India Heat Pump Market Size, Share, Trends and Forecast by Rated Capacity, Product Type, End Use Sector, and Region, 2026-2034

India Heat Pump Market Summary:

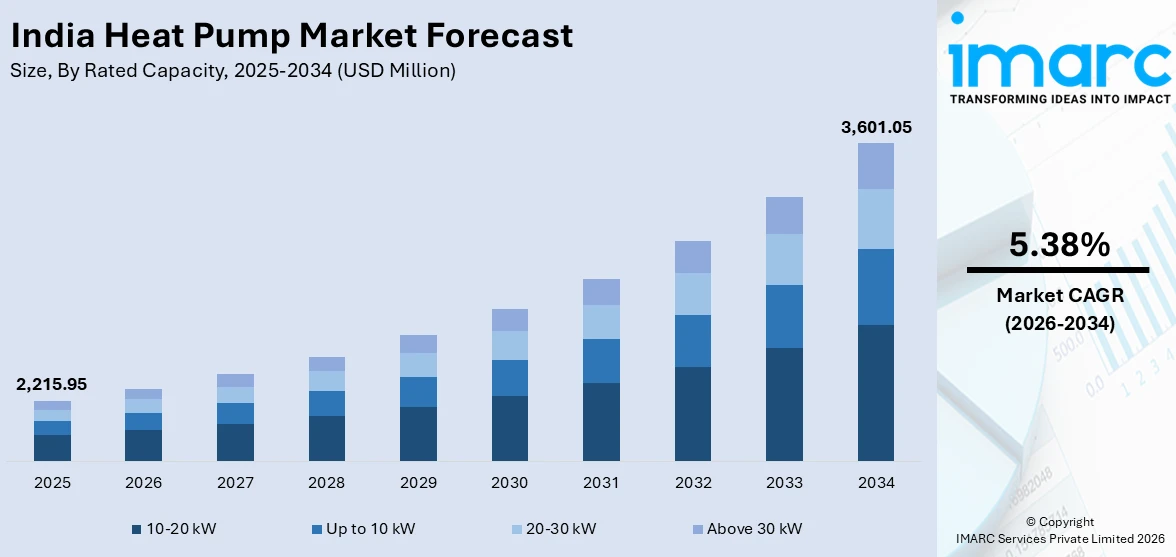

The India heat pump market size was valued at USD 2,215.95 Million in 2025 and is projected to reach USD 3,601.05 Million by 2034, growing at a compound annual growth rate of 5.38% from 2026-2034.

The market is driven by India’s growing emphasis on sustainable and energy-efficient heating and cooling technologies, supported by robust government initiatives targeting greenhouse gas reductions and energy conservation. Rising urbanization, progressive electrification across residential and commercial sectors, and heightened consumer awareness about the environmental impact of conventional systems are accelerating adoption. Growing deployment across hospitality, industrial, and commercial verticals further reflects the expanding India heat pump market share.

Key Takeaways and Insights:

- By Rated Capacity: 10-20 kW dominates the market with a share of 34.2% in 2025, driven by its strong fit for mid-sized commercial buildings, hospitality properties, and light industrial applications.

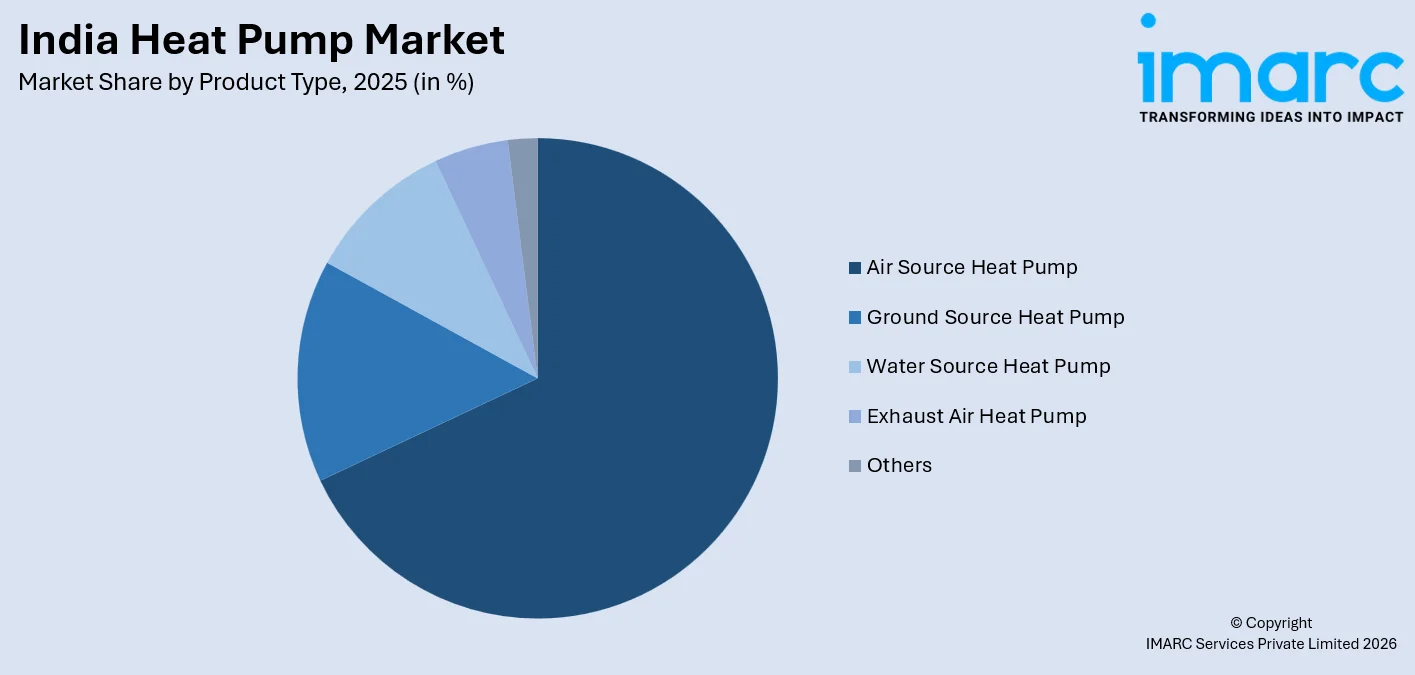

- By Product Type: Air source heat pump leads the market with a share of 68.5% in 2025, owing to lower installation costs, broad climate compatibility, and versatility across residential and commercial applications.

- By End Use Sector: Commercial represents the largest segment with a market share of 28.5% in 2025, driven by expanding corporate infrastructure, green building mandates, and rising demand for energy-efficient HVAC solutions.

- By Region: South India leads the market with a share of 30.5% in 2025, driven by favorable state-level energy efficiency policies, strong commercial infrastructure, and proactive clean energy adoption.

- Key Players: The India heat pump market features a moderately competitive landscape, with global HVAC corporations and domestic manufacturers competing across product type, capacity, and application segments on the basis of efficiency, innovation, and service network strength.

To get more information on this market Request Sample

The India heat pump market is experiencing robust expansion, underpinned by favorable policy frameworks, growing urban infrastructure, and evolving energy consumption patterns. The bureau of energy efficiency's standards and labeling programs and the perform, achieve and trade scheme are steering industries and commercial buildings toward higher-efficiency thermal systems. In December 2025, Purever partnered with South Korea’s Hyundai Corporation to introduce advanced heat pump technology in India, targeting residential, commercial and hospital applications and supporting broader energy‑efficiency adoption. The government's ambitious national climate target has catalyzed sustained investments in low-carbon heating and cooling technologies across residential, commercial, and industrial segments. South India has emerged as the leading regional market owing to additional state-level grants, proactive energy efficiency policies, and superior energy efficiency index rankings. The healthcare, hospitality, and industrial sectors are demonstrating compelling adoption momentum, as operators increasingly prioritize long-term energy cost savings and environmental compliance.

India Heat Pump Market Trends:

Accelerating Shift Toward Sustainable HVAC Infrastructure

India's built environment is undergoing a fundamental transformation as commercial developers, hospitality groups, and industrial operators prioritize low-carbon heating and cooling infrastructure. Regulatory frameworks are redirecting procurement away from conventional fossil-fuel-based heating systems toward thermodynamically efficient alternatives. Energy conservation building codes are increasingly mandating efficiency standards that favor heat pump-centered systems across new commercial and institutional construction. In August 2025, Triveni Turbines, in collaboration with the Indian Institute of Science, launched India’s first CO₂‑based high‑temperature heat pump capable of delivering heat up to 122 °C, marking a significant leap for industrial heat pump applications and supporting the shift from fossil fuels. Sector-wide decarbonization commitments are amplifying demand for high-temperature heat pumps capable of supporting industrial-grade process applications, creating durable structural demand across multiple verticals.

Deployment of IoT-Enabled Heat Pumps with Integrated Smart Controls

Modern heat pump deployments in India are increasingly incorporating smart connectivity, enabling real-time performance monitoring, remote diagnostics, and automated energy optimization. This trend is gaining prominence in large commercial campuses and hospitality properties, where facility managers demand seamless integration with building management systems. In February 2026, Midea Building Technologies launched its “Smart in One” platform, integrating heat pumps with BMS for real‑time monitoring, predictive maintenance, and energy optimization across commercial and hospitality buildings. Intelligent defrosting, variable-speed compressor controls, and adaptive load management are enhancing system efficiency and reducing lifecycle energy costs.

Growing Adoption Across Industrial and Process Heating Applications

High-temperature heat pumps are increasingly finding applications in India's food and beverage, chemicals and petrochemicals, and paper and pulp industries, where they serve as energy-efficient alternatives to steam-based heating. In November 2025, TRIGeN Decarbonisation signed an MoU with Thermax Ltd. to develop and deploy high‑temperature electric heat pumps (up to 180 °C) for industrial process heat, enabling cleaner thermal energy solutions across Indian manufacturing sectors. Waste heat recovery configurations are gaining traction, enabling industrial plants to recapture and reuse low-grade thermal energy from process streams. The expansion of domestic manufacturing capabilities is broadening product availability and reducing costs for industrial-grade configurations, substantially extending the addressable market well beyond traditional HVAC applications into process-heavy manufacturing verticals.

Market Outlook 2026-2034:

The India heat pump market is poised for sustained and progressive growth throughout the forecast period, driven by escalating energy efficiency mandates, large-scale urbanization, and the accelerating electrification of heating and cooling across diverse end-use sectors. Robust commercial real estate development, expanding industrial decarbonization requirements, and strengthening government policy frameworks will collectively underpin market revenue expansion. As heat pump technology becomes increasingly cost-competitive and consumer awareness deepens, adoption is expected to broaden significantly across residential, commercial, and industrial segments, reinforcing the market's long-term outlook. The market generated a revenue of USD 2,215.95 Million in 2025 and is projected to reach a revenue of USD 3,601.05 Million by 2034, growing at a compound annual growth rate of 5.38% from 2026-2034.

India Heat Pump Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

|

Rated Capacity |

10-20 kW |

34.2% |

|

Product Type |

Air Source Heat Pump |

68.5% |

|

End Use Sector |

Commercial |

28.5% |

|

Region |

South India |

30.5% |

Rated Capacity Insights:

- Up to 10 kW

- 10-20 kW

- 20-30 kW

- Above 30 kW

10-20 kW dominates with a market share of 34.2% of the total India heat pump market in 2025.

The 10-20 kW has emerged as the most commercially significant segment in India's heat pump market, reflecting its strong alignment with the thermal demand profiles of mid-sized commercial buildings, hospitality establishments, educational institutions, and food service operations. Systems within this range offer a compelling combination of operational efficiency, installation flexibility, and cost-effectiveness, making them a practical choice for building managers seeking meaningful energy savings without the infrastructure complexity associated with higher-capacity configurations. In April 2025, Carrier India launched a Centre of Excellence with Jamia Millia Islamia, training professionals on medium-capacity heat pumps for commercial applications.

Demand for systems in the 10-20 kW range is further supported by waste heat recovery initiatives in food and beverage and light manufacturing facilities, where these systems serve dehumidification, pasteurization support, and drying applications. The growing availability of locally manufactured units has improved supply chain reliability and reduced lead times considerably. As building codes increasingly mandate HVAC efficiency compliance across commercial construction projects, this capacity segment is expected to maintain its leadership position and broad commercial appeal throughout the forecast period.

Product Type Insights:

Access the comprehensive market breakdown Request Sample

- Air Source Heat Pump

- Ground Source Heat Pump

- Water Source Heat Pump

- Exhaust Air Heat Pump

- Others

Air source heat pump leads with a share of 68.5% of the total India heat pump market in 2025.

Air source heat pumps have established themselves as the dominant technology in India's heat pump landscape, driven by their lower capital costs, simpler installation requirements, and strong operational performance under India's predominantly warm climate. Their ability to function effectively across both heating and cooling modes makes them well-suited for mixed-use commercial buildings, hospitality establishments, and residential complexes. The versatility of air-to-water and air-to-air configurations has enabled broad applicability across diverse end-use settings throughout the country.

Continued product innovation from domestic and international manufacturers is further strengthening the position of air source heat pumps. The introduction of inverter-based variable-speed models with advanced seasonal energy efficiency ratings addresses growing demand for premium-grade systems compliant with regulatory labeling requirements. Manufacturers are also developing low-ambient variants capable of maintaining efficiency across a broader temperature range, extending market reach to northern regions and making air source heat pumps progressively accessible across commercial and mid-scale industrial segments nationwide.

End Use Sector Insights:

- Residential

- Commercial

- Hospitality

- Retail

- Education

- Food and Beverage

- Paper and Pulp

- Chemicals and Petrochemicals

- Others

Commercial exhibits a clear dominance with a 28.5% share of the total India heat pump market in 2025.

The commercial sector has emerged as the leading end-use segment for heat pumps in India, reflecting the rapid expansion of corporate office infrastructure, mixed-use commercial developments, and institutional buildings across Tier 1 and Tier 2 cities. In September 2025, field data from a CO₂ heat pump‑chiller at an 87‑room hotel in Goa showed efficient hot water production and simultaneous cooling performance, affirming effectiveness in Indian commercial buildings. Growing awareness of long-term operational cost savings, coupled with mandatory energy efficiency compliance requirements under building codes, is driving procurement decisions toward heat pump-based HVAC systems.

The commercial sector's appetite for heat pumps is further reinforced by the growing adoption of green building certification frameworks, which actively reward energy-efficient HVAC installations and incentivize developers to prioritize sustainable systems. Real estate developers in South India have benefited from additional state-level grants and strong rankings in the state energy efficiency Index, creating a more supportive adoption environment. As commercial real estate construction activity intensifies across urban and peri-urban markets and energy cost pressures on facility operators continue to rise, the commercial sector is expected to remain the dominant application area.

Regional Insights:

- North India

- West and Central India

- South India

- East and Northeast India

South India dominates with a market share of 30.5% of the total India heat pump market in 2025.

South India represents the most advanced regional market for heat pumps in India, benefiting from a convergence of proactive state-level energy policies, a high concentration of commercial and industrial infrastructure, and strong institutional awareness of energy efficiency technologies. Several southern states have consistently ranked among the top performers in national energy efficiency indices, with additional grants effectively offsetting installation costs for eligible projects. The region's thriving IT, hospitality, healthcare, and manufacturing sectors provide a broad and growing base of motivated end-users.

The healthcare and hospitality sectors in South India have been particularly active, with institutional buyers investing in heat pump systems to reduce energy overheads across large commercial and medical properties. The region's warm and humid climate is well-suited to air source heat pump operation, shortening payback periods and improving economic viability across diverse project types. As infrastructure development expands into secondary urban centers, South India is expected to maintain its lead in adoption intensity and market revenue contribution throughout the forecast period.

Market Dynamics:

Growth Drivers:

Why is the India Heat Pump Market Growing?

Supportive Government Policies and Regulatory Frameworks

India's heat pump market is receiving sustained impetus from an expanding ecosystem of government policies designed to promote energy efficiency and low-carbon technologies. As per sources, the Government of Andhra Pradesh and Energy Efficiency Services Limited (EESL) announced a first‑of‑its‑kind pilot air source heat pump project for tourist facilities in Araku, boosting policy support for heat pump adoption. Standards and labeling programs are being progressively extended to cover a wider range of HVAC equipment, steering buyers toward higher-efficiency systems. Energy conservation building codes are setting minimum efficiency benchmarks for commercial buildings, effectively orienting developers toward heat pump-centered solutions.

Rapid Urbanization and Commercial Infrastructure Expansion

India's accelerating urbanization trajectory is creating large volumes of new residential, commercial, and institutional floor space, all of which require modern and energy-efficient climate control solutions. The proliferation of corporate campuses, healthcare facilities, retail developments, and educational institutions in Tier 1 and Tier 2 cities is generating sustained procurement activity for advanced HVAC systems. Building codes now require efficiency standards that increasingly favor variable-speed reversible systems, creating a structural tailwind for heat pump adoption across new construction and retrofit projects throughout the country.

Rising Energy Costs and Growing Focus on Operational Efficiency

Escalating electricity and fossil fuel costs are compelling building owners, facility managers, and industrial operators across India to prioritize technologies that deliver measurable reductions in long-term energy expenditure. Heat pumps, with their superior coefficient of performance relative to conventional heating systems, present a compelling economic case that strengthens as energy prices rise. In November 2025, a study reported heatwaves alone drove nearly a 9% surge in peak electricity demand in India, deepening reliance on fossil‑fuel‑based power and intensifying operational costs for commercial and industrial consumers. This cost-driven motivation is reinforcing technology adoption across commercial, hospitality, and industrial segments, encouraging operators to view heat pumps as a strategic investment in operational resilience and sustained cost competitiveness.

Market Restraints:

What Challenges the India Heat Pump Market is Facing?

High Upfront Capital Costs

Despite delivering superior long-term energy savings, heat pump systems require significantly higher upfront investment compared to conventional heating and cooling alternatives. Installation costs for ground source and water source systems are particularly elevated, including substantial site preparation and infrastructure work. This financial barrier disproportionately affects price-sensitive buyers in residential and small commercial segments, limiting broader market penetration despite favorable lifecycle economics.

Limited Skilled Workforce for Installation and Maintenance

The successful deployment and ongoing operation of heat pump systems require specialized technical expertise that remains unevenly distributed across India. Trained HVAC engineers and certified technicians are concentrated primarily in major metropolitan areas, leaving Tier 2 and Tier 3 markets underserved. This skills gap increases installation lead times, elevates maintenance costs, and deters risk-averse buyers from committing to heat pump investments in regions with limited-service infrastructure.

Grid Reliability and Power Quality Concerns

Heat pumps are electrically powered systems whose performance is directly contingent on a stable and reliable electricity supply. In regions where power supply remains intermittent or subject to voltage fluctuations, operational viability is compromised and equipment longevity reduced. Until grid reliability improves uniformly across all regions, electricity supply uncertainty will continue to constrain heat pump adoption beyond well-served urban and industrial markets.

Competitive Landscape:

The India heat pump market features a moderately competitive landscape, shaped by the presence of established multinational HVAC corporations and a growing base of domestic manufacturers competing across product type, capacity, and end-use application segments. Global players leverage deep technological expertise, extensive product portfolios, and strong brand recognition to maintain their market positions, while domestic manufacturers increasingly compete on cost-effectiveness, localized service networks, and faster delivery timelines. Competitive differentiation is centered on energy efficiency ratings, smart connectivity features, compliance with regulatory labeling requirements, and the ability to offer customized solutions for diverse commercial, hospitality, and industrial applications. Ongoing investments in local manufacturing capabilities and after-sales service infrastructure are further intensifying competition across all market tiers.

Recent Developments:

- In July 2025, Racold launched its 500-litre commercial heat pump water heater in Delhi, designed for energy efficiency, sustainability, and reliability. Targeting hospitality, healthcare, manufacturing, and educational sectors, the system features high COP, reduced operational costs, lower carbon emissions, and consistent performance for large-scale commercial applications.

India Heat Pump Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Rated Capacities Covered | Up to 10 kW, 10–20 kW, 20–30 kW, Above 30 kW |

| Product Types Covered | Air Source Heat Pump, Ground Source Heat Pump, Water Source Heat Pump, Exhaust Air Heat Pump, Others |

| End Use Sectors Covered | Residential, Commercial, Hospitality, Retail, Education, Food and Beverage, Paper and Pulp, Chemicals and Petrochemicals, Others |

| Regions Covered | North India, West and Central India, South India, East and Northeast India |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Heat Pump Market Research Report and Industry Forecast Report

The India heat pump market size was valued at USD 2,215.95 Million in 2025.

The India heat pump market is expected to grow at a compound annual growth rate of 5.38% from 2026-2034 to reach USD 3,601.05 Million by 2034.

10-20 kW holds the largest share in the India heat pump market, owing to its optimal fit for mid-sized commercial buildings, hospitality properties, and light industrial applications, offering an ideal balance of operational efficiency, installation flexibility, and cost-effectiveness.

Key factors driving the India heat pump market include supportive government policies, rapid urbanization and commercial infrastructure expansion, rising industrial electrification, and growing consumer and industry awareness of energy efficiency and sustainability.

Major challenges facing the India heat pump market include high upfront capital costs that deter price-sensitive buyers, a limited pool of skilled technicians for installation and maintenance, and persistent concerns surrounding grid reliability and power quality across certain regions of India.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)