India Hemodialysis Market Size, Share, Trends and Forecast by Segment, Modality, End User, and Region, 2026-2034

India Hemodialysis Market Summary:

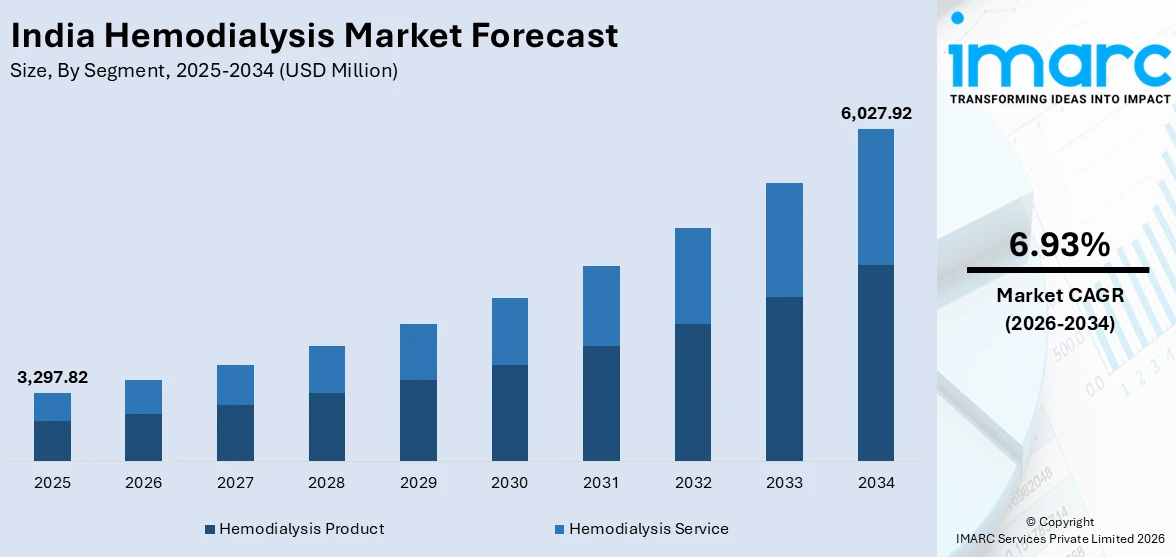

The India hemodialysis market size was valued at USD 3,297.82 Million in 2025 and is projected to reach USD 6,027.92 Million by 2034, growing at a compound annual growth rate of 6.93% from 2026-2034.

The India hemodialysis market is experiencing sustained expansion driven by the escalating burden of chronic kidney disease, widespread prevalence of diabetes and hypertension, and accelerating government-led healthcare infrastructure development. Increasing urbanization, lifestyle-related health risks, and growing awareness of early renal diagnosis are amplifying the demand for hemodialysis services. Technological advancements in dialysis equipment, including AI-enabled and cloud-connected machines, are enhancing treatment efficacy and accessibility. Additionally, the expansion of dialysis networks through public-private partnerships and the growing presence of organized dialysis service providers are strengthening the India hemodialysis market share.

Key Takeaways and Insights:

- By Segment: Hemodialysis product dominates the market with a share of 55% in 2025, driven by continuous demand for advanced dialysis machines, dialyzers, and consumables essential for effective renal replacement therapy across hospital and independent dialysis facilities.

- By Modality: Conventional hemodialysis leads the market with a share of 70% in 2025, owing to its established clinical protocols, widespread availability in hospital settings, and proven efficacy in managing end-stage renal disease patients requiring regular dialysis sessions.

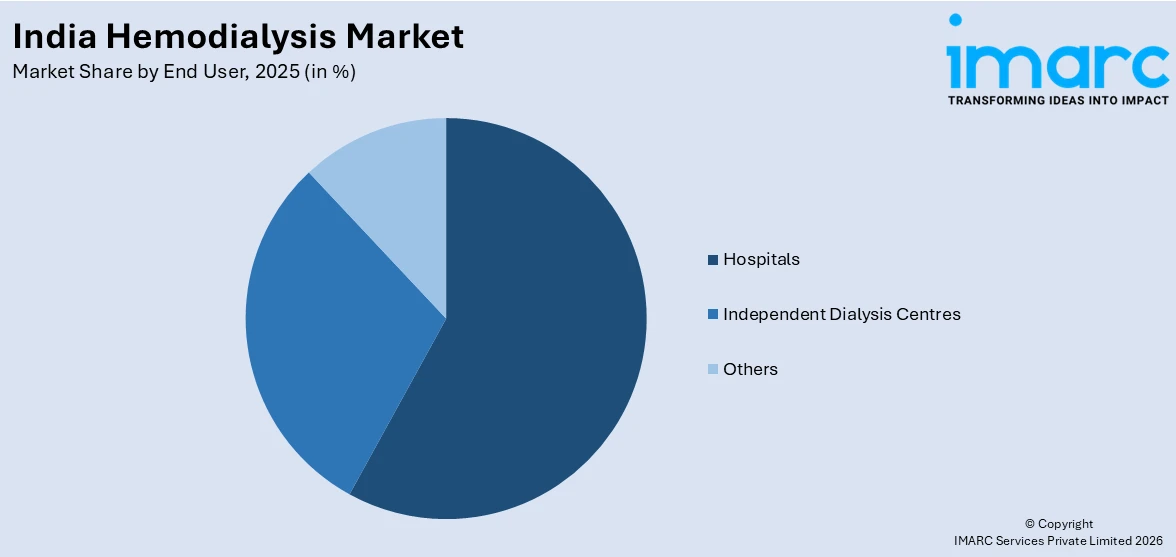

- By End User: Hospitals represent the largest segment with a market share of 58% in 2025, supported by comprehensive nephrology departments, availability of trained medical staff, advanced diagnostic infrastructure, and integrated patient management systems for critical renal care.

- Key Players: The India hemodialysis market exhibits a moderately competitive landscape with established multinational medical device manufacturers competing alongside expanding domestic dialysis service providers, fostering innovation in technology, service delivery models, and affordability across urban and semi-urban markets.

To get more information on this market Request Sample

The India hemodialysis market is evolving rapidly as the country confronts a growing burden of chronic kidney disease linked to rising diabetes and hypertension prevalence. The government’s Pradhan Mantri National Dialysis Programme has significantly expanded access, with 1,704 dialysis centres operational across 751 districts in all 36 States and Union Territories as of June 2025. Simultaneously, the organized private dialysis sector is scaling operations, with leading service providers expanding into tier II and tier III cities through hospital partnerships and public-private partnership models. Technological innovation is reshaping the market, with the introduction of indigenously developed AI-enabled hemodialysis machines that integrate real-time remote monitoring and cloud connectivity, reducing treatment costs and improving patient outcomes. The convergence of government support, private sector investment, and technological advancement is creating a robust foundation for sustained India hemodialysis market growth.

India Hemodialysis Market Trends:

Integration of AI and IoT Technologies in Dialysis Equipment

The India hemodialysis market is witnessing a significant shift toward technology-enabled dialysis solutions, with artificial intelligence and Internet of Medical Things transforming clinical workflows and patient monitoring. Advanced hemodialysis systems incorporating artificial intelligence, predictive safety mechanisms, and cloud-integrated tele-nephrology capabilities are transforming renal care delivery. These smart machines allow healthcare professionals to remotely track patient parameters, optimize treatment settings, and make timely adjustments to improve safety and clinical outcomes. The development of indigenous, digitally connected dialysis platforms is particularly supporting expansion into primary and community healthcare facilities, strengthening access to quality renal therapy in semi-urban and rural areas while reducing reliance on imported technologies.

Expansion of Organized Dialysis Networks into Underserved Areas

Organized dialysis service providers are rapidly expanding their footprint beyond metropolitan centres to reach patients in smaller cities and towns. This trend is driven by the growing recognition that dialysis services must be geographically accessible to reduce treatment dropout rates and improve patient compliance. For instance, in October 2025, NephroCare Health Services (NephroPlus) crossed the milestone of 500 clinics globally, with 125 clinics operating in tier II cities and 218 clinics in tier III cities across India as of March 2025. The company generated over 1,642 jobs in these underserved markets during fiscal year 2025, reflecting the sector’s commitment to equitable healthcare delivery.

Growing Emphasis on Home-Based Hemodialysis Solutions

Home hemodialysis is emerging as an important trend in India, driven by patient preference for treatment convenience, reduced travel burden, and improved quality of life. Healthcare providers are increasingly offering home-based dialysis programs that leverage portable machines and remote monitoring technologies to deliver clinical-grade treatment in residential settings. Leading dialysis service providers are increasingly extending home hemodialysis offerings across major metropolitan areas. Companies are actively working toward introducing structured home-based dialysis models, while several hospital networks are designing standardized home care protocols to address rising demand for patient-focused renal treatment. This shift reflects a broader transition toward decentralized care delivery, enabling greater convenience, improved quality of life, and enhanced accessibility for individuals requiring long-term dialysis support.

Market Outlook 2026-2034:

The India hemodialysis market is positioned for robust expansion over the forecast period, supported by increasing chronic kidney disease incidence, expanding healthcare infrastructure, and rising government investment in renal care accessibility. The convergence of digital health technologies, AI-powered treatment optimization, and scalable dialysis service delivery models is expected to enhance treatment outcomes and market penetration. Growing private sector participation and public-private partnerships will further accelerate the establishment of dialysis centres across underserved regions. The market generated a revenue of USD 3,297.82 Million in 2025 and is projected to reach a revenue of USD 6,027.92 Million by 2034, growing at a compound annual growth rate of 6.93% from 2026-2034.

India Hemodialysis Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

|

Segment |

Hemodialysis Product |

55% |

|

Modality |

Conventional Hemodialysis |

70% |

|

End User |

Hospitals |

58% |

Segment Insights:

- Hemodialysis Product

- Machines

- Dialyzers

- Others

- Hemodialysis Service

- In-center Services

- Home Services

Hemodialysis product dominates with a market share of 55% of the total India hemodialysis market in 2025.

The hemodialysis product segment’s leadership reflects the essential and recurring demand for dialysis machines, dialyzers, bloodlines, and concentrates that form the operational backbone of every hemodialysis session. India’s growing dialysis infrastructure, comprising an estimated 50,000 machines, generates consistent demand for replacement consumables and equipment upgrades. The availability of domestically manufactured advanced dialysis systems is further strengthening this segment. The introduction of AI-enabled hemodialysis machines developed within the country has improved affordability and reduced overall ownership costs compared to imported equipment. As a result, advanced renal care technology is becoming more accessible to smaller hospitals and healthcare facilities, supporting wider adoption and enhancing treatment capacity across diverse care settings.

Ongoing expansion in product demand is further reinforced by public procurement efforts under national dialysis initiatives, which have facilitated the installation of hemodialysis machines across numerous centres and districts nationwide. In parallel, strategic manufacturing collaborations between domestic medical technology companies and established industrial partners are enhancing local production capabilities. These partnerships are contributing to greater self-reliance in dialysis equipment manufacturing while reducing dependence on imported systems and strengthening the country’s renal care infrastructure.

Modality Insights:

- Conventional Hemodialysis

- Short Daily Hemodialysis

- Nocturnal Hemodialysis

Conventional hemodialysis leads the market with a share of 70% of the total India hemodialysis market in 2025.

Conventional hemodialysis maintains its dominant position owing to its well-established treatment protocols, broad availability across hospital and independent dialysis centre settings, and compatibility with existing healthcare infrastructure. This treatment approach generally requires multiple weekly sessions of several hours each and continues to represent the primary therapy recommended by nephrologists for individuals with end-stage renal disease. National dialysis initiatives largely focus on supporting conventional hemodialysis services, ensuring widespread availability across public healthcare facilities. These programs aim to provide cost-free treatment access to financially disadvantaged patients living with kidney failure, thereby strengthening equitable access to essential renal care services.

The preference for conventional hemodialysis is reinforced by the availability of trained technicians, standardized clinical protocols, and comprehensive insurance coverage under government health schemes. While alternative modalities such as short daily and nocturnal hemodialysis are gaining attention for their potential clinical benefits, conventional hemodialysis continues to account for most dialysis sessions performed in India due to established patient familiarity, institutional readiness, and the logistical challenges associated with implementing more intensive or extended treatment schedules at scale.

End User Insights:

Access the comprehensive market breakdown Request Sample

- Hospitals

- Independent Dialysis Centres

- Others

Hospitals represent the largest share at 58% of the total India hemodialysis market in 2025.

Hospitals maintain their leadership in the end user segment due to their comprehensive clinical infrastructure, availability of specialized nephrology departments, and ability to manage complex patients requiring multidisciplinary care. Dialysis units within hospital settings benefit from comprehensive infrastructure, including in-house laboratory facilities, emergency care services, and access to transplant programs, advantages that standalone centres often lack. Large hospital networks continue to expand their renal care footprint by establishing new dialysis clinics through strategic collaborations with local authorities. These facilities typically provide dedicated dialysis beds, specialist consultations, and integrated rehabilitation services, enhancing the overall continuum of care for patients requiring long-term renal therapy.

The hospital segment continues to gain momentum through public–private partnership frameworks that allow organized dialysis providers to manage dedicated units within government and private hospital premises. Under this model, specialized renal care operators utilize existing hospital infrastructure while contributing focused dialysis management expertise and operational efficiency. This integrated approach has been especially effective in broadening access to dialysis services in tier II and tier III cities, where standalone centres often struggle with sustainability. By aligning with hospitals, providers benefit from steady patient inflow, clinical support systems, and shared resources, thereby enhancing service reach and long-term operational stability.

Regional Insights:

- North India

- West and Central India

- South India

- East and Northeast India

North India represents a significant market for hemodialysis services, driven by high population density, elevated prevalence of diabetes and hypertension in states such as Uttar Pradesh, Delhi, and Rajasthan, and expanding healthcare infrastructure in both urban and semi-urban centres.

West and Central India benefit from strong commercial and industrial centres in Maharashtra and Gujarat that support advanced healthcare delivery, with Mumbai and Pune serving as major hubs for organized dialysis service providers and medical device manufacturing.

South India has emerged as a key market due to its well-developed healthcare ecosystem, higher healthcare literacy, and the concentration of leading hospital chains and specialized dialysis networks across Tamil Nadu, Karnataka, Telangana, and Andhra Pradesh.

East and Northeast India presents significant growth potential, with increasing government investment under the PMNDP to establish dialysis centres in underserved districts, although the region faces challenges related to healthcare workforce availability and infrastructure gaps.

Market Dynamics:

Growth Drivers:

Why is the India Hemodialysis Market Growing?

Rising Prevalence of Chronic Kidney Disease and Associated Comorbidities

India is experiencing a significant escalation in chronic kidney disease cases, primarily driven by the growing burden of diabetes and hypertension across both urban and rural populations. The country records approximately 2.2 lakh new end-stage renal disease cases annually, generating demand for an estimated 3.4 crore dialysis sessions each year. Population-based epidemiological assessments show that chronic kidney disease (CKD) affects a significant proportion of individuals across various regions of India. Diabetes and hypertension are consistently identified as the leading underlying conditions accelerating renal impairment, thereby contributing to the growing need for long-term dialysis management and structured renal care services nationwide. The increasing adoption of sedentary lifestyles, unhealthy dietary patterns, and rising obesity rates among younger demographics are accelerating the incidence of metabolic disorders that predispose individuals to renal complications, expanding the patient pool requiring hemodialysis intervention.

Government-Led Expansion of Dialysis Infrastructure

The Government of India has reinforced its focus on improving dialysis access through dedicated policy measures and sustained healthcare infrastructure development. A flagship initiative under the National Health Mission provides free hemodialysis and peritoneal dialysis services to economically disadvantaged patients living with advanced kidney failure. In addition, a centralized digital platform integrated with the Ayushman Bharat Health Account system supports streamlined patient registration and service portability nationwide, promoting continuity of care and improving access under a unified dialysis framework.

Technological Innovation and Indigenous Manufacturing Capabilities

India’s hemodialysis market is undergoing significant transformation driven by technological innovation and the rise of domestic manufacturing, reducing reliance on imported equipment. The introduction of AI-enabled, cloud-connected, and IoT-integrated dialysis systems is improving treatment accuracy, supporting remote patient monitoring, and enhancing operational efficiency for healthcare providers. Indigenous development of advanced smart dialysis machines has strengthened the country’s position in high-value medical device production. Strategic collaborations between medical technology companies and established industrial partners are further expanding manufacturing capabilities, reinforcing supply chain resilience and accelerating the adoption of advanced renal care solutions across healthcare facilities.

Market Restraints:

What Challenges the India Hemodialysis Market is Facing?

Acute Shortage of Trained Nephrologists and Dialysis Technicians

India faces a critical shortage of qualified nephrology professionals, with an estimated 3,000 practising nephrologists serving a population of over 1.4 billion. This disparity severely limits the capacity to diagnose, treat, and manage chronic kidney disease patients effectively, particularly in rural and semi-urban areas where specialist availability is extremely constrained, resulting in delayed diagnosis and suboptimal treatment outcomes.

High Treatment Costs and Limited Insurance Coverage

Despite government subsidies, hemodialysis remains financially burdensome for many patients due to recurring costs associated with sessions, consumables, medications, and transportation. Limited private health insurance coverage for long-term dialysis treatment creates significant out-of-pocket expenses, leading to treatment discontinuation and financial catastrophe for families, especially those above the poverty line threshold but with limited disposable income.

Inadequate Infrastructure in Rural and Remote Regions

While urban centres have witnessed significant expansion of dialysis facilities, rural and remote areas continue to face substantial infrastructure gaps. The lack of reliable electricity supply, clean water access, and transportation networks in many regions hampers the establishment and sustained operation of dialysis centres. These logistical challenges increase treatment dropout rates and limit effective healthcare delivery to populations with the greatest unmet need.

Competitive Landscape:

The India hemodialysis market exhibits a dynamic competitive landscape characterized by the presence of established multinational medical device manufacturers, rapidly expanding domestic dialysis service providers, and emerging indigenous medical technology companies. Market participants compete across multiple dimensions, including product innovation, service delivery scale, geographical coverage, and cost optimization. Strategic mergers and acquisitions, public-private partnership agreements, and investments in technology-enabled service platforms are intensifying competition. The growing emphasis on affordable and accessible dialysis solutions is prompting both domestic and international players to develop localized strategies, expand into underserved markets, and invest in indigenous manufacturing capabilities to strengthen their competitive positioning across the value chain.

Recent Developments:

- December 2025: Lords Mark Industries received the CDSCO licence to manufacture Class C AI-based smart hemodialysis machines, along with EU CE marking certification, becoming one of only six brands worldwide with this certification for dialysis systems, significantly advancing India’s med-tech manufacturing capabilities.

- November 2025: Lords Mark Industries acquired an 85% stake in Renalyx Health Systems, the Bengaluru-based developer of India’s first indigenous AI-enabled hemodialysis machine, with plans to reach 92% holding by March 2026 and leverage its national distribution network for faster market penetration.

- June 2025: Renalyx Health Systems, headquartered in Bengaluru, introduced an advanced hemodialysis system that integrates artificial intelligence and cloud connectivity, enabling real-time remote supervision and seamless clinical data integration. The newly launched device, branded as RxT21, is priced at ₹6.7 lakh and is positioned as a cost-effective alternative to imported dialysis machines, offering substantially lower pricing while maintaining smart monitoring capabilities.

India Hemodialysis Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Segments Covered |

|

| Modalities Covered | Conventional Hemodialysis, Short Daily Hemodialysis, Nocturnal Hemodialysis |

| End Users Covered | Hospitals, Independent Dialysis Centers, Others |

| Regions Covered | North India, West and Central India, South India, East and Northeast India |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Hemodialysis Market Report

The India hemodialysis market size was valued at USD 3,297.82 Million in 2025.

The India hemodialysis market is expected to grow at a compound annual growth rate of 6.93% from 2026-2034 to reach USD 6,027.92 Million by 2034.

The hemodialysis product held the largest market share at 55% in 2025, driven by sustained demand for dialysis machines, dialyzers, and consumables essential for effective renal replacement therapy across India’s expanding network of dialysis facilities.

Key factors driving the India hemodialysis market include rising chronic kidney disease prevalence linked to diabetes and hypertension, expanding government dialysis infrastructure under PMNDP, technological innovation in AI-enabled dialysis equipment, and growing organized dialysis service networks.

Major challenges include acute shortage of trained nephrologists and dialysis technicians, high recurring treatment costs with limited insurance coverage, inadequate infrastructure in rural and remote regions, and significant patient dropout rates due to financial and logistical barriers.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade