India Hospitality Market Size, Share, Trends and Forecast by Type, Segment, and Region, 2026-2034

India Hospitality Market Summary:

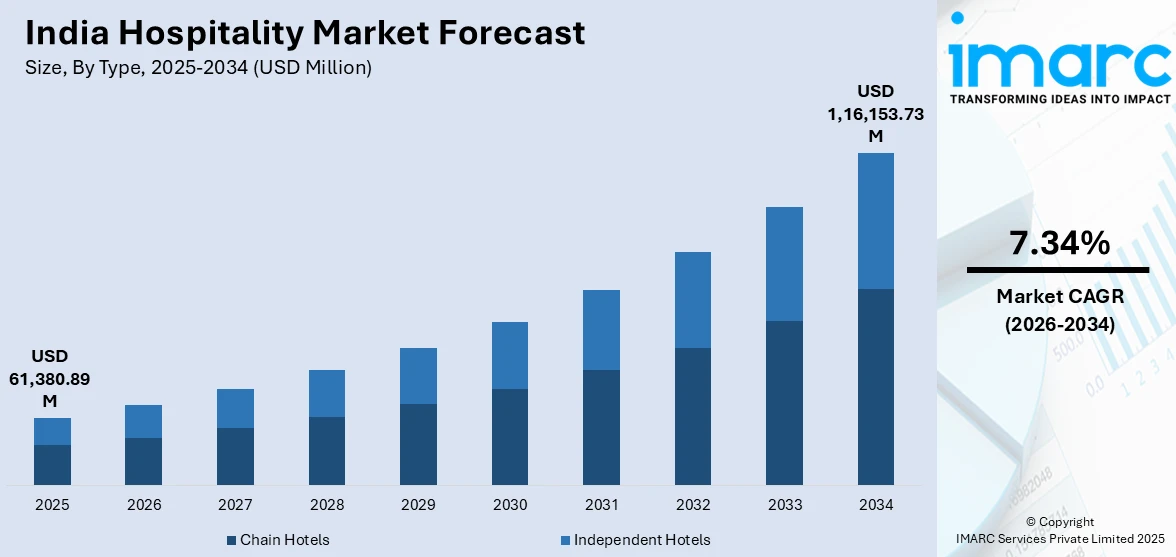

The India hospitality market size was valued at USD 61,380.89 Million in 2025 and is projected to reach USD 1,16,153.73 Million by 2034, growing at a compound annual growth rate of 7.34% from 2026-2034.

A growing middle class with increased travel expectations, rising domestic tourism, and rising disposable incomes are all contributing factors to the steady rise of the Indian hospitality business. Sectoral growth is being accelerated by government measures that support the development of tourism infrastructure and destination marketing activities. Consumer access to high-quality lodging is being expanded by the growth of digital booking platforms and the spread of branded hotel chains into tier-two and tier-three cities. Religious and spiritual tourism circuits, wellness retreats, and corporate travel continue to diversify demand streams, contributing to continued rise in the India hospitality market share.

Key Takeaways and Insights:

- By Type: Chain hotels dominate the market with a share of 54.1% in 2025, because they draw both business and leisure passengers with their consistent service offerings, well-established brand recognition, and large reward programs. Rising consumer preference for consistent quality fuels continuous expansion.

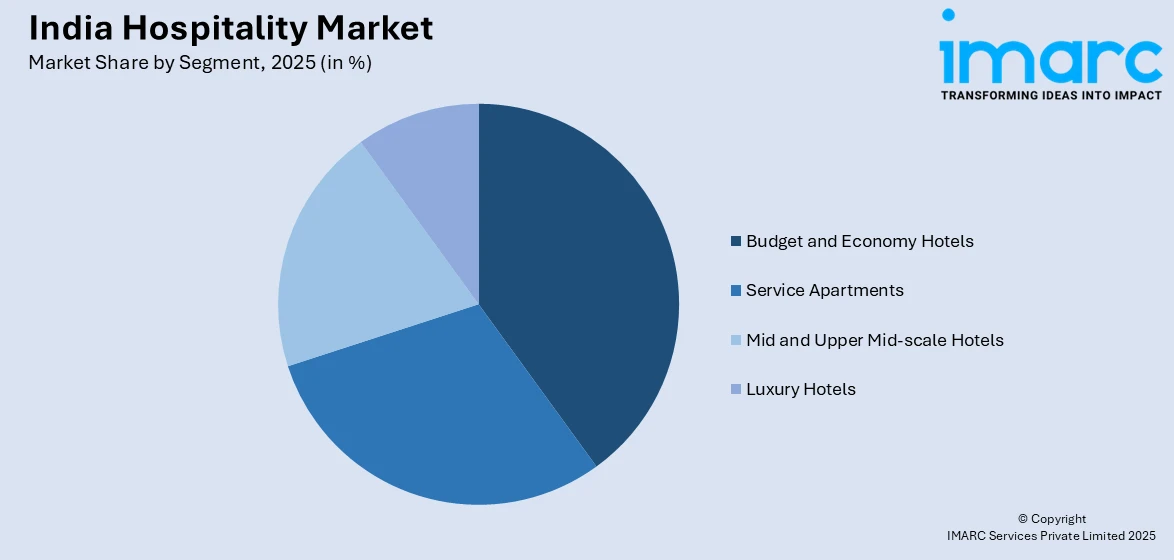

- By Segment: Budget and economy hotels lead the market with a share of 39.7% in 2025, reflecting considerable demand from price-conscious domestic tourists, millennials, and students seeking economical yet clean rooms. Budget solutions are more dependable and accessible thanks to online booking sites.

- By Region: West India is the largest region with 35.2% share in 2025, spurred by Goa's beach tourism appeal, Mumbai's status as the commercial center, and the strong need for business travel throughout the industrial belts of Gujarat and Maharashtra.

- Key Players: Key players drive the India hospitality market by expanding portfolios across multiple segments, investing in digital technologies for enhanced guest experiences, and pursuing asset-light expansion strategies through management contracts and franchising to achieve rapid geographic penetration.

To get more information on this market Request Sample

The India hospitality market is witnessing transformative growth characterized by unprecedented investment activity and strategic brand expansions. In 2024, hotel transactions totaled USD 340 Million, establishing India as the second-largest hotel investment market in the Asia Pacific region, surpassing Japan and reflecting strong investor confidence in the sector's long-term potential. The market is benefiting from favorable government policies. Domestic tourism remains the primary growth engine, supported by improved air connectivity, highway network expansion, and the proliferation of digital booking platforms. The industry is transitioning from volume-driven growth to rate-led expansion, with average daily rates demonstrating consistent year-over-year improvement. Religious and pilgrimage tourism, exemplified by Ayodhya attracting 110 Million visitors in the first half of 2024, is emerging as a significant demand driver alongside traditional business and leisure segments.

India Hospitality Market Trends:

Asset-Light Expansion Models Reshaping Industry Growth

The India hospitality market is experiencing a fundamental transformation in ownership and operational models, with management contracts and franchising agreements becoming increasingly prevalent over traditional owned-hotel arrangements. This strategic shift enables hotel chains to achieve rapid geographic expansion while minimizing capital exposure and balance-sheet risk. In October 2024, Indian Hotels Company Limited accelerated its growth with 35 new signings and 12 hotel openings, taking its total portfolio to 345 hotels with an industry-leading pipeline of 115 hotels, demonstrating the effectiveness of asset-light strategies.

Digital Transformation Enhancing Guest Experience and Operational Efficiency

With hotels investing in AI, mobile apps, and personalized service platforms, technology integration is emerging as a crucial differentiation in the Indian hospitality business. Booking systems, guest relationships, and revenue management skills are all changing as a result of digital innovations. To improve guest interactions and operational efficiency, top hotel operators are implementing AI-powered customer service systems. These platforms use machine learning to provide tailored recommendations and expedite service requests.

Tier-Two and Tier-Three City Expansion Driving Market Penetration

In an effort to meet growing demand, hotel chains are aggressively branching out from established urban centers into smaller cities and unexplored markets. This growth is fueled by expanding trade activity, greater highway connectivity, and growing religious and leisure travel in secondary destinations. As operators look for new development frontiers, branded hotel registrations are becoming more concentrated in tier-two and tier-three cities, highlighting the industry's strategic expansion outside of traditional metropolitan regions.

Market Outlook 2026-2034:

The India hospitality market outlook remains exceptionally positive, supported by sustained economic growth, expanding middle-class demographics, and government commitment to tourism infrastructure development. The market generated a revenue of USD 61,380.89 Million in 2025 and is projected to reach a revenue of USD 1,16,153.73 Million by 2034, growing at a compound annual growth rate of 7.34% from 2026-2034. Major infrastructure projects including the Navi Mumbai airport and Noida International Airport are expected to fuel additional demand, while continued expansion in business hubs such as Bengaluru, Delhi, and Hyderabad will sustain corporate travel volumes. The branded hotel inventory is projected to add over 100,000 rooms by 2029, yet demand growth is anticipated to outpace supply, creating favorable conditions for increased occupancy and robust average daily rates. Religious and spiritual tourism destinations continue attracting significant investment, while wellness tourism and destination weddings emerge as high-growth segments contributing to market diversification.

India Hospitality Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Type |

Chain Hotels |

54.1% |

|

Segment |

Budget and Economy Hotels |

39.7% |

|

Region |

West India |

35.2% |

Type Insights:

- Chain Hotels

- Independent Hotels

Chain hotels dominate with a market share of 54.1% of the total India hospitality market in 2025.

Chain hotels continue to dominate the market thanks to their uniform service offerings, well-known brands, and extensive reward programs that appeal to both domestic and foreign tourists. To maximize operational effectiveness and profitability, these operators take advantage of economies of scale, centralized procurement processes, and advanced revenue management technologies. Strong customer trust that is developed through reliable service delivery, quality control procedures, and easy booking experiences across several properties is advantageous to the segment. In order to accelerate their growth trajectories, chain operators continue to implement aggressive expansion tactics throughout the Indian market, forging strategic partnerships and alliances.

Asset-light business models, which allow for quick regional expansion while preserving uniform service quality across facilities, are highly advantageous to the chain hotel industry. Management contracts and franchise agreements allow operators to reach emerging markets without major capital expenditure, boosting brand visibility in previously untapped destinations. This strategic preference for capital-efficient growth mechanisms boosts return on invested capital for both owners and operators. In addition to strengthening competitive positioning, digital loyalty ecosystems and centralized marketing capabilities draw upwardly mobile Indian tourists who place a higher value on consistency and dependability than just inexpensive prices.

Segment Insights:

Access the comprehensive market breakdown Request Sample

- Service Apartments

- Budget and Economy Hotels

- Mid and Upper Mid-scale Hotels

- Luxury Hotels

Budget and economy hotels lead with a share of 39.7% of the total India hospitality market in 2025.

Millennials, students, and domestic visitors looking for reasonably priced, sanitary lodging with basic amenities are drawn to budget and economy hotels. The availability and dependability of low-cost options have been greatly improved by the growth of online travel agencies and digital booking platforms, which allow customers to compare costs and read reviews before to making bookings. This segment caters to the vast majority of Indian travelers who prioritize value for money while expecting clean, comfortable, and conveniently located properties. Branded economy hotel companies continue proving commercial sustainability and expansion possibilities across secondary cities throughout the country.

The cheap hotel market is witnessing particularly robust development in tier-two, tier-three, and tier-four cities where value-driven tourism is on the rise and quality accommodation alternatives were previously limited. The growth of religious and pilgrimage tourism circuits across the nation, enhanced highway connections, and increased trade activity all boost these sectors. In emerging regions, where demand for standardized, reasonably priced lodging continues to exceed supply, the branded economy hotel sector is a high-potential growth frontier that gives significant opportunity for operators targeting underserved destinations.

Regional Insights:

- North India

- South India

- East India

- West India

West India exhibits a clear dominance with 35.2% share of the total India hospitality market in 2025.

West India maintains market leadership driven by Mumbai's position as the nation's commercial and financial capital, generating substantial corporate travel demand throughout the year. The region benefits from Goa's internationally renowned beach tourism appeal, Maharashtra's diverse industrial corridors, and Gujarat's growing business travel requirements. The hospitality infrastructure continues strengthening through ongoing hotel development activity, with multiple premium properties expected to commence operations, further reinforcing the region's dominant market position within the India hospitality landscape. Major metropolitan centers and coastal destinations attract consistent visitor volumes across business and leisure segments throughout the calendar year.

The West India hospitality market draws balanced demand across all hotel categories, from luxury properties catering to high-net-worth travelers and international business executives to budget accommodations serving domestic tourists and corporate travelers. Mumbai leads nationally in terms of average daily rates and occupancy levels, reflecting strong demand fundamentals and premium positioning. Continued growth is anticipated driven by upcoming airport infrastructure developments and expanding convention center facilities that are expected to attract additional MICE and business travel demand, sustaining the region's market leadership position.

Market Dynamics:

Growth Drivers:

Why is the India Hospitality Market Growing?

Rising Domestic Tourism and Middle-Class Expansion

India's expanding middle class and rising disposable incomes are fundamentally transforming travel patterns across the country, with more Indians prioritizing leisure experiences and domestic tourism. The proliferation of affordable air travel, improved road infrastructure, and digital booking platforms has democratized travel access, enabling broader population segments to explore destinations previously considered inaccessible. Government initiatives promoting tourism infrastructure development, including the development of top tourist destinations and enhanced connectivity programs, are creating new demand centers nationwide. The Indian travel and tourism sector continues making substantial contributions to the country's GDP, securing India's position as one of the largest tourism economies worldwide and among the leading markets in the Asia Pacific region, underscoring the substantial economic foundation supporting continued hospitality market expansion.

Religious and Spiritual Tourism Driving Accommodation Demand

The spiritual tourism market represents a significant and growing demand driver for the India hospitality industry, with pilgrimage destinations experiencing unprecedented visitor volumes and infrastructure investment. Government programs focused on developing tourist circuits at pilgrimage sites are channeling substantial capital into destination development and accommodation infrastructure. The development of branded hotels at religious destinations is accelerating, with operators recognizing the substantial revenue potential of these high-traffic locations. Major pilgrimage cities are witnessing significant hotel development activity following the inauguration of prominent religious monuments and temples, with numerous new hotels expected to open over the coming years to accommodate growing visitor demand at these sacred destinations.

Infrastructure Development and Enhanced Connectivity

Rapid infrastructure development across transportation networks is creating new demand centers and improving accessibility to previously underserved destinations throughout India. The expansion of airport infrastructure, highway networks, and regional air links is connecting smaller towns and tier-two cities with major urban hubs, stimulating tourism and business travel to emerging markets. Government investment in tourism infrastructure, combined with private sector participation in destination development, is laying the foundation for sustained hospitality market growth. The number of operational airports in India has increased substantially in recent years, while major upcoming airport projects are expected to further enhance connectivity and fuel accommodation demand in surrounding regions, supporting the continued expansion of hospitality infrastructure across the country.

Market Restraints:

What Challenges the India Hospitality Market is Facing?

Skilled Labor Shortage and Workforce Challenges

The India hospitality market continues to face a significant shortage of skilled professionals across operational and managerial levels, with demand for trained staff often outpacing supply in rapidly expanding markets. Smaller towns and emerging tourist destinations suffer most acutely, struggling to attract and retain qualified personnel with appropriate soft skills, service etiquette, and customer handling capabilities. The inconsistent quality of hospitality training institutions further compounds this challenge, affecting service quality and guest satisfaction particularly in mid-range and premium properties.

Seasonality and Demand Volatility

The India hospitality market exhibits pronounced seasonality with peak tourist periods tied to specific weather conditions, festivals, and regional events, creating fluctuations in occupancy rates and revenue instability. Hill stations experience demand surges during summer months but remain largely vacant during winters, while coastal destinations peak in winter but face monsoon-driven slowdowns. This uneven demand cycle challenges hotels in maintaining consistent staffing levels, inventory management, and financial stability throughout the year.

Regulatory Complexity and Lack of Infrastructure Status

The absence of infrastructure status for hospitality projects materially constrains expansion, particularly for mid-scale and regionally focused hotel developers seeking favorable financing terms. Hospitality projects are inherently capital-intensive with long gestation periods of seven to ten years, yet they continue to be financed under real estate lending norms with higher interest rates. Multiple licensing requirements, land acquisition challenges, and multi-agency clearances elevate total project costs and extend payback periods, discouraging investment in emerging markets.

Competitive Landscape:

The India hospitality market exhibits moderate fragmentation with opportunities for market consolidation, as leading operators collectively account for a substantial portion of branded room inventory. Major domestic players including Indian Hotels Company Limited, ITC Hotels, and Oberoi Hotels compete alongside international chains such as Marriott, Hilton, Accor, and Hyatt, creating a dynamic competitive environment. Asset-light business models through management contracts and franchising agreements have become the dominant expansion strategy, enabling rapid geographic penetration while minimizing capital intensity. Technology adoption, sustainability initiatives, and loyalty program integration are emerging as critical competitive differentiators, with operators investing in digital platforms to enhance guest experiences and operational efficiency. Strategic partnerships between international brands and local developers are intensifying competition across all market segments.

Recent Developments:

- In April 2025, Accor and InterGlobe announced a landmark partnership to create India's fastest-growing hospitality enterprise, targeting a network of 300 hotels under Accor brands by 2030. The collaboration includes joint investment in Treebo, India's leading budget hotel platform managing 800 hotels across 120 cities, with Treebo signing ten new Mercure properties under a master license agreement.

India Hospitality Market Report Coverage:

|

Report Features |

Details |

|

Base Year of the Analysis |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Units |

USD Million |

|

Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

|

Types Covered |

Chain Hotels, Independent Hotels |

|

Segments Covered |

Service Apartments, Budget and Economy Hotels, Mid and Upper Mid-scale Hotels, Luxury Hotels |

|

Regions Covered |

North India, South India, East India, West India |

|

Customization Scope |

10% Free Customization |

|

Post-Sale Analyst Support |

10-12 Weeks |

|

Delivery Format |

PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the India Hospitality Market Report

The India hospitality market size was valued at USD 61,380.89 Million in 2025.

The India hospitality market is expected to grow at a compound annual growth rate of 7.34% from 2026-2034 to reach USD 1,16,153.73 Million by 2034.

Chain hotels dominated the market with a share of 54.1%, driven by standardized service offerings, established brand recognition, and comprehensive loyalty programs attracting both business and leisure travelers.

Key factors driving the India hospitality market include rising domestic tourism, expanding middle-class demographics, government tourism infrastructure initiatives, religious pilgrimage circuit development, and enhanced air and road connectivity.

Major challenges include skilled labor shortages, seasonal demand volatility, lack of infrastructure status for hospitality projects, complex regulatory requirements, and inconsistent training institution quality affecting service standards.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade