India Healthcare IT Market Size, Share, Trends and Forecast by Product and Services, Component, Delivery Mode, End User, and Region, 2026-2034

India Healthcare IT Market Size, Share, Trends & Forecast (2026-2034)

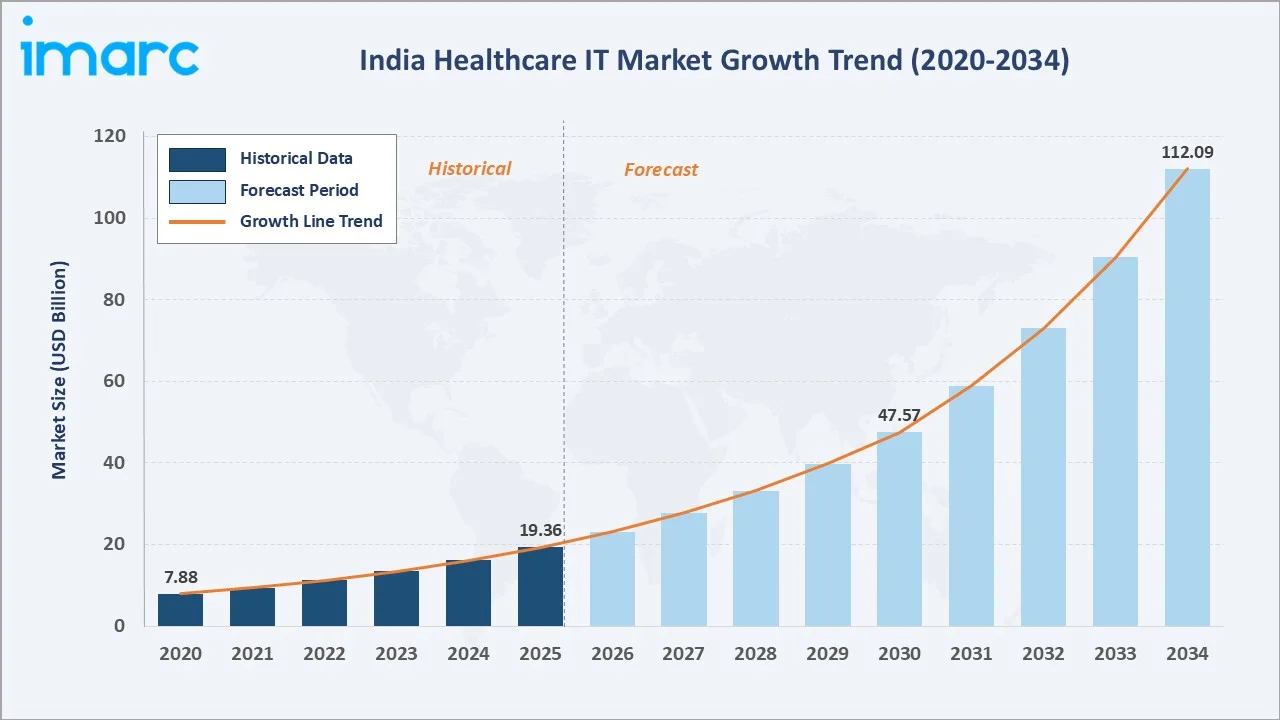

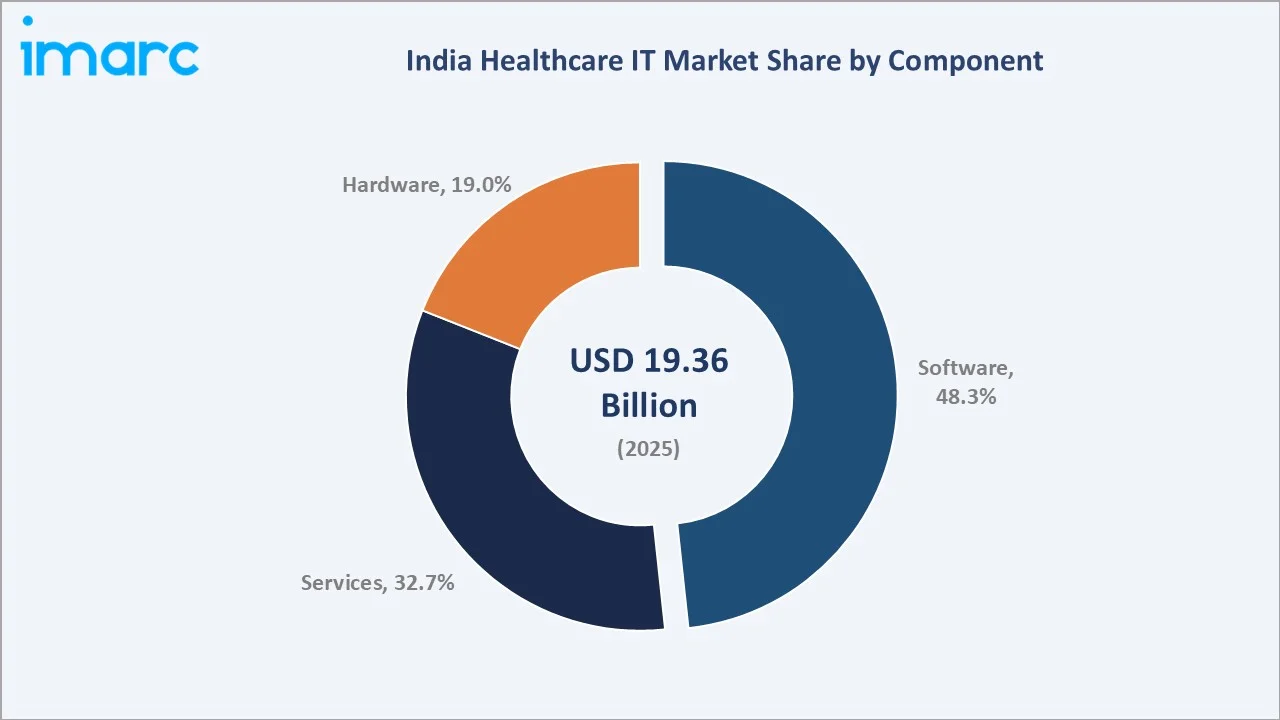

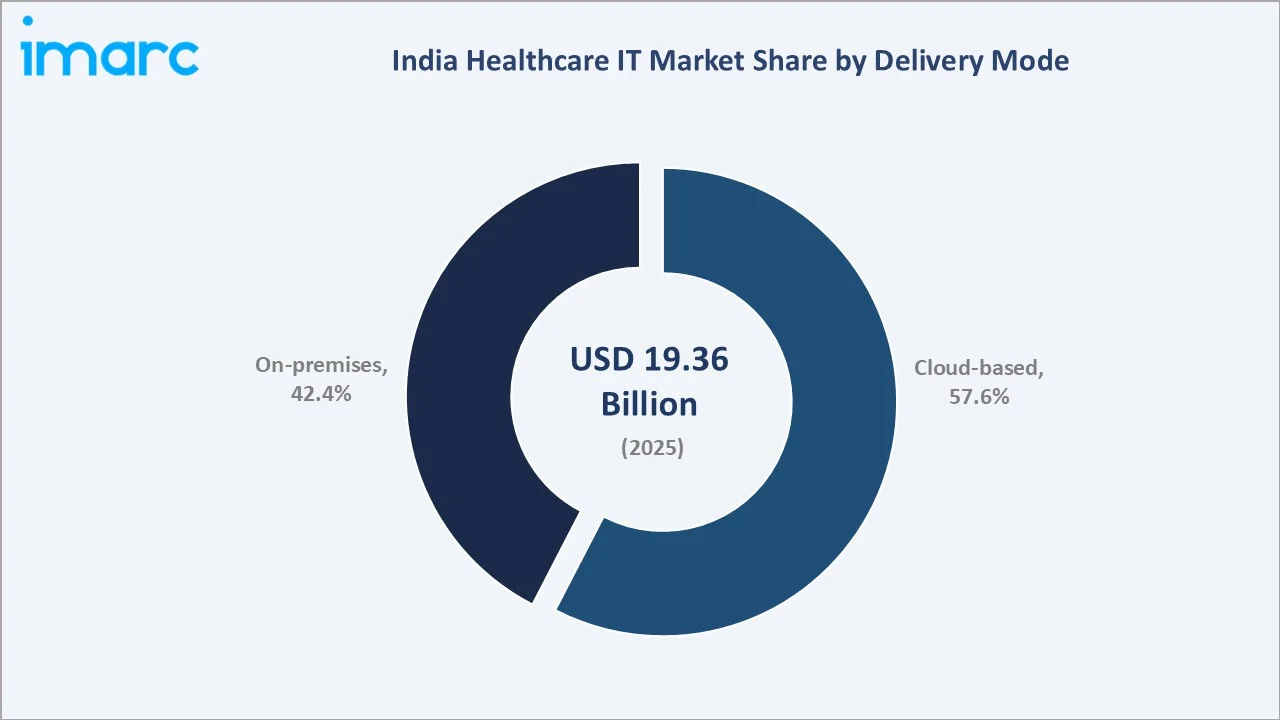

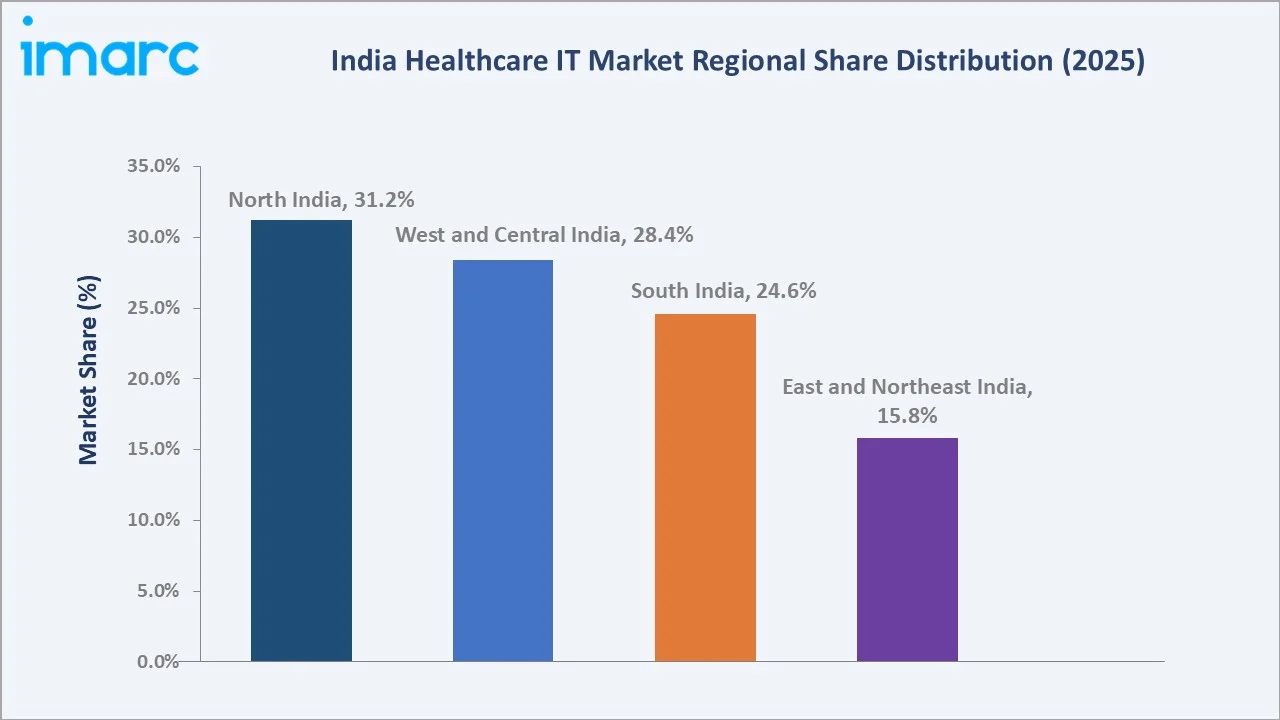

The India healthcare IT market size was valued at USD 19.36 Billion in 2025 and is projected to reach USD 112.09 Billion by 2034, exhibiting a CAGR of 19.70% during the forecast period 2026-2034. Rapid expansion of the Ayushman Bharat Digital Mission (ABDM), surging telemedicine consultations exceeding 31.86 crore on eSanjeevani as of December 2024, accelerating cloud adoption among hospital chains, and the integration of AI in diagnostics are driving the India healthcare IT market growth. Software leads the component segment at 48.3% in 2025, while Cloud-based delivery dominates at 57.6%. North India accounts for 31.2% of revenue in 2025, the country's largest regional market.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 19.36 Billion |

|

Forecast Market Size (2034) |

USD 112.09 Billion |

|

CAGR (2026-2034) |

19.70% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

North India (31.2% share, 2025) |

|

Fastest Growing Region |

South India (CAGR ~20.3%) |

|

Leading Component |

Software (48.3%, 2025) |

|

Leading Delivery Mode |

Cloud-based (57.6%, 2025) |

The India healthcare IT market growth trajectory from 2020 through 2034 reflects a steep historical expansion supported by digital health policy momentum, followed by a forecast curve powered by ABDM scale-up, cloud-native EHR deployments, and AI-led diagnostic integration.

To get more information on this market, Request Sample

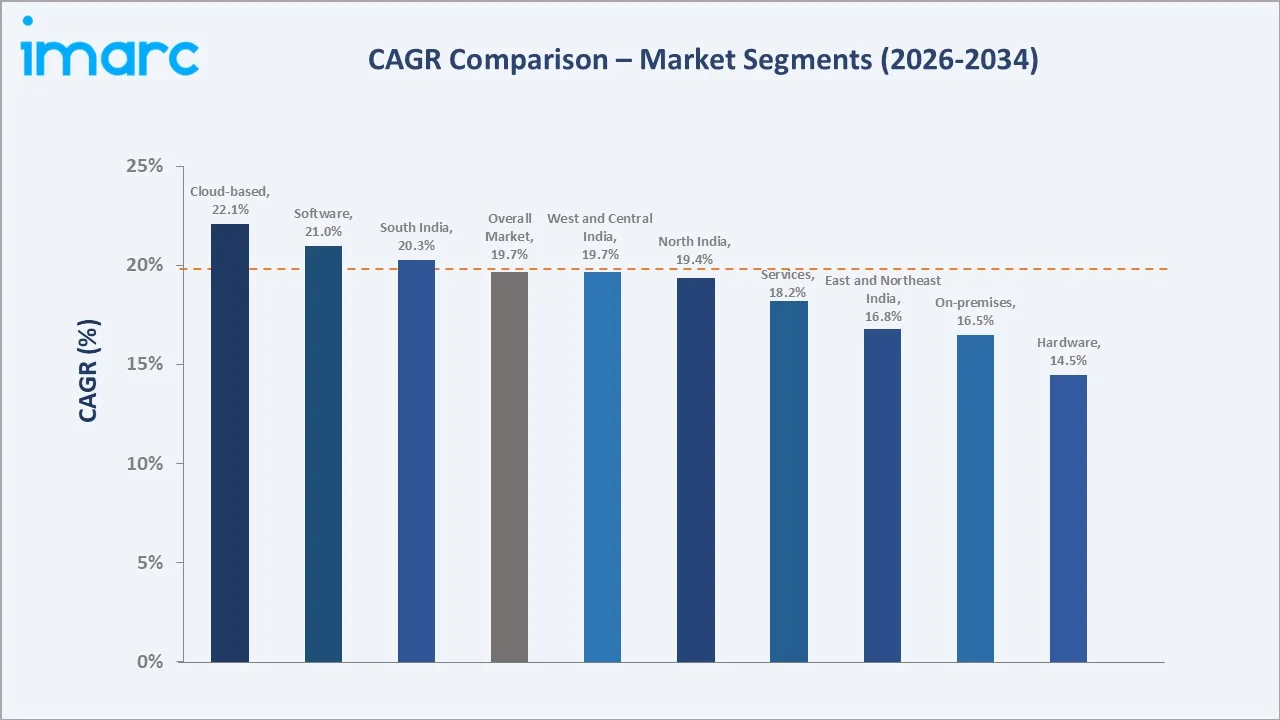

Segment-level CAGR comparisons highlight cloud-based delivery and software components as two of the fastest-growing categories, both outpacing the overall 19.70% market expansion through the forecast horizon.

Executive Summary

The India healthcare IT market is undergoing a structural shift driven by national-scale digital health programs, hospital digitisation, and the convergence of cloud, AI, and analytics in care delivery. Valued at USD 19.36 Billion in 2025, the market is projected to reach USD 112.09 Billion by 2034 at a CAGR of 19.70%. The Ayushman Bharat Digital Mission has issued more than 79 crore Ayushman Bharat Health Account (ABHA) IDs by 2025, creating a unified digital backbone that compels hospitals, diagnostic labs, and pharmacies to adopt interoperable IT systems.

Software dominates the component segment at 48.3% in 2025, anchored by hospital information systems (HIS), electronic health records (EHR), e-prescription, and revenue cycle management deployments across both private chains and government facilities. Services account for 32.7%, reflecting the heavy reliance on system integration and managed services delivered by Indian IT majors, while hardware contributes 19.0% of revenue.

North India leads with a 31.2% share in 2025, supported by Delhi-NCR's hospital density, the AIIMS network, and concentrated government health-tech procurement. West and Central India follow at 28.4%, driven by Mumbai-Pune private hospital chains and Gujarat's medical tourism corridor. South India holds 24.6%, anchored by Bengaluru's IT services ecosystem and Chennai's hospital base, while East and Northeast India account for 15.8%, reflecting rapidly expanding rural digital health adoption through eSanjeevani.

Key Market Insights

|

Insight |

Data |

|

Largest Component |

Software - 48.3% share (2025) |

|

Leading Delivery Mode |

Cloud-based - 57.6% share (2025) |

|

Leading Region |

North India - 31.2% revenue share (2025) |

|

Second Region |

West and Central India - 28.4% revenue share (2025) |

|

Top Companies |

TATA Consultancy Services Limited, Infosys Limited, Wipro, HCL Technologies Limited, Siemens Healthcare Private Limited, IBM India, Oracle India, Karkinos Healthcare, and Practo |

Key Analytical Observations Supporting The Above Data:

- Software's 48.3% lead in 2025 reflects accelerated EHR, HIS, and revenue cycle deployments across Apollo, Fortis, Max, and 700+ tier-1 and tier-2 private hospitals scaling digitally.

- Cloud-based delivery's 57.6% share in 2025 is driven by AWS, Azure, and Google Cloud's healthcare-compliant data centres in India and the cost-efficiency advantage for mid-sized hospitals.

- North India's 31.2% dominance in 2025 reflects Delhi-NCR hospital concentration, AIIMS digitisation programs, and central government health-tech procurement headquartered in the region.

India Healthcare IT Market Overview

Healthcare IT in India refers to the use of digital systems and platforms for managing clinical, administrative, and financial workflows across hospitals, diagnostic labs, payers, and pharmacies. The ecosystem spans EHR and HIS software, telemedicine platforms, claims and analytics tools, hardware infrastructure, and IT outsourcing services.

Applications cover the full provider-payer-patient continuum, including hospital management, e-prescription, lab information systems, PACS/RIS for imaging, claims processing, fraud analytics, and population health management. Macroeconomic enablers include India's USD 372 Billion healthcare expenditure in 2023, ABDM digital infrastructure scaling, 900 million internet users by 2025, and rising health insurance penetration covering 58 crore lives during 2024-25.

Market Dynamics

To evaluate market opportunities, Request Sample

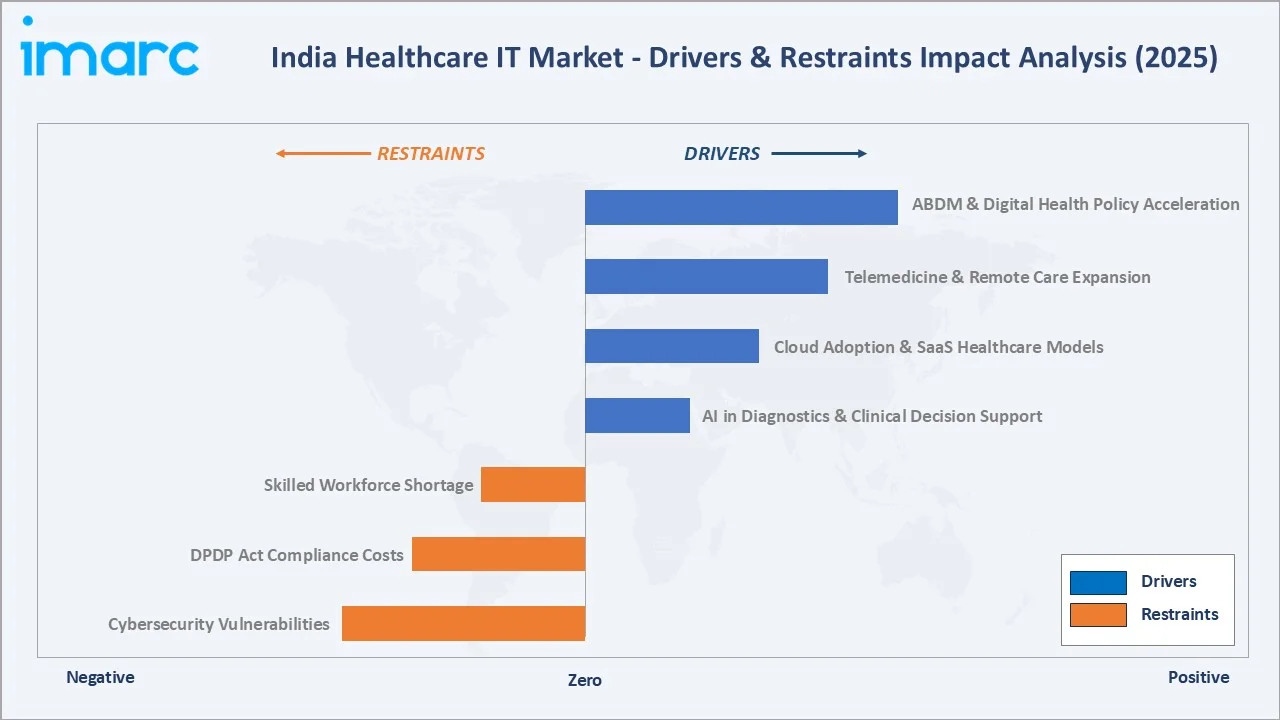

Market Drivers

- ABDM and Digital Health Policy Acceleration: The Ayushman Bharat Digital Mission has issued over 79 crore ABHA IDs and on-boarded more than 6 lakh healthcare professionals by 2025, mandating interoperable EHR adoption across public and private facilities.

- Telemedicine and Remote Care Expansion: eSanjeevani crossed 31 crore consultations by 2024, generating sustained demand for video infrastructure, scheduling software, and integrated EHR-prescription platforms across hospitals and government PHCs.

- Cloud Adoption and SaaS Healthcare Models: Cloud-native HIS adoption is rising as hospitals shift from capex-heavy on-prem servers to subscription-based EHR, billing, and analytics platforms.

- AI in Diagnostics and Clinical Decision Support: Indian hospitals deployed AI-based radiology screening, oncology decision support, and pathology image analysis tools at scale in 2025, supported by IRDAI-cleared digital pathways.

Market Restraints

- Data Privacy and DPDP Act Compliance Costs: The Digital Personal Data Protection Act 2023 imposes strict consent, storage, and breach reporting obligations on health data fiduciaries, raising compliance overhead for smaller IT vendors.

- Cybersecurity Vulnerabilities: AIIMS Delhi's 2022 ransomware incident and subsequent attacks on hospital networks in 2023-2024 have heightened the perceived risk profile of digital health infrastructure investment.

- Skilled Healthcare IT Workforce Shortage: India faces an estimated 30-35% shortfall in clinical informaticists and certified health-IT specialists relative to demand from rapidly expanding hospital chains in 2025.

Market Opportunities

- Tier-2 and Tier-3 Hospital Digitisation: Over 65% of small and mid-sized hospitals outside metro India remain on partial or paper-based workflows, representing a multi-billion-dollar greenfield SaaS opportunity through 2030.

- AI-Powered Population Health Analytics: The convergence of ABDM data lakes with AI analytics opens opportunities for chronic disease management platforms targeting approximately 89.8 million diabetic population in India in 2024.

- Insurer-led Claims Automation: Health insurance gross premium crossed INR 1.18 lakh crore in FY 2024-25, fuelling demand for AI-driven claims processing, fraud detection, and provider network management platforms.

Market Challenges

- Interoperability Across Legacy Systems: Hospitals still operate fragmented HIS, LIS, RIS, and billing modules with limited HL7/FHIR adoption, slowing ABDM-linked exchange and raising integration costs.

- Pricing Pressure in Public Sector Tenders: Government health-IT tenders frequently default to lowest-bidder pricing, compressing margins for quality vendors and leading to under-spec deployments in PHCs and CHCs.

- Limited Reimbursement for Telehealth: Insurance reimbursement frameworks for telemedicine remain partial in 2025, dampening sustainable revenue models for pure-play digital-first care platforms.

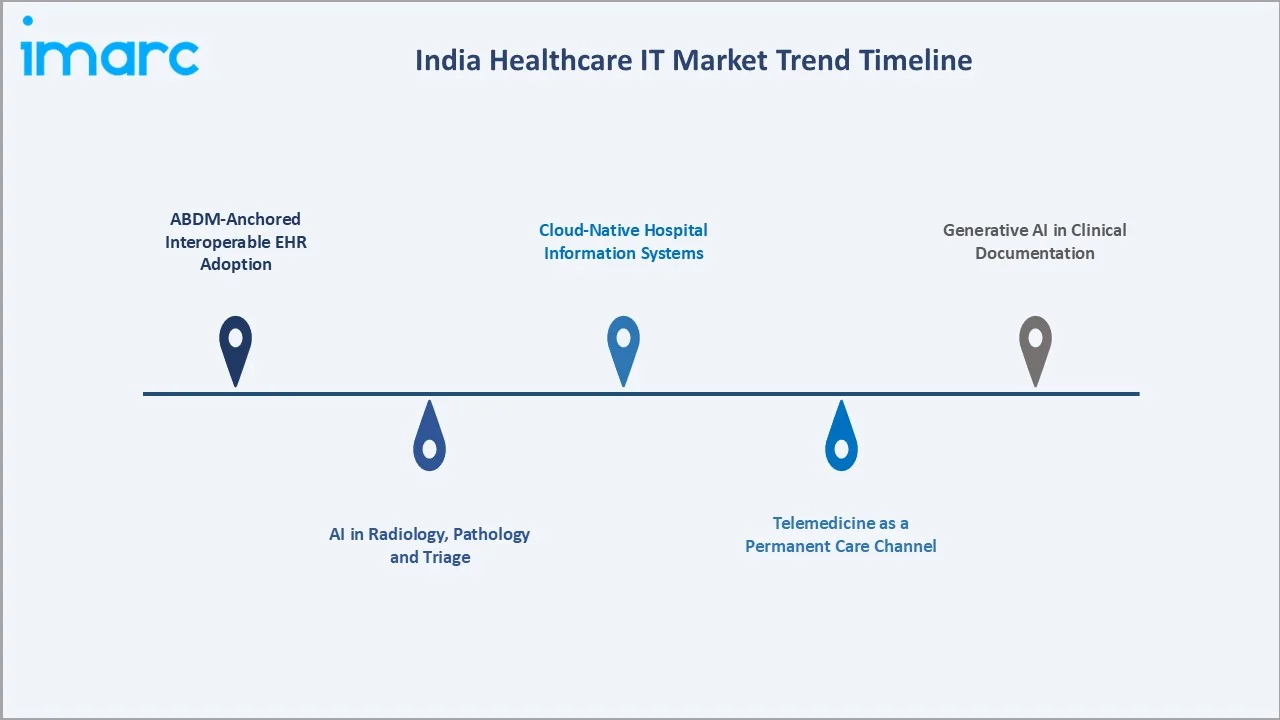

Emerging Market Trends

1. ABDM-Anchored Interoperable EHR Adoption

ABDM has shifted EHR from a hospital-internal record to a portable, patient-controlled longitudinal record. By 2025, more than 50 crore health records are linked to ABHA IDs, compelling vendors to redesign EHR products around FHIR APIs and consent management.

2. AI in Radiology, Pathology, and Triage

AI-based radiology platforms from Qure.ai, SigTuple, and Predible Health are being adopted across Apollo, Fortis, and government tele-radiology programs. In 2024, Apollo delivered 1.2 million teleconsultations and deployed 20 industry-certified clinical AI tools in acute care, diagnostics and public health use cases, expanding specialist access to tier-2 cities.

3. Cloud-Native Hospital Information Systems

Hospital chains are migrating from on-premise HIS to cloud-native multi-tenant SaaS, reducing infrastructure capex and enabling rapid scale-up. Cloud-based HIS adoption is projected to grow significantly through 2034, surpassing on-premise.

4. Telemedicine as a Permanent Care Channel

Post-pandemic, telemedicine has consolidated as a permanent care delivery mode. eSanjeevani has crossed 43 crore consultations as of November 2025, while private platforms like Practo and Tata 1mg are integrating EHR, pharmacy, and labs into unified consumer journeys.

5. Generative AI in Clinical Documentation

Ambient voice scribing and large language models are entering Indian hospital workflows in 2025, automating clinical note generation, discharge summaries, and coding tasks. Early deployments report 35-45% reductions in physician documentation time.

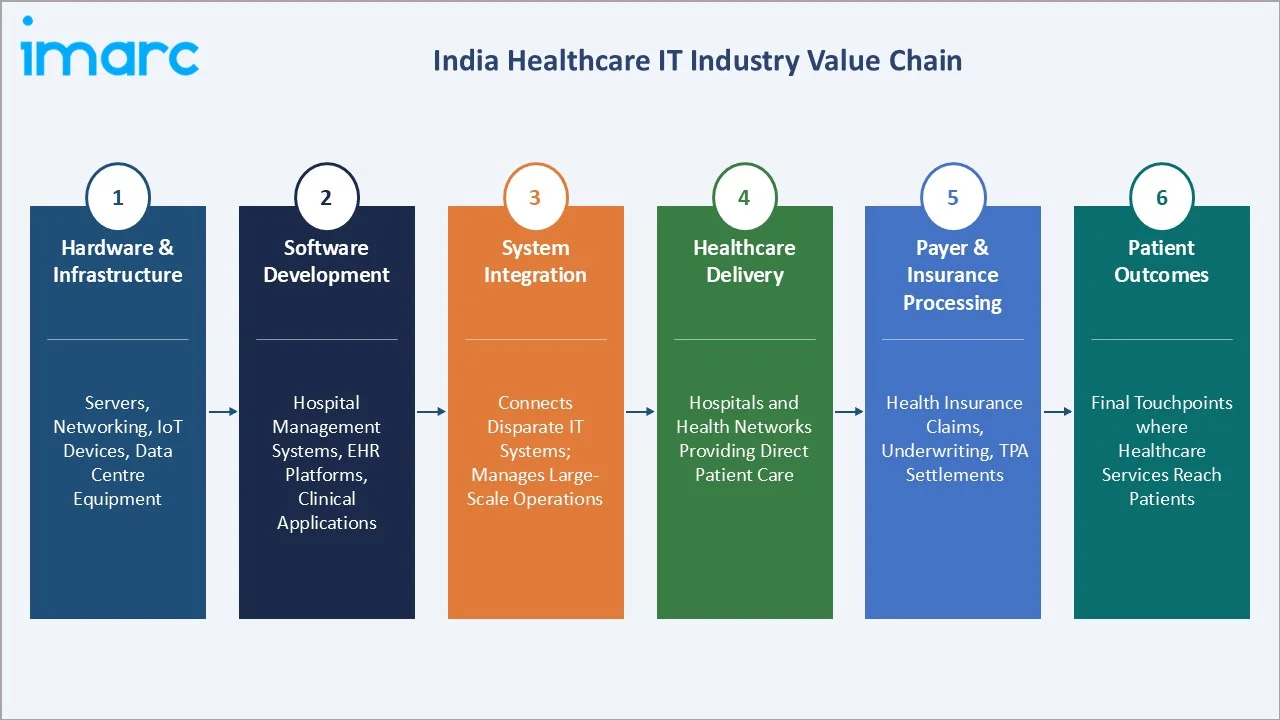

Industry Value Chain Analysis

The India healthcare IT value chain spans six integrated stages, each with distinct margin profiles and competitive dynamics. Software development and system integration capture the highest share of value, followed by healthcare delivery operators and payer-side processing platforms.

|

Stage |

Key Players / Examples |

|

Hardware & Infrastructure |

Provides physical servers, networking, IoT devices, and data centre equipment. |

|

Software Development |

Builds hospital management systems, EHR platforms, and clinical applications. |

|

System Integration |

Connects disparate IT systems and manages large-scale healthcare technology operations. |

|

Healthcare Delivery |

Hospitals and health networks that directly provide patient care services. |

|

Payer & Insurance Processing |

Manages health insurance claims, underwriting, TPA settlements, and reimbursements. |

|

Patient Outcomes |

Final touchpoints where healthcare services reach patients and communities. |

Indian IT services majors occupy a uniquely strong position by combining global healthcare-IT delivery experience with domestic provider relationships, allowing them to capture revenue in both export markets and the rapidly digitising Indian healthcare ecosystem.

Technology Landscape in the India Healthcare IT Industry

Cloud and Data Infrastructure

Healthcare-compliant cloud is the dominant technology platform shift in 2025. AWS, Microsoft Azure, and Google Cloud have launched India-resident healthcare data zones, supporting MeitY localisation and DPDP Act 2023 compliance for over 350 hospitals and lab customers across the country.

Materials and Hardware Innovation

Hardware investment is shifting from generic servers to purpose-built medical IoT, edge devices, and digital pathology scanners. The PLI scheme for medical devices, with INR 3,420 crore outlay, is incentivising domestic production of imaging and patient-monitoring hardware through 2027.

Smart Connectivity and Interoperability

FHIR R4, HL7, DICOM, and ABDM Health Information Provider (HIP) and Health Information User (HIU) standards form the connectivity stack. By 2025, more than 4 lakh health facilities are ABDM-registered and exchanging electronic records via consent-based APIs.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Product and Services | 🔒 | 🔒 | 2025 |

| Component | Software | 48.3% | 2025 |

| Delivery Mode | Cloud-based | 57.6% | 2025 |

| End User | 🔒 | 🔒 | 2025 |

| Region | North India | 31.2% | 2025 |

By Component

Software commands a 48.3% majority share in 2025, driven by widespread EHR, HIS, e-prescription, lab information system (LIS), and revenue cycle management deployments across hospitals, payers, and pharmacy chains. Software grows at the fastest pace within the component mix as cloud-native SaaS replaces legacy on-prem licences.

To access detailed market analysis, Request Sample

Services account for 32.7% of revenue in 2025, encompassing system integration, managed services, IT outsourcing, training, and consulting. Indian IT majors, including TCS, Infosys, Wipro, and HCL leverage global healthcare delivery experience to serve domestic hospital chains and payers, growing services significantly.

Hardware contributes 19.0% in 2025, including servers, networking, medical IoT devices, kiosks, and digital diagnostic equipment. Hardware grows moderately, constrained by the shift to cloud-hosted and as-a-service consumption models that prioritize on-premise capex.

By Delivery Mode

Cloud-based delivery dominates at 57.6% in 2025, propelled by AWS, Azure, and Google Cloud's India-resident healthcare zones and the cost-efficiency advantage for hospitals avoiding capex-heavy on-prem deployments.

On-premises delivery accounts for 42.4% in 2025, retained primarily by tertiary-care hospitals, government tertiary institutions, and chains with strict data residency policies. While share continues to decline gradually, on-premise growth remains substantial as legacy systems are upgraded rather than fully retired.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

North India |

31.2% |

Delhi-NCR hospital density, AIIMS digitisation, central government health-tech procurement |

|

West and Central India |

28.4% |

Mumbai-Pune private chains, Gujarat medical tourism, Maharashtra BFSI-led payer demand |

|

South India |

24.6% |

Bengaluru IT ecosystem, Chennai hospital base, Hyderabad pharma cluster, Kerala telemedicine |

|

East and Northeast India |

15.8% |

eSanjeevani-led rural digitisation, Kolkata tertiary hubs, NE telehealth corridor |

North India commands a 31.2% share in 2025, anchored by Delhi-NCR's dense tertiary hospital network, including AIIMS, Max, Fortis, and Medanta. Centralised government procurement and the headquarters of major payers and TPAs in the region structurally tilt healthcare-IT spend toward the north.

West and Central India holds 28.4% in 2025, led by Mumbai's BFSI and payer concentration, Pune's Tata-Cummins-Bharat Forge corporate health ecosystems, and Gujarat's medical tourism corridor centred on Ahmedabad. Telangana and Madhya Pradesh add further growth through state-level digital health programs.

South India contributes 24.6% in 2025, supported by Bengaluru's IT services and health-tech start-up base, Chennai's tertiary hospital ecosystem (Apollo, MIOT, Global Hospitals), Hyderabad's pharma and digital clusters, and Kerala's strong eSanjeevani uptake. Regulatory support from state IT policies further accelerates adoption.

East and Northeast India account for 15.8% in 2025, with Kolkata's tertiary care base, Bhubaneswar's emerging health-tech hubs, and rapidly scaling rural telemedicine across Northeast states. The region is the fastest-improving on a percentage basis as ABDM rollouts close historical infrastructure gaps.

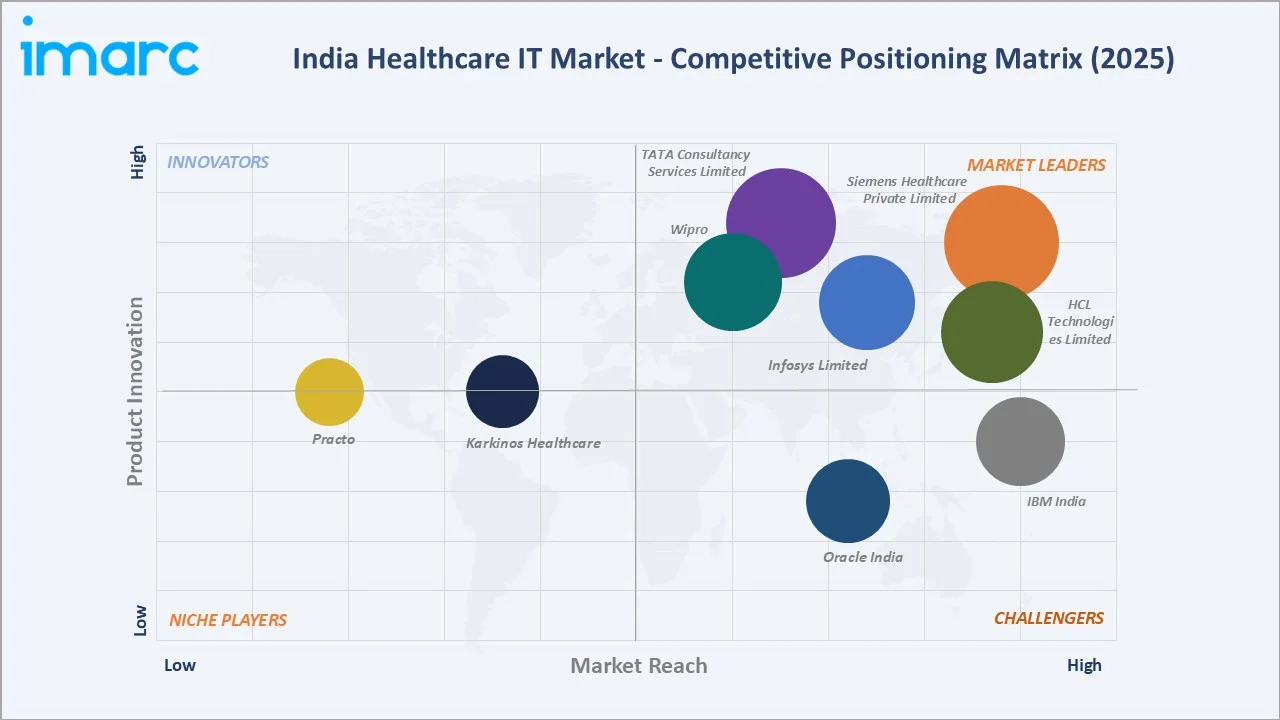

Competitive Landscape

|

Company Name |

Key Platform / Brand |

Market Position |

Core Strength |

|

TATA Consultancy Services Limited |

TCS Healthcare |

Leader |

Global healthcare-IT delivery, payer platforms, cloud migration |

|

Infosys Limited |

Infosys Helix |

Leader |

AI-led claims processing, payer analytics, EHR integration |

|

Wipro |

Healthcare services |

Leader |

Provider IT outsourcing, virtual care platforms |

|

HCL Technologies Limited |

HCLTech |

Leader |

System integration, infrastructure managed services |

|

Siemens Healthcare Private Limited |

Syngo |

Leader |

Imaging IT, RIS-PACS, digital diagnostics |

|

IBM India |

IBM Watsonx |

Challenger |

AI analytics, hybrid cloud healthcare, claims AI |

|

Oracle India |

Oracle Health |

Challenger |

EHR platform, hospital information system |

|

Karkinos Healthcare |

Digital Oncology Platform |

Emerging |

Oncology IT platform, distributed care networks |

|

Practo |

Practo Ray / Practo Consult |

Emerging |

SaaS for clinics, telemedicine, e-pharmacy |

The competitive landscape combines large Indian IT services majors with deep global healthcare-IT delivery experience, multinational platform vendors offering EHR and analytics suites, and a fast-growing layer of Indian health-tech specialists targeting telemedicine, oncology IT, and AI diagnostics.

Key Company Profiles

Tata Consultancy Services Limited

TCS is one of the largest healthcare-IT services providers globally, serving payers, providers, and life-sciences companies across India and over 50 international markets, with healthcare and life-sciences contributing a meaningful share of its USD 30 billion-plus revenue.

- Product & Platform Portfolio: TCS HOBS, TCS Optumera, TCS Healthcare Cloud, payer analytics platforms, and clinical data exchange solutions.

- Recent Developments: In 2024, TCS, ranked a global leader in healthcare industry cloud services by Everest Group, is among the IT majors positioned to deliver ABDM-aligned digital health transformation for Indian providers.

- Strategic Focus: TCS prioritises payer modernisation, provider cloud migration, AI-led claims processing, and cross-border healthcare delivery from India-based GCC hubs serving US and European clients.

Infosys Limited

Infosys is a leading Indian IT services major with a dedicated Life Sciences and Healthcare practice serving providers, payers, MedTech, and pharma clients globally, with healthcare-related delivery accounting for a sizeable portion of group revenue.

- Product & Platform Portfolio: Infosys Helix (AI-powered healthcare platform), Finacle Healthcare, Topaz AI services, claims automation, and EHR integration accelerators.

- Recent Developments: In March 2026, Infosys announced a major move to strengthen its healthcare IT portfolio by acquiring Optimum Healthcare IT, a digital transformation and consulting firm focused on healthcare providers.

- Strategic Focus: Infosys focuses on AI-first claims and member-experience platforms, payer-provider connectivity, and end-to-end digital transformation across hospital networks and insurers in India and abroad.

Siemens Healthcare Private Limited

Siemens Healthineers is a leading global medical technology company with a strong India presence, offering imaging, diagnostics, and digital health platforms anchored by its syngo and teamplay solutions.

- Product & Platform Portfolio: syngo enterprise imaging suite, teamplay digital health, AI-Rad Companion, RIS-PACS solutions, and laboratory IT systems.

- Recent Developments: In April 2026, Siemens Healthineers announced a collaboration with the Karnataka government to establish centres of excellence in life sciences, healthcare, and medical technology.

- Strategic Focus: Siemens Healthineers prioritises imaging IT leadership, AI-augmented diagnostics, and integrated digital health platforms that connect imaging, lab, and clinical data into unified hospital workflows.

Market Concentration Analysis

The India healthcare IT market exhibits moderate concentration. The top 5 players, including TCS, Infosys, Wipro, HCL Technologies, and Siemens, collectively account for an estimated 32-38% of revenue in 2025, while the rest is distributed across hundreds of mid-sized vendors and start-ups.

Fragmentation is highest at the EHR and HIS software layer, where domestic specialists like Napier Healthcare, Akhil Systems, and Birlamedisoft compete alongside global vendors. System integration and managed services exhibit the highest concentration, dominated by Indian IT majors with end-to-end delivery capability.

Consolidation is accelerating through M&A, with Indian IT majors acquiring health-tech specialists, and global PE funds rolling up regional EHR vendors to build scaled platforms targeting hospital chains and government health-IT contracts.

Investment & Growth Opportunities

Fastest-Growing Segments

Cloud-based delivery is the fastest-growing sub-segment, followed by AI-led diagnostics and clinical decision support tools growing within the broader software stack. Cloud-native HIS represents the largest single investment opportunity by absolute value.

Emerging Market Expansion

Tier-2 and tier-3 cities, where over 65% of hospitals remain partially digitised in 2025, represent a multi-billion-dollar greenfield market for SaaS HIS, telemedicine, and lab-IT platforms. East and Northeast India is the fastest-improving regional opportunities in percentage terms.

Venture & Private Investment Trends

Indian healthcare-IT and health-tech start-ups raised USD 1.13 Billion in cumulative funding during 2023-2024, with notable rounds in Practo, Tata 1mg, PharmEasy, Qure.ai, and Karkinos Healthcare. Private equity is actively rolling up hospital-IT and lab-IT vendors to build national-scale platforms.

Future Market Outlook (2026-2034)

The India healthcare IT market forecast projects revenue to scale from USD 19.36 Billion in 2025 to USD 112.09 Billion by 2034 at a CAGR of 19.70%, a near-six-times expansion driven by national digital health infrastructure, hospital cloud migration, AI deployment in diagnostics, and rising health insurance penetration.

Three technology disruptions are most likely to reshape the market through 2034: generative AI in clinical documentation and decision support, FHIR-native interoperability becoming the default architecture, and ambient clinical sensing combined with wearables generating continuous health data streams that feed analytics platforms.

By 2034, the India healthcare IT industry is forecast to evolve from a primarily software-licence and services market into a platform economy where SaaS subscriptions, AI-as-a-service, data analytics, and outcome-based contracts represent a meaningful share of revenue across providers, payers, and pharmacy networks.

Research Methodology

Primary Research

Primary research included over 45 structured interviews conducted in 2024-2025 with CIOs of Indian hospital chains, CTOs of payers and TPAs, leaders at Indian IT services majors, ABDM ecosystem stakeholders, health-tech founders, and institutional investors. Insights were used to validate market sizing, segmentation, technology adoption timelines, and competitive positioning.

Secondary Research

Secondary sources include Ministry of Health and Family Welfare publications, NITI Aayog digital health reports, ABDM dashboards, IRDAI annual reports, NASSCOM health-tech studies, MeitY publications, hospital chain annual reports, IT services company filings, and trade publications including Express Healthcare and BW Healthcare World.

Forecasting Models

Market size estimation and forecasts were derived using a combination of top-down and bottom-up models, incorporating GDP growth, healthcare expenditure trajectories, hospital bed additions, insurance penetration, ABDM rollout milestones, and historical software-services-hardware mix evolution. Scenario analysis covering base, optimistic, and conservative cases was performed to account for macro and policy uncertainty.

India Healthcare IT Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product and Services Covered |

|

| Components Covered | Software, Hardware, Services |

| Delivery Modes Covered | On-premises, Cloud-based |

| End Users Covered |

|

| Regions Covered | North India, West and Central India, South India, East and Northeast India |

| Companies Covered | TATA Consultancy Services Limited, Infosys Limited, Wipro, HCL Technologies Limited, Siemens Healthcare Private Limited, IBM India, Oracle India, Karkinos Healthcare, Practo, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the India healthcare IT market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the India healthcare IT market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the India healthcare IT industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the India Healthcare IT Market Report

The India healthcare IT market was valued at USD 19.36 Billion in 2025, supported by ABDM scale-up, telemedicine demand, and rapid hospital cloud adoption.

The market is projected to reach USD 112.09 Billion by 2034, expanding at a CAGR of 19.70% during 2026-2034, driven by digital health infrastructure and AI deployment.

Software leads with a 48.3% share in 2025, anchored by EHR, HIS, e-prescription, and revenue cycle management deployments across private and public hospitals.

Cloud-based delivery leads at 57.6% in 2025, supported by India-resident healthcare data zones from AWS, Azure, and Google Cloud, plus cost-efficiency for hospitals.

North India leads with a 31.2% share in 2025, driven by Delhi-NCR hospital density, AIIMS digitisation, and concentrated central government health-tech procurement.

Key drivers include ABDM rollout with over 70 crore ABHA IDs, telemedicine on eSanjeevani, cloud adoption, AI in diagnostics, and rising health insurance penetration.

Cloud-based delivery is the fastest-growing segment at over 22% CAGR through 2034, followed closely by AI-led diagnostics and clinical decision support tools.

Leading companies include TATA Consultancy Services Limited, Infosys Limited, Wipro, HCL Technologies Limited, Siemens Healthcare Private Limited, IBM India, Oracle India, Karkinos Healthcare, and Practo.

ABDM mandates interoperable, FHIR-based EHR adoption across 1.4 lakh-plus health facilities, driving demand for compliant software, integration services, and consent platforms.

AI powers radiology screening, oncology decision support, claims fraud detection, and ambient clinical scribes. Indian hospitals deployed over 1,000 AI tools by 2025.

Telemedicine has consolidated as a permanent care channel. eSanjeevani crossed 34 crore consultations by 2024, generating recurring demand for IT platforms and infrastructure.

Key challenges include cybersecurity vulnerabilities, DPDP Act compliance costs, interoperability across legacy systems, skilled workforce shortages, and pricing pressure in tenders.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)