India Hospital Market Size, Share, Trends and Forecast by Ownership, Type, Bed Capacity, Regionality, Type of Services, and Region, 2026-2034

India Hospital Market Size, Share, Trends & Forecast (2026-2034)

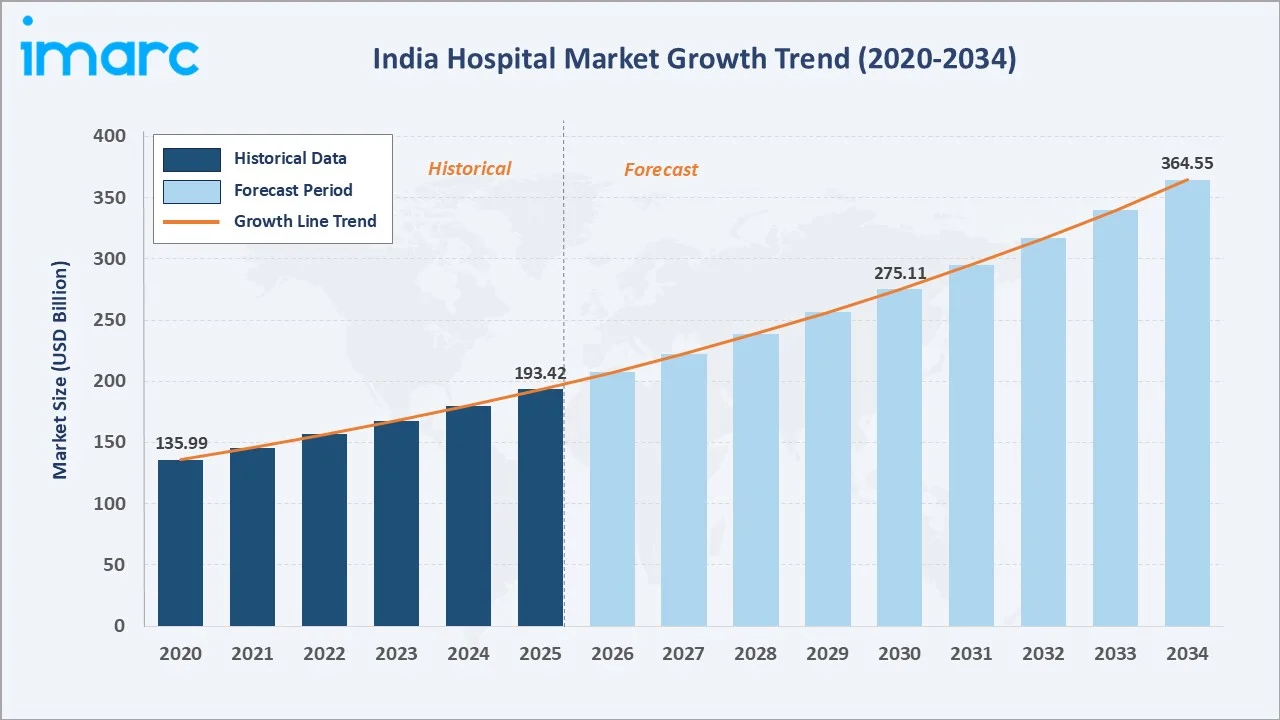

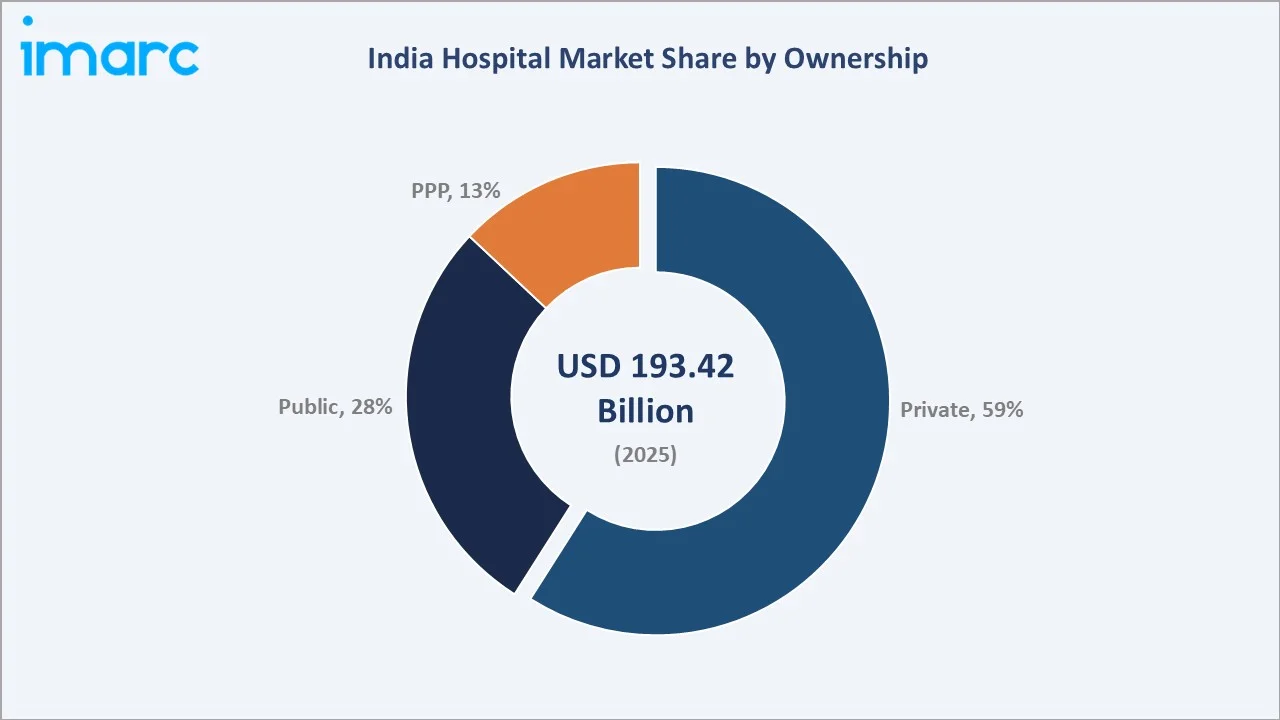

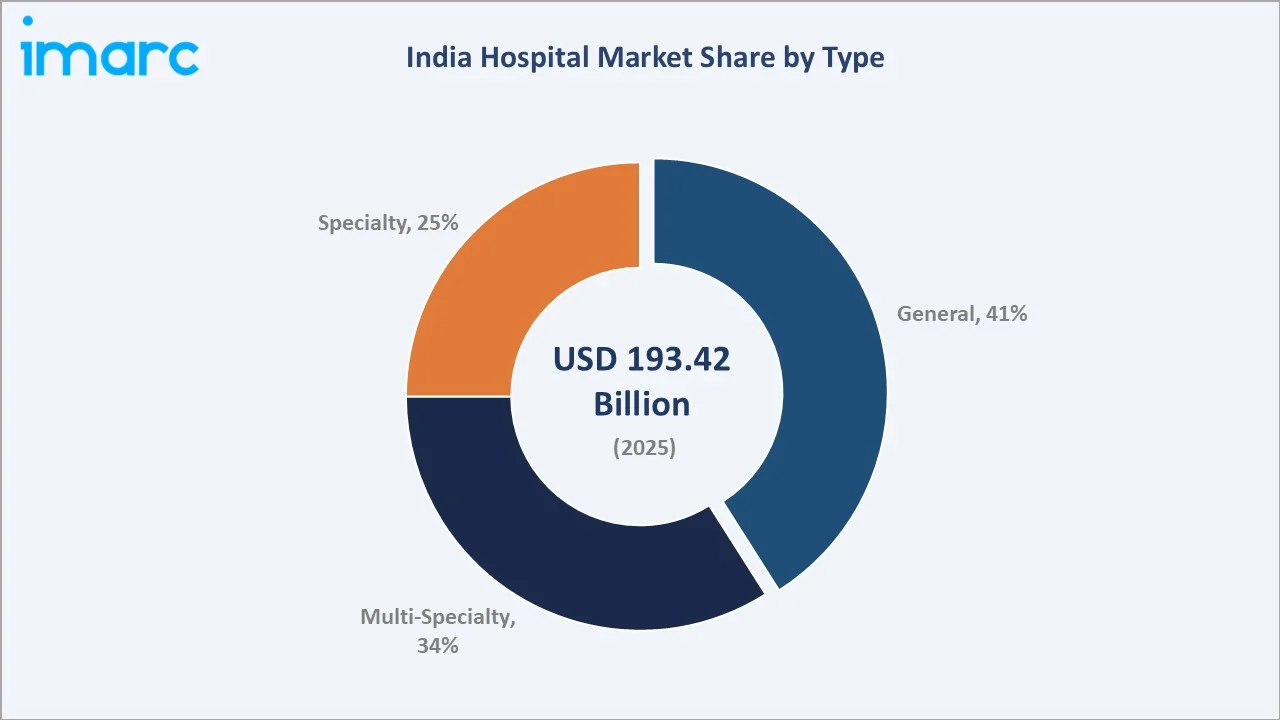

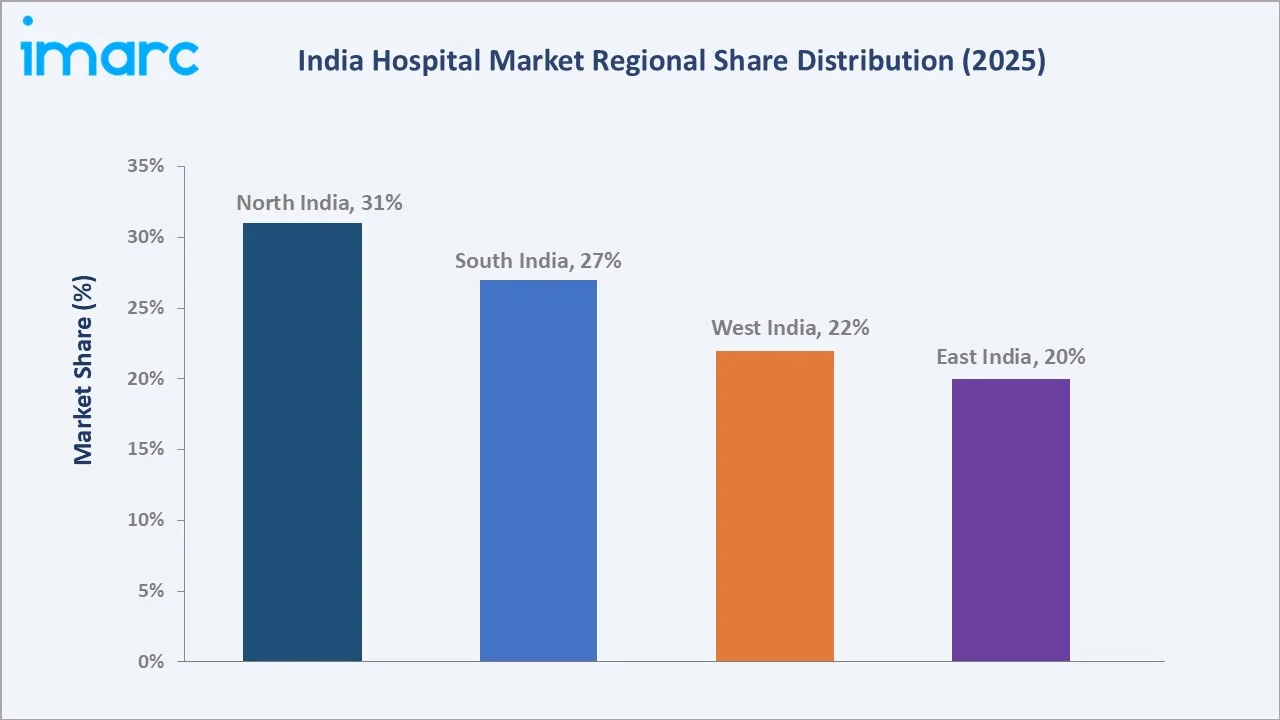

The India hospital market reached USD 193.42 Billion in 2025 and is projected to reach USD 364.55 Billion by 2034, growing at a CAGR of 7.30% during 2026-2034. The Ayushman Bharat Pradhan Mantri Jan Arogya Yojana, implemented by the National Health Authority under the Ministry of Health and Family Welfare, provides cashless hospitalization coverage of up to ₹5 lakh per family annually to poor and vulnerable families for secondary and tertiary healthcare services. The scheme is driving the India hospital market by increasing patient access to organized healthcare services, boosting hospital admissions, and encouraging expansion of private and public healthcare infrastructure across urban and rural regions. Private hospitals dominate at 59%. General hospitals lead at 41% by type. North India commands 31% of the regional market share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 193.42 Billion |

|

Forecast Market Size (2034) |

USD 364.55 Billion |

|

CAGR (2026-2034) |

7.30% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Ownership |

Private (59%, 2025) |

|

Dominant Type |

General (41%, 2025) |

|

Leading Region |

North India (31%, 2025) |

The market expanded from USD 135.99 Billion in 2020 to USD 193.42 Billion in 2025, anchored at USD 275.11 Billion in 2030, and forecast to reach USD 364.55 Billion by 2034. COVID-19 created the most consequential healthcare demand shock in India's history, disrupting elective surgery revenue, accelerating telemedicine adoption from negligible penetration to digital consultations, and permanently expanding government health expenditure commitments through Ayushman Bharat PM-JAY's scale-up as a political priority. Post-COVID healthcare spending recovery from 2022 has been robust, sustained by pent-up demand for elective surgeries, rising insurance penetration, and disease burden.

To get more information on this market, Request Sample

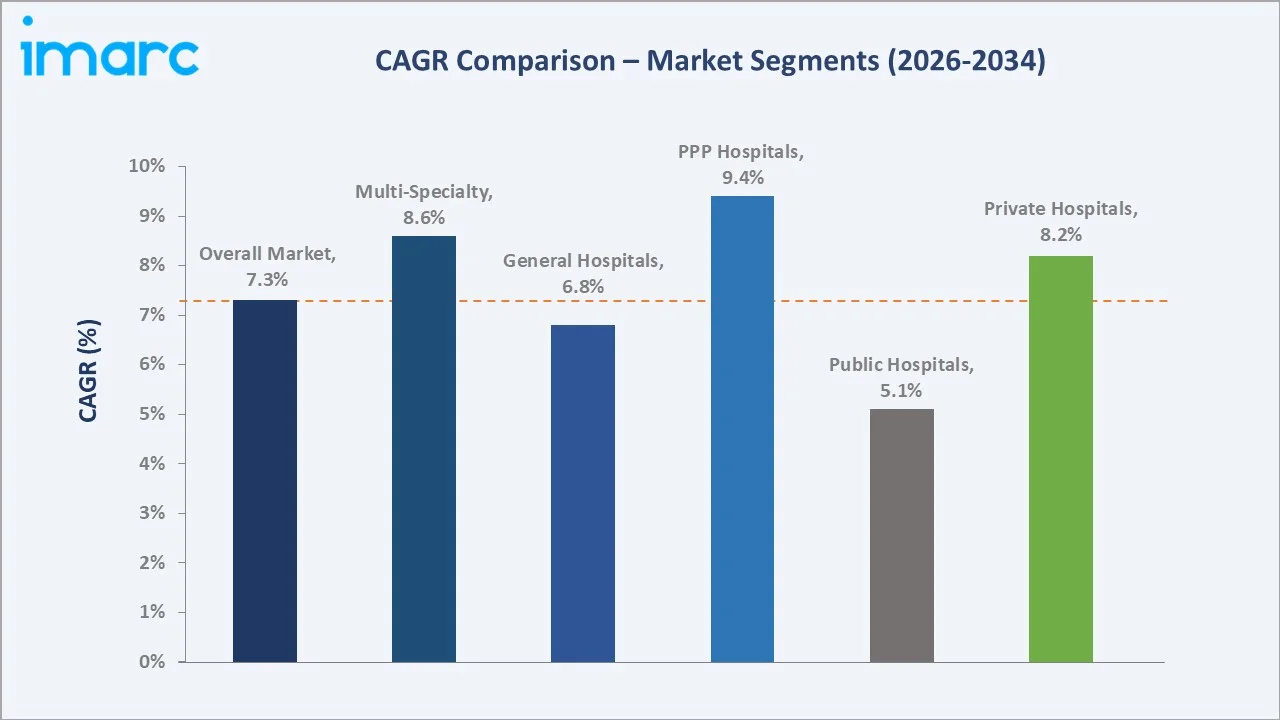

PPP hospitals grow fastest at ~9.4% CAGR, reflecting the government's recognition that India's hospital bed deficit cannot be addressed through public expenditure alone, necessitating public-private partnership models where government land and viability gap funding combine with private hospital operators' management efficiency. Multi-specialty hospitals grow at ~8.6% CAGR as disease burden concentrates healthcare demand in comprehensive tertiary care facilities rather than general medicine.

Executive Summary

The India hospital market reached USD 193.42 Billion in 2025, representing the one of the world's largest national healthcare market by revenue and among the fastest-growing at 7.30% CAGR, a growth rate that reflects India's unique convergence of structural healthcare demand growth drivers: a high population with rising per-capita income, an unprecedented government commitment to universal health coverage through Ayushman Bharat, an disease burden creating structural demand for specialist tertiary care, and a medical tourism competitive position that attracts international patients annually at 10-20% of equivalent Western world costs. India's hospital market is simultaneously a high-growth domestic healthcare economy and a globally competitive medical services export industry. The market is projected to reach USD 364.55 Billion by 2034 at 7.30% CAGR.

Private hospitals at 59% dominate as India's primary healthcare delivery channel for the urban middle class, the private health insurance-covered employed population, and international medical tourists. General hospitals at 41% reflect India's foundational hospital infrastructure serving routine acute care, maternal health, minor surgery, and general medicine across primary and secondary care levels in both public and private sectors. North India at 31% leads through Delhi-NCR's concentration of India's highest-revenue private hospital networks and the region's role as the primary destination for India's medical tourism from South and Central Asia.

Key Market Insights

|

Insight |

Data |

|

Dominant Ownership |

Private - 59% share (2025) |

|

Dominant Type |

General - 41% market share (2025) |

|

Leading Region |

North India - 31% market share (2025) |

Key Analytical Observations Supporting the Above Data:

- Private at 59%, reflecting India's historic underinvestment in public healthcare, creating private sector dominance as the default quality care provider: India's public healthcare expenditure has historically been among the world's lowest as a percentage of GDP, leaving a structural care delivery gap that private hospitals have filled. India's private hospital beds demonstrate that private investment has built 2.5x more hospital capacity than the government.

- General hospitals at 41% reflecting India's primary and secondary care hospital volume base across both public system and private nursing homes: India's General hospital category encompasses the broadest spectrum, from District Government hospitals providing basic acute care to India's rural majority, through urban private nursing homes, to large multi-facility public health systems. General hospital dominance reflects India's healthcare delivery reality: the vast majority of India's population's hospital interactions are for childbirth, routine infections, trauma, and minor surgery that do not require the specialist complexity and technology intensity of multi-specialty hospitals.

- North India at 31%: The region’s large population base, strong concentration of multi-specialty hospitals, and expanding healthcare infrastructure across major cities such as Delhi, Chandigarh, and Lucknow. Rising medical tourism, increasing government healthcare investments, and growing demand for advanced tertiary care services are further strengthening the region’s market leadership.

India Hospital Market Overview

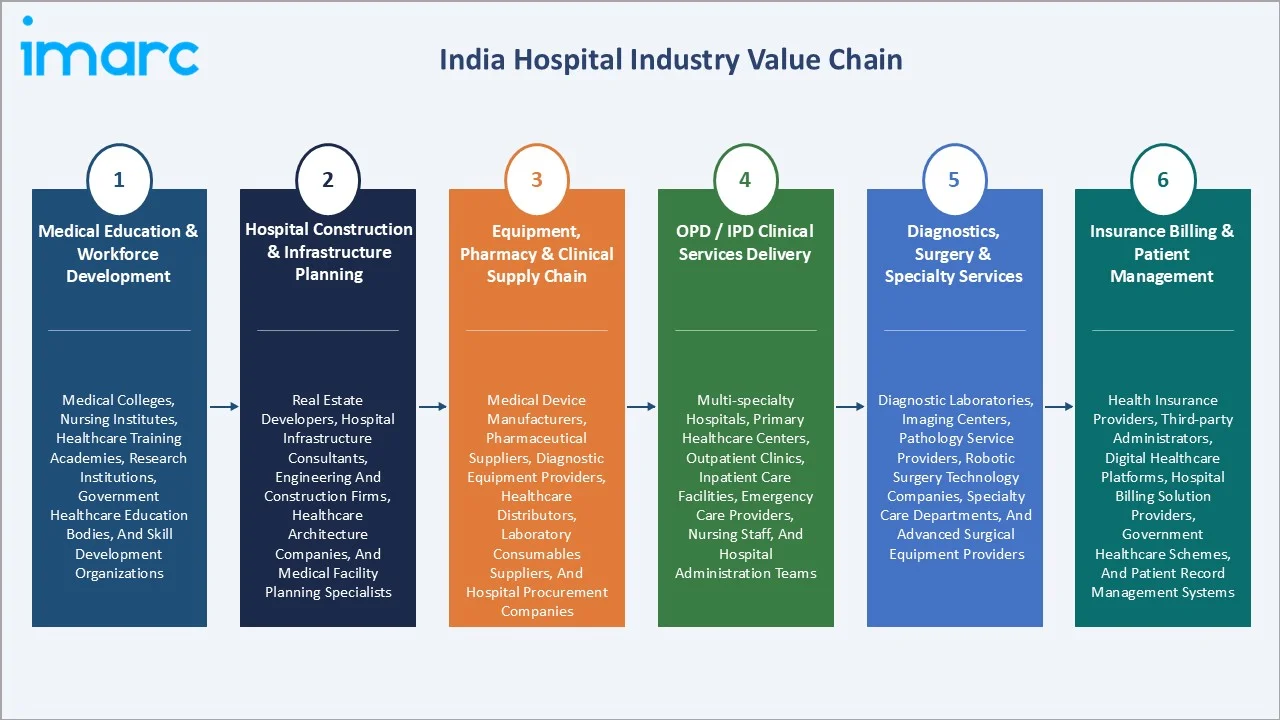

India's hospital market encompasses all forms of organized inpatient and outpatient healthcare service delivery in licensed hospital facilities across public, private, and PPP sectors. The market spans primary health centers providing basic services, community health centers providing secondary care, district hospitals providing general and surgical care, and tertiary care hospitals providing specialist, critical care, and complex surgical services. Hospital revenue includes outpatient consultation fees, inpatient bed charges, surgical procedure fees, diagnostic service revenues, pharmacy revenues, and ancillary service revenues.

The ecosystem integrates medical education and physician workforce development, hospital infrastructure development, clinical supply chain, service delivery, health financing, and hospital management information systems (HMISs), enabling clinical and financial operations. Macroeconomic factors include rising healthcare expenditure, rapid urbanization, increasing health insurance penetration, and growing disposable incomes.

Market Dynamics

To evaluate market opportunities, Request Sample

Market Drivers

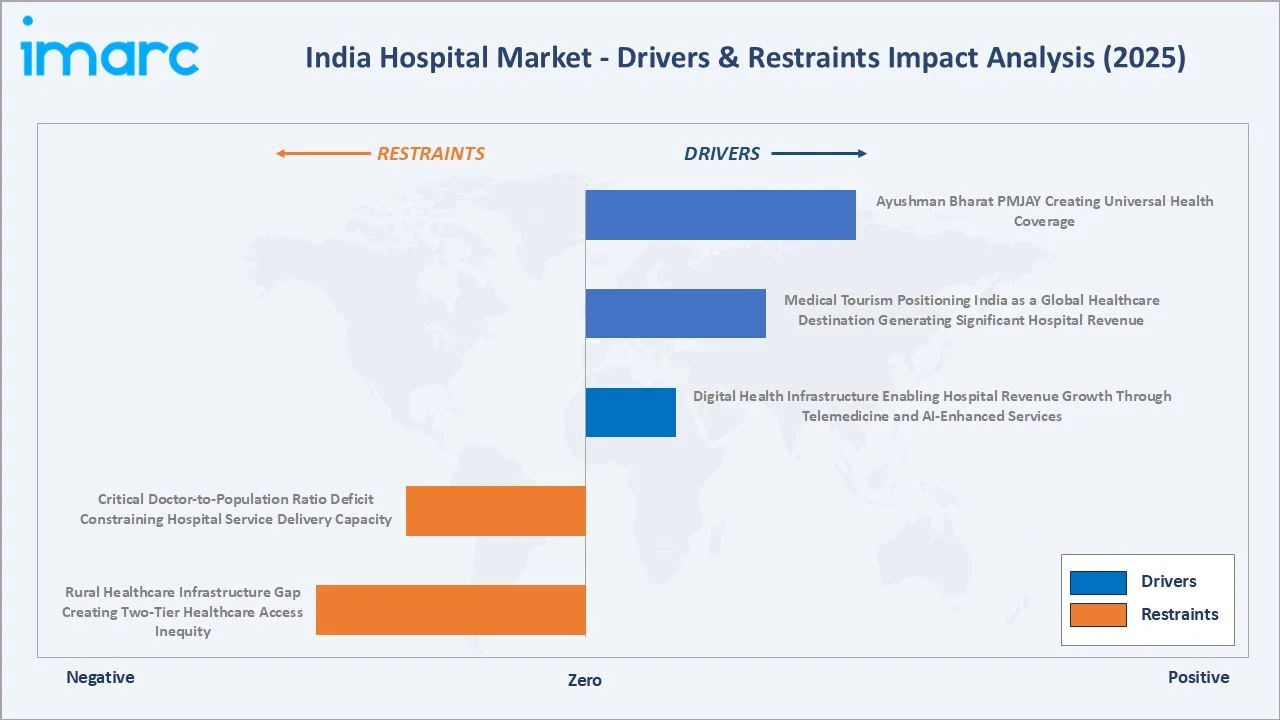

- Ayushman Bharat PMJAY Creating Universal Health Coverage: Ayushman Bharat Pradhan Mantri Jan Arogya Yojana (PMJAY), the world's largest government-funded health insurance scheme, provides INR 5 Lakh per family per year cashless hospitalization coverage to India's bottom population. The scheme is increasing hospital admissions, strengthening demand for organized healthcare services, and encouraging hospitals to expand capacity across urban and rural regions.

- Medical Tourism Positioning India as a Global Healthcare Destination Generating Significant Hospital Revenue: Approximately 2 million patients visit India each year for medical, wellness and IVF treatments. This growing medical tourism is positioning India as a major global healthcare destination by attracting international patients seeking cost-effective and high-quality medical treatments. This is generating significant revenue for hospitals, increasing occupancy rates, and encouraging investments in advanced healthcare infrastructure and specialized treatment facilities.

- Digital Health Infrastructure Enabling Hospital Revenue Growth Through Telemedicine and AI-Enhanced Services: India's digital health ecosystem is creating infrastructure for hospital revenue enhancement through digital channels. Apollo 24x7 provides teleconsultation, e-pharmacy, and diagnostic home collection services that drive patient acquisition for Apollo's physical hospitals. Electronic Health Records (EHR) integration is improving hospital billing efficiency, reducing claim denials for Ayushman Bharat empaneled hospitals, and enabling data-driven clinical protocol optimization that improves average revenue per patient.

Market Restraints

- Critical Doctor-to-Population Ratio Deficit Constraining Hospital Service Delivery Capacity: India's physician density and nurse density create a fundamental healthcare worker supply constraint that limits hospital capacity expansion even when physical infrastructure exists. India produces over 1.8 lakh doctors annually, but specialist formation takes an additional 3 years with limited seat capacity, creating a specialist formation bottleneck.

- Rural Healthcare Infrastructure Gap Creating Two-Tier Healthcare Access Inequity: India's rural population has access to government primary health centers and community health centers that are chronically understaffed, under-equipped, and under-resourced relative to urban private hospital standards. Rural patients requiring tertiary care must travel to district headquarters or state capitals, incurring significant transportation and accommodation costs on top of hospital treatment costs.

Market Opportunities

- Tier-2 and Tier-3 City Hospital Expansion as India's Largest Hospital Revenue Growth Opportunity: India's tier-2 and tier-3 cities collectively host a huge number of urban Indians who have above-average incomes, private health insurance penetration of 15-25%, and historically traveled to tier-1 cities for specialist care. Each tier-2 city hospital of 200-300 beds targeting a catchment of 1-2 million underserved population can reach EBITDA positive within 5-7 years at India's current healthcare demand growth rates, providing investment returns that institutional investors are actively allocating capital to support.

- Health and Wellness Infrastructure Expansion Through Preventive Care Services: India's hospital market is progressively incorporating preventive and wellness services alongside curative care as a revenue diversification strategy. Preventive oncology screening, cardiac risk assessment, and lifestyle disease management programs are each growing at 20-30% annually, representing the fastest-growing hospital-adjacent revenue category.

Market Challenges

- Healthcare Regulation and Price Control Creating Margin Pressure for Private Hospitals: India's government has progressively introduced price controls on essential medicines, surgical implant price caps, and regulatory oversight of hospital billing practices that are often perceived as below market rates by private hospitals. These regulatory price pressures, combined with increasing hospital regulatory compliance requirements, create cost and margin management challenges for private hospital operators seeking to deliver clinical quality at commercially viable economics.

- Medical Talent Retention and Specialist Physician Compensation Inflation: India's private hospital chains face escalating specialist physician compensation pressure as the supply of experienced subspecialist surgeons and physicians is constrained by the postgraduate training bottleneck.

Emerging Market Trends

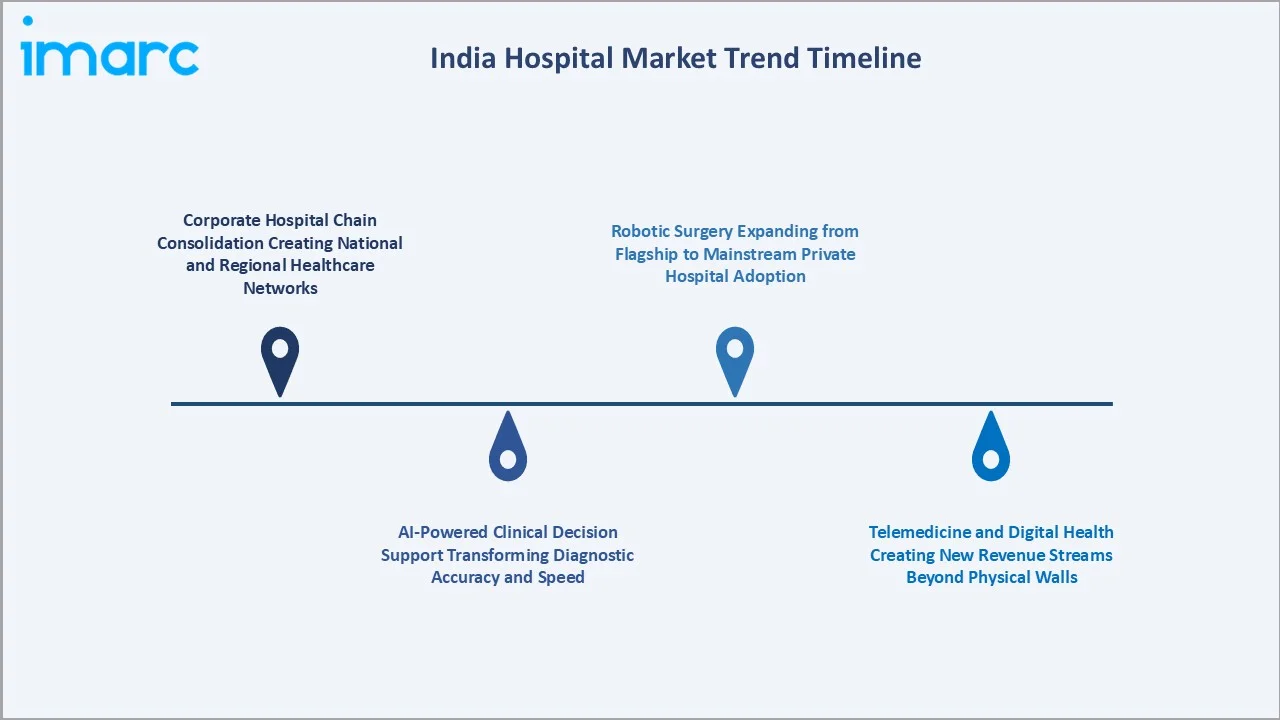

1. Corporate Hospital Chain Consolidation Creating National and Regional Healthcare Networks

Corporate hospital chain consolidation is emerging as leading healthcare providers expand through mergers, acquisitions, and multi-city hospital networks. Large hospital groups are strengthening their regional presence to improve operational efficiency, standardize treatment quality, and expand access to specialized healthcare services. This consolidation trend is also increasing investments in advanced medical technologies, integrated healthcare systems, and tier-II and tier-III city expansion across India.

2. AI-Powered Clinical Decision Support Transforming Diagnostic Accuracy and Speed

AI-powered clinical decision support systems improve diagnostic accuracy, reducing human error, and accelerating treatment decisions. Hospitals are increasingly adopting AI-based imaging analysis, predictive analytics, and patient data management tools to enhance clinical efficiency and optimize healthcare outcomes. The growing integration of artificial intelligence into radiology, pathology, and critical care workflows is also supporting faster diagnosis and improved patient management across healthcare facilities.

3. Robotic Surgery Expanding from Flagship to Mainstream Private Hospital Adoption

Robotic surgery is transitioning from a rare premium offering at tier-1 flagship hospitals toward a competitive differentiator that major urban private hospital chains are deploying across their networks. Apollo Hospitals in Chennai introduced India’s first Robotics and Telesurgery Program through the launch of the Apollo Institute of Robotics & Telesurgery (ART), strengthening its position in advanced technology-driven surgical care. The initiative combines robotic surgical systems with digital connectivity solutions to support remote surgical assistance, medical training, and collaborative procedures, enabling wider access to specialized surgical expertise across multiple locations in India.

4. Telemedicine and Digital Health Creating New Revenue Streams Beyond Physical Walls

Telemedicine and digital health services enable hospitals to extend healthcare delivery beyond physical facilities. Hospitals are increasingly offering virtual consultations, remote patient monitoring, digital diagnostics, and online pharmacy services to improve patient accessibility and operational efficiency. In May 2026, Vedanta Aluminium launched a 24x7 telemedicine facility in Lanjigarh, Odisha, in a partnership with Tata 1mg to improve access to specialist healthcare services. These platforms are creating new revenue streams, expanding patient reach into rural and underserved areas, and strengthening long-term patient engagement for healthcare providers.

Industry Value Chain Analysis

India's hospital value chain integrates medical education and clinical workforce development, hospital construction and infrastructure planning, equipment and pharmaceutical supply chain, outpatient and inpatient clinical service delivery, specialist diagnostics and surgical services, and health insurance billing and patient relationship management.

|

Stage |

Key Participants |

|

Medical Education & Workforce Development |

Medical colleges, nursing institutes, healthcare training academies, research institutions, government healthcare education bodies, and skill development organizations. |

|

Hospital Construction & Infrastructure Planning |

Real estate developers, hospital infrastructure consultants, engineering and construction firms, healthcare architecture companies, and medical facility planning specialists. |

|

Equipment, Pharmacy & Clinical Supply Chain |

Medical device manufacturers, pharmaceutical suppliers, diagnostic equipment providers, healthcare distributors, laboratory consumables suppliers, and hospital procurement companies. |

|

OPD / IPD Clinical Services Delivery |

Multi-specialty hospitals, primary healthcare centers, outpatient clinics, inpatient care facilities, emergency care providers, nursing staff, and hospital administration teams. |

|

Diagnostics, Surgery & Specialty Services |

Diagnostic laboratories, imaging centers, pathology service providers, robotic surgery technology companies, specialty care departments, and advanced surgical equipment providers. |

|

Insurance Billing & Patient Management |

Health insurance providers, third-party administrators, digital healthcare platforms, hospital billing solution providers, government healthcare schemes, and patient record management systems. |

The health insurance billing and patient management tier is India's hospital value chain's fastest-evolving commercial element. The transition from cash-only out-of-pocket payment toward cashless insurance-settled billing is creating billing complexity but also revenue predictability.

Technology Landscape in the India Hospital Industry

Hospital Management Information Systems (HMIS)

In March 2026, the Telangana government opened the Telangana Institute of Medical Sciences and Research (TIMS), Sanathnagar, as a fully digitised hospital with an integrated electronic Hospital Management Information System (e-HMIS). These systems enable efficient appointment scheduling, billing, pharmacy management, laboratory integration, and real-time patient data access, enhancing operational efficiency and patient care quality. Increasing adoption of digital healthcare infrastructure and government focus on healthcare digitization are accelerating HMIS implementation across hospitals in India.

Advanced Medical Imaging Technology

Advanced medical imaging technology enables faster, more accurate, and minimally invasive diagnosis across multiple medical specialties. Hospitals are increasingly adopting high-resolution MRI, CT, PET, ultrasound, and AI-assisted imaging systems to improve diagnostic precision and treatment planning. Rising demand for early disease detection, expanding specialty care services, and increasing investments in modern healthcare infrastructure are driving the adoption of advanced imaging technologies across Indian hospitals.

Electronic Health Records and Clinical Data Analytics

Electronic Health Records (EHR) and clinical data analytics enable centralized patient information management and data-driven clinical decision-making. These technologies improve care coordination, reduce medical errors, and enhance treatment efficiency through real-time access to patient histories, diagnostics, and treatment records. Increasing focus on healthcare digitization, interoperability, and predictive analytics is accelerating EHR adoption across hospitals and multi-specialty healthcare networks in India.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Ownership |

Private |

59% |

2025 |

|

Type |

General |

41% |

2025 |

|

Bed Capacity |

🔒 |

🔒 |

2025 |

|

Regionality |

🔒 |

🔒 |

2025 |

|

Type of Services |

🔒 |

🔒 |

2025 |

|

Region |

North India |

31% |

2025 |

By Ownership

Private hospitals lead at 59% market share (2025). India's private hospital sector encompasses the full spectrum from small 20-bed nursing homes to 2,000+ bed tertiary care hospitals. The organized corporate private hospital chains represent approximately 15-20% of private hospital revenues, while the vast majority of private hospital revenue comes from the fragmented standalone and small-chain private hospital sector.

To access detailed market analysis, Request Sample

Public hospitals at 28% serve India's most vulnerable populations at subsidized or zero cost, with revenue primarily from government budget allocations rather than patient fees. PPP hospitals at 13% grow fastest at ~9.4% CAGR, as the government expands PPP hospital programs to bridge the infrastructure deficit without equivalent public capital expenditure.

By Type

General hospitals lead at 41% market share (2025). India's general hospital segment encompasses all hospitals providing primary and secondary care across medicine, surgery, obstetrics, and pediatrics without deep specialty concentration. Government district hospitals, community health centers, urban primary health centers, and private nursing homes all fall within the general hospital category.

Multi-Specialty hospitals at 34% represent the corporate hospital chains' flagship facilities, offering clinical specialty departments, advanced surgical suites, comprehensive ICU infrastructure, and integrated diagnostics under one roof. Specialty hospitals at 25% encompasses dedicated disease-specific facilities, including cancer hospitals, cardiac hospitals, eye hospitals, and orthopedic hospitals.

Regional Market Insights

|

Region |

Share (2025) |

Key Hospital Market Drivers & Characteristics |

|

North India |

31% |

Driven by dense population, strong concentration of multi-specialty hospitals, and rapidly expanding healthcare infrastructure across major metropolitan cities. |

|

South India |

27% |

Characterized by advanced healthcare infrastructure, high adoption of medical technologies, and a strong presence of leading corporate hospital chains. |

|

West India |

22% |

Driven by rapid urbanization, expanding private healthcare investments, and increasing demand for specialized medical services across industrial and commercial centers. |

|

East India |

20% |

Driven by improving healthcare accessibility, rising public and private healthcare investments, and increasing expansion of organized hospital networks into underserved areas. |

North India's 31% market leadership through Delhi healthcare hub status is sustained by the region's role as India's primary medical tourism destination from South and Central Asia. North India's Ayushman Bharat implementation in UP, Rajasthan, Madhya Pradesh, and Haryana is creating significant private hospital empanelment revenue as tier-2 city private hospitals gain PMJAY patient volumes.

South India's 27% reflects the region's clinical excellence concentration and medical tourism leadership. West India's 22% is driven by Maharashtra's Mumbai premium hospital market and Gujarat's rapidly growing private hospital investment. East India's 20% reflects the region's large healthcare deficit being progressively addressed by private hospital chain expansion.

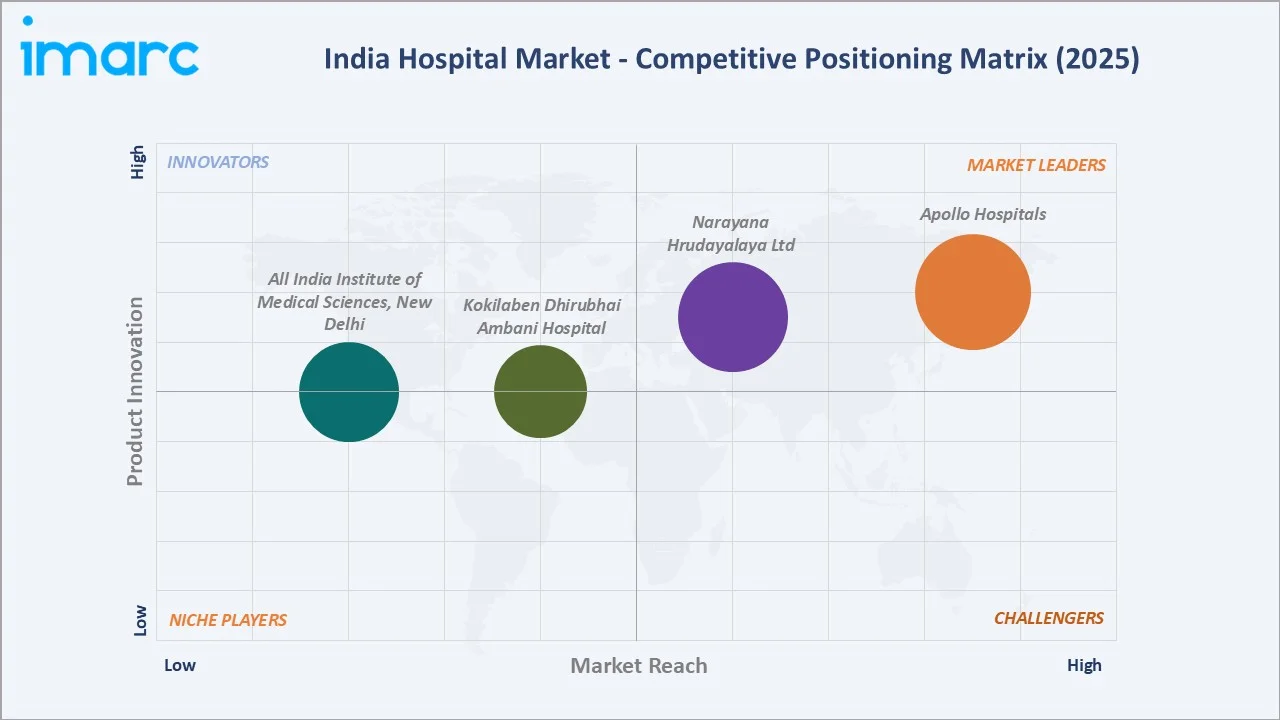

Competitive Landscape

India's hospital competitive landscape exhibits high fragmentation at the total market level, with increasing concentration at the organized corporate chain level. The top-listed and prominent private hospital chains collectively generate approximately USD 12-15 Billion in annual revenues, representing 6-8% of the total private hospital market, with the remaining 92-94% distributed across tens of thousands of standalone and small-chain private hospitals, government facilities, and mission hospitals.

|

Hospital Name |

Key Networks |

Market Position |

Core Strength |

|

Apollo Hospitals |

Andhra Pradesh, Gujarat, Karnataka, Madhya Pradesh, Tamil Nadu, Odisha, Delhi & NCR, Telangana, Kerala, West Bengal, Lucknow, Maharashtra |

Market Leader |

Apollo Hospitals delivers world-class healthcare by combining advanced medical technology with the expertise of highly experienced specialists across key clinical disciplines. |

|

Narayana Hrudayalaya Ltd |

Bangalore, Guwahati, Mumbai, Raipur, Dharwad, Kolkata, Ahmedabad, Jaipur, Barasat, Gurugram, Howrah, Delhi, Mysore, Hosur |

Market Leader |

From quality standards to research and training, Narayana strengthens care through measurable systems & continuous learning |

|

Kokilaben Dhirubhai Ambani Hospital |

Mumbai, Navi Mumbai, Indore |

Established Player |

Kokilaben Dhirubhai Ambani Hospital & Medical Research Institute is one of India’s most advanced tertiary care facilities. |

|

All India Institute of Medical Sciences, New Delhi |

Delhi, Bhubaneswar, Jodhpur, Patna, Raipur, Rishikesh, Bhopal, and others |

Established Player |

India's most prestigious medical institution with national referral center status |

The PPP hospital model's institutionalization represents the competitive landscape's most important structural change, as government PPP programs scale, they create concession-based revenue opportunities for hospital chains that can efficiently operate government-owned infrastructure.

Key Company Profiles

Apollo Hospitals

Apollo Hospitals is India's largest integrated healthcare organization and now represents the country's most comprehensive and globally recognized healthcare brand.

- Key Networks: Andhra Pradesh, Gujarat, Karnataka, Madhya Pradesh, Tamil Nadu, Odisha, Delhi & NCR, Telangana, Kerala, West Bengal, Lucknow, Maharashtra.

- Recent Developments: In April 2026, Apollo Hospitals strengthened its nationwide healthcare presence by opening its 76th facility, a 400-bed smart hospital located in Hyderabad’s Financial District. The hospital developed as a digitally connected healthcare ecosystem integrating advanced clinical services, intelligent operational systems, and patient-focused infrastructure to improve end-to-end care delivery across India.

- Strategic Focus: Focused on expanding its digitally integrated multi-specialty healthcare network across India through smart hospitals, advanced clinical technologies, telemedicine services, and patient-centric tertiary care infrastructure.

Narayana Hrudayalaya Ltd

Narayana Hrudayalaya Ltd has built India's most distinctive hospital model combining world-class clinical quality with radical cost efficiency, making sophisticated cardiac surgery and oncology care accessible to India's lower-income majority.

- Key Networks: Bangalore, Guwahati, Mumbai, Raipur, Dharwad, Kolkata, Ahmedabad, Jaipur, Barasat, Gurugram, Howrah, Delhi, Mysore, Hosur.

- Recent Developments: In August 2025,

- Strategic Focus: Focused on expanding affordable tertiary and quaternary healthcare services across India through high-volume hospital networks, digital healthcare integration, and cost-efficient specialized cardiac and multi-specialty care delivery.

Market Concentration Analysis

India's hospital market is highly fragmented at the total market level, with licensed hospitals including community health centers, government hospitals, and private hospitals ranging from 5-bed nursing homes to 2,000-bed tertiary care facilities. Market concentration increases significantly at the premium private hospital segment level. Hospital market concentration is increasing through three mechanisms: corporate chain acquisitions of standalone hospitals that convert standalone facilities into branded chain units; PMJAY's empanelment quality requirements effectively excluding low-quality standalone nursing homes from the insured patient market; and real estate and capital cost economics that prevent new standalone hospital entrants from competing on both quality and price against established chains with scale purchasing advantages.

Investment & Growth Opportunities

Highest Growth Hospital Segments

PPP hospitals (~9.4% CAGR), multi-specialty hospitals (~8.6% CAGR), private hospitals overall (~8.2% CAGR), specialty cancer hospitals (~12-15% CAGR from rising cancer burden), and digital health and telemedicine revenue streams (~25-30% CAGR from small base) represent India's highest-growth hospital investment vectors.

Emerging Investment Opportunities

India's home care and hospital-at-home services market represents the fastest-emerging hospital revenue extension opportunity. The COVID-19 era's demonstration of home oxygen therapy, IV infusion at home, and teleconsultation-supervised home care normalized high-acuity home healthcare delivery that previously seemed implausible in India's infrastructure context. Hospital chains investing in certified home healthcare service wings can extend their revenue generation beyond the hospital's physical walls while capturing the growing premium home care market.

Investment Themes

- Tier-2 and tier-3 city hospital network expansion as the primary capital deployment opportunity: Private equity capital has demonstrated 3-5x return potential from hospital chain investments in India's growing market, with listed hospital chains providing liquid exit pathways. Build-operate-transfer models require INR 30-80 Crore per 100-bed hospital unit in tier-2 cities, representing capital-efficient deployment given the addressable market at each tier-2 catchment area.

- Cancer care network expansion to address India's new cancer cases: India's cancer care infrastructure is severely under-resourced, with only 450-500 dedicated oncology facilities for new cancer cases, creating access deficits that result in late-stage diagnosis and poor survival outcomes. Each dedicated cancer center of 50-100 beds serving a catchment of 2-3 million population can generate EBITDA of INR 20-40 Crore annually once mature, representing attractive healthcare infrastructure investment returns.

Future Market Outlook (2026-2034)

The India hospital market is projected to grow from USD 193.42 Billion in 2025 to USD 364.55 Billion by 2034, delivering a 7.30% CAGR over the forecast period. The market's anchor value of USD 275.11 Billion in 2030 represents an Indian hospital industry where Ayushman Bharat PMJAY coverage has been extended to beneficiaries under successive government expansions, corporate hospital chains have collectively commissioned new hospital beds across tier-2 and tier-3 Indian cities, and India's medical tourism industry is making it Asia's largest medical tourism destination.

Three structural forces define India's hospital market growth through 2034 with high confidence: India's NCD epidemic intensification; India's per-capita income growth multiplying the population tier willing and able to pay for quality private hospital care; and the irreversible digitization of India's health system under ABDM creating data infrastructure, insurance claim processing efficiency, and patient engagement platforms that structurally improve hospital revenue per episode and patient acquisition costs for digitally-capable hospital operators.

Research Methodology

Primary Research

Primary research comprised structured interviews with 55+ industry stakeholders (2025), including CEOs and CFOs; hospital group strategy directors and business development executives; National Health Authority (NHA) PMJAY empanelment and claims processing officers; NABH (National Accreditation Board for Hospitals) assessors and quality program managers; private health insurance chief medical officers; medical technology company representatives; and investment professionals from private equity firms active in Indian healthcare.

Secondary Research

Secondary research encompassed National Health Authority (NHA) PMJAY annual report 2024-25; National Health Accounts India; Ministry of Health and Family Welfare Annual Report 2024-25; individual company annual reports and investor day presentations; accreditation status database; National Sample Survey Office (NSSO) Health Survey data; WHO Global Health Observatory India data; Healthcare Committee publications; and Indian Journal of Medical Research epidemiology publications. Over 70 secondary sources were reviewed.

Forecasting Models

Market revenue forecasts were developed using top-down and bottom-up models calibrated against hospital revenue data, individual hospital chain revenue, India's health expenditure as a percentage of GDP, health insurance penetration growth projections, and population health demand models. Key inputs include GDP growth, per-capita health expenditure growth elasticity relative to income growth, health insurance penetration expansion trajectory, and PMJAY program scale-up timeline based on government budget allocation data.

India Hospital Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Ownerships Covered | Public, Private, Public-Private Partnerships (PPP) |

| Types Covered | General, Multi-Specialty Hospitals, Specialty |

| Bed Capacities Covered | Up to 100 Beds, 101-300 Beds, 301-700 Beds, Above 700 Beds |

| Regionalities Covered | Regional/District, Rural, Others |

| Type of Services Covered | In-Patient Services, Out-Patient Services |

| Regions Covered | North India, South India, East India, West India |

| Companies Covered | Apollo Hospitals, Narayana Hrudayalaya Ltd, Kokilaben Dhirubhai Ambani Hospital, All India Institute of Medical Sciences, New Delhi, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Hospital Market Research Report and Industry Forecast Report

The India hospital market reached USD 193.42 Billion in 2025, driven by Ayushman Bharat PMJAY's authorized hospitalizations, rising NCD burden, medical tourism industry growth, growing private health insurance penetration, and corporate hospital chain expansion, generating above-market GDP growth in healthcare services.

The market grows at 7.30% CAGR during 2026-2034, reaching USD 364.55 Billion by 2034, driven by PMJAY coverage expansion, NCD epidemic intensification driving specialist hospital demand, India's per-capita income growth expanding the private hospital addressable market.

Private hospitals lead at 59% through decades of investment, filling India's public healthcare infrastructure gap, NCD specialist care concentration in private multi-specialty hospitals, and PMJAY's commercial benefit to private hospital empaneled networks.

General hospitals lead at 41% through India's foundational primary and secondary care hospital volume.

North India leads at 31% through Delhi-NCR's concentration of India's highest-revenue private hospital networks, primary medical tourism destination, and the UP-Rajasthan-Haryana PMJAY beneficiary base generating the country's largest government health insurance claim volumes.

Leading companies include Apollo Hospitals, Narayana Hrudayalaya Ltd, Kokilaben Dhirubhai Ambani Hospital, and All India Institute of Medical Sciences, New Delhi, among others.

The market is projected to reach approximately USD 275.11 Billion by 2030, with PMJAY cumulative hospitalizations authorized, corporate hospital chains adding new beds in tier-2 cities, medical tourism growth, AI diagnostics standard across organized private hospitals, and India's 70+ age group PMJAY coverage creating new senior citizen health insurance beneficiaries, generating geriatric care hospital demand.

Ayushman Bharat PMJAY (Pradhan Mantri Jan Arogya Yojana) is the world's largest government-funded health insurance scheme, providing INR 5 Lakh per family per year cashless hospitalization coverage to beneficiaries through empaneled hospitals.

India's medical tourism industry growth, with international patients choosing India for cardiac surgery, orthopedic procedures, cancer treatment, and transplant services at 10-20% of equivalent Western world costs.

Three priority opportunities: tier-2 city hospital network development; cancer care network expansion to address India's new cancer cases through dedicated oncology hospitals; and health technology investment in AI diagnostics, digital health platforms, and teleICU systems enabling hospital revenue enhancement through diagnostic throughput, patient acquisition efficiency, and premium pricing justification through clinical excellence demonstration.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)