India Home Textile Market Size, Share, Trends, and Forecast by Product, Distribution Channel, and Region, 2026-2034

India Home Textile Market Size, Share, Trends & Forecast (2026-2034)

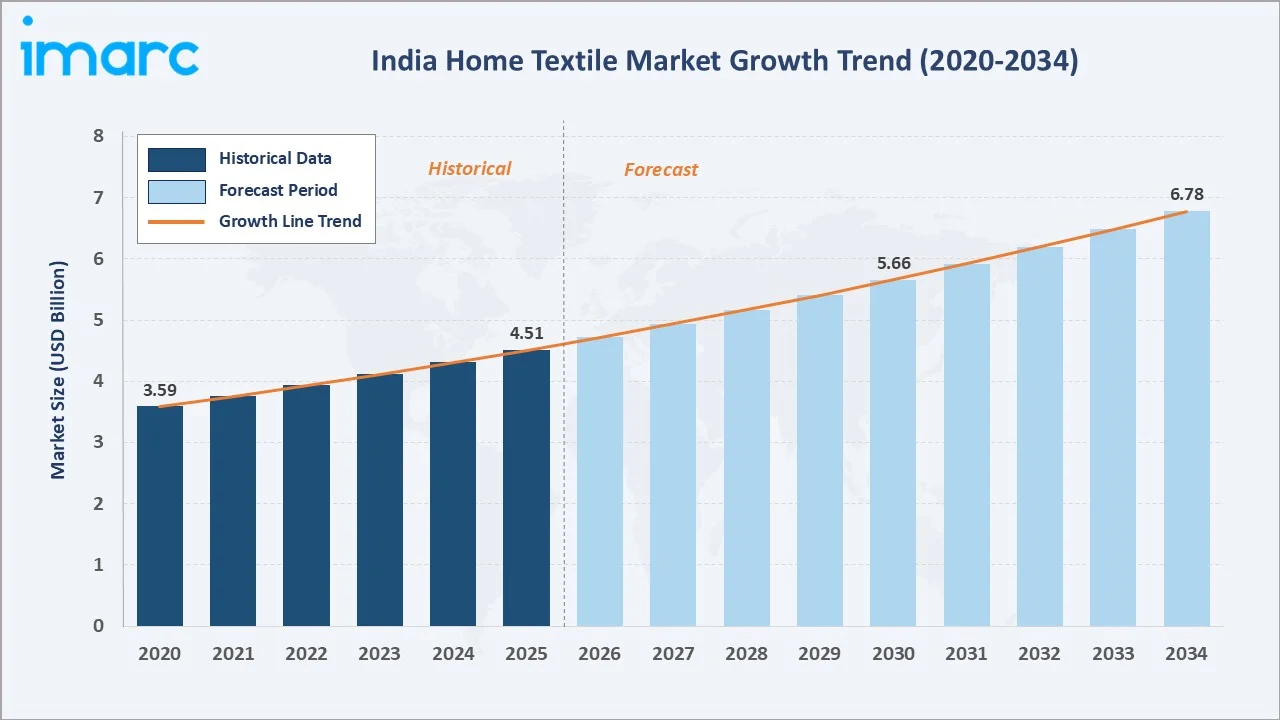

The India home textile market size reached USD 4.51 Billion in 2025 and is projected to reach USD 6.78 Billion by 2034, exhibiting a CAGR of 4.65% during 2026-2034. Rising urbanization, growing middle-class incomes, and shifting consumer preferences toward premium home décor products are primary drivers.

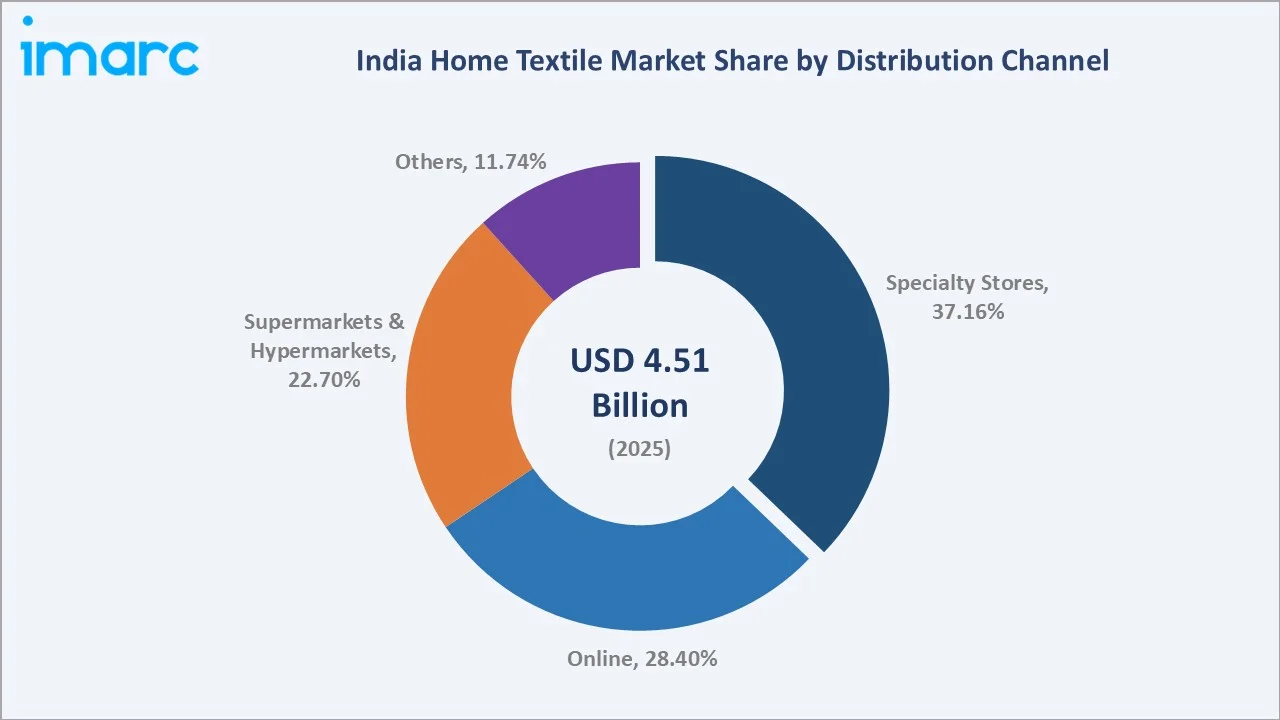

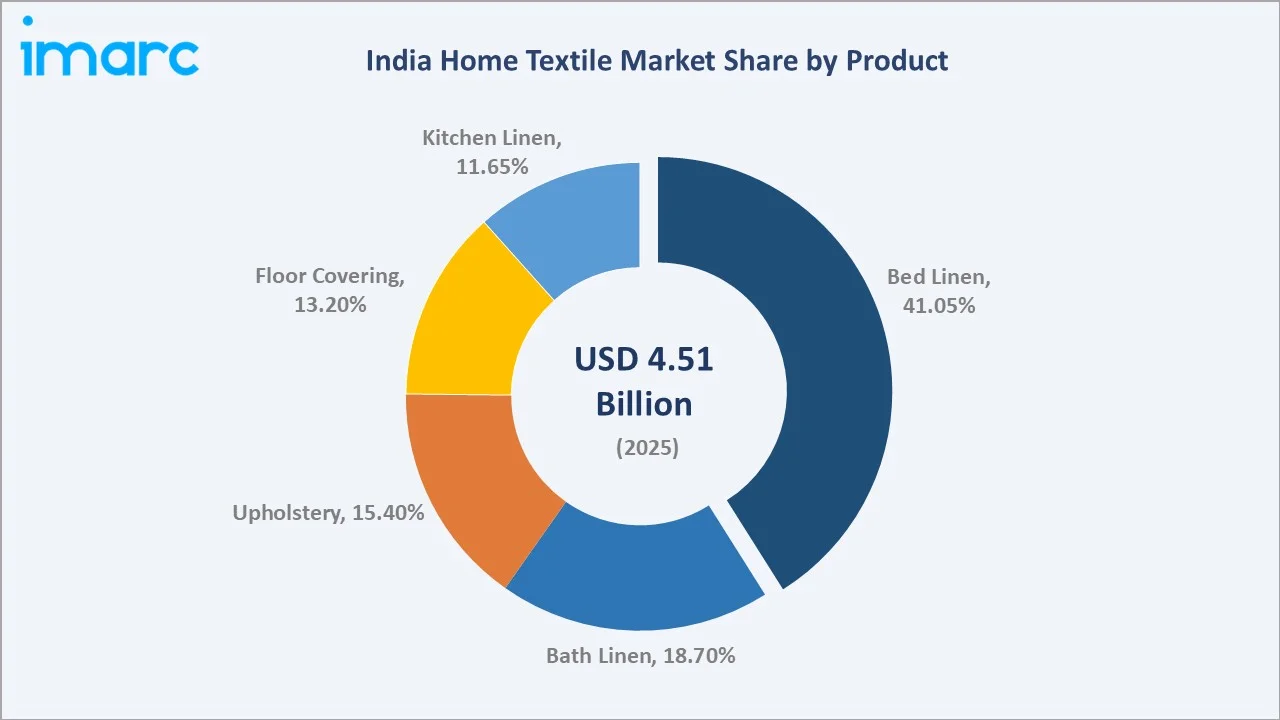

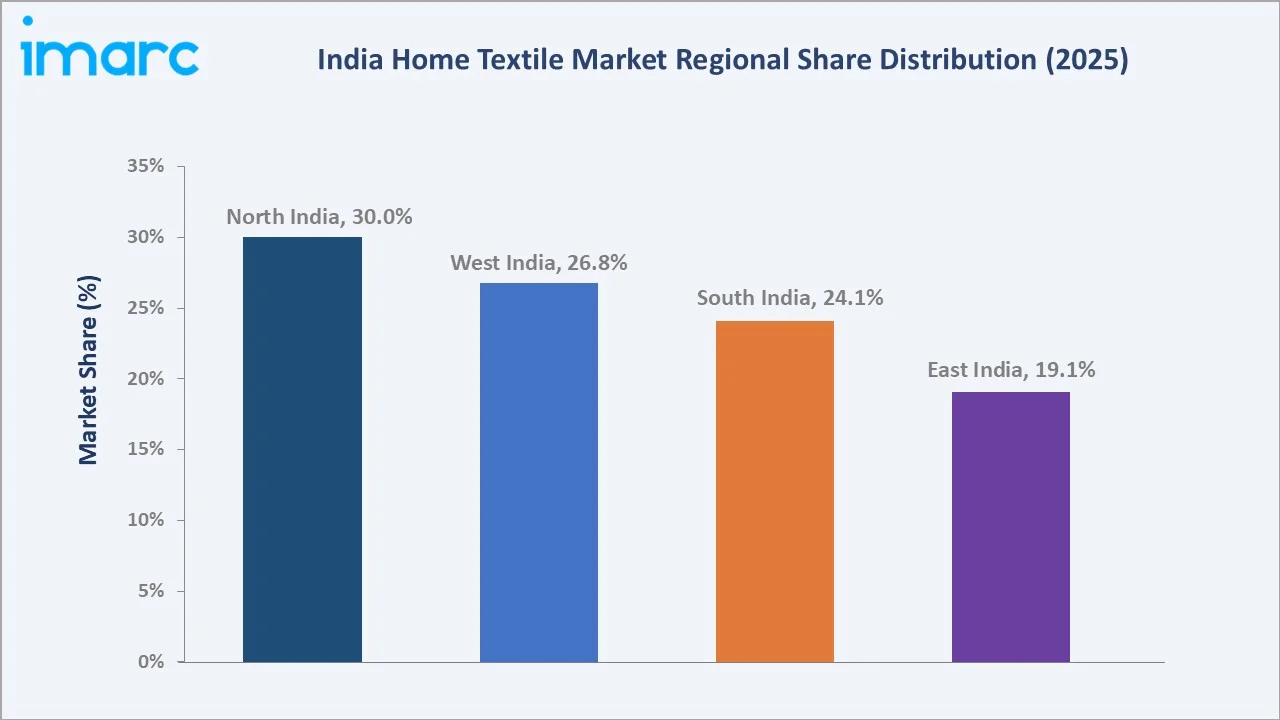

Specialty stores dominate distribution at 37.16%, while bed linen leads the product mix at 41.05%. North India commands a dominant 30.0% regional share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 4.51 Billion |

|

Forecast Market Size (2034) |

USD 6.78 Billion |

|

CAGR (2026-2034) |

4.65% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

North India (30.0% share, 2025) |

|

Second Largest Region |

West India (26.8% share, 2025) |

|

Leading Distribution Channel |

Specialty Stores (37.16%, 2025) |

|

Leading Product |

Bed Linen (41.05%, 2025) |

The India home textile market growth trajectory from 2020 through 2034, with the historical expansion to USD 4.51 Billion in 2025, reflects consistent income-driven and urbanization-led demand. The forecast to USD 6.78 Billion captures e-commerce acceleration, real estate growth, and premiumization trends through 2034.

To get more information on this market, Request Sample

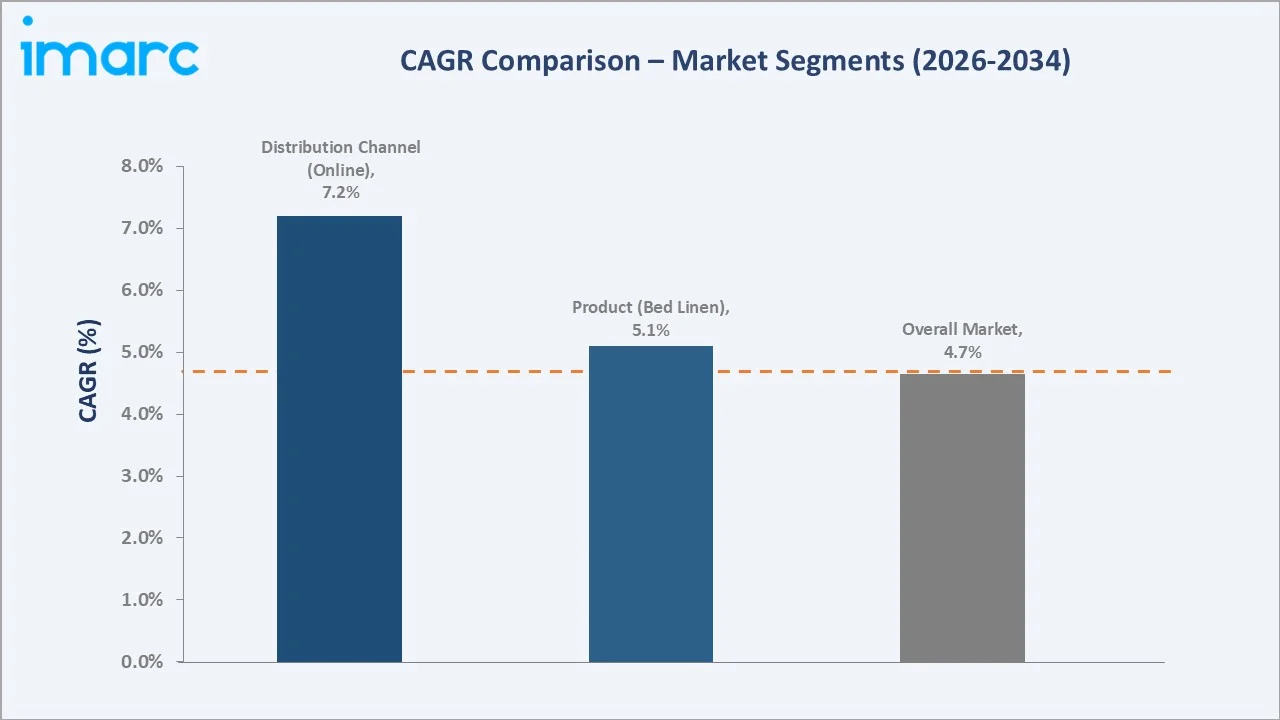

The CAGR trajectories across key distribution channel and product sub-segments, with online channels at ~7.20% CAGR and bed linen at ~5.1% CAGR, represent the fastest-growing categories within the India home textile industry through 2034.

Executive Summary

The India home textile market is on a sustained growth trajectory from USD 4.51 Billion in 2025 to USD 6.78 Billion by 2034. Home textiles encompass bed linen, bath linen, kitchen linen, upholstery, and floor coverings serving residential, hospitality, and institutional end users.

Specialty stores dominate distribution at 37.16% in 2025, offering curated assortments and personalized service. Online channels at 28.4% are the fastest-growing distribution segment, driven by e-commerce proliferation and digital-native consumers in Tier-1 and Tier-2 cities.

Bed linen leads the product mix at 41.05% in 2025, driven by universal residential and commercial demand, continuous product innovation, and growing premiumization of bedding.

North India commands 30.0% regional share, anchored by Delhi-NCR metropolitan concentration and high purchasing power.

Key Market Insights

|

Insight |

Data |

|

Leading Distribution Channel |

Specialty Stores – 37.16% share (2025) |

|

Fastest-Growing Channel |

Online – 28.4% share, ~7.20% CAGR (2026-2034) |

|

Leading Product |

Bed Linen – 41.05% share (2025) |

|

Leading Region |

North India – 30.0% share (2025) |

|

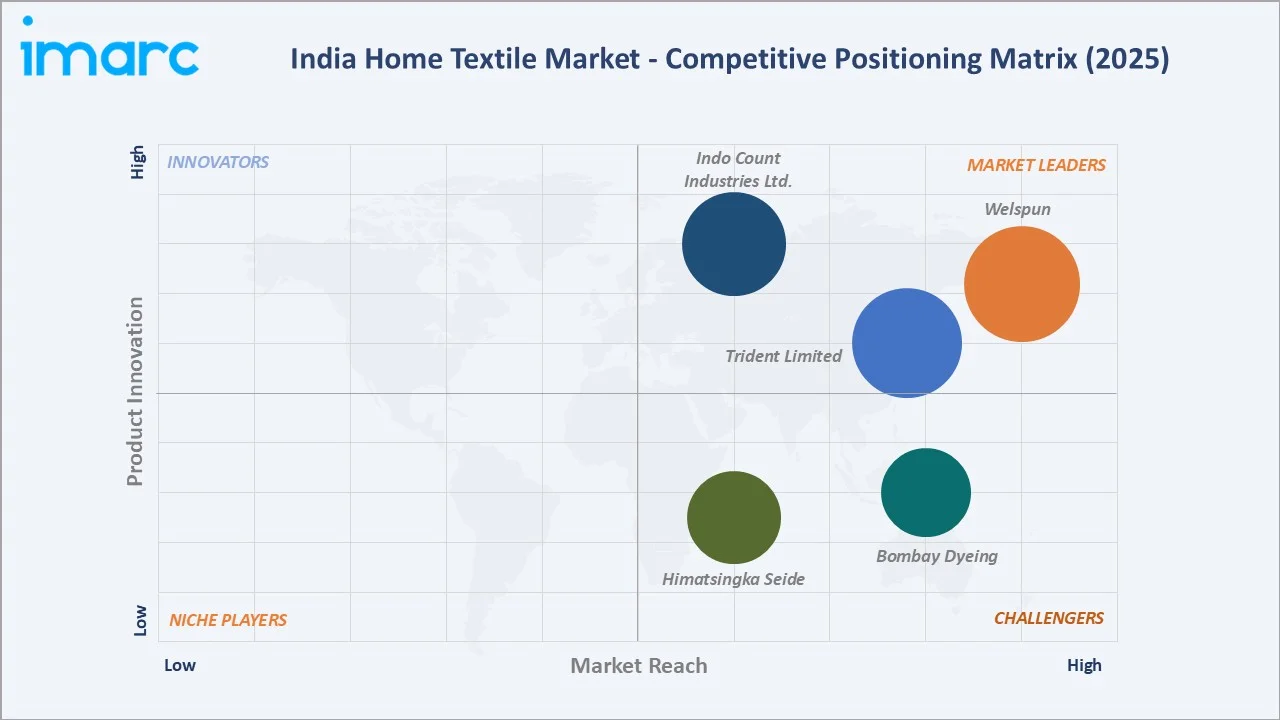

Top Companies |

Welspun, Trident Limited, Indo Count Industries Ltd., Himatsingka Seide, Bombay Dyeing |

Key Analytical Observations Expanding on the Above Data:

- Specialty stores, with 37.16% in 2025, dominate because they offer tactile shopping experiences, expert fabric consultation, and curated assortments. For premium buyers evaluating thread counts and material quality, in-store guidance and physical product evaluation remain critical purchase enablers.

- Online channels, at 28.4% in 2025, are the fastest-growing segment at ~7.20% CAGR, driven by e-commerce expansion, smartphone penetration beyond Tier-1 cities, influencer-led home décor content, and competitive pricing with easy return policies that de-risk online textile purchases.

- Bed linen at 41.05% dominates because of universal residential and commercial replacement demand. Hotels, hospitals, and households continuously replenish bed linen, and premiumization toward higher thread counts and organic cotton has expanded average selling prices and revenue contribution.

- North India's 30.0% share reflects Delhi-NCR's concentration of high-income households, strong organized retail infrastructure, and proximity to key manufacturing clusters that supply cost-competitive products across the region.

India Home Textile Market Overview

Home textiles are fabric-based products designed for domestic and institutional use, encompassing bed linen, bath linen, kitchen linen, upholstery fabrics, and floor coverings. Products are manufactured from cotton, polyester, blended, and specialty fibers using weaving, knitting, and tufting technologies with finishing treatments for softness, anti-microbial properties, and durability.

The India home textile ecosystem integrates cotton farmers, spinning mills, weaving units, dyeing and finishing processors, branded manufacturers, organized retailers, and e-commerce platforms. India's position as the world's second-largest cotton producer provides a competitive raw material cost advantage for domestic manufacturers serving both domestic and export markets.

Market Dynamics

To evaluate market opportunities, Request Sample

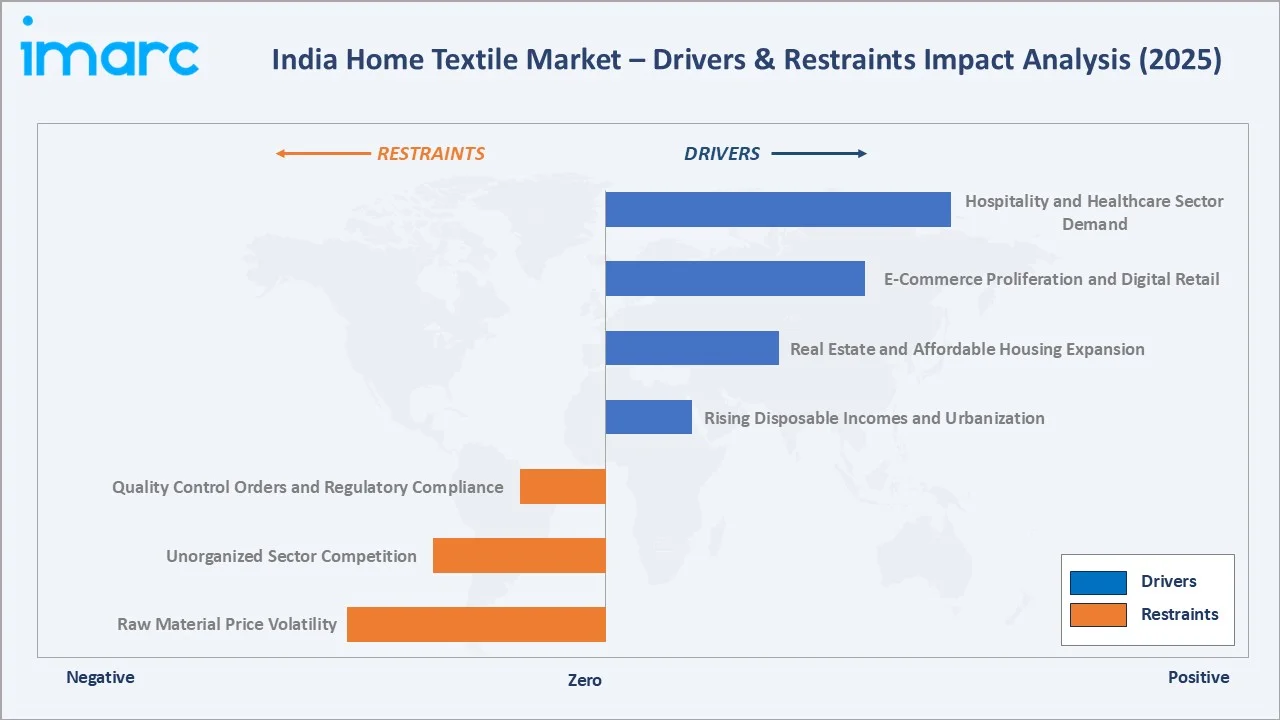

Market Drivers

- Rising Disposable Incomes and Urbanization: India's per capita net national income rose to INR 188,892 in FY24, with urban household spending on home furnishings growing from 3.1% to 4.2% of monthly expenditure between 2020 and 2025. The Ministry of Housing projects urbanization to reach 40% by 2030, adding 60 million new households.

- Real Estate and Affordable Housing Expansion: Government programmes including PM Awas Yojana targeting 20 million urban housing units generate large-scale demand for home textiles. Each new household represents a procurement event for bed linen, bath products, upholstery, and floor coverings across all price tiers.

- E-Commerce Proliferation and Digital Retail: India's e-commerce penetration in home textiles is accelerating as platforms invest in product visualization, customer reviews, and easy returns. Influencer-driven social commerce and quick-commerce pilots are expanding premium home textile access to semi-urban consumers.

- Hospitality and Healthcare Sector Demand: India's hotel industry targets 200,000+ new room additions through 2028, while healthcare facility expansion generates institutional procurement. Each hotel room requires multiple sets of bed linen and bath towels, creating recurring high-volume demand from the hospitality sector.

Market Restraints

- Raw Material Price Volatility: Cotton prices exhibit significant volatility, with futures fluctuating sharply between 2022 and 2024. This compresses manufacturer margins and creates pricing uncertainty for organized players competing with unorganized bazaar suppliers who carry lower inventory holding costs.

- Unorganized Sector Competition: India's home textile market remains significantly unorganized, with local weavers and power loom clusters in major textile towns offering unbranded products at 30-50% discount to organized retail prices, constraining pricing power for branded manufacturers.

- Quality Control Orders and Regulatory Compliance: BIS mandatory quality control orders for home textiles require annual audits and testing, imposing compliance costs per product category for manufacturers. Smaller units struggle with the compliance burden, creating consolidation pressure across the fragmented market.

Market Opportunities

- Sustainable and Organic Textiles: Consumer demand for GOTS-certified organic cotton, bamboo fiber, and recycled polyester home textiles is growing rapidly in premium segments. India's established organic cotton farming base and export certification infrastructure position domestic manufacturers to capture high-margin sustainable product growth.

- Export Market Expansion via PLI Scheme: Export market expansion is being supported by government-led incentive programs aimed at boosting outbound shipments from the home textiles sector. These initiatives are encouraging manufacturers to scale up production capacity, enhance operational efficiency, and align with global quality and compliance standards. As a result, leading players are increasingly focusing on international markets to drive growth and diversify revenue streams. This trend is strengthening the sector’s competitiveness in global trade while supporting long-term export-oriented expansion strategies.

Market Challenges

- Tariff Risk: Potential tariff actions and trade policy shifts in major importing countries pose a risk to the price competitiveness of home textile exports. Any increase in duties can impact demand, particularly in price-sensitive segments, and create uncertainty for exporters dependent on a few large markets. This may lead to margin pressure and the need for price adjustments to retain market share. In response, manufacturers are increasingly diversifying export destinations and strengthening cost efficiencies to mitigate geopolitical and trade-related risks.

- Fast Fashion and Short Replacement Cycles: Consumer preference for frequent home décor refreshes, while increasing unit volumes, also pressures average selling prices. Manufacturers must balance high-volume affordable offerings with premium product development to maintain healthy margin profiles.

Emerging Market Trends

1. Digital Printing and Customization Transforming Product Differentiation

Digital fabric printing technology enables mass-customization of home textile patterns at minimal incremental cost, transforming product differentiation strategies. Personalized bed linen and digitally printed upholstery fabrics command 40-60% price premiums over standard dobby and jacquard weave offerings in organized retail channels.

2. Sustainable Certifications and Eco-Friendly Fabric Adoption

OEKO-TEX Standard 100, GOTS certification, and BCI membership are becoming procurement prerequisites for hospitality and institutional buyers. Leading manufacturers' sustainability roadmaps and renewable energy investments reflect industry-wide shifts toward certification-led product differentiation in export and premium domestic market segments.

3. Smart Home Integration and Functional Textiles

Temperature-regulating, moisture-wicking, and anti-microbial functional textiles are expanding beyond healthcare into residential markets. Functional fabric innovations including phase-change materials and nano-silver finishes command significant premiums, addressing urban India's growing wellness-oriented home environment demand.

4. Direct-to-Consumer and Brand-Building Investments

D2C brands leveraging Instagram, quick commerce, and subscription models hold notable premium segment share. Established manufacturers are investing in owned digital channels, brand storytelling, and lifestyle positioning to reduce dependence on specialty retailer margins and build direct consumer relationships.

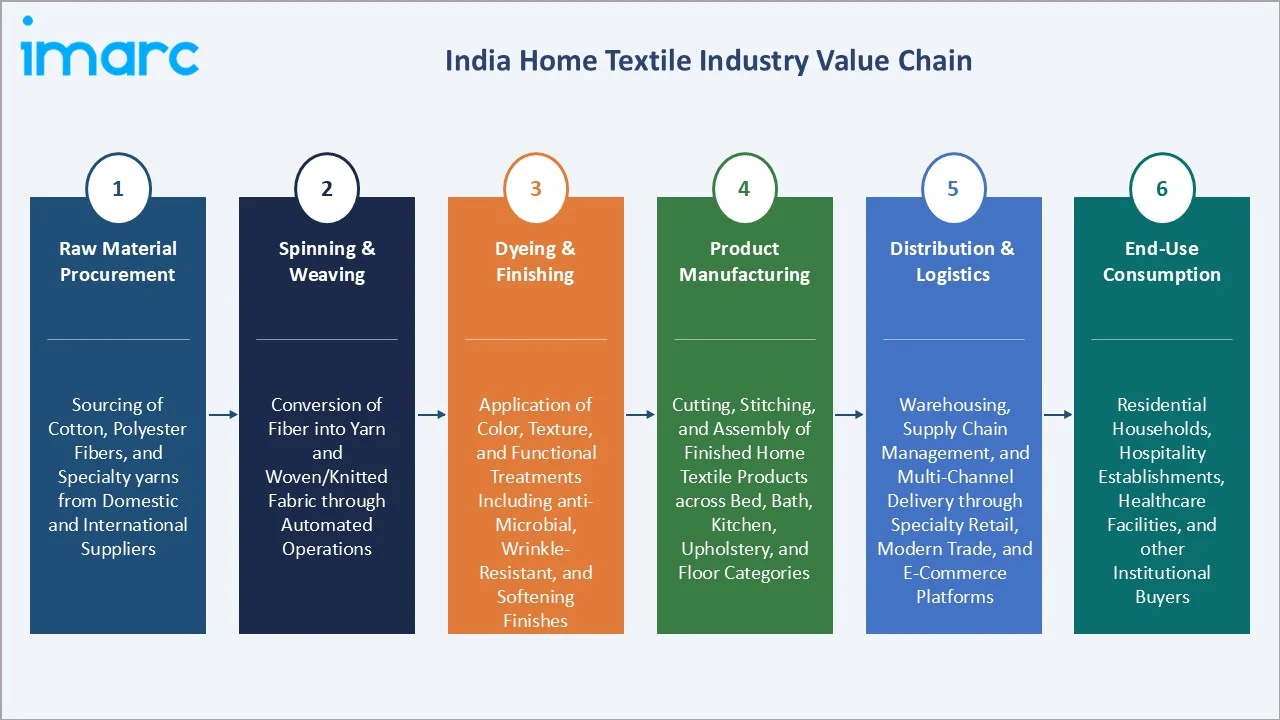

Industry Value Chain Analysis

The India home textile value chain spans six stages from raw material procurement through end-user consumption. Fabric finishing and branded product manufacturing capture the highest value-add margins, while distribution logistics create significant working capital requirements favoring larger organized manufacturers.

|

Stage |

Description |

|

Raw Material Procurement |

Sourcing of cotton, polyester fibers, and specialty yarns from domestic and international suppliers |

|

Spinning & Weaving |

Conversion of fiber into yarn and woven/knitted fabric through automated spinning and loom operations |

|

Dyeing & Finishing |

Application of color, texture, and functional treatments including anti-microbial, wrinkle-resistant, and softening finishes |

|

Product Manufacturing |

Cutting, stitching, and assembly of finished home textile products across bed, bath, kitchen, upholstery, and floor categories |

|

Distribution & Logistics |

Warehousing, supply chain management, and multi-channel delivery through specialty retail, modern trade, and e-commerce platforms |

|

End-Use Consumption |

Residential households, hospitality establishments, healthcare facilities, and other institutional buyers |

Technology Landscape in the India Home Textile Industry

Weaving Technology: Shuttleless Looms and Jacquard Automation

Adoption of air-jet and rapier shuttleless looms with computerized Jacquard systems enables complex pattern weaving at speeds four to six times higher than conventional shuttle looms. CNC-controlled finishing lines with automated folding, packaging, and quality scanning are reducing labor intensity and improving dimensional consistency for export-quality products.

Fiber Innovation: Organic Cotton, Bamboo, and Technical Blends

India's textile technology landscape is advancing toward specialty fiber blends with functional properties. Tencel-cotton blends, bamboo-viscose fabrics, and recycled PET polyester meet growing consumer demand for sustainable, breathable home textiles with technical finishes that extend product utility and command pricing premiums.

Digital Commerce and AI-Enabled Personalization

AI-powered recommendation engines on e-commerce platforms generate 25-30% higher average order values for home textile categories through coordinated room set suggestions. Virtual room visualization tools enabling consumers to preview textiles in their home environment are reducing return rates and increasing premium product conversion.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Product | Bed Linen | 41.05% | 2025 |

| Distribution Channel | Specialty Stores | 37.16% | 2025 |

| Region | North India | 30.0% | 2025 |

By Distribution Channel

Specialty stores command a 37.16% majority share in 2025, reflecting the critical role of physical retail in enabling tactile product evaluation for textiles. Consumer preference to assess fabric softness, thread count, and weave quality before purchase sustains specialty store dominance across premium and mid-market price tiers.

To access detailed market analysis, Request Sample

Online channels at 28.40% in 2025, growing at the fastest channel CAGR of ~7.20%, are reshaping distribution economics. Platform investments in HD product photography, certified review systems, and hassle-free returns are systematically reducing consumer hesitation toward online textile purchases.

By Product

Bed linen commands a 41.05% majority share in 2025, driven by universal residential and commercial replacement demand, continuous product innovation incorporating organic fabrics and premium thread counts, and growing consumer aspirations for aesthetically superior bedroom environments.

Bath linen at 18.70% in 2025 benefits from hotel sector procurement growth and rising household hygiene standards. Premium cotton terry and zero-twist towel technologies are expanding the average selling price band, with eco-certified bamboo and organic cotton bath products commanding significant premiums.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

North India |

30.0% |

High urban household income; strong organised retail; major metropolitan demand concentration |

|

West India |

26.8% |

Growing real estate activity; organised retail expansion; rising middle-class consumer base |

|

South India |

24.1% |

IT-sector income growth; expanding premium retail infrastructure; strong hospitality demand |

|

East India |

19.1% |

Emerging middle-class formation; increasing organised retail; growing e-commerce penetration |

North India's 30.0% market dominance in 2025 is driven by the concentration of high-income urban households in major metropolitan areas, strong organised retail infrastructure, and proximity to major textile manufacturing clusters that enable short supply chains and cost-competitive product availability.

West India at 26.8% benefits from a booming real estate market generating high-value home textile demand, India's cotton-producing heartland reducing raw material procurement costs for regional manufacturers, and a growing technology and finance sector-driven middle-class consumer base investing in home décor upgrades.

Competitive Landscape

The India home textile market is moderately fragmented, with organised players holding significant value share while the unorganised sector maintains volume dominance in commodity tiers. Key players compete on brand equity, product quality certifications, distribution breadth, and sustainability credentials across domestic and export markets.

|

Company Name |

Key Products |

Market Position |

Global Strategic Focus |

|

Welspun |

Bed linen, bath linen, rugs, flooring |

Leader |

Export leadership; DTC expansion; sustainability certifications |

|

Trident Limited |

Towels, bed sheets, yarn |

Leader |

Integrated manufacturing; eco-practices; institutional supply |

|

Indo Count Industries Ltd. |

Bed linen, utility bedding, fashion bedding |

Leader |

Patent innovations; branded retail entry |

|

Himatsingka Seide |

Luxury bed linen, designer home textiles |

Challenger |

Premium brand portfolio; US and Europe export focus |

|

Bombay Dyeing |

Bed linen, bath linen, furnishings |

Challenger |

Heritage brand; domestic retail network; lifestyle positioning |

Key players include Welspun, Trident Limited, Indo Count Industries Ltd., Himatsingka Seide, Bombay Dyeing, and others.

Key Company Profiles

Welspun

Welspun is India's largest home textile exporter, with distribution across 50+ countries, partnering with leading global retailers. The company is recognised for its sustainability leadership and advanced textile manufacturing capabilities.

- Product Portfolio: Bed linen, bath linen, rugs, flooring solutions, and advanced textiles including smart and anti-microbial fabric innovations.

- Recent Developments: In December 2025, Welspun has inaugurated a new terry towel manufacturing facility in Anjar, Gujarat, further strengthening its position in the home textiles market. The state-of-the-art plant, equipped with advanced technologies and a wide product range, significantly enhances the company’s production capabilities and operational scale.

- Strategic Focus: Welspun's strategy balances export leadership with domestic brand-building, investing in DTC channels, sustainability certifications, and advanced textile innovation to defend premium positioning against price competition.

Trident Limited

Trident Limited is one of India's largest integrated home textile manufacturers, with manufacturing facilities in Punjab and Madhya Pradesh. The company exports to various countries and maintains large production capacity across towels and bed linen, with pioneering eco-friendly manufacturing practices.

- Product Portfolio: Towels, bed sheets, yarn, and specialty paper manufactured from agricultural residue for eco-friendly production.

- Strategic Focus: Trident leverages its integrated model from yarn spinning through finished product to achieve cost structures that support both premium hospitality supply and mid-market domestic retail competitiveness with ECO certifications supporting export growth.

Indo Count Industries Ltd.

Indo Count Industries is a leading bed linen manufacturer headquartered in Maharashtra, directing most of its production toward United States retail chains. The company has filed multiple patents for innovative fabric finishes and is transitioning from pure export manufacturing toward domestic branded retail.

- Product Portfolio: Fashion bedding, utility bedding, institutional bedding, and specialty bed linen incorporating proprietary finish technologies.

- Recent Developments: In September 2024, Indo Count Industries has acquired a majority stake in US-based Fluvitex, a manufacturer of pillows and quilts, as part of its strategy to expand its presence in the bedding market. The acquisition provides access to an established manufacturing facility and strengthens the company’s position in the utility bedding segment.

- Strategic Focus: Indo Count focuses on product innovation and patent-backed differentiation for export markets while building domestic brand infrastructure to diversify revenue and capture India's emerging premium bedding consumer segment.

Market Concentration Analysis

The India home textile market is moderately fragmented at the national level, with organised players estimated to hold 35-45% of total market value while the unorganised sector dominates volume through major power loom clusters. No single company holds more than 8-10% of domestic value market share.

Consolidation in the organised segment is advancing as brand-building investments widen the quality and distribution gap with unorganised players. PLI scheme-driven capacity investments are accelerating vertical integration among leading manufacturers, improving cost competitiveness and enabling premium product expansion across domestic and export channels.

Investment & Growth Opportunities

Fastest-Growing Segments

Online distribution channels at ~7.20% CAGR through 2034 represent the highest-growth opportunity for brand-building investments, digital commerce capabilities, and last-mile logistics infrastructure. Brands investing in platform excellence and digital marketing are positioned to capture disproportionate share of e-commerce growth.

Bed linen at ~5.1% CAGR and bath linen at ~4.9% CAGR through 2034 represent stable, volume-driven growth opportunities. Premiumisation toward organic, sustainable, and functional textiles within these categories is expanding average selling prices and improving margin profiles for organised manufacturers.

Emerging Markets

South India at accelerating CAGR is emerging as the second-fastest growing region, driven by technology economy expansion. West India's real estate market and North India's premium retail growth in the National Capital Region continue to drive organised market expansion ahead of the national average.

Venture & Investment Trends

D2C home textile brands leveraging social commerce are attracting early-stage venture investment, while established PE firms are exploring consolidation opportunities among mid-scale organised manufacturers. PLI scheme benefits and export incentives are catalysing strategic capital expenditure by leading listed companies for capacity and technology expansion.

Future Market Outlook (2026-2034)

The India home textile market is forecast to expand from USD 4.51 Billion in 2025 to USD 6.78 Billion by 2034 at a CAGR of 4.65%, adding USD 2.27 Billion in incremental annual market value over the forecast period. This sustained growth reflects income-driven premiumisation, urbanisation, and organised retail expansion.

Three structural forces will most significantly shape the India home textile market through 2034. India's urban population is projected to reach 600 million by 2031, adding tens of millions of households to the organised home textile addressable market annually, with rising incomes shifting purchasing toward branded, premium, and sustainable home textiles.

The PLI scheme for home textiles targeting USD 2.4 Billion incremental exports by 2028 will drive manufacturing quality upgrades and global brand building, positioning India to increase its share of global home textile trade. Digital commerce penetration will continue to reshape distribution dynamics, with online channels projected to reach 35-40% share by 2034.

Research Methodology

Primary Research

Primary research encompassed structured interviews with India home textile industry stakeholders including brand marketing directors, retail category managers, e-commerce platform heads, procurement specialists at leading hospitality chains, and textile industry association executives. Primary data validated market sizing, distribution channel shares, product segment estimates, and regional demand assessments.

Secondary Research

Key secondary sources include Ministry of Textiles Annual Reports, TEXPROCIL export statistics, FICCI Home Textile Sector Reports, DPIIT investment data, BIS quality control order publications, and annual reports of leading listed home textile companies. Trade publications and government statistical data supplemented proprietary research.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models incorporating GDP growth rates, urbanisation indices, household formation rates, organised retail expansion trajectories, and export growth assumptions. Scenario analysis accommodated macroeconomic variability and policy change impacts.

India Home Textile Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Products Covered | Bed Linen, Bath Linen, Kitchen Linen, Upholstery, Floor Covering |

| Distribution Channels Covered | Supermarkets and Hypermarkets, Specialty Stores, Online, Others |

| Regions Covered | North India, South India, East India, West India |

| Compsnies Covered | Welspun, Trident Limited, Indo Count Industries Ltd., Himatsingka Seide, Bombay Dyeing, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Home Textile Market Report

The India home textile market reached USD 4.51 Billion in 2025, reflecting consistent demand growth driven by urbanisation, rising household incomes, and expanding organised retail infrastructure across metropolitan and Tier-1 cities.

The market is projected to reach USD 6.78 Billion by 2034, growing at a CAGR of 4.65% during 2026-2034, driven by urban household formation, premiumisation trends, e-commerce expansion, and institutional demand from the hospitality and healthcare sectors.

Specialty stores lead with a 37.16% channel share in 2025, valued by consumers for tactile product evaluation and expert fabric guidance. However, online channels at 28.4% are growing fastest at ~7.20% CAGR, projected to potentially surpass specialty stores by the mid-2030s.

Bed linen leads at 41.05% in 2025, driven by universal residential and commercial demand, continuous product innovation incorporating organic and functional fabrics, and growing consumer investment in premium bedding that improves sleep quality and bedroom aesthetics.

North India commands a 30.0% market share in 2025, driven by high-income metropolitan concentration, strong organised retail infrastructure, and proximity to major textile manufacturing clusters that provide cost-competitive supply to the region's large consumer base.

Online channels are the fastest-growing at ~7.20% CAGR through 2034, accelerated by smartphone penetration, platform investments in home textile merchandising, influencer-driven home décor social commerce, and competitive pricing with hassle-free return policies.

Leading companies include Welspun, Trident Limited, Indo Count Industries Ltd., Himatsingka Seide, Bombay Dyeing, and others.

Key applications include residential bedroom and bathroom furnishing, hotel and resort linen procurement, hospital and healthcare institutional supply, kitchen and dining table accessories, and upholstery fabrics for furniture covering both residential and commercial end-use segments.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)