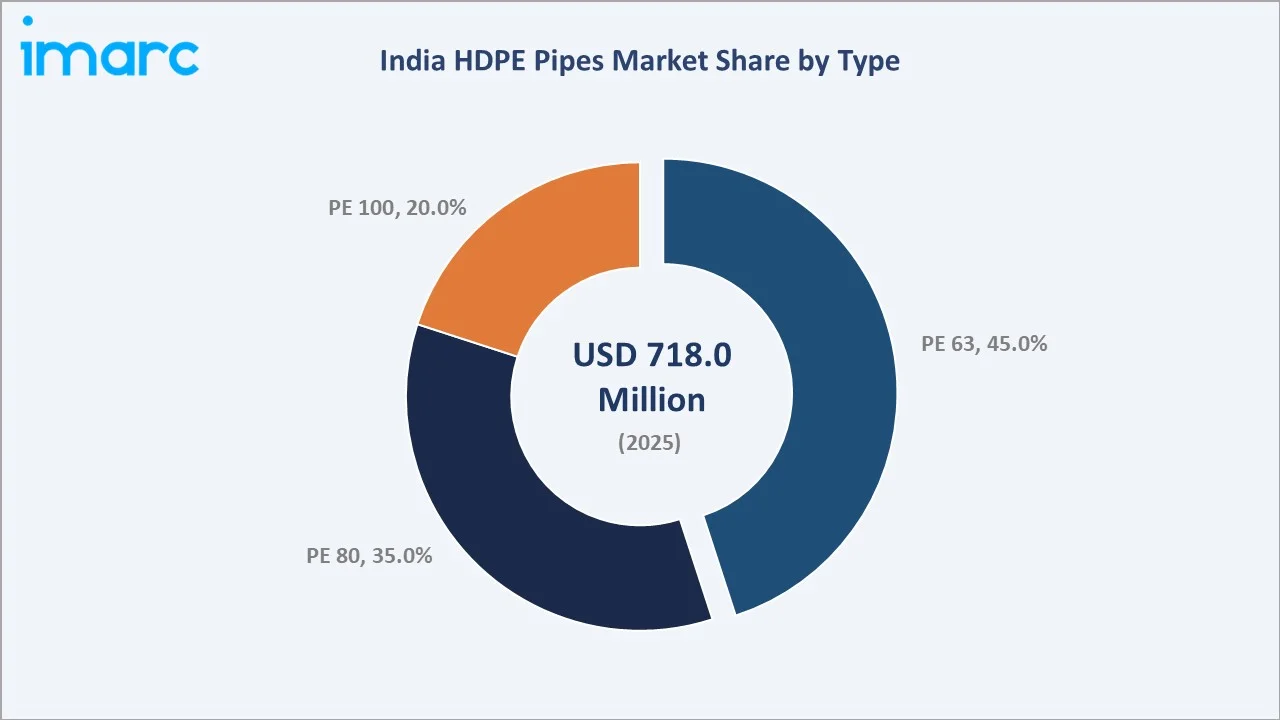

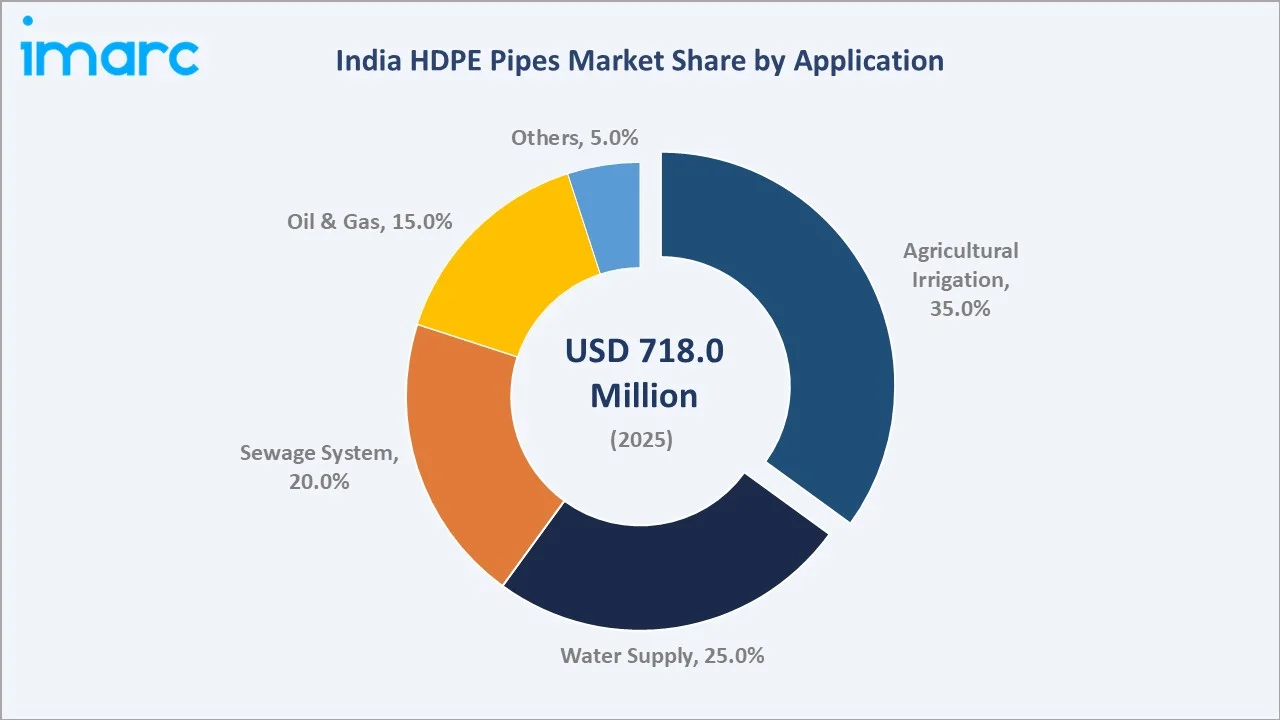

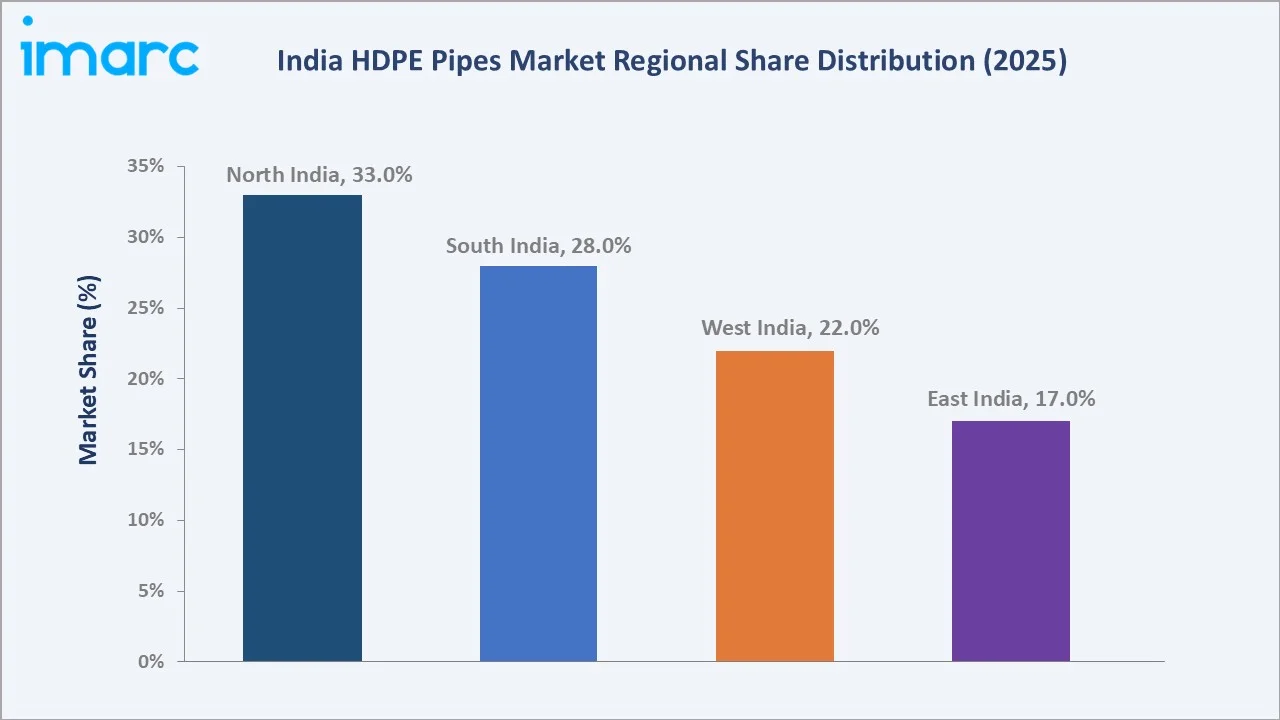

The India HDPE pipes market was valued at USD 718.0 Million in 2025 and is projected to reach USD 1,029.1 Million by 2034, expanding at a CAGR of 3.94% during the forecast period (2026-2034). Growth is anchored by the Jal Jeevan Mission (JJM)’s INR 3.60 lakh crore water infrastructure program, PM Krishi Sinchayee Yojana (PMKSY) agricultural irrigation expansion, PNGRB city gas distribution network development, and systematic replacement of aging GI, CI, and AC pipes with HDPE. PE 63 leads with 45% type share, agricultural irrigation dominates application at 35%, and North India commands 33% regional share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 718.0 Million |

|

Forecast Market Size (2034) |

USD 1,029.1 Million |

|

CAGR (2026-2034) |

3.94% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Region |

North India (33.0%, 2025) |

|

Fastest Growing Region |

South India (CAGR ~4.3%, 2026-2034) |

The India HDPE pipes market growth expanded from USD 591.9 Million in 2020 to USD 718.0 Million in 2025, anchored by Jal Jeevan Mission procurement and post-COVID infrastructure restart. Anchored at USD 870.8 Million in 2030, the forecast to USD 1,029.1 Million by 2034, driven by India’s USD 1.4 Trillion National Infrastructure Pipeline and progressive replacement of aging galvanized iron and cement asbestos pipelines nationwide.

To get more information on this market, Request Sample

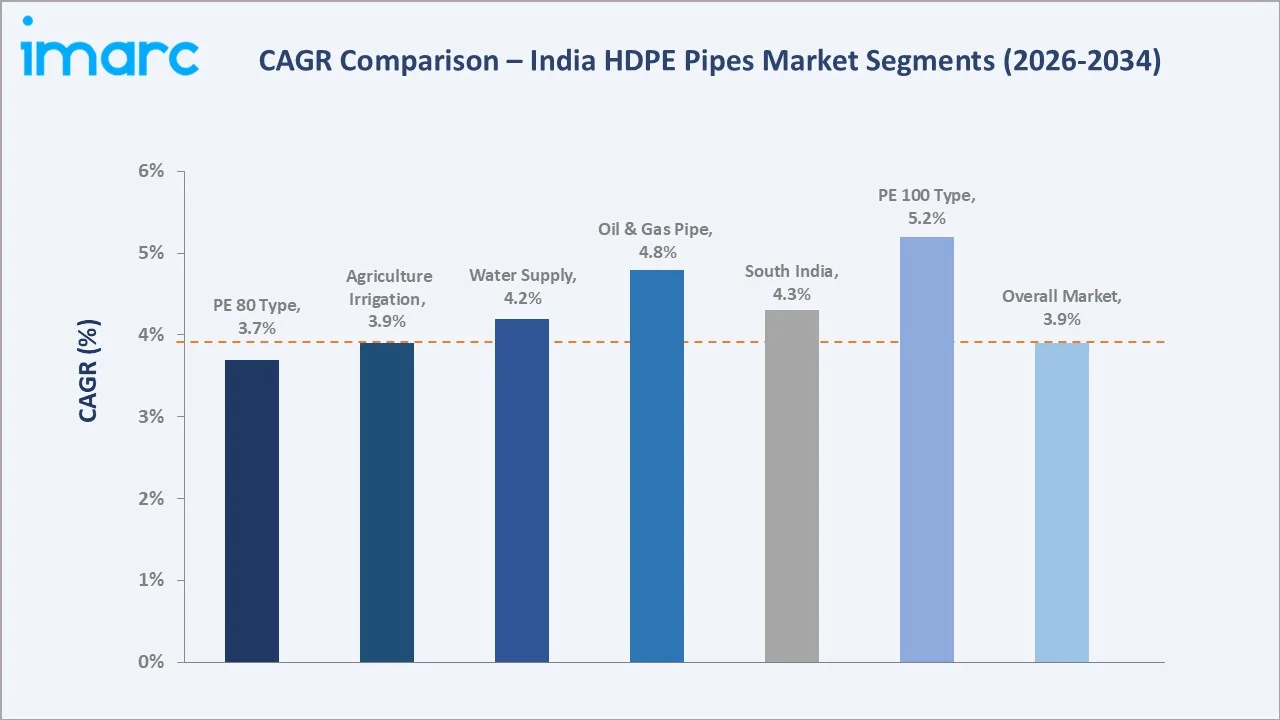

The CAGR across key segments with PE 100 at ~5.2% CAGR grows fastest by type, reflecting its superior pressure rating (PN 16 and above), longer 50-year design life, and mandatory specification for AMRUT 2.0 water distribution networks and city gas distribution pipelines. South India, at ~4.3% CAGR, grows fastest regionally, driven by Tamil Nadu, Karnataka, and Andhra Pradesh’s accelerated Jal Jeevan Mission implementation and South India’s canal irrigation upgrade programs.

Executive Summary

The India HDPE pipes market has grown from USD 591.9 Million in 2020 to USD 718.0 Million in 2025, sustained through COVID-19’s construction and project execution disruptions, the 2022 HDPE resin price surge linked to crude oil volatility, and supply chain normalization challenges. This growth trajectory is anchored by three programs of unparalleled infrastructure scale: the Jal Jeevan Mission (JJM)’s mandate to deliver piped water to all 193.5 million rural households, which consumed a high amount of HDPE pipes and the PM Krishi Sinchayee Yojana’s drip and sprinkler irrigation expansion, accelerating the demand for HDPE lateral pipes. The market’s 3.94% CAGR forecast to USD 1,029.1 Million by 2034 reflects this sustained government-demand anchor supplemented by growing urban sewage infrastructure demand from India’s Smart City Mission and AMRUT 2.0 programs.

PE 63’s 45% dominance reflects its dominant role in agricultural irrigation. India’s farming households accessing PMKSY drip irrigation subsidies predominantly install PE 63 micro-irrigation lateral pipes at 20–60mm diameter. PE 80 at 35% serves water supply and medium-pressure applications, while PE 100 at 20% is growing fastest at ~5.2% CAGR, driven by PNGRB city gas distribution network expansion and large-diameter urban water transmission main applications requiring higher pressure resistance. Agricultural irrigation leads application at 35%, serving India’s agricultural holdings with PMKSY-subsidized drip and sprinkler infrastructure.

North India’s 33% dominance reflects the Indo-Gangetic Plain of irrigated agricultural land and Rajasthan-UP-Haryana’s JJM rural water supply mega-projects. South India, at 28%, captures Tamil Nadu, Karnataka, AP, and Telangana’s combination of agricultural HDPE demand, Jal Jeevan Mission implementation, and PNGRB city gas distribution network expansion. The South India market is growing fastest at ~4.3% CAGR, driven by Tamil Nadu and Andhra Pradesh’s aggressive JJM implementation timelines and IGL-equivalent city gas expansion.

Key Market Insights

|

Insight |

Data |

|

Dominant Type |

PE 63 – 45.0% revenue share (2025) |

|

Dominant Application |

Agricultural Irrigation – 35.0% revenue share (2025) |

|

Leading Region |

North India – 33.0% revenue share (2025) |

|

Fastest Growing Region |

South India (CAGR ~4.3%, 2026-2034) |

Key Analytical Observations Supporting the Above Data:

- PE 63 at 45% (2025) sustained by agricultural irrigation volume: India’s PMKSY Har Khet Ko Pani scheme targets micro-irrigation coverage, consuming high PE 63 HDPE lateral pipes for drip emitter lines and sprinkler sub-mains.

- Agricultural irrigation at 35% (2025) underpinned by PM-KUSUM and PMKSY: PM-KUSUM (Pradhan Mantri Kisan Urja Suraksha evam Utthaan Mahabhiyan)’s 34,800 MW solar pump component requires HDPE drip irrigation pipes for solar pump installations.

- North India at 33% reflecting Indo-Gangetic agricultural and JJM concentration: Uttar Pradesh’s JJM program, India’s largest state JJM project at 2.63 crore rural household connections, driving the demand for HDPE pipes.

India HDPE Pipes Market Overview

High-Density Polyethylene (HDPE) pipes are thermoplastic pressure pipes manufactured from HDPE resin by continuous extrusion, classified into three performance grades, PE 63, PE 80, and PE 100, based on minimum required strength (MRS) per ISO 9080 standards. PE 63 (MRS 6.3 MPa) serves low-pressure agricultural irrigation; PE 80 (MRS 8.0 MPa) serves water supply and medium-pressure applications; PE 100 (MRS 10.0 MPa) serves high-pressure city gas distribution, large-diameter water transmission, and critical infrastructure. HDPE pipes are governed by BIS IS 4984 (agricultural and general), IS 14333 (water supply and sewage), and IS 4427 (city gas distribution) standards in India.

India’s HDPE pipe ecosystem encompasses domestic HDPE resin producers, pipe manufacturers, BIS certification bodies, and government procurement agencies. HDPE pipe’s 50-year+ service life, corrosion immunity, chemical resistance, flexibility, and superior hydraulic efficiency drive systematic replacement of GI, CI, and AC pipes across India’s water infrastructure estate. Macroeconomic drivers include JJM water infrastructure budget, PMKSY agricultural irrigation funds, PNGRB CGD authorizations, and India’s GDP-linked construction and infrastructure investment growth.

Market Dynamics

To evaluate market opportunities, Request Sample

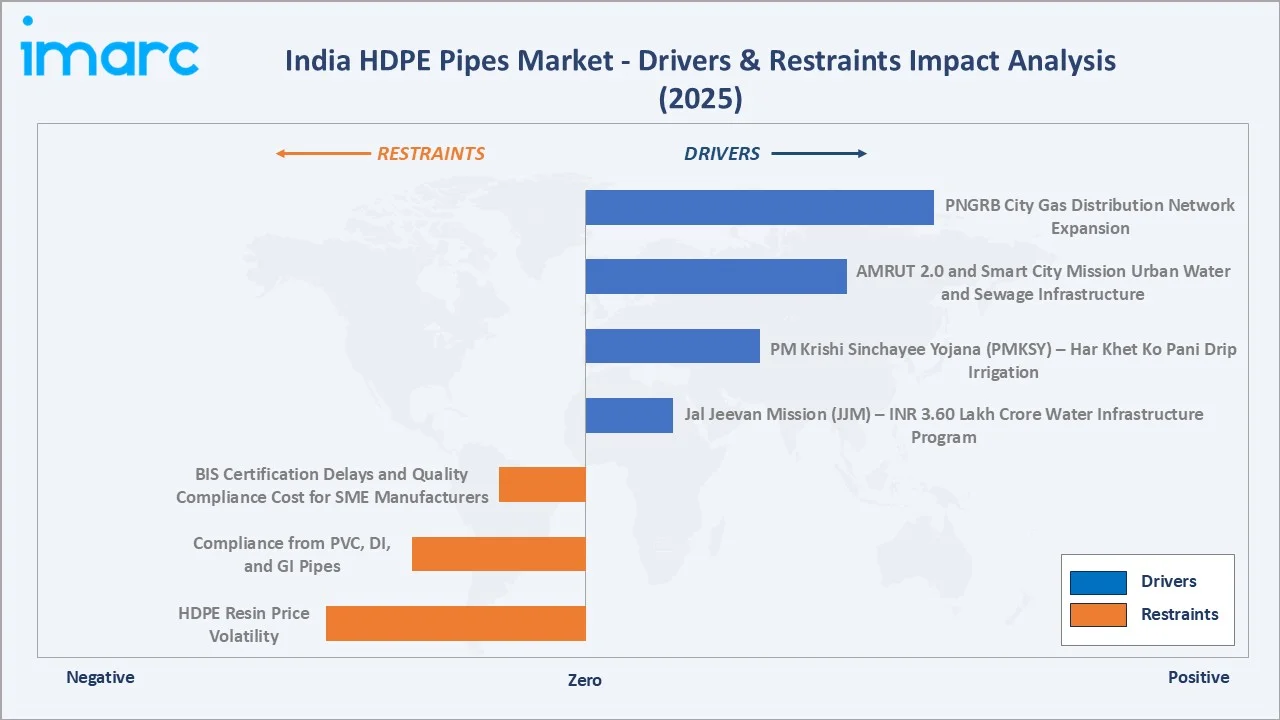

Market Drivers

- Jal Jeevan Mission (JJM) – INR 3.60 Lakh Crore Water Infrastructure Program: Jal Jeevan Mission’s mandate to connect all 19.3 crore rural households with piped water, with more than 15.79 crore (81.57%) households are reported to have tap water supply in their homes by January 2026. India’s largest infrastructure program by beneficiary count, with huge consumption of HDPE water supply pipes.

- PM Krishi Sinchayee Yojana (PMKSY) – Har Khet Ko Pani Drip Irrigation: PMKSY Micro Irrigation Fund (INR 5,000 crore under NABARD) is subsidizing the drip irrigation installation cost for small and marginal farmers, the primary demand driver for PE 63 HDPE agricultural lateral pipes.

- AMRUT 2.0 and Smart City Mission Urban Water and Sewage Infrastructure: AMRUT (Atal Mission for Rejuvenation and Urban Transformation) 2.0’s INR 2.99 lakh crore urban infrastructure investment includes household water connections in urban local bodies and sewage network coverage in all AMRUT cities, generating systematic urban demand for HDPE water supply and sewage pipes.

Market Restraints

- HDPE Resin Price Volatility Tied to Crude Oil Cycles: India imports HDPE resin requirements. HDPE resin prices oscillated, creating severe margin compression for pipe manufacturers operating under fixed-price government tenders awarded 6–12 months earlier.

- BIS Certification Delays and Quality Compliance Cost for SME Manufacturers: India’s HDPE pipe manufacturers include SMEs without BIS IS 4984 or IS 14333 certifications, excluding them from government tenders and limiting them to unorganized private market supply.

Market Opportunities

- PE 100 Segment Growth from CGD Network and Water Transmission Mains: India’s city gas distribution build-out requiring PE 100 SDR 11 HDPE pipes. Simultaneously, India’s urban local bodies (ULBs) are progressively upgrading water transmission mains from DI and AC pipes to PE 100 HDPE, creating an HDPE water transmission market growth.

- Trenchless Technology Adoption for Urban HDPE Pipe Renewal: India’s urban infrastructure rehabilitation market is adopting horizontal directional drilling (HDD) and pipe bursting trenchless technology that specifically requires HDPE pipes (HDPE’s flexibility and fusion jointing enable trenchless installation that PVC and DI cannot achieve).

Market Challenges

- Government Tender Execution Delays and Fund Utilization Gaps: JJM and AMRUT project implementation has faced systematic execution delays, indicating execution bottlenecks in contractor procurement, state agency capability, and beneficiary household identification. These delays create lumpy HDPE pipe procurement patterns that concentrate demand in project acceleration periods and create demand troughs in fund release gaps.

- Quality Enforcement Gap in Unorganized Pipe Market: India’s HDPE pipe market includes significant unorganized production where non-BIS-certified manufacturers supply PE 63 agricultural irrigation pipes at 20–30% below certified product pricing through informal dealer channels.

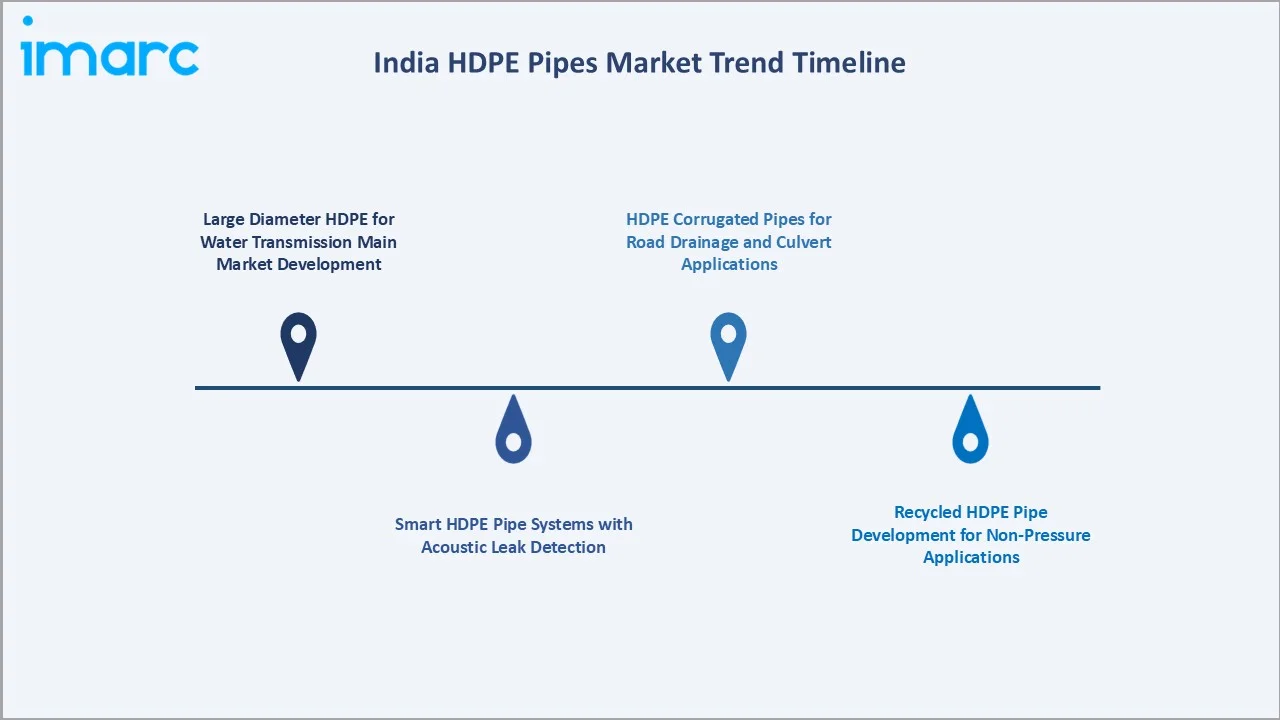

Emerging Market Trends

1. Large Diameter HDPE for Water Transmission Main Market Development

India’s water supply infrastructure is transitioning from distribution-only HDPE deployment to large-diameter HDPE water transmission main applications, where PE 100’s superior pressure ratings enable replacement of CI and AC transmission mains.

2. Smart HDPE Pipe Systems with Acoustic Leak Detection

India’s NRW (Non-Revenue Water) crisis is driving investment in acoustic leak detection and smart monitoring for HDPE water distribution networks. Sensors embedded in HDPE pipe joints (correlating leak-generated acoustic signals) are being piloted.

3. Recycled HDPE Pipe Development for Non-Pressure Applications

India’s Extended Producer Responsibility (EPR) regulations for plastics and the Central Pollution Control Board’s guidance on plastic waste recycled content are catalyzing development of recycled HDPE pipes for non-pressure applications, storm water drains, cable conduits, agricultural drainage channels, and landscaping uses.

4. HDPE Corrugated Pipes for Road Drainage and Culvert Applications

Double-wall corrugated HDPE (DWCDPE) pipes for road drainage, culverts, and underground stormwater management are growing as NHAI (National Highways Authority of India), state PWDs, and Smart City drainage projects systematically replace concrete and corrugated metal culverts.

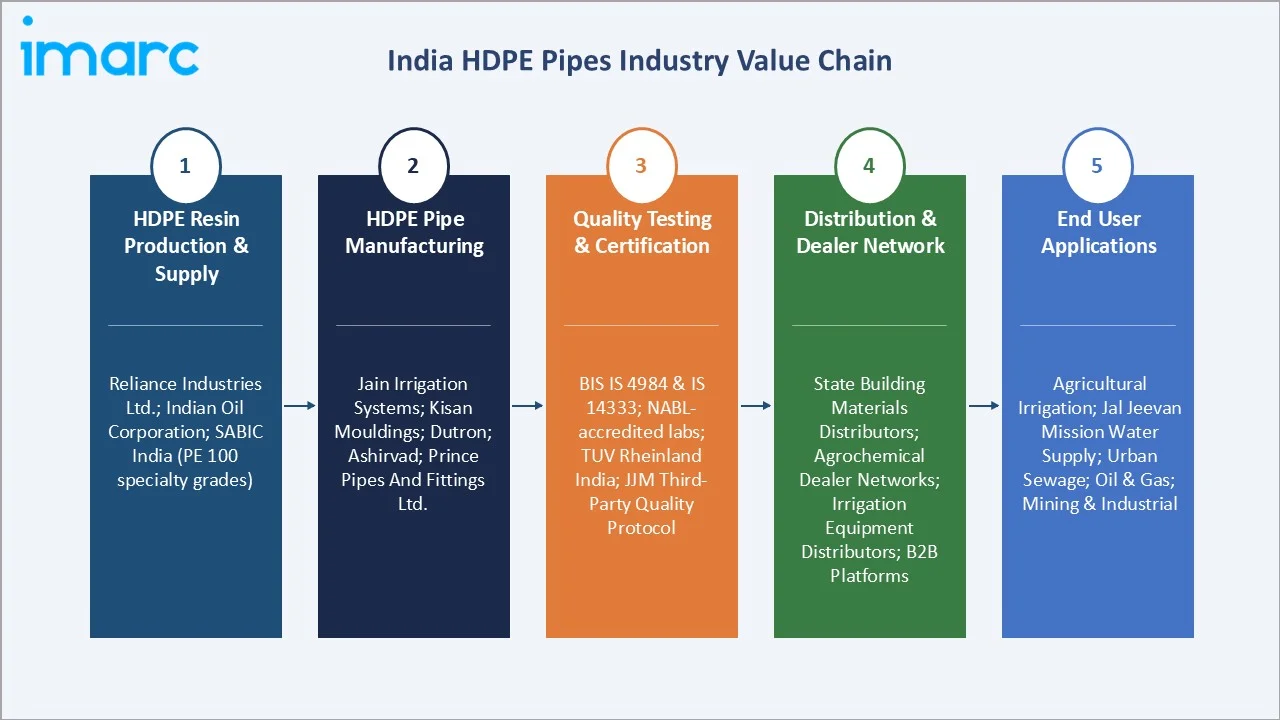

Industry Value Chain Analysis

India’s HDPE pipe value chain integrates domestic HDPE resin production, pipe extrusion manufacturing, quality testing and BIS certification, multi-tier distribution, and government procurement through state jal boards, PHED departments, and PNGRB-authorized city gas distribution companies.

|

Stage |

Key Participants |

|

HDPE Resin Production & Supply |

Reliance Industries Ltd., Indian Oil Corporation, SABIC India import supply for PE 100 specialty grades |

|

HDPE Pipe Manufacturing |

Jain Irrigation Systems Ltd., Kisan Mouldings Ltd., Dutron, Ashirvad, and Prince Pipes And Fittings Ltd. |

|

Quality Testing & Certification |

BIS (Bureau of Indian Standards) IS 4984 and IS 14333 certifications; NABL (National Accreditation Board for Testing) accredited pipe testing laboratories; TUV Rheinland India hydrostatic pressure testing; SGS India HDPE pipe material certification; Jal Jeevan Mission (JJM) quality assurance third-party testing protocol for water supply pipes |

|

Distribution & Dealer Network |

State-level building materials distributors and agrochemical dealer networks; irrigation equipment distributors; plumbing and civil engineering supplier networks; HDPE pipe project suppliers for government tenders; online B2B platforms |

|

End User Applications |

Agriculture; Jal Jeevan Mission water supply; Urban sewage; Oil & Gas; Mining and industrial applications |

HDPE pipe manufacturers operating under BIS certification capture the premium government tender market, depending on diameter and grade, while unorganized non-certified manufacturers compete in the private market at 20–30% lower pricing.

Technology Landscape in the India HDPE Pipes Industry

PE 100 and PE 100 RC Resin Technology Advancement

The transition from PE 80 to PE 100 and PE 100 RC HDPE pipe grades reflects material science advances in polyethylene bimodal molecular weight distribution technology. PE 100’s bimodal resin architecture, combining long-chain HDPE molecules with shorter chains, achieves MRS 10.0 MPa versus PE 80’s MRS 8.0 MPa, enabling 20–25% wall thickness reduction at equivalent pressure rating.

Electrofusion and Butt Fusion Welding Technology for Leak-Free Joints

HDPE pipe’s fusion jointing technology, butt fusion (mirror welding) for large diameter DN 63+ and electrofusion (EF) for service connections and fittings below DN 250mm, provides zero-leak permanently bonded joints that metal pipe flanged and threaded connections cannot match for underground pressure applications.

Trenchless Installation Technology Driving HDPE Market Penetration

Horizontal Directional Drilling (HDD), pipe bursting, and microtunneling trenchless technologies specifically require HDPE pipes. HDPE’s flexibility (fusion-jointed continuous pipeline, bending radius up to 20× pipe diameter), pressure rating consistency, and corrosion immunity make it the only practical material for urban trenchless water main and sewer rehabilitation.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Type |

PE 63 |

45.0% |

2025 |

|

Application |

Agricultural Irrigation Pipe |

35.0% |

2025 |

|

Region |

North India |

33.0% |

2025 |

By Type

PE 63 leads at 45.0% market share (2025). This grade’s dominance reflects India’s agricultural irrigation market’s farming households’ demand for PE 63 lateral pipes (DN 16–63mm) under PMKSY drip irrigation schemes. PE 63’s lower wall thickness and consequent lower material cost per metre make it the economically optimal grade for farm-level low-pressure irrigation distribution, where the PE 80/PE 100’s higher pressure ratings are unnecessary.

To access detailed market analysis, Request Sample

PE 80 at 35.0% serves the largest application diversity, JJM rural water supply, urban distribution mains, AMRUT sewage distribution, and general industrial applications. PE 100 at 20.0% is growing at the fastest CAGR of 5.2%, driven by PNGRB city gas distribution’s mandatory PE 100 specification, large-diameter JJM transmission main upgrades, and premium construction applications where long-term performance justifies the price premium over PE 80 equivalents.

By Application

Agricultural irrigation leads at 35.0% market share (2025). This dominance is sustained by India’s agricultural irrigated land at 44.41 % in 2023 and agricultural households’ drip and sprinkler irrigation adoption under PMKSY’s subsidy for micro-irrigation installation. The agricultural irrigation segment’s 35% share is relatively stable, given the structural nature of subsidy-driven demand and India’s total cultivable area, which represents a multi-decade HDPE agricultural pipe adoption journey.

Water supply at 25.0% is growing rapidly under JJM’s rural household connection program. Sewage at 20.0% serves AMRUT 2.0, Smart City Mission, and the state sewage treatment program HDPE pipe procurement. Oil & gas at 15.0% is growing fastest at ~4.8% CAGR from PNGRB city gas distribution. Others at 5.0% includes telecom duct, mining, and industrial pipe applications.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

North India |

33.0% |

Haryana, Punjab, Rajasthan, UP, Madhya Pradesh agricultural belt – India’s largest irrigated land cluster consuming HDPE drip and sprinkler irrigation pipes under PM-KUSUM and PMKSY schemes |

|

South India |

28.0% |

Tamil Nadu’s Pambar Basin and Cauvery-based irrigation scheme rehabilitation using HDPE replacing asbestos and GI pipes; Andhra Pradesh and Telangana’s Mission Bhagiratha and Mission Kakatiya water supply using PE 80/PE 100 HDPE |

|

West India |

22.0% |

Maharashtra’s Nashik, Pune, Aurangabad Marathwada drought-zone drip irrigation expansion consuming HDPE PE 63 micro-irrigation pipes; Gujarat SCADA-monitored agricultural distribution pipeline network rehabilitation |

|

East India |

17.0% |

Odisha, West Bengal, Bihar, Jharkhand, Assam JJM rural water supply – lowest pipe infrastructure penetration nationally creating above-average replacement demand |

North India’s 33.0% dominance is reinforced by UP’s 2.63 crore JJM household connections (India’s largest state program), Rajasthan’s Indira Gandhi Nahar Pariyojana project, and Haryana-Punjab’s agricultural drip irrigation expansion.

South India’s 28.0% share is supported by Telangana Mission Bhagiratha and Tamil Nadu’s TWAD Board rural water supply schemes. South India’s fastest regional CAGR (~4.3%) reflects the combination of still-significant JJM implementation remaining and PNGRB city gas distribution network. East India’s 17.0% share represents India’s highest-growth potential region – Bihar, Odisha, West Bengal, and Jharkhand have the lowest existing water supply infrastructure coverage nationally and are simultaneously implementing JJM at the highest pace per state budget release.

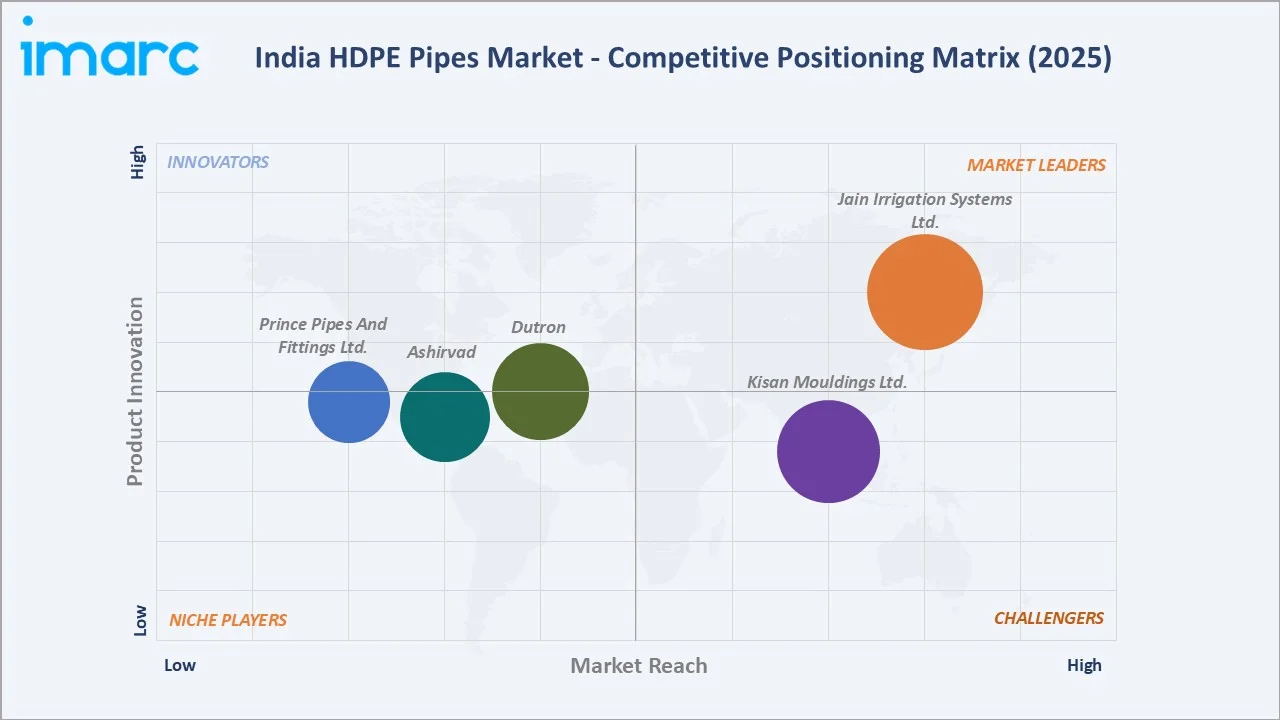

Competitive Landscape

India’s HDPE pipe market is moderately concentrated among BIS-certified organized manufacturers while remaining highly fragmented at the overall industry level. Jain Irrigation Systems and Kisan Mouldings collectively account for approximately 40–45% of India’s organized HDPE pipe market by value.

|

Company Name |

Product Range |

Market Position |

Core Strength |

|

Jain Irrigation Systems Ltd. |

HDPE Pipes, PE Large Diameter Pipes, HDPE Pipe with Tracer Wire, HDPE Power Duct (Multilayer Pipes), Perforated HDPE Pipe For Infiltration Gallery |

Market Leader |

India’s largest agricultural irrigation company and the dominant HDPE pipe supplier for drip and sprinkler irrigation systems |

|

Kisan Mouldings Ltd. |

HDPE pipes in sizes 20 to 630mm OD, with pressure ratings from PN-2.5 to PN-16.5 |

Strong Challenger |

Maharashtra-based HDPE and agriculture pipe specialist with a strong West India market position |

|

Dutron |

DUTRON HDPE pipes |

Established |

HDPE and PVC pipe manufacturer; Dutron’s HDPE pipe capacity serves India market |

|

Ashirvad |

Swasth HDPE Pipes |

Established |

Belgium-headquartered Aliaxis Group’s India operations with Bangalore-headquartered Ashirvad Pipes as the largest premium plumbing brand |

|

Prince Pipes And Fittings Ltd. |

PRINCE PE FIT Aqua (Pipes 20mm to 315mm) |

Established |

Mumbai-headquartered pipe manufacturer with HDPE pipes; Prince’s seven manufacturing plants (Haridwar, Athal, Dadra, Kolhapur, Telangana, Rajasthan, Chennai) provide a multi-regional manufacturing presence |

The top five combined share approximately 60–65% of the organized market. The remaining 35–40% of the organized market is distributed across manufacturers, with the top-20 accounting for approximately 85% of BIS-certified production capacity

Key Company Profiles

Jain Irrigation Systems Ltd.

Jain Irrigation Systems is one of India’s largest agricultural irrigation companies and the dominant HDPE pipe supplier for drip and sprinkler irrigation.

- Product Portfolio: HDPE Pipes, PE Large Diameter Pipes, HDPE Pipe With Tracer Wire, HDPE Power Duct (Multilayer Pipes), Perforated HDPE Pipe For Infiltration Gallery, and others.

- Recent Developments: In November 2025, Jain Irrigation Systems Ltd. received eight Export Excellence Awards from PLEXCONCIL for 2023–24 and 2024–25, recognizing its performance across categories such as drip irrigation, PVC foam sheets, fittings, and pipes & hoses, achieving a notable third consecutive win.

- Strategic Focus: Agricultural HDPE market dominance through PMKSY and PM-KUSUM irrigation system integration, complete system selling (emitter, pipe, filter, controller) versus commodity pipe selling.

Kisan Mouldings Ltd.

Kisan Mouldings is a plastic pipe manufacturer with a strong West India market position in HDPE agricultural irrigation and JJM water supply pipes.

- Product Portfolio: HDPE pipes in sizes 20 to 630mm OD, with pressure ratings from PN-2.5 to PN-16.5.

- Recent Developments: Kisan Mouldings’ plant capacity expanded for PE 100 production, targeting GSPC Gas and GAIL Gas Gujarat CGD network supply.

- Strategic Focus: Gujarat SAUNI Yojana and PMKSY distribution pipeline supply as anchor revenue; PE 100 CGD expansion through GSPC Gas, GAIL Gas, and Torrent Gas Gujarat network qualification; Maharashtra Jal Jeevan Mission supply expansion as the second-largest state market.

Prince Pipes and Fittings Ltd.

Prince Pipes and Fittings is a Mumbai-headquartered pipe manufacturer with eight manufacturing plants serving North, South, West, and Central India markets.

- Product Portfolio: PRINCE PE FIT Aqua (Pipes 20mm to 315mm).

- Recent Developments: In March 2025, Prince Pipes and Fittings Limited (PPFL) launched its eighth manufacturing facility in Begusarai, Bihar.

- Strategic Focus: Multi-plant geographic manufacturing strategy reduces logistics cost and delivery time for time-sensitive JJM tender supply; Haridwar plant as North India mountain JJM supply base, where flexible HDPE outperforms rigid GI and CI in challenging terrain.

Market Concentration Analysis

India’s HDPE pipe market demonstrates a clear dual-tier structure. In the organized BIS-certified segment, Jain Irrigation Systems and Kisan Mouldings collectively represent 40–45% market share. This moderate concentration, lower than India’s PVC pipe market reflects HDPE’s more complex multi-application market structure spanning agricultural irrigation, water supply, and city gas distribution (PE 100 specialists) simultaneously.

The top five combined share approximately 60–65% of the organized market. Market fragmentation is highest in PE 63 agricultural irrigation and lowest in PE 100 large-diameter applications. This concentration asymmetry, fragmented at the commodity end and concentrated at the premium end, creates parallel market dynamics where commodity PE 63 competes on price and dealer network proximity while premium PE 100 competes on certification, technical capability, and project execution reliability.

Investment & Growth Opportunities

Fastest Growing Segments

PE 100 grade (~5.2% CAGR), Oil & Gas application (~4.8% CAGR), South India regional market (~4.3% CAGR), PE 100 RC trenchless installation segment (~15–20% CAGR from small base), and recycled HDPE drainage pipes (~20–25% CAGR) represent India’s highest-growth HDPE pipe investment vectors.

Emerging Opportunities

East India’s Bihar, Odisha, and West Bengal JJM Phase II expansion in incremental annual HDPE pipe demand growing at a 6–8% CAGR through 2030 as these states’ JJM implementation acceleration programs consume HDPE at the highest per-state growth rate. NRW reduction programs in Delhi, Mumbai, Bangalore, and Hyderabad in premium PE 100 replacement demand are growing as trenchless rehabilitation becomes the standard approach for urban water main renewal.

Investment Themes

JJM’s INR 3.60 lakh crore program, PMKSY’s INR 93,068 crore irrigation fund, AMRUT 2.0’s INR 2.99 lakh crore, and PNGRB’s GA CGD build-out collectively create high investment in government infrastructure with HDPE pipe requirements, representing the most policy-visible investment case of any Indian construction material market.

- Key investment themes: PE 100 and PE 100 RC pipe manufacturing capacity expansion for CGD and urban water applications; large-diameter HDPE extrusion equipment for JJM transmission main supply; BIS IS 4984 and IS 14333 certification support for mid-tier manufacturers; EF fitting supply chain development for PNGRB CGD network supply; recycled HDPE drainage pipe R&D aligned with EPR regulations.

- Government procurement catalysts: JJM Phase II urban connectivity, PMKSY Har Khet Ko Pani, PM-KUSUM Phase B 35,000 MW solar pump HDPE drip integration, PNGRB CGD household connection target, and AMRUT 2.0 sewage network expansion collectively anchor India’s HDPE pipe market demand through 2034.

Future Market Outlook (2026-2034)

The India HDPE pipes market is positioned for sustained, government program-anchored growth through 2034. From USD 718.0 Million in 2025, the market will reach USD 1,029.1 Million by 2034, at a 3.94% CAGR that represents consistent compound growth despite India’s construction sector’s historical cyclicality. The defining characteristic of this growth trajectory is its policy anchor: JJM, PMKSY, AMRUT 2.0, and PNGRB CGD government infrastructure investment with systematic HDPE pipe requirements. This government procurement concentration growth, as government infrastructure programs execute their committed pipelines, creates a market growth floor that private sector demand supplementation converts into above-CAGR performance in program acceleration years.

Research Methodology

Primary Research

Primary research included structured interviews with 110+ industry stakeholders in 2025, comprising HDPE pipe manufacturing directors, state jal board project engineers for JJM procurement in UP, Rajasthan, and AP, PNGRB city gas distribution operators, HDPE resin commercial managers at Reliance Industries and GAIL, BIS IS 4984 committee technical experts, and agricultural irrigation dealer network managers across Maharashtra, Gujarat, and Rajasthan.

Secondary Research

Secondary research encompassed JJM (Jal Jeevan Mission) Progress Dashboard data, PMKSY annual progress reports (DAC&FW), PNGRB annual report and CGD network data, BIS HDPE pipe certification database, MoRTH NHAI drainage specification documents, CMA (CIPET Materials Analysis), PLEXUS global PE pipe market data, company annual reports, and Reliance Industries petrochemical segment polymer pricing data. Over 150 secondary sources were reviewed.

Forecasting Models

Market forecasts were developed using a bottom-up application-type-region aggregation validated against top-down macroeconomic models. Key inputs include JJM household connection pipeline, PMKSY micro-irrigation area targets, PNGRB CGD connection program, AMRUT 2.0 water supply funding, India PE pipe capacity addition plans, and Reliance Industries HDPE resin production expansion schedule.

India HDPE Pipes Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | PE 63, PE 80, PE 100 |

| Applications Covered | Oil and Gas Pipe, Agricultural Irrigation Pipe, Water Supply Pipe, Sewage System Pipe, Others |

| Regions Covered | North India, South India, East India, West India |

| Companies Covered | Jain Irrigation Systems Ltd., Kisan Mouldings Ltd., Dutron, Ashirvad, Prince Pipes And Fittings Ltd., etc |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the India HDPE pipes market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the India HDPE pipes market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the India HDPE pipes industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the India HDPE Pipes Market Report

The India HDPE pipes market was valued at USD 718.0 million in 2025 and is projected to reach USD 1,029.1 million by 2034.

The India HDPE pipes market is forecast to grow at a CAGR of 3.94% during 2026-2034, driven by JJM water infrastructure, PMKSY drip irrigation, PNGRB city gas distribution, and AMRUT 2.0 sewage expansion.

PE 63 leads with 45.0% revenue share (2025), driven by India’s 68 million farming household drip irrigation adoption under PMKSY subsidies, consuming a high amount of PE 63 lateral pipes.

Agricultural irrigation leads with 35.0% revenue share (2025), sustained by PMKSY Har Khet Ko Pani scheme micro-irrigation coverage and PM-KUSUM solar pump drip irrigation integration.

North India leads with 33.0% market share (2025), driven by UP’s JJM 2.63 crore household connection program, Rajasthan IGNP pipeline rehabilitation, and Haryana-Punjab agricultural drip irrigation expansion.

Key companies include Jain Irrigation Systems Ltd., Kisan Mouldings Ltd., Dutron, Ashirvad, and Prince Pipes and Fittings Ltd.

Key drivers include Jal Jeevan Mission INR 3.60 lakh crore program, PMKSY agricultural drip irrigation subsidies, PNGRB city gas distribution PE 100 network expansion, AMRUT 2.0 sewage infrastructure, and urban water supply NRW reduction trenchless replacement programs.

Key trends include PE 100 RC trenchless HDD adoption, large-diameter PE 100 water transmission main upgrades, smart acoustic leak-detection HDPE networks, recycled HDPE drainage pipes, and double-wall corrugated HDPE highway culvert applications.

Key challenges include HDPE resin price volatility, PVC price competition in agricultural segment, BIS certification barriers for SMEs, government tender payment delays extending 120–180 days, and JJM execution delays creating lumpy demand patterns.

South India grows at ~4.3% CAGR driven by AP Mission Bhagiratha pipeline, Tamil Nadu JJM implementation acceleration, PNGRB city gas PE 100 expansion in Hyderabad-Chennai-Bangalore.

Top opportunities include PE 100 large-diameter extrusion capacity, PE 100 RC trenchless pipe manufacturing, CGD network PE 100 SDR 11 qualified supply, Bihar-Odisha JJM Phase II supply, NRW urban replacement program PE 100 supply, and recycled HDPE drainage pipe EPR-aligned production.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)