India Health Insurance Market Size, Share, Trends and Forecast by Provider, Type, Plan Type, Demographics, Provider Type, and Region, 2026-2034

India Health Insurance Market Size, Share, Trends & Forecast (2026-2034)

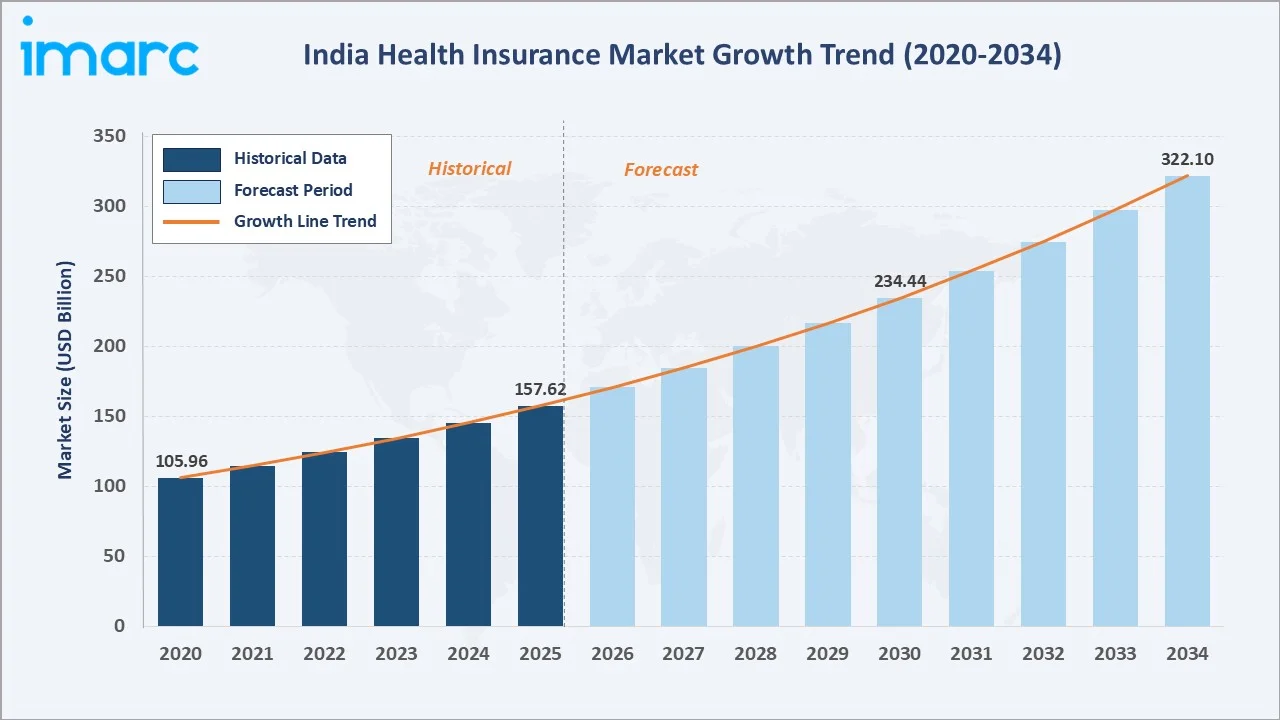

The India health insurance market size was valued at USD 157.62 Billion in 2025 and is projected to reach USD 322.10 Billion by 2034, exhibiting a CAGR of 8.27% during 2026-2034. Rising health awareness post-COVID-19, increasing middle-class incomes, expanding digital insurance distribution, and strong government policy support through Ayushman Bharat are driving robust market growth. Private providers dominate with a 63% share in 2025, while Term Insurance leads with 59%. North India holds the largest regional share at 29%, supported by high policy adoption in Delhi-NCR, Uttar Pradesh, and Punjab.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 157.62 Billion |

|

Forecast Market Size (2034) |

USD 322.10 Billion |

|

CAGR (2026-2034) |

8.27% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

North India (29.0% share, 2025) |

|

Fastest Growing Region |

South India |

|

Leading Provider Segment |

Private Providers (63%, 2025) |

|

Leading Type Segment |

Term Insurance (59%, 2025) |

The chart shows India’s health insurance market growth (2020–2034), driven by COVID-led awareness and government schemes, with future expansion supported by digital channels and broader coverage mandates.

To get more information on this market, Request Sample

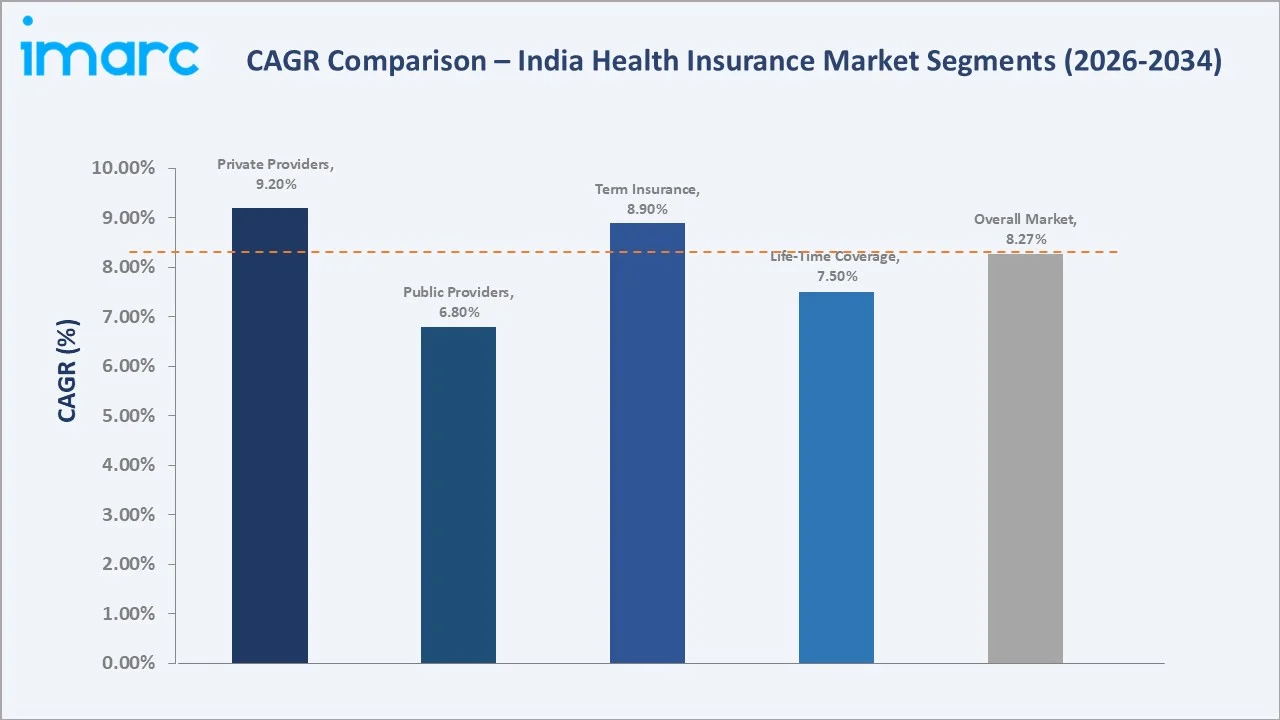

CAGR analysis identifies Private Providers and Term Insurance as the fastest-growing segments in the India health insurance market through 2034, supported by digital-first distribution and rising urban demand.

Executive Summary

India's health insurance market is undergoing a structural transformation, propelled by post-pandemic health awareness, a rising middle class, and government-led coverage expansion. The market was valued at USD 157.62 Billion in 2025 and is forecast to reach USD 322.10 Billion by 2034 at a CAGR of 8.27%. Key growth catalysts include expanding digital distribution channels, rising incidence of lifestyle-related ailments, growing employer-sponsored insurance, and Ayushman Bharat's 500-million-plus beneficiary coverage.

Private insurers hold 63% market share in India’s health insurance, driven by strong networks, innovation, and digital services. The 59% share for term insurance is not relevant to health insurance; individual and group policies dominate. Rising healthcare inflation low double digits is increasing adoption due to high out-of-pocket medical expenses.

North India leads with 29% market share in 2025, driven by corporate coverage in Delhi-NCR and high adoption in Uttar Pradesh and Punjab. South India is the fastest-growing region due to healthcare investments and InsurTech expansion. India is set to become a key Asia Pacific growth market, supported by rising penetration and a large insurable population.

Key Market Insights

|

Insight |

Data |

|

Largest Provider Segment |

Private Providers – 63% share (2025) |

|

Second Provider Segment |

Public Providers – 37% share (2025) |

|

Largest Type Segment |

Term Insurance – 59% share (2025) |

|

Leading Region |

North India – 29.0% revenue share (2025) |

|

Fastest Growing Region |

South India |

|

Top Companies |

Star Health, HDFC ERGO, Niva Bupa, Care Health, New India Assurance |

|

Market Opportunity |

Tier-2/3 city penetration and digital micro-insurance expansion |

Key Analytical Observations Supporting the Above Data:

- Private Providers' 63% dominance in 2025 reflects their superior hospital tie-ups, cashless claim networks exceeding 10,000 hospitals, and tech-enabled policy management platforms attracting urban and semi-urban policyholders.

- Public providers hold 37% share in 2025, driven by schemes like Pradhan Mantri Jan Arogya Yojana and Central Government Health Scheme, with PM-JAY covering over 500 million people and expanding nationwide insurance access.

- Term Insurance’s 59% dominance in 2025 reflects strong demand for affordable, defined-benefit plans with clear coverage limits, particularly among working-age adults prioritizing cost-efficient protection.

- North India’s 29% share is supported by strong corporate group health adoption in Delhi-NCR and large-scale state-backed insurance schemes in populous states like Uttar Pradesh, which has a population exceeding 200 million.

- South India is among the fastest-growing regions, driven by rising healthcare costs in cities like Bengaluru and Chennai, along with expanding private healthcare infrastructure, which is accelerating voluntary health insurance adoption.

- Star Health and Allied Insurance Company Limited, the largest standalone health insurer in India, reported a gross written premium of over INR 15,000 Crore in FY2024, reinforcing the strong role of private players in the health insurance market.

India Health Insurance Market Overview

Health insurance in India covers hospitalization and medical expenses through public and private insurers, with some plans including critical illness and outpatient care. The ecosystem includes insurers, Insurance Regulatory and Development Authority of India, TPAs, hospital networks, brokers, agents, bancassurance partners, and InsurTech platforms.

Applications include individual, family floater, group, senior citizen, and government-sponsored health plans. Health insurance penetration in India remains below 1% of GDP, significantly lower than global averages, indicating strong growth potential. Key drivers include rising healthcare costs, increasing NCD prevalence, digital adoption in Tier-2/3 cities, and improving financial awareness.

Market Dynamics

To evaluate market opportunities, Request Sample

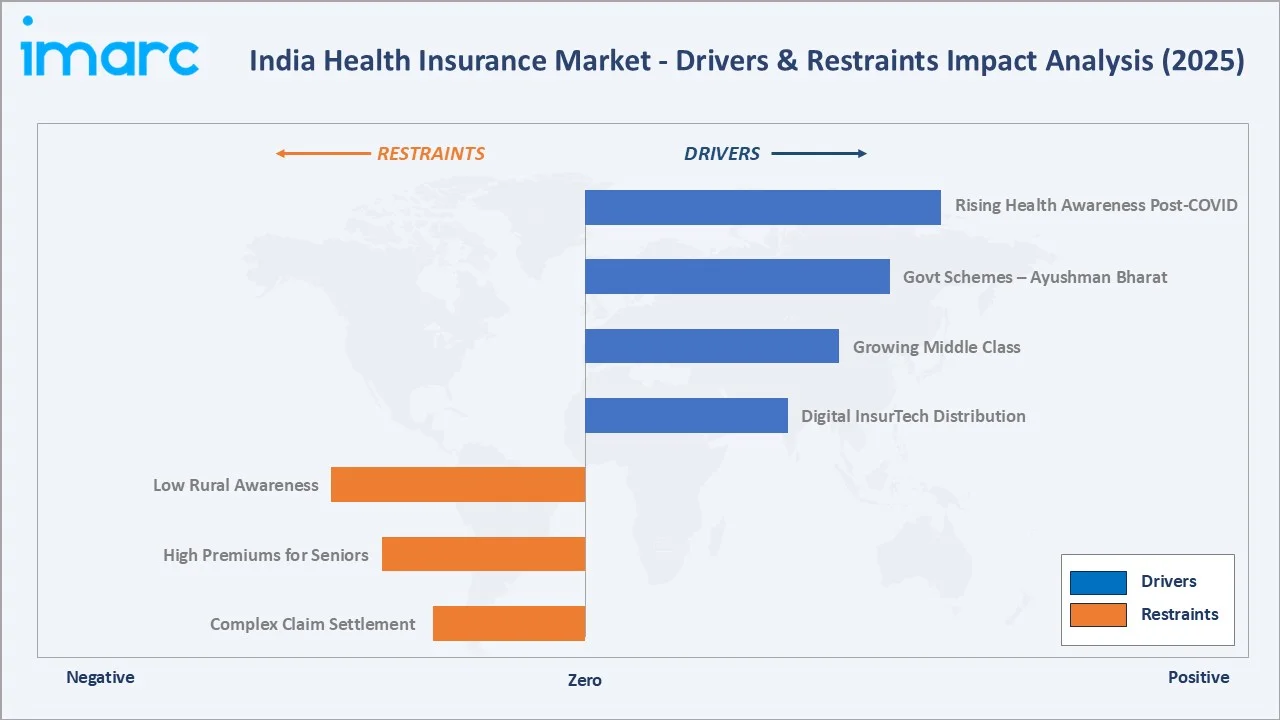

Market Drivers

- Rising Health Awareness and Post-COVID-19 Coverage Demand: COVID-19 significantly increased health insurance uptake in India, with insurers reporting strong growth in policy sales during 2020–2022 due to heightened awareness of medical costs and risks.

- Government Schemes – Ayushman Bharat PM-JAY: The scheme provides health coverage of up to INR 5 lakh per family per year to around 10–12 crore vulnerable families, significantly expanding insurance access among low-income populations.

- Growing Middle-Class Income and Urbanization: India’s middle class is expected to expand significantly by 2030, supporting higher discretionary spending, including health insurance, particularly in urban and semi-urban areas.

- Digital Insurance Distribution via InsurTech Platforms: Digital platforms such as Policybazaar, Acko, and Go Digit General Insurance are driving online policy adoption, improving accessibility and customer experience, with digital channels contributing a growing share of new policies.

Market Restraints

- Low Insurance Penetration and Awareness in Rural Areas: Health insurance coverage in India remains relatively low, with significant gaps in rural areas due to limited awareness, affordability constraints, and access barriers.

- High Premium Costs for Senior Citizen and Critical Illness Plans: Premiums for senior citizen health insurance have risen in recent years due to higher claim ratios and medical inflation, limiting affordability for elderly populations.

- Complex Claim Settlement Processes: While insurers have improved claim processing, issues such as exclusions, sub-limits, and co-payments continue to affect customer experience and trust.

Market Opportunities

- Tier-2 and Tier-3 City Penetration via Digital Channels: India has a large and growing internet user base in smaller cities, creating strong potential for digital insurance distribution, especially among underinsured populations.

- Senior Citizen and Critical Illness Coverage Growth: India’s elderly population (60+) is projected to rise significantly in the coming decades, increasing demand for senior-focused and critical illness health insurance products.

- Employer-Sponsored Group Health Insurance Expansion: Growth in formal employment and corporate sector expansion is driving demand for employer-sponsored group health insurance, a key growth segment for insurers.

Market Challenges

- Rising Claims Ratios and Profitability Pressure: Medical inflation in India remains high, putting pressure on insurers’ loss ratios and profitability, with several insurers reporting elevated combined ratios in recent years.

- Regulatory Compliance Complexity: Frequent regulatory updates by IRDAI, including standardization of health products and faster claim processing norms, increase compliance and operational requirements for insurers.

- Fraud and Mis-Selling Risk: Insurance fraud and mis-selling practices remain key challenges in India, impacting insurer profitability and customer trust, particularly in health insurance claims and agent-led sales.

Emerging Market Trends

The following five trends are reshaping the India health insurance market structure through 2034:

1. AI-Driven Underwriting and Claims Automation

Artificial intelligence is increasingly used by insurers like HDFC ERGO and Niva Bupa to automate underwriting, claims processing, and fraud detection, improving turnaround time, operational efficiency, and accuracy in risk assessment.

2. Micro-Insurance and Bite-Sized Health Products

Insurance Regulatory and Development Authority of India promotes micro-insurance through sandbox initiatives, enabling insurers like Acko and Digit Insurance to offer affordable, simplified health policies targeting underserved and low-income populations.

3. Preventive Health and Wellness-Linked Premiums

Insurers such as Star Health and HDFC ERGO are incorporating wellness programs, fitness tracking, and preventive check-ups into policies, incentivizing healthier lifestyles while improving customer engagement and long-term risk management.

4. Integrated Digital Health Ecosystems

Health insurers are expanding into telemedicine, pharmacy delivery, and diagnostics to create end-to-end health management ecosystems. Niva Bupa's ReAssure and Care Health's digital health platforms bundle insurance coverage with teleconsultations, prescription management, and preventive screening access, improving customer retention and lifetime value.

5. Group and Corporate Insurance Digitalization

Digital platforms such as Plum, Onsurity, and Riskcovry are streamlining group health insurance for SMEs through digital onboarding, policy management, and claims support, improving accessibility and administrative efficiency.

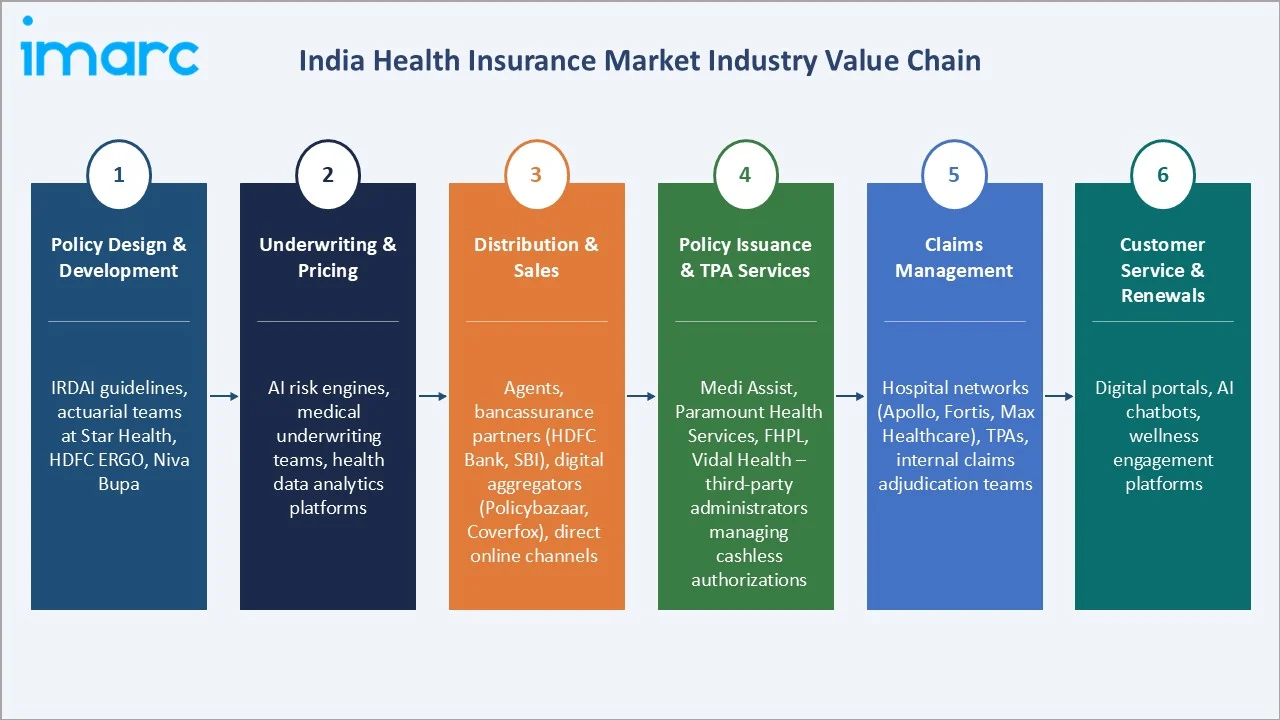

Industry Value Chain Analysis

The India health insurance value chain spans six stages, from product design and underwriting through to customer service and renewals, each involving distinct competitive dynamics and operational capabilities.

|

Stage |

Key Players / Examples |

|

Policy Design & Product Development |

IRDAI guidelines, Actuarial teams at Star Health, HDFC ERGO, Niva Bupa, New India Assurance |

|

Underwriting & Pricing |

AI-based risk engines, medical underwriting teams, health data analytics platforms (SAS, IBM Watson Health) |

|

Distribution & Sales |

Agents, bancassurance partners (HDFC Bank, SBI), digital aggregators (Policybazaar, Coverfox), direct online channels |

|

Policy Issuance & TPA Services |

Medi Assist, Paramount Health Services, FHPL, Vidal Health – third-party administrators managing cashless authorizations |

|

Claims Management |

Hospital networks (Apollo, Fortis, Max Healthcare), TPAs, internal claims adjudication teams, NHCX (National Health Claims Exchange) |

|

Customer Service & Renewals |

Digital self-service portals, AI chatbots, customer experience teams, wellness engagement platforms |

Private insurers lead the market through strong product innovation, wide hospital networks, and digital-first distribution, integrating underwriting, cashless claims, and wellness services creating a competitive edge over smaller regional players.

Technology Landscape in the Health Insurance Industry

AI-Powered Underwriting and Risk Assessment

AI and machine learning are increasingly used by insurers such as HDFC ERGO and Niva Bupa to automate underwriting and claims. While exact automation rates are undisclosed, insurers report faster policy issuance and improved risk profiling through predictive analytics.

Telemedicine and Digital Health Integration

Telemedicine adoption has accelerated, supported by platforms like Practo. Insurers integrating teleconsultation services enhance healthcare access and help reduce non-critical hospital visits, leading to more efficient claims management and improved cost control.

Blockchain for Claims Transparency and Fraud Prevention

Insurance Regulatory and Development Authority of India has explored blockchain via sandbox initiatives to enhance claims transparency. While large-scale adoption is limited, blockchain can reduce fraud and enable faster claims through secure, tamper-proof records and automation.

InsurTech and API-Driven Distribution Platforms

Digital insurers like Acko General Insurance, Digit Insurance, and Policybazaar use APIs to embed insurance across digital ecosystems. While user figures vary, these platforms significantly expand reach via app-based onboarding and partnerships.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Provider |

Private Providers |

63.0% |

2025 |

|

Type |

Term Insurance |

59.0% |

2025 |

|

Plan Type |

Medical Insurance |

51.0% |

2025 |

|

Demographics |

Adults |

59.0% |

2025 |

|

Provider Type |

Preferred Provider Organizations (PPOs) |

36.0% |

2025 |

|

Region |

North India |

29.0% |

2025 |

By Provider

To access detailed market analysis, Request Sample

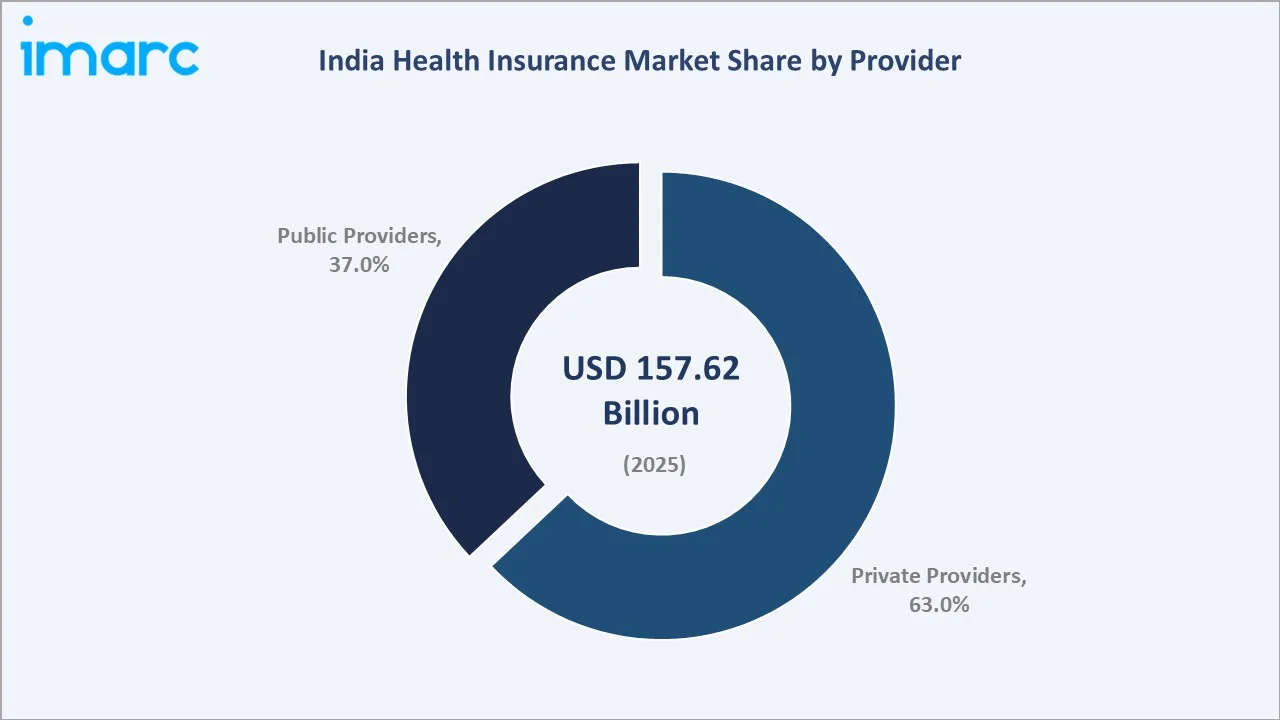

Private providers dominate India's health insurance market with a 63% share in 2025, supported by wider hospital networks, strong cashless claim systems, and digital product offerings. According to IRDAI reports, private insurers consistently hold a higher share than public players, with market leadership driven by innovation and customer-centric offerings. Consolidation among top insurers further strengthens their competitive position.

Public providers account for 37% of the market in 2025, driven by government schemes like PM-JAY, CGHS, and state programs. However, their share is gradually declining as private insurers expand digital access across semi-urban and rural areas.

By Type

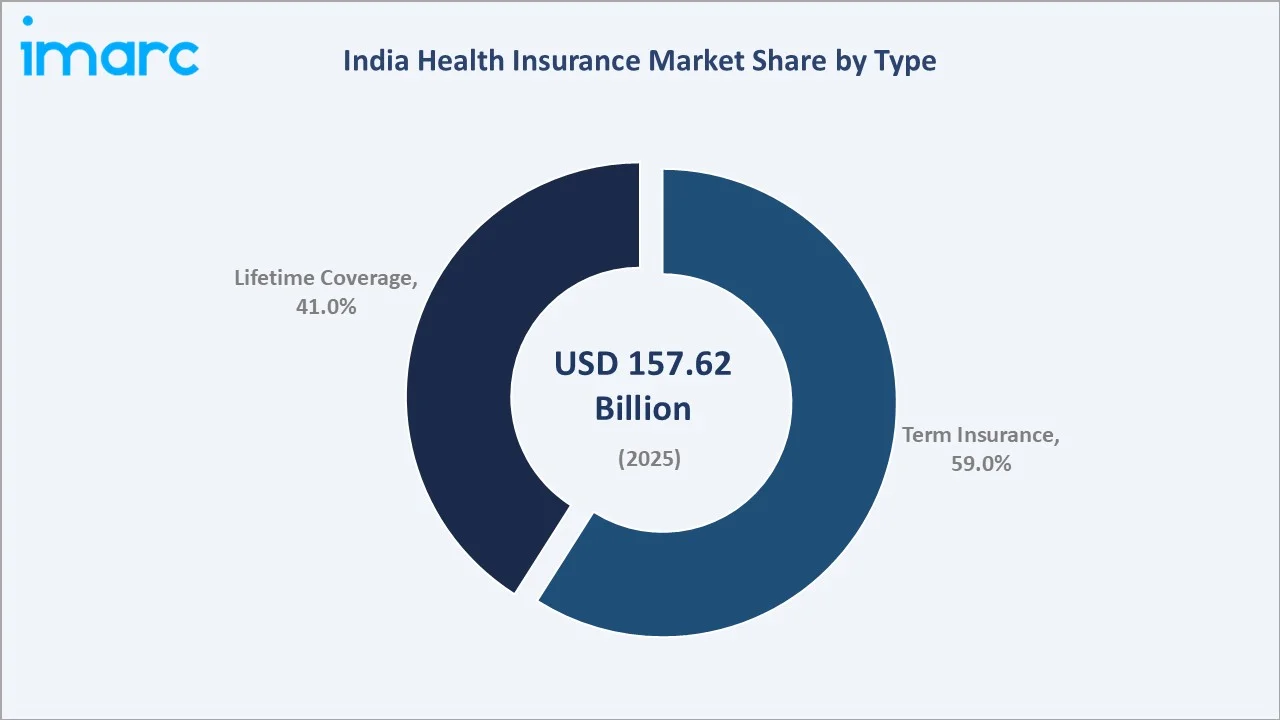

Term Insurance leads with a 59% share in 2025, preferred by policyholders for its defined-duration, affordable premium structures. Term health plans are popular among young working adults seeking cost-effective hospitalization coverage without lifetime premium commitments. Growing awareness of financial risk from acute illness episodes is sustaining strong demand for term health plans through the forecast period.

Lifetime coverage plans hold 41% in 2025,” driven by demand for continuous protection without renewal risk. IRDAI regulations mandate lifelong renewability and prohibit denial based on age, while recent reforms removing entry-age limits have strengthened adoption among seniors and high-risk individuals.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

Major Companies |

|

North India |

29.0% |

Corporate group policies in Delhi-NCR; UP government schemes; high urban coverage |

Star Health, HDFC ERGO, New India Assurance |

|

West & Central India |

26.8% |

Mumbai and Pune corporate insurance; Gujarat industrial workforce; Maharashtra state schemes |

Bajaj Allianz, Niva Bupa, HDFC ERGO |

|

South India |

25.3% |

IT sector group health in Bengaluru; CM health schemes in TN and AP; rising InsurTech adoption |

Star Health, Care Health, United India |

|

East India |

18.9% |

Growing awareness in West Bengal and Odisha; government scheme expansion in Bihar and Jharkhand |

National Insurance, New India Assurance, Star Health |

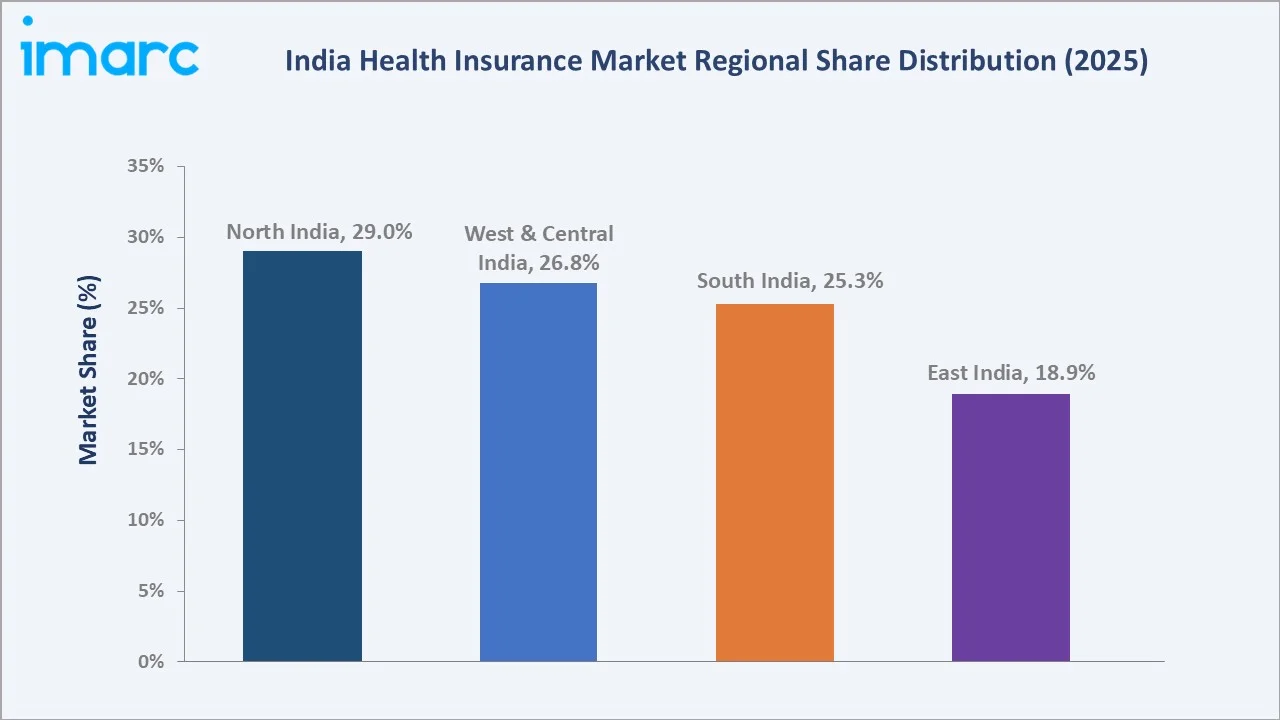

North India holds 29% of India’s health insurance market in 2025, driven by strong corporate group coverage in the Delhi-NCR corridor and wide state-backed scheme adoption across Uttar Pradesh, Rajasthan, and Haryana, with Delhi showing among the highest individual insurance penetration levels in the country.

West and Central India hold 26.8% in 2025, supported by Maharashtra’s large workforce and Gujarat’s industrial insurance adoption. South India accounts for 25.3%, driven by IT-led group policies and schemes like Chief Minister's Comprehensive Health Insurance Scheme covering millions. East India, at 18.9%, remains smaller but is improving with PM-JAY expansion and rising digital penetration.

Competitive Landscape

|

Company Name |

Key Brand |

Market Position |

Core Strength |

|

Star Health & Allied Insurance Co. Ltd. |

Star Health |

Leader |

Largest standalone health insurer; 14,000+ hospital network; digital claims platform |

|

HDFC ERGO General Insurance Co. Ltd. |

HDFC ERGO / Optima Secure |

Leader |

Bancassurance distribution via HDFC Bank; AI underwriting; premium corporate plans |

|

Niva Bupa Health Insurance Company Ltd. |

Niva Bupa / ReAssure |

Leader |

Global Bupa backing; preventive health integration; fast claim settlement technology |

|

Care Health Insurance Ltd. |

Care Health / Care Supreme |

Leader |

Diversified product portfolio; strong critical illness plans; digital-first customer experience |

|

The New India Assurance Co. Ltd. |

New India / Mediclaim |

Challenger |

Largest public sector insurer; extensive tier-2/3 reach; government scheme administrator |

|

Bajaj General Insurance Limited |

Bajaj General / Health Guard |

Challenger |

Allianz global backing; competitive family floater products; strong agent network |

|

United India Insurance Company Ltd. |

United India |

Challenger |

Pan-India public sector presence; strong rural and semi-urban market penetration |

|

ACKO General Insurance Ltd. |

Acko Health |

Emerging |

Fully digital InsurTech; direct-to-consumer model; low-cost micro-health products |

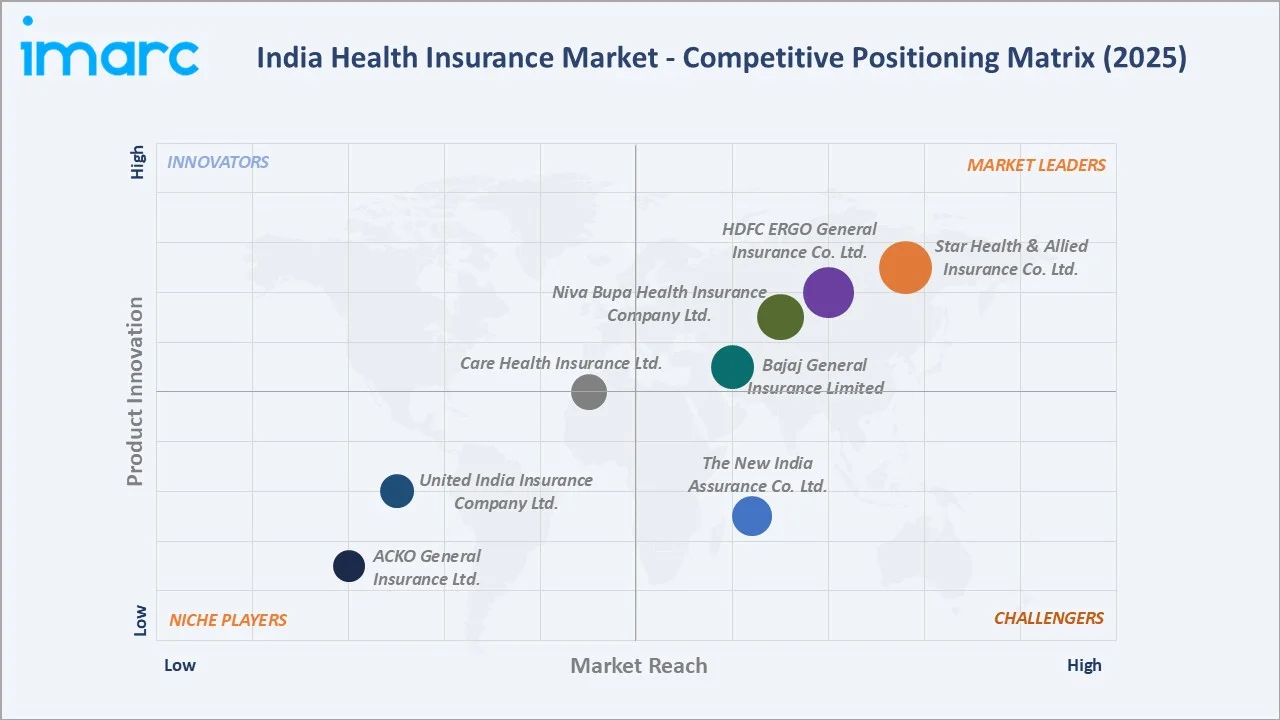

India’s health insurance market is moderately concentrated, with leading players such as Star Health, New India Assurance, HDFC ERGO, Niva Bupa, and Care Health collectively holding a significant share of premiums; standalone health insurers, despite fewer players, contribute a disproportionately large share, reflecting the strength of specialized health-focused business models.

Key Company Profiles

Star Health and Allied Insurance Company Limited

Star Health and Allied Insurance, founded in 2006 and headquartered in Chennai, is India’s largest standalone health insurer. It reported over INR 15,000 crore GWP in FY2024, serving millions through an extensive hospital network and strong retail focus.

- Product & Service Portfolio: Star Health offers retail, family floater, senior citizen, disease-specific, critical illness, personal accident, and group health insurance products, supported by cashless hospitalization, wellness programs, and digital claims services.

- Recent Developments: In FY2024, Star Health and Allied Insurance Company Limited reported a Gross Written Premium (GWP) of INR 15,254 crore, maintaining its leadership among standalone health insurers, while expanding its network to 14,000+ hospitals to strengthen nationwide cashless access.

- Strategic Focus: Star Health focuses on strengthening retail health leadership through deeper Tier-2/3 penetration, expanding hospital networks, enhancing digital claims infrastructure, and scaling distribution via agency, bancassurance, and direct channels.

HDFC ERGO General Insurance Co. Ltd.

HDFC ERGO General Insurance, headquartered in Mumbai, is a leading private insurer formed as a joint venture between HDFC Ltd. and ERGO International. It strengthened its health portfolio after acquiring Apollo Munich and serves millions through multi-channel distribution including bancassurance.

- Product & Service Portfolio: HDFC ERGO offers comprehensive retail and corporate health insurance products including Optima Secure, my:health Suraksha, Optima Restore, critical illness, senior citizen, and disease-specific plans, supported by wellness programs, digital claims, and cashless hospitalization services.

- Recent Developments: In 2025, HDFC ERGO General Insurance Company Limited expanded its healthcare provider network to 16,000+ hospitals, strengthening nationwide cashless access, and simultaneously launched Optima Lite, an affordable health insurance plan to improve penetration among price-sensitive and emerging customer segments.

- Strategic Focus: HDFC ERGO focuses on expanding retail health insurance through product innovation, deepening bancassurance via HDFC Bank, enhancing digital and AI-driven claims capabilities, and scaling corporate health solutions across India’s growing insured workforce.

Niva Bupa Health Insurance Company Ltd.

Niva Bupa Health Insurance, headquartered in New Delhi, is a leading standalone health insurer backed by Bupa and Fettle Tone. Formerly Max Bupa, it reported over INR 5,000 crore GWP in FY2024, serving millions through a growing hospital network and digital-first model.

- Product & Service Portfolio: Niva Bupa offers retail and group health insurance products including ReAssure 2.0, Aspire, GoActive, Health Companion, and Senior First, supported by cashless hospitalization, wellness benefits, preventive care programs, and digital health management services.

- Recent Developments: Niva Bupa Health Insurance Company Limited reported improved profitability with Q3 FY26 profit rising to ₹76 crore, driven by operational efficiencies, while strengthening its retail portfolio through the launch of the ‘Rise’ health insurance product offering flexible payments and digital healthcare benefits.

- Strategic Focus: Niva Bupa focuses on digital-first health insurance delivery, expanding in Tier-2/3 cities, strengthening preventive healthcare and wellness offerings, and leveraging Bupa’s global expertise to enhance underwriting, pricing, and customer-centric healthcare solutions.

Market Concentration Analysis

India’s health insurance market remains moderately concentrated in terms of premium volume, with the top five insurers – Star Health and Allied Insurance, HDFC ERGO General Insurance, Niva Bupa Health Insurance, Care Health Insurance, and The New India Assurance Company – collectively contributing around 55–60% of total health insurance gross written premiums in FY2025.

Market fragmentation is more pronounced in Tier-2 and Tier-3 cities, driven by the presence of standalone health insurers, general insurers offering health products, and government schemes. Many IRDAI-registered insurers intensifies competition, particularly in SME-focused group health plans.

Consolidation trends are gradually emerging, driven by technology investment requirements, capital adequacy norms, and rising claims management complexity. IRDAI's composite license framework proposal, if implemented, could trigger mergers between standalone health insurers and composite players, further reshaping market concentration through the 2026–2034 forecast period.

Investment & Growth Opportunities

Fastest-Growing Segments

India’s ageing population is rising rapidly, with the 60+ segment expected to expand significantly over the next decade. Despite this, insurance coverage remains low due to affordability constraints and pre-existing disease exclusions. This segment is expected to witness above-average growth, driven by product innovation and regulatory support.

India’s large informal workforce (over 350–400 million) presents a major opportunity for low-ticket, flexible health insurance products. InsurTech-led micro-insurance models are expanding rapidly, supported by increasing digital adoption and investor interest in embedded and bite-sized insurance offerings.

Emerging Market Expansion

Southern states are witnessing strong growth due to higher healthcare awareness, private hospital penetration, and digital adoption. Meanwhile, eastern states such as Bihar and Jharkhand remain underpenetrated in voluntary health insurance, creating significant headroom for expansion through digital distribution and government-private partnerships.

Venture & Strategic Investment Trends

India’s health insurance ecosystem is attracting increasing venture and private equity interest, particularly in AI-based underwriting, fraud analytics, and digital claims platforms aligned with initiatives like National Health Claims Exchange. Investors such as Tiger Global Management, SoftBank Vision Fund, and Multiples Alternate Asset Management have participated in multiple funding rounds, reflecting strong long-term growth expectations.

Future Market Outlook (2026-2034)

India’s health insurance market is set for strong growth, expanding from USD 157.62 Billion in 2025 to USD 322.10 Billion by 2034 at a CAGR of 8.27%, adding USD 164.48 Billion. Growth is driven by rising penetration, government initiatives, digital distribution, and demand for specialized health products.

Three transformational forces will redefine India's health insurance market through 2034. First, the National Health Claims Exchange (NHCX) will create a standardized, interoperable claims ecosystem, reducing settlement times and improving transparency industry-wide. Second, AI-driven personalized health underwriting will enable risk-based premium pricing at the individual level using wearable and health record data, improving insurer loss ratios while rewarding healthy behaviors. Third, embedded insurance distribution through UPI, e-commerce platforms, and healthcare apps will significantly expand retail reach beyond traditional agent and bancassurance channels.

By 2034, India’s health insurance penetration is expected to rise significantly. Although still below the global average, this shift will position India among Asia Pacific’s top five markets by premium volume, creating strong long-term opportunities for domestic and international insurers.

Research Methodology

Primary Research

Primary research encompassed structured interviews and surveys conducted in 2024–2025 with India health insurance industry stakeholders, including senior underwriting officers at private and public insurers, actuarial professionals, insurance regulatory experts at IRDAI, healthcare network heads at Medi Assist and FHPL, digital distribution platform leads at Policybazaar and Coverfox, and corporate HR heads managing group health policies at Fortune 500 India companies.

Secondary Research

Secondary sources include IRDAI Annual Reports (2021–2025), GIC Re Annual Reports, company annual reports (Star Health, HDFC ERGO, Niva Bupa, New India Assurance), Insurance Regulatory and Development Authority of India data releases, National Health Authority PM-JAY program publications, Ministry of Health and Family Welfare reports, FICCI insurance sector research, and trade publications including Insurance Asia and India Insurance Review.

Forecasting Models

Market size and forecasts were estimated using top-down and bottom-up models, incorporating GDP growth, healthcare spending trends, insurance penetration benchmarks, historical premium data, digital adoption trends, and scenario analysis (base, optimistic, conservative), including PM-JAY expansion assumptions.

India Health Insurance Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Providers Covered | Private Providers, Public Providers |

| Types Covered | Life-Time Coverage, Term Insurance |

| Plan Types Covered | Medical Insurance, Critical Illness Insurance, Family Floater Health Insurance, Others |

| Demographics Covered | Minor, Adults, Senior Citizen |

| Provider Types Covered | Preferred Provider Organizations (PPOs), Point of Service (POS), Health Maintenance Organizations (HMOs), Exclusive Provider Organizations (EPOs) |

| Regions Covered | North India, West and Central India, South India, East India |

| Companies Covered | Star Health & Allied Insurance Co. Ltd., HDFC ERGO General Insurance Co. Ltd., Niva Bupa Health Insurance Company Ltd., Care Health Insurance Ltd., The New India Assurance Co. Ltd., Bajaj General Insurance Limited, United India Insurance Company Ltd., ACKO General Insurance Ltd., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Health Insurance Market Report

India's health insurance market was valued at USD 157.62 Billion in 2025, driven by rising health awareness, digital insurance expansion, and government-led scheme coverage.

The market is projected to reach USD 322.10 Billion by 2034, growing at a CAGR of 8.27% during 2026-2034, driven by expanding coverage, InsurTech growth, and senior segment demand.

Private providers lead with a 63% share in 2025, driven by superior hospital networks, cashless claim infrastructure, and technology-enabled product distribution platforms.

Term Insurance holds a 59% share in 2025, preferred for its affordability and straightforward hospitalization coverage among working-age adults aged 25–45 across urban India.

North India leads with a 29% share in 2025, anchored by corporate group policies in Delhi-NCR and high coverage in Uttar Pradesh through government and private schemes.

Key drivers include post-COVID health awareness, Ayushman Bharat PM-JAY expansion, rising income levels, healthcare inflation at 12–14%, and digital InsurTech distribution growth.

South India is the fastest-growing region, driven by rising IT sector group health policies, InsurTech adoption in Bengaluru and Chennai, and expanding state government schemes.

Leading companies include Star Health & Allied Insurance Co. Ltd., HDFC ERGO General Insurance Co. Ltd., Niva Bupa Health Insurance Company Ltd., Care Health Insurance Ltd., The New India Assurance Co. Ltd., Bajaj General Insurance Limited, United India Insurance Company Ltd., and ACKO General Insurance Ltd.

PM-JAY covers over 100 million families with up to INR 5 lakh annual coverage. CGHS, ESIS, and state schemes together extend health protection to a large share of the population, though exact combined beneficiary estimates vary across sources.

InsurTech platforms, AI underwriting, telemedicine integration, and API-driven distribution are enabling faster policy issuance, lower premiums, and improved claim settlement across India.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)