India Home Appliances Market Size, Share, Trends and Forecast by Product, Distribution Channel, and Region, 2026-2034

India Home Appliances Market Size, Share, Trends & Forecast (2026-2034)

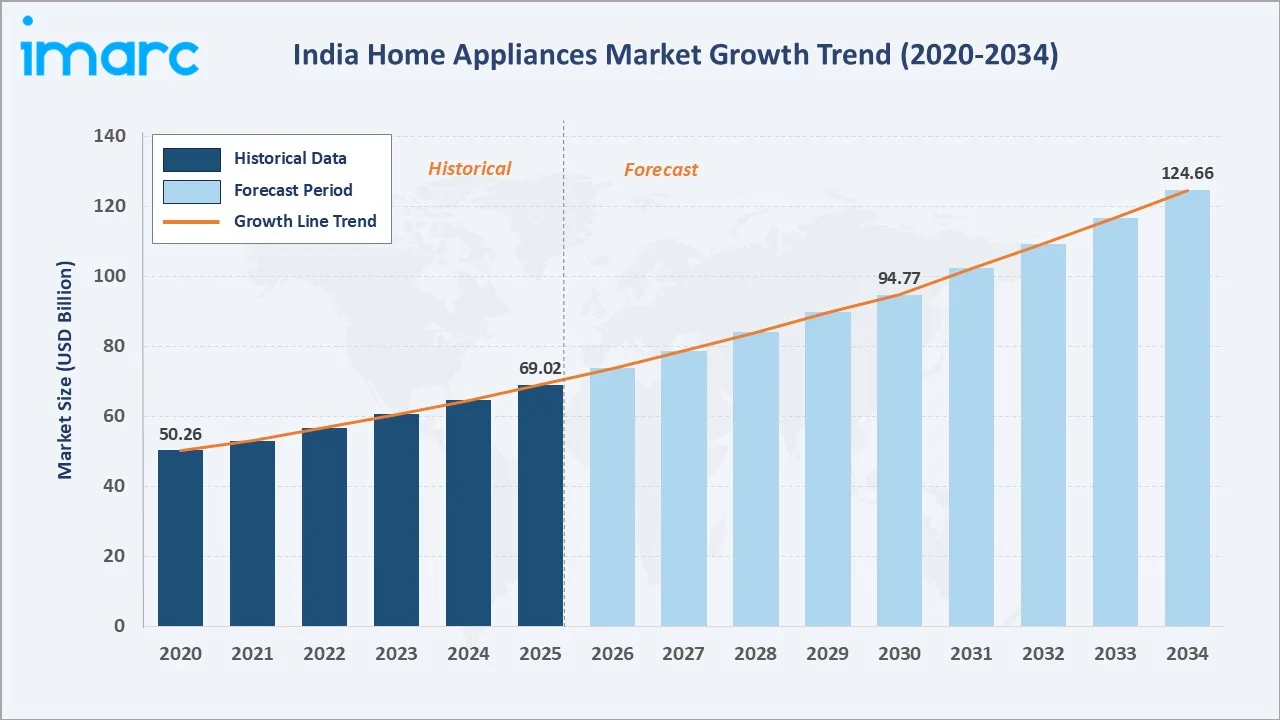

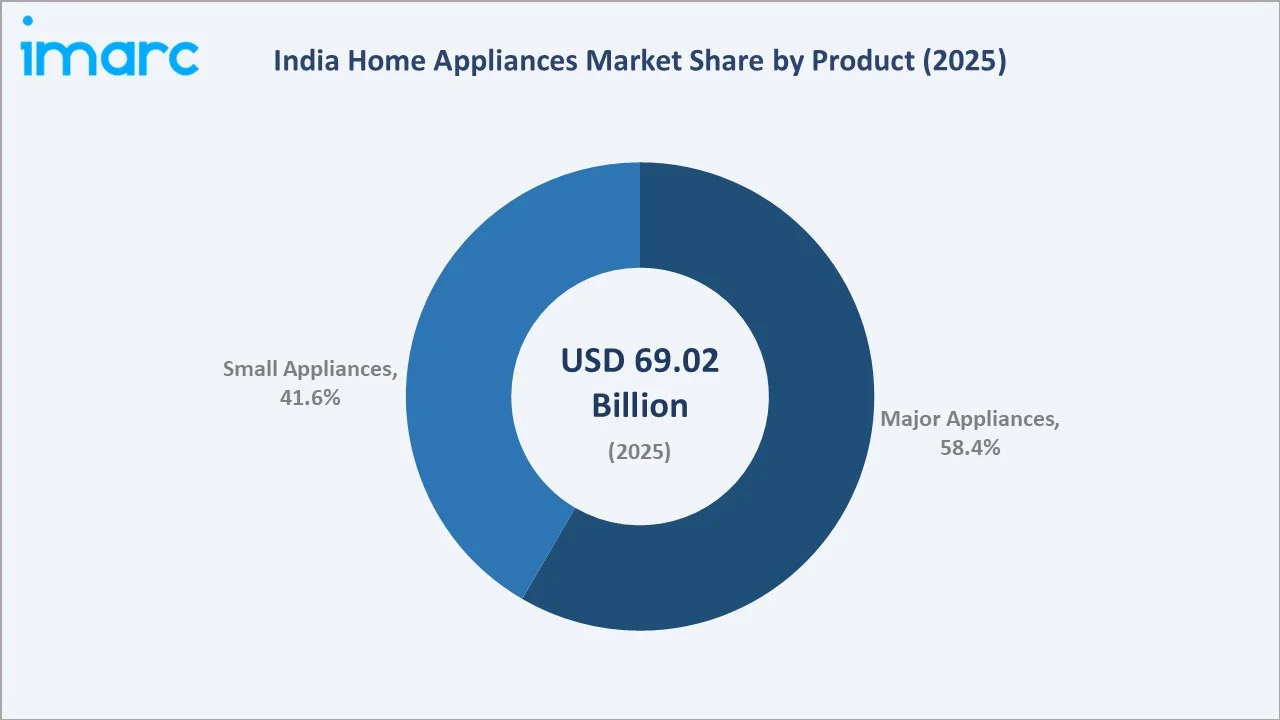

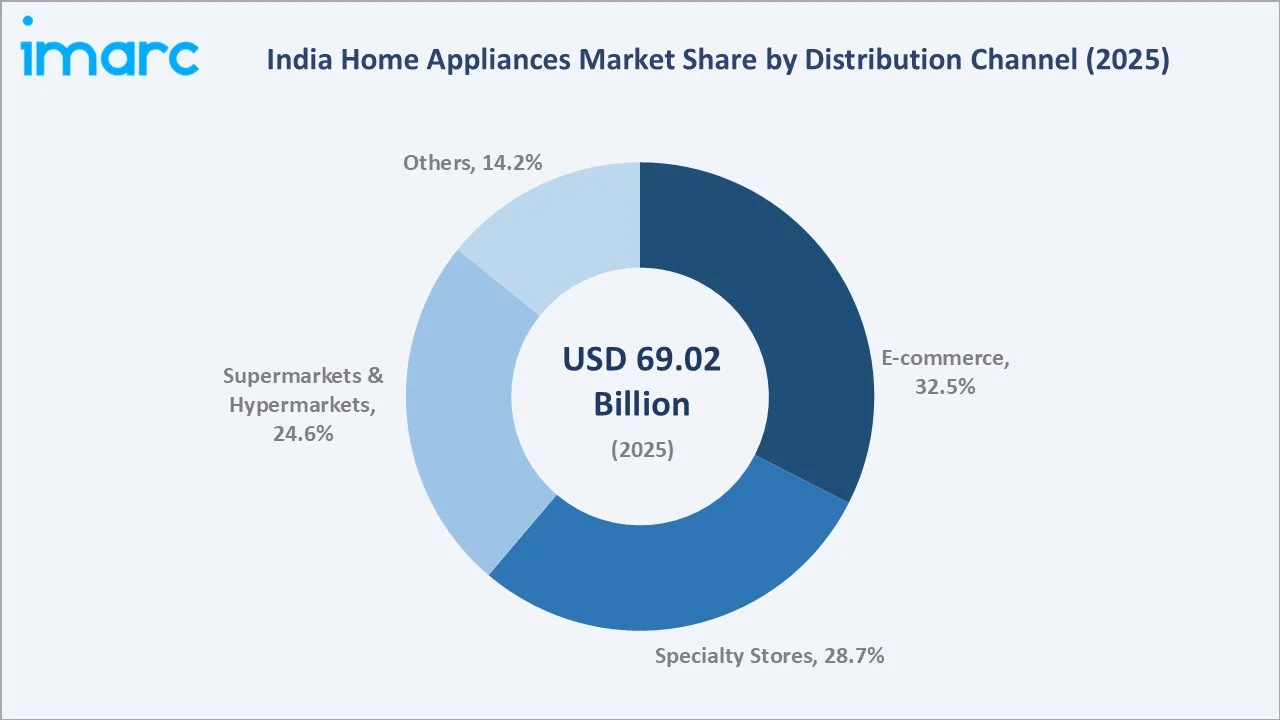

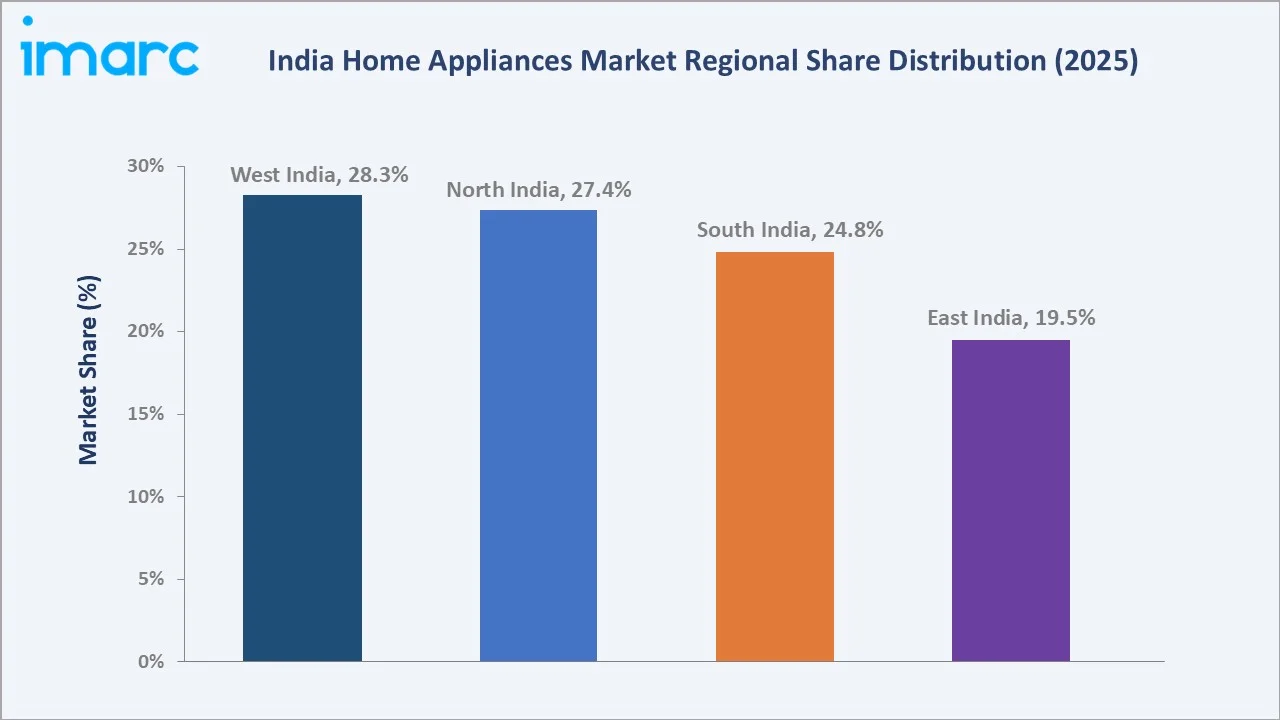

The India home appliances market size reached USD 69.02 Billion in 2025 and is projected to reach USD 124.66 Billion by 2034, exhibiting a CAGR of 6.55% during the forecast period 2026-2034. Rising disposable incomes, rapid urbanization, government "Make in India" incentives, expanding e-commerce penetration, and strong consumer preference for smart, energy-efficient appliances are the primary drivers of India home appliances market growth. Major Appliances commanded 58.4% of the product mix in 2025, while E-commerce emerged as the dominant distribution channel at 32.5%. West India accounted for the largest regional share at 28.3% in 2025, reflecting higher urban density and robust retail infrastructure.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 69.02 Billion |

|

Forecast Market Size (2034) |

USD 124.66 Billion |

|

CAGR (2026-2034) |

6.55% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

West India (28.3% share, 2025) |

|

Fastest Growing Region |

South India (CAGR ~7.2%) |

|

Leading Product Segment |

Major Appliances (58.4%, 2025) |

|

Leading Distribution Channel |

E-commerce (32.5%, 2025) |

To get more information on this market, Request Sample

Executive Summary

The India home appliances market is experiencing a structural transformation fuelled by a rapidly growing middle class, technology-driven consumer expectations, and a shift toward convenience-oriented lifestyles. Valued at USD 69.02 Billion in 2025, the market is forecast to nearly double to USD 124.66 Billion by 2034 at a CAGR of 6.55%. As per industry reports, India's middle class is expected to nearly double to 61% of the total population by 2046–2047, representing a massive latent demand pool for both basic and premium appliances across urban and rural segments.

Major Appliances retained dominance at 58.4% in 2025 – spanning refrigerators, air conditioners, washing machines, and dishwashers – driven by higher unit economics and government energy-efficiency star rating mandates. The E-commerce distribution channel grew to 32.5% in 2025, led by Amazon India and Flipkart's aggressive same-day delivery expansions in tier-2 cities. Smart appliance categories – including Wi-Fi-enabled air conditioners and AI-powered washing machines – are growing at an estimated CAGR of ~13.5%, well above the market average, driven by falling IoT hardware costs and rising broadband penetration, which crossed millions of users in India in 2024.

West India commands the largest regional share at 28.3% in 2025, anchored by Maharashtra and Gujarat's strong urban retail ecosystem. North India follows at 27.4%, with Delhi-NCR and Punjab driving premium segment sales. South India at 24.8% is growing fastest at an estimated CAGR of ~7.2%, driven by IT-sector affluence in Bengaluru, Hyderabad, and Chennai and a high propensity to adopt energy-efficient appliances. East India at 19.5% remains the fastest-expanding frontier market.

Key Market Insights

|

Insight |

Data |

|

Largest Product Segment |

Major Appliances – 58.4% share (2025) |

|

Leading Distribution Channel |

E-commerce – 32.5% share (2025) |

|

Leading Region |

West India – 28.3% revenue share (2025) |

|

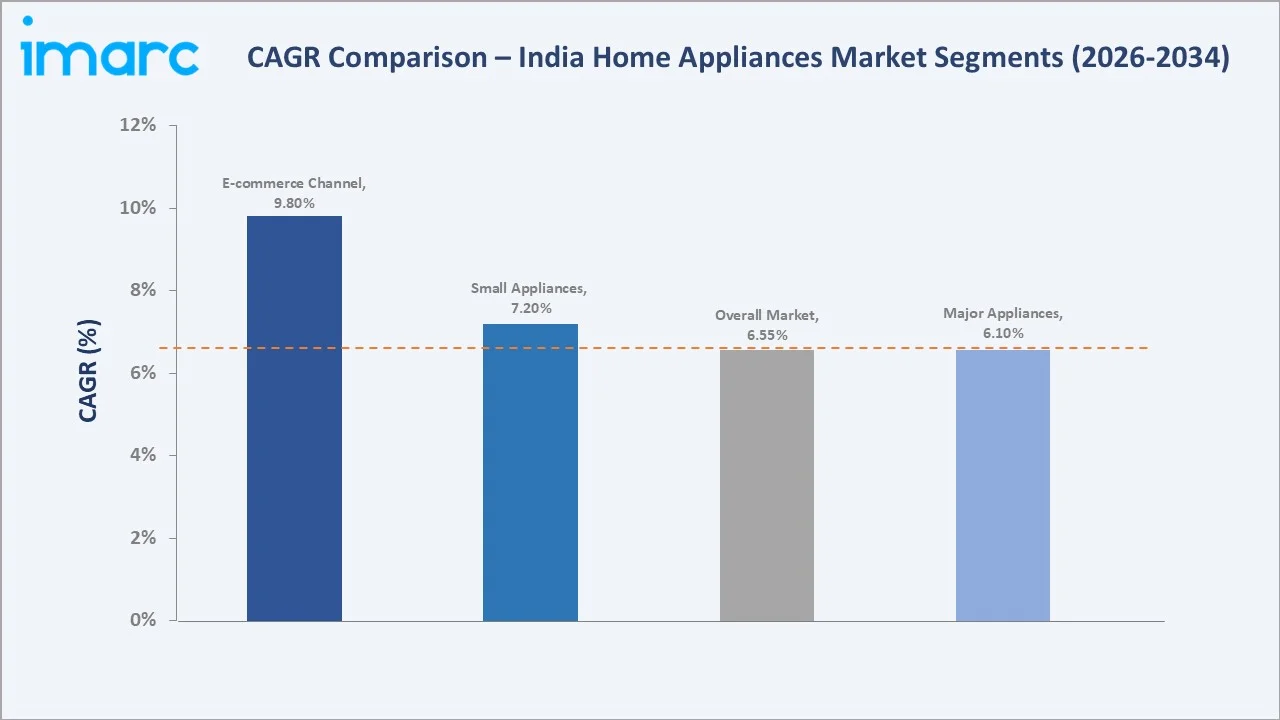

Fastest Growing Channel |

E-commerce – CAGR ~9.8% (2026-2034) |

|

Top Companies |

Samsung, LG, Godrej, Whirlpool, Haier, Voltas, IFB |

|

Market Opportunity |

Smart & IoT-enabled appliances growing at ~13.5% CAGR |

Key Analytical Observations Supporting the Above Data:

- Major Appliances' 58.4% dominance in 2025 reflects rising aspirational demand for refrigerators, ACs, and washing machines across urban and semi-urban households, supported by easy consumer financing and EMI schemes from brands like Samsung and LG.

- E-commerce's 32.5% channel share in 2025 signals a fundamental retail transformation. Platforms like Amazon India and Flipkart captured over 50% of appliance sales during festive sale events in 2024, underscoring the channel's growing strategic importance.

- West India's 28.3% regional leadership reflects Mumbai, Pune, Ahmedabad, and Surat's robust retail infrastructure, high per-capita income, and strong brand presence of Godrej, Voltas, and Whirlpool in the region.

- Government Production Linked Incentive (PLI) scheme allocated INR 6,238 crore for appliance manufacturing, attracting 42 approved applicants and targeting to reduce AC manufacturing cost disadvantage from 18% to 12% by 2026.

Global India Home Appliances Market Overview

Home appliances are electromechanical devices used in Indian households to perform domestic tasks including cooking, food preservation, space conditioning, laundry, and personal care. They span two broad product tiers: Major Appliances (refrigerators, washing machines, air conditioners, dishwashers) with unit values typically above INR 15,000 (~USD 180), and Small Appliances (mixers, irons, vacuum cleaners, water purifiers) priced below INR 15,000.

The India home appliances ecosystem encompasses domestic manufacturers, multinational OEM brands, component specialists, logistics networks, and multi-channel retail systems covering modern retail, kirana-adjacent electronics stores, and e-commerce platforms. The Bureau of Energy Efficiency (BEE) star rating framework governs energy consumption standards and is a critical demand-side driver. Macroeconomic enablers include India's GDP growth target of 6.5%–7.0% annually through 2030, a young median age of 28 years, and accelerating rural electrification with grid connectivity now exceeding 99.9% of villages.

Market Dynamics

To evaluate market opportunities, Request Sample

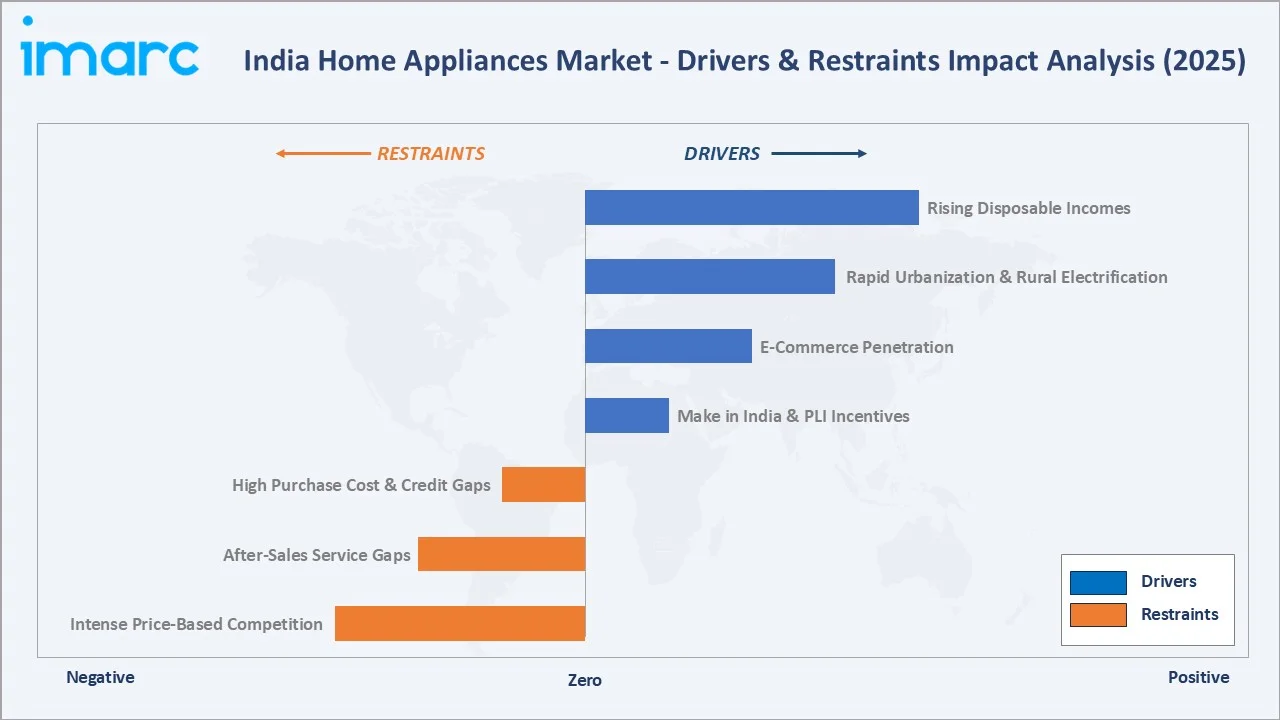

Market Drivers

- Rising Disposable Incomes & Middle-Class Expansion: India's per capita disposable income for the year 2023–24 has surged to INR 2.14 lakh, showing a robust growth rate of 13.3% for the year FY23. A doubling middle-class population to 61% by 2047 creates structural long-term demand for both major and small appliances across all price tiers.

- Rapid Urbanization & Rural Electrification: Over 40% of India's population is projected to be urban by 2030. Rural household electrification crossing 99.9% of villages opens a massive untapped base for first-time appliance buyers, particularly refrigerators and fans.

- E-Commerce Penetration & Digital Retail Infrastructure: India's e-commerce penetration in appliances is projected to surpass 40% by 2028. Flipkart and Amazon India's Big Billion Days and Great Indian Festival events each generate USD 2–3 Billion in electronics and appliance GMV.

- Make in India & PLI Policy Incentives: The PLI scheme's INR 6,238 crore allocation for white goods is catalysing domestic manufacturing, enabling brands to reduce import-led cost premiums and price appliances more competitively for price-sensitive Indian consumers.

Market Restraints

- High Initial Purchase Cost & Credit Penetration Gaps: Despite EMI financing, appliances priced above INR 30,000 remain aspirational for bottom-of-pyramid households. Rural areas with limited access to formal credit remain a penetration barrier.

- After-Sales Service Gaps in Tier-2/Tier-3 Cities: Authorised service centres for premium brands are concentrated in top-30 cities. Service gaps in smaller towns suppress conversion rates and fuel preference for local unbranded products.

Market Opportunities

- Smart & IoT-Enabled Appliance Segment: The smart home devices market in India was valued at USD 8.33 Billion in 2025, projected to grow at 23.33% CAGR to USD 54.97 Billion by 2034. Integration of appliances with voice assistants (Alexa, Google Home) and mobile apps represents a premium revenue expansion opportunity.

- Premium Segment Premiumization in Urban Markets: India's urban consumer is rapidly adopting inverter-technology ACs, multi-door refrigerators, and front-load washer-dryers. The premium appliance segment (INR 50,000+) is growing at ~11% CAGR, significantly outpacing the base market.

- Tier-2 & Tier-3 City Penetration: Refrigerator penetration in rural India is below 25%, AC penetration below 10%, and washing machine penetration at 16%. Each percentage point increase in penetration across these underpenetrated markets represents USD 600M–800M in incremental market opportunity.

Market Challenges

- Intense Price-Based Competition from Chinese & Domestic Brands: Haier, Midea, and Hisense compete aggressively on price in the sub-INR 20,000 segment, creating margin pressure on premium global brands and domestic incumbents like Godrej.

- Consumer Trust & Brand Switching in Online Channels: E-commerce's rapid growth brings increased exposure to counterfeit products and unverified third-party sellers, eroding consumer trust and increasing return rates that inflate fulfilment costs for brands.

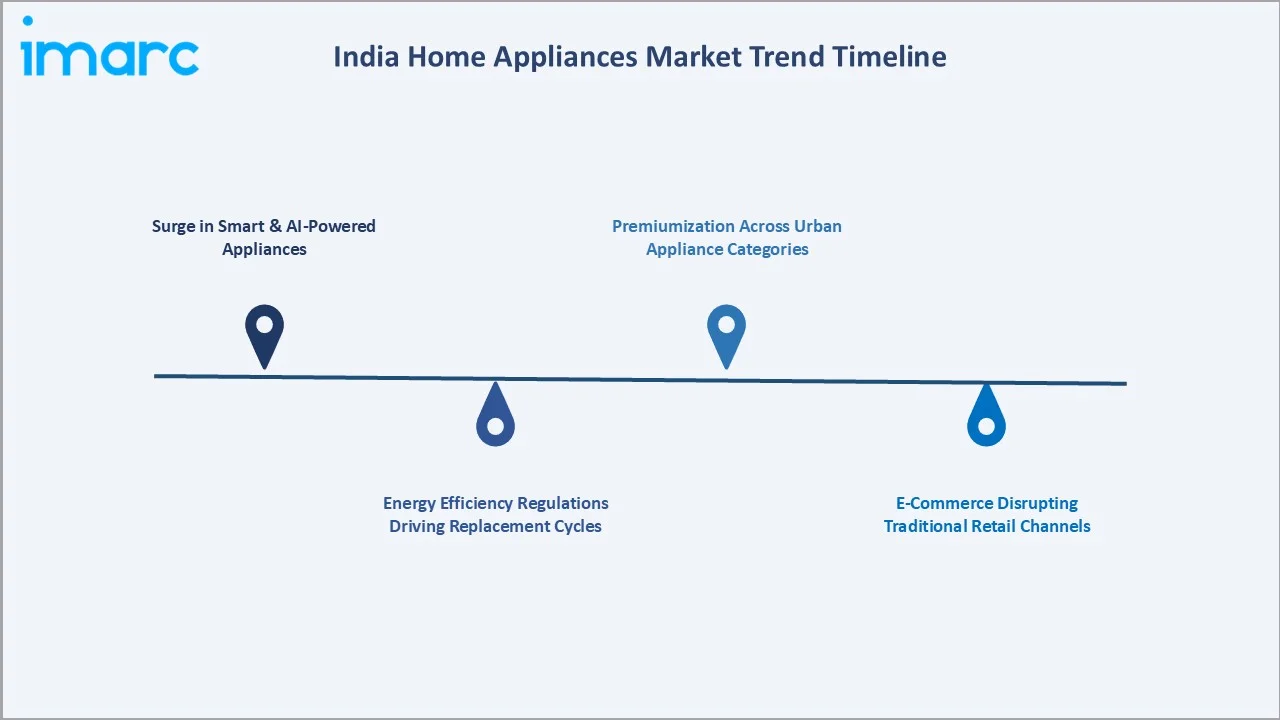

Emerging Market Trends

1. Surge in Smart & AI-Powered Appliances

Smart appliances are moving from a premium niche to a mass-market expectation. Samsung launched the Bespoke AI Washer Dryer in March 2025 – featuring intelligent fabric care and Wi-Fi monitoring – while LG's ThinQ AI ecosystem now spans over 12 appliance categories. IoT-enabled appliances growing at ~13.5% CAGR will redefine the India home appliances market size composition by 2030.

2. Energy Efficiency Regulations Driving Replacement Cycles

The Bureau of Energy Efficiency's progressive tightening of minimum energy performance standards is forcing faster product replacement cycles. ACs must achieve a minimum 5-star rating by 2025 under revised BEE norms, incentivising consumers to trade-in older, less efficient units. This regulatory push has added an estimated USD 800M–1B to annual replacement demand.

3. E-Commerce Disrupting Traditional Retail Channels

E-commerce's 32.5% channel share in 2025 is growing at ~9.8% CAGR, supported by same-day delivery in 400+ cities and aggressive No-Cost EMI financing. D2C e-commerce portals of Samsung, LG, and Godrej grew 40%+ year-on-year in 2024, reducing dependence on multi-brand retail and enabling direct consumer relationship management.

4. Premiumization Across Urban Appliance Categories

Urban Indian consumers – particularly millennials aged 25–40 – are trading-up across all appliance categories. The multi-door refrigerator segment grew 22% in 2024; convertible-technology washing machines grew 18%. Brands are launching India-specific premium product lines: Samsung's Bespoke series and LG's PuriCare ACs cater directly to this premiumizing consumer.

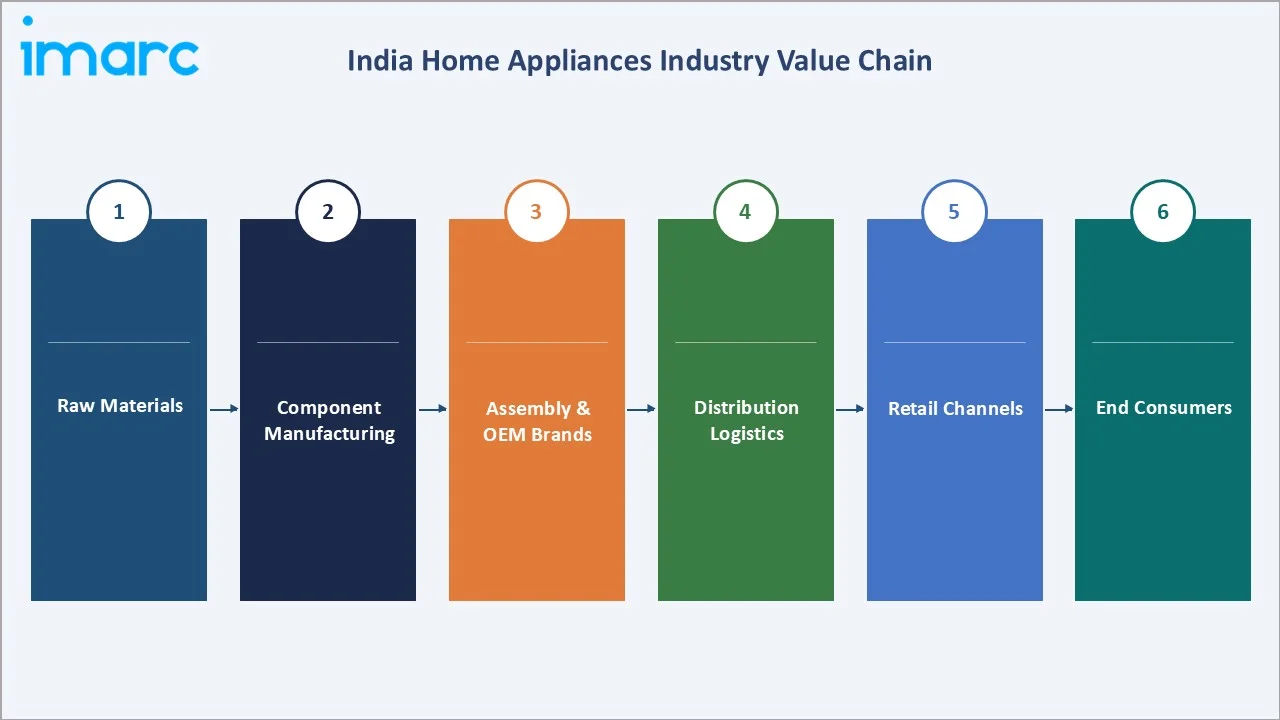

Industry Value Chain Analysis

The India home appliances value chain spans six integrated stages from raw material sourcing through end-consumer delivery. Each stage features distinct competitive dynamics, margin profiles, and policy influences particularly relevant to the Indian market context.

|

Stage |

Key Players / Examples |

|

Raw Materials |

Hindalco (aluminium), Tata Steel (steel), BASF India (polymers) |

|

Component Manufacturing |

Tecumseh India (compressors), Nidec (motors) |

|

Assembly & OEM Brands |

Samsung, LG, Godrej, Whirlpool, Haier, Voltas, IFB, Havells/Lloyd, Panasonic |

|

Distribution Logistics |

Blue Dart, DTDC, Delhivery, OEM-owned regional distributor networks |

|

Retail Channels |

Amazon India, Flipkart, Croma, Reliance Digital, Vijay Sales, Local Electronics Stores |

|

End Consumers |

Urban & semi-urban households, rural first-time buyers, hospitality & commercial users |

OEM brands occupy the highest strategic value position, integrating sourced components with proprietary technology and distribution networks. However, e-commerce platforms are increasingly enabling direct-brand access, reducing reliance on traditional multi-brand retail intermediaries.

Technology Landscape in the India Home Appliances Industry

Inverter Technology & Energy Management

Inverter-technology compressors and motors have become the industry standard for refrigerators, ACs, and washing machines in India. Inverter ACs now account for over 65% of AC unit sales in 2025, delivering 30–50% energy savings versus fixed-speed equivalents. LG's DUAL Inverter compressor and Daikin's inverter scroll technology represent leading R&D benchmarks. BEE's star rating system directly incentivises inverter adoption.

IoT Connectivity & Smart Home Integration

Wi-Fi and Bluetooth-enabled appliances are integrating with India's 500M+ broadband subscriber base. Samsung SmartThings and LG ThinQ platforms enable voice control, remote monitoring, and predictive maintenance alerts via mobile apps. Amazon Alexa and Google Assistant voice control compatibility is now standard in mid-premium appliance launches. Smart water purifier segment leaders – Kent and A.O. Smith – introduced IoT filter replacement alert systems in 2024.

Artificial Intelligence & Machine Learning in Appliances

AI-driven appliance features are gaining commercial traction. Samsung's Bespoke AI refrigerator (launched February 2025) uses AI energy mode to learn household usage patterns and reduce power consumption by up to 15%. IFB's AI Wash function detects fabric type and load weight to auto-configure washing parameters. These AI-enhanced features justify 15–25% price premiums and reduce post-purchase service calls by ~30%.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product |

Major Appliance |

58.4% |

2025 |

|

Distribution Channel |

E-commerce |

32.5% |

2025 |

|

Region |

West India |

28.3% |

2025 |

By Product

To access detailed market analysis, Request Sample

Major Appliances commands a 58.4% majority share in 2025, driven by India's rapidly expanding urban middle class upgrading from shared or rented appliances to owned units. The sub-segment is led by air conditioners – benefiting from intensifying summer heat waves and expanding electricity access – refrigerators and washing machines. Government energy labelling compliance further accelerated the upgrade cycle of older inefficient units.

Small Appliances at 41.6% in 2025 – covering kitchen appliances, water purifiers, vacuum cleaners, and personal care devices – are growing faster at an estimated CAGR of ~7.2% through 2034. Kitchen appliances sub-segment was valued at USD 6.5 Billion in 2025 (IMARC), growing at 7.32% CAGR to USD 12.5 Billion by 2034. Water purifiers are expanding fastest in tier-2/tier-3 cities due to rising water quality awareness.

By Distribution Channel

E-commerce leads at 32.5% in 2025 as the fastest-growing channel at ~9.8% CAGR through 2034. Amazon India and Flipkart's festive season events alone account for a significant portion of annual appliance revenue. Specialty stores hold 28.7%, anchored by Croma (Tata), Reliance Digital, and Vijay Sales – which offer experiential showrooming and after-sales service bundles that online-only players cannot match.

Supermarkets and Hypermarkets at 24.6% – led by BigBasket Quick Commerce and D-Mart – serve mid-range and impulse-purchase small appliances. Others (14.2%) include direct brand outlets, MBO kirana-adjacent electronics stores, and B2B institutional channels serving hospitality and housing developers.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

West India |

28.3% |

Mumbai, Pune, Ahmedabad retail density; high per-capita income; festive buying |

|

North India |

27.4% |

Delhi-NCR premium demand; Punjab rural income growth; UP scale expansion |

|

South India |

24.8% |

IT-sector affluence; Bengaluru/Hyderabad tech adopters; strong energy norms compliance |

|

East India |

19.5% |

First-time buyers growth in WB & Odisha; rising rural income; e-commerce expansion |

West India commands the largest regional share at 28.3% in 2025. Maharashtra alone contributes an estimated 18–20% of the region's appliance revenue, driven by Mumbai's affluent consumer base and Pune's expanding tech workforce. Gujarat's strong festive buying culture – particularly during Navratri and Diwali – creates significant seasonal demand peaks. Brands including Godrej, Voltas, and Whirlpool maintain strongest regional distribution penetration in West India.

North India at 27.4% is anchored by Delhi-NCR's premium appliance demand and Punjab's rising rural agricultural income. NCR contributes the highest average ticket size per appliance purchase nationally, with strong demand for inverter ACs and multi-door refrigerators. South India at 24.8% is the fastest-growing region at an estimated ~7.2% CAGR, driven by Bengaluru and Hyderabad's IT-sector consumer base, which demonstrates strong early adoption of smart appliances and energy-efficient products.

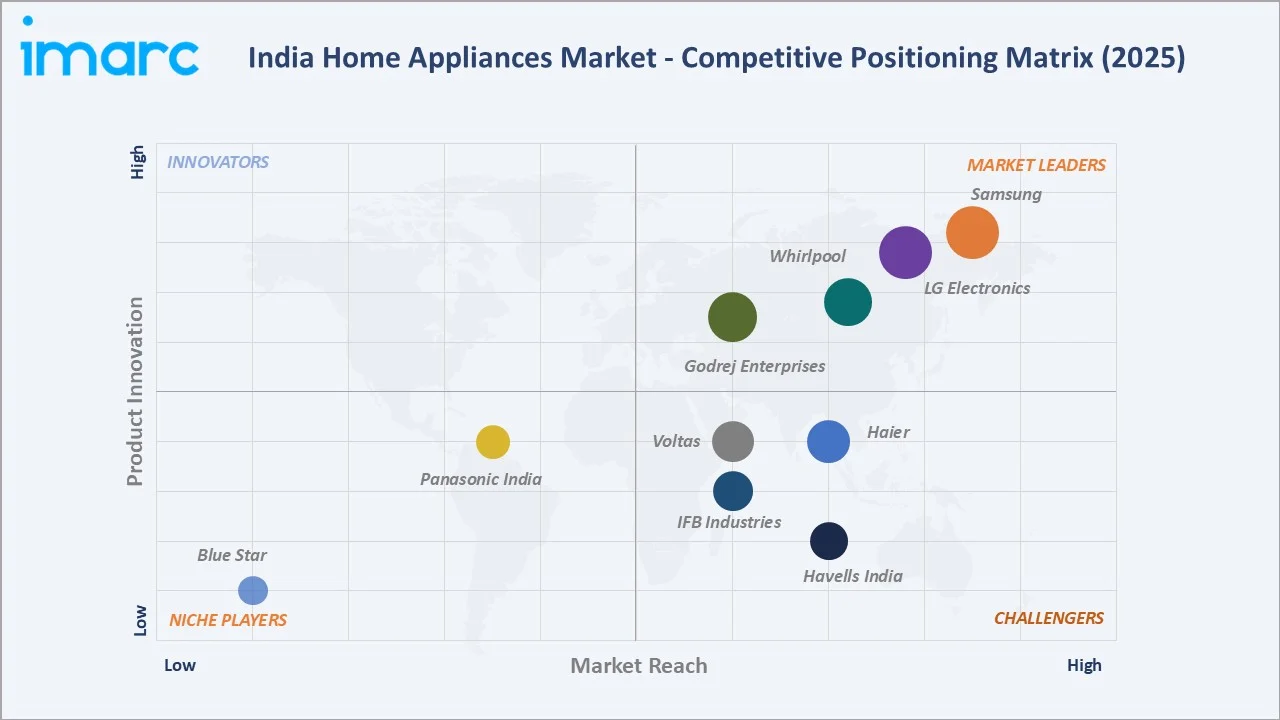

Competitive Landscape

|

Company Name |

Key Brand / Platform |

Market Position |

Core Strength |

|

Samsung |

Samsung Bespoke |

Leader |

Smart appliance ecosystem, premium refrigerators, washers |

|

LG Electronics India Limited |

DUAL Inverter |

Leader |

Inverter tech, AI-enabled appliances, service network |

|

Whirlpool |

Whirlpool / Intella-Wash |

Leader |

Mid-market washers, rural penetration, contract mfg. |

|

Godrej Enterprises |

Godrej EON / Align |

Leader |

Deep freezers, energy-efficient fridges, India-first design |

|

Haier Group |

Smart Home |

Challenger |

Affordable pricing, aggressive capacity expansion |

|

Voltas Limited |

Voltas / Beko |

Challenger |

AC market leadership, Tata brand trust, tier-2 reach |

|

IFB Industries Limited |

IFB / Neptune |

Challenger |

Premium front-load washers, dishwashers, IoT features |

|

Havells India Ltd |

Lloyd / Havells |

Challenger |

AC & large appliance integration, fast retail expansion |

|

Panasonic Life Solutions India Pvt. Ltd |

Panasonic NanoeX |

Emerging |

Air purifiers, split ACs, 90% local mfg. target by 2026 |

|

Blue Star Limited |

Blue Star |

Emerging |

Commercial & residential ACs, growing home segment |

The India home appliances competitive landscape is characterised by a clear tier structure: global brands (Samsung, LG, Whirlpool) dominating premium urban segments; domestic champions (Godrej, Voltas, IFB) leveraging localisation and government PLI support; and Chinese entrants (Haier, Midea) competing aggressively on price in the mass market.

Key Company Profiles

Samsung

Samsung India is the market leader in premium home appliances, leveraging its SmartThings IoT ecosystem to cross-sell AI-integrated refrigerators, washing machines, and ACs. Samsung's Bespoke product line – launched in India in 2024–2025 – targets urban millennial consumers with customisable panel designs and AI energy management.

- Product Portfolio: Bespoke AI refrigerators, DUAL Inverter ACs, Bespoke AI Washer Dryer, microwave ovens, vacuum cleaners, connected home ecosystem (SmartThings platform).

- Recent Developments: In March 2025, Samsung launched the Bespoke AI Washer Dryer (12KG/7KG) with all-weather laundry capability and intelligent fabric care.

- Strategic Focus: Samsung's India strategy prioritises premiumisation through AI feature integration, SmartThings ecosystem lock-in across appliance categories, and expanding PLI-supported local manufacturing to reduce import-linked cost disadvantages.

LG Electronics India Limited

LG Electronics is a co-leader in premium appliances with particular strength in inverter-technology air conditioners, multi-door refrigerators, and front-load washing machines. Its ThinQ AI platform connects appliances via a unified mobile app with voice-assistant integration.

- Product Portfolio: DUAL Inverter split ACs, ThinQ-enabled refrigerators and washing machines, OLED TVs, water purifiers, air purifiers, microwave ovens.

- Recent Developments: LG Electronics will debut compressor solutions engineered for India at ACREX 2026, highlighting locally manufactured rotary and reciprocating compressors for residential air conditioners and refrigerators.

- Strategic Focus: LG focuses on inverter technology leadership, ThinQ ecosystem integration, and deepening service infrastructure in tier-2/tier-3 cities to capture post-sale service revenue alongside hardware sales.

Godrej Enterprises

Godrej Enterprises is the dominant domestic appliance brand with a 90-year heritage in Indian households. It leads in deep freezers and energy-efficient refrigerator categories, leveraging strong brand equity particularly in South and West India.

- Product Portfolio: Eon NXT refrigerators, Align washing machines, Pentacool ACs, deep freezers, air coolers, water coolers, and microwave ovens.

- Recent Developments: Godrej is about to unveil portfolio spans split ACs, cassette ACs, tower ACs, and window ACs across capacities from 1 Ton to 4 Ton, with a strategic focus on higher‑tonnage models in 2026. The lineup is available in 5‑star and 3‑star energy ratings and puts a strong spotlight on Smart ACs.

- Strategic Focus: Godrej's strategy centres on India-first product design (hard-water-compatible washers, voltage-fluctuation-resistant refrigerators), eco-friendly refrigerant transition, and PLI scheme utilisation to strengthen manufacturing competitiveness.

Market Concentration Analysis

The India home appliances market exhibits moderate concentration, with the top five players (Samsung, LG, Whirlpool, Godrej, and Haier) collectively accounting for approximately 55–62% of national market revenue in 2025. However, concentration varies significantly by product sub-category: the premium refrigerator segment is highly concentrated at ~70% top 3 share, while the AC segment is more fragmented with Voltas, Daikin, Blue Star, and 8+ brands each holding meaningful positions.

Fragmentation is highest in small appliances, with numerous domestic, imported, and private-label brands competing across categories like mixer-grinders and personal care devices, keeping market concentration low.

Consolidation is accelerating in AC and washing machine segments as PLI-linked scale advantages favor large OEMs and pressure smaller assemblers. By 2027–2028, the top three AC brands are projected to exceed 50% market share (from ~42% in 2025), driven by rising energy-efficiency compliance costs.

Investment & Growth Opportunities

Fastest-Growing Segments

Smart and IoT-connected appliances represent the highest-CAGR sub-segment at ~13.5% through 2034. India's smart home devices market projected to grow from USD 8.33 Billion in 2025 to USD 54.97 Billion by 2034 at 23.33% CAGR (IMARC) provides the demand context for appliance-connected ecosystem investment. E-commerce channel infrastructure – same-day delivery capability, regional fulfilment centres, and no-cost EMI financing – represents a priority investment area for brands and logistics investors.

Emerging Market Expansion

East India at 19.5% share in 2025 – and the tier-2/tier-3 city belt nationally – represents the most underpenetrated opportunity. Refrigerator penetration below 30%, AC penetration below 10%, and washing machine penetration below 15% in rural and semi-urban India collectively imply a USD 15–20 Billion addressable opportunity that current market leaders are actively contesting. South India's IT-corridor cities (Bengaluru, Hyderabad, Chennai) are the premium smart appliance expansion frontier.

Venture & Strategic Investment Trends

PLI scheme participation has attracted significant committed investment from global brands: Haier India announced INR 1,000 crore capacity expansion targeting USD 2 Billion revenue by FY2029. Dixon Technologies – a key contract manufacturer – received INR 200+ crore in capacity expansion financing in 2024. LG is investing INR 100 crore in local manufacturing of dual Inverter air conditioner compressors, signalling long-term manufacturing commitment to India's favourable cost and policy environment.

Future Market Outlook (2026-2034)

The India home appliances market forecast projects strong value expansion from USD 69.02 Billion in 2025 to USD 124.66 Billion by 2034 at a CAGR of 6.55% – an 80%+ cumulative growth – underpinned by premiumisation, smart technology adoption, energy-efficiency regulation, and structural penetration increases in tier-2/tier-3 markets.

Two major disruptions will reshape India’s home appliances industry through 2034: the evolution of smart-connected platforms (e.g., Samsung SmartThings, LG ThinQ) into integrated smart-home ecosystems, and the rise of AI-driven predictive maintenance shifting competition toward software-led service quality. The market will transition from a hardware-centric model to a software-augmented ecosystem with subscription-based services, energy analytics, and in-app commerce generating recurring revenues. The competitive landscape is expected to consolidate at the premium end (Samsung, LG, Godrej), while players like Haier and Midea focus on mass-market growth through pricing and energy efficiency.

Research Methodology

Primary Research

Primary research involved structured interviews (2024–2025) with appliance OEM executives, retail partners (including e-commerce and large-format stores), service technicians, and consumer durables investors. Insights were used to validate market size, segment shares, technology adoption trends, and regional demand patterns.

Secondary Research

Secondary research drew from industry databases, government reports (BEE, Ministry of Commerce), and institutional publications such as IBEF and CII-BCG studies. Company annual reports and trade journals further supported data validation and market benchmarking.

Forecasting Models

Market forecasts were developed using a blend of top-down macroeconomic analysis and bottom-up penetration modelling across product categories. Scenario-based forecasting incorporated GDP growth expectations, with the base case assuming a 6.55% CAGR aligned with India’s projected 6.5%–7.0% economic growth trajectory.

India Home Appliances Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Products Covered |

|

| Distribution Channels Covered | Supermarkets and Hypermarkets, Specialty Stores, E-Commerce, Others |

| Regions Covered | North India, South India, East India, West India |

| Companies Covered | Samsung , LG Electronics India Limited, Whirlpool , Godrej Enterprises, Haier Group, Voltas Limited, IFB Industries Limited, Havells India Ltd, Panasonic Life Solutions India Pvt. Ltd, Blue Star Limited, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Home Appliances Market Report

The India home appliances market was valued at USD 69.02 Billion in 2025, driven by rising incomes, urbanisation, and expanding e-commerce distribution networks across major cities.

The market is projected to reach USD 124.66 Billion by 2034, growing at a CAGR of 6.55% during 2026-2034, driven by smart appliance adoption and tier-2/tier-3 city penetration.

Major Appliances (refrigerators, ACs, washing machines) leads with a 58.4% share in 2025, driven by urban household upgrades and government energy-efficiency policy support.

E-commerce is the fastest-growing channel at ~9.8% CAGR through 2034, commanding 32.5% share in 2025, led by Amazon India and Flipkart during festive sale events.

West India holds the largest regional share at 28.3% in 2025, anchored by Maharashtra and Gujarat's high urban density, strong retail infrastructure, and elevated per-capita incomes.

South India is the fastest-growing region at an estimated ~7.2% CAGR, powered by Bengaluru and Hyderabad's tech-sector affluence and high early adoption of smart appliances.

The leading companies are Samsung, LG Electronics India Limited, Whirlpool , Godrej Enterprises, Haier Group, Voltas Limited, IFB Industries Limited, Havells India Ltd, Panasonic Life Solutions India Pvt. Ltd, and Blue Star Limited.

Key drivers include rising middle-class incomes, rapid urbanisation, BEE energy-efficiency regulations accelerating upgrades, Make in India PLI incentives, and surging e-commerce penetration.

Key trends are AI-powered smart appliance adoption (~13.5% CAGR), energy-efficiency standard upgrades, e-commerce channel dominance, premiumisation in urban markets, and tier-2/tier-3 city expansion.

Small appliances (mixers, water purifiers, vacuum cleaners, irons) held 41.6% of the India home appliances market in 2025, growing at an estimated 7.2% CAGR through 2034.

India's smart home devices market is projected to grow from USD 8.33 Billion in 2025 to USD 54.97 Billion by 2034 at a 23.33% CAGR, making it the highest-growth sub-market within home appliances.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)